Resona Holdings, Inc.: The Service Revolution of Japanese Banking

I. Introduction & Episode Roadmap

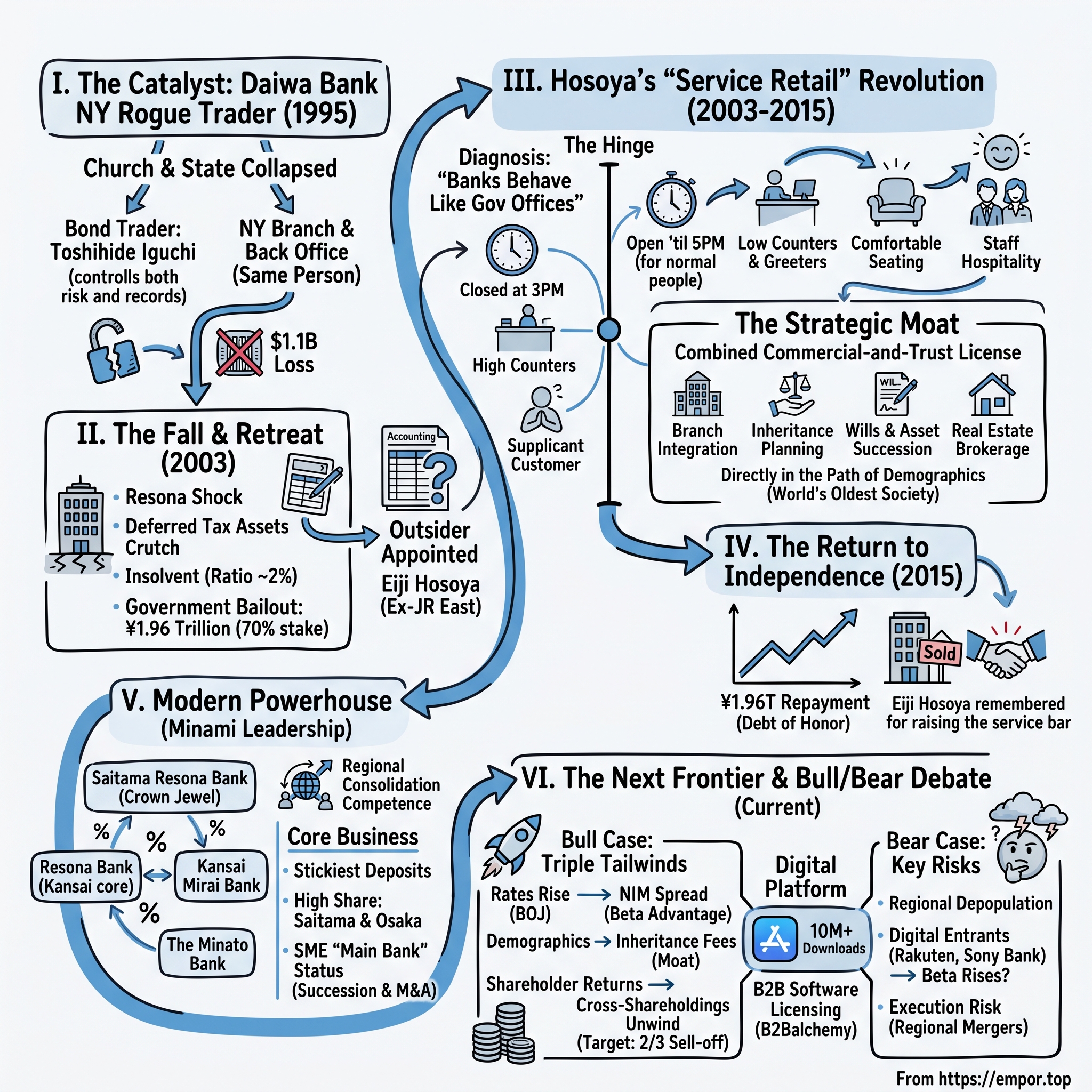

Picture a Japanese bank in the spring of 2003. Not a metaphor for the whole system — one specific institution, the country's fourth-largest banking group, its capital quietly evaporating in the back offices while depositors queued at the counters as if nothing were wrong. On paper, the bank had been surviving on an accounting fiction: it counted years of hypothetical future tax refunds — 繰延税金資産 deferred tax assets — as though they were real capital sitting in the vault today. When the auditors finally refused to bless that fiction, the group's regulatory capital ratio collapsed toward 2%, roughly half the 4% floor a domestic Japanese bank is required to hold.2 The bank was, in the language regulators avoid using out loud, insolvent.

What happened next became known in Japan as the りそなショック Resona Shock. Rather than let a top-tier lender fail and risk a chain reaction through an already fragile financial system, the government injected roughly ¥1.96 trillion of public money and took an effective controlling stake of around 70% of the voting rights.3 The old management was swept out. This was the closest thing modern Japan had to a nationalization of a major bank.

Most stories that begin this way end in the slow suffocation of bureaucracy — a ward of the state, kept alive on subsidies, managed for survival rather than customers. Resona did something stranger. The government reached past the entire fraternity of career bankers and handed the wreck to an outsider: 細谷英二 Eiji Hosoya, a former executive of the privatized railway 東日本旅客鉄道 JR East. Hosoya arrived with a heretical premise — that a bank is not a licensed utility administering money on the state's behalf, but a member of the "service retail industry," in the same business as a department store or a hotel.[^4]

The destination, more than two decades later, is the subject of this story. 株式会社りそなホールディングス Resona Holdings, Inc. (8308.T, listed on the Tokyo Stock Exchange operated by 日本取引所グループ Japan Exchange Group)10 repaid the last yen of that ¥1.96 trillion bailout in June 2015, returning fully to private hands.3 Under Group CEO 南昌宏 Masahiro Minami, it is today Japan's largest of the "super-regional" retail banking groups, built on a rare combined commercial-and-trust banking license, a digital app used by more than ten million people, and a structural tailwind it waited nearly a decade for: the 日本銀行 Bank of Japan finally letting interest rates rise again.46

Why should a global investor care about a Japanese super-regional bank at all? Because Resona sits at the intersection of three of the most important themes in Japanese markets today: the end of deflation and the return of positive interest rates after a generation; the corporate-governance reform that is finally prying loose the cross-shareholdings that locked up Japanese balance sheets for decades; and the demographic transition of the world's oldest large society, which is turning inheritance and business succession into central financial problems. Resona is a concentrated bet on all three at once. It is also a case study in institutional resurrection — a template for how a broken organization can be rebuilt not by financial engineering alone but by importing an outsider's idea of what the business is even for.

This is where we're headed. The roadmap: the 1995 New York rogue-trader scandal that banished Daiwa Bank from global finance; the Daiwa–Asahi merger and the 2003 audit that detonated the Resona Shock; the railwayman who rewrote the Japanese banking playbook; the four-bank regional model and the economics of Saitama and Osaka; the shift from negative rates to a net-interest-margin story; the quiet software business hiding inside a brick-and-mortar bank; management under Minami and the great cross-shareholding unwind; the moat tested against Helmer and Porter; and finally the bull-and-bear debate. Throughout, the posture is independent: management's claims are treated as claims until the evidence backs them, and where the celebrated story rests on assumptions rather than proof, we will say so.

II. The Precursor: The $1.1 Billion NY Rogue Trader & Daiwa Bank's Banishment

The story does not begin in Osaka boardrooms. It begins in a bond-trading room in lower Manhattan, and with a confession letter thirty pages long.

In September 1995, 大和銀行 Daiwa Bank — one of the two principal ancestors of today's Resona — disclosed that a single trader at its New York branch, 井口俊英 Toshihide Iguchi, had accumulated roughly $1.1 billion in losses on unauthorized U.S. Treasury bond trading. The staggering detail was the duration: the losses had built up in the shadows over eleven years, hidden by a man who controlled both the trading and the back-office record-keeping — the two functions that are supposed to be kept religiously separate precisely so this cannot happen.1 Iguchi forged records and sold off securities held in custody for clients to cover his tracks, papering over each hole by digging a deeper one.

To understand how one man hid a loss larger than many banks' entire capital base, you have to understand the structural sin at the heart of the affair. Iguchi ran the trading desk and also supervised the back office that recorded and confirmed those trades. In a properly run institution these are church and state — the people who take the risk are never allowed to keep the books that measure it, precisely because the temptation to hide a bad bet is overwhelming. Daiwa's New York branch had collapsed the two roles into one man, and that man spent more than a decade selling off Treasury securities held in the bank's custody accounts to fund his losses, then forging the statements that were supposed to prove the securities were still there. Each cover-up demanded a bigger one. By the end he was managing an eleven-year lie that had metastasized into eleven digits.

The scandal that destroyed Daiwa, though, was not the trading loss itself. It was what management did after learning of it. Iguchi confessed in a long letter to his superiors in Japan, and rather than immediately reporting the matter to U.S. authorities, the bank sat on the information for roughly two months while senior executives weighed how to handle it — an interval U.S. regulators treated as a deliberate cover-up by the institution itself, not merely by a rogue employee. That distinction was fatal. A single bad trader is a control failure; a bank that conceals losses from the Federal Reserve is a bank that cannot be trusted to operate in the country. The reaction from Washington was ferocious. Daiwa was indicted, pleaded guilty to a raft of federal charges, and agreed to pay a $340 million penalty, and — the truly consequential part — was ordered to shut down all of its banking operations in the United States and leave.1 Iguchi himself was sentenced to prison and later wrote a memoir about the affair.

Think about what that meant for a Japanese bank in the mid-1990s. This was the era when the giants of Japanese finance were planting flags in London and New York, competing to underwrite global bond issues and chase the prestige of international investment banking. To be expelled from the world's deepest capital market was not merely a fine; it was a strategic amputation. Daiwa's global ambitions were over.

And here is the twist that makes this an origin story rather than a footnote. While peers doubled down abroad and later loaded their balance sheets with the exotic securitized products that would blow up in 2008, Daiwa had no choice but to retreat home — to become a domestic commercial and retail bank serving Japanese households and small businesses. A humiliation imposed from outside hardened, over time, into a strategic constraint. Constraints, as this whole story will argue, are not always the enemy of a business. Sometimes they decide what a company is allowed to become.

It is worth pausing on how differently this could have read in real time. In 1995, being cut off from Wall Street looked like a competitive catastrophe. The prestige of the age belonged to the banks with New York and London trading floors; a domestic-only bank sounded like a demotion, a provincial lender consigned to the slow lane. No executive would have chosen it. But strategy is often written by what you are prevented from doing as much as by what you decide to do. The banks that kept their global ambitions spent the following decade accumulating precisely the kind of cross-border, hard-to-value exposures that turned poisonous in the global financial crisis. Daiwa, and later Resona, simply were not in that game. The moat that would eventually define Resona — a deep, sticky, purely domestic retail-and-SME franchise — was in a sense handed to it by a scandal it would have given anything to avoid. Daiwa was about to be forced back inside Japan just as Japan's banking system was walking toward a cliff of its own making.

III. The Collision: The Daiwa-Asahi Merger and the "Resona Shock"

By the turn of the millennium, the Japanese government wanted its wounded banks to huddle together for warmth. The bursting of the 1980s asset bubble had left the sector buried under bad property loans, and Tokyo's policy was consolidation: fewer, larger banks that could absorb losses and be supervised more easily. Out of this pressure, in 2001–2002, 大和銀行 Daiwa Bank combined with あさひ銀行 Asahi Bank — itself the earlier union of Kyowa Bank and Saitama Bank — to form the group that would be branded Resona.

On the surface it was a sensible marriage: Daiwa brought its Osaka and Kansai roots and a prized trust-banking franchise; Asahi brought a dense retail network across greater Tokyo and, crucially, near-total dominance of Saitama prefecture. The complementarity was almost textbook — two regional footprints that barely overlapped, one anchored in Kansai and one in the Kanto suburbs, joined into a group that could plausibly claim to be the leading retail bank in both of Japan's great population centers. Consolidation was also politically fashionable: the megabank groups were forming in the same window, and the government's not-so-subtle message to the second tier was to combine or be left exposed.

But both banks were carrying the same disease, and no amount of network complementarity cures a solvency problem. Their balance sheets were riddled with post-bubble non-performing loans — the residue of the 1980s, when Japanese banks lent against land and stock collateral at valuations that assumed prices only ever rose. When the bubble burst, those loans curdled, and the sector spent the 1990s in a slow-motion crisis that Japan never fully lanced. Both Daiwa and Asahi leaned on the same accounting crutch to look healthier than they were, and it is that crutch — not the merger — that would bring the new group to its knees.

That crutch deserves a plain-English explanation, because the entire crisis turns on it. When a bank writes off bad loans, it books a loss — but that loss can reduce its future tax bills. Accounting rules let the bank record the value of those expected future tax savings as an asset today: a deferred tax asset. Japanese banks were permitted to count a chunk of these DTAs as regulatory capital. The problem is that a future tax saving is only worth anything if you earn future profits to save tax against. For a bank bleeding money, counting five years of hypothetical future tax refunds as "capital" is like a struggling household listing next decade's expected tax rebates as cash in its checking account. It flatters the picture without adding a single yen of loss-absorbing substance.

In early 2003, the auditors decided they had had enough of the charade. Resona's independent accountants — the firms then known as Tohmatsu and Shin Nihon — balked at certifying the bank's practice of counting five years' worth of these deferred tax assets and forced the horizon down to three years.2 It sounds like an arcane adjustment. It was a detonator. Stripping out those phantom years of tax benefit sent Resona's capital adequacy ratio tumbling to roughly 2% — beneath the 4% minimum required of a domestic bank, and low enough to mean the institution could no longer stand on its own.2

The timing turned an accounting dispute into a national emergency. This was the era of 竹中平蔵 Heizo Takenaka, the economist Koizumi had installed to force Japan's banks to finally confront their bad loans rather than "evergreen" them indefinitely — rolling weak borrowers over year after year to avoid recognizing losses. Takenaka's program deliberately tightened the screws on how banks could count deferred tax assets and how rigorously auditors had to scrutinize them. Resona was, in effect, the first major bank to be caught in the closing jaws of that policy. Its auditors were not acting in a vacuum; they were responding to a regulatory climate that had suddenly made the old fictions untenable.

In May 2003, the government convened an emergency meeting, declared a systemic risk to the financial system, and — under Prime Minister 小泉純一郎 Junichiro Koizumi — authorized the roughly ¥1.96 trillion public capital injection that took an effective 70% voting stake and cleared out incumbent management.3 This was the りそなショック Resona Shock: the first rescue of a top-tier Japanese banking group on this scale since the acute crisis years of the late 1990s, and a jolt that rippled through global markets watching to see whether Japan would let a major bank fail or backstop it. The stakes were enormous. Had Tokyo let Resona collapse, depositors at every other wobbly regional bank would have asked whether they were next, and a system already starved of confidence could have seized up entirely.

Tokyo chose the backstop. But the choice was not purely mechanical recapitalization; it carried a message. Unlike some earlier interventions that quietly propped up banks and left management in place, the Resona rescue publicly removed the incumbents and put the institution under state control, signaling that a bailout came with consequences. And then the government attached to it something no one expected to matter as much as it did: a change of leadership that would come from entirely outside banking. That single personnel decision — the choice of who would run the nationalized bank — is the hinge on which the entire modern history of Resona turns.

IV. The Phoenix: Eiji Hosoya's "Resona Reform" & The Journey to Repayment

When the government went looking for someone to run its newly nationalized bank, the obvious candidates were the usual grandees — a retired megabank president, a senior figure from the Ministry of Finance. Instead it chose a 57-year-old railwayman.

細谷英二 Eiji Hosoya had spent his career at Japan National Railways and then at 東日本旅客鉄道 JR East, the enormous passenger railway carved out of the privatization of the state rail monopoly. He had helped turn a bloated, debt-laden public entity into a commercial operator that had to earn its keep by selling tickets and, increasingly, by turning stations into shopping destinations. He knew nothing about credit derivatives. What he knew was how a monopoly mindset rots an organization from the inside — and how to reverse it.[^4]

Why an outsider at all? Because the government, and Hosoya himself, understood that the disease at Resona was cultural as much as financial. Career bankers had built the fictions, tolerated the bad loans, and internalized the belief that a bank's job was to administer money on behalf of the state and the keiretsu, not to serve individual customers. Asking one of them to reform the culture was like asking a fish to critique water. JR East had faced a structurally similar problem a generation earlier — a sprawling, unionized, deficit-ridden public monopoly that had to learn, almost overnight, to think like a business that could lose customers. Hosoya had lived that transformation. He arrived at Resona not with banking expertise but with a template for turning a state utility into a commercial enterprise.

Hosoya's diagnosis of Japanese banking was blunt: banks behaved like government offices. They opened when it suited them, closed at three in the afternoon, hid their staff behind high counters, and treated customers as supplicants who should feel grateful to be served. His premise was that a bank is part of the service retail industry — that it competes for attention and loyalty the way a department store does — and from that premise flowed the program known as りそな改革 Resona Reform.[^4] He was fond of pointing out that the customer standing at the counter did not care about the bank's balance-sheet troubles; the customer cared whether the bank was open, whether the staff were pleasant, and whether the visit wasted an afternoon. Fix that, and trust would follow; fail at it, and no amount of financial engineering would save the franchise.

The reforms were almost provocatively concrete. Every other bank in Japan shut its branch doors at 3:00 PM; Hosoya ordered Resona branches to stay open until 5:00 PM, so that ordinary working people could actually visit their bank after work. He tore out the intimidating high counters and rebuilt branches to feel like retail stores, with greeters, comfortable seating, and private consultation booths where a customer could discuss a mortgage or an inheritance without an audience. Staff were trained in hospitality rather than in stamping forms. To a Western reader this can sound trivial; in the context of Japanese banking culture in 2003, it was close to revolutionary, and it forced every competitor to reconsider what "service" meant.

The reforms extended into the machine room as well as the lobby. Hosoya attacked the bank's notoriously expensive and error-prone systems and paperwork, pushing a "quality" campaign borrowed in spirit from manufacturing — treating a mistake in a branch the way a factory treats a defect on the line, as something to be measured and engineered out rather than tolerated. The point was cultural: a service business that constantly inconveniences customers with its own back-office errors cannot credibly claim to put them first. Efficiency and hospitality, in his framing, were the same project seen from two angles.

The most commercially shrewd move, though, was one Hosoya made by preserving rather than inventing. Daiwa had historically held a full-line trust banking license — the right to conduct 信託兼営 combined commercial and trust business under one roof. Most Japanese commercial banks did not have this; they had to hand trust work off to a separate specialist subsidiary, which meant a lost customer, a shared fee, and a fractured relationship. Hosoya kept the license and did something with it that others structurally could not: he pushed trust services — wills, inheritance planning, real estate brokerage, asset succession — directly out through ordinary commercial branches, so that the same relationship manager who arranged a small-business owner's loan could also help that owner plan the transfer of the family business and estate. In an aging country, that is not a side business. It is arguably the business. The demographic wave Japan now faces — trillions of yen in household wealth held by people in their seventies and eighties, waiting to pass to the next generation — was already visible in 2003, and Hosoya positioned the branches to be standing directly in its path.

Then came the grind, and it is the least glamorous but most instructive part of the story. A nationalized bank could have coasted under the state's protection, treating the public money as a permanent cushion. Hosoya instead treated it as a debt of honor to be repaid as fast as prudence allowed, and set a disciplined path back to independence: aggressively writing off the bad loans that had caused the crisis in the first place, closing redundant branches, cutting headcount, and steering the bank toward higher-margin retail and SME products where relationships, not balance-sheet scale, decide the winner. The discipline was cultural as much as financial — a nationalized institution that behaves like it is in a hurry to leave state control is signaling something about its self-respect to its own employees.

The repayment stretched across more than a decade, spanning the global financial crisis and the long deflationary grind that followed, which makes the persistence more impressive: this was not a bank riding a boom back to health, but one clawing its way out during some of the worst years for banking anyone could remember. Year by year, Resona bought back the government's holdings. In June 2015 it completed the final repayment of the public funds, returning to full private ownership — every yen of the roughly ¥1.96 trillion accounted for.3 Hosoya did not live to see it; he died in 2012, and is remembered in Japan as the outsider who saved a bank and permanently raised the bar for how banks treat customers.[^4] The image that endures is of a railwayman who looked at an insolvent bank and saw not a balance-sheet problem but a service business that had forgotten it had customers.

There is an honest caveat worth registering before we canonize the turnaround. Resona repaid the public funds in full, but "in full" for capital of this kind means principal plus the dividends the government collected along the way — it is a story of survival and restored independence, not of taxpayers earning a venture-capital return. What Hosoya bought Japan was avoided catastrophe and a functioning institution, which was the entire point. The bank that emerged carried a distinctive DNA into its next chapter.

V. The Modern Powerhouse: Saitama Resona & The "Four-Bank Model"

Walk into a Resona branch in a Saitama commuter town on a weekday afternoon and you are standing inside the payoff of Hosoya's bet. The counter is low, the staff greet you, and the customers are overwhelmingly local: households paying mortgages, retirees managing pensions, and the owners of the small manufacturers and shops that form the connective tissue of the regional economy. This is the opposite of a global investment bank, and deliberately so.

Structurally, Resona today runs what it calls a multi-bank regional model, concentrated in two of Japan's densest and wealthiest economic zones — the Tokyo metropolitan area and the Kansai region around Osaka, Kobe, and Kyoto. The group operates through 株式会社りそな銀行 Resona Bank, Limited, the core national and Kansai commercial-and-trust franchise; 株式会社埼玉りそな銀行 Saitama Resona Bank, Limited, dedicated to Saitama prefecture; 株式会社関西みらい銀行 Kansai Mirai Bank, Limited in the Kansai region; and 株式会社みなと銀行 The Minato Bank, Ltd. in Hyogo prefecture.7

The Kansai footprint was assembled through a piece of consolidation chess. In 2017–2018 Resona built 関西みらいフィナンシャルグループ Kansai Mirai Financial Group (KMFG) by combining Kansai Urban Banking, Kinki Osaka Bank, and Minato Bank — knitting together several weak regional lenders into a group with real scale in Osaka and Hyogo. Then, in April 2024, Resona folded KMFG fully into the parent holding company, delisting the intermediate group and turning Kansai Mirai Bank and Minato Bank into direct subsidiaries.[^5] The logic was mundane but real: eliminating a listed intermediate holding company removes duplicated governance and minority-interest leakage, lets back-office systems be centralized, and speeds the recirculation of capital across the group. Nikkei framed the move plainly as a cost-cutting integration.[^5] The analytical read is that Resona had learned to treat regional-bank consolidation as an operating competence rather than a trophy hunt — buy the deposits and the customers, then strip the redundant corporate structure.

The crown jewel of the model is Saitama Resona. Saitama prefecture is a suburban expanse north of Tokyo with a population north of seven million — a vast bedroom community whose residents commute into the capital but bank close to home. Within that market Saitama Resona occupies a position most banks can only envy: it is the designated financial institution for the prefectural government and for the overwhelming majority of its municipalities, giving it the payroll, tax, and settlement flows of the local public sector, and it commands a commanding share of regional loans and deposits.9 When a bank is embedded in a region's government plumbing and its residents' paychecks, its deposit base becomes both large and extraordinarily sticky.

It is worth dwelling on why that designated-institution status is so valuable, because it is easy to underrate. When Saitama Resona is the bank through which prefectural salaries are paid, local taxes are collected, and public accounts are settled, it sits at the center of the region's money flows in a way a competitor cannot dislodge by offering a slightly better rate. Every civil servant whose paycheck arrives at Saitama Resona is a default customer for a mortgage, a savings account, and eventually an inheritance consultation. The relationship is inherited almost by geography. That is close to a local monopoly on the highest-quality, lowest-cost deposits in one of the richest suburban markets on earth — and it explains why Saitama Resona has historically been one of the most profitable pieces of the entire group despite its narrow footprint. The lesson for the investor is that market share in banking is not a vanity statistic; in a business where funding cost is destiny, dominance of a wealthy local deposit base is the whole game.

That stickiness is the economic engine. Where the megabanks — 三菱UFJフィナンシャル・グループ MUFG, 三井住友フィナンシャルグループ SMBC, and みずほフィナンシャルグループ Mizuho — depend heavily on thin-margin lending to global corporations, Resona's profits come from local, retail, relationship-driven business. Broadly, its gross profits split into roughly equal halves between personal banking and corporate (chiefly SME) banking, with a smaller markets/treasury contribution — a mix weighted toward stable fee income and cheap-funded domestic lending rather than volatile trading.8

On the personal side, the drivers are residential mortgages — where Resona is a top-tier national originator — plus fee income from investment trusts, insurance, and the trust services (inheritance, wills, real estate) that Hosoya wired into the branches. This fee income deserves emphasis, because it is the part of the business that does not depend on interest rates at all. Every will drafted, every inheritance settled, every investment trust sold generates a fee for essentially no balance-sheet risk, and it deepens a relationship that competitors would have to unwind account by account. In the negative-rate years, when lending spreads were crushed, it was precisely this fee machine — and ruthless cost control — that kept Resona's returns respectable while pure-lending regionals struggled.

On the corporate side, the franchise is built almost entirely around small and medium enterprises, where Resona holds coveted "main bank" status for large numbers of businesses in Saitama and Osaka — the primary banking relationship through which a company runs its accounts, borrows, and increasingly seeks succession and M&A advice. For a firm whose owner is aging and whose children may not want the business, that advisory relationship is worth far more than the loan spread; helping a retiring owner sell or transfer a company generates advisory fees, and often keeps the successor's banking relationship inside Resona for another generation. Business succession has quietly become one of the defining commercial problems of corporate Japan, and a bank with thousands of SME main-bank relationships is sitting on a natural pipeline of that work.

The materiality point for investors is simple: Resona's earnings are geographically narrow but functionally broad, and the profitability lives in the depth of each relationship, not the breadth of the map. It is a bank that has chosen to own two rich regions completely rather than to be a thin presence everywhere. The risk embedded in that choice — regional concentration in a country that is depopulating outside its biggest cities — is real, and we will return to it. But what the concentration needs above all to keep working is a rising rate environment, so that the enormous, cheap deposit base finally earns a spread again. After nearly a decade of the opposite, that environment finally arrived.

VI. The Next Frontier: Positive Interest Rates & The NIM Resurgence

For a domestic Japanese bank, the years after 2016 were an exercise in trying to earn a living with the oxygen turned down. When the Bank of Japan pushed its policy rate below zero, it was trying to force money out into the economy; the side effect was that banks earned almost nothing on the gap between what they paid for deposits and what they charged for loans. That gap — the net interest margin, or NIM — is the fundamental profit spring of banking, the difference between the cost of the money a bank takes in and the yield on the money it lends out. Under negative rates it was compressed to a sliver, and banks like Resona survived on fee income and relentless cost-cutting rather than on lending spreads.

Then the tide turned. In March 2024 the Bank of Japan ended its negative interest rate policy and raised rates for the first time in seventeen years, signaling a genuine regime shift for Japanese lenders after a generation of near-zero and sub-zero money.4 Rates have continued to edge higher since. For most of the economy this is a mixed blessing; for a deposit-heavy retail bank it is close to a windfall, and understanding why is the crux of the modern investment case.

Resona sits on an enormous pool of cheap, sticky deposits — a group deposit base of around ¥63.7 trillion, well over half of it from individuals.6 Those depositors are not chasing yield; they bank with Resona because their salary lands there and their mortgage is drawn there. This matters because of an asymmetry bankers call deposit beta. When market rates rise, a bank can reprice its loans upward relatively quickly — especially floating-rate mortgages and corporate loans — but it can raise the interest it pays ordinary depositors slowly, and by only a fraction of the move, because those depositors are not going anywhere. The spread between the two widens, and because it applies across a multi-trillion-yen balance sheet, small changes in rate translate into large changes in profit.

A concrete analogy helps. Imagine a household that has lent out ¥60 trillion at a variable rate and borrowed the same money from its own family members who never ask for interest. When the market rate rises by a percentage point, the household's income from its loans rises by roughly ¥600 billion a year, while what it pays the family barely changes. That is a caricature of Resona's balance sheet, but only a mild one: the bank borrows overwhelmingly from patient retail depositors and lends into a book that reprices upward with the BOJ. The gearing is enormous precisely because the balance sheet is enormous relative to the profit.

The FY2025 numbers (the year ended March 31, 2026) show the mechanism turning. Net income attributable to owners rose about 21% year on year to roughly ¥258.7 billion, with domestic net interest income lifted by a "rate factor" of tens of billions of yen as higher rates flowed through the book.6 The residential loan engine kept feeding the effect: new mortgage originations grew nearly 20% to around ¥1.53 trillion, and — the detail that makes Resona so rate-sensitive — roughly 96% of that new lending was variable-rate, meaning it reprices upward as the BOJ moves.6 Management guided FY2026 net income up toward ¥310 billion, a further step on the path it has laid out to FY2028.6 Management's own scenario framing is that a 1.0% policy rate supports a return on equity near 12%, rising toward 14% at 1.5%.56

There is a Japanese cultural wrinkle worth flagging for foreign investors, because it is a genuine swing factor: the enormous popularity of variable-rate mortgages. In most countries households prize the certainty of a fixed rate; in Japan, after a generation of near-zero rates, borrowers grew accustomed to floating-rate loans that were always cheap. That is wonderful for a lender when rates rise — the interest income climbs immediately. But it also transfers rate risk onto households that have never in their adult lives seen their mortgage payment increase. If rates rise far and fast, some of that floating-rate book could turn into credit stress, which is why the quality of Resona's mortgage underwriting, not just the size of the spread, matters to the story.

Here neutrality requires a hard look at the other side of that same equation, because the bull case and the bear case are the same coin. Low deposit beta is an assumption, not a law. It holds as long as depositors stay loyal at rates far below what they could earn elsewhere; the moment digital competitors or rising money-market yields make that gap painful enough to notice, beta rises and the windfall narrows. A variable-rate mortgage book that reprices up also carries credit risk if higher payments strain over-extended households. And rate sensitivity cuts both ways — every basis point of upside the bank enjoys on the way up reverses if the BOJ pauses or retreats. The rate story is real and it is powerful, but it is a bet on the BOJ's path and on depositor inertia, not a guaranteed annuity. Which is exactly why Resona has been building a second engine that does not depend on interest rates at all.

VII. The Hidden Growth Engine: Open Financial Digital Platform

Here is a problem that keeps regional-bank executives across Japan awake at night. Modern retail banking runs on software — slick mobile apps, cloud back-ends, real-time payments — and building that software costs billions of yen a year. A megabank can amortize that spend across tens of millions of customers. A small regional bank with a few hundred thousand customers cannot, which leaves it exposed to digital-native rivals like 楽天銀行 Rakuten Bank, ソニー銀行 Sony Bank, and the reorganized SBI新生銀行 SBI Shinsei Bank that were born without branches and without legacy cost. For a traditional regional lender, the app it cannot afford to build is a slow-motion existential threat.

Resona's answer was to build the app anyway, and build it well. The りそなグループアプリ Resona Group App became one of the most heavily used banking apps in Japan, surpassing ten million cumulative downloads by early 2026 — a scale that, for a bank whose customers skew older and regional, represents a genuine behavioral shift rather than a vanity metric.6 The app is not merely a balance-checker; it is Resona's lowest-cost distribution channel, the place where it can nudge a depositor into an investment trust or an inheritance consultation without the fixed cost of a branch visit.

The strategically interesting move is what Resona chose to do with that platform once it worked: instead of guarding it as proprietary, it began offering it to others. Resona has white-labeled and licensed its digital banking platform to independent regional banks and embedded banking functions into corporate partners' apps — for example, integrating banking services into the WESTER app of 西日本旅客鉄道 JR West.7 The pitch to a fellow regional bank is compelling: rather than spend years and billions building an inferior app, rent a world-class one, keep your brand on the front, and let Resona run the plumbing behind it.

The business model this creates is qualitatively different from lending. Resona earns recurring, fee-based, capital-light income — revenue that requires almost no additional balance sheet and does not consume regulatory capital the way a loan does. In banking terms this is close to alchemy: a loan ties up capital and carries default risk, whereas a software licensing fee is nearly pure margin that scales with the partner's customer base rather than Resona's own balance sheet. If it scales, it converts an expensive internal cost center (IT R&D) into a B2B software franchise sold to the very ecosystem of regional banks Resona might otherwise only compete with. That is the theory, and it is a genuinely attractive one.

There is also a defensive logic that is easy to miss. Even if the licensing fees never become large, every regional bank that adopts Resona's platform becomes, in a sense, an extension of Resona's technology footprint rather than a customer for a digital-native rival like Rakuten Bank. Resona is effectively organizing a coalition of traditional regional banks around shared infrastructure, spreading the fixed cost of staying technologically relevant across many balance sheets instead of one. In an industry where the fear is that scale players and fintechs will pick off regional banks one by one, being the aggregator of the regionals' technology is a genuinely clever position to occupy — if it works.

The independent caveat is proportion. As of today this platform business is strategically important but financially small relative to a group earning a quarter-trillion yen a year from banking; the licensing revenue is not yet a needle-mover on group profit, and Resona does not break it out as a large standalone line. There is also execution risk in becoming a vendor to your competitors — partners may worry about depending on a rival's infrastructure, and Resona must keep the platform genuinely best-in-class to justify the arrangement. The right way to hold this is as real optionality with a plausible path to scale, not as a proven earnings pillar.

There is a second-layer risk that the digital pivot quietly amplifies, and it deserves a flag: operational and cybersecurity exposure. Japanese banking has a painful institutional memory of system failures — the most infamous being the repeated IT meltdowns at a megabank rival that drew regulatory censure and eroded customer trust. As Resona pushes more of its customer relationships and, increasingly, other banks' relationships onto a shared platform, it concentrates operational risk: a serious outage or a data breach would now damage not only Resona's own customers but its partners' as well, converting a technology strength into a reputational and regulatory liability. Running critical infrastructure for a coalition of banks is a heavier responsibility than running your own app, and the 金融庁 Financial Services Agency watches these things closely. Whether the platform becomes an earnings pillar rather than a liability depends heavily on execution — and on the person now setting the group's agenda.

VIII. Management Under the Microscope: Masahiro Minami's Playbook

Consider the strangeness of the assignment. A young man joins Daiwa Bank in 1989, at the absolute peak of the Japanese bubble, when the country's banks were briefly the largest in the world and a job at one was a job for life at the summit of the economy. Within a few years he watches the New York scandal humiliate his employer, then the bubble collapse, then the slow-motion banking crisis, then the audit that pushes his bank into the arms of the state, then a railwayman arrive to tear up everything he was taught about how a bank should behave. He stays through all of it. Three decades later, that man is running the company. That is the biography of 南昌宏 Masahiro Minami, and it is impossible to understand his leadership without it.

If Eiji Hosoya was the outsider who broke the old bank, Minami is the insider charged with compounding what the outsider built. Minami has been Group CEO since 2020, and his résumé is the mirror image of Hosoya's: a lifer who has spent his entire career inside the institution.7 Where Hosoya's authority came from knowing nothing about banks — from being unable to see why "that's how we've always done it" was a reason for anything — Minami's comes from the opposite source: from having lived every chapter of this one, and therefore knowing exactly which of the old instincts nearly destroyed the bank and must never be allowed to return. It is a credibility with staff and board earned over three decades, and it is the right kind of credibility for the phase Resona is now in. The break was Hosoya's job; the compounding is Minami's.

That insider status is a double-edged asset, and an independent appraisal should say so. A lifer knows where the bodies are buried and can move an organization without a fight; a lifer can also be the last person to challenge the institution's comfortable assumptions. The way to judge Minami is not by his biography but by his behavior over time — his target-setting, his capital discipline, and whether the story stays consistent across successive filings and calls.

On alignment, the picture is honestly mixed and typical of Japanese "salaryman" chief executives. Minami's personal shareholding is small — on the order of tens of thousands of shares, a modest sum relative to the enterprise he runs — which is a governance weakness by the standards activists prefer.7 Resona has moved to address this with a performance share unit trust scheme that pays a meaningful slice of executive compensation in stock tied to medium-term targets including ROE, net income, and ESG metrics.7 It is a step toward the "eat your own cooking" alignment Anglo-American investors expect, though a step, not a transformation.

The clearest test of Minami's ambition is the new medium-term management plan branded "Shift to the Next Stage," setting out the path to FY2028. The headline targets are deliberately aggressive: consolidated net income of around ¥390 billion and a return on equity in the low-teens — framed as roughly 12% at a 1.0% policy rate and as high as 14% if rates reach 1.5% — a clear step up from the prior plan's ambitions, which had centered on an ROE target closer to 8%.56 Tethering the ROE target explicitly to the BOJ's rate path is intellectually honest, because it admits the single biggest swing factor is outside management's control; it is also convenient, because it gives management a ready explanation if the target is missed. Investors should track whether Resona hits the net income figure on operating execution or leans on the rate tailwind to carry it.

Credibility in management is not built by setting targets; it is built by hitting the ones you set before. Here Resona's recent record is a point in its favor. The FY2025 net income of roughly ¥258.7 billion came in ahead of the company's own initial guidance for the year, and the 21% growth was not a one-line surprise but the compounding of the levers management had told investors it would pull — rising loan yields, disciplined costs, and gains crystallized from selling cross-shareholdings.6 A management team that raises its multi-year ambitions is only credible if it is also delivering against the current year, and on that narrow test the numbers cooperate. The harder question — whether the low-teens ROE survives if the rate tailwind stalls — cannot be answered from a single good year, and a skeptical investor is right to keep it open.

One subtle discipline worth watching is narrative consistency. Across successive investor presentations and results briefings, Resona has kept telling the same story in the same order — retail and SME focus, trust and fee income, capital returned as cross-shareholdings unwind, rates as the swing factor. Management teams in trouble tend to change the subject; the ones worth trusting tend to bore you with consistency. So far Resona's messaging has been of the boring kind, which for a bank that once nearly collapsed is not nothing.

The most concrete evidence of discipline is capital allocation, and here Resona is doing something structurally important to Japanese finance: unwinding its cross-shareholdings. For decades Japanese banks held 政策保有株式 policy-oriented stockholdings — friendly equity stakes in their corporate clients, held to cement relationships rather than to earn a return, and locking up capital in the process. Resona has committed to cutting these holdings by two-thirds or more by book value by March 2030 versus March 2024, a reduction that on the group's own framing would leave it having shed the large majority of the cross-shareholdings it carried at its early-2000s peak.5 In FY2025 alone the sell-down generated over ¥100 billion in gains.6 The freed capital is being pointed in two directions: reinvestment in growth (IT, the digital platform, SME consulting) and returns to shareholders, with a committed total shareholder return ratio of 50% or higher and a targeted dividend-on-equity ratio around 3.5% by the end of the decade.56 Behaviorally, this is the most credible part of the story — a specific, measurable, multi-year commitment that can be checked against results each year rather than a vague aspiration. Whether it is fast enough is exactly what the skeptics contest.

IX. Strategic Moat Analysis: 7 Powers & 5 Forces

Strip away the narrative and ask the cold question a competitor's strategist would ask: what actually stops someone from taking Resona's business? Run it through Hamilton Helmer's 7 Powers, and a few genuine advantages survive scrutiny — while others turn out to be softer than the company would like.

The strongest is best described as a cornered resource: the combined commercial-and-trust banking license. Because Resona can cross-sell inheritance planning, real estate brokerage, and asset-succession services directly through the same branches that make loans and take deposits — rather than referring customers to a separate trust subsidiary the way most commercial banks must — it sits in a structurally advantaged spot in the one market that Japan is guaranteed to have in abundance. Japan is aging faster than almost any society in history, and a vast pool of household financial assets is passing from one generation to the next. Being the bank that already has the relationship and the legal capacity to handle that transfer is a durable edge that a competitor cannot simply decide to copy; it would need the license, the branch integration, and the decades of relationships all at once.

The second power is switching costs, expressed through main-bank status. For the small-business owner in Saitama or Osaka whose payroll, tax payments, credit lines, and settlement all run through Resona, changing banks is not a matter of comparing rates — it is a disruptive operational project touching every part of the business. Rewiring payroll, migrating years of transaction history, re-establishing credit lines with a new lender that does not yet know the business: the friction is enormous, and it compounds with age as the relationship accumulates. This is why deposit funding at a well-embedded regional bank is so stable and so cheap. The same logic explains why Resona deliberately avoids fighting the megabanks for large corporations, whose treasurers can and do shop their business across banks with a spreadsheet; the SME, by contrast, is far more captive, and captivity — put less pejoratively, loyalty backed by switching cost — is the foundation of the funding advantage.

The third, process power, is the one to hold most skeptically. The customer-centric operating culture Hosoya embedded — long hours, high-touch service, trust cross-selling as a reflex — is a genuine organizational asset that competitors have struggled to replicate wholesale. But two decades on, rivals have copied the visible pieces (few banks still slam the doors at 3 PM as a point of pride), and "our culture is better" is the kind of moat that is easy to assert and hard to prove. Treat it as a supporting advantage, not a load-bearing one.

Porter's Five Forces sharpen the competitive map. The threat of new entrants is low in the traditional sense — banking licenses are tightly guarded by the 金融庁 Financial Services Agency — but digital-only banks are a soft entrant chipping at plain-vanilla deposits and payments. Buyer power is split: depositors have little leverage and less inclination to move (the sticky-funding advantage), while large corporate borrowers can and do play Resona off against the megabanks, which is precisely why Resona concentrates on SMEs rather than blue-chips. Supplier power — in banking, the suppliers of capital and labor — is favorable, because cheap retail deposits are the lowest-cost funding a bank can have. The threat of substitutes is real and growing: online brokers such as SBI証券 SBI Securities and independent asset managers are capturing retail investment flows that might otherwise sit in Resona's fee-generating products, a pressure Resona counters with its own digital wrap accounts and investment trusts. And competitive rivalry is intense but geographically bounded: Resona rarely fights the megabanks for global corporates, instead facing regional heavyweights like コンコルディア・フィナンシャルグループ Concordia Financial Group (parent of Bank of Yokohama) and 千葉銀行 Chiba Bank in the greater Tokyo area, and a scrum of local lenders in Kansai. The honest synthesis: Resona's moat is real where it rests on the trust license and main-bank switching costs, and thinner where it rests on culture and on deposits that a better app could eventually pry loose.

X. Investment-Story Spine: Bull vs. Bear Case & Activist Stress Test

Every good investment debate can be reduced to a single sentence for each side, and then tested. Let us do both — but first, three consensus narratives about Resona are worth holding up to the light, because each is half true and half misleading.

Myth: Resona is "just a bailed-out Japanese bank." Reality: it repaid every yen of the public funds and has since run a genuinely differentiated retail-and-trust model. But the caveat matters — "repaid in full" means principal plus the dividends the government collected, a story of survival rather than of taxpayers being enriched, and the bank still carries the conservative instincts of an institution that once nearly failed.

Myth: rising rates are unambiguously good for Resona. Reality: they are good on balance and clearly showing up in the numbers, but the benefit is contingent on depositor loyalty (low deposit beta) and on households absorbing higher variable-rate mortgage payments without defaulting. The upside is real; the assumptions underneath it are not guaranteed.

Myth: the digital platform makes Resona a fintech. Reality: it is a traditional bank with a very good app and an interesting, still-small B2B licensing business. Treating the platform as a proven earnings engine today would be getting ahead of the evidence. With those corrections in mind, the bull and bear cases come into sharper focus.

Why Resona wins from here. The bull case rests on four legs. First, it is arguably the purest listed play on Bank of Japan rate normalization — a deposit-funded retail bank whose margins expand mechanically as rates rise, with the FY2025 results already showing the effect flowing to the bottom line. Compared with the megabanks, whose earnings are diluted by global markets businesses, overseas lending, and complex trading books, Resona's profit-and-loss is a cleaner transmission belt from the domestic policy rate to net income; there is less noise between the BOJ's decision and Resona's margin. Second, the inheritance wave: Japan's demographics turn the trust license into a multi-decade tailwind for high-margin fee income exactly as household wealth transfers between generations, and Resona is one of the very few commercial banks structurally equipped to capture it inside its own branches. Third, the capital-return machine: the disciplined unwind of cross-shareholdings converts dead capital into buybacks and dividends, with a committed 50%-plus total return ratio and a targeted dividend-on-equity ratio near 3.5%, and mathematically supports the march toward a low-teens ROE by shrinking the equity base even as profits grow. Fourth, the asset-light digital platform offers optionality to diversify away from cyclical lending. Each leg has real evidence behind it, which is more than many bull cases can say — the results, the demographics, the license, and the buyback commitments are all observable today, not just projected.

Why the case could break. The bear case is not the mirror of naive optimism; it attacks the same facts from the other side. The demographics that create the inheritance opportunity also shrink the customer base: Saitama and Kansai are aging, and if regional population decline outruns the growth in wealth-transfer fees, core loan demand simply contracts. Inheritance is, after all, a one-time transfer of an existing pool of wealth, not a renewable source of new customers — the fees can be lucrative even as the underlying population shrinks, but a bank cannot grow forever by helping its customers die tidily. The sticky-deposit advantage is a behavioral assumption that a generational shift could invalidate — if younger, digitally-native customers permanently migrate to Rakuten or Sony Bank, Resona's cheap funding erodes, deposit beta rises, and the celebrated NIM expansion quietly reverses. The very fact that Resona has poured resources into its own app is an implicit admission that this threat is real; the app is as much a moat-defense project as a growth project. And the consolidation competence has limits: integrating legacy regional banks in Kansai carries real friction from labor practices and entrenched local cultures, and the back-office and headcount savings promised in a merger are notoriously easier to announce than to bank. The April 2024 absorption of Kansai Mirai Financial Group is still being digested, and the true measure of that deal will be the cost synergies that actually show up in the numbers over the next few years, not the ones in the announcement deck.[^5]

The activist and skeptic's stress test. A hard-nosed long/short investor would press three points. The first is on the ROE target: "12% is optimistic if the BOJ slows or reverses — strip out the rate tailwind and show me the underlying operating improvement." That is a fair challenge, and it is why the rate-contingent framing of the target, while honest, invites scrutiny. A low-teens ROE would still lag the best global banks, and much of Japanese banking has historically earned returns below its cost of equity — the reason so many trade at or below book value. Resona is asking the market to believe it can decisively cross that line and stay there.

The second is on capital allocation: activists have argued Resona should sell down its residual policy stocks faster than the 2030 timetable and return closer to 100% of the proceeds directly through buybacks, rather than recycling capital into lower-return regional-banking partnerships and platform investments whose payoff is unproven. The unwind of 政策保有株式 is one of the clearest governance improvements available to any Japanese bank, because these holdings tie up capital, obscure the true return on the core business, and create conflicts of interest with the very companies the bank lends to. The debate is not whether to sell but how fast, and who gets the proceeds. An impatient activist wants it all now and returned to shareholders; management wants to reinvest some of it in growth. Both cannot be fully right.

The third is governance itself. A CEO with minimal personal shareholding, running a group that still carries the complexity of a multi-bank structure, invites the question of whether capital is being managed for per-share value or for institutional preservation. A skeptic would also probe the durability of the fee income, the credit quality hiding inside a fast-growing variable-rate mortgage book, and whether the reported cost discipline survives once the easy rate-driven profits arrive and the pressure to cut relents. Resona's answer, in effect, is that it can do both — grow and return capital — and the coming years of results are the only thing that will settle whether that is discipline or having it both ways. The most useful stance for an investor is to withhold the benefit of the doubt and watch the cash: the buyback execution, the pace of the stock sales, and whether the operating profit grows when you neutralize the rate tailwind.

XI. Playbook & Business Lessons

Step back from the balance sheet, and Resona offers four lessons that travel well beyond banking.

Constraints breed focus. The 1995 New York scandal felt like a death blow, and in the narrow sense it was — it ended Daiwa's global ambitions. But the banishment from international markets meant Daiwa never loaded up on the toxic securitized products that devastated globally-minded peers in 2008. A humiliation forced a focus on the domestic core, and the focus turned out to be the safer, more defensible business. The lesson is not that constraints are good; it is that a forced narrowing of scope can concentrate a company on what it actually does well.

Service can be a structural advantage, not a cost. Hosoya's reforms proved that even a nationalized utility can be reanimated by importing customer-first principles from an outside industry. The insight worth stealing is that the reforms came from a railwayman, not a banker — sometimes the person who cannot see why "that's how it's always been done" is the only one who can change it.

Bundle regulated products into a single interface. Resona's most durable moat comes from stapling two separate regulatory licenses — commercial banking and trust — into one customer relationship. The general principle: when you can legally combine two products your competitors are forced to keep separate, the combination itself becomes the moat, because copying it requires re-fighting regulatory and structural battles that took decades to win.

Platformize the cost center. Rather than treat its expensive app as a defensive necessity, Resona is trying to sell it to the same regional banks it competes with, turning IT spend into recurring fee revenue. The lesson — proven in software, still being tested here — is that if you are forced to build something expensive and you build it well, the build itself can become a product.

XII. Epilogue & Outro

For the investor who wants to follow this story rather than take a snapshot of it, three numbers matter more than the rest.

The first is the yen net interest margin — the single clearest gauge of how much of the Bank of Japan's rate normalization is actually reaching Resona's bottom line, and whether the celebrated deposit-beta asymmetry is holding or eroding. The second is Resona Group App engagement — not just cumulative downloads past the ten-million mark, but whether the bank is successfully converting those users into buyers of fee-generating trust and investment products, which is where the app earns its keep. The third is the book value of policy-oriented stockholdings — the running tally of the promised two-thirds reduction by March 2030, the cleanest test of whether management's capital-return commitments are being executed on schedule or quietly slipping.

The arc of Resona Holdings is one of the more remarkable and least-told corporate resurrections in modern finance. It ran from a rogue trader in Manhattan to an accounting reckoning that forced a near-nationalization, and from there to full taxpayer repayment and a distinctive retail-and-trust franchise leaning into the first rising-rate environment Japanese banks have seen in a generation. What makes it worth studying is not that Resona survived — plenty of bailed-out banks survive — but that it used the crisis to redefine what a Japanese bank could be.

There is a broader lesson embedded in the timing, too. For most of the last three decades, being a domestically-focused Japanese bank meant being trapped: trapped by deflation, by zero rates, by a shrinking population, by cross-shareholdings that dead-weighted the balance sheet. Resona's whole strategy was, in effect, a wager that these conditions would eventually reverse — that rates would normalize, that governance reform would let capital be freed, and that an aging society would generate demand for exactly the trust and succession services Resona was uniquely licensed to provide. Around 2024, those wagers began paying off more or less simultaneously. The risk for any investor is mistaking a favorable turn in the macro tide for the permanent triumph of the strategy. The tide can go back out.

Whether Resona's redefinition compounds into the low-teens returns management now promises is a question the next several years, and the three KPIs above, will answer. The independent posture is to admire the resurrection, respect the strategy, and still make the company prove it — quarter by quarter, in the net interest margin, in app engagement that converts to fees, and in the steady disappearance of the cross-shareholdings from the balance sheet. The rogue trader, the audit that nearly killed the bank, and the railwayman who saved it are all history now. What remains is the harder, quieter test of whether a resurrected institution can turn a lucky macro turn into a durable machine.

References

-

Rogue Trader Sentenced to 4 Years in Daiwa Case — The New York Times, 1996-12-17 ↩↩

-

Auditors Spar Over Capital Adequacy at Troubled Banks — The Japan Times, 2003-05-20 ↩↩↩

-

Japan's Resona Holdings Repays Last of Bailout Funds — Reuters, 2015-05-29 ↩↩↩↩

-

BOJ Ends Era of Negative Rates With First Hike in 17 Years — Bloomberg, 2024-03-19 ↩↩

-

Resona Holdings' FY2025 Results and the FY2028 Path to Value Creation — Fintech Observer, 2026 ↩↩↩↩↩↩↩↩↩↩↩

-

Resona Holdings Investor Relations Portal — Resona Holdings, Inc. ↩↩↩↩↩

-

Resona Group Integrated Report 2025 — Resona Holdings, Inc. ↩

-

Official Corporate Information of Saitama Resona Bank — Saitama Resona Bank ↩

-

Tokyo Stock Exchange Listed Company Profile: Resona Holdings (8308) — Japan Exchange Group ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube