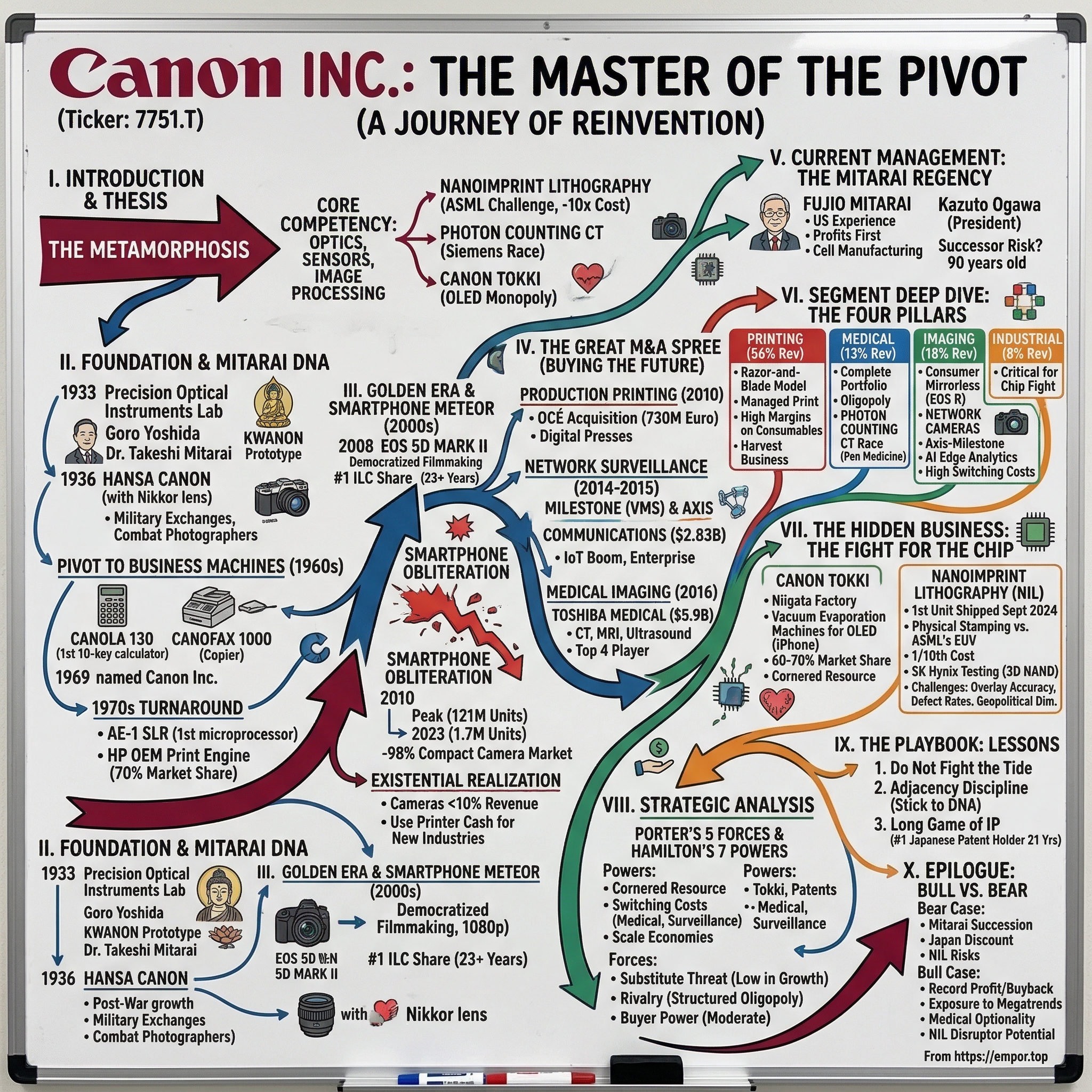

Canon Inc.: The Master of the Pivot

I. Introduction: The "Invisible" Giant

The red logo is everywhere. Slung around the necks of tourists at the Eiffel Tower, mounted on tripods at the Super Bowl sideline, tucked into the camera bags of wedding photographers from São Paulo to Seoul. For most people, Canon means cameras. Maybe printers, if they work in an office. It is a consumer brand so familiar it has become invisible, like wallpaper in a room you stopped noticing years ago.

But here is what most people do not know: Canon is currently locked in a technological arms race against ASML, the Dutch semiconductor equipment monopolist whose machines underpin the entire modern chip industry. Canon's weapon is something called Nanoimprint Lithography, a process that, if it works at scale, could slash the cost of manufacturing advanced semiconductors by a factor of ten. At the same time, Canon's medical division is racing Siemens Healthineers to commercialize Photon Counting CT, a diagnostic imaging technology so precise it can detect cancers that today's machines miss entirely. And tucked away in a factory surrounded by rice paddies in Niigata Prefecture, a Canon subsidiary called Canon Tokki holds a near-monopoly on the vacuum evaporation machines that deposit the organic layers inside every OLED screen on every iPhone shipped worldwide.

This is not your grandfather's camera company.

The thesis of this story is simple but profound: Canon is the ultimate case study in corporate metamorphosis. When the smartphone obliterated the consumer camera market, destroying more than eighty percent of global shipments in under a decade, Canon did not fight the tide. It did not pour billions into a doomed effort to make compact cameras relevant again. Instead, it took the cash still gushing from its printer business and used it to buy its way into entirely new industries, each one anchored by the same core competency that built the original camera business: optics, sensors, and image processing. The result is a company that looks nothing like it did fifteen years ago, yet is unmistakably the same organism, its DNA running through every division like a thread through a tapestry.

The journey from the Kwanon prototype of 1934 to the six-billion-dollar acquisition of Toshiba Medical Systems is a story about patience, reinvention, and the quiet power of compound engineering knowledge. It is also a story about one man, Fujio Mitarai, who spent twenty-three years in the United States learning to think like an American CEO, then returned to Japan and spent the next three decades transforming a camera company into an industrial conglomerate. He is ninety years old now, still serving as Chairman and CEO, and the question of what happens after him is one of the most consequential succession puzzles in Japanese corporate history.

II. Foundation and the Mitarai DNA

In a modest room on the third floor of the Takekawaya Building in Roppongi, Tokyo, a movie camera repairman named Goro Yoshida sat hunched over a disassembled Leica in 1933. He had taken the German camera apart piece by piece, expecting to find some secret, some exotic material or proprietary mechanism that justified its extraordinary price. A Leica cost 420 yen, roughly six months' salary for a Japanese university graduate. Surely there was something inside worth that kind of money.

There was not. Yoshida found brass, aluminum, iron, and rubber. Ordinary materials, assembled with extraordinary precision. "I was surprised that when these inexpensive materials were put together into a camera, it demanded an exorbitant price," he later recalled. The anger and the ambition that moment produced would birth one of the largest technology companies in the world.

Yoshida partnered with his brother-in-law Saburo Uchida and colleague Takeo Maeda to establish the Precision Optical Instruments Laboratory in November 1933. Uchida brought a critical connection: his brother Ryonosuke had been an auditor at Nippon Kogaku, the company that would later become Nikon. That relationship would prove essential when Canon needed lenses for its first commercial camera. The trio's goal was straightforward and audacious: build a Japanese camera that could rival the Leica at a fraction of the price.

Yoshida named his prototype the Kwanon, after Kannon, the Buddhist goddess of mercy. The logo featured the thousand-armed goddess surrounded by flames, and the lens was christened Kasyapa, after one of Buddha's disciples. It was a beautiful piece of engineering and marketing symbolism, though the Kwanon itself never reached commercial production. Yoshida claimed he completed ten units; none were ever verified, and he left the laboratory in the fall of 1934 over disagreements about the company's direction.

The financial backbone came from an unlikely source. Dr. Takeshi Mitarai was a practicing gynecologist who ran the Mitarai Obstetrics and Gynaecology Hospital in Mejiro, Tokyo. He provided capital and organizational structure, eventually abandoning medicine entirely to become president of the company in 1942. In February 1936, the team produced its first commercial product: the Hansa Canon, a rangefinder camera fitted with a Nikkor 50mm f/3.5 lens supplied by Nippon Kogaku. It sold for 275 yen, roughly sixty-five percent of the Leica's price. The company formally incorporated on August 10, 1937, as Precision Optical Industry Co., Ltd., the date Canon still recognizes as its founding.

The post-war years brought a stroke of opportunistic brilliance from Takeshi Mitarai. He persuaded Allied occupation forces to stock Canon cameras in military exchanges and ships' stores. When American servicemen returned home, they carried Canon cameras with them, planting the seeds of brand recognition in the largest consumer market on earth. The Korean War amplified the effect: combat photographers discovered that Canon lenses matched German quality at lower prices, and word spread through the professional community.

But the pivotal transformation came in the 1960s, when Canon made the leap from cameras to business machines. The Canola 130 electronic calculator, introduced in 1964, was the first in the world to feature the ten-key keyboard layout that every calculator and number pad still uses today. Canon entered the copier market in 1965 with the Canofax 1000, directly challenging Xerox's seemingly impregnable monopoly. By 1969, the diversification was so pronounced that the company dropped "Camera" from its name entirely, becoming simply Canon Inc.

The late 1960s and early 1970s were a period of stumbling. Canon had the technology but not the marketing discipline to commercialize it effectively. By 1975, the company failed to pay a dividend for the first time since the war, a humiliation that forced a reckoning. The turnaround came through two innovations that would define Canon's next chapter. First, the Canon AE-1 in 1976, the world's first SLR camera with an embedded microprocessor, which eliminated roughly 300 mechanical parts and slashed manufacturing costs. Backed by television advertising featuring tennis star John Newcombe, the AE-1 sold over 5.7 million units and catapulted Canon past Nikon in Japanese camera sales. Second, and more consequentially for the long term, Canon developed a semiconductor laser beam printer engine that would become the heart of both the first HP LaserJet in 1984 and the first Apple LaserWriter. That OEM print engine relationship with Hewlett-Packard would eventually capture roughly seventy percent of the global laser printer market and generate billions in cumulative profit.

This is the DNA that matters for understanding modern Canon: a company that has always been more than cameras, that built its identity on optical precision but has never been afraid to apply that precision to adjacent markets, from copiers to calculators to laser printers. And the person who would take that DNA and amplify it into a global industrial conglomerate was already being shaped by his experience thousands of miles away.

III. The Golden Era and the Smartphone Meteor

Picture the Canon booth at Photokina 2008, the biennial imaging trade show in Cologne, Germany. The atmosphere is electric. Canon has just unveiled the EOS 5D Mark II, a twenty-one-megapixel full-frame DSLR priced at twenty-seven hundred dollars. It is a photography workhorse, but buried in the spec sheet, almost as an afterthought, is a feature that will accidentally reshape an entire creative industry: 1080p video recording.

Within weeks of its release, Pulitzer Prize-winning photojournalist Vincent Laforet published "Reverie," a short film shot on a pre-production 5D Mark II. The footage went viral. Cinematographers were stunned. The shallow depth of field, the film-like grain, the low-light performance, all from a camera that cost three thousand dollars with a lens, compared to thirty thousand or more for a Red One digital cinema camera and vastly more for a traditional 35mm film setup. Photography forums erupted. The 5D Mark II was used for Saturday Night Live's 35th season opening titles, for a full season of the medical drama House, and for sequences in Iron Man 2 and The Avengers. Canon had stumbled into democratizing filmmaking.

The broader 2000s were Canon's golden age. The company held the number one share of the global interchangeable-lens camera market beginning in 2003, a streak that remarkably continues to this day, now stretching twenty-three consecutive years. The original EOS 5D, launched in September 2005, had already revolutionized professional photography by bringing a full-frame sensor to a price point that Nikon would not match for another two and a half years. The printer business was printing money, quite literally: Canon's OEM laser engines powered the machines in offices around the world, and cumulative toner cartridge production had already surpassed one hundred million units by 1992.

Then the meteor hit.

The iPhone 4 launched in June 2010 with a five-megapixel backside-illuminated sensor that, in good lighting, produced images competitive with budget point-and-shoot cameras. HDR mode arrived that same year. iOS 5 added composition grid lines in 2011. One-button camera access from the lock screen came in 2012. Each iteration was a small cut, but collectively they bled the compact camera market to death.

The numbers are staggering. In 2010, the global camera industry shipped over 120 million units, with compact cameras accounting for roughly 109 million. By 2012, shipments had dropped forty-eight percent from the prior year. In 2013, the industry lost over 35 million units in a single year, the largest annual decline on record. By 2018, total camera shipments had fallen more than eighty percent from their peak. And by 2023, compact camera shipments had collapsed to just 1.7 million units, a decline of over ninety-eight percent from the 2010 high.

The speed of this destruction was breathtaking. Annual declines of twenty to thirty percent became the norm between 2012 and 2015. It was not a gradual erosion; it was a cliff. The smartphone did not just replace the compact camera as a product. It replaced the entire distribution channel. People stopped walking into electronics stores. They stopped thinking of photography as something that required a separate device. The best camera became the one you always had with you, and you always had your phone.

For Canon, the strategic realization was existential but not fatal. Unlike Olympus or Pentax, which were overwhelmingly dependent on camera sales, Canon had diversified decades earlier under the leadership of the Mitarai family. By the mid-1990s, cameras already represented less than ten percent of Canon's total revenue. The copier, printer, and optical equipment businesses provided a massive buffer. But the writing was on the wall: the consumer imaging business that had defined the brand for eighty years was entering permanent structural decline. The question was not whether Canon needed to transform, but how aggressively, and where the money would go.

The answer would arrive in a flurry of acquisitions that remade the company from the inside out.

IV. The Great M&A Spree: Buying the Future

Fujio Mitarai understood something that many Japanese CEOs of his generation did not: a cash cow is only valuable if you milk it before it runs dry. Canon's printing business, still generating roughly fifty-five percent of corporate revenue with fat margins on ink and toner cartridges, was the perfect cash cow. Office printing was not going to disappear overnight the way compact cameras had. But secular decline was inevitable as the world moved toward digital workflows. The strategic imperative was clear: use the printing cash to buy high-barrier-to-entry businesses in markets where Canon's optical and imaging DNA would provide a genuine competitive advantage.

The first major move came not with surveillance or medical, but with production printing. In 2010, Canon acquired Océ, the Dutch production printing specialist, for 730 million euros, a seventy percent premium to the share price at the time of the offer. Océ was not a household name, but in the world of high-speed commercial printing, transactional printing for banks and insurers, and wide-format printing for architects and engineers, it was a dominant force. The acquisition transformed Canon from a company that sold office printers into the operator of what amounted to a digital printing press for the twenty-first century. More importantly, it demonstrated Mitarai's willingness to pay premium prices for businesses with entrenched customer relationships and high switching costs.

The surveillance bet came next. In June 2014, Canon first acquired Milestone Systems, the leading video management software platform. Then in 2015, Canon acquired Axis Communications, the Swedish network video surveillance pioneer, for approximately 2.83 billion dollars at 340 Swedish kronor per share. The price represented roughly twenty-five times EBITDA, a significant premium that raised eyebrows among analysts accustomed to Canon's reputation for financial discipline. Together, the two acquisitions gave Canon the number one position in network video surveillance, combining Axis's best-in-class cameras with Milestone's industry-standard software.

The logic was vintage Mitarai: surveillance cameras are, at their core, imaging devices. The optics, the sensors, the image processing algorithms, all draw from the same engineering pool that built Canon's camera business. But unlike consumer cameras, network video surveillance is a recurring-revenue business with deep enterprise relationships, and it was riding the tailwind of the IoT boom. A hotel chain that installs five thousand Axis cameras across its properties is not ripping them out three years later because a competitor drops its price by ten percent. The switching costs are enormous: the software integration, the training, the physical installation.

The early skepticism about the price proved misplaced. By fiscal year 2024, Canon's network camera business had grown to 357.5 billion yen, up nearly thirteen percent year over year. The surveillance division had become a genuine growth engine, bolstered by the increasing integration of AI-powered video analytics, facial recognition, and automated monitoring systems. What looked expensive at twenty-five times EBITDA in 2015 looked prescient a decade later.

But the largest and most consequential deal was still to come. In March 2016, Canon announced the acquisition of Toshiba Medical Systems for 665.5 billion yen, approximately 5.9 billion dollars. The context was extraordinary. Toshiba was in the middle of the worst corporate scandal in Japanese history, having been caught overstating profits by 1.2 billion dollars over seven years. The company was hemorrhaging cash and desperately needed to sell assets to shore up its balance sheet. Toshiba Medical, which made CT scanners, MRI machines, ultrasound systems, and X-ray equipment, was the crown jewel.

Canon structured the deal in a way that was clever, controversial, and arguably changed the landscape of Japanese M&A. Rather than acquiring Toshiba Medical directly, which would have triggered a lengthy antitrust review and given rival bidders time to intervene, Canon used a special purpose company to warehouse the shares while regulatory approval was pending. Fujifilm, which had been in advanced negotiations to buy Toshiba Medical itself, was furious. Fujifilm's CEO publicly called the maneuver "a mockery of the law." European antitrust authorities agreed, at least in part: the European Commission fined Canon 28 million euros for "gun jumping," completing the acquisition before receiving formal regulatory clearance. The U.S. Department of Justice extracted a separate 2.5 million dollar settlement.

Canon paid the fines and moved on. The strategic prize was worth the regulatory bruises. The acquisition instantly transformed Canon into a global top-four player in diagnostic medical imaging, joining the oligopoly of Siemens Healthineers, GE HealthCare, and Philips. At roughly 2.5 times revenue, the price was rich but not outlandish by the standards of medical device M&A, where barriers to entry are immense, regulatory approval cycles are measured in years, and customer relationships last a decade or more.

The integration has not been without pain. In fiscal year 2024, Canon took a 165.1 billion yen write-down on the medical business, acknowledging that the acquisition had not yet delivered the returns originally projected. This is a material accounting judgment that investors should monitor: the gap between the acquisition price and the business's current carrying value reflects the challenge of integrating a complex medical device operation into a company whose core expertise lay elsewhere. But the strategic logic remains intact: medical imaging is a growing, high-margin, oligopolistic market where Canon's optical engineering expertise provides genuine differentiation.

Taken together, the three major acquisitions, Océ, Axis-Milestone, and Toshiba Medical, represent a corporate transformation of remarkable ambition. Canon spent roughly ten billion dollars in a five-year span to buy its way into three entirely new industries. Each acquisition was expensive by conventional metrics. Each was criticized at the time. And each was driven by the same underlying logic: find businesses where optics, sensors, and image processing are the critical competitive advantage, where switching costs are high, where customer relationships are deep, and where the secular growth trends are favorable.

V. Current Management: The Mitarai Regency

In January 2026, Fujio Mitarai stepped down as president of Canon for the third time. He remains Chairman and CEO. He is ninety years old.

That sentence alone tells you everything you need to know about the concentration of power at Canon. Mitarai has been the dominant figure in the company since 1995, when the board bypassed six more senior executives to install him as president after his cousin, the previous president, died unexpectedly. In the three decades since, Canon's trajectory has been inseparable from Mitarai's vision.

The biographical details are essential for understanding the man. Born in September 1935 in Kamae, a small town on the coast of Kyushu, Mitarai was the nephew of Canon founder Takeshi Mitarai. Unlike his three brothers, who followed the family patriarch into medicine, Fujio studied law at Chuo University and joined Canon in 1961. Five years later, at age thirty, his uncle sent him to Canon's tiny American subsidiary in Manhattan, where he was one of just seven employees.

What Mitarai discovered in those early years in New York would shape his entire management philosophy. His first earnings report revealed that Canon USA had made six thousand dollars in profit on three million in revenue, a margin so thin that the IRS opened an investigation, suspecting transfer pricing manipulation. There was no manipulation. Canon was simply terrible at making money. Mitarai spent years traveling the country, promoting cameras, staying in budget hotels, and learning the American way of doing business.

He rose to become president of Canon USA in 1979 and held the role for a decade. During that period, he brokered the partnership with Hewlett-Packard that put Canon's laser print engines inside the HP LaserJet. He regularly played golf with GE's Jack Welch and absorbed Welch's relentless focus on cash flow, return on equity, and the willingness to exit unprofitable businesses. These were alien concepts in Japanese corporate culture of the 1980s, where market share and revenue growth were the metrics that mattered, and where lifetime employment was sacrosanct.

When Mitarai returned to Japan in 1989, he found a company riddled with underperforming divisions. When he became president in 1995 and CEO in 1997, he moved with a decisiveness that stunned the Japanese business establishment. He killed Canon's PC business, shut down electric typewriters, exited LCD manufacturing, and consolidated the company into four core divisions: copiers, printers, cameras, and optical equipment. He replaced traditional assembly lines with a "cell manufacturing" system in which small groups of workers built entire products from start to finish. A cell of twelve workers could match the output of thirty on a conventional line, saving an estimated 300 million dollars and boosting productivity by thirty percent.

The financial results were dramatic. Within five years, Mitarai tripled Canon's net profits and stock price, even as Japan's broader economy remained mired in stagnation. Net profits reached 1.4 billion dollars by 2002. Canon eliminated borrowing for capital investment entirely, funding all growth from internal cash flow. He declared early in his tenure: "I changed the mindset at Canon by getting people to realize that profits come first." For a Japanese CEO in the 1990s, this was heresy.

The compensation structure at Canon reflects the Japanese corporate tradition more than the Western one. Executive pay is relatively modest by global standards, consisting of base salary plus performance bonus, with none of the stock option windfalls that define Silicon Valley compensation. But Mitarai imposed Western-style financial discipline on the entire organization. The metrics that matter are return on equity, which reached 9.7 percent in fiscal 2025, and dividend growth, which has increased steadily from 140 yen per share to 160 yen. Canon announced a 200-billion-yen share buyback program for fiscal 2026, a signal that Mitarai understands the expectations of his shareholders.

The ownership structure adds an important dynamic. Approximately thirty percent of Canon's shares are held by foreign institutional investors, a significant proportion by Japanese standards and one that creates constant pressure for capital efficiency and shareholder returns. This foreign ownership acts as a counterweight to the traditional Japanese corporate tendency toward empire-building and capital hoarding.

His successor as president, Kazuto Ogawa, is sixty-seven and has served as COO. But Mitarai remains CEO and Chairman, and nobody inside or outside Canon believes the power dynamic has fundamentally shifted. The question every investor asks is the obvious one: what happens when the man who has been the company's strategic compass for thirty years is no longer there? He has built the systems, the culture, and the strategy, but corporate Japan is littered with examples of founder-era greatness that dissipated under successor management. This succession question is not a distant risk. It is a present one, and it hangs over every long-term investment thesis for Canon.

VI. Segment Deep Dive: The Four Pillars

Walk into any mid-sized law firm, insurance company, or hospital administrative office in the developed world, and you will find Canon hardware humming away in a corner: multi-function devices spitting out contracts, scanners digitizing patient records, printers churning through invoices. The Printing segment is not glamorous, but it is the engine that powers everything else Canon does. In fiscal year 2024, Printing generated approximately 2,523 billion yen, representing about fifty-six percent of Canon's total revenue. It is the largest segment by a wide margin and the financial foundation upon which the entire transformation strategy rests.

The business model is the classic razor-and-blade: sell the printer at a modest margin, then capture recurring revenue on ink and toner cartridges for the life of the machine. In office environments, where multifunction devices are leased rather than purchased, the model extends to service contracts and managed print services. The margins on consumables are extraordinary, often exceeding fifty percent, and customer switching costs are high because organizations build their document workflows around a specific vendor's ecosystem.

But this is not just about desktop printers gathering dust in home offices. The Océ acquisition gave Canon a dominant position in production printing: the massive, industrial-speed machines that print bank statements, insurance policies, direct mail campaigns, and book interiors. This is a segment where a single machine can cost hundreds of thousands of dollars and where Canon competes against Ricoh, Konica Minolta, and Xerox. The shift toward digital printing from traditional offset has been a secular tailwind, as shorter print runs and variable data printing favor digital presses over analog ones.

The strategic challenge for Printing is secular volume decline. As organizations digitize workflows, the number of pages printed globally has been falling for years. Canon has responded by pushing into higher-value segments where margins are richer and the competitive moat is deeper. The segment remains highly cash-generative, but it is a harvest business, not a growth business. The cash it produces is what funds the acquisitions and R&D investments in the other three pillars.

The Medical segment tells a different story entirely. At 568.8 billion yen in fiscal 2024, it represents about thirteen percent of revenue, making it the smallest of the four pillars in revenue terms but arguably the most strategically important as a growth driver. The Toshiba Medical acquisition gave Canon a complete portfolio of diagnostic imaging equipment: CT scanners, MRI machines, ultrasound systems, and X-ray equipment. Canon competes in a tight oligopoly with Siemens Healthineers, GE HealthCare, and Philips, a market structure that supports pricing discipline and sustained margins.

The technology frontier in medical imaging is Photon Counting CT, and this is where Canon's optical engineering heritage becomes directly relevant. Traditional CT scanners use energy-integrating detectors that measure the total energy of incoming X-rays. Think of it like pouring all the rain from a storm into a single bucket and then measuring how much water you collected. You know how much rain fell, but you cannot tell anything about individual raindrops. Photon Counting CT, by contrast, uses cadmium zinc telluride detectors that count individual X-ray photons and measure each one's energy level independently. Now you are counting every raindrop and measuring its size. The clinical implications are profound: dramatically higher image resolution, lower radiation doses for patients, and the ability to distinguish between different tissue types and contrast agents in a single scan. For oncologists, this means detecting tumors at earlier stages and monitoring treatment response with greater precision.

Siemens Healthineers holds the lead with its NAEOTOM Alpha, which received FDA approval in 2021 and is already installed at major research hospitals. Canon showcased its own Photon Counting CT system at the Radiological Society of North America conference in late 2025 and has a research collaboration with Penn Medicine. Canon is behind in this race, but the technology is still in its early innings, and Canon's deep expertise in sensor technology gives it a credible path to closing the gap.

The Imaging segment, at roughly 803.5 billion yen or about eighteen percent of revenue, is the one most people associate with the Canon brand. But it has undergone a quiet transformation. Consumer cameras still matter: Canon has dominated the mirrorless camera market with its EOS R system and maintained its twenty-three-year streak atop the interchangeable-lens camera rankings. But the real growth within Imaging comes from network cameras. The Axis and Milestone acquisitions created a surveillance and video analytics business that has grown to 357.5 billion yen, now representing a substantial portion of the overall segment. These are not the grainy CCTV cameras of the 1990s. Modern network cameras are intelligent edge computing devices equipped with AI processors that can identify objects, detect anomalies, count people, read license plates, and trigger automated responses. Once a retail chain, a city government, or an airport installs thousands of cameras running on Milestone's platform, with custom analytics trained on their specific use cases, the switching costs are enormous.

Finally, the Industrial segment. At 356.5 billion yen, roughly eight percent of revenue, it is the smallest pillar. But in strategic importance per revenue dollar, it is arguably the most consequential business Canon operates. This is where the semiconductor lithography equipment lives, and this is where Canon is attempting something that, if successful, could reshape the entire semiconductor industry. But that story deserves its own chapter.

VII. The Hidden Business: The Fight for the Chip

Somewhere in the rice paddies of Niigata Prefecture, far from Tokyo's gleaming corporate towers, sits a factory that the global smartphone industry cannot function without. Canon Tokki, a subsidiary that most investors have never heard of, manufactures the vacuum thermal evaporation machines used to deposit organic materials onto glass substrates to create OLED screens. These are not small machines. They are room-sized pieces of precision equipment, each one costing tens of millions of dollars, and they are essential for producing the displays inside every iPhone, every Samsung Galaxy flagship, and an increasing share of laptop and tablet screens.

The OLED manufacturing process requires depositing layers of organic compounds mere nanometers thick onto glass with extraordinary uniformity. To grasp the precision involved, imagine trying to spread a layer of butter across a football field, and that layer needs to be exactly the same thickness everywhere, down to millionths of a millimeter. Canon Tokki's machines achieve this by heating organic materials in a vacuum chamber until they vaporize, then allowing the vapor to condense onto the substrate in precisely controlled patterns. Variations of even a few nanometers produce dead pixels or color inconsistencies that render a display unusable. Canon Tokki has spent decades refining this process, and its machines hold an estimated sixty to seventy percent share of this roughly two-billion-dollar niche market.

For years, Samsung Display was Canon Tokki's largest customer, and the relationship was so tight that Canon Tokki essentially allocated its entire annual production capacity, sometimes as few as a handful of machines per year, to Samsung. As Apple pushed its suppliers to adopt OLED for the iPhone starting in 2017, the demand expanded to include LG Display, BOE, and other panel makers. The bottleneck was not demand but supply: Canon Tokki simply could not build machines fast enough. This is the kind of cornered resource that competitive strategists dream about. The knowledge embedded in Canon Tokki's engineering team is not something a competitor can replicate by throwing money at the problem. It was built over decades of iterative refinement.

But the bigger story in Canon's industrial segment, the one with the potential to truly move the needle on the company's valuation, is Nanoimprint Lithography.

To understand why this matters, you need to understand how chips are made today. The dominant technology is photolithography, and the undisputed king is ASML, the Dutch company whose Extreme Ultraviolet lithography machines cost upward of 350 million dollars each, weigh 150 tons, require dedicated foundations in the factory floor, and use a process that borders on science fiction: a high-powered laser fires fifty thousand pulses per second at tiny droplets of molten tin, generating plasma that emits extreme ultraviolet light, which is then focused through a series of mirrors polished to atomic-level smoothness to project circuit patterns onto a silicon wafer coated with photosensitive material. It is one of the most complex machines humans have ever built, and ASML has a monopoly on it. Every advanced chip made by TSMC, Samsung, or Intel depends on ASML's EUV machines.

Canon's Nanoimprint Lithography takes a fundamentally different approach. Instead of projecting the pattern with light, NIL physically stamps it. Think of it as the difference between projecting a movie onto a screen using an enormously complex projector versus pressing a rubber stamp directly onto the surface. A master template, or mask, is created with the desired circuit pattern etched into it at nanometer scale. The wafer is coated with a liquid resist material using inkjet printing. The mask is pressed onto the resist, which fills the nanoscale features of the template through capillary action. Ultraviolet light cures the resist, hardening it into the desired pattern. The mask is lifted away, and the pattern remains on the wafer.

The elegance of this approach is its simplicity relative to EUV. There is no need for the tin-droplet plasma system, no need for the extraordinarily expensive multilayer mirrors, no need for the massive vacuum chambers. Canon claims that NIL can achieve comparable resolution to EUV at roughly one-tenth the cost per exposure step. If that claim holds at volume production, the implications for the semiconductor industry are enormous.

Canon shipped its first commercial Nanoimprint Lithography unit in September 2024, a milestone that followed over a decade of development. SK Hynix, the South Korean memory chipmaker, has been testing NIL for 3D NAND flash production, a segment where the technology's strengths in patterning repeating structures at high density are well suited. The early results have been promising enough to sustain industry interest.

But the challenges are real, and they are significant. Overlay accuracy, the ability to align successive pattern layers with nanometer precision, remains roughly four times worse than what EUV achieves. Think of it like trying to perfectly align a rubber stamp over a previous impression: even tiny misalignments compound across dozens of patterning steps. Mask durability is a concern, since physically pressing a template against a resist thousands of times introduces wear that does not exist in optical lithography. Defect rates, caused by particles trapped between the mask and the wafer, remain higher than what leading-edge logic chipmakers will tolerate. And throughput, the number of wafers processed per hour, has not yet matched EUV's production speeds.

No leading-edge logic foundry has committed to NIL for production. The technology's most likely path to commercialization runs through memory chips, where the tolerance for overlay errors is somewhat higher and where the cost savings are most impactful. If Canon can prove NIL's viability in high-volume NAND production, it could then iterate toward the tighter specifications required for logic chips.

The geopolitical dimension adds another layer of significance. ASML's EUV monopoly has become a chokepoint in the global technology supply chain, one that the Dutch government, under pressure from the United States, has used to restrict China's access to advanced chipmaking equipment. A viable alternative to EUV, even one initially limited to memory chips, would alter the strategic calculus for every major semiconductor-producing nation. Canon, as a Japanese company, operates under a different set of export control regimes, and the implications of that difference have not been lost on policymakers in Beijing, Tokyo, or Washington.

VIII. Analysis: Porter's Five Forces and Hamilton's Seven Powers

Canon occupies a fascinating strategic position: dominant in declining markets, a challenger in growing ones, and a dark horse in a potential technological revolution. Applying rigorous competitive frameworks reveals why the company is more strategically interesting than its modest valuation multiple suggests.

Start with Hamilton Helmer's 7 Powers. Canon possesses at least three of the seven powers in meaningful degree. The first is Cornered Resource. Canon Tokki's OLED deposition machines represent a near-textbook case: the accumulated engineering knowledge, the supplier relationships, the decades of process refinement, none of this can be acquired by a competitor through capital expenditure alone. Samsung Display famously waited years for Canon Tokki to fulfill its orders because no alternative existed. Similarly, Canon's library of optical and sensor patents, the company has ranked in the top ten of U.S. patent grants for forty-two consecutive years and was first among Japanese companies for twenty-one straight years, constitutes an intellectual property estate that competitors must design around, adding cost and complexity to their products.

The second power is Switching Costs, and Canon has them in abundance in its two most important growth segments. In medical imaging, switching costs are measured not in dollars but in years. When a hospital installs a Canon CT scanner, it simultaneously trains its radiologists on Canon's proprietary software interface, integrates the machine with its picture archiving and communication system, establishes maintenance contracts, and builds clinical workflows around Canon's specific image reconstruction algorithms. Switching to Siemens or GE means retraining staff, re-integrating systems, and disrupting clinical operations. The average installed life of a diagnostic imaging system is ten to fifteen years, and vendor loyalty through that period is extraordinarily high. The same dynamic applies in enterprise printing and in network surveillance, where thousands of installed cameras running on Milestone's software create deep ecosystem dependencies.

The third power is Scale Economies, particularly in Canon's distribution and service networks. Maintaining a global fleet of office multifunction devices requires a service infrastructure, trained technicians, parts warehouses, logistics networks, that represents an enormous fixed-cost investment. Canon and Ricoh have built these networks over decades, and they represent an almost impenetrable moat against new entrants. A startup with a superior printer design cannot compete without the ability to service machines in Omaha, Osaka, and Ouagadougou.

Now layer Porter's Five Forces. The threat of substitutes is the defining strategic variable, and it varies dramatically by segment. For consumer cameras, the threat was existential, and the substitution has already largely occurred. For medical imaging, the threat of substitutes is extremely low: there is no alternative to CT, MRI, or ultrasound for the clinical applications they serve, and regulatory barriers to entry are immense. For lithography equipment, the threat is asymmetric. ASML's EUV faces no substitute threat from Canon's NIL today, but if NIL matures, it becomes a substitute that could fundamentally disrupt ASML's pricing power.

Competitive rivalry is intense but structured. In mirrorless cameras, Canon faces Sony, which has captured a significant share of the professional market with its Alpha series, and Nikon, which has mounted a credible comeback with the Z system. But in medical imaging, the competitive structure is oligopolistic: four players control the vast majority of the global market, and price competition is restrained by the high cost of R&D, regulatory compliance, and service infrastructure. In network surveillance, Axis competes primarily against Hikvision and Dahua, Chinese manufacturers that dominate on price but face increasing regulatory restrictions in Western markets due to security concerns, a dynamic that has been structurally favorable for Axis.

The bargaining power of buyers is moderate in most of Canon's segments. Hospital systems and large enterprises have procurement leverage, but switching costs limit their ability to extract concessions. The bargaining power of suppliers is generally low, as Canon manufactures most critical components, lenses, sensors, print engines, internally, one of the advantages of vertical integration. The threat of new entrants is low across Canon's key segments, for different reasons in each case: regulatory barriers in medical imaging, service network requirements in production printing, and sheer technological complexity in semiconductor lithography.

The competitive comparison that matters most for Canon's future is the one with its medical imaging peers. Siemens Healthineers trades at roughly twenty-five to thirty times earnings, reflecting its leadership in high-growth areas like Photon Counting CT and interventional imaging. GE HealthCare trades at a lower multiple but benefits from its scale in the U.S. market. Canon Medical, buried within the parent company's consolidated financials, is valued by the market at a significant discount to what it would fetch as a standalone entity. This is the conglomerate discount in action, and it is one of the central tensions in Canon's investment case.

IX. The Playbook: Lessons for Investors and Founders

The first lesson Canon teaches is deceptively simple: do not fight the tide. When the smartphone destroyed the compact camera market, Canon did not double down on a losing hand. It did not launch a desperate smartphone of its own, as some analysts suggested. It did not try to convince consumers that dedicated cameras were still worth carrying. Instead, it acknowledged the structural reality, continued to serve the professional and enthusiast segments where dedicated cameras retained genuine advantages, and redirected the printing segment's cash toward entirely new growth vectors.

This sounds obvious in retrospect, but it is extraordinarily rare in practice. Corporate history is littered with companies that poured resources into defending their legacy business long after the battle was lost. Kodak, the most famous cautionary tale in the imaging industry, invented the digital camera but refused to cannibalize its film business until it was too late. BlackBerry saw the iPhone coming and responded by insisting that business users needed physical keyboards. Nokia dominated mobile phones for a decade and then fumbled the smartphone transition because it could not let go of its Symbian operating system. Canon's willingness to accept the decline of its iconic consumer business and move on is a case study in corporate pragmatism.

The second lesson is about adjacency. Every major acquisition Canon has made is connected to its core competency in optics, sensors, and image processing. A CT scanner is, at its most fundamental level, an imaging device that uses radiation instead of visible light. A network surveillance camera is a camera connected to a network with software intelligence. A semiconductor lithography system uses light, or physical imprinting, to create patterns at nanometer scale. Canon did not diversify into random industries. It extended its technological DNA into adjacent markets where that DNA provided a genuine competitive advantage.

This adjacency discipline is what separates Canon's M&A strategy from the conglomerate-building binges that have destroyed value at so many companies. When a company acquires businesses outside its circle of competence, it typically overpays and underperforms because it lacks the domain expertise to integrate and operate the acquired business effectively. Canon avoided this trap because every acquisition was, at its core, an optical or imaging business, even if the end market was completely different from consumer photography.

The third lesson is about the long game of intellectual property. Canon has ranked in the top ten of annual U.S. patent grants for forty-two consecutive years. This is not a vanity metric. It reflects a systematic investment in research and development, currently running at roughly eight percent of revenue, that ensures Canon owns the foundational technologies of the next decade. Nanoimprint Lithography, Photon Counting CT, OLED deposition technology: none of these emerged from a single research project. They are the products of decades of accumulated knowledge, built layer by layer, patent by patent.

For founders, the lesson is that core competency is not a product category. It is a set of capabilities that can be applied across many product categories. Canon's core competency was never "cameras." It was the ability to manipulate light and images with extreme precision. That competency has proven applicable to printing, medical imaging, surveillance, semiconductor manufacturing, and display technology.

For investors tracking Canon's ongoing transformation, two KPIs matter above all else. First, the Medical segment's revenue growth rate on a constant-currency basis. This is the bellwether for whether the Toshiba Medical acquisition is finally delivering the returns that justified its price tag. Consistent high-single-digit growth would validate the thesis; stagnation would suggest the conglomerate discount is permanent. Second, the Industrial segment's order pipeline for Nanoimprint Lithography tools: the number shipped and, critically, the identity of the customers. A second major customer beyond SK Hynix, particularly a logic foundry, would be a transformative signal.

X. Epilogue: The Bull Case vs. The Bear Case

The bear case against Canon begins with the man who built modern Canon. Fujio Mitarai is ninety years old. He has run the company for three decades, and while Kazuto Ogawa now holds the president title, the CEO and Chairman role still belongs to Mitarai. Japanese corporate transitions are notoriously difficult even when they are well-planned, and Mitarai's shadow is so long that it is unclear whether any successor can replicate his unique blend of Western financial discipline and Japanese operational patience. The risk is not that Ogawa is incompetent. The risk is that Mitarai's departure will reveal how much of Canon's strategic coherence depended on a single individual's judgment.

Beyond succession, the bear case points to the persistent "Japan discount." Japanese equities have historically traded at lower multiples than their American or European counterparts, reflecting concerns about corporate governance, capital allocation, and the glacial pace of change in Japanese boardrooms. Canon trades at a fraction of the multiples assigned to Siemens Healthineers or ASML, and the market's skepticism is not entirely irrational: the 165-billion-yen write-down on the medical business in fiscal 2024 was a reminder that Canon's M&A track record is imperfect. The Printing segment's secular decline, while slow, is relentless. And the consumer camera business, though still profitable for now, is a wasting asset.

The most specific bear argument concerns Nanoimprint Lithography. ASML's EUV technology has the benefit of being proven in mass production at the most demanding specifications. Billions of dollars of infrastructure have been built around it. Chip designers have optimized their processes for it. NIL's technical challenges, overlay accuracy, mask durability, defect rates, throughput, are not trivial, and there is a real possibility that Canon never overcomes them sufficiently to compete in leading-edge logic. If NIL remains confined to memory applications, it becomes a nice niche business but not the valuation catalyst that bulls are hoping for.

The bull case starts with valuation. Canon reported record revenue of approximately 4.62 trillion yen in fiscal 2025, with record profitability, a growing dividend, and the 200-billion-yen buyback program. The company has exposure to some of the most important technology megatrends in the world: medical imaging, AI-powered surveillance, and semiconductor manufacturing. If the market ever re-rates Canon to reflect the quality and growth potential of its medical and industrial segments, the upside is significant.

The bull case on Nanoimprint Lithography is not that it replaces EUV. It is that it does not need to. The global semiconductor equipment market is enormous, worth well over a hundred billion dollars annually, and growing rapidly as nations invest in domestic chip manufacturing capacity. If NIL captures even ten percent of the lithography market, it transforms Canon's Industrial segment from a marginal contributor into a major profit center. The cost advantage, potentially one-tenth the cost per exposure step compared to EUV, is so large that it creates a powerful incentive for chipmakers to at least diversify their lithography portfolios, particularly in cost-sensitive applications like NAND flash memory.

The medical business offers a similar optionality argument. Photon Counting CT is still in its early stages globally. Canon is behind Siemens, but the technology transition will play out over a decade or more as hospitals cycle through their installed equipment base. Canon's installed base, service relationships, and optical engineering expertise give it a credible position in a market likely to grow at mid-to-high single digits for the foreseeable future, driven by aging populations, increasing healthcare spending in emerging markets, and the expanding role of diagnostic imaging in precision medicine.

And then there is Canon Tokki, quietly generating extraordinary margins in its Niigata factory, holding a cornerstone position in the OLED supply chain that is only becoming more important as OLED displays expand from smartphones into laptops, tablets, automotive dashboards, and televisions.

Canon is not an easy company to categorize. It is not a pure-play growth stock. It is not a deep-value trap. It is something rarer: a century-old company that has repeatedly reinvented itself by applying the same set of core capabilities to entirely new markets, led for three decades by a man whose management philosophy bridges two cultures, and now sitting at an inflection point where any of three different technology bets could catalyze a fundamental re-rating.

The camera company that everyone knows is disappearing. What is emerging in its place is something far more interesting.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube