ORIX Corporation: The Ultimate Financial Chameleon & Capital Recycling Machine

I. Introduction & Episode Roadmap

Somewhere in a Dublin office park, a team of lease accountants is marking to market a fleet of Airbus A320neos. At almost the same moment, a control room outside Osaka is watching passenger throughput tick past twenty-three million a year at an airport built on a man-made island in the middle of a bay. In Rotterdam, portfolio managers are rebalancing hundreds of billions of euros of global equities. In Doha, a sovereign wealth fund has just wired its share of a $2.5 billion commitment into a fund that will buy up ageing Japanese family businesses whose founders have no heir. And in Tokyo, a sixty-two-year-old financial company most investors still file under "leasing" is watching its own stock print record after record through the first half of 2026 — the New York-listed ADR peaking at $39.92 in late May, capping a roughly fifty-percent run over its fiscal year.12

All of these things are the same company. That is the puzzle of ORIX Corporation (オリックス株式会社 ORIX Corporation).

Here is the enigma worth sitting with. How does a post-war lease shop, founded in 1964 by a consortium of Osaka banks and trading houses to rent textile looms to companies the banks would not lend to, end up owning Dublin aircraft lessors, running the main airports of the Kansai region, becoming Japan's largest solar generator, operating a leading mid-market private equity franchise, and managing European money through Robeco? The lazy answer is "it's a conglomerate." The more interesting answer is that ORIX is something Japan has almost never produced: a home-grown hybrid of Berkshire Hathaway and Blackstone that runs primarily on its own balance sheet, and that has spent the last decade teaching itself to stop hoarding assets and start recycling them.

That word — recycling — is the crux of this whole story. For most of its life ORIX was an asset accumulator: it bought things that threw off yield, parked them on the balance sheet, and collected the spread. The modern ORIX is trying to become an asset rotator: buy a business, fix it, grow it, and sell it at the top to somebody who will pay a premium, then redeploy the cash into the next thing before the market has finished applauding. The cleanest proof of that shift landed in April 2026, when ORIX agreed to sell 100% of its own bank — a prestigious, decades-old deposit franchise — to Daiwa for roughly ¥370 billion in cash.[^3] A company that will sell its own bank is a company that has genuinely stopped being sentimental about its balance sheet.

This episode traces that transformation. We start with the post-war credit famine that created the original counter-positioned business. We watch Orient Leasing become ORIX in 1989 and sprawl into real estate, life insurance, and — improbably — professional baseball. We study two of the most successful cross-border acquisitions in Japanese corporate history, Robeco and Avolon, and ask why they worked when so many Japanese overseas deals have not. We follow the pivot to "capital recycling" under Makoto Inoue, the handover to a new CEO on January 1, 2026, and the "Growth Strategy 2035" that stakes the company's credibility on a single number: a 15% return on equity. Then we size the actual engine room segment by segment, run ORIX through Hamilton Helmer's 7 Powers and Porter's Five Forces, and stress-test the bull and bear cases the way a skeptical activist would. The prize for getting this right is understanding whether ORIX is a genuine alpha allocator — or an elegant black box that has been lucky with its exits.

Let's begin where every good origin story does: with a shortage.

II. The Post-War Lease Revolution & Osaka Roots

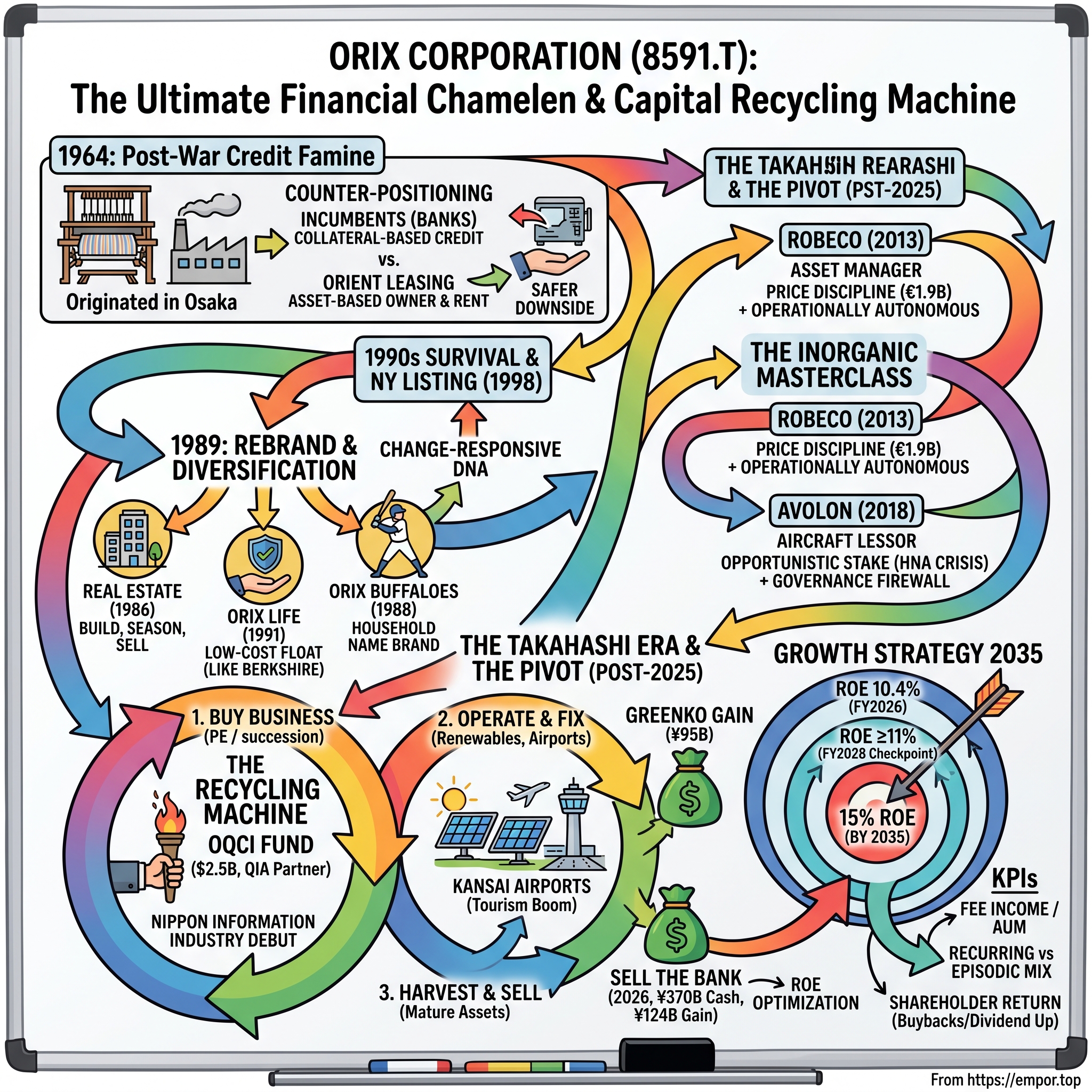

Picture Japan in the early 1960s. The economy is growing at a pace the West finds almost frightening — double-digit real GDP growth, factories going up faster than anyone can finance them, a whole nation trying to buy Western machine tools and textile looms as fast as it can lay hands on foreign exchange. But there is a bottleneck, and the bottleneck is capital. Japan's main banks are wired to serve the giant enterprise groups descended from the pre-war zaibatsu. Credit flows through relationships, and it flows against collateral — overwhelmingly real estate. If you are a small or mid-sized manufacturer with a full order book, skilled workers, and machines that print cash, but no land to pledge, the banking system essentially cannot see you. You are starved in the middle of a boom.

Into that gap, in April 1964, walked a strange little company called Orient Leasing Co., Ltd., set up in Osaka with just ¥100 million of capital and a staff of thirteen.3 It was not a startup in the garage sense; it was a consortium play. The trading house Nichimen (日綿實業, today part of 双日 Sojitz) and Sanwa Bank (三和銀行, today part of 三菱UFJ MUFG) convened the founding, pulling in additional trading companies and banks — names like Nissho and Iwai Sangyo (which would themselves later merge into Sojitz), Toyo Trust, the Industrial Bank of Japan, and others — to seed a new kind of financial animal Japan had barely seen.3 One of those thirteen founding employees was a young man named 宮内 義彦 Yoshihiko Miyauchi, who had recently gone to the United States to learn the mechanics of a business that scarcely existed at home, absorbing the leasing model through a cooperative arrangement with U.S. Leasing International.3

The choice of teacher matters here. Leasing as a formal industry had been pioneered in the United States in the 1950s — U.S. Leasing International in San Francisco was one of its inventors — and it barely existed in Japan when Miyauchi went to study it. He came home carrying a business model that was, in Japanese terms, almost science fiction: a company that would make its living not by lending money but by owning things and renting them out. Transplanting an American financial innovation into the utterly different soil of Japan's relationship-banking system was the founding act of arbitrage, and ORIX has been running variations of that same trade — spot a proven model somewhere the incumbents aren't looking, adapt it, scale it — ever since.

Here is the elegant trick at the heart of the whole thing, and it is worth slowing down on because everything ORIX later became is an echo of it. A traditional bank lends you money and takes your land as security; if you default, it seizes the land. Orient Leasing did something structurally different. It bought the machine itself — the loom, the lathe, the press — kept legal ownership, and rented it to the manufacturer. The credit decision was no longer "how much land can this company pledge?" but "does this machine generate enough operating cash to cover the lease?" If the customer failed, ORIX did not chase collateral through the courts; it simply took back an asset it already owned and re-leased it to somebody else.

That reframing did something profound to the risk equation. The bank's downside on a defaulted loan is a legal fight over land whose value may have collapsed alongside the borrower. ORIX's downside was a used machine tool it could redeploy to the next customer in a booming economy that was desperate for exactly that machine. In a high-growth, capital-starved market, owning the productive asset was safer than holding a lien on real estate, not riskier — the precise opposite of banking orthodoxy. And it let ORIX serve the fast-growing SMEs that were the real engine of the Japanese miracle but which the establishment banks had written off as un-bankable. The company was, from day one, structurally biased toward the customers everyone else ignored.

In Hamilton Helmer's language, this is textbook counter-positioning: a newcomer adopts a business model that incumbents cannot copy without damaging their existing franchise. The banks could not casually pivot to equipment leasing, because doing so would have cut against the collateral-based, relationship-driven credit culture their entire risk apparatus was built on. Leasing to the un-collateralized SME wasn't a product the banks were failing to offer out of laziness; it was a product their DNA actively resisted. That gave Orient Leasing a protected lane to grow in — serving exactly the customers the establishment couldn't. What it reveals, and this is the thread to hold across sixty years, is that ORIX's founding edge was never a product. It was a stance: find the financing need the incumbents structurally can't serve, and serve it.

Miyauchi understood something else, too, and it would become the company's central nervous system. He saw that plain-vanilla leasing was a commodity waiting to happen. The moment leasing proved profitable, the banks would eventually build or buy their own leasing arms, margins would compress, and a one-product lease shop would slowly suffocate. His answer was a management philosophy he'd repeat for decades — a "change-responsive" business that refuses to define itself by any single industry, product, or asset class. When he formally took the top job in 1980, that philosophy stopped being a slogan and started being a strategy: never let what you were constrain what you're allowed to become. It is a deceptively radical idea for a Japanese company of that era, and it is the reason the next chapter isn't about leasing at all — it's about a company deliberately blowing up its own identity.

III. Rebranding to ORIX & The Multi-Armed Financial Chameleon

By the late 1980s the company had a problem that most firms would kill for: it had outgrown its own name. "Orient Leasing" told customers, regulators, and investors exactly one thing — we rent equipment — at precisely the moment management wanted to be understood as something far broader. So in 1989, in the middle of Japan's roaring asset bubble, the company rebranded to ORIX Corporation. The "OR" nodded to Orient; the "IX" was chosen to evoke an open-ended, unfixed quantity — the "X" of algebra, a variable that could stand for anything. It was, in effect, a corporate mission statement disguised as a logo: we are the company whose business is a variable.

The rebrand was less a cause than a ratification of what was already happening. Through the 1980s ORIX had begun spraying capital across adjacent financial territories, each move a small bet on the same idea — that a change-responsive company should follow the cash flows wherever they were richest, not stay loyal to the asset class it grew up on.

Real estate came first, around 1986. Having spent two decades financing other people's construction equipment, ORIX started using its own balance sheet to develop and own the buildings — office towers, residential blocks, later hotels and inns. The logic was seductive during the bubble years, and dangerous: real estate is where a financial company goes to swing for a home run, and also where it can concuss itself when the cycle turns. ORIX would spend the following decades learning to treat property as something to build, season, and sell rather than hold forever — a lesson that becomes central later in this story.

Life insurance came in 1991, with the launch of オリックス生命保険 ORIX Life. This was a quieter, more durable move than real estate, and arguably a smarter one. Insurance gave ORIX a structurally different kind of asset: long-dated, sticky, and — crucially — a source of low-cost float, the same substance that powers Berkshire. ORIX Life's edge was distribution discipline. Rather than fielding an army of salarymen the way Japan's legacy insurers did, it leaned into simple, transparent medical and term products sold direct and through agencies, undercutting incumbents whose costs were bloated by their own sales forces. It is not glamorous. It is a cash machine, and we'll see it still throwing off over a hundred billion yen of segment profit three decades later.

And then, in 1988, ORIX bought a baseball team — the Hankyu Braves, a storied franchise that would eventually, after a 2004 merger, become the オリックス・バファローズ Orix Buffaloes. It is easy to file this under vanity, and every conglomerate has its trophy. But there's a colder reading. In Japan, owning a beloved professional baseball club is one of the very few ways a business-to-business financial company can buy nationwide household name recognition more or less overnight — the kind of ambient trust that a firm renting lathes to factories would otherwise never accumulate. Whether that brand equity truly lowered ORIX's later cost of retail deposits at オリックス銀行 ORIX Bank, as the bullish version of the story claims, is genuinely hard to prove, and we should treat the tidy causal arrow with some skepticism. What is clearer is the intent: ORIX wanted to be known, not just used. A chameleon that keeps changing colors still needs people to remember its name.

Then the bubble burst, and the diversification stopped being a slogan and became a survival test. When Japan's asset bubble collapsed at the start of the 1990s, land and equity values fell for years, dragging a generation of over-leveraged financial companies into insolvency. This was the moment ORIX's real-estate ambitions could have killed it. Many of its natural peers — the specialty lenders, the jusen housing-loan companies, the property speculators — simply did not survive the decade. ORIX did, and the reason is instructive: because its earnings did not all come from one place, a wound in one arm did not exsanguinate the whole body. The insurance float kept coming in. The leasing book kept amortizing. The diversification Miyauchi had pursued for offensive reasons — chasing the richest cash flows — turned out to be defensive insurance against the single-industry death that took down its rivals. That lesson, that spreading across uncorrelated cash flows is a form of solvency insurance, is stamped into ORIX's DNA and explains a lot about why it still refuses to simplify itself even when investors beg it to.

Surviving the 1990s intact left ORIX standing while competitors were rubble, and it used that relative strength to do something almost no Japanese financial company did in that decade: look outward with confidence. In 1998 it listed its shares on the New York Stock Exchange, a deliberate act of subjecting itself to American disclosure standards and American investor scrutiny at a time when Japanese corporate governance was a global punchline. It was a signal — to itself as much as to the market — that ORIX intended to play a global game and would hold itself to a global standard of transparency. Whether it has fully lived up to that promise is a fair question we'll return to when we discuss the conglomerate discount. But the ambition was set early, and it points directly at the next chapter.

Step back and the shape of the thing is visible. By the turn of the millennium ORIX was no longer a leasing company that had a few side businesses; it was a diversified financial platform that happened to have started in leasing. But every one of these arms — real estate, insurance, even baseball — was still fundamentally domestic. And Japan's domestic market was staring down a demographic and monetary winter with no obvious end: a shrinking, ageing population and, before long, interest rates pinned near zero for two decades. Organic growth at home was going to be a grind. To keep compounding, ORIX would have to do the thing Japanese companies are historically worst at: buy foreign businesses and not break them. That is the subject of the next chapter, and it contains the two deals that most define modern ORIX.

IV. The Inorganic Masterclass: Robeco & Avolon

There is a graveyard of Japanese cross-border acquisitions, and every investor in Tokyo knows where the headstones are. A Japanese giant overpays at the top of a cycle, sends in a battalion of head-office managers who don't speak the language or trust the locals, imposes 稟議 ringi-style consensus decision-making on a business that needs speed, watches the talent walk out the door, and quietly writes the whole thing down five years later. ORIX did two enormous overseas deals in the 2010s and — this is the remarkable part — neither one blew up. Understanding why is the key to understanding what ORIX actually is.

Robeco: buying an asset manager and then leaving it alone

In February 2013, ORIX agreed to buy 90% (plus one share) of the Dutch asset manager Robeco Groep from Rabobank for roughly €1.94 billion — about ¥250.7 billion at the final adjusted price, or around $2.6 billion at the time.4 Rabobank, bruised by the post-crisis environment and a rate-rigging scandal, needed capital and was willing to part with a crown jewel. At the close in July 2013, Robeco brought with it something like $249.5 billion in assets under management.4 ORIX later mopped up the rest to reach full ownership by 2016.

Two things made this deal a masterclass rather than a gamble.

The first was price discipline. Paying roughly €1.9 billion for a manager overseeing close to a quarter of a trillion dollars means ORIX paid on the order of one percent of AUM — a strikingly modest multiple for an established, globally distributed franchise that included respected boutiques like Boston Partners and Harbor Capital under its umbrella. Asset managers are, at bottom, a claim on fee streams; buying one cheaply relative to the assets it manages is how you build in a margin of safety. ORIX did not chase; it bought a forced seller's crown jewel at a disciplined number.

The second, and more important, was restraint after the deal. ORIX did the opposite of the stereotype. Rather than parachuting Tokyo managers into Rotterdam, it left Robeco operationally autonomous — its own brand, its own investment process, its own culture — while positioning the group (rebranded over time under the ORIX Europe / Robeco banner) to plug into ORIX's distribution reach in Asia. This is the "hands-off" model, and it reflects a genuine philosophical insight: an asset manager's entire value is its people and its performance track record, both of which evaporate the instant you smother the culture that produced them. ORIX understood that the worst thing it could do to a €1.9 billion investment was to "help."

Avolon: a fire-sale stake with a firewall

The second deal is stylistically the opposite — opportunistic, fast, and built around a distressed seller — but it rhymes with the first. In August 2018, ORIX, through ORIX Aviation, agreed to acquire a 30% stake in Avolon, then the world's third-largest aircraft lessor, for $2.2 billion.5 The seller was Bohai Capital, a leasing arm of China's 海航集团 HNA Group, which was in the middle of a full-blown liquidity crisis and being forced to dump assets to survive. The deal implied an Avolon enterprise value of $23.7 billion.5 ORIX, in other words, was the well-capitalized buyer showing up at exactly the moment a motivated seller had to raise cash — the single best position to negotiate from in all of finance.

But buying into a highly leveraged aircraft lessor is dangerous precisely because it is leveraged: a lessor's credit rating is its lifeblood, since it borrows enormous sums to buy planes and re-lends them at a spread. Sit next to a distressed Chinese parent and your own rating can get dragged down by association. So ORIX built a governance firewall — board seats, veto rights, and a structure designed to insulate Avolon's investment-grade credit standing from HNA's troubles — protecting the platform's ability to keep borrowing cheaply. What ORIX bought, beyond a stream of leasing income, was access: a seat at one of the industry's largest aircraft order books at a time when new planes from Boeing and Airbus would soon become scarce and precious.

It is worth naming the counterfactual to see how easily both deals could have gone the other way, because the Japanese corporate landscape is littered with the wreckage. Japan Post paid billions for Australia's Toll Holdings and wrote almost all of it off. Daiichi Sankyo bought India's Ranbaxy and watched it curdle into a regulatory nightmare. Toshiba's Westinghouse nuclear acquisition helped push the parent to the brink of collapse. The common thread in the failures is hubris about integration — the belief that the Japanese acquirer knew better than the local management and could impose its systems. ORIX's discipline was, in a sense, an act of humility: it bought things it understood well enough to price but was wise enough not to run. That is a rarer trait than it sounds, and it is the strongest single piece of evidence that ORIX's M&A record reflects genuine skill rather than luck.

Put the two deals side by side and the ORIX method comes into focus. Both were opportunistic purchases from sellers under pressure. Both were bought at disciplined prices. Both left the acquired business its operational freedom while ORIX kept an iron grip on the two things that actually protect capital — the credit rating and the risk framework. This is the pattern the company would later formalize as "centripetal and centrifugal balance," and it is the closest thing ORIX has to a repeatable, defensible skill. Which raises the question the rest of the story answers: if ORIX is this good at buying, could it get equally disciplined about selling? That is the pivot that reinvented the company.

V. The Pivot: From Balance Sheet to "Capital Recycling"

For most of its history, ORIX made money the way a landlord does: own the asset, collect the yield, repeat. It is a comfortable model and a quietly corrosive one, because it has a mathematical ceiling. Every yen of yield sits on top of a growing pile of assets, and the more assets you accumulate, the more equity you need to hold against them, and the lower your return on that equity drifts. A company can look busy and profitable for years while its ROE slowly bleeds out. By the mid-2010s, ORIX's leadership had diagnosed this disease in themselves.

The man who put the company on a different footing was 井上 亮 Makoto Inoue, who ran ORIX from 2014 to 2025. Inoue's core insight was almost embarrassingly simple, which is often the mark of a good one: holding assets to collect yield is capital-intensive and dilutes ROE; you make more money buying businesses, making them better, and selling them. He wanted ORIX to think and behave less like a bank and more like a private equity firm that happened to invest off its own balance sheet — an operator-investor that treated every asset as something with a natural holding period and an eventual exit, not a permanent fixture.

It helps to make the ROE math concrete, because it is the mechanical engine under everything that follows. Imagine ORIX buys a stabilized office building that yields a steady, respectable return year after year. On day one that's a fine investment. But as the building sits on the balance sheet, it ties up equity that could be working harder elsewhere, and its return, however dependable, is fixed — it will never suddenly jump. Now imagine ORIX instead develops that building, leases it up, seasons it for a few years, and sells it to a pension fund hungry for stable income at a price that crystallizes several years of future yield all at once. The capital comes back, the gain is booked, and — crucially — the same equity can now be deployed into the next development. The second path can generate a dramatically higher return on equity over a cycle, because the capital turns over rather than sitting still. Recycling, in other words, is how you make a balance-sheet business behave like an asset-light one. The cost is that your earnings become lumpier, front-loaded into the moments of sale rather than smoothed across years of yield — a trade-off that will haunt the bear case.

This is the "capital recycling" doctrine, and it demands a kind of institutional coldness that most conglomerates never develop. It means that an asset's history — how long you've owned it, how prestigious it is, how attached management feels — is irrelevant to the sell decision. The only question is whether the return on that asset still clears the group's hurdle rate. If it doesn't, it goes, no matter how beloved. That sounds obvious written down. In practice, it is the single hardest discipline in capital allocation, because organizations are sentimental and executives fall in love with what they built — and because selling a cash-generating asset means voluntarily shrinking this year's recurring income in exchange for a gain and a promise to redeploy well.

Two proof points show the doctrine working in opposite directions — one about buying and operating, one about selling.

The Kansai airports concession is the buy-and-operate example. In 2016, ORIX and France's VINCI Airports each took 40% of a consortium (with local Kansai investors holding the remaining 20%) that won a 44-year concession to operate Kansai International Airport, Osaka's Itami airport, and later Kobe — a financial package on the order of €2.1 billion.6 This was ORIX stepping decisively out of "finance" and into operating real infrastructure, betting that hands-on management of a critical regional asset could compound value in a way passive ownership never could. It also planted ORIX squarely in the path of the coming inbound-tourism boom, as we'll see when we open up the segments.

The Greenko divestment is the sell example, and it is the cleaner illustration of the doctrine. ORIX had held a long-term stake in the Indian renewable-energy developer Greenko, nurturing it for years. In its fiscal year ended March 2026, ORIX exited, and the transfer of those shares — together with associated valuation gains — delivered a profit contribution on the order of ¥95 billion, a single-shot gain large enough to swing an entire segment from loss to record profit.7 There was nothing wrong with Greenko. It was, if anything, a success. ORIX sold it anyway, because a mature asset that has already delivered its outsized return is exactly the kind of thing a recycling machine is supposed to harvest.

By the time Inoue prepared to hand over the reins, the philosophy was in place and the proof points were on the board. What was missing was a hard, externally verifiable target — a number the whole strategy could be graded against, so that "capital recycling" couldn't quietly decay back into asset accumulation with better slides. Supplying that number, and staking his tenure on it, would be the job of the man who took over on the first day of 2026.

VI. The Takahashi Era & The "Growth Strategy 2035"

On January 1, 2026, 高橋 英雅 Hidetake Takahashi formally became Group CEO of ORIX, with Inoue moving up to Chairman.8 Takahashi was not a parachute hire or a finance-committee compromise; he was a roughly thirty-year insider who had come up through the parts of ORIX that mattered most to its future — real estate, private equity, and renewable energy — which is to say he had personally lived the shift from balance-sheet landlord to operator-investor. He had also been the principal architect, as Group COO, of the strategy he would now be judged on.9 That continuity is worth flagging on both sides of the ledger: it means the strategy has an author who believes in it and understands its plumbing, and it means there is no fresh outsider incentivized to challenge the house religion.

The strategy is called Growth Strategy 2035, unveiled in May 2025, and its headline is refreshingly unambiguous for a Japanese conglomerate: get return on equity to 15% by the fiscal year ending March 2035, with a near-term checkpoint of 11% or better by the fiscal year ending March 2028, and roughly ¥1 trillion of annual net profit over the decade.9 To appreciate why that is a bold number, you have to understand the disease it is meant to cure: the conglomerate discount. Markets systematically distrust sprawling multi-business holding companies, because investors can't see inside them, can't value the parts, and suspect (often correctly) that capital is being shuffled into mediocre uses. ORIX has traded at a discount to the sum of its parts for years. Takahashi's entire mandate is to prove the discount is unwarranted by making the return on the company's capital high and visible enough that the market has no excuse.

The mechanism is the "asset-light" or "asset-rotation" platform. Instead of funding everything with its own balance sheet — which caps ROE by definition — ORIX aims to bring in third-party capital to invest alongside it. The company keeps a slice of the economics plus a fee for managing outside money, which is a far more capital-efficient way to earn a return: you're now getting paid on assets you don't fully own. It is, in essence, ORIX trying to bolt a Blackstone-style fee engine onto its Berkshire-style balance sheet. On the fiscal-2026 earnings call, management framed the whole program around "portfolio optimization" with, in their words, "no sacred areas" — deliberately signaling that nothing, however historic, is off the table for sale.10

They meant it, and they proved it within months.

Selling the bank

On April 27, 2026, ORIX signed an agreement to sell 100% of ORIX Bank to Daiwa Next Bank, a subsidiary of 大和証券グループ Daiwa Securities Group, for approximately ¥370 billion in cash, with the deal set to close around October 2026.[^3]11 The transaction is expected to generate a pre-tax gain of roughly ¥124.2 billion in the fiscal year ending March 2027.[^3] For Daiwa the logic is straightforward — it bolts a lending and deposit franchise onto its securities business, with the combined banks' assets running to something like ¥9 trillion, at a moment when rising Japanese rates have made deposits worth fighting over.[^3]

But the interesting question is ORIX's side. Why sell a bank now, when rising rates are supposed to be good for banks? The answer management gave is the tell. On the earnings call, executives were blunt that the bank's deposits weren't especially sticky and its margins were hard to grow in the new rate environment — in other words, it was a low-return, heavily regulated business consuming a large amount of scarce capital for a mediocre return on it.10 Judged purely on the recycling doctrine, that makes it a sell, and the sentimentality of owning your own eponymous bank is exactly the kind of feeling the doctrine is designed to override. Extracting ¥370 billion of cash to redeploy into higher-returning renewable energy, real estate, and global private equity — while funding aggressive buybacks — is the doctrine operating on the largest and most symbolic asset ORIX had.

There is a neutral observer's caveat worth stating plainly. A pre-tax gain of that size flatters a single year's earnings, and one-off gains are not the same thing as a durably higher run-rate of return. Whether selling the bank was genuinely value-accretive depends on whether ORIX actually earns more on the redeployed cash than the bank would have earned holding it — and that verdict won't be readable in the financials for years. What we can say today is that the sale is powerful evidence about management's revealed preferences: this is a team willing to sell a core, historic franchise to raise its return metrics. That is either admirable discipline or a company optimizing for a headline ROE number; the segments will help us judge which.

On the question of management credibility, the record so far cuts mostly in Takahashi's favor, and it's worth grading honestly because a strategy is only as good as the people executing it. ORIX set a concrete, falsifiable ROE glide path and then, in its first year under the new plan, actually moved the number — from the high single digits toward 10.4% — rather than merely reiterating the ambition.210 It guided fiscal 2027 net income up to roughly ¥530 billion and ROE toward 11.7%, numbers that would put the near-term ≥11% checkpoint within reach ahead of schedule.10 And it backed the words with the two hardest, most irreversible actions available — a giant divestment and a large buyback — rather than the soft commitments (a "medium-term plan," a "review") that Japanese managements often substitute for real capital allocation. The skeptic's rejoinder is that it is easy to look disciplined while riding a bull market in Japanese equities and a boom in inbound tourism, and that the true test comes when the cycle turns and the gains dry up. That test has not yet arrived. But the behavior — set a hard target, act irreversibly to hit it, tie your own pay to it — is the behavior of a management that expects to be held to account, and it is a meaningful upgrade over ORIX's historically vaguer posture.

There is also a myth to puncture here, because it is the reason the stock has been cheap. The consensus label — "ORIX, the boring Japanese leasing company" — is not just outdated; it is almost the inverse of the truth. Leasing in the old sense is now a modest slice of a group whose profit engine is private equity, energy, insurance, asset management, and infrastructure operations. The reality is a balance-sheet alternative-asset manager wearing a leasing company's old uniform. The gap between that reality and the market's tired mental model is the conglomerate discount — and closing it is precisely what Takahashi's strategy is engineered to do. Which brings us to the only real test of whether the reality is as good as the pitch: where the money actually comes from.

VII. Segment Deep-Dive: Where the Money Actually Comes From

Numbers first, then meaning. In its fiscal year ended March 2026, ORIX generated total segment profits of roughly ¥732.6 billion, up about 35% year on year, which flowed through to record net income of ¥447.3 billion (up 27%) and an ROE of 10.4% — a meaningful step up from the high-single-digits it had been stuck at, though still a long way from the 15% finish line.210 The dividend rose about 30% to ¥156.1 per share, and the company completed a ¥150 billion buyback over the year.10 That is the scoreboard. Now let's walk the engine room, in the order the outline lays it out, because the composition of that profit tells you far more than the total.

1. PE Investment and Concession — roughly ¥125.6 billion.12 This is the flagship of the new ORIX, and it does two very different things under one roof. The private-equity side is aimed squarely at one of the largest structural opportunities in Japan: the business-succession crisis. Hundreds of thousands of profitable small and mid-sized Japanese companies are run by founders in their seventies with no successor, and someone has to buy, professionalize, and keep them alive. ORIX has spent years building exactly that muscle. The landmark development came in November 2025, when ORIX and the قطر للاستثمار Qatar Investment Authority launched the OQCI Fund, a $2.5 billion vehicle — ORIX committing 60%, QIA 40% — targeting Japanese succession deals, take-privates, and corporate carve-outs.13 This matters beyond its size: it is the first time ORIX has brought international third-party capital into its domestic PE engine, which is the asset-light doctrine made concrete. The fund proved it wasn't a press release by closing its debut deal in May 2026, acquiring 100% of Nippon Information Industry, a roughly 2,400-person IT services firm founded in 1969.14 On the concession side sits Kansai Airports, the VINCI-partnered operator of the region's three airports. It has swung from pandemic devastation — when international traffic essentially vanished and the concession looked like a millstone — to boom, riding the record surge of inbound tourism into Japan that the weak yen unleashed. That is a reminder worth holding onto: ORIX's infrastructure bet was also, inadvertently, a leveraged bet on the yen staying cheap and the foreign traveler coming back, and both bets paid off spectacularly. It is a genuinely operating business — gate fees, retail concessions, parking, duty-free — not a paper trade, and it demonstrates ORIX's willingness to get its hands dirty running physical infrastructure rather than merely financing it. The caveat, as with all things tied to tourism, is that the tailwind is cyclical and currency-dependent; a stronger yen or a travel shock would deflate it as quickly as it inflated.

2. Environment and Energy — roughly ¥115.8 billion.12 This is the most dramatic swing in the whole company, and it's a perfect case study in why lumpy earnings are both ORIX's superpower and its liability. The segment went from a loss of about ¥4.9 billion in fiscal 2025 — dragged down by a ¥25.9 billion write-down on coal-biomass assets — to a ¥115.8 billion profit in fiscal 2026.12 What powered the reversal was not a surge in operating electricity sales; it was harvest, chiefly the ~¥95 billion Greenko gain plus other equity monetizations.712 Strip out the one-offs and the underlying renewable business is real but far smaller than the headline. ORIX is now Japan's largest solar generator and is pushing into battery storage and European wind, so there is a genuine operating business here — but an investor should mentally separate the recurring generation earnings from the episodic recycling gains, because only one of them repeats.

3. Insurance — roughly ¥102.9 billion.12 After the fireworks of the energy segment, insurance is almost boring, and that is precisely its value. ORIX Life is the steady, high-quality cash generator we met back in 1991, still winning by keeping its cost of distribution structurally below the legacy Japanese giants and selling clean, comprehensible medical and term products. In a company whose earnings can lurch on a single asset sale, a hundred-billion-yen annuity of dependable insurance profit is the ballast that keeps the whole ship from rolling over. Analytically, it's the antidote to the bear case's "lumpiness" charge — proof that not all of ORIX is dependent on the M&A window staying open.

4. Corporate Financial Services and Maintenance Leasing — roughly ¥100.7 billion.12 Here is the original DNA, sixty years on, and it is quietly one of the best businesses ORIX owns. The jewel is ORIX Auto, Japan's leader in fleet leasing and vehicle management. Its edge isn't the financing — anyone can finance a car — it's the integration: telematics, maintenance scheduling, and fleet-management software woven so deeply into a corporate customer's operations that ripping it out means re-plumbing how the whole company runs its vehicles. That is workflow-level switching cost, the same mechanic that makes enterprise software so sticky, and it lets ORIX earn a durable margin on what would otherwise be a commoditized leasing product. The lease shop from 1964 grew up into a software-defended franchise.

5. Aircraft and Ships — roughly ¥66.6 billion.12 For readers who've never thought about why aircraft lessors exist, the logic is worth a sentence, because it explains the whole segment. Airlines are cyclical, often thinly capitalized, and hate tying up billions of dollars in metal that sits on their balance sheet for twenty-five years. A lessor buys the plane, owns it, and rents it to the airline — giving the airline flexibility and the lessor a long, contracted, dollar-denominated income stream secured by a mobile asset it can repossess and re-lease anywhere in the world. It is, in spirit, the exact same trade Orient Leasing invented with textile looms in 1964, just with a much bigger, more mobile, more globally fungible asset. There is a pleasing symmetry in the fact that ORIX's most modern-looking international business is a direct descendant of its founding one.

This segment rode the post-pandemic aerospace recovery through Dublin-based ORIX Aviation and the 30% Avolon stake. With Boeing and Airbus unable to build new planes fast enough — supply chains snarled, certification backlogs long — existing aircraft and the leases on them became scarce and valuable, pushing lease rates and used-aircraft values up across the industry. It is a genuinely good cyclical tailwind, and ORIX bought into it, via Avolon, at a distressed price years before the shortage. It is also, as we'll stress in the bear case, a leveraged and cyclical business whose fortunes are hostage to global travel demand, fuel prices, and geopolitics; the same operating leverage that magnifies profit in a shortage magnifies pain in a freeze. Aviation is where ORIX makes its biggest, most concentrated bet on the world staying calm.

6. ORIX Europe [Robeco] — roughly ¥63.1 billion, up about 42% year on year.12 The Robeco franchise had a strong year, carried by buoyant global equity markets — which mechanically lift the fee-earning asset base — and by recycling gains, including monetization tied to its Indian asset-management joint venture. The economics of an asset manager are worth appreciating because they are close to magical when they work: fees are charged as a small percentage of assets under management, and because managing an extra billion dollars costs almost nothing incremental, the marginal fee falls almost entirely to profit. That operating leverage is why asset managers mint money in rising markets. It is also, inverted, why they can be brutal in falling ones: the same leverage runs in reverse when markets drop and clients redeem. So this profit line is best read as quality earnings with a market-beta kicker — structurally durable, because Robeco's brand and track record keep clients sticky, but variable in amount because the level rides the tape. The strategic value of Robeco, beyond the fee stream, is that it gave ORIX a genuine, credible foothold in global asset management and a template for the fee-plus-balance-sheet model it is now trying to replicate at home with the QIA fund.

7. ORIX USA — roughly ¥954 million.12 And here is the wound. ORIX USA earned about ¥12.1 billion in fiscal 2025 and collapsed to under ¥1 billion in fiscal 2026 — a plunge of roughly 98% — hammered by goodwill impairments, higher provisions for credit losses, and the brutal state of U.S. commercial real estate.12 This is the most important humility check in the entire ORIX story. The company's edge — sourcing, operating, and turning around mid-market businesses — appears to be culturally specific. It travels beautifully within Japan and works through autonomy-preserving deals like Robeco. But dropped into the hyper-efficient, intensely competitive U.S. market as a direct operator, ORIX has struggled to replicate its home-field underwriting advantage. An investor should weight this heavily: it suggests ORIX's moat is partly a local moat, and that the "global" in its ambitions is doing some heavy lifting.

Notice, too, what the segment map reveals about concentration. There is no single business here on which ORIX's survival depends — a stark contrast to a monoline lender or a pure aircraft lessor. The largest segment is barely a sixth of total profit, and the profit is spread across finance, operations, and investments, across Japan, Europe, and the U.S., across cyclical and defensive assets. That is the diversification that saved the company in the 1990s, still doing its quiet defensive work. The flip side is that this same spread is what makes ORIX hard to value and easy to discount: no analyst can be expert in leasing and aircraft and asset management and solar and airport concessions and U.S. credit, so the market throws up its hands and applies a haircut to the whole thing. Diversification is simultaneously ORIX's insurance policy and the source of its valuation problem — a tension the company cannot fully escape, only manage.

Put it all together and a clear-eyed picture emerges. ORIX's recurring engine — insurance, auto/leasing, asset management fees, aviation lease income — is genuinely diversified and defensible, worth comfortably north of ¥300 billion of segment profit on its own. But the growth and the record in any given year lean heavily on episodic recycling gains: Greenko this year, the bank next year. That duality is the whole investment debate, so let's frame it properly.

VIII. The Seven Powers & Five Forces Stress Test

Strip away the sixty years of narrative and ask the cold analytical question: does ORIX actually have durable competitive advantage, or is it just a well-run allocator enjoying a good cycle? Frameworks help here — not as box-ticking, but as a discipline for separating real moats from flattering stories.

Start with Hamilton Helmer's 7 Powers. ORIX plausibly holds three, in descending order of conviction.

The strongest candidate is Process Power — the hardest of the seven to acquire and the hardest to copy, because it lives in an organization's accumulated routines rather than in any single asset. ORIX's genuine, rare capability is executing continuous cross-border capital recycling — buying, operating, and exiting businesses across wildly different industries and geographies — without the parent company either strangling its subsidiaries or losing control of risk. The "centripetal/centrifugal" balance we saw in Robeco and Avolon (total operating autonomy for the subsidiary; iron control of credit rating and risk at the center) is a learned organizational skill built over decades. It is not something a competitor can buy off the shelf, which is exactly what makes it Process Power rather than mere competence. The honest caveat: the ORIX USA collapse suggests this power has a geographic boundary, and Process Power that stops at the water's edge is worth less than one that travels.

The second is Scale Economies, though narrower than ORIX's size implies. In Japanese fleet leasing and domestic renewable generation, ORIX's sheer scale genuinely lowers unit costs — better procurement terms on vehicles and panels, fixed operating and software costs spread over a bigger base. This is real but local; it does not obviously extend to, say, competing with Blackstone globally.

The third, and softest, is Branding. The Buffaloes and ORIX Life give the group a level of household trust unusual for a B2B financial firm. It is real, but one should not overweight a baseball team; brand is a supporting actor here, not the lead.

Notably absent are Network Economies and Switching Costs at the group level — the ORIX Auto stickiness is real but doesn't extend across the conglomerate — which is a useful reminder that ORIX's moat is a portfolio of narrow, mostly domestic advantages rather than one wide structural one.

Equally important is a power ORIX used to have and has largely lost: the counter-positioning that founded the company. Six decades on, the megabanks long ago built their own leasing arms, and equipment finance is a commodity fought over on basis points of spread. The original moat has silted up entirely — which is not a failure so much as the whole point of Miyauchi's "change-responsive" doctrine. ORIX has spent its life watching its edges commoditize and deliberately migrating to the next un-contested niche before the old one closed. The strategic question for the next decade is whether the newest edges — operating skill in Japanese PE and infrastructure, the QIA-style fee model — prove more durable than leasing did, or whether they too will be competed away as global capital floods into the same Japanese succession and take-private opportunities ORIX has spotted. The arrival of Blackstone, KKR, and Carlyle as serious bidders for Japanese assets is exactly the kind of margin-compressing catch-up ORIX has faced before. The company's whole history says it will simply move again. But "we'll find the next thing" is a bet on management, not a structural guarantee, and an honest analyst should price it as such.

Now Porter's Five Forces, which grade the industry ORIX competes in rather than the firm.

Threat of new entrants: low. You cannot easily conjure a diversified global platform spanning leasing, insurance, PE, aviation, and asset management. The regulatory capital, the licenses, the accumulated risk apparatus, and the balance sheet required constitute a genuine barrier. Nobody is going to build a new ORIX from scratch.

Bargaining power of customers: low to medium. In the sticky corners — fleet management, corporate leasing — switching costs protect margins. In the commoditized corners — vanilla lending, financing — customers have all the leverage, which is precisely why ORIX has been fleeing toward alternatives and asset-light platforms where it can price on value rather than on spread.

Competitive rivalry: high in core finance, low in the niches. This is the strategic crux. In plain-vanilla domestic finance, ORIX is knife-fighting with megabanks who will always undercut it on lending margin — a fight ORIX cannot win and has wisely chosen to exit. Its whole strategy is a deliberate retreat from the high-rivalry zones (selling the bank!) into specialized, less-contested niches where its operating skill, not its balance-sheet size, sets the price.

Threat of substitutes and supplier power are less binding, but the substitute worth naming is third-party capital itself: as global PE giants raise Japan-focused funds, ORIX's balance-sheet-plus-fee model competes directly with Blackstone, KKR, and Carlyle for the same succession deals. The QIA partnership is partly a response to exactly that pressure.

The synthesis is this: ORIX's advantages are real but they are plural and mostly domestic — a bundle of niche moats held together by a genuine, rare, but geographically bounded Process Power. That is a defensible position. It is not an impregnable one. Which sets up the fight between the bulls and the bears.

IX. Investment Spine: Bull vs. Bear & Risk Radar

Here is the question an activist walks into the room with: is ORIX an alpha allocator — a rare organization that genuinely creates value by buying, fixing, and selling better than the market — or is it a black box, a sprawling conglomerate whose good years are really just a string of well-timed exits dressed up as strategy? Both cases are serious. Let's argue them honestly.

The bull case: why ORIX wins from here

The strongest bull argument is revealed discipline. Talk is cheap and every conglomerate promises to "optimize the portfolio"; ORIX just sold its own bank for ¥370 billion in cash and booked a ¥124.2 billion gain to prove it wasn't bluffing.[^3] That is management doing the hard, unsentimental thing rather than saying it. Paired with the completed ¥150 billion buyback in fiscal 2026 and a fresh authorization to repurchase up to ¥250 billion — as much as roughly 9% of shares outstanding, of which ¥39.6 billion had been executed by the end of June 2026 — you have a capital-return story with teeth.1015 A company aggressively shrinking its own share count while raising its return metrics is doing exactly what the ROE target requires.

The second bull pillar is macro fit. Rising Japanese interest rates are a slow poison for traditional banks stuffed with low-yielding government bonds, but they are broadly constructive for a hands-on operator of real estate and an active turnaround investor — ORIX gets to buy assets from stressed sellers and reprice risk, rather than sit on a bond portfolio bleeding value. Add the structural tailwind of Japan's succession crisis (an almost inexhaustible supply of good companies needing new owners) and the QIA-backed fee engine to attack it with capital-efficiently, and the growth runway is credible.

The third pillar is alignment. A new Performance Share Unit plan beginning in fiscal 2027 ties executive compensation explicitly to consolidated ROE and to total shareholder return relative to peers.9 That directly bolts management's wallet to the two metrics shareholders care about most — a meaningful upgrade over the vaguer incentive structures common in corporate Japan, and a reason to take the 2035 target as more than a slide. It also fits a broader, verifiable pattern of shareholder-friendly behavior: a dividend up roughly 30% in fiscal 2026, a progressive payout policy, and back-to-back buybacks scaling from ¥150 billion to ¥250 billion.1015 For a company that spent decades as a classic empire-building Japanese conglomerate, the recent posture toward returning capital is a genuine cultural shift, and it is the kind of thing that, sustained, can slowly re-rate a stock regardless of what any single year's earnings do.

Worth flagging as a fourth, quieter support: the tailwind of Japan's own corporate-governance reform. Tokyo's stock exchange has been publicly pressuring companies trading below book value to fix their capital efficiency, and the whole market has tilted toward buybacks, unwound cross-shareholdings, and ROE discipline. ORIX is, in effect, swimming with a powerful national current rather than against it — which both helps the strategy and, the skeptic notes, makes it harder to know how much of the recent re-rating is ORIX's own doing versus a rising tide lifting all governance-improving Japanese boats.

The bear case: what breaks the story

The sharpest bear argument is earnings lumpiness, and it is not a quibble — it goes to the heart of what ORIX is. Look again at fiscal 2026: the record was powered materially by the ¥95 billion Greenko gain, and fiscal 2027's headline will lean on the ¥124.2 billion bank gain.7[^3] Strip the big divestment gains out of any given year and the growth rate deflates dramatically. A skeptic reasonably asks: is this a business compounding, or a portfolio liquidating its best assets one prestige exit at a time to hit its numbers? If the M&A market freezes — if buyers disappear and multiples compress — ORIX loses the exits that make its ROE math work, and the recurring engine alone won't carry the 15% target. The quality of ORIX's earnings is genuinely lower than the headline growth rate implies, and honest bulls should concede it.

The second bear pillar is the U.S. black hole. ORIX USA's ~98% profit collapse is not a rounding error; it is evidence that the company's core skill may not export to efficient Western markets, which quietly caps the "global platform" ambition and raises the risk of further impairments in U.S. real estate and credit.12

The third is aviation tail risk. The 30% Avolon stake is riding a beautiful cyclical wave, but aircraft leasing is a leveraged, capital-intensive business acutely exposed to any global travel shock, oil spike, or geopolitical rupture — the kind of asset that produces years of steady profit and then one catastrophic year. The COVID collapse of 2020, which briefly grounded the world's fleet and forced lessors into painful lease restructurings, is only five years in the rear-view mirror; the memory of how fast that business can invert should temper any straight-line extrapolation of today's boom.

Underlying all three is the governance and complexity critique an activist would press hardest: ORIX is a ten-segment box that even sophisticated investors struggle to value from the outside, which is why it trades at a conglomerate discount in the first place. The bull says the discount is a gift that closes as discipline shows through; the bear says the discount is the market's rational price for opacity, lumpiness, and the ever-present risk of "diworsification" — capital wandering into a new adventure just when the last one was starting to pay off. An activist would also press on disclosure: with earnings this dependent on the timing and pricing of discretionary asset sales, management holds enormous latitude over which year a given gain lands in, and therefore over the smoothness of the reported growth story. That is not an accusation of wrongdoing; it is an observation that the numbers require more trust in management than a simple operating business would, and trust is exactly what a conglomerate discount refuses to extend for free.

A brief second-layer aside for the diligent: the entire recycling model rests on a foundation most casual observers never look at — ORIX's own funding cost and credit standing. A balance-sheet investor that borrows to buy assets lives and dies by its access to cheap capital; a credit-rating downgrade would raise ORIX's cost of funds across every segment at once and quietly compress the spreads the whole enterprise runs on. That is why the "centripetal" control of the credit rating from Tokyo is not bureaucratic caution but existential defense. It is also why rising Japanese rates are genuinely double-edged for ORIX: helpful for buying assets from stressed sellers, but a headwind for the cost of the debt that funds the aviation and leasing books. The investor who wants to understand ORIX's risk should watch its funding spreads and rating outlook as closely as its ROE.

The risk radar and the KPIs that actually matter

The material risks are refreshingly specific rather than generic: refinancing / cost-of-capital risk across the leveraged leasing and aviation books as global rates stay higher for longer; execution risk in the asset-light transformation, which requires ORIX to keep raising outside capital on good terms; U.S. commercial-real-estate and credit exposure; and concentration in episodic gains that could disappoint in any year the exit window narrows.

Which distills to the handful of numbers a long-term investor should actually track, ignoring the noise:

- Return on equity versus the glide path — is ORIX genuinely climbing from 10.4% toward the ≥11% fiscal-2028 checkpoint and the 15% fiscal-2035 goal, and how much of each year's ROE is recurring versus one-off gains? This single ratio is the entire thesis.910

- Fee income and third-party assets under management in the asset-light platform — is outside capital (the OQCI fund and its successors) actually scaling? This is the cleanest signal of whether the Blackstone-style pivot is real or rhetorical.

- The recurring vs. episodic profit mix — track base earnings (insurance, leasing, fees, lease income) separately from divestment gains, because the durability of the whole story lives in that split.

Everything else — a good quarter at Kansai, a strong tape for Robeco — is texture around those three.

X. Playbook & Durability Lessons

Zoom out from the segments and the stock and three transferable lessons remain — the things a builder or allocator should actually steal from ORIX's sixty years.

One: your legal and historical identity is a liability, not an asset. ORIX's founding genius was a counter-positioned business model, but its enduring genius was refusing to be imprisoned by it. Had the company stayed loyal to the name "Orient Leasing," it would have been ground into dust by margin compression as the megabanks copied leasing — exactly as Miyauchi predicted in the 1970s. "Change-responsive" management is not a platitude; it is the discipline of continuously asking what you are allowed to become, and treating your own past as sunk cost. The 1989 rebrand to a name meaning "variable" was the philosophy made visible.

Two: get the centripetal/centrifugal balance right, and cross-border acquisitions stop being graveyards. The reason Robeco and Avolon worked while so many Japanese overseas deals failed is that ORIX granted its subsidiaries near-total operational autonomy (centrifugal) while keeping absolute control of capital allocation, credit rating, and risk at headquarters (centripetal). Most acquirers get this exactly backwards — they micromanage operations they don't understand while letting risk and capital discipline drift. The ORIX USA struggles are the exception that proves the rule: where the model gets pushed into direct operating in an alien market, the balance breaks down.

Three: the hardest and most valuable skill in capital allocation is selling things you love. Any competent team can buy assets; a great one knows when a mature, prestigious, emotionally-freighted asset should be harvested to fund a higher return elsewhere. Selling Greenko at a peak, and then selling the company's own eponymous bank for a record price purely to lift group ROE, is emotion-free capital allocation of a kind that is genuinely rare in corporate Japan — or anywhere. The open question, and the reason to keep watching rather than to conclude, is whether ORIX can redeploy that harvested capital as skillfully as it harvests it. Harvesting is proven. Redeployment at 15% ROE is not.

XI. Outro

Return to the image we opened with: one company that is simultaneously a Dublin aircraft lessor, an Osaka airport operator, a European asset manager, a Qatar-backed private equity fund, and — for a few more months — a Japanese bank. For most of corporate history that description would be an indictment: a company that is everything is usually good at nothing. ORIX's wager, sixty-two years running, is the opposite — that the skill itself is the ability to be anything, to treat the balance sheet not as a warehouse where assets go to sit forever, but as a flowing river of capital that is always moving toward its highest use.

Whether that wager pays off from here is genuinely undecided, and that is the honest place to end. The bull sees a newly disciplined allocator, aligned by fresh incentives and armed with ¥370 billion of incoming bank-sale cash and a Qatari partner, finally forcing the market to close a discount it never deserved. The bear sees an unknowable ten-segment box whose record years are really a controlled liquidation of its best assets, with a growth rate that deflates the moment the exit window shuts. Both are looking at the same company; the difference is entirely in how much of ORIX's return you believe is repeatable skill versus well-timed harvest.

The three numbers in the last section will settle the argument over the coming years better than any narrative can — the trajectory of ROE and how much of it recurs, the scale of genuine third-party fee capital, and the split between base earnings and one-off gains. The chameleon has changed color more successfully than almost any company Japan has produced. The test of the Takahashi era is whether it can now do the one thing a chameleon has never had to prove: that the next color is worth more than the last.

References

-

One Year On: How Hidetake Takahashi Is Reshaping ORIX — ORIX IN ACTION, 2026-05-12 ↩↩↩

-

ORIX completes acquisition of Robeco — ORIX Corporation, 2013-07-01 ↩↩

-

Orix Buys Stake in Jet-Lessor Avolon as HNA Extends Asset Sale — Bloomberg, 2018-08-08 ↩↩

-

ORIX and VINCI Airports sign the Project Agreement for the Kansai International Airport and Osaka (Itami) International Airport Concession — ORIX Group, 2015-12-15 ↩

-

ORIX Corporation FY2026 Fourth Quarter Consolidated Financial Results Presentation — ORIX Corporation, 2026-05 ↩↩↩

-

ORIX names new CEO and unveils global organizational overhaul (Form 6-K) — StockTitan / ORIX Corporation ↩

-

From Profit to Profitability: ORIX lays out 2035 Growth Strategy for the next decade — ORIX IN ACTION, 2025-05-15 ↩↩↩↩

-

Earnings call transcript: Orix Corp Q4 2026 sees record profits, stock surges — Investing.com, 2026-05 ↩↩↩↩↩↩↩↩↩

-

Daiwa to buy Orix Bank for $2.3 billion in lending expansion — The Japan Times, 2026-04-28 ↩

-

ORIX Corporation FY2026 Fourth Quarter Financial Results — segment data — ORIX Corporation, 2026-05 ↩↩↩↩↩↩↩↩↩↩↩

-

ORIX and QIA Partner to Launch USD 2.5 billion Japan-Targeted Private Equity Platform — ORIX Group, 2025-11-11 ↩

-

ORIX: Qatar SWF-Backed OQCI Fund Acquires Nippon Information Industry — Pulse 2.0, 2026-05 ↩

-

ORIX Steps Up Share Buybacks With ¥39.6 Billion Repurchased by June 30 — The Globe and Mail, 2026-07 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube