BYD: The Vertical Integration Colossus

I. Introduction & Episode Roadmap

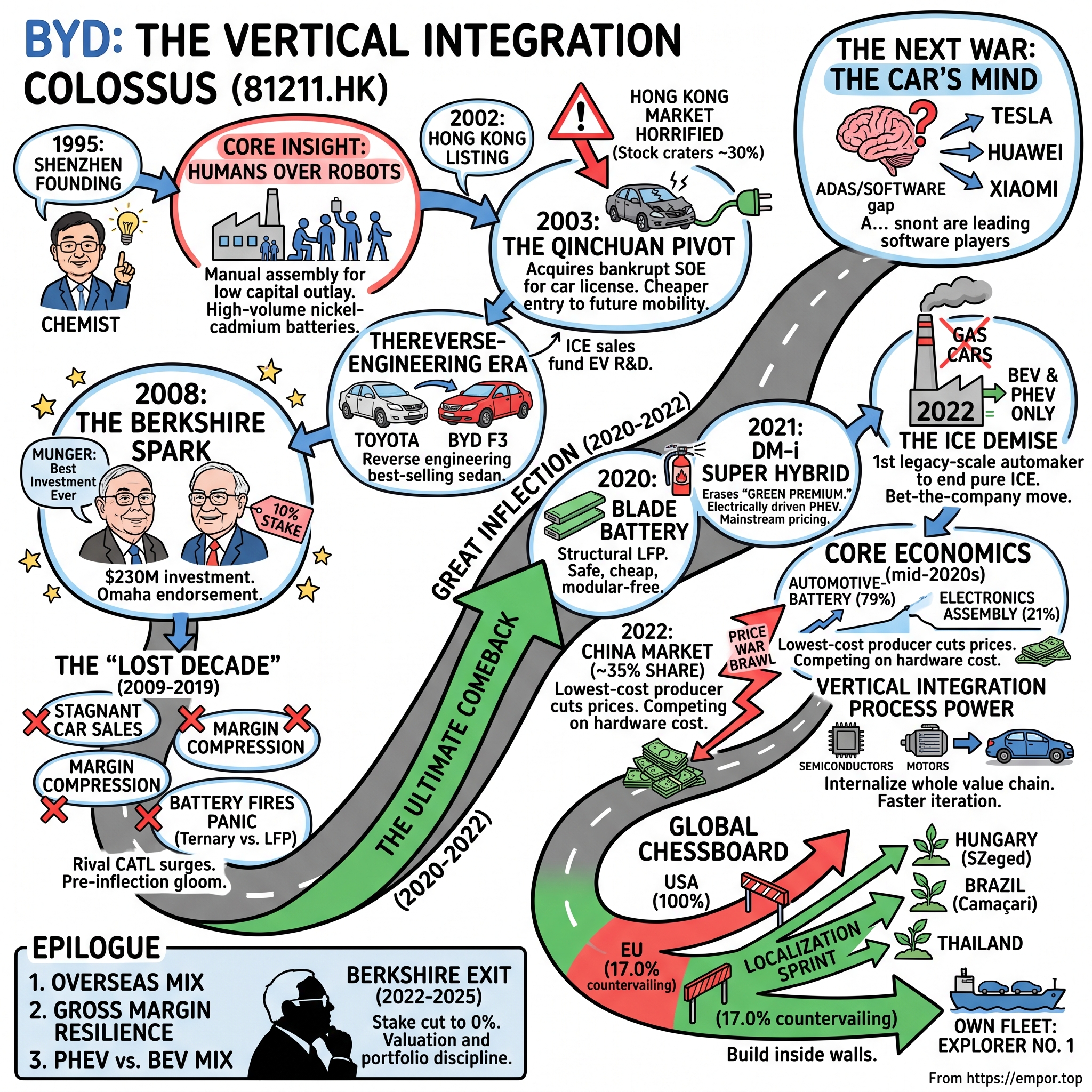

In the spring of 1995, a 29-year-old metallurgical chemist walked out of a government research institute in Beijing, borrowed money from a relative, and moved to 深圳 Shenzhen to make rechargeable batteries by hand. He could not afford the automated Japanese production lines that his competitors used, and he could not get a bank loan. Three decades later, the company he founded — 比亚迪 BYD — builds more plug-in vehicles than any other manufacturer on Earth, fabricates its own microchips and electric motors, casts its own battery cells, digs lithium out of its own mines, and sails its finished cars across oceans on its own fleet of car-carrier ships. Along the way it has thrown the world's legacy automakers into something close to existential panic.

That chemist, 王传福 Wang Chuanfu, still runs the place. And the scale he has assembled is genuinely difficult to hold in your head. In its 2024 financial year, BYD reported revenue of RMB 777.1 billion — roughly $107 billion — up 29% year over year, with net profit attributable to shareholders of RMB 40.3 billion, up 34%.[^1]1 It sold 4.27 million new energy vehicles (NEVs) in the year, a 41% jump.1 Tucked inside the group is a separately listed consumer-electronics arm, 比亚迪电子 BYD Electronic (00285.HK), that assembles phones and components for the likes of Apple and represents roughly a fifth of the top line — a business most people don't even associate with the BYD badge.[^1]

Here's the mystery that makes BYD such a compelling case study rather than a victory lap. For 17 years, 伯克希尔 Berkshire Hathaway owned a piece of this company. Charlie Munger called it one of the best investments he ever touched. The stake compounded more than twenty-fold. And then, quietly, Berkshire sold every last share — its filings recorded the position at zero by the autumn of 2025.2 Why would one of the most patient pools of capital in the world walk away from the winner of the electric-vehicle era, precisely as that winner was crushing its competition?

Consider the sheer physical throughput. Four-and-a-quarter million vehicles in a single year is more than double what Tesla delivered globally, and it makes BYD, by volume, one of the largest automakers on the planet — a company that did not sell a single car until it was nearly a decade old. Sitting behind those cars is a level of manufacturing self-sufficiency that has no real analog among Western OEMs. Where Volkswagen or General Motors buys cells from 宁德时代 CATL, LG, or Panasonic, buys chips from the merchant semiconductor market, and buys the ocean freight to move finished cars, BYD makes or owns nearly all of it. That is not a marketing flourish; it is the entire investment case, and the entire risk, compressed into one word: integration.

This is the story of how you get from a hand-assembly battery workshop to an industrial machine that frightens Volkswagen and Toyota — and of the questions a sober investor should ask about whether that machine can keep compounding. We'll trace the audacious purchase of a bankrupt state-owned carmaker, the invention of a battery shaped like a razor blade, the hybrid that erased the price gap between electric and gasoline cars, the capital-markets endorsement from Omaha and its eventual withdrawal, the disciplined bargain-hunting inside the electronics arm, the brutal price war now grinding down margins across China, and the geopolitical wall of tariffs going up around the Western world. Throughout, the posture here is neutral: BYD's engineering is real, its cost advantage is measurable, and its risks — a software gap, a margin-destroying home market, and a hostile trade environment — are equally real. This is not a shareholder letter. It's an attempt to test a thesis. Let's start where it started: with a man who decided that robots were overrated.

II. The Chemist's Gambit: Batteries, Shanzhai Phones, & The Qinchuan Pivot (1995–2003)

Wang Chuanfu was an orphan raised by his older siblings in rural 安徽 Anhui province, a scholarship student who trained as a metallurgical chemist and specialized in the electrochemistry of batteries. In the early 1990s he was studying a market gap that most people missed: Japanese giants were quietly exiting the low-end nickel-cadmium battery business, judging it dirty and unglamorous, just as China's mobile-phone boom was creating insatiable demand for cheap rechargeable cells.3 Wang saw a door swinging open. In February 1995 he founded BYD in Shenzhen with capital of RMB 2.5 million, seeded by a loan from his cousin, 吕向阳 Lu Xiangyang, who was then working in financial services.3

What Wang did next is the founding legend of the company, and it matters because it explains everything that came after. A fully automated Japanese battery line cost millions of dollars — money BYD did not have. So Wang tore the problem apart. He broke each step of battery manufacturing down into discrete manual tasks, then hired hundreds of low-wage workers and equipped them with specialized jigs and fixtures to do by hand what a robotic arm would do in Osaka. This "human robots" approach let BYD build a competitive cell for a fraction of the capital outlay. It was labor-intensive where rivals were capital-intensive — and in a low-wage economy, that was a devastating cost advantage.

Notice what this reveals about Wang's temperament, because it is the through-line of the whole company. He did not accept the industry's cost structure as a given. He decomposed it, found the assumption that made it expensive — that batteries must be built by machines — and attacked that assumption directly. Decades later he would do the same thing to the assumption that a battery must be built from modules, and to the assumption that an electric car must cost more than a gasoline one. BYD's culture is, at bottom, a culture of refusing to accept that a cost is fixed. It is worth naming this early because it is the closest thing BYD has to a repeatable, non-copyable asset: not any single patent, but an institutional habit of vertical, first-principles cost reduction.

It worked spectacularly. Through the late 1990s BYD undercut the Japanese incumbents and won supply contracts with Motorola, Nokia, and Ericsson, climbing to become one of the largest mobile-battery makers on the planet across both nickel-cadmium and lithium-ion chemistries.3 The company rode the explosion of China's 山寨 shanzhai phone ecosystem — the freewheeling, fast-copying handset industry of 深圳 Shenzhen — supplying the cells and, increasingly, the assembly for a torrent of devices. In 2002 the company listed in Hong Kong, raising roughly HK$1.65 billion.3 For most founders, that would have been the whole story: a cash-generative components supplier with a defensible cost position. Here is where BYD stops resembling a normal company.

Wang looked at his own success and saw a ceiling. A mobile battery is a commodity — small, finite, and destined for margin compression. He reasoned that the natural end-state for battery technology was not the phone in your pocket but the car in your driveway. The trouble was that in China, you could not simply decide to build cars. You needed one of a tightly rationed set of state-issued production licenses. So in January 2003, Wang went out and bought a license the hard way: BYD acquired a 77% stake in a failing state-owned automaker, 秦川汽车 Qinchuan Automobile, for HK$269 million (about $33 million), inheriting a dilapidated factory in 西安 Xi'an along with the coveted permit.3

Hong Kong's institutional investors were horrified. BYD was a battery company with zero automotive experience buying a money-losing carmaker in an industry dominated by global giants. On the news, the stock cratered — sinking roughly 30% as fund managers dumped shares and analysts described the move in near-suicidal terms.3 From the outside it looked like a chemist's vanity project. From Wang's chair, it was the cheapest possible entry ticket to what he correctly judged would be the largest consumer shift of the 21st century: the electrification of the automobile.

The logic, once you sit inside it, is more coherent than the panic suggested. Wang understood that the value of battery technology would be realized not in the small, low-margin cell but in the large, high-value system — and the largest battery system a consumer would ever buy is the one under the floor of a car. Selling cells to carmakers would forever leave BYD as a price-taking supplier at the mercy of its customers. Owning the car meant owning the destination for its own most important product. The Qinchuan license was the only legal on-ramp, and it was going cheap precisely because everyone else thought the asset was worthless. That is a pattern worth marking: Wang has repeatedly paid low prices for assets the consensus dismissed — a bankrupt carmaker in 2003, an out-of-favor battery chemistry in the 2010s, a contract-manufacturing business at a distressed multiple in 2023.

The market hated it. That tension — between a founder's long-horizon conviction and the capital market's short-horizon fear — is a theme that recurs throughout BYD's history, and it's worth holding onto as we watch a far more famous investor arrive on the scene, one temperamentally built to buy exactly what the crowd is fleeing.

III. The Berkshire Spark & The First Hybrid Vision (2003–2019)

BYD's first problem as a carmaker was that it did not know how to make cars. Its solution was pure BYD: buy a Toyota Corolla, take it apart, and learn. The resulting BYD F3, launched in the mid-2000s, was an unabashed reverse-engineering of the world's best-selling sedan — cheap, reliable, and unpretentious, down to a silhouette that made double-takes on the street. It sold well precisely because it was familiar, and the cash it threw off quietly funded the electric-vehicle research that was the whole point of the Qinchuan gamble. The F3 was not the mission; it was the war chest.

There's a lesson in that sequencing that separates BYD from the many EV startups that flamed out over the following two decades. BYD did not begin by selling investors a vision of an all-electric future and burning venture capital to chase it. It began by building a boring, profitable gasoline car for real customers, and used those profits to self-fund the moonshot. The electric ambition was patient and cash-backed rather than promissory. When the shakeout of Chinese EV startups came in the 2020s — dozens of subsidy-chasing brands collapsing — BYD survived precisely because its EV program had always been financed by an operating business, not by the kindness of capital markets.

Then came the phone call that put BYD on the global map. In 2008, at the urging of Charlie Munger, Berkshire Hathaway's MidAmerican Energy subsidiary invested $230 million for roughly 225 million shares — about a 10% stake.4 Warren Buffett was skeptical; he did not know the company and generally avoided technology and China. Munger was immovable. He described Wang Chuanfu as "a combination of Thomas Edison and Jack Welch" — Edison for the relentless engineering problem-solving, Welch for the operational drive — and later said he had never helped do anything at Berkshire "that was as good as BYD."4 It was one of the great endorsements in modern investing, and it conferred on an obscure Shenzhen carmaker the imprimatur of Omaha.

To appreciate the size of Munger's call, sit with the eventual arithmetic. That $230 million stake was worth roughly $9.5 billion at its 2022 peak — a return of more than forty-fold on paper, and the single best investment, by Munger's own account, that he ever helped Berkshire make.4 It is the kind of outcome that in retrospect looks obvious and at the time looked reckless: a US insurance-and-utility conglomerate buying a tenth of an unprofitable Chinese battery-and-car company most Western investors had never heard of. Munger's edge was not information; it was the temperament to buy quality that the crowd found unfamiliar and to hold it through a decade in which, for long stretches, the thesis appeared to be failing.

The same year, BYD delivered a genuine world-first: the F3DM, the first mass-produced plug-in hybrid electric vehicle to reach market, beating General Motors' Chevrolet Volt to the punch. On paper, BYD was years ahead of Detroit. In practice, the F3DM barely sold. And this is the part of the BYD story that hagiographies skip: the decade that followed was not a triumphant march but a long, grinding slog. The charging infrastructure didn't exist. Electric cars were too expensive for the customers BYD served. The technology promise kept outrunning the market's readiness to pay for it. The Berkshire stake, so celebrated in hindsight, spent years underwater or flat; conviction was rewarded only much later, and only for those who could stomach the wait.

BYD survived this "lost decade" the way it always had — on cash from unglamorous businesses. Its consumer-electronics assembly arm kept generating steady cash. Municipal contracts for the K9 electric bus gave it a foothold in electrified transport where economics were driven by government fleets rather than fickle retail buyers — and, tellingly, put BYD electric buses on the streets of London, Los Angeles, and dozens of other cities long before its passenger cars went global, quietly building the manufacturing and cell-supply muscle it would later need. And, crucially, BYD leaned on the generous NEV subsidies that Beijing was pouring into the sector as a matter of industrial policy. It's important to be honest about this: for years, BYD was as much a beneficiary of state subsidy as a triumph of the free market, and a skeptical investor in 2016 could reasonably have called it a subsidy-dependent conglomerate with a founder's expensive electric obsession. That skepticism was fair at the time — and it is exactly the kind of claim that later became testable, because the subsidies were eventually phased down, and BYD's competitiveness had to survive their withdrawal. Broadly, it did, which is itself a piece of evidence about how much of the early success was real versus policy-manufactured.

The nadir came in 2018–2019. A wave of battery fires across the Chinese EV industry frightened regulators and consumers, and much of the industry responded by shifting toward higher-energy-density ternary (nickel-manganese-cobalt, or NMC) chemistries — the batteries that pack more range into less weight. BYD, historically wedded to the safer but less energy-dense lithium-iron-phosphate (LFP) chemistry, suddenly looked technologically behind. Its car sales stagnated, margins compressed, and the narrative curdled. It is worth pausing on how genuinely precarious this was, because it is the moment that most tests the "unstoppable BYD" narrative. Rival 宁德时代 CATL was surging on the strength of exactly the ternary chemistry BYD had underweighted, and for a stretch CATL, not BYD, looked like the winner of China's battery race. The company that had been first to a mass-market plug-in hybrid now looked like it had backed the wrong chemistry and missed the moment. A skeptical investor in 2019 would have had every reason to conclude that BYD's window had closed. What happened next is one of the great comebacks in industrial history — and it hinged on a single, deceptively simple piece of engineering that turned BYD's supposed weakness into the industry's new standard.

IV. The Great Inflection: Blade Battery, DM-i, & The ICE Demise (2020–2022)

To understand why BYD came roaring back, you have to understand the trade-off at the heart of every EV battery. Ternary NMC cells store a lot of energy in a small space — great for range — but they are chemically less stable and can enter "thermal runaway," the industry's polite term for catching fire, when punctured or overheated. LFP cells are inherently far more stable and much cheaper, because they use no expensive cobalt or nickel — but they store less energy per kilogram, which historically meant shorter range or a bigger, heavier pack. For years the industry treated this as a hard trade-off: safety and cost, or range. Pick one.

In March 2020, BYD's in-house battery division, 弗迪电池 FinDreams Battery, unveiled its answer: the 磷酸铁锂 Blade Battery. The engineering insight was structural rather than chemical. Instead of packing many short, fat cells into modules and then bolting modules into a pack — a design that wastes enormous space on inactive structure — FinDreams built long, thin, blade-shaped LFP cells that slot directly into the battery pack like books on a shelf, doubling as the pack's structural members. By eliminating the module layer, BYD dramatically improved how much of the pack's volume actually holds energy, closing much of the range gap with NMC while keeping LFP's safety and cost advantages.

Think of it as the difference between shipping wine in individual bottles packed into crates, versus shipping it in long tanks that are themselves the walls of the truck. The old module design wastes space and weight on packaging and internal structure. The Blade design makes the cells do double duty as both container and chassis, so far more of the pack's volume is doing the one thing you actually want — holding energy. That is a manufacturing and packaging innovation as much as a chemistry one, and it is squarely in BYD's wheelhouse of first-principles industrial engineering rather than exotic materials science.

The demonstration that sold it was theatrical and effective. BYD subjected the Blade Battery to the "nail penetration" test — driving a steel nail straight through a charged cell, the industry's most brutal short-circuit torture — and it neither caught fire nor emitted smoke, while comparable ternary cells in the same test ignited, some violently. For a public still nervous about EV fires, the message was visceral: this battery is safe. Just as importantly, LFP chemistry runs roughly 20–30% cheaper than ternary, and it freed BYD from dependence on cobalt supply chains dogged by ethical and geopolitical problems. The chemistry that had made BYD look behind in 2019 became, through structural cleverness, its single greatest weapon — and the wider industry noticed. Over the following years the global battery market swung hard back toward LFP, vindicating a bet BYD had been forced into as much by conviction as by its own cost discipline.

If the Blade Battery fixed BYD's safety and cost story, the DM-i Super Hybrid, launched in 2021, fixed its demand story. Conventional hybrids bolt an electric motor onto a gasoline drivetrain to assist the engine. BYD's Dual Mode intelligent (DM-i) architecture inverted the logic: the car is fundamentally electric-driven, and the small, high-efficiency gasoline engine mostly acts as a generator, charging the battery or feeding the motor, only occasionally driving the wheels directly at highway speeds.3 The result was fuel economy in the neighborhood of 3.8 liters per 100 kilometers — sipping fuel — in a car priced at or below the equivalent gasoline model. That last point is the whole game: DM-i erased the "green premium." A middle-class Chinese family no longer had to pay more to go electric-ish. They could pay the same or less and cut their fuel bill in half.

Why does the generator-first design matter so much for the customer? Because it attacks the two things that keep mainstream buyers away from electrification: range anxiety and price. A DM-i car never needs to be plugged in — it will happily run on gasoline, refueling in three minutes at any station — so there is no infrastructure dependency. But because it drives electrically most of the time, and because the engine runs only in its most efficient band, it sips fuel like a far more expensive hybrid. Crucially, BYD built DM-i around its own cheap LFP cells, its own motors, and its own power electronics, which is how it hit a mainstream price point that Toyota's or Honda's more complex hybrid systems could not touch. Vertical integration is what turned a clever architecture into an affordable product.

That set up the boldest strategic commitment in the modern auto industry. In March 2022, BYD announced it would stop building pure internal-combustion vehicles entirely — the first legacy-scale automaker in the world to do so — converting its whole lineup to battery-electric (BEV) and plug-in hybrid (PHEV) models.3 It was a bet-the-company move made from a position of technological strength rather than regulatory compulsion, and it aligned BYD's entire industrial base behind electrification years before Western rivals were willing to commit. There is a strategic elegance to abandoning the internal-combustion engine that competitors overlooked: BYD no longer had to split its engineering talent, capital, and factory floor between two drivetrains it was trying to phase out. Every yuan of R&D and every hour of assembly time now pointed in one direction. Legacy rivals, by contrast, remained trapped defending profitable gasoline franchises while trying to fund an electric transition — fighting a two-front war BYD had simply refused to enter.

The market's verdict was swift: by 2023 BYD's NEV sales passed three million units a year, and the company had become the rare EV maker actually turning a profit.3 The contrast with the graveyard of loss-making EV pure-plays is the whole point — profitability at scale is the proof that the cost architecture works, not just the marketing. The question for the next section is how that translates into money — and whether the economics are as sturdy as the sales charts suggest once the price war is factored in.

V. Core Business Economics: Inside the Chinese NEV Price War

Peel open BYD's income statement and you find not one company but two very different ones bolted together. The larger is the automobile-and-battery business, which generated the overwhelming majority of 2024 revenue — on the order of RMB 617 billion, or about 79% of the group.[^1] This is where the profit and the strategic value live: the cars, the Blade Batteries, the electric drivetrains. The smaller is the mobile-handset components and assembly business — the BYD Electronic arm — which contributed roughly RMB 160 billion, about 21% of revenue.[^1] But that second business earns thin net margins, in the low single digits, because contract electronics assembly is a scale-and-efficiency grind. It is best understood not as a growth engine but as a cash-generative ballast: high volume, low margin, steady, and a useful counterweight when the car business gets turbulent.

This two-headed structure has an underappreciated analytical consequence: BYD's blended, group-level margins understate the economics of the automotive business that actually drives the equity story. When a headline says BYD's net margin looks thin for a company its size, part of that is the low-margin electronics revenue diluting the picture. The disciplined way to analyze BYD is by segment — to look at the automotive-and-battery gross margin on its own, because that is the number that reveals whether the price war is winning or the cost moat is holding. Conflating the two segments is one of the more common mistakes outside observers make about this company.

And turbulent it is. BYD sits atop the Chinese NEV market with a share in the mid-30s percent — the clear leader — but leadership in China in 2024 and 2025 has meant fighting a price war of almost unprecedented ferocity.[^1] Beijing engineered an EV industry with dozens of players and enormous capacity, and the resulting overcapacity has turned the domestic market into a demolition derby. BYD, as the low-cost producer, has repeatedly been the one to fire the opening salvo, cutting prices to pressure weaker rivals — a strategy that grows volume and share but grinds on everyone's margins, including its own.

To grasp the ferocity, picture a market where the government spent a decade subsidizing anyone willing to build electric cars, producing a landscape of dozens of brands and factory capacity far exceeding what China's buyers can absorb. When capacity outruns demand in a commodity-like product, price is the only weapon, and 2023 through 2025 became a running war of price cuts, each one forcing the next. This is the environment in which BYD's ~35% share was won — not in a genteel market, but in a demolition derby the company itself often started, because as the lowest-cost producer it can survive a price at which its rivals bleed.

Its opponents each attack from a different angle, and war-gaming them is instructive. 特斯拉 Tesla competes with high-margin, software-rich pure BEVs and a genuine lead in autonomy and brand, but it has no plug-in hybrid to offer the huge swath of Chinese buyers who want electrification without range anxiety — and in mid-2024, Tesla's China-made sales were falling even as BYD extended its lead.5 吉利汽车 Geely Auto, through its Galaxy line and its Zeekr and Lynk brands, is the most credible domestic challenger, scaling hybrids and BEVs with real engineering depth. 理想汽车 Li Auto has carved out the premium extended-range SUV niche and, notably, does it profitably — a warning that BYD does not own the only viable model. And looming over all of them is 华为 Huawei, whose smart-car software stack, sold to partner automakers, threatens to define the next axis of competition. Each rival is dangerous in its lane; none yet matches BYD's combination of scale and vertical integration across the mass market. But "none yet" is doing real work in that sentence, and the software front is where the "yet" is most exposed.

Why does BYD keep winning the cost fight? It's worth running the business through Hamilton Helmer's 7 Powers framework, because BYD arguably holds three of them at once. The first is scale economies: building three-million-plus cars a year lets BYD spread fixed costs — tooling, R&D, the depreciation on enormous battery plants — across a vast unit base, so its cost per car falls where a subscale rival's does not. The second, and the most distinctive, is process power through extreme vertical integration. BYD makes its own battery cells, electric motors, power electronics, and even automotive-grade microchips through 比亚迪半导体 BYD Semiconductor, and it moves its finished cars on its own ocean-going car carriers.6 When Bloomberg mapped this integration in 2024, the picture that emerged was of a company that has internalized nearly the entire value chain, capturing supplier margins and compressing the time and cost of getting a new model to market.6

A useful way to feel the process-power advantage is to ask what happens when a new model needs a new component. At a conventional automaker, engineering sends a specification to an outside supplier, negotiates a price and a timeline, waits, and integrates whatever comes back — a process measured in quarters, with the supplier keeping a margin. Inside BYD, the cell team, the motor team, the power-electronics team, and the semiconductor team are colleagues down the hall. Iteration is faster, the supplier's margin stays in-house, and the design can be co-optimized across the whole system rather than bolted together from parts each built to a separate spec. Multiply that across every component and every model, and you get both a cost advantage and a speed advantage — BYD ships new models and new technology generations at a cadence that leaves incumbents flat-footed.

The third power is a cornered resource: the Blade Battery's structural patents and BYD's direct stakes in lithium mining assets, which give it privileged access to the raw material and the proprietary pack design that rivals cannot simply copy. The clearest expression of all three working together arrived in May 2024, when BYD launched its fifth-generation DM technology. The specifications were startling: a claimed thermal efficiency of 46.06% for the gasoline engine (a figure at the frontier of what internal combustion can achieve), fuel consumption as low as 2.9 liters per 100 kilometers, and a combined driving range of up to 2,100 kilometers on a single tank and charge.[^8]7 BYD put this technology into the 秦L Qin L and 海豹06 Seal 06 sedans starting at 99,800 yuan — under $14,000.[^8] Sit with that number for a moment. A family sedan that goes 2,100 kilometers between fills and burns under three liters per 100 kilometers, priced below the equivalent gasoline Corolla or Sylphy. For a joint-venture gasoline sedan from Volkswagen, Toyota, or Honda — cars that for thirty years were the aspirational default of China's rising middle class — that price-performance combination is close to unanswerable. The joint ventures that once minted profits for their foreign parents saw their China sales and margins collapse, and several began shuttering plants.

The strategic meaning is stark, and it's worth stating as the analytical conclusion the numbers point to: BYD is not merely winning the EV market, it is dismantling the economics of the gasoline cars that still fund its foreign rivals' global balance sheets. When you kill your competitor's cash cow, you don't just take share in one market — you weaken their ability to fund the fight everywhere. That is the deeper competitive logic of DM-i 5.0. The obvious counter-question, which the bear case will press, is whether BYD can actually make money at 99,800 yuan, or whether it is buying market share with margin it cannot sustain. Both integration and price wars are only half the capital-allocation story — the other half plays out inside the electronics arm.

VI. Capital Allocation Masterclass: BYD Electronic & The Jabil Acquisition

Every great capital allocator has a discipline you can watch in action, and BYD's is countercyclical, price-first acquisition — buy assets the market has soured on, at multiples that build in a margin of safety, and only when they strengthen the wider machine. Nowhere is that discipline cleaner than in a deal that most observers filed under "phones" and moved on from.

It is easy, amid the drama of cars and batteries, to overlook the shrewdest piece of financial engineering BYD has executed in recent years — and it happened in the unglamorous world of phone assembly. The transaction was first announced in September 2023, and in late December 2023 BYD Electronic completed the acquisition of the mobility-electronics manufacturing business of Jabil Inc., the US contract manufacturer, in 成都 Chengdu and 无锡 Wuxi, for roughly $2.2 billion (about RMB 15.8 billion) in cash.8 On its surface it was a bolt-on. Look closer and it's a case study in buying quality cheaply — and in an American manufacturer choosing to sell down its China exposure to a Chinese buyer eager to deepen it, a small vignette of the larger decoupling reshaping global supply chains.

The price is what makes it remarkable. BYD Electronic paid a multiple of roughly 2.96 times EV/EBITDA and around 8.9 times earnings for a profitable, cash-generative business — a rock-bottom valuation at a time when comparable electronics manufacturers such as Foxconn Industrial Internet and 蓝思科技 Lens Technology traded in the range of 8 to 16 times EV/EBITDA. In other words, BYD acquired an established, cash-throwing asset at a fraction of the multiple the market assigned its peers. This is the discipline that separates good capital allocators from empire-builders: BYD used its cash hoard to buy low, not to buy big.

What did the money actually buy, strategically? Two things. First, deeper penetration of the Apple supply chain — Jabil's mobility unit was a supplier into premium smartphones, and folding it into BYD Electronic increased BYD's share of that lucrative, if demanding, ecosystem. Second, and more interesting, it bought specialized precision-casing and metal-forming technology. That capability does not stay trapped in the phone business; BYD can redeploy the same precision manufacturing into high-end automotive interiors, cockpit assemblies, and the housings for the sensors that advanced driver-assistance systems rely on. It is vertical integration by acquisition — buying a competence in one division and cross-pollinating it into the crown-jewel car business.

Step back and the electronics arm tells you something important about how BYD thinks. BYD Electronic was itself spun out and separately listed in Hong Kong back in 2007, and for years it lived in the shadow of Foxconn as a contract manufacturer of casings and assemblies. It was never the glamorous part of the group. But it has served three quiet purposes: it generates steady cash regardless of the car cycle, it keeps BYD embedded in the precision-manufacturing frontier of consumer electronics, and — increasingly — it is being repurposed as an automotive-electronics supplier, building the intelligent cockpits, sensors, and assemblies that BYD's cars now need. The Jabil deal accelerated all three at once. That is capital allocation with a systems view: buy a cheap asset that also strengthens the flywheel elsewhere.

There is a healthy skeptic's footnote here, and an independent platform should say it plainly. Cheap multiples are sometimes cheap for a reason: contract electronics assembly is a low-margin, cyclical, customer-concentrated business, heavily exposed to the fortunes of a small number of smartphone clients and to the broader handset cycle. A single large customer — the Apple supply chain looms large here — going soft, or shifting assembly out of China for its own geopolitical reasons, would hit this business hard. Buying it at 3x EBITDA is only a triumph if the earnings prove durable rather than melting away with the next iPhone refresh cycle. So far the arithmetic has favored BYD, and the deal fits a consistent pattern of counter-cyclical, price-disciplined buying that runs all the way back to the Qinchuan purchase. But the quality of a bargain is only knowable in hindsight, and this one is still being written. From the disciplined deployment of capital at home, the story now turns outward — to the far messier arithmetic of selling Chinese cars into a world that is busy building walls.

VII. Global Chessboard: Tariffs, Localization, & The EM Offensive

For most of its life BYD was a China story. Over the past three years it has become a geopolitical one, and the geopolitics are not friendly. As BYD's exports surged, Western governments moved to protect their domestic industries. The United States and Canada imposed tariffs of 100% on Chinese-made electric vehicles — effectively a wall, not a tariff. And after a lengthy anti-subsidy investigation, the European Union finalized country-specific countervailing duties in October 2024, landing BYD with an additional duty of 17.0%, layered on top of the standard 10% car-import tariff.9 BYD did not accept this quietly; in December 2024 it filed a legal challenge to the EU duties at the European Court of Justice, arguing the anti-subsidy probe was flawed.[^12]

It's worth being precise about why the tariffs exist and what they claim, because it frames the risk. The EU's duties are not blanket protectionism dressed up; they are the outcome of a formal anti-subsidy investigation that concluded Chinese EV makers benefit from state support — cheap financing, subsidized inputs, favorable land — that lets them undercut European rivals. BYD's rate of 17.0% was the lowest of the major Chinese firms named, which the company noted reflected its cooperation with the probe, but it still lands on top of the standard 10% car-import tariff.9 The deeper point for an investor is that this is a structural, policy-level headwind, not a one-off. It can escalate, and it reflects a Western political consensus that a flood of cheap Chinese cars is a strategic threat, not merely a competitive one.

BYD's commercial response to Europe's wall has been characteristically adaptive. Rather than continue pushing pure BEVs into a market where the countervailing duties bite hardest and charging infrastructure lags, BYD tilted its European export mix toward plug-in hybrids, which have generally faced lower duty rates and suit European drivers still wary of range. It's a reminder that BYD's dual BEV-and-PHEV capability isn't just a domestic advantage; it's a tariff-arbitrage and demand-matching tool abroad. The strategy amounts to selling Europe the product the rules and the infrastructure actually favor, rather than the product BYD would prefer to sell — a nimbleness that a single-drivetrain rival simply does not possess.

The deeper play is localization — building cars inside the tariff walls. And here the story is messier and more instructive than the triumphant version usually told. BYD's flagship European plant is in 塞格德 Szeged, Hungary, where the company has been racing to start vehicle production, with output expected to begin around the fourth quarter of 2026.10 But the Hungarian project has attracted scrutiny of its own, including allegations around labor practices that European authorities have probed — a reminder that operating inside the EU means operating under EU norms and politics. Meanwhile, a planned $1 billion plant in 马尼萨 Manisa, Turkey — announced in 2024 to build 150,000 vehicles a year and reach the EU tariff-free via the EU-Turkey customs union — was put on hold in mid-2026. BYD's Stella Li told reporters that rising EU tariffs had undercut the economics of the Turkish site, and that Hungary was now "the number one priority."11 Turkish authorities, which had granted tax incentives, warned they might claw them back.11

This is the honest picture of localization: expensive, slow, politically fraught, and subject to reversal. The Turkish about-face is especially instructive, because it shows the strategy interacting with itself — the very EU tariffs that made a customs-union backdoor attractive also shifted the math toward building directly inside the EU in Hungary, stranding the Turkish plan. Management, to its credit, has been willing to say so publicly rather than pretend the reversal didn't happen; Stella Li openly reframed Hungary as the priority and acknowledged the search for a second European site.11 That candor is worth something when assessing management credibility, but it doesn't erase the underlying reality: BYD's overseas manufacturing ramp is running behind the pace at which the trade walls are rising. It also underscores a genuine risk in the bear case — that the walls close faster than the factories open, temporarily locking the company out of its richest export markets.

Where BYD has moved fastest and met the least resistance is the Global South. In Brazil, it took over Ford's shuttered Camaçari plant in Bahia to anchor a Latin American manufacturing hub. Across Southeast Asia — Thailand above all — the Middle East, and Latin America, BYD has built commanding EV market-share positions in places where Western protectionism does not reach and where Japanese incumbents, having largely skipped the EV transition, have no competitive answer.6 Thailand is the clearest case study: a market Toyota and Honda dominated for generations, where BYD and its Chinese peers have rapidly seized the EV segment, and where BYD is building local assembly to serve the broader ASEAN region. The strategic pattern is consistent — go where the Japanese are strong but complacent, where governments welcome the investment and jobs, and where there is no political appetite to keep cheap electric cars out.

To move all those cars, BYD did something no carmaker had done at this scale: it went to sea. Its first dedicated car carrier, the LNG-powered BYD Explorer No. 1, entered service in January 2024 with capacity for 7,000 vehicles, the first of a planned fleet of roughly eight ro-ro ships intended to lift over a million cars a year.1213 The move was born of necessity as much as strategy — during the post-pandemic export surge, third-party car-carrier freight rates spiked and capacity was scarce, throttling every exporter's ability to reach foreign markets. BYD's response was pure company DNA: if the freight market is a bottleneck and a cost you don't control, internalize it. Owning the ships, like owning the mines and the chip fabs, is the same instinct expressed on the ocean — control the chain, capture the margin, remove the dependency. It is vertical integration extended from the factory floor all the way to the customer's dockside. Whether owning a shipping fleet is a wise use of capital when freight rates eventually normalize is a fair question; it could look brilliant in a tight market and like a stranded, cyclical asset in a loose one. The people who built this control-the-chain instinct into the company, and who must now decide how far to extend it, are the subject of the next section.

VIII. Current Management & Corporate Governance

Walk into BYD's Shenzhen headquarters expecting a typical billionaire-founder's court, and you'd be disappointed. Wang Chuanfu, Chairman and CEO, is famously an engineer first and an executive a distant second. He is reported to spend the majority of his working time — by many accounts 60–70% — on technical research and development rather than on the investor-relations circuit or the Davos speaking tour, and he holds roughly 17% of BYD's total equity, a stake that dominates his personal net worth.3 This is a founder whose incentives are welded to the long-term value of the enterprise, not to the vesting schedule of an option grant. That alignment is one of the most durable features of the BYD story, and it cuts both ways: it means patient, contrarian capital allocation, but also that a single individual's engineering convictions steer an enormous industrial base.

Wang's personal style reinforces the point. He is not a product-launch showman in the Musk mold, nor a globe-trotting dealmaker; colleagues describe an engineer who is happiest on the factory floor or in a battery lab, who lives relatively modestly for a man of his wealth, and whose public appearances tend to be dense with technical detail rather than vision-speak. For an investor, a founder-engineer with this profile is a double-edged asset. On one edge, it produces the genuine, hard-won technological leads — the Blade Battery, DM-i, the in-house chips — that a finance-driven CEO would likely have outsourced. On the other, it concentrates enormous strategic authority in one man's engineering intuition, with the attendant key-person and succession risk that comes with it. There is no obvious second Wang Chuanfu.

Beside him sits his cousin and original backer, Lu Xiangyang, now Vice Chairman, whose personal holdings and stakes through 融捷投资 Youngy Investment represent a substantial ownership position and who has long provided the financial and capital-markets ballast to Wang's engineering zeal.3 The pairing is almost archetypal: the obsessive technologist and the financier cousin who believed in him when a bank would not. The third pillar is 李柯 Stella Li, an Executive Vice President who has been with BYD since 1996, rising from within to run the international expansion — the Americas, government relations, tariff negotiations, and factory site selection. Li is arguably the most important executive at BYD after Wang himself, precisely because the company's next chapter is an overseas one, and overseas is where an engineering-first culture is weakest and diplomacy matters most. It was Li who publicly explained the Turkish pause and named Hungary the priority; she is, in effect, the face BYD presents to the world's governments and regulators.11

The capital-allocation record deserves scrutiny rather than applause, and it rewards the scrutiny. BYD has consistently reinvested a large share of revenue into research and development — RMB 54.2 billion in 2024 alone, up nearly 36%, with cumulative R&D spending exceeding RMB 180 billion — a figure that in several years has approached or exceeded net profit.1 For a company in a capital-intensive, fast-moving industry, plowing R&D spending back at that intensity is a deliberate choice to prioritize long-term technological lead over near-term reported earnings. Management frames this as building the durable technology base — batteries, drivetrains, chips, and now smart-vehicle software — rather than chasing quarterly optics, and the behavior has been consistent enough across cycles to be credible rather than rhetorical. The counter-check an analyst should keep running is whether that spend translates into the software and autonomy capabilities where BYD is behind, or merely reinforces the hardware lead it already holds.

The R&D has funded a multi-brand ladder that lets BYD climb out of the low-margin mass market, where the price war is bloodiest, toward richer segments. The core 王朝 Dynasty and 海洋 Ocean series cover the mainstream. Above them sit 腾势 Denza in the premium tier, 方程豹 Fangchengbao for personalized off-road models, and 仰望 Yangwang at the ultra-luxury top, whose U8 SUV performs headline-grabbing feats like four-motor "tank turns" — pivoting in place — and briefly floating on water. These flourishes are marketing theater, but the strategic intent beneath them is serious: prove that BYD is not condemned to be a cheap-car company, that its technology can command a premium, and that it can build brand equity above the value tier. The premium brands are growing fast off a small base, and their success or failure is a real KPI in miniature — because a BYD that can only win at 99,800 yuan is a very different, and lower-margin, business than one that can also sell a profitable luxury SUV. The perennial risk of a multi-brand sprawl is dilution and confusion; so far the ladder looks coherent, but it bears watching for signs of "diworsification."

The contrast with Western legacy OEMs on incentive alignment is worth drawing sharply, because it is one of the more genuine structural differences in the story. At a Volkswagen or a General Motors, the chief executive is a hired professional manager whose compensation is dominated by salary and option grants that vest over a few years, tuned to metrics a board can measure over that horizon. Their downside is bounded; a bad decade costs them a job, not a fortune. Wang Chuanfu and Lu Xiangyang, by contrast, have the overwhelming majority of their personal wealth locked in BYD equity they cannot casually sell. That aligns them almost perfectly with long-horizon shareholders and helps explain the willingness to spend R&D at levels that depress near-term earnings, or to abandon a profitable gasoline business in one stroke. The flip side of that same coin is the governance concentration: founder-family control this dominant means minority shareholders are, in effect, betting on the judgment and integrity of a small, related group with limited ability to check it.

The governance skeptic's questions are the obvious ones. Concentrated founder control and a web of related-party ownership — the cousin's investment vehicle, family stakes — demand careful reading of disclosures, and heavy R&D capitalization is an accounting area where aggressive judgment can flatter earnings; both deserve ongoing attention rather than blind trust. And the multi-brand sprawl carries the ever-present risk of "diworsification" — spreading engineering and capital across too many nameplates. So far the brands look coherent rather than scattered, and the founder's skin in the game argues against value-destroying vanity. But an independent observer files these under "watch," not "resolved." With the people and their incentives on the table, we can finally stress-test the investment case itself.

IX. Investment Thesis Stress Test: The Bull vs. Bear Case

Every great company invites the same discipline: state plainly why it wins from here, then try to break the case. Let's do both.

The bull case — why BYD wins. The core of it is a cost position that no rival has matched, produced by the marriage of scale and vertical integration described earlier. When you make your own cells, motors, chips, and ships, you capture margin at every link and you control your own destiny on supply and timing. The Blade Battery has moved from house technology toward industry standard, with BYD supplying battery technology into rival automakers — a sign that even competitors concede its cost and safety edge, and a second revenue stream that turns a cost center into a merchant business. And the fifth-generation DM-i hybrid gives BYD a decade-long runway to sell electrified cars to the enormous global population that isn't ready for a pure BEV, either because the charging infrastructure isn't there or because the price still scares them.

Run it through Porter's Five Forces and the structural picture is favorable on most axes. Barriers to entry are formidable: the capital, the integrated know-how, and the scale are nearly impossible to assemble from scratch, as the graveyard of failed EV startups attests. Supplier power is muted because BYD is largely its own supplier — it does not negotiate with a cell maker, it is one. Buyer power, in the fragmented consumer auto market, is diffuse. The threat of substitutes — gasoline cars — is precisely what BYD is busy destroying. The one force that is genuinely hostile is internal rivalry: the Chinese market is a brawl of well-funded competitors, and that rivalry is exactly what turns the price war into a permanent condition rather than a phase. Four of five forces favor BYD; the fifth is where the bear case lives.

The bear case — what breaks it. Four threats stand out, and none is trivial. The first is the geopolitical trap: escalating trade walls could lock BYD out of North America and much of Europe before its local factories are running — and the Turkish stall shows that localization can slip.11 A company whose growth story increasingly depends on exports is uniquely exposed to a world turning protectionist. The second is domestic margin erosion: the Chinese price war is not a passing storm but arguably a structural feature of an overcapacity market, and even the low-cost producer bleeds when it keeps cutting prices to hold share. Watch whether BYD's gross margin can hold; if the price war permanently resets industry economics lower, the whole sector's returns compress.

The third threat is the one that keeps thoughtful bulls up at night: the ADAS and software deficit. BYD is a hardware colossus, but the frontier of the automobile is shifting toward software-defined vehicles and autonomous driving, where the leaders are Tesla, 华为 Huawei, and 小米 Xiaomi. Here is why this is genuinely dangerous rather than a talking point. BYD's moat is a cost-and-manufacturing moat — it is the best in the world at building a physical car cheaply. But if the axis on which cars compete shifts from hardware cost to software experience, then BYD is defending a hill the battle has moved away from. It risks the fate of the contract hardware maker in any tech industry: doing the hard, capital-intensive physical work at commodity margins while a software layer someone else owns captures the value and the customer relationship. BYD's answer is its "Xuanji" smart-vehicle platform and a stated push to put driver-assistance across even its cheapest models, effectively trying to make advanced ADAS a standard feature rather than a premium one. That is a plausible strategy — democratize the software the way it democratized the battery — but it is a race BYD is running from behind, against rivals whose entire DNA is software, and the outcome is unproven. An honest assessment files this as the single most important open question in the whole thesis.

The fourth threat is sovereign and policy risk: BYD operates at the pleasure of Beijing, subject to industrial mandates, the shifting winds of 共同富裕 common prosperity policy, and the reality that state priorities can change. A national champion enjoys tailwinds until the day the state decides the champion should share more of its spoils, or that the ruinous domestic price war is destabilizing an industry Beijing would prefer to see consolidated and profitable. Chinese regulators have already signaled unease about the price war's toll on the sector's health, and a state-directed push toward consolidation could reshape the competitive field in ways no company controls.

An activist short-seller looking at BYD would press on a few specific soft spots beyond the strategic ones. First, working capital and supplier financing: a company growing this fast, squeezing suppliers this hard, warrants close reading of payables, receivables, and any off-balance-sheet supplier-financing arrangements to confirm the cash flow is as clean as the headline suggests. Second, the aggressiveness of R&D capitalization versus expensing, which directly affects reported margins. Third, the sheer complexity — a group spanning cars, batteries, electronics, chips, and shipping, with a separately listed subsidiary and a web of founder-family ownership vehicles, is inherently harder to audit than a pure-play, and complexity is where problems hide. None of these is a smoking gun; all are legitimate items on a diligence list rather than dismissible.

Run it through Helmer's 7 Powers one more time and the verdict is nuanced. BYD clearly holds scale economies, process power, and a cornered resource in batteries. What it conspicuously lacks are the powers that protect software businesses — network economies and switching costs. A BYD owner faces little lock-in; there is no ecosystem trapping them the way an iPhone user is trapped. That absence is exactly why the software question matters so much. Which brings us to the metrics that will tell us, in real time, which case is winning.

X. Epilogue & Key KPIs to Watch

Strip away the noise, and three numbers will tell you more about BYD's trajectory than any headline.

The first is the overseas sales mix — the share of BYD's vehicles sold outside China. This matters because export margins are meaningfully richer than the blood-soaked domestic market, and because the whole localization gamble is a bet that BYD can keep growing abroad faster than the tariff walls rise. In 2024, overseas revenue reached roughly RMB 222 billion and international vehicle sales jumped nearly 72% off a small base.[^1]1 The direction is clearly up; the open question is whether factories in Hungary, Brazil, and elsewhere come online fast enough to sustain it against protectionism. Every point of overseas mix is a point of margin mix and a point of geopolitical resilience.

There is a myth-versus-reality note worth sounding here, because the export story is often told too triumphantly. The reality is that BYD's overseas success is still concentrated in markets — Southeast Asia, Latin America, the Middle East — where it faces no serious protectionism and no serious EV competition from incumbents. The genuinely hard markets, the large and wealthy ones in North America and Europe, are precisely the ones walling it out. So the overseas-mix KPI must be read with a qualitative overlay: growth in Thailand or Brazil is real but comparatively easy; converting a European or a shielded developed market is the actual test of whether BYD can be a global champion rather than a Global South one.

The second is gross margin resilience. BYD has run a group gross margin in the high teens to around 20% — remarkable for a mass-market automaker, and the direct payoff of its cost position. The price war is a continuous assault on that number. If BYD can hold this margin while still cutting prices, it proves the integration moat is real and self-funding — that the company can lower prices faster than its costs and still keep a spread. If the margin erodes materially, it signals that even the low-cost producer cannot escape the gravity of overcapacity, and that market share is being bought rather than earned. This is the single most important financial tell in the entire bear-versus-bull debate, because it is where the cost moat either proves itself in the numbers or fails to. A related read-through is the split between richer overseas margins and thinner domestic ones: as the export mix rises, blended margin should get support even if the China fight stays brutal, so watch the two together rather than in isolation.

The third is the PHEV-versus-BEV mix, in China and abroad. The adoption curve of the DM-i hybrid against pure-electric models is a live readout of BYD's central strategic bet — that the world electrifies through hybrids first and batteries later, giving BYD a bridge product its BEV-only rivals lack. Watch how that mix shifts as charging infrastructure matures and as tariffs tilt the export math. A rising PHEV share signals that BYD's bridge thesis is playing out and that it is monetizing markets Tesla structurally cannot reach; a collapse toward pure BEVs faster than expected would erode one of BYD's most distinctive advantages and pull it into a straight fight on the software-and-battery terrain where rivals are stronger. The mix is, in effect, a real-time referendum on how the global transition actually unfolds — and BYD has positioned itself to win under the messy, gradual scenario rather than the clean, all-at-once one.

A fourth number sits behind all three as a kind of master variable, even if it isn't a headline KPI: the trajectory of BYD's smart-driving and software capability relative to Tesla, Huawei, and Xiaomi. It is the hardest thing to measure from the outside — there is no clean line item for "is our autonomy competitive?" — but it is where the long-term margin structure of the whole company will ultimately be decided. Watch it through proxies: how BYD's assisted-driving features review against rivals, whether it wins or loses the software-defined comparison in the press and among buyers, and whether its premium brands can command a price for intelligence rather than only for hardware.

Berkshire's full exit, with which we began, is the fitting place to end — because it is not obviously a verdict of doubt. Berkshire had been trimming the position for three years, its stake first slipping below the 5% Hong Kong disclosure threshold in mid-2024 before reaching zero in its filings by the autumn of 2025.2[^12]14 It sold as BYD's stock had risen more than twenty-fold and as Berkshire repositioned a legendary but ageing portfolio in the wake of Munger's death; the sale reflected valuation and portfolio discipline as much as any negative view of the business. Reading it as a signal that BYD is doomed would be as lazy as reading Munger's original purchase as proof that it could not fail. The truth is that the company he championed is stronger operationally than it has ever been, and simultaneously more exposed than ever to forces — trade politics, a domestic price war, and a software race — that lie outside its formidable control.

The enduring lesson of BYD is the one Wang Chuanfu has been demonstrating since he replaced Japanese robots with human hands: true process power and deep vertical integration, once they reach escape-velocity scale, are nearly impossible to disrupt on cost. That lesson has a boundary, and naming it is the honest way to close. Cost leadership is a devastating advantage right up until the terms of competition change — until the thing customers pay a premium for shifts from how cheaply the car is built to how intelligently it drives itself. BYD has already survived one such shift, the one from its old chemistry to a new one, by out-engineering the problem. Whether it can repeat that trick on the far less familiar terrain of software and autonomy is the single question on which the next decade turns. BYD is not merely an EV company; it is an industrial-integration machine that has conquered the physics and the economics of the automobile. The open question — the one worth tracking through every quarter of KPIs — is whether it can also win the war for the car's mind.

References

-

BYD scores YoY jump in 2024 annual revenue, net profit — Gasgoo, 2025-03-25 ↩↩↩↩

-

BYD shares fall after Buffett's Berkshire Hathaway exits stake — BusinessGreen, 2025-09-22 ↩↩

-

From Batteries to EV Powerhouse: The BYD Story — CKGSB Knowledge ↩↩↩↩↩↩↩↩↩↩↩

-

Charlie Munger says BYD was his best investment at Berkshire Hathaway — Fortune, 2023-02-16 ↩↩↩

-

Tesla's China-made EV sales fall in June as BYD maintains lead — Reuters, 2024-07-02 ↩

-

How BYD's extreme vertical integration is rewiring the global auto industry — Bloomberg, 2024-03-20 ↩↩↩

-

BYD's new hybrid technology achieves 2.9L/100km fuel consumption — China Daily, 2024-05-29 ↩

-

US electronics maker Jabil to sell China mobility business to BYD Electronic for $2.2 billion — Reuters, 2023-09-26 ↩

-

EU finalizes tariffs on China-made electric vehicles — Reuters, 2024-10-29 ↩↩

-

BYD nears decision on second European plant site — Automotive World, 2026 ↩

-

Chinese carmaker BYD suspends major project in Turkey — AGBI, 2026-06 ↩↩↩↩↩

-

BYD's 1st car carrier goes into service — CnEVPost, 2024-01-11 ↩

-

BYD will operate 7 ro-ro ships to expand NEV exports in coming two years — Global Times, 2024-02 ↩

-

Berkshire Hathaway trims stake in China's BYD to below 5% — Reuters, 2024-07-22 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube