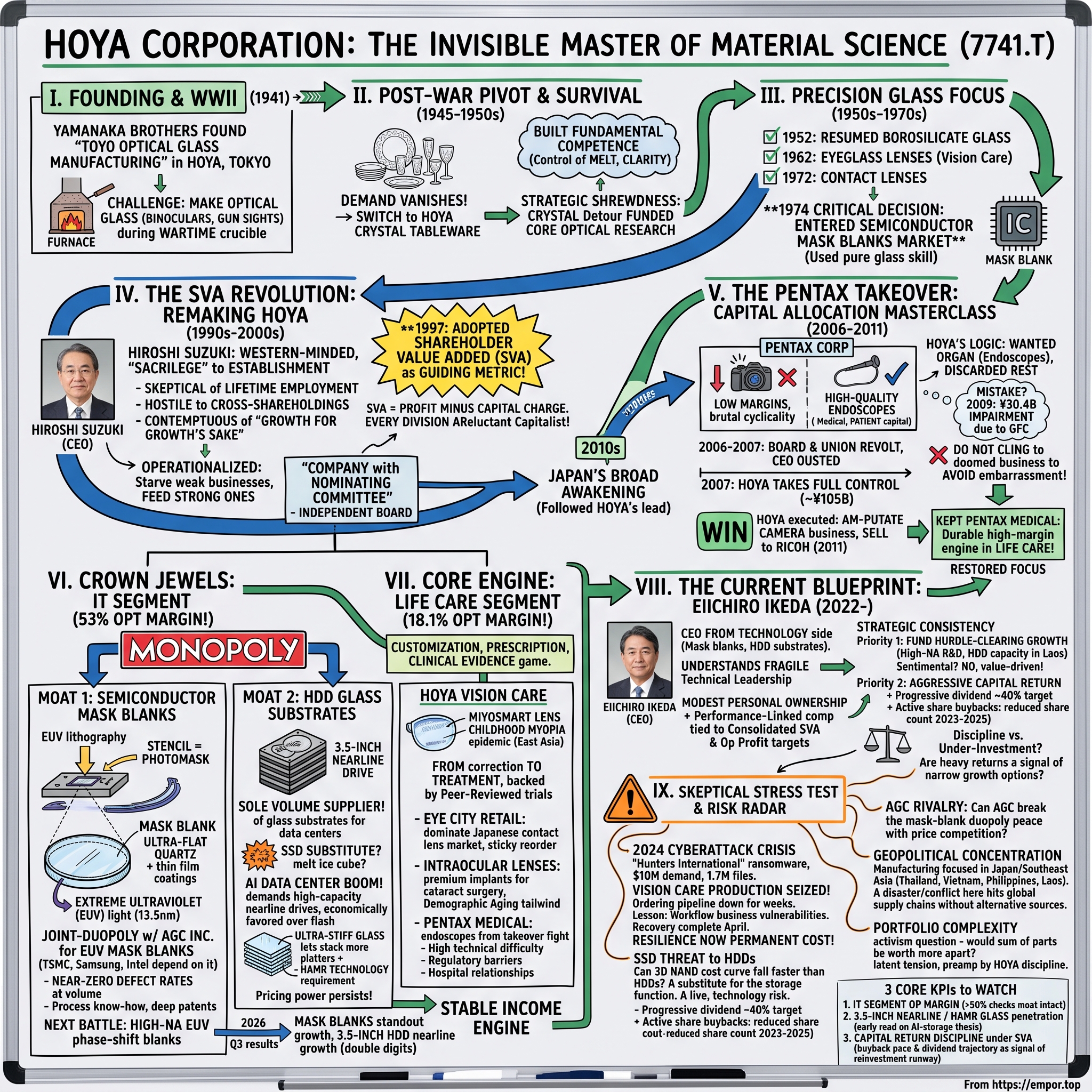

The Invisible Master of Material Science: HOYA Corporation

I. Introduction & The Silent Monopolist

Start with the puzzle, because the puzzle is the whole point. Open HOYA's results for the third quarter of the fiscal year ending March 31, 2026, and you find two businesses living under one roof that could not look more different on paper. The Information Technology segment—the part that makes glass for chips and hard drives—booked ¥92.9 billion in revenue and turned it into ¥49.3 billion of operating profit. That is a 53% operating margin.1 Read that again. For every ¥100 of sales, more than ¥53 falls to operating profit, before a single yen of corporate overhead is subtracted. Enterprise software companies dream of margins like that. HOYA achieves them by melting, coating, and polishing glass.

Sitting beside it is the Life Care segment—eyeglass lenses, contact lens retail, surgical endoscopes, cataract implants—which earned ¥27.4 billion of operating profit on ¥151.5 billion of revenue, an 18.1% margin.1 A perfectly respectable, cash-generative consumer-health business. But it is the IT segment's software-like economics on heavy, capital-intensive, physical hardware that stops you in your tracks. How does a glassmaker earn margins like a monopolist?

Because, in the most important senses, it is one.

To sit with that number for a moment: a 53% operating margin is not what heavy industry produces. Steelmakers, chemical companies, and glassmakers of the ordinary kind live and die in the single digits, forever pouring cash back into furnaces and kilns just to stay in the race. A margin north of fifty means that HOYA has escaped the usual gravity of manufacturing—that it has found a way to make a physical, capital-intensive product and yet capture value the way a toll booth or a patent licensor does. That escape is not luck. It is the endpoint of a very deliberate, decades-long strategy of pointing a rare capability only at the places where rareness is rewarded. The rest of this story is the explanation of how a company gets there and, just as importantly, whether it can stay.

The two moats, stated plainly. HOYA is the world's only volume manufacturer of the glass substrates—the pristine platters—that go inside high-capacity hard disk drives. Not the market leader. The only one. Every hyperscale data center running so-called "nearline" bulk storage is, at the level of physics, dependent on glass that comes from HOYA's fabs.[^2] And in semiconductors, HOYA together with AGC株式会社 AGC Inc. (the former 旭硝子 Asahi Glass) controls the overwhelming majority of the world's supply of Extreme Ultraviolet (EUV) mask blanks—the flawless quartz "master stencils" without which TSMC, Intel, and 삼성전자 Samsung Electronics cannot print a 3-nanometer or 2-nanometer chip.[^3]

Why does a business get to occupy positions like this? The short answer is that both products sit at the exact intersection of two things that are individually hard and almost impossibly hard together: extreme precision and extreme reliability at industrial scale. Anyone can make one perfect piece of glass in a laboratory given enough time. The trick—the thing that took HOYA the better part of a century to master—is making it perfectly, repeatably, defect-free, thousands of times over, to tolerances measured in atoms, for customers who will accept nothing less. Precision without scale is a science project. Scale without precision is a commodity. HOYA lives in the narrow band where both are required and almost no one else can operate.

Now, a monopoly is a claim, and claims deserve scrutiny rather than applause. A neutral observer should immediately ask: are these positions durable, or are they the kind of temporary lead that competitors and substitutes erode? Is HDD glass a growth story or a melting ice cube dressed up as a moat? Is AGC a genuine threat in mask blanks or a comfortable duopoly partner? Those questions are the spine of this episode, and we will keep returning to them rather than taking management's word for anything.

But first, the shape of the thing. HOYA trades on the 東京証券取引所 Tokyo Stock Exchange under ticker 7741.T, and it has grown into one of Japan's most valuable companies, a business worth tens of billions of dollars whose name means nothing to the people whose lives it touches.2 What makes it fascinating is not just the moats—it is that the company deliberately, decades ago, rebuilt itself around a single financial idea imported from Western finance, and then had the discipline to actually live by it while most of corporate Japan did not.

The roadmap from here: we begin in a farming town called Hoya in 1941, follow the improbable survival of an optical-glass maker through war and occupation, watch a Western-minded heir tear up the Japanese corporate playbook in the 1990s, dissect the Pentax deal that became a masterclass in buying what you want and selling what you don't, take apart the physics of the two crown-jewel monopolies, examine the high-margin eyecare engine, weigh the current management's promises against its record, and finally stress-test the whole edifice against the things that could break it—a ransomware crew, a flash-memory price war, and a rival glassmaker with ambitions of its own. To understand how HOYA thinks, you have to go back to two brothers and a furnace.

II. The Yamanaka Brothers & The Birth of Hoya Glass

Picture a farming town on the western fringe of Tokyo in November 1941. The town is called Hoya. Japan is weeks away from Pearl Harbor, the economy is being bent entirely toward the military, and optical glass—the specialty glass needed for binoculars, gun sights, and camera lenses—is a strategic material that Japan has historically had to import or reverse-engineer from Germany. Into this moment, two brothers, 山中昭一 Shoichi Yamanaka and 山中茂 Shigeru Yamanaka, opened an optical-glass production plant originally called 東洋光学硝子製造所 Toyo Optical Glass Manufacturing, later renamed after the town itself: 保谷硝子 Hoya Glass.3

It was a terrible time to start a precision-manufacturing business and, paradoxically, a perfect one. Terrible, because raw materials, fuel, and skilled labor were being swallowed by the war machine. Perfect, because the military desperately needed exactly what the brothers were trying to make. Optical glass is not window glass. Its refractive index has to be controlled to extraordinary tolerances, its internal purity has to approach the flawless, and getting there requires obsessive control over melting temperature, cooling rate, and chemistry. The wartime crucible—learning to make specialty glass for military optics under acute shortages—forged the one capability that would define the company for the next eighty years: the ability to melt and finish glass to tolerances almost no one else could hit.

Then the war ended, and with it the entire customer base. Military demand did not decline; it vanished overnight under Allied occupation. A lesser company would have died. Here HOYA made the first of what would become a signature series of pivots: it turned its furnaces toward the consumer. Out of the same glass-melting expertise came HOYA Crystal—high-end crystal tableware, stemware, vases, and art objects. It sounds like a footnote, and today it is nearly one, but the crystal business did something vital: it generated the cash that kept the lights on and, crucially, funded the survival of the core optical-research effort through the lean post-war years. The lesson HOYA learned early—that a cash-throwing business exists to fund the strategically important one—would later become corporate doctrine.

It is worth dwelling on why the crystal detour was strategically shrewd rather than a desperate lurch. Making fine crystal draws on the same fundamental competence as making optical glass—control of the melt, of clarity, of the way light moves through a solid. HOYA did not abandon its identity to survive; it found an adjacent commercial market that let it keep the furnaces hot and the metallurgists employed while the high-value applications it truly cared about were dormant. When you keep a difficult capability alive through a lean decade, you emerge on the other side with an advantage over every competitor who let theirs atrophy. The crystal business was, in retrospect, a bridge that carried HOYA's core skill across the wasteland of the immediate post-war years.

By the 1950s the company circled back to precision. In 1952 it resumed production of borosilicate optical glass—the BK7-type glass that is the workhorse of serious optics—and rebuilt its reputation for purity.3 From there it walked steadily toward the consumer's eye: eyeglass lenses in 1962, contact lenses in 1972, each move pushing HOYA deeper into markets where its glass touched a human face.3

But the decision that mattered most for the company we are analyzing today came in 1974, and it had nothing to do with eyes. HOYA's managers looked at the emerging microelectronics boom and asked a simple question: what does making a semiconductor actually require? The answer, at one critical step, was a piece of glass—ultra-flat, ultra-pure glass used as the substrate for the photomasks that pattern integrated circuits. HOYA already knew how to make glass flatter and purer than almost anyone alive. In 1974 it began manufacturing glass substrates for IC photomasks, planting the seed of what would, half a century later, become a 53%-margin monopoly.3

That single move contains the whole HOYA strategy in miniature: take a hard-won, general-purpose capability—precision glass—and keep pointing it at the highest-value, highest-barrier corner of whatever industry is growing fastest. The brothers built the furnace. The next generation would decide, with unusual rigor, exactly where to point it. And that decision would be governed not by ambition or nostalgia, but by a number.

III. The SVA Revolution: Remaking a Japanese Conglomerate

Here is where the story stops being a Japanese industrial fairy tale and becomes something genuinely strange for its time and place. To understand why, you have to understand what "normal" looked like in corporate Japan in the 1990s: lifetime employment, sprawling cross-shareholdings between friendly companies, boards stuffed with insiders who had spent forty years climbing the same ladder, and an almost religious commitment to growth and market share for their own sake, profitability be damned. Return on capital was, for many Japanese firms, an afterthought bordering on a foreign concept.

Into this world stepped 鈴木洋 Hiroshi Suzuki. The leadership had passed from the founding orbit through 鈴木哲夫 Tetsuo Suzuki, and then to his son Hiroshi, who would run HOYA as CEO from 2003 to 2022.4 Hiroshi Suzuki was, by the standards of the Japanese establishment, close to a heretic. He had spent formative time thinking in Western financial terms, and he rejected the sacred cows one by one: he was skeptical of lifetime employment, hostile to the web of cross-shareholdings that dulled accountability, and openly contemptuous of "growth for growth's sake." Where his peers wanted a bigger company, Suzuki wanted a more valuable one, and he understood those are not the same thing.

It helps to picture the man. Hiroshi Suzuki did not fit the archetype of the Japanese salaryman-executive who had spent four decades absorbing the unwritten rules of consensus and never once questioning them. He thought like an investor who happened to run a company, and he was willing to say out loud things that made the Japanese establishment wince—that a job for life is not a birthright, that owning shares in your customers and suppliers to keep everyone friendly is a way of hiding from accountability, and that a bigger company is not a better one unless it earns more than the cost of the capital it consumes. In a culture that prized harmony and continuity, this was close to sacrilege. It also happened to be correct, and HOYA's shareholders reaped the benefit for a generation.

The intellectual turning point came in 1997, when HOYA formally abandoned Return on Equity as its guiding metric and adopted Shareholder Value Added (SVA).5 The idea is not complicated, but its consequences were profound. SVA takes net operating profit after tax and then subtracts a charge for the capital employed to generate it—a charge set by the company's weighted average cost of capital. In plain English: it is not enough for a division to make a profit. It has to make a profit larger than the rent on the money it tied up to do so. If your division earns ¥10 but consumed capital that costs ¥12 to hold, you did not create value. You destroyed it. On an accounting income statement you look profitable; under SVA you are a drain.

What makes this more than a slogan is how brutally HOYA operationalized it. Every division manager was treated as though they ran an independent business with their own internal balance sheet and their own capital charge. A division that could not clear its cost of capital was not comforted and subsidized in the traditional Japanese way—it was denied expansion capital, restructured, or sold. Capital flowed toward the businesses that could compound it above their hurdle rate and was starved from the ones that couldn't. This is the mechanism that, decades later, explains the 53% IT margin: it is not an accident of good products, it is the residue of thirty years of relentlessly reallocating capital away from mediocre uses and toward exceptional ones.

The governance followed the philosophy. HOYA became an early Japanese adopter of the "company with a nominating committee" structure—a board form that hands real power over nominations, audit, and compensation to committees dominated by independent outside directors, rather than to insiders policing themselves.5 For a Japanese company of its era to build a board genuinely controlled by experienced outsiders was close to radical, and it turned HOYA into a reference point that reformers would later cite when Japan finally began, in the 2010s, to take corporate governance seriously.

Consider what this does to the psychology of a division head. In most large companies, capital is something you lobby for—the manager who tells the most exciting growth story, or who is closest to the CEO, gets the budget, and the money's true cost is invisible because no one ever charges you rent on it. Under SVA, the rent is explicit and unavoidable. A manager who wants to build a new plant has to believe it will earn more than the cost of the money, because that cost will be deducted from their scorecard whether the plant performs or not. It converts every executive into a reluctant capitalist, forced to reckon with the opportunity cost of the cash they command. Over decades, that single change in incentives compounds into a company that has systematically starved its weak businesses and fed its strong ones—which is exactly the pattern you see when you look at the modern HOYA and ask why so much of its profit comes from so narrow a slice of what it makes.

The timing of all this matters for appreciating just how far ahead of its peers HOYA was. Japan's broad corporate-governance awakening—the Stewardship Code, the Corporate Governance Code, the Tokyo Stock Exchange's later campaign to pressure companies trading below book value to improve their capital efficiency—largely arrived in the 2010s and 2020s. HOYA had internalized the substance of all of it in the 1990s, not because a regulator required it but because its own leadership concluded it was the right way to run a company. When the rest of corporate Japan finally began, under external pressure, to talk about return on capital and independent boards, HOYA had already been living that way for the better part of two decades. Being early is not the same as being right, but in this case the two coincided, and the compounding head start is visible in the business today.

A neutral analyst should note both the power and the limits here. SVA is a genuinely disciplining framework, and HOYA's willingness to act on it—to sell beloved businesses, to say no to empire-building—is rare and real. But SVA is also a system that can quietly encourage under-investment, milk mature assets, and financial-engineer returns through buybacks when growth is scarce. The interesting question is not whether HOYA preaches discipline—every company does—but whether its behavior over decades matches the sermon. The single best test of that came when HOYA went hunting for a struggling optical icon named Pentax.

IV. The Pentax Takeover: A Masterclass in Restructuring & Portfolio Optimization

Every great capital-allocation story needs a deal that reveals character under pressure. For HOYA, that deal was Pentax—and it is worth telling in full, because it shows the SVA doctrine surviving contact with drama, impairment, and the temptation to sink good money after bad.

Pentax Corporation in the mid-2000s was a company at war with itself. On one side sat a famous, beloved consumer camera brand—an institution in Japanese photography, adored by enthusiasts, and financially miserable: low margins, brutal cyclicality, and a losing multi-front war against Sony, Nikon, and Canon in a market that was about to be eaten alive by the smartphone. On the other side sat something far more interesting to a company like HOYA: a genuinely high-quality medical endoscope business, built on exactly the kind of advanced fiber optics and precision flexible-tube engineering that rewards patience and technical depth, and that throws off the fat, durable margins of medical devices.

HOYA's logic was clinical to the point of coldness. It wanted the endoscopes to scale up its high-margin Life Care ambitions. It had precisely zero interest in bleeding capital in the consumer camera wars. The problem, of course, is that you usually cannot buy half a company off the shelf—the endoscopes came welded to the cameras.

Step back and admire the elegance of what HOYA was actually attempting, because it is subtle. It wanted to perform surgery on another company—to reach inside Pentax, extract the one organ it valued, and discard the rest. In an efficient market for corporate assets, you would simply negotiate to buy the endoscope division on its own. But businesses are not sold that way, especially not in Japan, and especially not when the part you want to discard is the emotional heart of the target and the part you want to keep is the quiet cash generator few outsiders even noticed. So HOYA had to swallow the whole animal in order to keep one organ, which meant it had to have a credible, pre-formed plan to dispose of everything else without destroying value in the process. That is a far harder trick than a simple takeover, and the fact that HOYA pulled it off is the reason the deal is studied at all.

The drama played out across 2006 and 2007. The two managements initially agreed to a friendly merger. Then Pentax's own board and its unionized workforce revolted, terrified that HOYA—a company with no sentiment about the Pentax name—would eventually kill the historic camera brand they had built their identities around. The friendly deal collapsed into a corporate governance brawl. Pentax's CEO was ousted amid the fight. HOYA, undeterred, pressed forward with a hard-edged tender offer—a maneuver that, in the consensus-driven world of 2007 Japan, sat uncomfortably close to hostile. The price to take full control came to roughly ¥105 billion, on the order of $860 million at the time.6 HOYA got its company.

And then, almost immediately, it looked like a mistake. The Global Financial Crisis arrived, demand cratered, and by March 2009 HOYA was forced to take a painful impairment charge of about ¥30.4 billion against Pentax's goodwill and fixed assets—an accounting admission that it had, on paper, overpaid.7 This is the moment the story could have become a cautionary tale about a disciplined company losing its head in a takeover fight.

Instead, it became the opposite. HOYA did what its own doctrine demanded. It attacked the cost base, restructured the operations, and refused to keep subsidizing a business that could not clear its cost of capital. Then, in 2011, it executed the move it had been aiming at all along: it sold the Pentax consumer imaging and camera business to 株式会社リコー Ricoh Company, Ltd.8 The camera brand that had caused all the anguish became someone else's problem—and someone else's brand.

What HOYA kept was the prize: the medical endoscope operation, now PENTAX Medical, retained at a fraction of the net cost once the camera proceeds and the shed losses were accounted for. Today PENTAX Medical is a core, profitable engine inside the Life Care segment. The episode is the cleanest possible illustration of the SVA mind at work: identify the one asset that can compound above its capital charge, pay up to get it even through a bruising fight, take your medicine publicly when the timing proves unlucky, amputate the part that doesn't fit, and walk away owning exactly what you wanted. It is the rare acquisition where the impairment charge is not evidence of failure but a way-station on the road to a very good outcome.

There is a subtler lesson here for anyone evaluating management teams, and it cuts against a lazy investor instinct. A goodwill impairment is usually read as a confession of failure—proof that the acquirer overpaid and mismanaged. HOYA's Pentax experience is a reminder that the headline charge and the ultimate outcome can point in opposite directions. The impairment reflected the accounting value of assets HOYA fully intended to sell or wind down anyway; the economic result—keeping a durable, high-margin medical business acquired at a modest net cost after the camera disposal—was a clear win. The discipline to publicly take the loss, rather than clinging to a doomed camera business to avoid the embarrassment of a write-down, is itself the behavior of a management that answers to value rather than to face. That is precisely the kind of behavioral evidence worth more than any mission statement about "shareholder focus."

That discipline—buy the moat, sell the commodity—is easiest to admire in the businesses where the moat is deepest. So let us go inside the two that make HOYA a genuine monopolist.

V. The Crown Jewels of Information Technology

To appreciate why HOYA's IT segment prints money, you have to get your hands dirty with the physics, because the physics is the moat. There is no clever marketing here, no brand, no network effect. There is only the fact that a handful of things in advanced manufacturing are almost impossibly hard to do, and HOYA can do them.

Moat 1: Semiconductor Mask Blanks & The EUV Monopoly. Start with what a photomask is, in kitchen terms. Making a chip is a bit like using a stencil to spray-paint an incredibly intricate pattern onto a wafer, over and over. The stencil is the photomask. But before you can etch a pattern into a photomask, you need a perfect blank to etch it onto—an ultra-flat plate of synthetic quartz glass coated with precisely engineered thin films that absorb or reflect light. That blank is the mask blank, and it is HOYA's product.

Now make it monstrously harder. For the most advanced chips, the industry moved to Extreme Ultraviolet lithography, which uses light with a wavelength of just 13.5 nanometers—light so energetic that it is absorbed by essentially every material, including air and ordinary glass. You cannot shine EUV light through a stencil the old way, because nothing transmits it. So EUV masks work by reflection instead: the blank is built as a mirror made of 40 to 50 alternating, atomically thin layers of silicon and molybdenum, stacked with such precision that the reflections from each layer add up constructively into a usable beam.[^3] Think of it as a mirror assembled one atomic sheet at a time, where a single misplaced atom in the wrong spot becomes a defect that ruins a chip.

That last point is the entire commercial story. A defect on a mask blank does not cause a small problem—it gets faithfully reproduced onto every chip printed with that mask, potentially destroying the yield of a multi-billion-dollar production run. So the buyers—TSMC, Samsung, Intel—have close to zero tolerance for defects, and the ability to hit near-zero defect rates at volume is the barrier that keeps everyone else out. It is not a matter of being willing to spend money on a cleanroom, though that is required too. It is the accumulated, hard-won, deeply patented know-how of defect detection and multilayer deposition that cannot be bought or rushed. That is why the field narrows to essentially two players—HOYA and AGC—and why switching between them is not a purchasing decision but a multi-year qualification ordeal for a fab.[^3]

The word "duopoly" can mislead here, so it is worth being precise. HOYA and AGC are not two interchangeable giants splitting a market down the middle; they are two firms that have each accumulated distinct, hard-won process knowledge, competing at the frontier of what is physically achievable while a customer base of a handful of leading-edge foundries scrutinizes their defect rates relentlessly. The barrier that keeps this a two-horse race is not primarily money—the largest chipmakers could fund a mask-blank operation if capital alone were the obstacle. The barrier is time and yield: the accumulated learning about how to detect a defect a few nanometers across on a mirror built of fifty atomic layers, and how to do it consistently enough that a fab will bet a production run on it. That kind of know-how cannot be bought; it has to be lived through, defect by defect, over many years. It is the reason a well-capitalized newcomer cannot simply appear, and the reason the incumbents' lead tends to persist across technology generations even as the specifics change.

It is worth pausing on just how few of these blanks the world consumes and how much each one matters, because it inverts the normal logic of manufacturing. Most factories chase volume—make millions of units, drive down the unit cost, win on price. The mask-blank business is the opposite: relatively small unit volumes, extreme value per unit, and a customer who cares about exactly one thing above all else, which is that the part be perfect. In that world, being the cheapest is irrelevant and being the most reliable is everything. A fab that has qualified HOYA's blanks and built its process around them is not going to risk a production run worth more than a small country's GDP to save a few percent on a component that is a rounding error in the total cost of the chips. This is why the pricing power is so durable: the thing the customer is buying is not glass, it is the near-certainty that the glass will not ruin their yield.

On the FY2026 third-quarter results, this business was visibly on fire: within the IT segment, semiconductor mask blanks were a standout growth driver, part of a segment where both sales and profit grew around 15% year on year.1 The next battleground is High-NA EUV—a new generation of ASML machines with a higher numerical aperture (0.55) that print even finer features—plentiful with the more advanced phase-shift mask blanks it demands. HOYA has said it is funding internal R&D hard to capture this wave. That is a claim about the future, and the honest analytical position is that leadership in current-generation EUV blanks does not automatically guarantee leadership in High-NA; it has to be won again. But the incumbency, the customer relationships, and the yield know-how give HOYA a real head start.

Moat 2: HDD Glass Substrates & The AI Data Center Boom. Now to the more contrarian of the two, because it requires killing a widespread misconception first. The consensus line is: "Solid-state drives are killing hard drives, so HOYA's disk business is a melting ice cube." That is half right, and the wrong half is where the money is. Yes, in laptops and phones, the small 2.5-inch drives got replaced by flash. But in the vast cold storage of hyperscale data centers—the bulk "nearline" storage where AWS, Google, and Microsoft keep the staggering and growing ocean of data that AI both consumes and generates—the economics still overwhelmingly favor big, cheap 3.5-inch hard drives.[^2]

Here is where glass becomes indispensable, and here is the analogy. To cram 24, 30, or more terabytes into a standard 3.5-inch drive, manufacturers stack the internal platters like records in a jukebox—ten or more of them, sealed in helium to reduce drag. But the thinner you make each platter, the more it behaves like a spinning vinyl record that starts to wobble and flutter at 7,200 RPM. Aluminum, the traditional platter material, flutters badly once you go below about half a millimeter. Glass does not. Glass is far stiffer, smoother, and flatter, which lets HOYA make substrates as thin as 0.38 millimeters—and thinner—without wobble.[^2] Less wobble means you can pack more platters into the same height and fly the read/write heads closer to the surface, which means more terabytes per drive. Glass is what makes the highest-capacity drives physically possible.

And the next technology generation makes glass not merely better but mandatory. Heat-Assisted Magnetic Recording (HAMR), the technique drive makers are using to push capacities higher still, works by using a tiny laser to heat a spot on the platter to around 450°C for a few billionths of a second before writing to it. Aluminum would warp and eventually deform under that thermal punishment. Glass survives it.[^2] In a HAMR world, the substrate essentially has to be glass—and HOYA is the sole volume supplier of it.[^2] The strategic beauty of HAMR, from HOYA's perspective, is that it does not merely preserve the glass-substrate business; it deepens the moat. Every generation of higher-capacity, thermally-assisted drives makes the substrate harder to manufacture and glass more clearly the only viable material, which pushes any lingering aluminum competition further toward irrelevance in the highest-value tier. The technology roadmap of the drive industry, in other words, keeps walking straight into HOYA's strengths. That is a very comfortable place to be—provided, and this is the whole debate, the drive industry itself keeps growing rather than ceding the field to flash.

Consider the strangeness of this situation from a data center's point of view. A hyperscaler can source its servers from many vendors, its chips from a few, its networking from several. But when it buys the highest-capacity hard drives to store the exabytes of data that modern AI workloads generate and consume, it is buying a product whose most critical internal component—the platter itself—traces back, in the glass generation, to a single company. The drive makers, Seagate and Western Digital, compete fiercely with each other on the drive; but on the substrate underneath, they share a common and singular dependency. That is a remarkable place for a supplier to sit, and it explains why HOYA can hold margins in this business that a mere component vendor could never dream of.

On the FY2026 third quarter, HDD substrate sales grew 9% year on year, with the crucial 3.5-inch nearline substrates growing double digits.1 That is the tell an investor should focus on: the total HDD number is being pulled up by the exact 3.5-inch, high-capacity category that the AI-storage thesis is about, even as legacy volumes fade. The customers on the other end—Seagate, Western Digital, and 株式会社東芝 Toshiba Corporation—are, at the level of raw materials, bottlenecked by a single supplier in Japan and Southeast Asia. That is an extraordinary position. Whether it is a durable one depends entirely on the SSD-versus-HDD cost curve, which we will stress-test later. For now, hold onto the tension: this is simultaneously HOYA's most profitable growth engine and its single most debated long-term risk.

Two monopolies built on the same eighty-year-old skill of melting and polishing glass to the edge of physical possibility. But HOYA is not only an IT company, and the other half of the house tells a very different story.

VI. The Life Care Engine: High-Margin Eyecare & Medical Tech

Walk into an optician almost anywhere in the developed world, order a pair of progressive lenses, and there is a meaningful chance the glass—or, more precisely, the high-index polymer—came through HOYA's network, even if the storefront brand is someone else's. This is a completely different kind of business from the mask-blank monopoly: not a physics chokepoint, but a distribution, prescription, and clinical-evidence game. And it is where HOYA's second engine, Life Care, lives.

Hoya Vision Care does not play the commodity retail game of selling identical lenses to the lowest bidder. Its model is a network of local prescription laboratories that grind custom, high-index lenses to an individual's prescription and get them to the optician fast. The value is in the customization, the optical quality, and the logistics of doing that at scale across dozens of countries—a workflow business more than a product business.

The genuinely interesting margin story inside vision care is a product called MiYOSMART. Here HOYA moved from selling correction to selling treatment. MiYOSMART is a spectacle lens designed not just to let a myopic child see clearly today, but to slow the progression of their nearsightedness over time—addressing a genuine and growing public-health problem, particularly in East Asia, where childhood myopia has reached epidemic levels. HOYA has promoted clinical data indicating the lenses can meaningfully slow myopia progression in children, a claim rooted in peer-reviewed trials rather than pure marketing. A lens that treats a disease, backed by clinical evidence and a patent, commands pricing and loyalty that a commodity lens never could. The analytical caveat is fair: myopia-control is now a competitive category, with rivals like EssilorLuxottica's Stellest pursuing the same market, so MiYOSMART is a strong product in a contested race, not an unassailable one.

The retail side runs through the アイシティ Eye City chain, HOYA's contact-lens retail network in Japan, which holds a dominant share of the domestic contact-lens market.2 The moat here is unglamorous but real: store density. When your local optician for contacts is on every convenient corner and holds your prescription and reorder history, the friction of switching is just high enough, and the repeat-purchase nature of contact lenses just sticky enough, that the business compounds quietly through customer retention.

The MiYOSMART example also illustrates a broader strategic instinct that runs through all of HOYA: the preference for products where technical or clinical difficulty creates pricing power, rather than products that compete purely on cost. A plain corrective lens is a commodity, and commodities earn commodity margins no matter how well you make them. A lens that has been through clinical trials, carries a health claim, and solves a problem parents are desperate to solve is a different economic animal entirely. It is the eyecare equivalent of what mask blanks are to semiconductors—the same company, applying the same instinct, in a completely different industry.

Then there are intraocular lenses—the premium polymer lenses surgically implanted to replace the eye's natural lens during cataract surgery. This is a high-margin medical-device business riding one of the most reliable tailwinds in the world: demographic aging. As the populations of North America, Europe, and East Asia grow older, the volume of cataract procedures rises almost mechanically, and each procedure needs a lens.

PENTAX Medical, the endoscope business salvaged from the Pentax saga, rounds out the portfolio and deserves its own note. An endoscope is a small marvel of engineering—a flexible tube that must snake through the human body carrying light, high-resolution imaging, and working channels for instruments, all while being reliable enough for a surgeon to trust and durable enough to be sterilized hundreds of times. It is a business of long product cycles, deep hospital relationships, and regulatory approvals that themselves function as a barrier to entry. It competes in a field led by Japanese rivals, and it is not the dominant player, but it fits HOYA's template neatly: high technical difficulty, recurring demand, and margins that reward patience rather than punish it. It is also a reminder that the original Pentax gamble was not about cameras at all—it was about acquiring exactly this kind of durable medical franchise, and everything else was noise to be disposed of.

Add PENTAX Medical's endoscopes—the prize from the Pentax saga—and Life Care becomes a coherent portfolio: eyeglass lenses, contact-lens retail, surgical implants, and diagnostic endoscopes, all pointed at the aging human body. It grew revenue 9% year on year in the FY2026 third quarter at an 18.1% operating margin.1 That is a good business, not a great one by HOYA's own IT-segment standard—and that gap is precisely why the SVA framework matters. Life Care must keep earning its place against a capital charge, not coast on the fact that it is larger and more visible than the IT segment. Which brings us to the person whose job is to enforce exactly that discipline today.

VII. The Current Captain: Eiichiro Ikeda & The Capital Allocation Blueprint

When 池田英一郎 Eiichiro Ikeda took over as CEO in 2022, he inherited something rare: a Japanese company that had already done the hard cultural work of becoming shareholder-focused, and whose main risk was not that a new leader would fail to reform it, but that a new leader might break the discipline that made it special.4 The interesting question about Ikeda, then, is not "will he transform HOYA?" but "will he leave the machine alone and keep it running?"

His background is telling. Ikeda is not a parachuted-in financier; he is a deep insider who joined HOYA in 1984 and spent his career on the technology and IT side of the house, rising through the research and commercialization function to serve as the group's chief technology officer before taking the top job.4 In other words, the man now running the whole company came up through the exact businesses—HDD substrates and semiconductor mask blanks—that generate its highest returns. He understands, from the inside, why the IT segment's moats are real and how fragile technical leadership can be if R&D slackens.

On ownership and incentives, the picture is worth stating precisely rather than romanticizing. Ikeda's direct shareholding is modest—on the order of a few thousand shares—so this is not a founder-CEO with a fortune riding on the stock.9 His alignment comes instead through performance-linked compensation tied to consolidated SVA and operating-profit targets—that is, he is paid on the same value-creation metric the whole company is run by, which is at least internally consistent.9 A skeptic would note that modest personal ownership plus incentive comp is a weaker form of alignment than a large equity stake; a fair rejoinder is that it is far better than the seniority-and-tenure pay that still dominates much of corporate Japan.

Assessing a CEO's credibility is ultimately about consistency over time—whether the story told on this year's earnings call matches the one told three years ago, whether guidance is met or quietly walked back, whether misses are explained or blamed on the weather. HOYA's communications have tended toward the concrete: on recent results the message has been steady and specific—semiconductor blanks and 3.5-inch HDD substrates driving the IT segment, disciplined capital return, no appetite for transformational deals.1 That steadiness is itself a form of credibility. A management team that says the same thing across a run of quarters, and whose numbers keep validating it, earns more benefit of the doubt than one that reinvents its strategic narrative every time the market mood shifts. The flip side, which a skeptic should hold onto, is that consistency is easy to maintain while the tailwinds blow; the real test of a management's candor is how it explains a genuine miss, and HOYA's most recent stumble—the cyberattack—was blamed on an external attacker rather than on any strategic error, which is fair but also convenient.

The more persuasive evidence of Ikeda's credibility is behavioral: strategic consistency. Under his tenure HOYA has conspicuously refused the empire-building path—no dilutive, transformational, ego-driven M&A—and has kept the SVA filter firmly in place. The capital-allocation blueprint he has maintained runs in a clear priority order. First, fund the growth that clears the hurdle rate: internal R&D for High-NA EUV and next-generation glass substrates, and capacity expansion, including HDD substrate manufacturing in Laos. Only after those investments are funded does surplus cash get returned—and returned aggressively.

The Laos expansion deserves a moment, because it is a small window into how the company thinks about cost. HDD substrate manufacturing is exacting but, unlike mask blanks, it is a genuine volume business where unit cost matters. Locating incremental capacity in a lower-cost Southeast Asian base rather than in Japan is the sort of unsentimental decision that a company optimizing for value—rather than for national prestige or headcount at home—makes without agonizing. It is the SVA logic reaching down into geography: put the capital where it earns the highest return net of its cost, and do not let sentiment about "made in Japan" get in the way. The same instinct that sold the Pentax cameras shows up in where the company chooses to pour glass.

The return policy pairs a progressive dividend, with a target payout ratio around 40%, with active share buybacks, and HOYA has signaled the intention to return effectively all excess capital once growth investments are funded.10 The buyback record backs the rhetoric: repurchases across 2023 to 2025, including a ¥60 billion authorization, materially shrank the share count and lifted per-share value for continuing holders.10 This is where the neutral lens matters most. Buyback-heavy capital return is genuinely shareholder-friendly when a company has more cash than good projects—but it is also the classic move of a business whose growth options are narrowing, and it can flatter per-share metrics while masking a lack of reinvestment runway. For HOYA the tension is live: is heavy capital return a sign of admirable discipline, or a quiet admission that even the mask-blank and glass-substrate moats cannot absorb all the cash they generate? Both can be true at once, and an investor should watch which one dominates over time.

For all the discipline, the machine is not invulnerable. In 2024 HOYA got a brutal reminder that a company can master the physics of matter and still be brought to its knees by something far more mundane.

VIII. The Skeptical Stress Test & Risk Radar

On the morning of March 30, 2024, HOYA discovered that something was badly wrong with its IT systems.[^13] What followed was the kind of operational nightmare that no amount of glass-melting genius can prevent, and it is the right place to begin a hard-nosed inventory of what could actually break this company.

The 2024 cybersecurity crisis. The attacker was a ransomware crew calling itself "Hunters International," and their demand, once they surfaced, was blunt: $10 million, reportedly under a stated no-negotiation, no-discount policy, in exchange for not leaking an alleged 1.7 million stolen files—roughly 2 terabytes of data—and for a decryptor.11 The mechanism of damage is what makes this instructive. HOYA's vision-care business runs on centralized IT to route lens orders to its network of prescription labs. When those systems went down, the ordering and production pipeline for eyeglass lenses seized up across much of the world, and labs were knocked offline for weeks; HOYA reported that restoration of the affected vision-care systems was substantially complete only by late April.[^13] The financial residue was a soft patch in vision-care sales for the period—a reminder that a workflow business's greatest strength, centralized coordination, is also a single point of catastrophic failure. Management's response was a large investment in hardened, more decentralized IT infrastructure and supply-chain redundancy. Whether that investment truly reduces the risk or merely reduces the last-known version of it is unknowable until the next attempt; the honest conclusion is that operational cyber-resilience is now a permanent line item in the HOYA risk ledger, not a one-time event that has been "fixed."

There is a governance angle to the cyberattack worth naming as well. A company that has spent decades cultivating a reputation for operational excellence and disciplined management was, for the better part of a month, unable to route eyeglass orders to its own labs. It exposed a truth that no amount of financial engineering can paper over: as manufacturing becomes more digitally coordinated, the attack surface grows, and a firm's most efficient systems become its most concentrated vulnerabilities. The relevant question for an investor is not whether HOYA can be attacked again—every company can—but whether management treats resilience as a permanent cost of doing business or as a box that was checked in 2025 and forgotten. The honest read from the outside is that the jury remains out, and that operational-continuity disclosure is something worth watching in future reports rather than taking on faith.

The SSD threat to nearline HDDs. This is the bear case that matters most to the crown jewel. The entire HDD-glass thesis rests on one economic fact: for bulk cold storage, hard drives remain dramatically cheaper per terabyte than flash. If the cost of 3D NAND flash fell faster than expected—because of a manufacturing breakthrough or a glut-driven price collapse—hyperscalers could begin swapping nearline HDDs for enterprise SSDs, and the long-term investment case for HOYA's glass substrates would erode from underneath. The counter-argument is that the cost gap is large and the data-growth curve from AI is steep enough that hard drives should stay economically necessary for years. But "should" is doing a lot of work in that sentence. This is a genuine, unresolved technology-substitution risk, and it is why a serious investor watches the HDD-versus-SSD cost-per-terabyte spread more closely than any single quarter's results.

The duopoly rivalry. In mask blanks, HOYA's comfort depends on AGC remaining a rational duopoly partner rather than an aggressive share-taker. AGC has been expanding its EUV mask-blank capacity, and a determined push for share could spark price competition that erodes exactly the margins that make the IT segment so extraordinary.[^3] Duopolies are lucrative precisely as long as both parties prefer margin to volume; the risk is always that one side decides to break the peace. There is no evidence of an all-out price war today, but the structural possibility is a permanent ceiling-check on HOYA's pricing power.

Geopolitical supply-chain concentration. Finally, geography. HOYA's manufacturing for substrates, lenses, and endoscopes is concentrated in Japan and Southeast Asia—Thailand, Vietnam, the Philippines, Laos. That concentration is efficient and, in the case of Laos HDD-substrate expansion, cost-driven. It is also a vulnerability: a major natural disaster, political instability, or a trade conflict hitting one of those hubs could interrupt a supply chain that the world's chipmakers and drive makers have no alternative source for. The very fact that HOYA is a sole or near-sole supplier turns its own supply-chain hiccups into everyone's problem—concentration risk with systemic reach.

One more overlay belongs on the radar, quieter than the rest: portfolio complexity itself. HOYA is, in the end, a genuine conglomerate—glass for chips, glass for drives, lenses for eyes, implants for cataracts, scopes for gastroenterologists—stitched together not by shared products or customers but by a shared financial philosophy. That structure is what allowed the Pentax surgery and the relentless capital reallocation, and in HOYA's case it has clearly created value rather than destroyed it. But conglomerate structures always invite the activist's question: would the sum of the parts be worth more apart? A pure-play mask-blank-and-substrate company might command a richer multiple than one where those crown jewels are bundled with a slower-growing consumer eyecare business. There is no evidence HOYA is under such pressure today, and its own discipline has largely pre-empted the critique. But it is the kind of latent tension that surfaces the moment execution wobbles, and it is worth holding in mind as part of the complete picture.

Put together, the risk radar is not a reason to dismiss HOYA; it is the set of things that a sober owner has to keep re-checking. With the risks on the table, we can weigh them formally against the powers that make HOYA what it is.

IX. Strategic Analysis: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the structural question a strategist would ask: why, precisely, does HOYA earn these returns, and what protects them? Two frameworks help—Hamilton Helmer's 7 Powers and Michael Porter's Five Forces—and applied honestly, they explain both the strength and the boundaries of the moat.

The 7 Powers at work. Three of Helmer's powers are clearly present, and it is worth being precise about which.

Scale economies show up in the sheer capital and know-how intensity of the crown-jewel businesses. Building synthetic-quartz fabrication and the multilayer vacuum-deposition tooling for EUV blanks, or the ultra-precision polishing lines for glass substrates, requires fixed investment and accumulated process expertise that only a very high-volume producer can justify and amortize. A subscale entrant would carry the same enormous fixed costs over far less output—an unwinnable unit-cost position.

Switching costs are, if anything, the deeper power. A fab does not simply buy mask blanks; it tunes its entire multi-billion-dollar lithography process around the exact chemical and physical characteristics of a specific supplier's blanks. Qualifying a new supplier means years of testing and putting chip yields at risk in the meantime. That is not a preference; it is a lock-in measured in years and billions, and it is why incumbency in this business is so valuable.

Cornered resource rounds it out: HOYA's proprietary glass-melting formulations and precision-polishing patents are, in effect, a resource competitors cannot replicate at scale. No one else can currently make HDD glass substrates to HOYA's flatness in volume—which is the literal definition of a cornered resource that has been converted into a 100% market share.

Notice which powers are absent, because that is equally revealing: HOYA has essentially no branding power (its customers are engineers who care about defect rates, not logos) and no network economies. Its moat is entirely a supply-side, technical-and-contractual moat. That matters, because supply-side moats can be leapfrogged by a technology shift in a way that demand-side network moats usually cannot. It is a formidable castle—but its walls are made of process know-how, and process know-how is exactly what a disruptive substitute renders worthless.

There is a fourth power worth mentioning by its absence-turned-presence: counter-positioning, the situation where an incumbent cannot copy a challenger without damaging its own existing business. HOYA does not obviously possess it in the crown jewels, but something adjacent operates in the HDD story. A pure aluminum-substrate maker cannot pivot to glass casually, because glass processing is a fundamentally different competence—melting, precision polishing, and defect control that HOYA spent decades acquiring and that an aluminum-stamping operation has no head start in. As the industry transitions toward the glass and HAMR era, the incumbent aluminum suppliers face exactly the kind of trap counter-positioning describes: the harder they lean into their existing strength, the further behind they fall in the technology that is winning. HOYA is on the right side of that transition, but only for as long as glass remains the answer.

Porter's Five Forces. The threat of new entrants in both crown-jewel businesses is close to zero, for all the reasons above—capital intensity, defect-rate barriers, and years-long qualification. The bargaining power of buyers is the most interesting force to get right. On paper the buyers are terrifyingly powerful: they are among the largest, most concentrated, most sophisticated companies on Earth—TSMC, Samsung, Intel, Seagate, Western Digital. Ordinarily, buyer concentration crushes supplier margins. Here it does not, because those mighty buyers have almost nowhere else to go. Concentration without alternatives is not leverage. That inversion—powerful buyers with weak actual bargaining position—is the single best explanation for the 53% margin. The threat of substitutes is the force that splits the company cleanly in two: it is high and existential in HDD substrates (SSDs are a real substitute for the underlying function of storage) and low in EUV mask blanks (there is no other way to pattern leading-edge chips). Rivalry, meanwhile, is muted in the mask-blank duopoly and, in HDD glass, essentially nonexistent by virtue of monopoly—so long as the market itself survives.

The frameworks converge on the same conclusion an honest analyst reaches from the numbers: HOYA's advantages are real, structural, and unusually durable against competitors, but meaningfully exposed to substitution and technology transition. The company is safe from being out-competed and vulnerable to being made obsolete. That is the precise shape of the bull and bear debate.

X. The Bull vs. Bear Case & 3 Core KPIs

So where does an owner come down? Not with a verdict—that is the reader's job—but with the strongest honest version of each side.

The bull case rests on three compounding tailwinds. First, that the semiconductor industry's march to High-NA EUV accelerates, driving demand for the more sophisticated and higher-value phase-shift mask blanks where HOYA's incumbency and yield know-how give it the inside track—turning a great business into an even better one. Second, that the AI data explosion forces hyperscalers to keep deploying ultra-high-capacity HAMR nearline drives, which require glass, expanding HOYA's addressable substrate market as the 3.5-inch category grows and legacy volumes fade into irrelevance. Third, that demographic aging across the developed world drives durable, high-margin growth in premium progressive lenses, myopia-control lenses, and intraocular implants. Layer those three on top of a management team that returns essentially all excess cash, and the bull sees a monopolist compounding value with disciplined capital allocation.

The bear case is the mirror image, and it is not a weak one. First, enterprise SSDs cannibalize data-center cold storage faster than expected, and the HDD-glass monopoly turns out to be a monopoly on a shrinking market—the worst kind. Second, AGC wins the High-NA blank race, converting a comfortable duopoly into a price war and stealing the pricing power that underpins those extraordinary margins. Third, another major cyberattack, or a geopolitical shock to the Southeast Asian manufacturing base, halts production at a company whose sole-supplier status makes any outage disproportionately damaging. The bear's core insight is the one the 7 Powers analysis surfaced: a supply-side technical moat protects you from rivals but not from obsolescence, and two of HOYA's three legs face exactly that kind of substitution risk.

It is worth noticing how asymmetric the two cases are in their timing. The bull case is a slow burn: High-NA adoption unfolds over years, HAMR ramps over years, demographic aging is the most gradual force in economics. None of it happens in a quarter. The bear case, by contrast, contains at least one item that could arrive suddenly—a step-change in flash economics, a determined AGC price war, another cyber or geopolitical shock. This asymmetry is characteristic of moat-protected monopolists generally: the upside compounds quietly while the downside, when it comes, tends to come fast. An owner of a business like this is essentially being paid a rich stream of profit in exchange for accepting a small probability of a sharp discontinuity. Understanding that trade—rather than pretending the discontinuity risk is zero because it has not happened yet—is the difference between owning HOYA with eyes open and owning a story.

The intellectually honest position holds both cases in tension rather than resolving them prematurely, and watches the evidence. Which is why the discipline for following this company reduces to a very small number of things that actually move the thesis.

The three KPIs that matter. First, the IT segment operating margin—the single cleanest gauge of whether HOYA's pricing power in mask blanks and HDD substrates is intact. As long as it holds around or above 50%, the moat is doing its job; sustained erosion would be the first hard evidence of an AGC price war or HDD-market decay. Second, the 3.5-inch nearline / HAMR glass-substrate penetration rate—tracked through Seagate's and Western Digital's high-capacity drive shipments and the mix shift toward glass. This is the earliest read on whether the AI-storage bull case is real or whether SSD substitution is winning. Third, capital return discipline under the SVA framework—the buyback pace and dividend trajectory, watched not just for generosity but as a signal of whether management still believes it has growth worth reinvesting in, or is quietly conceding it does not. Those three, tracked over time, tell you almost everything about whether the story below is intact.

XI. Epilogue & Outro

The deepest lesson of HOYA is a rebuke to a comforting modern assumption. We have been trained to believe that the ultimate power in the digital economy accrues to the consumer-facing software brands—the platforms, the apps, the logos on our screens. HOYA is the counter-example that refuses to go away: a company almost no consumer can name, holding two of the tightest chokepoints in all of technology, earning software-like margins on physical glass, precisely because it mastered the unglamorous, unbrandable, near-impossible physics that the flashy companies depend on and cannot do themselves.

There is a second lesson braided through the first, and it is about temperament. HOYA's edge is not only technical; it is behavioral. The willingness to abandon a sacred metric in 1997, to charge every manager rent on the capital they use, to swallow a whole company in order to keep one division and take the write-down without flinching, to build capacity in Laos rather than at home, to return cash rather than hoard it for empire-building—each of these is a decision that many companies, and especially many Japanese companies of their era, could not or would not make. The physics gave HOYA its moats. The discipline is what turned the moats into decades of compounding value rather than a squandered advantage. A competitor could, in theory, copy the second even where it cannot copy the first—and the fact that so few do is itself a kind of moat.

From two brothers and a furnace in a Tokyo farming town in 1941, through the wreckage of war, a crystal-tableware detour that paid the bills, a heretical embrace of Western capital discipline, a bruising takeover fight, and a relentless narrowing toward only the highest-return corners of material science, HOYA became the silent master of the global technology supply chain. Whether it stays that way depends not on out-competing anyone—almost no one can compete—but on whether the physical worlds it dominates, glass for chips and glass for drives, remain the worlds the future is built on. That is the question worth carrying forward. The furnace is still burning.

References

-

HOYA (7741.T) Reports Q3 FY2026 Results — segment revenue and operating profit — BigGo Finance, 2026-01-30 ↩↩↩↩↩↩

-

Investor Relations Portal / Company History — HOYA Corporation ↩↩↩↩

-

Leadership — Directors and Executive Officers — HOYA Corporation ↩↩↩

-

HOYA tender offer to acquire Pentax (~¥105 billion, 2007) — Reuters ↩

-

HOYA Financial Results — Pentax goodwill impairment (FY ended March 2009) — HOYA Corporation ↩

-

Ricoh to Acquire HOYA's Pentax Camera Business — DPReview, 2011-07-01 ↩

-

Executive Officers / management shareholding and compensation — HOYA Corporation ↩↩

-

Who Owns HOYA — capital allocation, buybacks (2023–2025) and dividend policy — MatrixBCG ↩↩

-

Optics Giant Hoya Hit with $10 Million Ransomware Demand — BleepingComputer, 2024-04-11 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube