Hon Precision: The Thermal Gatekeeper of the AI Era

I. Introduction: The 1,000-Watt Problem

Picture a chip the size of a dinner plate. Not a silicon sliver you might imagine slipping into a smartphone, but a massive, multi-layered slab of compute—Nvidia's Blackwell GPU, assembled using TSMC's CoWoS advanced packaging technology, containing hundreds of billions of transistors fused together in a feat of engineering that would have seemed like science fiction a decade ago. Now picture trying to test that chip. The moment you power it on and push electrical signals through its pathways, it generates enough heat to rival a small toaster oven. A thousand watts of thermal energy, concentrated into a few hundred square centimeters. If you cannot pull that heat away—precisely, instantly, and uniformly—the chip warps, the solder joints crack, and your thirty-thousand-dollar piece of silicon becomes an expensive paperweight.

This is the problem that Hon Precision solves. And in solving it, this relatively obscure company from Taichung, Taiwan, has positioned itself as arguably the single most critical bottleneck enabler in the entire AI hardware supply chain.

The thesis is deceptively simple: every AI chip that Nvidia designs, every advanced package that TSMC assembles, must pass through a final test before it ships. That test requires a "handler"—a robotic system that picks up the chip, places it onto a test socket, runs electrical diagnostics, and sorts it by quality grade. But when the chip under test generates a thousand watts of heat, the handler is no longer just a robotic arm. It becomes a thermal management system, a precision refrigerator that must maintain the chip at exact temperature targets while simultaneously feeding it test signals at blazing speed. Hon Precision builds these thermal handlers. More specifically, it builds the only thermal handlers in the world capable of managing the heat loads generated by the most advanced AI processors.

The financial profile is staggering for a company most global investors have never heard of. In fiscal year 2024, Hon Precision posted revenue of nearly fourteen billion New Taiwan dollars, up roughly forty-seven percent year over year, with net income exceeding five billion. But 2025 was the breakout year: revenue more than doubled, with first-half net income alone surpassing the entire prior year's total. Net margins hover around forty percent—a figure that would make most semiconductor equipment companies weep with envy. For context, Advantest, the Japanese giant that dominates automated test equipment, operates at net margins around twenty-four percent. Teradyne, its American counterpart, manages roughly seventeen percent. Hon Precision nearly doubles both of them.

How does a company with fewer than five hundred employees, headquartered in a mid-sized Taiwanese city, achieve margins that rival the most profitable software companies on earth? The answer lies in a twenty-five-year journey from humble automation shop to thermal gatekeeper—a story of engineering obsession, strategic positioning, and the kind of timing that only comes when preparation meets an industry inflection point of historic proportions.

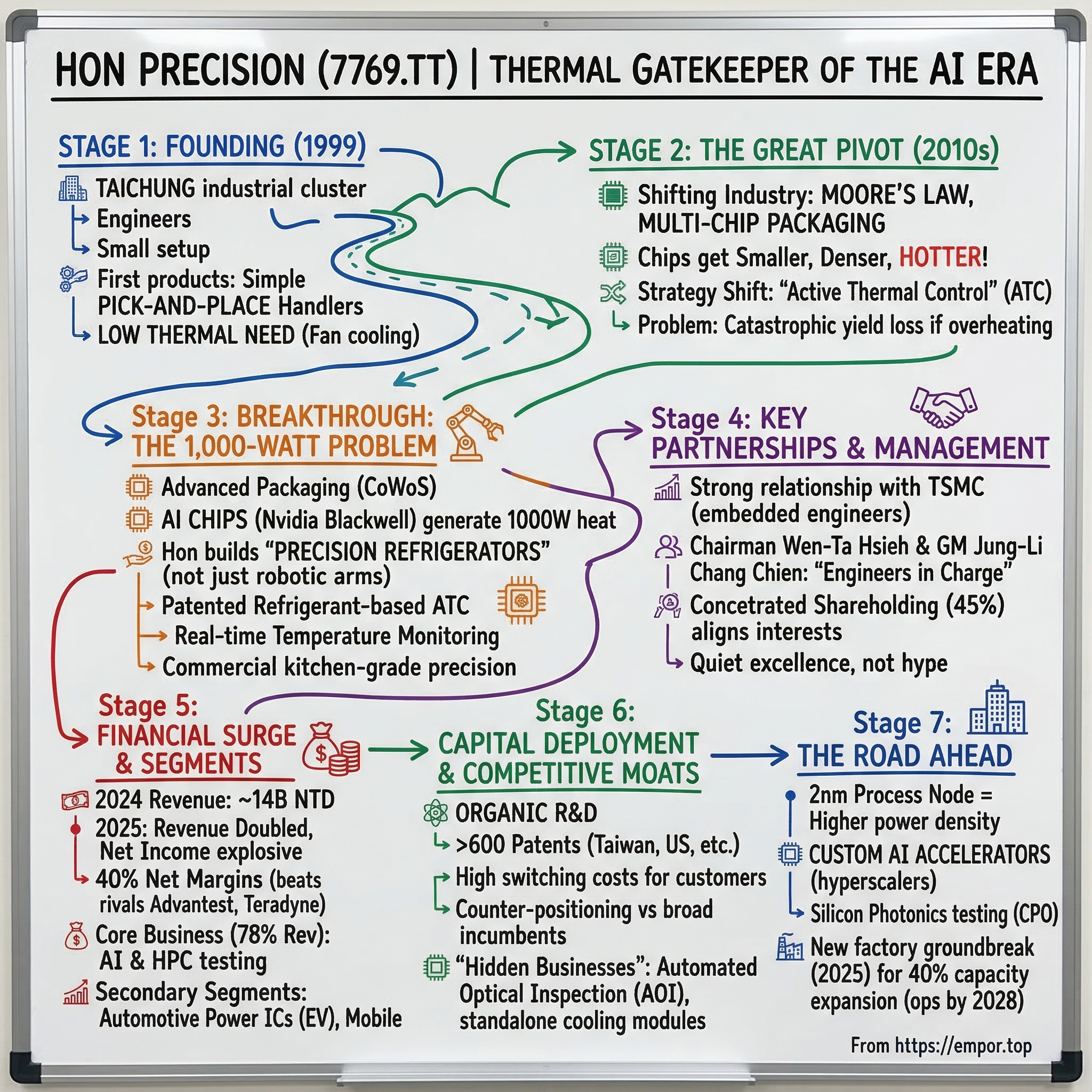

II. Founding and the "Automation" DNA

To understand Hon Precision, you first have to understand Taichung. If Taipei is Taiwan's financial and political capital, and Hsinchu is its semiconductor brain, then Taichung is its industrial backbone—a sprawling metropolitan area in central Taiwan where precision machinery, machine tools, and automation equipment have been manufactured for decades. The city and its surrounding districts host one of the densest clusters of small and mid-sized engineering firms in all of Asia. Walk through the industrial parks of Daya District and you will find shop after shop producing CNC components, robotic arms, pneumatic systems, and custom automation rigs. This is the ecosystem that birthed Hon Precision.

The company traces its operational roots to 1999, when a group of engineers with backgrounds in semiconductor automation equipment decided to strike out on their own. They were not visionaries in the Steve Jobs mold—there was no garage mythology, no grand pronouncement about changing the world. They were craftsmen, deeply fluent in the language of mechanical tolerances, servo motors, and pneumatic actuators, who saw an opportunity in Taiwan's booming electronics industry. The local semiconductor supply chain was expanding rapidly, and every chip fabrication and packaging facility needed equipment to handle, sort, and test the devices rolling off their production lines.

The early years were spent building general-purpose pick-and-place handlers—machines that could grab a chip from a tray, place it onto a test socket, run a diagnostic routine, and sort it into the appropriate output bin. This was bread-and-butter work in the semiconductor backend. The handlers needed to be fast, reliable, and precise, but the thermal requirements were modest. The chips of the early 2000s—mobile phone processors, memory chips, basic microcontrollers—generated manageable amounts of heat during testing. A simple fan or a basic heater plate was sufficient.

What set the founding team apart was not the sophistication of their first products but rather an obsessive commitment to reliability. In the Taichung engineering culture, a machine that breaks down on a customer's production floor is not just a warranty claim—it is a reputational catastrophe. The founding engineers embedded this philosophy into every aspect of their design process: over-engineer the mechanical components, test relentlessly before shipping, and maintain a direct relationship with the customer's production team long after the sale. This culture of "high-reliability first" would prove to be the foundation upon which everything else was built.

Throughout the 2000s, Hon Precision steadily expanded its product line. It moved from basic final-test handlers into system-level test handlers, burn-in ovens, and flash memory test equipment. Each new product category brought the company deeper into the semiconductor backend ecosystem and closer to the major packaging and testing houses that would eventually become its most important customers. The company was not yet a high-growth story—it was a steady, profitable niche player building institutional knowledge about how chips behave under stress.

But something was changing in the semiconductor industry that would transform Hon Precision's trajectory entirely. Chips were getting smaller, denser, and dramatically more powerful. And with that power came heat—lots of it.

III. The Great Pivot: From Mechanical to Thermal

The inflection point arrived gradually, then all at once. Throughout the 2010s, a fundamental shift was underway in semiconductor design. Moore's Law was pushing transistor counts higher while advanced packaging techniques like TSMC's InFO and later CoWoS began stacking multiple chiplets together into single packages. The result was chips that consumed far more power than their predecessors—and consequently generated far more heat during the testing phase.

To appreciate why this matters, consider what happens during a chip's final test. The handler places the device into a test socket and a tester pushes electrical patterns through it at high speed, checking billions of circuit pathways for defects. During this process, the chip heats up—sometimes to temperatures that can damage the device or alter its electrical behavior enough to produce false test results. If the chip gets too hot, you might reject a perfectly good die. If it does not get hot enough, you might pass a defective one. Either outcome is catastrophic for yield, and yield is the lifeblood of semiconductor manufacturing.

For decades, the industry managed this problem with relatively simple thermal solutions. Forced air cooling—essentially blowing cold air onto the chip during testing—worked fine for devices that generated a few dozen watts. Liquid nitrogen systems offered more aggressive cooling but were expensive, difficult to control precisely, and posed safety concerns. Most handler manufacturers treated thermal management as an afterthought, a feature bolted onto an otherwise mechanical system.

Hon Precision's leadership saw the opportunity differently. As chip power levels climbed past a hundred watts and headed toward several hundred, then toward a thousand, the thermal management problem was no longer a feature—it was the product. The company made a strategic decision to pivot its core competency from mechanical handling to what it calls Active Thermal Control, or ATC.

The technical approach was elegant. Rather than using brute-force cooling methods like liquid nitrogen, Hon developed a proprietary refrigerant-based system. Think of it as a miniaturized, highly precise air conditioning unit built directly into the test handler. Each test site—the physical location where a chip sits during testing—gets its own independent temperature control loop. Sensors monitor the chip's temperature in real time, a control algorithm adjusts the refrigerant flow, and the system maintains the target temperature within extremely tight tolerances, even as the chip's power consumption fluctuates during different test patterns.

The analogy that best captures this is a commercial kitchen refrigerator versus a home freezer. A home freezer maintains a roughly constant temperature with simple on-off cycling. A commercial kitchen needs precise, zone-by-zone temperature control—the meat locker at one temperature, the vegetable cooler at another, the blast chiller at yet another—all adjustable in real time as food moves in and out. Hon Precision built the equivalent of that commercial kitchen for chip testing, while competitors were still selling home freezers.

This was not a trivial engineering challenge. The refrigerant-based system required deep expertise in thermodynamics, fluid dynamics, and control systems—disciplines far removed from the mechanical engineering that traditionally defined the handler industry. Hon invested heavily in internal R&D, building up a patent portfolio that now exceeds six hundred patents across Taiwan, the United States, China, South Korea, and Japan. The patents cover not just the cooling hardware but also the control algorithms, the sensor integration, and the system-level architecture that ties everything together.

The breakthrough came when TSMC began ramping its CoWoS advanced packaging for Nvidia's data center GPUs. CoWoS—Chip on Wafer on Substrate—is the packaging technology that enables Nvidia to combine multiple GPU dies, high-bandwidth memory stacks, and interposer layers into a single massive package. These packages are the physical embodiment of the AI revolution, and they generate enormous heat during testing. TSMC and its outsourced assembly and test partners needed handlers that could manage these thermal loads, and Hon Precision's ATC technology was the only solution that met the requirements.

The relationship deepened rapidly. Hon became the preferred handler supplier for CoWoS test lines, embedding its engineers directly alongside TSMC's production teams to co-develop solutions for each new chip generation. In 2025, TSMC recognized Hon Precision with its Supplier Environmental Safety and Hygiene Award—a signal of just how deeply integrated the two companies had become.

This was the pivot that changed everything. Hon Precision was no longer a general-purpose handler manufacturer competing on price and delivery time. It was the thermal gatekeeper—the company whose proprietary technology determined whether the world's most advanced AI chips could be tested at scale. And as Nvidia's GPU roadmap accelerated from H100 to H200 to Blackwell, with each generation pushing power consumption higher, Hon's competitive position only strengthened.

IV. Current Management: The Engineers in Charge

Walk into Hon Precision's headquarters in Daya District and you will not find the trappings of a typical high-flying tech company. There is no gleaming corporate campus, no celebrity CEO giving keynote speeches at industry conferences. What you will find is an engineering-driven organization led by people who prefer to let their machines do the talking.

Chairman Wen-Ta Hsieh—known in international circles as Alan Hsieh—leads the company with a style that reflects the Taichung industrial culture that produced it. Hsieh is not the original founder but rather the leader who navigated Hon Precision through its most transformative period: the transition from a private automation shop to a publicly traded company and the explosive growth driven by AI demand. His background is rooted in the precision machinery industry, and colleagues describe his management philosophy as deeply technical—he cares about engineering specifications and customer relationships, not investor presentations and media appearances.

General Manager Jung-Li Chang Chien complements Hsieh's leadership with operational expertise in scaling production. The challenge of the past two years has been enormous: demand for Hon's thermal handlers has surged so rapidly that the company's production capacity has been the binding constraint on its growth. Managing that ramp—hiring and training engineers, qualifying new suppliers, expanding cleanroom space—while maintaining the quality standards that earned the company its reputation has required careful operational execution.

Vice President and company spokesman Colin Weng serves as Hon Precision's primary interface with the investment community and media. His public statements have been characterized by a careful restraint—acknowledging the strength of demand while consistently emphasizing that the company's capacity remains fully booked. In October 2025, Weng told reporters that "customers' demand still outpaces our capacity," with equipment delivery lead times stretching to four to five months and production fully booked for the next two quarters.

The shareholding structure tells an important story about alignment and control. The company's top five shareholders—Hung Min Development, Hongji Investment, Hong Yu Development, Hong Cheng Investment, and Hong Jun Co.—all share the "Hong" prefix and collectively hold approximately forty-five percent of outstanding shares. These are widely understood to be family and management-related investment vehicles, creating a concentrated ownership structure that aligns the leadership team's financial interests with long-term equity value creation rather than short-term earnings management.

Chairman Hsieh personally holds roughly 1.8 percent directly, but his effective control through these investment vehicles is substantially larger. This structure is common among Taiwan's most successful industrial companies—a legacy of the island's family-business culture adapted for the public markets. The key advantage is stability: management can invest in multi-year R&D programs and capacity expansions without the quarterly earnings pressure that haunts many Western equipment companies.

The incentive philosophy reflects the broader culture of Taiwan's technology sector. With net margins around forty percent, Hon Precision generates substantial cash flow that funds both reinvestment and employee compensation. The company's high-performance bonus culture—where engineers and production staff share in the upside of strong financial results—has been critical for talent retention in a labor market where TSMC, ASE, and other major players aggressively recruit skilled semiconductor equipment professionals.

What makes this management team distinctive is what they do not do. They do not give forward guidance. They do not host flashy analyst days. They do not announce grand strategic visions. They quietly build machines, ship them to the world's most demanding customers, and let the financial results speak for themselves. In an industry where hype cycles can inflate valuations far beyond fundamentals, this quiet excellence has paradoxically contributed to Hon Precision's premium valuation—investors trust management that under-promises and over-delivers.

V. The "Hidden" Businesses and Segments

The headline number is eye-catching: seventy-eight percent of Hon Precision's revenue now comes from AI and high-performance computing testing. This is the explosive core of the business, driven by Nvidia's GPU ramp, the proliferation of custom AI accelerators from hyperscalers like Google, Amazon, and Microsoft, and the broader buildout of AI infrastructure worldwide. Every H100, every H200, every Blackwell chip that ships to a data center passed through a test handler, and an overwhelming share of those handlers were built by Hon Precision.

But focusing exclusively on the AI segment misses important pieces of the story. The company's business breaks down into several distinct areas, each with its own growth trajectory and strategic significance.

The automotive segment contributes roughly twelve percent of revenue and represents what management views as a crucial diversification hedge. Modern electric vehicles are packed with power management integrated circuits—the chips that regulate voltage, manage battery charging, and control motor drives. These power ICs operate at high voltages and currents, which means they generate significant heat during testing. The same ATC technology that Hon developed for AI chip testing translates directly to automotive power IC testing, giving the company a natural adjacency that does not require entirely new R&D investment. As EV adoption continues to grow globally, this segment provides a revenue floor that is somewhat independent of the AI investment cycle.

The mobile phone segment, which contributed roughly six percent of revenue in the first quarter of 2025, is declining as a share of the business—not because mobile testing is shrinking in absolute terms, but because AI testing is growing so much faster. However, mobile remains strategically important for a reason that points to Hon's future: the next generation of mobile processors, built on two-nanometer process technology, will use wafer-level multi-chip module packaging that dramatically increases power density. These chips will need the same kind of aggressive thermal management during testing that today's AI GPUs require, potentially reigniting growth in the mobile segment.

Perhaps the most intriguing "hidden" business is Hon Precision's work in Automated Optical Inspection, or AOI. The company has developed AI-integrated inspection systems that can detect micron-level defects on semiconductor packages at speeds of a thousand pieces per minute. This is not a separate business line so much as a natural extension of the handler platform—if you are already picking up every chip and placing it for testing, why not inspect it visually at the same time? The AI-driven inspection algorithms learn from millions of images to identify crack patterns, solder defects, and packaging anomalies that human inspectors would miss.

Hon Precision has also begun selling its thermal management technology as standalone subsystems—cooling modules that can be integrated into other companies' testing platforms. This is a subtle but significant strategic move. By licensing or selling its ATC technology as a component, Hon expands its addressable market beyond complete handler systems while simultaneously establishing its thermal technology as an industry standard. It is the classic platform play: become the thermal layer that everyone else builds upon.

The company has publicly identified five technology growth directions: large-package solutions for the ever-growing die sizes of AI processors, high-power ATC thermal technology pushing beyond current kilowatt-class cooling, micro-channel cold plate testing for next-generation cooling architectures, system-level test solutions that go beyond simple pass-fail diagnostics, and co-packaged optics testing for the silicon photonics chips that will connect future data center servers. Each of these directions represents a natural extension of Hon's existing capabilities into adjacent high-value niches.

The geographic revenue split is also worth noting. The United States contributed approximately fifty-two percent of first-half 2025 revenue—a reflection of Nvidia's dominance as the primary end customer. The company maintains a subsidiary in Austin, Texas, along with operations in Suzhou, China, and Berlin, Germany, plus agent and distributor relationships across Japan, Korea, Southeast Asia, Israel, India, and Vietnam. This global footprint ensures that wherever advanced chip testing happens, Hon Precision can provide local support.

VI. Capital Deployment and Benchmarking

In the semiconductor equipment industry, the default growth playbook is acquisition. Advantest bought Salland Engineering for its memory test capabilities. Teradyne acquired Universal Robots to diversify into industrial automation. Cohu purchased Xcerra to consolidate the mid-range handler market. The logic is straightforward: buy technology and market access rather than building it internally, then extract synergies by cutting overhead and cross-selling.

Hon Precision has taken the opposite approach, and the results speak for themselves. The company has grown almost entirely through organic R&D investment, plowing profits back into its core thermal management technology rather than acquiring competitors or adjacent businesses. Its patent portfolio of more than six hundred patents was built internally, not purchased. Its ATC technology was developed by its own engineers, not licensed from a university or acquired from a startup.

This organic growth model has several powerful advantages. First, it preserves the company's engineering culture. Acquisitions inevitably bring culture clashes, integration distractions, and the risk of losing the very talent that made the acquired company valuable. Hon Precision's deep technical expertise is concentrated in a relatively small team of fewer than five hundred employees, all of whom share the same institutional knowledge and engineering philosophy. That cohesion is extraordinarily difficult to maintain through acquisition-driven growth.

Second, organic growth produces superior margins. When a company acquires a competitor, it typically pays a premium that must be amortized over years, creating goodwill charges and integration costs that weigh on profitability. Hon Precision's balance sheet is unburdened by acquisition-related overhead, which is a significant contributor to its industry-leading margins. The net margin comparison is stark: Hon at roughly forty percent versus Advantest at twenty-four percent versus Teradyne at seventeen percent. Part of this gap reflects Hon's pure-play positioning in the highest-value segment of the test flow, but part of it reflects the inherent efficiency of organic growth.

Third, the organic model creates a tighter feedback loop between R&D investment and commercial results. When Hon's engineers develop a new iteration of the ATC system—version 5.1, version 5.3, and so on—they are responding directly to technical challenges encountered on customer production floors. There is no lag between identifying a problem and deploying a solution, no committee of acquired-company executives debating product roadmap priorities.

The company's capital deployment in 2025 and 2026 has focused on capacity expansion. In October 2025, management announced plans to increase production capacity by roughly forty percent, breaking ground on a new factory in Taiwan with operations expected to begin in 2028. Quarterly handler shipments are projected to increase from five hundred fifty to seven hundred fifty units. This expansion is being funded from operating cash flow—a testament to the business's cash-generative economics.

The capacity expansion also reveals management's confidence in the durability of demand. A new factory takes years to build and equip, meaning the capital committed today is a bet on AI testing demand persisting through the end of the decade. Given that Nvidia's GPU roadmap extends through Rubin and beyond, and that every major hyperscaler is developing custom AI accelerators that will require similar testing capabilities, this bet appears well-founded.

On the public markets side, Hon Precision's listing journey has been characteristically methodical. The company initially traded on the Taipei Exchange Emerging Stock Board—Taiwan's equivalent of an over-the-counter market for smaller companies. By October 2025, it had become the most expensive stock on that board, trading at around 2,235 New Taiwan dollars per share. In July 2025, the company submitted its application for transfer listing to the main Taiwan Stock Exchange, and by early 2026, shares were trading on the TWSE at approximately 4,160 New Taiwan dollars—nearly doubling from the Emerging Board price in just a few months. The listing upgrade has brought increased institutional investor attention and liquidity, further validating the company's transition from niche industrial player to recognized semiconductor equipment leader.

VII. The Playbook: Hamilton's 7 Powers

Hamilton Helmer's framework for durable competitive advantage identifies seven sources of strategic power that enable a business to sustain above-average returns over time. Hon Precision exhibits at least three of these powers in compelling fashion, and understanding them is essential for evaluating whether the company's extraordinary margins and growth trajectory are sustainable.

Cornered Resource is the most obvious power at work. Hon Precision's proprietary Active Thermal Control technology represents a cornered resource in the purest sense—it is a capability that competitors cannot replicate quickly, regardless of how much money they spend. The physics of managing a thousand watts of heat dissipation from a chip under test, while maintaining temperature uniformity within tight tolerances across multiple test sites simultaneously, is not something you solve by throwing engineers at the problem for six months. It required over two decades of iterative development, hundreds of patents, and deep collaboration with the specific customers whose chips defined the thermal envelope. A competitor starting from scratch today would need years—likely a full decade—to develop equivalent technology, qualify it with TSMC and Nvidia, and establish the production track record that earns a spot on advanced packaging test lines.

Switching Costs represent the second major power. Once Hon Precision's handlers are designed into a TSMC CoWoS test line, the cost of switching to a different handler supplier is not merely financial—it is existential. A test line for advanced AI chips represents billions of dollars in capital equipment. Changing the handler requires requalifying every test program, revalidating yield correlations, retraining operators, and accepting the risk of yield loss during the transition. For a chip that sells for thirty thousand dollars, even a fraction of a percent yield loss during a handler transition translates into hundreds of millions of dollars in lost revenue. No rational production manager would accept that risk unless the incumbent handler supplier fundamentally failed to perform.

The switching costs are further amplified by the tight integration between Hon's handlers and the specific thermal profiles of each chip generation. When Nvidia moves from one GPU architecture to the next, Hon's engineering team works alongside the customer months before production begins, developing the specific thermal recipe for that chip. This co-development process creates deep institutional knowledge that is specific to the customer relationship, making switching not just expensive but practically impossible on any reasonable timeline.

Counter-Positioning is the third power that explains Hon's competitive success. The legacy automated test equipment giants—Advantest and Teradyne—are broad-based companies serving the entire semiconductor testing ecosystem. They sell testers, handlers, and software to every segment of the chip industry, from commodity memory to analog to digital logic. Their business models are optimized for breadth: large sales forces, global service networks, and product portfolios that span dozens of chip categories.

Hon Precision counter-positioned against these incumbents by focusing exclusively on the thermal management bottleneck in the highest-power, highest-value segment of the test flow. This is the classic counter-positioning dynamic: the incumbents could theoretically develop competing thermal handler technology, but doing so would require them to cannibalize their existing handler businesses, reallocate R&D resources away from profitable product lines, and adopt a fundamentally different go-to-market approach. The incumbents' rational response is to continue serving their broad customer base while conceding the thermal handler niche to Hon—exactly as has happened.

Beyond Helmer's framework, Hon Precision also benefits from what might be called process power—the accumulated know-how embedded in its production processes that enables it to build thermal handlers with higher quality and lower cost than a new entrant could achieve. This is distinct from the ATC technology itself; it is the institutional knowledge of how to manufacture, calibrate, and service these systems at scale. It lives in the hands and minds of the production team, not in patent filings, making it even harder to replicate.

VIII. Analysis: Porter's Five Forces

Examining Hon Precision through Michael Porter's competitive framework reveals a company operating in an unusually favorable industry structure—one that explains both its extraordinary margins and the durability of its competitive position.

Threat of New Entrants: Very Low. The barriers to entering the high-power thermal handler market are formidable on multiple dimensions. The technical barrier alone—developing refrigerant-based ATC technology capable of managing kilowatt-class heat loads with precision—would require years of R&D and hundreds of millions of dollars in investment. But the technical challenge is only the beginning. A new entrant would then need to qualify its equipment with TSMC, Nvidia, and the major outsourced assembly and test companies—a process that typically requires years of field trials, yield correlation studies, and production validation. During this qualification period, the entrant would generate zero revenue while burning cash on R&D and customer engagement. The incumbency advantage is profound: TSMC and its partners are not going to risk their most valuable production lines on unproven equipment from an unknown supplier.

Bargaining Power of Suppliers: Moderate. Hon Precision sources components—compressors, sensors, servo motors, control electronics—from a variety of industrial suppliers. None of these individual components are proprietary to the point of creating supplier lock-in. The value creation happens in Hon's system integration and control algorithms, not in any single purchased component. This gives the company reasonable negotiating leverage with its supply base.

Bargaining Power of Buyers: Moderate with an Asymmetric Twist. On paper, Hon Precision's customer base is concentrated—TSMC, ASE Technology, and a handful of other major packaging and test houses represent the bulk of revenue. These are enormous companies with significant purchasing power. However, the asymmetry lies in the fact that Hon's handlers are mission-critical equipment for which no substitute exists at the required performance level. When Nvidia needs to ship a billion dollars' worth of Blackwell GPUs in a quarter, the test handler is not a line item where the procurement team haggles for a five percent discount. It is an enabling technology without which those GPUs cannot ship at all. This shifts the bargaining dynamic decisively in Hon's favor, enabling the premium pricing that sustains forty percent net margins.

Threat of Substitutes: Low. The primary substitute for Hon's thermal handlers would be a fundamentally different approach to chip testing—one that does not require physical contact between the chip and a handler. While there is academic research into contactless testing methods and wafer-level testing that might reduce the need for final test, these approaches remain years away from commercial viability for the most advanced AI chips. The trend toward larger, hotter, and more complex packages actually increases the need for sophisticated thermal handlers rather than reducing it.

Competitive Rivalry: Low in the Niche. Within the specific market for high-power thermal test handlers, Hon Precision has effectively created what can be described as a "monopoly of one." There is competitive activity in the broader handler market—Advantest, Cohu, TechWing, and Changchuan Technology all sell handlers for various semiconductor testing applications. But in the specific niche of kilowatt-class thermal management for advanced packaging test, Hon Precision has no direct competitor operating at the same scale and performance level. This is not a market where five companies battle for share by cutting prices; it is a market where one company has defined the category and set the performance standard.

The combined effect of these five forces is a competitive environment that is almost uniquely favorable. Low entry barriers would attract competition and compress margins; moderate buyer power might limit pricing; substitute threats might reduce demand. Instead, Hon Precision faces high entry barriers, limited substitute risk, and buyers who need its products more than it needs any individual buyer. This structural advantage is the foundation of margins that seem almost too good to be true—but are, in fact, the logical outcome of the company's competitive position.

IX. The Bull vs. Bear Case

The Bull Case: Structural Growth Beyond the Current Cycle

The most compelling bull argument for Hon Precision rests not on the current AI GPU cycle—which is already priced into the stock—but on the structural trend toward higher power density in semiconductors that extends far beyond today's products.

Consider the roadmap. Nvidia's current Blackwell architecture already pushes chip power to kilowatt levels during testing. The successor architectures—Rubin and whatever follows—will push even higher. But Nvidia is just the beginning. Every major hyperscaler is developing custom AI accelerators: Google's TPU, Amazon's Trainium, Microsoft's Maia, Meta's MTIA. Each of these chips requires advanced packaging and each requires thermal handlers capable of managing extreme heat during testing. The addressable market for Hon's technology is expanding not because more of the same chips are being built, but because more types of chips are crossing the thermal threshold where Hon's ATC technology becomes essential.

The two-nanometer process node transition amplifies this trend. As chip features shrink to two nanometers, power density increases even if total power consumption stays flat—the same wattage concentrated into a smaller area creates a more intense thermal challenge. Mobile phone processors built on two-nanometer technology with multi-chip module packaging will, for the first time, require the kind of aggressive thermal management during testing that was previously limited to data center GPUs. This means Hon's addressable market could expand from a few thousand high-end AI chips to tens of millions of mobile processors—a step-change in volume.

The capacity expansion announced in October 2025—a new factory expected to begin operations in 2028 with a forty percent increase in quarterly shipment capacity—positions the company to capture this growth. Order visibility already extends six months, with production fully booked through mid-2026 as of the most recent disclosures. The backlog provides unusual revenue visibility for a capital equipment company.

The co-packaged optics opportunity adds another dimension. As data centers push toward higher bandwidth interconnects, silicon photonics chips that combine optical and electronic functions are emerging as a critical technology. These chips present unique thermal challenges during testing, and Hon has identified CPO-related testing as one of its five strategic growth directions.

The Bear Case: Concentration, Cyclicality, and Customer Dependency

The bear case is equally straightforward and deserves sober consideration. Hon Precision is, at its core, a company tethered to the AI semiconductor capital expenditure cycle. Seventy-eight percent of revenue comes from AI and HPC testing, with Nvidia's supply chain representing the dominant share. If the AI infrastructure buildout slows—whether due to a macroeconomic downturn, a reassessment of AI's near-term return on investment, or a shift in hyperscaler spending priorities—Hon Precision's revenue would decline sharply. There is no diversification buffer large enough to offset a meaningful contraction in AI chip testing demand.

Customer concentration compounds this risk. While Hon Precision serves the broad semiconductor backend, its growth is overwhelmingly driven by a small number of relationships—TSMC's advanced packaging lines and the chip designers whose products flow through them. Any disruption to these relationships—whether from geopolitical tensions affecting Taiwan's semiconductor industry, a shift in TSMC's packaging technology strategy, or a new entrant developing competitive thermal handler technology—could have outsized impact on Hon's financial performance.

The valuation reflects perfection. Trading at approximately 4,160 New Taiwan dollars per share as of March 2026, after nearly doubling from its Emerging Board price in just a few months, the stock carries expectations of continued hypergrowth and sustained forty percent margins. Any miss—a quarter of slower-than-expected shipments, a yield issue that delays a new chip's test qualification, or even a shift in market sentiment toward AI-related stocks—could trigger significant multiple compression.

There is also the question of whether the competitive moat is as impregnable as it appears. While Hon Precision's ATC technology has a decade-plus head start, the semiconductor equipment industry has a history of technical leapfrogs. Advantest and Teradyne have enormous R&D budgets and deep customer relationships of their own. If the thermal handler market grows large enough—and the bull case argues it will—the incumbents may decide that the opportunity justifies the investment required to compete directly. Changchuan Technology in China, backed by government subsidies and motivated by the imperative to develop a domestic semiconductor equipment ecosystem, represents another potential competitive threat on a longer time horizon.

Finally, there is geopolitical risk that cannot be dismissed. Hon Precision is a Taiwanese company whose primary customer is a Taiwanese foundry manufacturing chips for American designers. Any escalation in cross-strait tensions, export controls, or technology restrictions could disrupt this finely tuned supply chain in ways that are difficult to predict or hedge against.

The KPIs That Matter

For investors tracking Hon Precision's ongoing performance, three metrics deserve particular attention above all others.

First, AI/HPC revenue as a percentage of total revenue tells you whether the company's growth engine is accelerating or decelerating. The move from seventy-three percent to seventy-eight percent in a single quarter during 2025 signaled explosive demand growth in the core segment. Stabilization or decline in this ratio would be an early warning signal.

Second, gross margin trajectory reveals whether Hon is maintaining pricing power as it scales. The move from fifty-five percent to fifty-nine percent gross margin between early 2024 and early 2025 indicated that scaling was actually improving unit economics—the hallmark of a business with genuine competitive advantage. Any compression in gross margins would suggest increasing competition or pricing pressure from customers.

Third, order backlog and delivery lead times serve as the best leading indicator of future revenue. When delivery lead times extend to four or five months and production is fully booked for two quarters, the revenue pipeline is robust. Shortening lead times or unfilled capacity would signal a demand slowdown before it appears in reported revenue.

X. Conclusion and Grading

The story of Hon Precision is, at its heart, a story about what happens when deep engineering expertise collides with an industry inflection point of historic magnitude. For twenty-five years, a team of engineers in Taichung quietly built the world's best thermal management technology for semiconductor testing. For most of that time, it was a respectable but unremarkable niche business—profitable, well-run, but invisible to the broader investment community. Then the AI revolution arrived, and suddenly the ability to manage a thousand watts of heat during chip testing became the gating factor for the entire supply chain.

The parallels to other "hidden infrastructure" companies that became indispensable during technology transitions are instructive. ASML spent decades developing extreme ultraviolet lithography before the industry's shift to sub-7nm manufacturing transformed it from a niche European equipment maker into the most valuable technology company in Europe. Tokyo Electron built its position in semiconductor deposition equipment over decades before the explosion in chip complexity made its technology essential for every leading-edge fab. Hon Precision may be following a similar trajectory—a company whose long-term R&D investment created a capability that only becomes valuable when the industry reaches a specific technological threshold.

The question for investors is whether this moment represents the beginning of a durable competitive position or the peak of a cyclical surge. The structural arguments are compelling: chips will continue to get hotter, advanced packaging will continue to get more complex, and the number of companies and chip types requiring kilowatt-class thermal testing will continue to grow. The organic R&D model, the six-hundred-plus patent portfolio, the deeply embedded customer relationships, and the fifteen-year head start in ATC technology all suggest a moat that will be difficult to breach.

But the risks are real. The customer concentration, the cyclical exposure to AI capital spending, the valuation premium that leaves no margin for error, and the ever-present geopolitical shadow over Taiwan's semiconductor industry all deserve weight in any investment calculus.

What is not in question is the company's significance. In a world where artificial intelligence is reshaping every industry, where trillions of dollars of investment are flowing into AI infrastructure, and where the physical constraints of semiconductor manufacturing are becoming the binding limits on the pace of progress, Hon Precision occupies a unique and critical position. It is the company that keeps the chips cool enough to test, the thermal gatekeeper without which the AI dream—quite literally—burns up.

The next chapter will be written by the two-nanometer transition, by the expansion of custom AI accelerators beyond Nvidia, and by the capacity ramp that management has committed to with the new factory breaking ground. Whether Hon Precision becomes the next great compounder or a cautionary tale about cyclical over-extension will depend on whether the structural thesis proves durable—and on whether a small team of engineers in Taichung can continue to solve thermal problems that no one else in the world can solve.

XI. Appendix and Further Reading

Key Resources for Further Research:

The Taiwan Stock Exchange (TWSE) listing for 7769 contains the company's prospectus and ongoing financial disclosures, including quarterly revenue reports and annual financial statements. The full-year 2025 audited results are expected around late March 2026.

For technical context on the CoWoS advanced packaging bottleneck that drives Hon Precision's growth, TSMC's annual technology symposium presentations provide detailed roadmaps of packaging technology evolution and capacity expansion plans. The interplay between chip design complexity, packaging density, and test requirements is central to understanding Hon's addressable market.

Digitimes, Taiwan's leading semiconductor industry publication, provides regular coverage of Hon Precision's order pipeline, capacity expansion plans, and customer relationships. Their October 2025 coverage of the company's AI GPU and ASIC testing equipment ramp offers particularly useful detail on order visibility and production schedules.

For competitive benchmarking, Advantest's annual reports explicitly name Hon Precision as a competitor in the handler segment and provide useful data on the broader automated test equipment market structure. Teradyne's investor presentations offer similar industry context from the American perspective.

SEMI, the global semiconductor equipment industry association, tracks capital equipment spending trends that serve as a proxy for overall demand in the test and handler market. Their annual equipment forecast reports provide the macro context within which Hon Precision's growth should be evaluated.

It is important to note that Hon Precision (鴻勁精密, ticker 7769) is entirely unrelated to Hon Hai Precision Industry (鴻海精密, Foxconn, ticker 2317), despite the similarity in English names. The companies operate in different segments of the electronics supply chain with no corporate affiliation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube