Pentamaster: The Automation Powerhouse of the Silicon Valley of the East

I. Introduction & Episode Roadmap

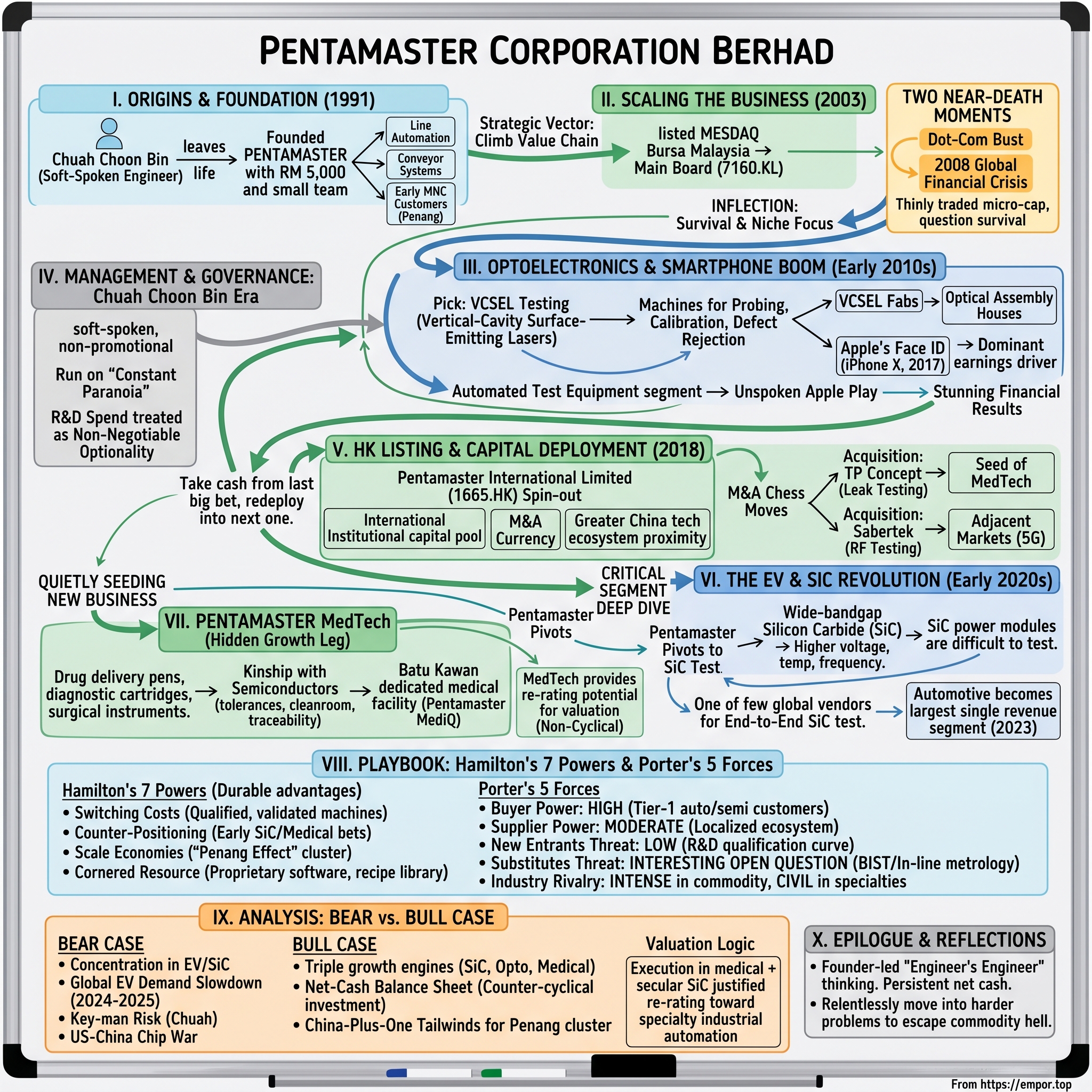

Drive twenty minutes south from George Town, past the cendol stalls of Bayan Lepas and the squat hangars of the Free Industrial Zone, and you arrive at a stretch of road that locals jokingly call "Wafer Street." It does not appear on any map. The signage tells the real story: Intel, AMD, Bosch, Broadcom, Western Digital, Lam Research, Osram, Jabil. Somewhere between the chip giants and the photonics labs, almost hiding in plain sight on Persiaran Cassia Selatan, sits a building most travelers would never notice — a tidy, low-rise complex with the green-and-blue logo of 槟杰科达 Pentamaster Corporation Berhad.1

It is one of the most consequential buildings in Southeast Asian technology that almost nobody outside Penang has heard of.

Walk inside and you find yourself surrounded by hulking machines the size of shipping containers. They look, at first, like ordinary industrial robots. They are not. These are automated test handlers — bespoke, software-rich systems that probe, calibrate, and validate the silicon brains that will end up inside iPhones, Tesla powertrains, ABB inverters, and a growing list of medical devices that quietly keep human beings alive.

The hook of Pentamaster is this: a company that started in 1991 with a founder, a small team, and roughly RM 5,000 of capital quietly became one of the very few suppliers in the world capable of providing end-to-end test solutions for 碳化硅 silicon carbide (SiC) power modules — the semiconductor heart of the electric vehicle revolution.23 If you have ever ridden in an EV, there is a non-trivial chance that one of the chips making it move was tested on a Pentamaster machine.

The numbers tell part of the story. Pentamaster is dual-listed: the parent 槟杰科达 Pentamaster Corporation Berhad trades in Kuala Lumpur as 7160.KL, and the operating subsidiary Pentamaster International Limited listed on the Hong Kong Stock Exchange as 1665.HK in 2018.4 Group revenue grew from a modest base in the mid-2010s into the hundreds of millions of ringgit, with automotive becoming the largest single segment by 2023.56 The company has consistently sat on a net-cash balance sheet — a rarity among capital-equipment makers — and has run return-on-equity figures that would make most software companies blush.

But the thesis we want to land in this episode is not about a number. It is about a posture. Pentamaster is not "an equipment maker." It is a solution architect — a company that thrives precisely when the customer's problem is too weird, too new, or too cross-disciplinary for a catalog vendor to solve. That posture explains how a small Malaysian firm ended up testing Apple's facial-recognition modules, then SiC inverters for European EV Tier-1 suppliers, and now single-use medical devices for a market that didn't exist on its income statement five years ago.

This is the roadmap. We start in the smoke-stack 1970s of Penang, when the "Eight Samurai" of American semiconductors landed in Bayan Lepas and rewrote Malaysia's industrial DNA. We meet 蔡春民 Chuah Choon Bin, the soft-spoken engineer who walked away from a comfortable corporate career to bet on local talent. We trace two near-death moments — the dot-com bust and the 2009 collapse — that forced a generalist contractor to become a precision-optics specialist. We dissect the 2018 Hong Kong listing and the M&A chess moves that followed. We unpack the EV and SiC bet, the under-appreciated medical pivot, and finish with a Hamilton Helmer powers analysis, a Porter's Five Forces walk-through, and the bull-bear case as it stands today, in April 2026.

Buckle in. By the end, you will understand why the same factory floor that once assembled mundane conveyor belts now sits at the intersection of 电动车 EVs, smartphones, and medical devices — three of the most important industrial stories of the decade.

II. Origins: The Penang "Silicon Valley" Context

To understand Pentamaster, you have to understand Penang in 1972. That year, the Malaysian federal government carved out the Bayan Lepas Free Trade Zone, offered a buffet of tax holidays, and — almost as a leap of faith — invited the American semiconductor industry to come set up packaging and test plants on a tropical island better known for laksa and beach hotels.7 The first to bite was Intel, opening its first overseas assembly facility in Penang in 1972.8 Within a decade, the locals had a nickname for the wave of multinationals that followed: the "Eight Samurai" — Intel, AMD, HP, Hitachi, Bosch, Osram, Clarion, and National Semiconductor. They did not make chips here. They packaged them, tested them, and shipped them. But in doing so, they trained a generation of Malaysian engineers in the most demanding manufacturing discipline of the late twentieth century.

One of those engineers was a young Chuah Choon Bin.

Chuah came of age in this Penang. He spent his formative engineering years inside 美国国家半导体 National Semiconductor and later at the Sime Darby industrial conglomerate, absorbing two very different cultures — the obsessive process discipline of an American chipmaker and the diversified, state-friendly capitalism of a Malaysian GLC.9 By his early thirties, he had learned a lesson the multinationals were too polite to spell out: every time the MNCs needed a custom test rig, a non-standard handler, or a small automation tweak, they had to fly an engineer in from California, Taiwan, or Singapore. The lead times were long, the costs absurd. Local Malaysian capability barely existed beyond simple jigs and fixtures.

Chuah saw the gap. In 1991, with roughly RM 5,000 of seed money and a tiny team, he founded 槟杰科达 Pentamaster.9 The company's earliest contracts were unglamorous: line automation for the same MNCs Chuah had worked with, conveyor systems, simple pick-and-place rigs. But the strategic vector was clear from day one — climb the value chain, from "copying" foreign designs to "innovating" home-grown ones.

In a country where the dominant business archetype was either a government-linked conglomerate or a family trading house, an engineer-founded automation specialist was a deeply unusual creature. Chuah did not have political patronage, palm-oil cash flow, or a real-estate land bank to fall back on. What he had was a roster of MNC customers who, slowly, learned that the local guy could ship a working machine in half the time of the imported alternative, with fewer translation errors and significantly lower spare-parts cost.

The first inflection arrived in 2003, when Pentamaster listed on the MESDAQ market of 马来西亚交易所 Bursa Malaysia (the precursor to the ACE Market) and migrated up to the Main Board in subsequent years.10 Going public was not a glamour move. It was an engineering CFO's response to a real problem: the MNC customers were demanding bigger, more sophisticated systems, and the working capital cycle for a custom automation vendor — design, build, install, validate, get paid — was punishing. Equity gave the company breathing room to take on more ambitious orders.

But the public-market debut was followed almost immediately by two near-death experiences. The dot-com bust shredded semiconductor capex globally; orders evaporated. Then came the 2008 Global Financial Crisis, which compounded the wound. Pentamaster spent much of the late 2000s as a thinly traded, sub-RM 100 million market-cap micro-cap, and at one point management openly questioned whether the generalist automation business model — selling project-based machines to whoever would buy — could survive the next downturn.

That doubt would turn out to be the company's most valuable asset. As we will see, surviving the 2009 trough forced Chuah to make the single most consequential strategic pivot in Pentamaster's history: away from generalist automation, toward 光电 optoelectronics. The next chapter of the story is the one that put Pentamaster on the global map — and, indirectly, into the device most readers are holding in their hand right now.

III. Inflection Point #1: The Smartphone & 3D Sensing Boom

If you want to understand why specialists eat generalists for breakfast, look at Pentamaster's income statement for fiscal year 2009. Revenue collapsed. Margins compressed to the point of triviality. The Penang technology corridor — the same one that had seemed bulletproof in 2007 — was suddenly a graveyard of half-finished orders and renegotiated payment terms. Chuah Choon Bin gathered his senior engineers and asked, with characteristic understatement, a brutal question: if every other automation house in Penang can do what we do, why should a customer pick us?

The honest answer was: they shouldn't. Generalist automation was a commodity. Margins would only ever go one way. The company needed a moat — a domain so specialized, so technically demanding, that customers would have to come to Pentamaster because there was nowhere else to go.

Chuah picked optoelectronics. Specifically, he picked the testing of 垂直腔面发射激光器 VCSELs (Vertical-Cavity Surface-Emitting Lasers).

For listeners who have not spent a weekend reading photonics datasheets — and that should be almost all of you — here is the simple version. A VCSEL is a tiny laser that emits light vertically out of a wafer rather than from the edge. Think of an ordinary edge-emitter as a flashlight pointing sideways out of a brick. A VCSEL is a flashlight pointing straight up out of a postage stamp. That orientation makes it cheap to manufacture in arrays, easy to test on-wafer, and astonishingly compact. By the early 2010s, VCSELs were quietly becoming the preferred light source for proximity sensing, gesture recognition, and — most importantly — 3D 感知 3D sensing modules.

3D sensing is the technology that lets your phone know your face is your face. It works by projecting a pattern of infrared dots onto a surface, capturing the reflections with a sensor, and reconstructing a depth map in real time. Apple's Face ID, launched with the iPhone X in late 2017, was the headline application. Behind it stood a sprawling supply chain of VCSEL fabs, optical assembly houses, and — critically — equipment makers capable of testing every laser, every diffractive optical element, and every assembled module to micron-level tolerances.11

This is where Pentamaster forced its way in.

The company invested years and a disproportionate share of its R&D budget into building automated test handlers for VCSELs and 3D-sensing modules — machines that could probe an array of microscopic lasers, characterize beam profile and wavelength, and reject defective parts at high throughput. The customers for this equipment were the photonics specialists supplying the world's largest smartphone vendors. Pentamaster, in turn, became what the local Penang grapevine euphemistically called "the unspoken Apple play." Management has historically been careful not to name end customers in financial disclosures, but 财经媒体 industry coverage has long identified Pentamaster as a critical, if indirect, supplier into the Cupertino supply chain.12

The financial result was stunning. Group revenue, which had limped along at modest levels through the early 2010s, accelerated sharply once the smartphone optoelectronics cycle ramped. Margins re-rated upward as the mix shifted from low-margin generic automation to high-margin precision optical testing. By the time the 2018 Hong Kong listing prospectus was filed, Pentamaster's automated test equipment segment — heavily levered to optoelectronics — was the dominant earnings driver of the group.4

The strategic lesson here is the one Chuah would repeat in every subsequent chapter of the company's life: the way to escape commodity hell is not to work harder at the commodity. It is to migrate, deliberately and at risk, into a problem so technically gnarly that very few competitors can follow. Pentamaster did not "diversify into" optoelectronics. It bet the company on it — at a moment when the consensus view in the Penang E&E sector was still that test handlers were a sleepy, mature business.

Of course, leaning the company on a single end-market — even one as glamorous as the smartphone — would have its own dangers. By the late 2010s, those dangers were already showing up in the cyclicality of phone shipments. That, more than anything, set up the next strategic pivot. But before we get there, we need to talk about the man who keeps making these bets, and the management culture he has built around them.

IV. Management & Governance: The Chuah Choon Bin Era

Walk into Pentamaster's headquarters expecting the usual founder-CEO theatrics — the curated lobby, the wall of magazine covers, the executive parking — and you will be quietly disappointed. Chuah Choon Bin, well into his late sixties, still moves through the building like a senior process engineer rather than a chairman of a multi-billion-ringgit listed group. Forbes, in a 2020 profile that came as close as the press has come to a personal portrait, described him as soft-spoken, deliberate, and almost allergic to self-promotion.13

That temperament is doing real work in the business.

Most Malaysian listed companies of Pentamaster's size live somewhere on a spectrum between two governance archetypes. On one end sit the Government-Linked Companies — the GLCs — with politically appointed boards, civil-service compensation grids, and a strong instinct for the safe move. On the other end sit the family trading houses, where the chairman is the patriarch, succession is by bloodline, and the board exists largely for administrative purposes. Pentamaster fits neither. It is unambiguously founder-led, with Chuah retaining a roughly 20% economic interest through direct holdings and family-linked vehicles, alongside his executive role.14 But it is also unmistakably engineer-run: the senior team is dominated by lifers who came up through the test-handler business, and capital is allocated with a discipline that looks more Taiwanese semiconductor than Malaysian conglomerate.

Chuah's operating philosophy can be reduced to a phrase he has used repeatedly in interviews and shareholder communications: he runs the company in a state of 常年警惕 constant paranoia. Not paranoia about competitors stealing today's deal — paranoia about today's profitable product line being obsolete in three years. The corollary is that R&D spend has consistently been treated as a non-negotiable charge, even when consensus said the cycle was about to roll over.15

That approach pays off in the form of optionality. By the time the smartphone optoelectronics cycle peaked, Pentamaster already had R&D programs running in 碳化硅 SiC test, leak testing, RF, and medical assembly. None of those programs originated as opportunistic responses to a customer RFP. They were seeded years before the revenue arrived — exactly the way 日本 Japanese precision-equipment makers like 东京电子 Tokyo Electron and 迪思科 Disco Corporation have historically operated.

The shareholding structure deserves special mention. Chuah's stake — and the stakes of his closest co-founders and family — sits high enough to align personal wealth tightly with the equity market's verdict on the company, and low enough that minority shareholders are not a footnote. Crucially, Pentamaster has been disciplined about not abusing related-party transactions, a chronic problem in Southeast Asian listed family businesses. The 2018 Hong Kong dual-listing introduced an additional layer of disclosure scrutiny under HKEX rules,4 which has kept governance hygiene at a level uncommon for a Malaysian-headquartered group.

Talent strategy is the other quiet weapon. Penang's E&E corridor has been a brutal market for senior engineers for two decades — every multinational on the island poaches relentlessly, and Singapore is a one-hour drive away. Pentamaster's response has been to lean hard into a culture of intrapreneurship, devolving meaningful P&L responsibility to segment heads and giving them latitude to chase new verticals. The MedTech business, as we will see, is the clearest example: it is run by a team that operates almost as a quasi-startup inside the parent group, with its own factory, its own commercial cadence, and its own strategic horizon.

The flip side of all this is unavoidable: Pentamaster is, in 2026, still substantially a Chuah Choon Bin company. Succession is the single most material governance question for any long-term shareholder. The company has been building bench strength below the founder for years, and the dual listing has formalized executive layers, but a true post-Chuah Pentamaster has not yet been tested. Bulls will note that the systems and the culture are now bigger than any one person. Bears will counter that the next downturn — and the next strategic pivot — will be the real proving ground.

That ongoing transition matters more than any single quarter's order book, because the next chapters of the company's story have all been driven by the same instinct: take the cash from the last big bet, and redeploy it into the next one. Which brings us, naturally, to Hong Kong.

V. Inflection Point #2: The HK Listing & Capital Deployment

By 2017, Pentamaster had a high-class problem. The optoelectronics business was throwing off cash. The Bursa-listed parent was carrying a balance sheet that looked more like a fund's than a manufacturer's — large net cash, modest leverage, and an order book stretching out comfortably. But the equity market that had supported the company through its rough years — the Malaysian small-cap market — was no longer a great fit for what Pentamaster had become. Liquidity was thin. International institutional investors barely covered the name. And the company's growth ambitions were increasingly global, with customers in Greater China, Europe, and North America.

The answer, in 2018, was a dual-listing. Pentamaster International Limited — the operating subsidiary that housed the bulk of the group's automated test equipment business — was spun out and listed on the Main Board of 香港交易所 the Hong Kong Stock Exchange under code 1665.HK.4 The parent, Pentamaster Corporation Berhad (7160.KL), retained a controlling stake.

Why bother? Three reasons, all strategic rather than financial-engineering driven.

First, capital pool diversity. Hong Kong is one of the largest, deepest, and most internationally connected equity markets in Asia. Listing there put Pentamaster on the radar of the global institutional buy-side — the long-only funds, the sovereign wealth funds, the Chinese A-share and H-share crossover investors — in a way that a standalone Bursa listing simply could not. Second, M&A currency. Acquisitions priced in Hong Kong dollars and supported by an HKEX-listed equity are a more credible weapon when negotiating with targets in Greater China or international photonics specialists. Third, proximity to the China tech ecosystem. As China's semiconductor self-sufficiency push accelerated, having a Hong Kong-listed entity created optionality around eventual partnerships, joint ventures, or supply agreements with mainland customers — without losing the regulatory benefits of a Malaysian operational base.

The capital pool itself remained conservatively managed. Pentamaster has consistently held a net cash position running into the hundreds of millions of ringgit on a group basis, even after sustained capex programs.5 That cash discipline is the foundation under everything else the company does. When the next cycle turns down — and in capital equipment, it always does — the company is positioned to keep R&D spending intact, keep paying its engineers, and (critically) shop for distressed assets while competitors are forced into retreat.

The first major M&A test of the new dual-listed structure came almost immediately, with the 2019 acquisition of TP Concept, a Penang-based specialist in 泄漏测试 leak testing equipment, for roughly RM 12 million.16 On the surface, the price tag looks small — almost trivial — for a group of Pentamaster's size. But the logic matters more than the dollar number. Leak testing is a discipline used heavily in medical devices (think: validating that a single-use device or drug-delivery component is hermetically sealed) and in high-end consumer products. The TP Concept deal was, in retrospect, the seed of what is today the MedTech segment. It was a textbook example of small, vertical, capability-driven M&A — paying a sensible multiple for technology and a team rather than paying a hype multiple for revenue.

The Sabertek acquisition, executed shortly after, expanded the group's 射频 RF (Radio Frequency) testing capability and gave Pentamaster the ability to address adjacent markets in wireless components and 5G-era equipment.17 Again, the deal sizes were measured in tens of millions of ringgit, not hundreds. The pattern is unmistakable: Pentamaster's M&A book is a series of small, thesis-driven, capability-tucks rather than transformational mega-deals. That discipline is rare. The graveyard of capital-equipment companies is full of CEOs who used a hot equity currency to overpay for a "strategic" target, only to write down the goodwill three years later.

The combination — a deep cash buffer, a dual-listed equity currency, and a disciplined acquisition cadence — gave Pentamaster the resources for what came next. Because the smartphone optoelectronics cycle, however lucrative, was always going to roll over. The question was whether the company had set up a credible second engine before the first one slowed. The answer, by the early 2020s, was an emphatic yes. And the engine had a name: silicon carbide.

VI. Segment Deep Dive: The EV & SiC Revolution

Here is the technical concept everything in this section turns on. Inside every electric vehicle is a power electronics stack — the thicket of inverters, converters, and onboard chargers that transforms the battery's DC voltage into the AC current driving the motor, and back again during regenerative braking. For two decades, that stack was built around IGBT 绝缘栅双极型晶体管 insulated-gate bipolar transistors made of silicon. They worked. They were cheap. They were also wasteful.

Silicon carbide changes the equation. SiC is a wide-bandgap semiconductor — the layperson translation is that it tolerates much higher voltages, much higher temperatures, and much higher switching frequencies than silicon. Swap the silicon IGBT in an EV inverter for a SiC MOSFET, and the vehicle gets meaningfully more range from the same battery pack, charges faster, and runs cooler. Tesla helped catalyze the trend by adopting SiC in the Model 3's main inverter back in 2017,18 and the rest of the industry has been racing to follow ever since.

So what does any of this have to do with a Penang automation house?

Everything. Because SiC parts, unlike legacy silicon, are devilish to test.

A SiC MOSFET intended for an EV inverter has to be characterized at high voltages (often 1,200 volts and up), at switching speeds far above legacy silicon, at elevated temperatures, and across a parameter set that bears almost no resemblance to a smartphone chip. The test handler that worked beautifully for a 3D-sensing module is functionally useless for SiC. You need new probe technology, new thermal control, new high-voltage isolation, new software. The market for "end-to-end SiC test solutions" — the rare vendor capable of taking a customer from wafer-level probing all the way through to packaged-module final test — is, globally, very small. Pentamaster is one of the credible names on that short list.19

The strategic decision to pivot the company aggressively toward automotive happened well before the EV conversation became a Wall Street obsession. Through the late 2010s and into the early 2020s, the company's 汽车 automotive segment migrated from "marginal contributor" to the largest single revenue line in the group, with a particularly fast acceleration as European and Chinese EV programs ramped.620 By the 2023 fiscal year, automotive comfortably crossed 50% of group revenue — an extraordinary mix shift for a company that had been a smartphone-optoelectronics story barely five years earlier.5

This is the part of the playbook that should make every investor pay attention. Pentamaster did not pivot to SiC by trying to copy somebody else's test handler. It pivoted by understanding, well in advance, that the next generation of vehicle electronics would require a fundamentally different test methodology — and by spending its smartphone-cycle profits on R&D that wouldn't show up on the income statement for years. That is the constant paranoia in action.

There are real headwinds here too, and a sober narrator has to name them. The global EV demand curve has not been the smooth hockey stick that 2021's most enthusiastic PowerPoint decks promised. Western EV adoption, in particular, slowed materially in 2024 and 2025 as price-sensitive consumers balked at higher-end pricing and as charging infrastructure rollout disappointed in some markets.21 Chinese EV producers, conversely, have been in a brutal price war that has compressed margins across the supply chain. Customers ordering test equipment have been willing to push out delivery schedules to manage their own working capital.

But the secular case for SiC content per vehicle remains intact. As legacy silicon gives way to SiC across an ever-broader band of EV applications — main traction inverters, onboard chargers, DC-DC converters, fast-charging stations — the dollar value of test equipment required per vehicle goes up, not down, even if vehicle volumes wobble. And SiC adoption is itself accelerating into industrial drives, renewable inverters, and rail traction, which broadens Pentamaster's addressable market well beyond the passenger car.

There is one more axis to this story that almost nobody outside the company is talking about. While the EV narrative was capturing every analyst's attention, Pentamaster was quietly seeding something else. Something that does not appear in the model. Something that, if it works, could re-rate the entire company.

VII. The "Hidden" Business: Pentamaster MedTech

The land in 峇都加湾 Batu Kawan does not look like much — flat, freshly graded, edged by palm-oil estates and the new wave of industrial parks that have sprung up on the mainland side of the second Penang bridge. But on a fenced-off plot here, Pentamaster has been building the physical embodiment of its longest-dated bet: a dedicated medical-grade manufacturing facility designed to do for healthcare what its Bayan Lepas facility did for semiconductors.22

The business name is Pentamaster MediQ. The thesis is straightforward and unusually patient.

Medical devices — and especially 一次性医疗器械 single-use medical devices like drug delivery pens, diagnostic cartridges, and certain surgical instruments — share a deep technical kinship with semiconductors. Both require manufacturing tolerances measured in microns. Both demand cleanroom protocols and rigorous traceability. Both are validated against regulatory regimes (FDA, MDR, PMDA) that punish defects ferociously and reward suppliers who can prove repeatable, auditable process control. The skills Pentamaster has built over thirty years in chip-test automation — high-precision motion control, vision systems, software-driven data capture, leak testing — translate astonishingly well into the medical assembly world.

The bet has three legs. First, build out the Batu Kawan facility as a dedicated medical-grade plant, separate from the semiconductor floor. Second, develop in-house capability in single-use medical device assembly — using the company's automation expertise to deliver high-throughput, high-yield assembly lines that contract pharma and device customers cannot easily build themselves. Third, expand into high-end assembly lines for pharmaceutical packaging and drug-delivery systems, where the global supplier base is dominated by a small handful of European and Japanese specialists with decade-long lead times.2223

Why does this matter so much for the equity story?

Because of how the market has been pricing Pentamaster. For most of its public life, the stock has been understood as a 周期性科技 cyclical tech name — earnings rise and fall with semiconductor capex cycles, multiples expand and compress accordingly. That framing puts a ceiling on valuation, because cyclical equipment names trade at lower multiples through the cycle than do, say, medical-technology specialists. The medical business, if it grows into something material, would force a re-rating of the consolidated entity. A medical-grade automation business with regulatory moats and recurring service revenue would deserve to be valued differently from a smartphone-test handler shop.

The numbers today are still small. The medical segment is growing off a base that contributes a single-digit percentage to group revenue, with the heaviest investment phase still ahead.5 Anyone modeling Pentamaster as a "medical device company" today would be extrapolating heroically. But anyone ignoring it entirely is missing the point. The strategic optionality is real and underwritten by a credible operational track record. And critically, the segment is being funded out of the group's own cash flow — there is no equity dilution, no leveraged acquisition, no balance-sheet risk being taken to chase the bet.

Compare this approach with what global medical-automation peers — the Swiss assembly specialists, the German cleanroom-equipment makers, the Japanese pharmaceutical packaging giants — charge for similar capabilities, and you start to see the contour of the long-term opportunity. Pentamaster is not trying to dethrone the incumbents. It is trying to build a credible, lower-cost, faster-iteration alternative anchored in a Southeast Asian manufacturing base — at exactly the moment when global pharma and medtech customers are looking to diversify their supply chains away from over-concentration in any single jurisdiction.

If even a fraction of that vision lands, the medical segment will not just be a contributor. It will be the second leg of a stool that — alongside SiC and the legacy optoelectronics business — defines the next decade of the company. And it nicely sets up the structural question every Acquired episode eventually has to ask: where does the moat come from?

VIII. Playbook: Hamilton's 7 Powers & Porter's 5 Forces

There is a temptation, when looking at a niche industrial supplier, to assume the moat is the technology itself. With Pentamaster, that would be only half-right. The technology is real, but the more durable advantages live in the layers around it. Walk through Hamilton Helmer's 7 Powers framework and the picture sharpens.

Switching Costs are the headline. A test handler integrated into a customer's manufacturing line is not a swappable component. It has been validated against the customer's process flow, integrated into the MES (manufacturing execution system), trained on by line operators, and — most importantly — qualified under the regulatory regime governing whatever end-product is being made. Swapping it out for a competitor's machine means re-validation, downtime, and risk. In semiconductors, that risk is measured in lost wafer starts. In automotive, it is measured in stalled production lines. In medical, it can mean re-filing with the FDA. The math almost always says: stick with what works.

Counter-Positioning is the more interesting power. Pentamaster's pivot into SiC and medical happened precisely when most of its automation peers were still chasing the easy money in smartphone-cycle handlers. The incumbents that owned the smartphone-test space had every incentive to milk that market for cash flow, not to retool their R&D for a fundamentally different end-market. By the time the pivot became consensus, Pentamaster had a multi-year head start in domain knowledge and customer relationships. Counter-positioning works only when the new market would cannibalize the incumbent's existing margin pool — which is exactly what shifting R&D from smartphones to SiC required.

Scale Economies show up here in a slightly unconventional form. Pentamaster does not benefit from manufacturing scale in the way a chip foundry does. It does benefit, enormously, from what you might call the Penang Effect — concentrated access to a localized supply chain of precision machining, motion components, vision modules, and contract engineers, all clustered within a thirty-minute drive of the headquarters. Recreating that ecosystem from scratch elsewhere is a multi-decade undertaking. The Free Trade Zone that produced Pentamaster also keeps producing the components and the engineering talent that make Pentamaster competitive.

Cornered Resource is harder to claim cleanly, but the company's library of customer-validated test recipes — the proprietary software, the calibration databases, the application-specific algorithms accumulated over thousands of customer engagements — functions as something close to one. A new entrant cannot simply hire away a few engineers and recreate that library; it is encoded across hundreds of installed machines.

Branding, Process Power, and Network Economies are real but secondary. The brand resonates inside the industrial customer base but means nothing in the consumer market. Process power in the form of cumulative manufacturing learning is genuine. Network effects, in the classical sense, do not really apply.

Now flip the lens to 波特五力 Porter's Five Forces.

Bargaining power of buyers is high — Pentamaster's customer base concentrates in a handful of global Tier-1s in autos, semiconductors, and consumer electronics, and those buyers are masters of the procurement game. The company mitigates this through technical uniqueness on the most demanding test problems and through relationship continuity that compounds over the years a particular machine spends on a customer's line.

Bargaining power of suppliers is moderate. Specialized components — high-precision linear actuators, vision modules, certain RF and high-voltage components — come from a relatively small set of vendors, mostly Japanese and German, who can extract some pricing power. The Penang ecosystem dilutes this somewhat by providing local alternatives for the less specialized parts.

Threat of new entrants is structurally low. The R&D and qualification timeline to enter the SiC test market or medical-grade automation is measured in years. The customers will not even take a meeting with a vendor that cannot show a credible installed base. Capital alone does not solve this — domain knowledge does, and that takes time.

Threat of substitutes is the most interesting open question. The most plausible substitution risk is not "another machine" but "different process architectures" — for instance, in-line metrology that reduces the need for end-of-line discrete test, or built-in self-test (BIST) capabilities embedded into the chip itself that displace some external test equipment. Pentamaster's product roadmap has to anticipate these architectural shifts; it cannot rely solely on staying ahead in a static problem.

Industry rivalry is intense in commoditized handler segments and surprisingly civil in the specialty segments, where customers prize technical depth over price competition. The strategic move, again, is to keep migrating up the specialty curve faster than rivals can follow.

Net the whole picture and the structural attractiveness of Pentamaster's chosen market segments is high — but it is held together by the company's willingness to keep moving. The day Pentamaster stops migrating into harder problems is the day the moat starts shrinking.

IX. Analysis: The Bear vs. Bull Case

Every Acquired episode has the moment where the analysis has to confront the inconvenient. For Pentamaster, the inconvenient comes in three flavors.

The Bear Case. The first concern is concentration. Automotive — particularly the EV power-electronics complex — has rapidly become the dominant slice of the company's revenue mix.6 That is great when EV capex is in upcycle. It is genuinely worrying if the global EV slowdown of 2024–2025 lengthens into something structural rather than cyclical.21 Western OEMs have been delaying or scaling back EV programs. Chinese EV producers have been waging a margin-destroying price war. Either dynamic, sustained, would translate into pushed-out test-equipment orders for Pentamaster's customers. The company's order book has been resilient to date, but resilience is not invulnerability.

The second concern is key-man risk. Chuah Choon Bin remains the strategic center of gravity. The company has been deliberate about building bench depth, and the dual-listing imposes governance discipline that mitigates the worst outcomes, but a transition has not been tested through a full downcycle. Investors who price the equity as if Chuah is a permanent fixture are taking a real, if quiet, risk.

The third concern is geopolitics. The intensifying US-China 半导体战 chip war — export controls, entity listings, retaliatory measures — has created a thicket of compliance requirements for any equipment maker with customers on both sides of the Pacific. Pentamaster's exposure is not catastrophic — its customer base is geographically diversified, and Malaysia is generally seen as a neutral ground — but every escalation cycle introduces new risks around shipment approvals, end-use certifications, and customer eligibility. The China Plus One strategy that has so benefited Malaysia could, in a darker scenario, give way to forced supply-chain bifurcation that would be disruptive even to the winners.

The Bull Case. The mirror image is genuinely strong.

First, the triple engine. Few peers in the global test-and-automation universe have three independent secular growth vectors stacked the way Pentamaster does: SiC and EV power electronics, smartphone and consumer optoelectronics with continued upgrade cycles into next-generation 3D sensing, and medical/single-use device automation. Most equipment companies are happy to have one secular driver. Pentamaster has three with credible roadmaps in each.

Second, the cash. A persistently net-cash balance sheet in a capital-intensive industry is a structural advantage. It means the company can keep R&D fully funded through downcycles, keep paying its engineers, keep buying small capability tucks — and let weaker competitors blink. In a sector where downturns regularly take out marginal players, a cash buffer is itself a moat.

Third, the China-Plus-One tailwind. The same geopolitical noise that creates risk also creates opportunity. As global semiconductor and medtech customers explicitly de-risk their supply chains away from over-concentration, Malaysia — and Penang specifically — has emerged as one of the most credible alternative manufacturing hubs.24 Pentamaster sits at the heart of that ecosystem.

Valuation Logic. This article does not recommend a multiple, and it does not recommend a price. But the shape of the argument is worth naming. Pentamaster has historically traded at multiples that reflect its categorization as a cyclical semiconductor equipment name. The bull thesis is that successful execution in medical, combined with the secular SiC ramp, justifies a re-rating toward the multiples accorded to specialty industrial automation businesses with structural growth and high returns on capital. The bear thesis is that the next cyclical downturn — combined with key-man and geopolitical concerns — compresses the multiple back toward the cyclical-tech average. Both thesis structures are internally consistent; the resolution depends on execution, which depends on the next several years of management decisions.

Key Performance Indicators worth tracking. Rather than drown in metrics, focus on three:

- Segment revenue mix. The single most informative number is the proportion of group revenue coming from automotive (EV/SiC) versus consumer electronics versus medical. A continued medical ramp toward double-digit share would be the clearest signal that the third leg is materializing.5

- Net cash balance. As long as net cash remains substantial relative to annual operating expenses, the company retains its capacity to invest counter-cyclically. A meaningful deterioration in cash without corresponding revenue acceleration would be the early-warning signal.5

- Order backlog and book-to-bill. In capital equipment, the income statement is a lagging indicator and the order book is a leading one. Watch sequential book-to-bill ratios disclosed in quarterly updates and management commentary.25

Hamilton Helmer's framing is that "powers" decay if not actively defended. Porter's is that structural attractiveness changes as competitors and substitutes evolve. For Pentamaster, both lenses point to the same conclusion: the company's position is genuinely strong today, but the position is earned by relentlessly moving into harder problems. The day the migration stops is the day the thesis has to be re-examined.

Which brings us, finally, to the lesson.

X. Epilogue & Final Reflections

Step back from the granular for a moment.

What we have just walked through is, in a literal sense, the journey of a company that began with roughly RM 5,000 of capital in a Penang office in 1991 and that now sits — through its dual listing and its operational reach — at the intersection of three of the most consequential industrial trends of the 2020s.9 If you had told an MNC procurement manager in 1995, watching Chuah Choon Bin's small team install a low-end conveyor system at an American chip-packaging plant, that the same company would one day be a critical supplier to the EV power-electronics complex and a credible entrant in medical device automation, the procurement manager would have laughed.

The journey itself contains the lesson, and the lesson is simple enough to fit on a single line: the way to escape commodity hell is not to work harder at the commodity. It is to migrate, deliberately and at risk, into harder problems where the margins live.

Pentamaster has executed that migration three times. Out of generalist factory automation, into smartphone optoelectronics. Out of single-end-market dependence, into automotive SiC. Out of cyclical-tech framing, into medical assembly. Each migration was funded by the cash flow of the previous one. Each was planned years before the revenue arrived. Each happened while competitors were still trying to optimize the prior generation.

That sequence is what an engineer-founded, founder-led company is supposed to look like when the founder really does run it like an engineer rather than like a finance person. The decisions have a temporal logic that you can only get from someone who has been watching the same factory floors for thirty years and who knows what is about to break before the customer asks.

The structural argument going forward is straightforward enough to state, even if its outcome is uncertain. If the 2010s were defined by the smartphone in your pocket — the device that turned a sleepy semiconductor packaging cluster in Penang into a global photonics nerve center — then the 2020s look increasingly defined by two adjacent stories. The 电动车 computer on your wheels, where the car has become a software-and-power-electronics platform that happens to also have wheels. And the tech in your body, where medical devices, drug delivery systems, and diagnostic platforms have become as software-rich and manufacturing-precise as any consumer electronics product.

Pentamaster is positioned for both. The position was earned, not granted. And whether it holds depends not on what the company has done — that is now a matter of historical record — but on whether the next generation of leadership has internalized the same constant paranoia that brought it here.

The final note worth landing is one that often gets lost in the temptation to mythologize founders. Chuah Choon Bin's most important act, looking back, may not have been any single product pivot. It may have been refusing — at every juncture where it would have been easier and more profitable in the short term to do otherwise — to let the company become merely a beneficiary of the Penang ecosystem rather than an active climber within it. The Eight Samurai came to Penang and gave Malaysia an industrial gift in 1972.78 Most beneficiaries cashed it in. A few — and Pentamaster is the cleanest example — took the gift and built something that the original givers now buy from.

That is the rare story. It is also, in a quiet way, what makes this one of the more interesting equity narratives in Southeast Asian technology heading into the back half of the decade.

References

-

Pentamaster banking on EV and medical sectors — The Star, 2024-02-26 ↩

-

Pentamaster eyes medical segment for next growth leg — The Edge Malaysia, 2023-05-15 ↩

-

Listing Prospectus — Pentamaster International Limited (1665.HK), 2017-12-29 ↩↩↩↩

-

Pentamaster International Full Year Results 2023 — HKEX, 2024-02-22 ↩↩↩

-

Tech supply chains shift to Malaysia — Financial Times, 2024-01-10 ↩↩

-

How Pentamaster became Malaysia's most valuable tech firm — The Ken (Southeast Asia), 2021-03-24 ↩↩

-

Malaysia's Automation King Chuah Choon Bin — Forbes Asia, 2020-09-02 ↩↩↩

-

Pentamaster Corporation Berhad Company Announcements — Bursa Malaysia ↩

-

Pentamaster International HK Listing and Strategy — Bloomberg ↩

-

Malaysia's Automation King Chuah Choon Bin — Forbes Asia, 2020-09-02 ↩

-

Pentamaster International Limited (1665.HK) Investor Centre ↩

-

Pentamaster Corporation Berhad Company Announcements — Bursa Malaysia ↩

-

Pentamaster International Limited (1665.HK) Investor Centre ↩

-

Pentamaster banking on EV and medical sectors — The Star, 2024-02-26 ↩

-

Pentamaster eyes medical segment for next growth leg — The Edge Malaysia, 2023-05-15 ↩

-

Pentamaster International Full Year Results 2023 — HKEX, 2024-02-22 ↩

-

Pentamaster banking on EV and medical sectors — The Star, 2024-02-26 ↩↩

-

Pentamaster eyes medical segment for next growth leg — The Edge Malaysia, 2023-05-15 ↩↩

-

Tech supply chains shift to Malaysia — Financial Times, 2024-01-10 ↩

-

Pentamaster International Limited (1665.HK) Investor Centre ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube