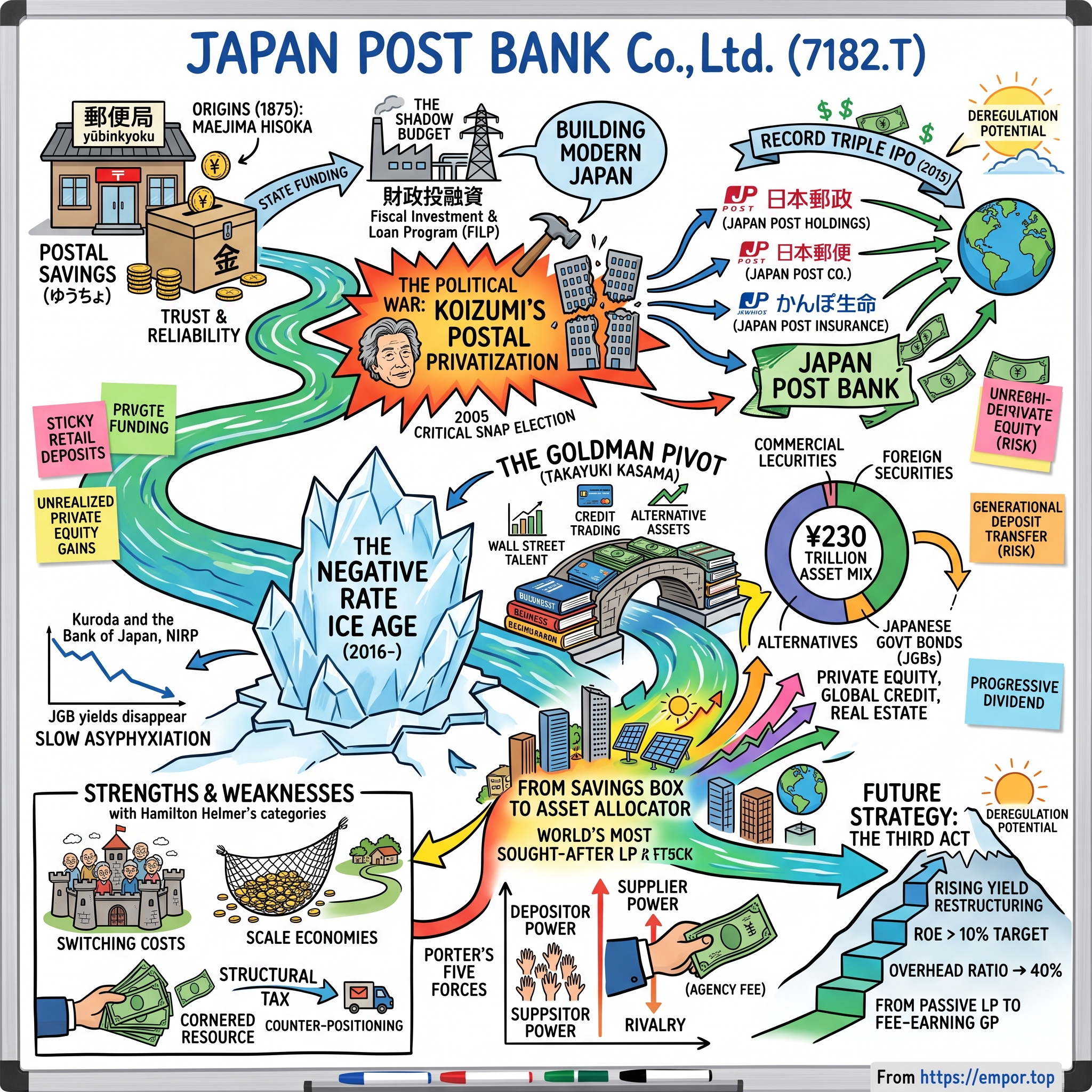

Japan Post Bank: The World's Largest Savings Box and its Goldman-Led Metamorphosis

I. Introduction & Episode Roadmap

Let's start with the number that breaks brains on trading desks. Total assets of ¥232.8 trillion. Retail deposits of ¥188.4 trillion, split between ¥125.4 trillion of liquid savings and ¥62.8 trillion of fixed-term deposits.1 Against that mountain of funding, a loan book of ¥4.5 trillion.1 Every commercial bank in history has been an engine for one thing: take in deposits cheaply, lend them out at a spread, manage the credit risk. Japan Post Bank was legally forbidden from doing the lending half. So what does it do with ¥188 trillion of other people's money? It invests it. It is, functionally, the world's largest fixed-income and alternatives fund that happens to be regulated as a bank and staffed by postal clerks.

The core paradox is historical. This institution began in 1875 as 郵便貯金 postal savings, dreamed up by a samurai-turned-bureaucrat named 前島密 Maejima Hisoka to teach ordinary Japanese to save and to bankroll a nation racing to industrialize. For most of the next century and a quarter, those savings were not really the saver's business — they were the state's. They flowed, almost automatically, into a shadow national budget that built the expressways, dams, and airports of modern Japan. How that quiet, state-directed savings machine metamorphosed into a public company selling shares to global investors, and then into a sophisticated Limited Partner writing billion-dollar checks to the world's top buyout firms, is the arc of this entire episode.

The modern story has a sharp pivot in it. For decades Japan Post Bank did one boring thing supremely well: it bought Japanese Government Bonds — JGBs — and clipped a modest coupon. Then Japan's central bank pushed interest rates below zero and blew up that business model. The bank's response was to hire Wall Street. It brought in alternative-asset and credit-trading talent, diversified into foreign securities and private markets, and, in a move almost unthinkable for a Japanese public institution, eventually handed the CEO's chair to one of those outsiders. The transition from the "ice age" of negative rates to a new world of rising Japanese yields — and the restructuring that rising rates force on a ¥230 trillion portfolio — is where the investment case lives today.

Here is the roadmap. Act I goes back to the samurai and the "second budget." Act II is the political war of the century — 小泉純一郎 Junichiro Koizumi's crusade to privatize the post office, and the snap election he bet his career on. Act III is the record-shattering 2015 triple IPO. Act IV is the negative-rate ice age and the Goldman pivot. Act V dissects the ¥230 trillion balance sheet. Act VI covers the current strategy — rising yields, restructuring, and the leap from passive investor to asset manager. And Act VII runs the skeptic's stress test and lays out, honestly, why this business might win from here and why it might not. We begin where all of it begins: with a man who invented the Japanese postal system and, almost as an afterthought, a way for a poor country to finance itself.

II. The Origins: Maejima Hisoka and the "Shadow Budget"

Picture Japan in the early 1870s. The samurai class is being dismantled, the feudal domains abolished, and a young Meiji government is trying to drag a medieval society into the industrial age in a single generation — terrified, all the while, that the Western powers circling East Asia will do to Japan what they had done to China. Into this ferment steps 前島密 Maejima Hisoka, a low-ranking former samurai with an unglamorous obsession: how information and money move through a country. Maejima had studied the British postal system, and he understood something his contemporaries missed — that the humble network of post offices could be far more than a way to deliver letters. It could be the circulatory system of a modern state.

In 1875, Maejima established 郵便貯金 postal savings, the service that would eventually be branded ゆうちょ Yūcho. The pitch was part financial engineering, part moral instruction. Ordinary Japanese — farmers, shopkeepers, widows — had no access to banks and no habit of saving. Maejima's postal savings offered them a place to put a few coins, backed by the full faith of the new imperial government, accessible in the same village office where they mailed a letter. It encouraged thrift, it built trust in the young state, and — crucially — it swept up the tiny savings of millions of people into one enormous, domestically-controlled pool of capital, exactly when a resource-poor nation needed capital to build railways and factories.

The post office as the beating heart of the town

To understand Japan Post Bank's competitive position 150 years later, you have to understand what the 郵便局 became in the Japanese imagination. In rural and small-town Japan, the post office was never merely a place to buy stamps. It was the social and financial hub of the community — often the only institution of the modern state that a villager interacted with regularly. The local postmaster was a figure of standing, frequently a hereditary role, embedded in the community for generations. The trust this generated was of a quality no private commercial bank could ever manufacture. When a Japanese saver thought of the post office, they thought of permanence, safety, and the government standing behind their money. That emotional inheritance is the single most valuable, and most underappreciated, asset on the modern bank's balance sheet.

The "second budget"

Now for the part that made postal savings genuinely powerful — and genuinely controversial. The Ministry of Finance recognized that this ever-growing pool of citizen deposits was too useful to leave idle. Through a mechanism called 財政投融資 Fiscal Investment and Loan Program, or FILP, the state institutionalized a flywheel that shaped postwar Japan. Ordinary citizens deposited yen at their local post office at government-guaranteed rates. Those deposits were funneled, automatically, to the Ministry of Finance's Trust Fund Bureau. And the state then deployed that money to build the physical Japan of the twentieth century — expressways, ports, airports, public housing, and loans to government-affiliated corporations. FILP became so large and so central that the Japanese themselves nicknamed it 第二の予算 — the "second budget." It was a shadow fiscal apparatus, funded not by taxes but by the savings of the very citizens it was ostensibly serving.

For a while, this was arguably a machine of genuine national genius: a way to mobilize domestic savings for development without borrowing from foreigners. Consider the scale of what it enabled. In the decades after the war, Japan went from a bombed-out ruin to the second-largest economy on Earth, and the physical scaffolding of that miracle — the Tōmei Expressway, the Shinkansen corridors, the network of regional airports and industrial ports — was disproportionately financed off the back of postal savings channeled through FILP. To a first approximation, the ordinary Japanese saver's passbook was a bond in the reconstruction of the nation, whether the saver understood it that way or not. The genius of the design was that it required no coercion and no visible tax: people saved because it was safe and habitual, and the state quietly borrowed their thrift to build the future.

But flywheels that face no market discipline eventually spin off the rails. By the 1980s and 1990s, FILP had become a byword for waste. Because the projects it funded did not have to earn a market return — the deposits kept flowing regardless — the system financed bridges to nowhere, redundant highways, and money-losing public corporations that no commercial lender would have touched. The pathology was structural, not incidental: when the cost of capital is effectively zero and the supply is politically guaranteed, the discipline that normally kills bad projects simply never operates. Local politicians competed to steer FILP-funded construction into their districts, a patronage machine dressed as development policy. Critics charged that the postal-savings-to-FILP pipeline crowded out private banks, propped up zombie institutions, and quietly misallocated an enormous share of national savings during exactly the years — the post-bubble "lost decade" — when Japan could least afford to waste capital. The pool of capital had grown so vast that reforming it became a first-order political question. Which brings us to the man who decided to blow the whole thing up.

III. The Battle of the Century: Koizumi's Postal Privatization

In April 2001, an unusual politician became Prime Minister of Japan. 小泉純一郎 Junichiro Koizumi had a mane of wavy grey hair, a taste for Elvis and heavy metal, and a reputation as a maverick who did not play the consensus-driven game of Japanese politics. He also had a single, career-defining obsession that he had nursed for decades: privatizing the postal system. To Koizumi, 郵政民営化 postal privatization was not one policy among many. It was, in his own framing, the mother of all reforms — the keystone that, once removed, would force the entire structure of Japan's cozy, state-directed political economy to change. His slogan captured the ideology in a phrase: from savings to investment, from public to private.

Why he wanted to break it

The economic case was, at its core, about discipline. As long as postal savings flowed automatically into FILP, the public projects it financed never had to justify themselves to anyone. Sever that link — force the deposits into a normal, privatized bank that had to earn a return — and suddenly every dam and highway would have to compete for capital on its merits. Koizumi also believed, in the abstract, that unlocking this trapped pool of capital could reinvigorate Japan's moribund financial markets and its stagnant, deflation-choked economy. The postal savings system was the largest single accumulation of household savings on Earth; freeing it was, to Koizumi, the great unfinished business of Japanese reform.

The political suicide mission

Here is what made it a war rather than a policy debate. The postal network was not just a bank and a mail service. It was the electoral machine of Koizumi's own Liberal Democratic Party. The nation's tens of thousands of postmasters — organized, respected, and rooted in every rural community — functioned as one of the LDP's most reliable vote-gathering and fundraising organizations. Asking the LDP to privatize the post office was like asking a machine to dismantle its own engine. Powerful factions within Koizumi's party regarded the plan as a betrayal, and many were prepared to sink it. This was the immovable object that had defeated every previous reformer.

The 2005 gamble

In August 2005, the confrontation came to a head. Koizumi's privatization legislation passed the lower house of the Diet by a razor-thin margin and was then rejected by the upper house — killed, in large part, by rebels within his own party.10 A conventional Prime Minister would have compromised or resigned. Koizumi did something audacious. He dissolved the lower house — which he had no constitutional need to do, since the bills died in the upper chamber — and called a snap general election, reframing the entire contest as a single-question referendum: are you for postal privatization, or against it?

Then he went to war inside his own party. Koizumi refused to endorse the LDP lawmakers who had voted against him and instead recruited high-profile challengers — celebrities, bureaucrats, business figures, dubbed 刺客 shikaku, or "assassins" — to run directly against the rebels in their own districts. It was political theater of a kind Japan had never seen, and it worked spectacularly. In September 2005, Koizumi's LDP won a crushing landslide, capturing a two-thirds supermajority in the lower house and an unambiguous mandate.10 The privatization laws passed weeks later.10 It remains one of the great demonstrations in modern democratic history of a leader betting his entire political capital on a single structural reform — and winning.

The split into four

Under Reform Minister 竹中平蔵 Heizo Takenaka — an economist and academic whom Koizumi had installed precisely because he was an outsider unbeholden to the postal lobby — the old monolithic Japan Post was broken apart on October 1, 2007, into a holding company presiding over distinct businesses. 日本郵政株式会社 Japan Post Holdings Co., Ltd. sat at the top. Beneath it: 日本郵便株式会社 Japan Post Co., Ltd., running the physical post offices and mail delivery; 株式会社ゆうちょ銀行 JAPAN POST BANK Co., Ltd., the savings bank; and 株式会社かんぽ生命保険 Japan Post Insurance Co., Ltd., the life insurer. For the first time in 132 years, the pool of postal savings had a corporate identity of its own, a balance sheet of its own, and — eventually — shareholders of its own.

It is worth pausing on how incomplete a victory this was. Koizumi left office in 2006, and the moment he did, the political tide began to turn back. When the opposition Democratic Party of Japan swept to power in 2009, it halted and partially unwound the privatization timetable, freezing share sales and softening the reform. The four-way structure survived, but the ambition to fully cut the postal system loose from the state stalled for years. This matters for investors because it establishes a pattern that still governs the stock today: postal reform in Japan advances in fits and reversals, hostage to whichever coalition holds power and to the enduring political weight of the postmasters. Separation from the state did not mean freedom. The newborn bank was handed its independence wrapped in a regulatory straitjacket, and that straitjacket would define its economics for the next two decades.

IV. Going Public and the Triple IPO

The moment Japan Post Bank became a standalone entity, Japan's private banks panicked. Imagine you are a 地方銀行 regional bank — one of the dozens of local lenders that form the backbone of provincial Japanese finance. Suddenly your new competitor is a bank with 24,000 branches, a brand every grandmother trusts, and a deposit base larger than the GDP of most countries. If that behemoth were allowed to lend freely and offer mortgages, it could vaporize the regional banking sector overnight. So the regional banks, through bodies like the 全国地方銀行協会 Regional Banks Association of Japan, lobbied ferociously for handicaps. And they got them.

The straitjacket

Two constraints, above all, defined the new bank. The first was the deposit cap: a hard regulatory ceiling on how much any single individual could park at Japan Post Bank. Originally set at ¥10 million per person, it was designed explicitly to stop the giant from hoovering up deposits from the private banks. Over time the ceiling was loosened — raised and then restructured in stages until, by 2019, an individual could hold up to ¥13 million in ordinary deposits and a further ¥13 million in other categories, for a combined ¥26 million.11 The very existence of a cap on how much a bank is allowed to accept in deposits tells you this was no ordinary institution; it was a public utility being cautiously let off the leash.

The second constraint was more fundamental: Japan Post Bank was, in effect, barred from the normal business of banking. It could not offer standard retail mortgages or make ordinary corporate loans without securing explicit approval from the Prime Minister and the Financial Services Agency — approval that the regional-bank lobby would fight tooth and nail. This is why the loan book is a rounding error to this day. The bank was born a lender in name and a bond investor in practice, legally boxed out of the very activity that makes banking profitable. Its only real way to earn money was to take the deposits and buy securities — overwhelmingly, at the time, JGBs.

The largest listing in a generation

By 2015, the government was ready to sell. On November 4, 2015, in the largest public listing Japan had seen since the privatization of Nippon Telegraph and Telephone in the 1980s, three companies debuted simultaneously on the Tokyo Stock Exchange: Japan Post Holdings (6178.T), JAPAN POST BANK (7182.T), and Japan Post Insurance (7181.T). The "triple IPO" raised roughly ¥1.4 trillion and ranked as the biggest initial public offering in the world that year.7 The banks running it read like a Wall Street who's who — and, in a detail that will matter enormously later, Goldman Sachs was among the global coordinators managing the concurrent listings.6 Japan Post Bank shares closed their first day up about 15%, a warm reception for what investors understood to be a safe, sleepy, government-adjacent dividend stock.7

And sleepy it was. At IPO, the pitch to investors was almost aggressively boring: a bank that took in retail deposits at near-zero cost and plowed the overwhelming majority — on the order of three-quarters or more of its assets — into Japanese government bonds. The appeal was stability and a dividend, not growth. In a country where investors had spent two decades starved of yield, a giant, government-linked institution throwing off a reliable payout had genuine appeal. It was a bond fund in a bank's clothing.

The 2015 listing, moreover, was only the opening move in a slow-motion privatization that is still unfolding today. The government did not sell the whole thing at once; it floated a minority and committed to grinding down the parent's stake over years. In March 2023, Japan Post Holdings executed a large secondary offering, selling roughly ¥1.3 trillion of Japan Post Bank shares and cutting its holding to below 90%, a step explicitly framed as progress toward the eventual goal of the parent owning no more than half.8 Each of these sell-downs matters to the investment case, because the bank's regulatory freedom is tied, in the government's own framework, to how far the parent's ownership falls — a thread we will pick up when we reach the present day. On the market, the bank trades as one of the larger financials on the Tokyo Stock Exchange, a widely-held blue chip whose share register is stuffed with domestic pension money and yield-seeking retail investors.12

The trouble was that the entire model rested on one silent assumption: that JGBs would keep paying a positive yield. Within ten weeks of the IPO, the Bank of Japan detonated that assumption.

V. The Kuroda Ice Age: Surviving Negative Interest Rates

On January 29, 2016, 黒田東彦 Haruhiko Kuroda, the governor of the Bank of Japan, stunned global markets by announcing that Japan would adopt a negative interest rate policy — NIRP. The idea, borrowed from Europe, was to charge banks for parking excess reserves at the central bank, forcing money out into the economy to fight the deflation that had haunted Japan for a generation. For most of the financial world it was an exotic monetary experiment. For Japan Post Bank, freshly public and built entirely around earning a spread on government bonds, it was an existential threat delivered ten weeks after the champagne of the IPO had gone flat.

The vise

To feel why NIRP was so dangerous, picture the bank's balance sheet as a simple machine with two sides. On the liability side sat well over ¥170 trillion in retail deposits — the savings of tens of millions of ordinary, often elderly, Japanese. The bank paid them almost nothing, effectively zero. But here was the trap: it could not pay them less than zero. Charging a negative interest rate to a retiree's post-office savings account would have triggered a public revolt and, quite possibly, a political crisis. Culturally and politically, the deposit rate was floored at zero. The liability side of the machine was frozen solid.

On the asset side, meanwhile, the ground was collapsing. As NIRP took hold, JGB yields cratered — the ten-year yield spent long stretches at or below zero.2 The bank's entire reason for existing was to buy those bonds and earn the gap between the near-zero it paid depositors and the modest coupon the bonds paid it. When the coupon vanished — when new government bonds paid nothing, or cost money to hold — the spread evaporated. The machine still had to pay its depositors zero, but the assets it bought no longer paid it anything at all. The gap that had funded the whole enterprise was being squeezed shut in real time.

The slow bleed

Crucially, this was not a sudden explosion but a slow, grinding asphyxiation — and understanding the mechanism matters for reading the bank even today. A bond portfolio does not reprice overnight. Japan Post Bank held a vast stock of older JGBs bought years earlier, when yields were meaningfully positive, and those bonds kept paying their higher coupons until they matured. But every year, a slice of the portfolio came due and had to be reinvested — and the only bonds available to buy were the new, zero-yielding ones. So the average yield of the portfolio ratcheted downward year after year, like a ratchet that only turns one way, as high-coupon bonds rolled off and were replaced by dead ones. Net interest margin — the core measure of a spread lender's profitability — compressed relentlessly. Management could see, with grim clarity, exactly where the trend line pointed: toward a structural decline in earnings that would continue for as long as rates stayed pinned to the floor.

There is a useful analogy here for anyone trying to grasp why this was so uniquely painful for Japan Post Bank specifically. A normal bank facing zero rates can fight back on both sides of its balance sheet — it can reprice loans, chase fee income, cross-sell insurance and cards, or push depositors toward products that still earn a spread. Japan Post Bank could do almost none of this, because the regulatory straitjacket had already amputated its lending arm and most of its product suite. It was a fighter sent into the ring with one hand tied behind its back, told to survive a monetary regime designed, in effect, to punish exactly the safe-bond strategy it had been legally steered into. The bank had done nothing reckless; it had done precisely what its charter and its regulators encouraged. And the reward for that prudence was a slow bleed. This is the deep irony at the heart of the ice age: the most conservative large bank in the developed world was among the most exposed to negative rates, not despite its caution but because of it.

The strategic conclusion was stark and unavoidable. A bank that cannot lend, cannot charge depositors, and can no longer earn a spread on government bonds has only one path to survival: it must change what it invests in. It had to move up the risk spectrum — out of dead domestic bonds and into assets that still paid a return. But Japan Post Bank, a former arm of the postal ministry staffed by career civil servants, had essentially no institutional capability to manage foreign credit, currency risk, or the byzantine world of private markets. It was a supertanker that suddenly needed to become a hedge fund, crewed by people who had spent their lives buying the single safest asset on Earth. To make that turn, it would have to import a completely different kind of brain — and it knew exactly where to shop.

VI. The Goldman Transition: Enter Takayuki Kasama and Alternative Assets

In November 2015 — the same month as the triumphant IPO, and just before Kuroda's guillotine fell — Japan Post Bank made a hire that, in hindsight, may prove more consequential than the listing itself. It recruited Takayuki Kasama, a man whose résumé was the antithesis of the postal bureaucracy he was joining. Kasama had spent his career on the sharp end of global markets. At Goldman Sachs he had risen to Managing Director by 2010 and to Head of Credit Trading by 2011, before serving as CEO and senior portfolio manager at a Singapore-based investment vehicle.3 He was a credit trader — a specialist in exactly the kind of complex, risk-priced fixed-income and alternative assets that Japan Post Bank had never touched. He joined as a Managing Director overseeing credit investments.3

Importing a new nervous system

Kasama was not a lone hire but the leading edge of a deliberate strategy: the bank went to Wall Street to buy the brains it did not have. The plan Kasama and his team executed between 2016 and the mid-2020s was, for a Japanese public institution, a quiet revolution. They began systematically rotating capital out of low- and no-yielding yen bonds and into two new frontiers. The first was foreign securities — global investment-grade corporate bonds and foreign government debt, held both hedged and unhedged, a way to capture the positive yields still available outside of Japan's frozen rate environment. The second, and more radical, was alternative investments: private equity, real estate, and infrastructure funds. The postal savings box was learning to invest like an endowment.

Becoming the world's most sought-after LP

The private-markets push turned Japan Post Bank into one of the most coveted Limited Partners on the planet — a "LP" being the passive capital-provider that commits money to funds run by professional General Partners. It is worth slowing down to explain this relationship in plain terms, because it is the heart of the modern bank. A private equity or infrastructure fund is run by a small team of dealmakers — the General Partners, or GPs — who source the deals, do the operational work, and take a cut of the profits (the famous "two and twenty": a management fee plus a share of the gains). But the GPs need someone to supply the actual money. That is the Limited Partner: a pension fund, an endowment, a sovereign wealth fund, or — in this case — a giant Japanese savings bank, which commits capital, stays passive, and collects the returns net of the GP's fees. Being a great LP requires almost the opposite temperament from running a branch network: patience measured in decade-long fund lives, the stomach to lock up billions in illiquid vehicles, and the analytical firepower to pick which GPs are worth backing.

When you control ¥188 trillion of stable, sticky retail deposits, you can write commitments at a scale that makes you a first-call investor for the world's top buyout, credit, venture, and real estate managers. A GP raising a new multi-billion-dollar fund wants an anchor investor who is enormous, reliable, and unlikely to demand its money back in a panic; Japan Post Bank was tailor-made for the role. Quietly, without the profile of a sovereign wealth fund, it became one of the great sources of institutional capital in global private markets. By March 31, 2026, the bank's "strategic investment areas" — its private equity, real estate, direct lending, and infrastructure book — had grown to roughly ¥15 trillion, from essentially nothing a decade earlier.5 The unrealized gains embedded in its private equity funds alone had swelled to about ¥1.45 trillion.5

This is the part of the story that deserves a skeptic's asterisk. Private-market marks are not the same as public-market prices — they are model-based estimates, updated with a lag, and they tend to look reassuringly smooth precisely when public markets are volatile. A ¥1.45 trillion pile of unrealized private-equity gains is real optionality, but it is also, by construction, an appraisal rather than a cash-in-hand result until the funds actually distribute. An investor should treat the alternatives book as a genuine source of return and a genuine source of opacity at the same time.

The outsider takes the throne

The most striking proof of how far the transformation had gone came in April 2024, when Takayuki Kasama was elevated to President and CEO of Japan Post Bank.3 Consider how unusual this was. Japanese public-sector-descended institutions are run by insiders — lifers who spent decades climbing the internal ladder, or retired bureaucrats parachuted in from the ministries. Handing the top job to a former Goldman Sachs credit trader who had joined less than a decade earlier was a decisive statement that the bank's identity had changed: it now saw itself, first and foremost, as an investor, and it wanted an investor in charge.

Kasama's governance profile is worth examining rather than simply praising. His compensation is tied to long-term performance through a points-based stock program, under which accumulated performance points convert into actual shares — an alignment mechanism designed to make him think like an owner over years, not quarters. And in a revealing episode, he had earlier accepted a temporary pay cut to take responsibility for compliance failures in the broader postal group, a gesture of accountability that plays well with institutional shareholders. These are constructive signals. But independent-minded investors should note the obvious tension in his seat: Kasama runs a bank whose controlling shareholder is a government-linked parent with its own, often non-commercial, priorities. A Wall Street pedigree and owner-aligned pay do not, by themselves, resolve the structural question of whom the bank is ultimately run for.

Myth vs. reality: the "Goldman takeover"

It is tempting, and the financial press has occasionally indulged the temptation, to tell this as a story of Wall Street conquering the sleepy Japanese post office — a Goldman Sachs alumnus riding in to remake a 150-year-old institution in his own image. That framing is half-true and worth puncturing. The reality is more constrained. Kasama did not stage a takeover; he was hired, promoted through the ranks over nearly a decade, and ultimately installed by a board and a parent that remain firmly in control. The board around him is still populated with figures from the old world — deputy presidents drawn from the former Ministry of Posts and Telecommunications and from legacy Japanese banking — alongside outside directors.3 The investment revolution he led is real, but it happened within the cage, not by breaking it. Kasama can change what the bank buys with its deposits; he cannot change the fact that it is barred from lending them, nor that it must rent its branches from a sister company, nor that its majority owner answers to the state. The useful mental model is not "Goldman took over the post office." It is "the post office hired a portfolio manager to make the most of a balance sheet whose fundamental terms someone else still sets." That question of who sets the terms runs straight through the balance sheet, which we turn to now.

VII. The Core Economics: Inside the ¥230 Trillion Balance Sheet

Let's open the machine up and look at the gears. As of September 30, 2025, Japan Post Bank's balance sheet stood at roughly ¥232.8 trillion in total assets.1 The liability side is almost monotonously simple, and that simplicity is the whole point: ¥188.4 trillion of deposits, of which ¥125.4 trillion sits in liquid accounts and ¥62.8 trillion in fixed-term.1 This is the cheapest, stickiest funding base in global banking — money that costs almost nothing and, as we'll see, almost never leaves. Everything interesting happens on the asset side, where that ¥188 trillion of deposits gets put to work.

Before we cross to the assets, though, sit with the liability side one more moment, because it hides the most important long-term question about the entire enterprise. That ¥188 trillion is not evenly distributed across the Japanese population; it is concentrated, disproportionately, in the hands of the elderly — the generation that came of age when the post office was the only bank worth trusting. This is what makes the deposits so gloriously sticky today, and it is also a slow-burning liability. Japan is the fastest-aging major society on Earth, its population shrinking and greying year after year. The depositors who anchor this funding base are, in the coldest actuarial sense, a wasting asset. When they pass, their savings do not automatically stay in the post office; they flow to heirs who bank on their phones, chase yield, and feel none of the inherited loyalty to a village counter. The bank has been notably quiet about how fast this generational transfer is eroding its core franchise — it is not a metric that appears cleanly in any disclosure — and that silence is itself something a careful investor should note. The greatest strength on the balance sheet and its greatest long-term vulnerability are the same line item, viewed across different time horizons.

Where the money actually goes

The old identity — the JGB buyer — is now a minority of the portfolio. At the end of September 2025, the bank held about ¥40.5 trillion in Japanese government bonds, but ¥87.8 trillion in foreign securities, including foreign bonds and investment trusts.12 Read those two numbers together and the transformation is undeniable: this is no longer a domestic-bond fund. It is a globally diversified investor whose single largest asset class is foreign securities, not the debt of its own government. Sitting alongside those are the strategic investment areas — the private markets book — and, almost as an afterthought, that famous ¥4.5 trillion sliver of loans.1 The bank has more than twenty times as much invested in foreign securities as it has lent to actual borrowers.

How it makes money

The profit engine, accordingly, looks nothing like a normal bank's. A typical lender earns most of its gross profit from net interest income on loans plus fees on retail services. Japan Post Bank earns its money from the spread between near-zero-cost deposits and the yield on its investment portfolio, supplemented by gains harvested from its market and strategic-investment activity — the redemptions and distributions from those private-equity and real-estate funds flow through as non-recurring gains.5 For the fiscal year ended March 31, 2026, net income attributable to owners rose 26.8% year on year to ¥525.5 billion, a jump the bank attributed largely to higher net interest income and strong contributions from its risk assets.5 For the six months to September 2025, net interest income had already climbed to ¥563.5 billion, up nearly ¥111 billion year on year, as the reinvestment tailwind began to bite.1 The core logic is the classic carry trade of a giant balance sheet: source funding at roughly zero, deploy it into assets yielding several percent, and earn the difference across an enormous base. When the spread widens even slightly, the earnings impact — multiplied across ¥200 trillion — is vast.

But that same leverage cuts both ways, and it is the reason a giant balance sheet is not automatically a good business. Japan Post Bank's return on equity was still running in the mid-single digits — around 4.9% for the first half of FY2026 — which is precisely the problem the current management plan exists to solve.1 A ¥230 trillion balance sheet that generates only a mid-single-digit return on its capital is, in the language of value creation, barely earning its cost of equity; it is enormous without being efficient. The whole strategic project of the past decade — the foreign securities, the alternatives, the rising-rate reinvestment, the cost cuts — can be read as one sustained attempt to close the gap between the bank's colossal scale and its stubbornly ordinary profitability. Scale, once again, is not the same thing as a moat, and it is certainly not the same thing as a good return.

The ¥300 billion tax nobody voted for

Now for the structural drag that every serious investor in this stock has to reckon with. Japan Post Bank has almost no branches of its own. It conducts the overwhelming majority of its retail business through the roughly 23,000 post offices operated by its sister company, Japan Post Co.4 For the use of that network — the counters, the clerks, the physical trust machine described back in Act I — the bank pays an enormous annual 委託手数料 agency consignment fee. In the fiscal year ended March 2026, that fee came to ¥297.8 billion, paid across to Japan Post Co.5

Sit with that figure. Nearly ¥300 billion — more than half of the bank's entire net income — flows out the door each year to its sister company. And the uncomfortable reality, from a minority shareholder's perspective, is what that money funds: the chronically unprofitable mail-and-parcel and post-office operations of Japan Post Co. The consignment fee is, in economic substance, a transfer from the bank's outside shareholders to subsidize a national postal service that loses money on its own. A skeptical investor would call it exactly what it is — a structural tax on the bank's earnings, levied to keep the letters moving in a depopulating countryside. The fee did edge down slightly year on year, from ¥302.8 billion, which management would point to as evidence of discipline.5 But it is the single largest reason the bank's returns lag what its balance sheet could otherwise generate, and no analysis of the stock is honest without it. That structural feature, in turn, shapes the competitive dynamics we examine next.

VIII. Porter's Five Forces & Hamilton Helmer's 7 Powers

Strip away the postal romance and the ¥230 trillion of assets, and ask the flinty question a strategy analyst would ask: does Japan Post Bank actually have durable competitive advantages, or is it simply enormous? Size and moat are not the same thing. Run it through Hamilton Helmer's 7 Powers and Michael Porter's Five Forces and a nuanced picture emerges — real advantages in some dimensions, real vulnerabilities in others.

The 7 Powers

Scale economies are the most obvious and the most genuine. With a ¥188.4 trillion deposit base costing essentially nothing, the bank enjoys a cost of funding that no private institution in Japan can match, and it can commit to global funds and securities at a scale that makes it a preferred counterparty.1 When you can write a €500 million commitment to a buyout fund without blinking, you get access, terms, and fee breaks that a regional bank never will. This is a real edge — though it is worth noting that scale in gathering deposits is only valuable if you can profitably deploy them, which regulation has historically prevented.

Cornered resource is the trust-laden post office network — the roughly 23,000 branches embedded in every corner of Japan, including rural and aging areas where no private bank would build.4 No competitor can replicate this physical footprint; it took 150 years and a national mandate to construct. The subtlety, of course, is that the bank does not own this cornered resource — Japan Post Co. does — and rents it back for ¥297.8 billion a year.5 It is a moat the bank pays a heavy annual toll to cross.

Switching costs are meaningfully high because of who the customers are. The core depositor is elderly, tech-resistant, physically attached to a specific local post office, and deeply inert about moving money for a few basis points of yield. This inertia is the reason ¥188 trillion of deposits sit still even at near-zero rates — a stickiness most banks would kill for. The demographic double-edge is that this customer base is, quite literally, dying off, and the open question is whether their children and grandchildren feel any of the same loyalty.

Counter-positioning is where the bank is deliberately weak, and knows it. Rather than fight the commercial megabanks — 三菱UFJ MUFG, 三井住友 SMBC, みずほ Mizuho — on corporate lending, origination, and investment banking, Japan Post Bank sidesteps that war entirely and operates as a pure-play asset allocator, an institutional LP that lets others do the hard, risky work of originating loans and deals. It is a coherent posture, but it is more an adaptation to a regulatory cage than a chosen strategic masterstroke.

The Five Forces

The threat of new entrants is essentially nil — the capital and regulatory barriers to building anything comparable are insurmountable. The bargaining power of depositors is low, for the demographic reasons above: they prioritize safety and physical access over yield, which is precisely why the bank can pay them nothing. The threat of substitutes is low-to-medium: cash remains stubbornly dominant in Japan, though digital wallets and app-based challengers are slowly nibbling at the edges of the young. Competitive rivalry is muted and oddly comfortable, because the regulatory lending limits that hobble Japan Post Bank also protect the regional banks from it — a mutual containment.

The most important force, by far, is the bargaining power of suppliers — and here the bank is genuinely captive. Its single indispensable supplier is Japan Post Co., which controls the branch network the bank cannot function without, and which extracts that ¥297.8 billion consignment fee.5 Because both companies sit under the same holding company, this is not an arm's-length negotiation between independent parties; it is a related-party transfer set by a parent balancing the interests of the whole group against those of the bank's minority owners. That is the structural knot at the center of the investment case — and it is precisely the knot that current strategy is trying to work loose.

IX. Current Strategy: The Third Act & The Rising Yield Restructuring

For the first time in almost a decade, the wind at Japan Post Bank's back has changed direction. Through 2024, the Bank of Japan finally began normalizing monetary policy, ending the negative-rate experiment and pushing Japanese interest rates up off the floor. The ten-year JGB yield, which had languished at or below zero, climbed toward and past 1.5% — territory unseen in years.2 For a giant that had spent the "ice age" watching its spread suffocate, rising domestic yields open what management frames as the "third act" of its modern history. But rising rates are a double-edged sword, and the bank is feeling both edges simultaneously.

The pain and the promise

The sharp edge first. When interest rates rise, the market value of existing low-coupon bonds falls — and Japan Post Bank sits on a colossal stock of them. As of September 30, 2025, the bank reported net unrealized losses of ¥740.2 billion on its securities portfolio after hedge accounting, with the JGB book alone carrying large unrealized losses as older, low-yielding bonds were marked down against higher prevailing rates.1 Those paper losses are the mirror image of the opportunity. Because the same rising rates mean that every yen of maturing bonds, and every yen of fresh deposit inflow, can now be reinvested into JGBs that actually pay a positive coupon again. After years of being forced to buy dead bonds, the bank can finally rebuild its yen-interest-rate portfolio at yields worth having. The bank's own framing is that it is deliberately shifting cash and low-yielding assets back into JGBs to capture the rising-rate trend.2

The investor's job is to weigh those two edges honestly. The unrealized losses are real and will pressure book value and capital if rates keep climbing, but — as we'll examine in the stress test — they are survivable given the bank's funding and liquidity. The reinvestment tailwind is also real, but it accrues slowly, bond by maturing bond, over years. This is not a switch that flips; it is the same ratchet as the ice age, now finally turning the other way.

From scale to quality

Kasama's medium-term management plan, covering the fiscal years 2026 through 2028, reframes the bank's ambition around this new environment. The headline goal is a deliberate break from the past: net income of over ¥1 trillion and a return on equity of around 10% by the plan's final year — a near-doubling of profit from the ¥525.5 billion of FY2026, and a level of profitability the bank has never sustained.45 The engine, management says, is the rebuilding of the yen-interest-rate portfolio pushing net interest income above ¥2.3 trillion, supplemented by growing returns from risk assets.4

Just as striking is the efficiency target. The plan calls for slashing the overhead ratio — costs as a share of gross profit — from 55.5% toward roughly 40% by FY2028, a dramatic improvement to be achieved through cost discipline and digital tools such as the ゆうちょ手続きアプリ Yūcho Procedures App and the Bankbook App, which push routine transactions off the expensive physical counter and onto the phone.4 Whether a bank still paying ¥300 billion a year to a branch network can actually reach a 40% overhead ratio is one of the central execution questions of the plan; it is a genuinely aggressive target, and management's credibility over the next three years will be measured against it.

On management credibility, the record so far cuts in the bank's favor, with caveats. The prior medium-term plan set relatively modest markers — a return on equity of 4% or more, an overhead ratio of 62% or less — and the bank has been clearing them: FY2026's ROE and cost ratio both landed comfortably inside those bands, and net income beat the company's own forecast.25 A management team that sets conservative targets and then exceeds them is behaving very differently from one that overpromises and misses, and the shift from the old plan's defensive goals to the new plan's ambitious ¥1 trillion / 10% ROE / 40% OHR framework reads as earned confidence rather than bravado. The caveat is that the new targets embed a large helping of macro luck: much of the projected profit growth depends on Japanese interest rates continuing to rise and the yield curve cooperating, which is a bet on the Bank of Japan's policy path, not on anything management controls. When the tailwind is doing the heavy lifting, it can be hard to distinguish skill from weather — and investors should keep that distinction firmly in mind when the next set of results comes in ahead of plan.

Up the value chain: from LP to GP

The most forward-looking piece of the strategy is the attempt to stop being merely a passive supplier of capital and start capturing the fees that its GPs earn. In April 2026, the bank established 株式会社日本郵政アセットマネジメント Japan Post Bank Asset Management Co., Ltd., formed by absorbing an existing asset-management entity, to move up the value chain — building products, forging alliances with external managers, lowering the fees it pays, and capturing a slice of the management-fee pool for itself.4 Alongside it runs the "Σ Business," a regional private-equity effort through Japan Post Bank Capital Partners, with a plan to execute roughly 60 regional deals totaling about ¥60 billion by FY2028 to channel capital into Japan's provincial economies.4 These are sensible moves that play to the bank's scale, but they are early-stage and small relative to the ¥230 trillion balance sheet; they are optionality, not yet earnings. Which brings us to the hardest question: is any of this enough to change the investment case?

X. The Investor's Stress Test & Bear vs. Bull Cases

Now put on the hat of the most skeptical investor in the room — a long/short manager or an activist — and interrogate this thing. Two challenges cut deepest.

The stress test

The first is the return question. Can minority shareholders ever earn a genuinely attractive return on equity when roughly ¥300 billion of cash is systematically drained out of the bank every year to subsidize a sister company's money-losing post offices?5 The consignment fee is not a market-set price; it is a related-party transfer, and as long as the government-linked parent needs the bank's cash to keep the national postal service afloat, an activist has limited leverage to force it down. This is the core bear thesis in one sentence: the bank may be structurally engineered to under-earn its own balance sheet for the benefit of stakeholders who are not its shareholders.

The second is the solvency question, and it deserves a careful answer because the superficial parallel is alarming. Japan Post Bank holds ¥40.5 trillion in JGBs and ¥87.8 trillion in foreign securities, and it is already carrying ¥740.2 billion in net unrealized losses; a sharp further spike in interest rates would deepen those mark-to-market losses considerably.1 Isn't this exactly the setup that killed Silicon Valley Bank in 2023 — a bank stuffed with underwater long-duration bonds? The answer is no, and the reason is the liability side. SVB died because its deposits were enormous, concentrated, uninsured, and above all flighty — a herd of venture-backed startups that fled in a coordinated digital bank run, forcing SVB to sell its bonds and crystallize the losses. Japan Post Bank's deposits are the polar opposite: ¥188 trillion spread across tens of millions of small, retail, culturally loyal, physically-anchored savers who have shown across decades that they do not move — reinforced by a controlling government-linked parent and unmatched access to central-bank liquidity.1 The unrealized losses are a real drag on capital and book value, but the mechanism that turns paper losses into a solvency crisis — a run that forces distressed selling — is precisely the mechanism this deposit base is built to resist. It is a genuine risk to earnings and equity value; it is not, on the current structure, an SVB-style existential one.

Why it could win

The bull case rests on three pillars, each testable. First, deregulation: with Japan Post Holdings having reduced its stake in the bank to 49.87% as of March 31, 2026 — below the symbolic 50% line, the culmination of the years-long sell-down that began with the IPO and continued through the 2023 secondary offering — the political conditions for finally relaxing the deposit caps and lending bans improve, which could one day let the bank compete as a real commercial lender and put its ¥188 trillion of funding to far more profitable use.589 Under Japan's privatization framework, the ownership threshold is not merely symbolic; the parent's stake falling and then eventually approaching disposal is the legal trigger that loosens the constraints on the bank's business. Crossing below 50% is the single most consequential structural event in the company's post-IPO history, and the bull case leans heavily on the government following through by actually widening the bank's permitted activities. Second, the yield tailwind: reinvesting the vast maturing portfolio into positive-yielding JGBs drives net interest income toward the ¥2.3 trillion target and lifts profit toward the ¥1 trillion goal.4 Third, the fee business: the new asset-management subsidiary and GP ambitions layer high-margin fee income on top of the balance-sheet carry.4 If even two of these three land, the bank re-rates from a sleepy dividend proxy to a genuinely growing financial franchise, and the mid-single-digit return on equity that has long defined it moves toward the double digits management now targets.

Why it might not

The bear case is the mirror image, and it is not a straw man. Deregulation may simply never come — the regional-bank lobby that built the straitjacket in the first place remains politically potent, and it has every incentive to keep the giant caged; the sub-50% stake is a milestone, not a guarantee of freedom. The consignment fee may prove permanently rigid, a non-negotiable tax set by a parent with priorities that diverge from minority shareholders'.5 And the rising-rate environment that promises the reinvestment tailwind is the same environment that threatens continued mark-to-market damage to book value and capital ratios if Japanese yields spike faster than the portfolio can roll over.1 In the bear scenario, Japan Post Bank remains what it has largely been: a colossal, cautious, structurally constrained savings box whose returns are quietly siphoned to serve national policy — the definition of a value trap.

There is also a quieter, second-layer point that both camps should weigh: capital and shareholder returns. The bank's consolidated capital adequacy ratio stood at 15.67% as of September 2025 on the domestic standard — comfortably capitalized, with room to absorb the unrealized-loss drag on its bond book without threatening its regulatory buffers.1 That capital strength is what underwrites the other half of the equity story that has always drawn investors to this stock: the dividend. Management has committed to a progressive dividend policy — growing the payout as profits grow — which, layered on a government-linked, over-capitalized institution, makes the shares function for many domestic holders as a bond substitute with upside.4 The bear would counter that a generous, reliable dividend is exactly what you would expect a controlling state-linked parent to insist upon, since it is itself a major beneficiary of those payouts — and that a fat dividend can be a way of placating minority holders precisely while the deeper structural constraints go unaddressed. A high yield is a return of capital; it is not, by itself, evidence that the underlying business is compounding value.

The honest synthesis is that this is a genuine two-sided bet whose resolution depends on politics as much as on management. Kasama can restructure the portfolio and build an asset-management arm; he cannot, by himself, repeal the deposit cap or renegotiate the consignment fee. The most important variables sit outside the CEO's control.

What to actually watch

If you follow this company, three indicators tell you almost everything — no need to compute them, just watch their direction. First, net interest income, and whether it is genuinely marching toward the ¥2.3 trillion target as the yen-rate portfolio rebuilds; this is the master gauge of whether the rising-rate thesis is working.4 Second, the overhead ratio, tracking down from 55.5% toward the promised 40% — the single clearest test of whether management can deliver the efficiency it has promised, consignment fee and all.4 Third, any change in the regulatory perimeter — a relaxation of the deposit cap, an approval to expand lending, or a meaningful renegotiation of the consignment fee. That third one is the re-rating catalyst; without it, the bank is optimizing within a cage.

Watch, too, the direction of that consignment fee itself, because it is the cleanest single read on whose interests the group is prioritizing. The modest ¥5 billion reduction in FY2026 is a data point, not yet a trend; if the fee keeps drifting down as the bank digitizes and the parent finds other ways to fund the post office, that is tangible evidence the structural tax is loosening. If it holds firm or creeps back up whenever Japan Post Co.'s mail losses widen, the bear's thesis — that the bank is run in part as a funding source for a national service — is being confirmed in real time. The beauty of these markers is that they require no forecasting model and no faith in management's rhetoric; they simply resolve, one disclosure at a time, into an answer.

XI. Playbook: Business & Investing Lessons

Step back from the ticker and Japan Post Bank offers a set of lessons that travel far beyond Japanese finance.

Trapped capital is worth more to whoever can free it. The entire modern story is about a vast, inert pool of household savings — 150 years in the accumulating — and the successive attempts to unlock it: Koizumi's political war to privatize it, the IPO to expose it to market discipline, and Kasama's investment revolution to actually earn a return on it. The recurring insight for investors is that enormous latent value can sit dormant inside a public or quasi-public institution for decades, and the catalyst that releases it is often political and structural rather than operational. The hard part is that you cannot underwrite the timing of a political catalyst the way you can a product cycle.

Governance and talent can change an institution's DNA — but not its constraints. Importing a Goldman Sachs credit trader and eventually making him CEO genuinely transformed how Japan Post Bank invests, and it is a powerful example of how the right outside brain can rewire a sclerotic organization. But it is equally a lesson in the limits of talent: a brilliant CEO cannot legislate away a deposit cap or refuse to pay a consignment fee mandated by the ownership structure. When you assess a management team, separate what they control from what they don't, and price the difference.

"Universal service" obligations are a permanent tax on the businesses that carry them. The consignment fee is the concrete expression of a broader truth: when a publicly traded company remains tethered to a national public-policy mandate — keeping the mail moving to every village — its minority shareholders subsidize that mandate whether they like it or not. Any investor in a formerly-state-owned enterprise should hunt for these obligations, because they rarely appear as a single tidy line and they almost never go away quietly.

In an aging, high-trust society, physical distribution and customer inertia remain a fortress. Perhaps the most counterintuitive lesson is that in an age of fintech and instant digital yield-shopping, the decisive competitive asset can still be a 150-year-old network of physical branches staffed by trusted local figures, holding ¥188 trillion of deposits in place with nothing more than habit and safety. Distribution and inertia are old-fashioned moats — but as long as the customer base persists, they are moats all the same. The strategic question that hangs over Japan Post Bank, and over the investment case, is the one no annual report can answer: whether the grandchildren of today's loyal depositors will keep the money in the box, or whether the fortress is slowly emptying one funeral at a time.

References

-

Selected Financial Information for the Six Months Ended September 30, 2025 — JAPAN POST BANK, 2025-11-14 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

FY2025 H1 IR Presentation — JAPAN POST BANK, 2025-11-20 ↩↩↩↩↩

-

Profile of Member of the Board of Directors (Takayuki Kasama) — JAPAN POST BANK ↩↩↩↩

-

Medium-Term Management Plan (FY2026–FY2028) Presentation — JAPAN POST BANK, 2026-05-19 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Selected Financial Information for the Fiscal Year Ended March 31, 2026 — JAPAN POST BANK, 2026-05-15 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Triple-Header: Goldman Sachs Manages the Concurrent IPOs of Japan Post Holdings, Japan Post Bank, and Japan Post Insurance — Goldman Sachs, 2015 ↩

-

Japan Post Shares Surge In World's Biggest IPO Since Alibaba — Fortune, 2015-11-04 ↩↩

-

Japan Post Holdings to sell about ¥1.3 trillion of Japan Post Bank shares — Reuters, 2023-03-01 ↩↩

-

Japan Approves Postal Privatization — The Washington Post, 2005-10-14 ↩↩↩

-

Notice Concerning Raising the Ceiling on Deposits — JAPAN POST BANK, 2019-03-13 ↩

-

JAPAN POST BANK Co., Ltd. (7182.T) Company Profile — Reuters ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube