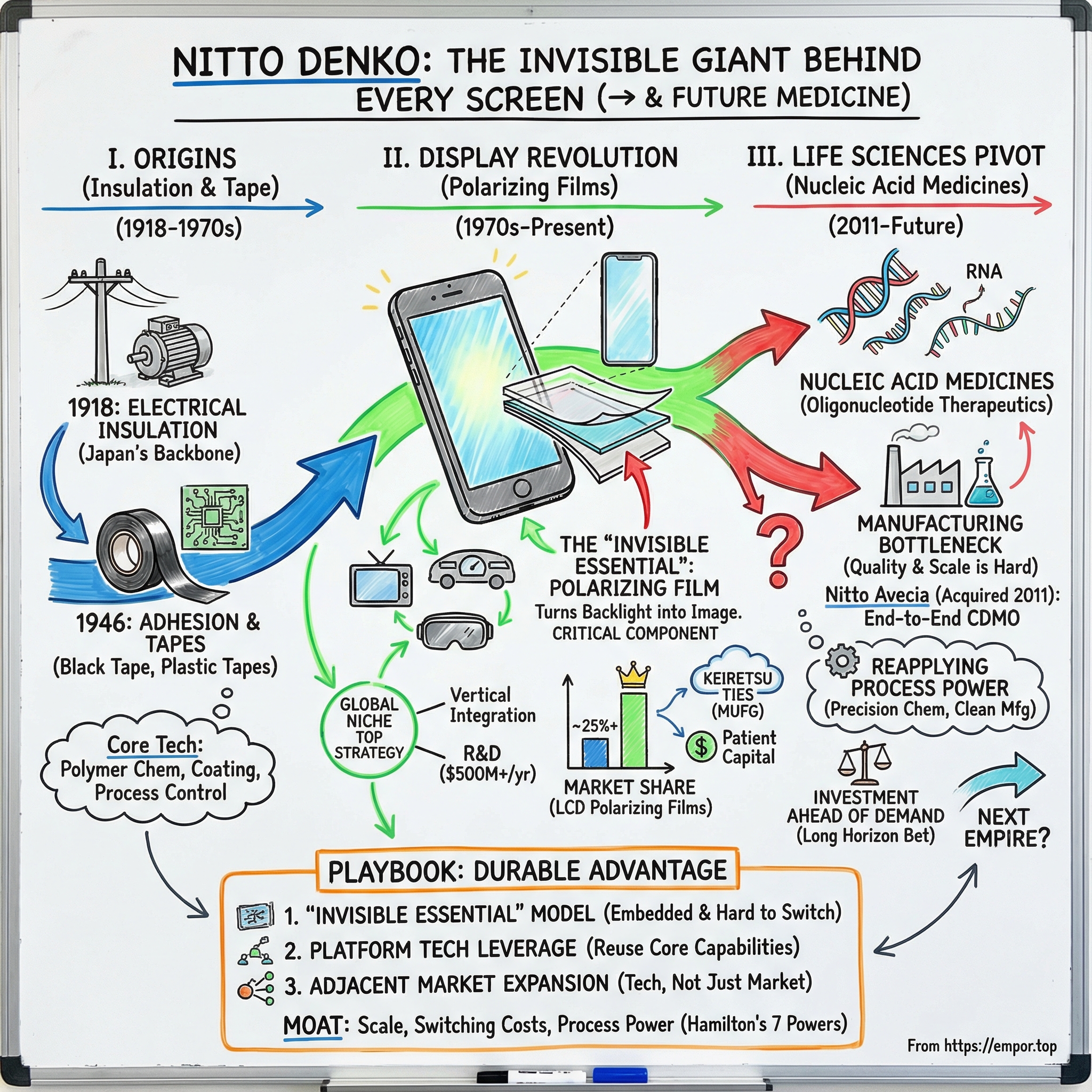

Nitto Denko: The Invisible Giant Behind Every Screen You Touch

I. Introduction & Episode Roadmap

Pick up your smartphone right now. Look at it. That bright, crisp display you’ve swiped through thousands of times would be basically unusable without a component you’ve almost certainly never heard of. Without it, you don’t get readable text or rich color. You get a glowing, washed-out rectangle.

The difference-maker is a polarizing film—so thin it’s measured in microns—that turns raw backlight into an image your eyes can actually interpret.

And there’s a very good chance that film came from Nitto Denko.

Nitto Denko, based in Japan, is widely recognized as the global leader in polarizing film for displays. It earned that position the unglamorous way: by building an unusually deep portfolio of materials technologies and then embedding itself with the world’s biggest display manufacturers through long-running, high-trust partnerships—especially in the fast-growing worlds of smartphones and TVs.

Which makes the next part even more interesting: almost nobody outside the industry knows Nitto exists.

That’s by design. Nitto Denko is an advanced materials company that wins in niches—products that look simple from the outside, but are brutally hard to make at scale with consistent quality. Today, its business spans three major areas: industrial tape, optical films, and health science materials. It sells an astonishing catalog of more than 15,000 products, and most of its revenue comes from Asia and Oceania, with Japan as the next-largest contributor.

This deep dive asks a straightforward but profound question: how does a 100-plus-year-old tape company become the invisible backbone of the global display industry—and then put itself in position to become just as important in nucleic acid medicine manufacturing?

As of 2024, Nitto maintained more than a quarter of global revenue share in LCD polarizing films. That leadership comes from two things that compound over time: vertical integration (the ability to control and optimize manufacturing end-to-end) and relentless investment in R&D—more than $500 million annually. But this isn’t just a story about screens. It’s the story of a company that has mastered a rare trick in business: becoming simultaneously invisible and indispensable.

The playbook is simple to say and hard to execute. Find a growing market. Identify a component that’s mission-critical but looks like a commodity to outsiders. Engineer it to standards competitors can’t reliably match. Then own the category while everyone else fights for attention in the flashy, consumer-facing layer.

That approach has produced a company with roughly $6.7 billion in revenue and a market capitalization above $15 billion—yet almost no consumer brand recognition. And in the fiscal year ending March 31, 2025, Nitto hit record revenue of ¥1,013.9 billion (about $6.65 billion), up 10.8% year over year, with operating profit rising 33.4% to ¥185.7 billion.

What makes this moment in the story so compelling is what Nitto is doing next. It’s placing a major bet on a very different frontier: nucleic acid medicines. The investor question is simple, and the stakes are huge: can the same capabilities that made Nitto essential to the display supply chain make it essential to the future of pharmaceutical manufacturing?

Because if the answer is yes, Nitto’s second century could be even more surprising than its first.

II. Origins: When Japan Needed to Build Its Own Industrial Backbone (1918–1945)

1918 was a brutal year to be dependent on global supply chains.

World War I had snarled trade routes and choked off imports, and Japan’s fast-industrializing economy suddenly faced a very specific, very dangerous constraint: the unglamorous materials that make electricity usable. Motors, generators, and transformers don’t run on ambition. They run on insulation—and much of Japan’s insulation supply came from overseas suppliers that could no longer deliver reliably.

That gap is where Nitto began.

On October 25, 1918, electrical engineer Tokushichi Sagawa founded the company in Osaki, Tokyo, as Nitto Electric Industrial Co., Ltd. His mission wasn’t abstract. It was straightforward: build high-quality electrical insulating materials in Japan, for Japan—so the country’s electrification wouldn’t hinge on foreign shipments arriving on time.

In the beginning, Nitto focused on the essentials: insulation materials like varnished cloth and paper, along with mica-based insulating materials and varnishes used throughout electrical equipment. The work wasn’t glamorous, but it was foundational. If you were building the electrical backbone of a modern nation, this was the stuff you couldn’t do without.

Even the name carried intent. “Nitto” signaled more than a new manufacturer—it reflected the era’s push for domestic industrial strength. In the Taishō period, Japan was rapidly shifting from a traditional society toward modern industry, and every locally produced component made the country a little more self-reliant.

The early years weren’t easy. Nitto had to secure raw materials, prove quality, and compete against established foreign suppliers. But demand was on its side: Japan’s electrical infrastructure was expanding fast, and the market needed dependable domestic production.

By 1924, Nitto moved beyond the most basic insulation products and introduced electrical insulating varnishes. It sounds like a small step, but it hinted at the company’s future. Varnishes weren’t just “materials.” They were chemistry, process control, and performance—higher value, harder to copy, and a first move toward becoming a specialty manufacturer rather than a simple supplier.

Then came World War II. Much of Japan’s industrial base was devastated, and Nitto’s central offices in Tokyo were destroyed. The company survived, and in the postwar period its headquarters later shifted to Osaka.

And that survival mattered. When the war ended, Japan faced an all-hands rebuilding effort: power grids, factories, homes, infrastructure—everything electrical needed to be remade, and all of it depended on insulation. Nitto, forged in the era when Japan first had to build its own industrial backbone, was positioned right at the intersection of necessity and capability.

III. Post-War Reinvention: From Insulation to Adhesion (1946–1970s)

In the wreckage of postwar Japan, Nitto faced a choice that would shape the next hundred years: stay an insulation specialist, or use the rebuild to become something broader—and more valuable.

In 1946, the company relocated its head office to Ibaraki, Osaka. Around the same time, it began producing “black tape.”

That product sounds almost laughably ordinary. But strategically, it was a hinge point. Tape isn’t just a strip of material. The real magic is the adhesive—getting something to stick reliably through heat, humidity, vibration, time, and abuse. That forces you into a different kind of engineering: polymer chemistry, surface science, and process control. With black tape, Nitto wasn’t just selling insulation anymore. It was learning adhesion, a capability it would reuse again and again in far more sophisticated markets.

Then came the moment that cemented that pivot. In 1951, Nitto produced Japan’s first plastic tapes. Plastic tapes weren’t new to the world, but making them domestically at industrial quality was a big deal. It meant mastering the toolkit that sits underneath modern materials manufacturing: polymer synthesis, film formation, and precision coating. Those skills would quietly become the foundation for everything Nitto would do next.

The 1960s piled on momentum. Nitto broadened its lineup—especially toward electronics—and in 1966 it began producing semiconductor encapsulating materials. The end use had changed, but the underlying need hadn’t: semiconductors still require insulation and protection. The difference was the scale and precision demanded by the emerging electronics era.

Nitto was also becoming a modern public company. By 1962 it was listed on the Second Sections of the Tokyo and Osaka Stock Exchanges, and by 1967 it had moved to the First Sections. It started planting flags overseas, too: Nitto Denko America, Inc. was established in 1968, and in 1969 the company opened its first overseas manufacturing base—Nitto Denko (Taiwan) Corporation—in the Kaohsiung Export Processing Zone.

That Taiwan move mattered more than it might have looked at the time. As electronics manufacturing spread across Asia and Japan’s labor costs rose, being close to customers became a competitive weapon. The factory in Kaohsiung was the first node in what would become a pan-Asian production network—built to follow the industry wherever it went.

And one more structural advantage sat in the background: Nitto was a member of the Mitsubishi UFJ Financial Group (MUFG) keiretsu. In postwar Japan, that web of relationships—banking ties, cross-shareholdings, long-term business partnerships—often meant something simple but powerful: stability. It gave Nitto access to patient capital and durable connections, letting it invest with a longer time horizon than companies built around constant short-term pressure.

By the end of the 1970s, the company that started as an insulation maker had something much more potent: a repeatable way to turn process know-how into specialized materials—and then scale them, quietly, alongside the world’s fastest-growing industries.

IV. The Display Revolution Bet: Flexible Circuits & Polarizing Films (1970s–1990s)

The early 1970s were the moment Nitto stopped being merely a strong specialty materials company and started becoming strategically unavoidable.

In 1973, it pioneered the production of flexible printed circuits—thin, bendable circuit boards designed for products where rigid boards simply couldn’t fit. At the time, it looked like a clever niche. In hindsight, it was Nitto getting early reps in the same kind of manufacturing discipline that would define its future: ultra-precise films, consistent quality, and production lines that could scale without falling apart.

Then, in 1975, came the decision that would shape the next half-century.

Nitto began developing and producing polarizing films for liquid crystal displays. In 1975, LCDs were still a curiosity—tiny screens in calculators and digital watches, dim and limited to simple characters. It was not obvious they’d ever become the default interface for modern life.

But Nitto’s engineers understood something structural about the technology: LCDs don’t work without polarizing film. Liquid crystals don’t create an image on their own; they manipulate light by rotating its polarization. The polarizing films—placed on either side of the liquid crystal layer—are what decide whether that light passes through or gets blocked. No polarizers, no picture.

That insight had a powerful implication. Every LCD required at least two polarizing films, and demand would grow right alongside the total display area produced worldwide. If LCDs went mainstream, polarizing film would become a massive, unavoidable bottleneck in the supply chain. And if Nitto could win that bottleneck, it wouldn’t need a consumer brand. It would be built into the product category itself.

A polarizing film is “just” an optical film that controls light to make a display readable—but its performance directly shapes screen quality. Over time, Nitto’s polarizing film technology enabled thinner displays, larger panels, and higher image quality. It ended up across the devices that would later define the era: smartphones, tablets, TVs, and vehicle displays—and it kept evolving as those products demanded more from every layer of the stack.

So why can only a handful of companies make polarizing film at the level the market demands?

Because it’s brutally hard. The film needs near-perfect optical performance across visible wavelengths. It has to hold that performance under heat from backlights. It has to be thin enough for sleek devices, but tough enough to survive years of use. And it has to be manufactured with vanishingly low defect rates—because one tiny contaminant or a slight thickness variation can show up as a visible flaw in the final screen.

Nitto spent the next two decades steadily refining its polarizer technology as LCDs expanded from calculators to laptops and desktop monitors. In 1998, it began producing Polarization Conversion Films (NIPOCS), another step in meeting the display industry’s never-ending demand for better optical performance.

One more milestone from this era is worth calling out, even though it wasn’t about screens. In 1983, Nitto introduced transdermal drug delivery patches. That move mattered less for near-term revenue and more as a signal: the company was learning how to take its core strengths—adhesives, films, and precision coating—and reapply them in totally different markets. That habit of technology reuse would become one of Nitto’s defining strategic advantages.

In 1978, Nitto went public on the Tokyo Stock Exchange, giving it more capital to invest through the long, expensive learning curve that advanced materials require.

And by 1988, the transformation was obvious enough to put into the corporate identity. The company renamed itself Nitto Denko Corporation to reflect a business that had grown far beyond electrical insulation. The “Denko”—“electric”—stayed, a nod to its roots, but by now Nitto’s real identity was something broader: a precision materials company quietly positioning itself at the critical junctions of multiple fast-growing industries.

V. Riding the Display Wave: Smartphones, Tablets & the Golden Era (2000–2015)

The smartphone revolution didn’t create the LCD polarizing film business. It put it on a rocket ship.

When Apple launched the iPhone in 2007, it set off a chain reaction across the entire supply chain. Suddenly, the display wasn’t a component anymore. It was the product. People expected vivid color, wide viewing angles, and screens they could read in bright daylight. And that raised the bar for the layers inside the panel—especially the polarizer. In smartphones, “good enough” materials show up as washed-out images, poor contrast, and ugly reflections. Only the most capable film makers could meet those specs at the volumes the world was about to demand.

This is the kind of market Nitto is built for. Its advanced materials ended up embedded throughout manufacturing supply chains whose customers are the suppliers to the OEMs—the companies building computers, smartphones, and automobiles. Nitto didn’t need to sell phones to win the smartphone era. It needed to be qualified, trusted, and ready to scale.

Then came 2008.

On December 4, 2008, Nitto’s stock hit its all-time low of 282 JPY as the global financial crisis slammed electronics demand. But the downturn didn’t change one core reality: when panel makers returned to growth, they couldn’t afford quality problems. Displays are too visible, defects are too costly, and switching materials suppliers is too risky. Coming out of the crisis, Nitto’s established relationships with major manufacturers like Samsung and LG helped it rebound with the industry—and keep its place in the most demanding part of the stack.

One snapshot of how Nitto played the game: its collaboration with 3M.

Nitto Denko and 3M jointly developed a high-durability, ultrathin LCD polarizing film—roughly half the thickness of existing products—while maintaining strong optical performance. The concept was simple and powerful: combine Nitto’s durable thin polarizer film with 3M’s ultrathin reflective polarizer.

The payoff wasn’t just “thinner.” The resulting film delivered higher brightness without sacrificing viewing angle, while also lowering power consumption compared with displays that didn’t use a reflective polarizer. That mattered because the device categories driving volume at the time—cell phones, MP3 players, and automotive displays—were all converging on the same set of requirements: thinner profiles, better durability, and more efficient screens.

More importantly, the partnership revealed something about Nitto’s strategy. It didn’t have to own every breakthrough itself. If someone else had a complementary piece of technology, Nitto was willing to co-develop, move faster, and stay focused on what it did best: polarizing film.

This era also forced a manufacturing reality check. The center of gravity in displays was shifting hard toward China, and Nitto needed to be where the growth was. The company had already formed Nitto Denko (Shanghai Pu Dong New Area) Company, Limited back in 1994, and that local footprint became increasingly important as Chinese panel makers began scaling up. Shipping polarizing film from Japan into China—then cutting and laminating it into panels—was a mismatch for the speed and cost pressure of just-in-time manufacturing.

That push only intensified later. In 2017, Nitto entered into a technical partnership contract with Hangzhou Jinjiang Group Company Ltd. to provide technological support in response to rising demand in mainland China for large-scale polarizing film used in LCD TVs. Under the agreement, Nitto would support Jinjiang’s efforts to introduce one of the world’s largest front-end polarizing film facilities in China.

Meanwhile, the technology transition everyone watched—OLED—could have been an existential threat. OLED displays are fundamentally different from LCDs. But Nitto adjusted its product lineup. NPF (Nitto Polarizing Film) is designed for displays such as OLED and LCD, with an emphasis on transparency, reliability, and workability, and Nitto also provides integrated processed products combined with various films.

And even as OLED grew, polarizers didn’t simply disappear. OLEDs still use polarizing films in certain applications to reduce reflections from ambient light. At the same time, automotive displays kept expanding as a market where LCD remained highly competitive on cost and brightness. Cars were turning into rolling screen farms—center stacks, instrument clusters, and head-up displays—pushing demand for polarizing films that could deliver anti-glare performance and wide viewing angles.

VI. The Life Sciences Pivot: Acquiring the Future of Medicine (2011–Present)

In 2011, Nitto made a move that, at the time, looked almost like a category error.

It acquired Avecia, an oligonucleotide contract manufacturer. To anyone who knew Nitto as a polarizing film powerhouse, the obvious reaction was: why would a display materials company buy a pharma manufacturer?

The answer sits in a simple pattern Nitto had followed for decades: find the next “invisible essential,” then bring its process and chemistry muscle to a market where quality and scale are brutally hard to achieve.

Oligonucleotide therapeutics—made from nucleic acids like DNA and RNA—are often described as the next generation of medicines after antibody therapeutics. They work by directly affecting gene expression, which raises the possibility of treating diseases that were previously difficult to address. As that promise started to move from theory into real commercialization efforts, manufacturing became the bottleneck. Not the science. The manufacturing.

That’s where Nitto saw the opening.

After acquiring Avecia, Nitto kept investing to build an end-to-end capability: raw material manufacturing, drug substance contract manufacturing, final formulation, drug product contract manufacturing, and analytical services. In other words, it wasn’t trying to dabble in life sciences. It was trying to become a core infrastructure provider to the companies developing these therapies.

And while “tape company buys DNA manufacturer” sounds strange, the technical overlap runs deeper than it looks. Oligonucleotide synthesis demands precision chemistry and tight process control—the same kind of hard-won know-how Nitto had accumulated through decades of polymer work in adhesives and films. The purification and processing steps echo the quality-control discipline of optical film manufacturing, where tiny inconsistencies can ruin the final product. And the clean environments required for pharma production weren’t alien either for a company already used to semiconductor-grade manufacturing standards.

Nitto Avecia built its reputation on experience and breadth. With more than 25 years in oligonucleotide development and production, it positioned itself as a partner to drug developers—and, alongside Nitto Avecia Pharma Services, it described itself as the first CMO offering a comprehensive, end-to-end oligonucleotide solution.

Then came the unmistakable signal that Nitto intended to scale this business, not just own it.

In 2021, Nitto announced it would invest roughly 25 billion yen into Nitto Denko Avecia Inc. and related group companies and facilities, aimed at significantly expanding oligonucleotide manufacturing capacity.

The timing matched the market’s direction. Early development had largely centered on rare diseases, but work toward oligonucleotide therapeutics for more common conditions—and intractable diseases like cancer—was moving toward commercialization. That shift changes everything, because commercialization isn’t just about making a molecule once. It’s about making it reliably, at scale, again and again.

At its Milford, Massachusetts headquarters, Avecia expanded process and analytical development, drawing on experience handling more than 1,200 oligonucleotide sequences to improve manufacturing process design services. It also planned a new building and production line for commercial-scale manufacturing of drug substance—capacity built explicitly for the moment therapies move from trials to sustained demand.

Nitto now describes this operation as the largest oligonucleotide manufacturing site in the world. Nitto Denko Avecia is a recognized leader in oligonucleotide development and manufacturing services, with facilities in Milford, MA and Cincinnati, OH spanning preclinical through commercial needs. Across those operations, the company has manufactured more than 1,500 oligonucleotide sequences and built a substantial late-phase portfolio.

But this pivot hasn’t been a smooth upward line.

In fiscal 2024, Nitto’s Human Life segment posted an operating loss for the second consecutive year. The core oligonucleotide contract manufacturing business ran into an uncomfortable reality: the market grew, but more slowly than expected.

That creates the classic tension of building infrastructure ahead of demand. Nitto is spending now to be ready for the future it believes is coming, while near-term profitability takes a hit. The company expected sales to increase in fiscal 2025, driven by anticipated commercial drug-related orders. And with the oligonucleotide contract manufacturing market projected to grow around 20% annually through 2030, Nitto is making up-front investments to capture demand as clinical programs expand and commercial drugs for major diseases scale.

The market forecasts are big: the global oligonucleotide synthesis market was valued at $8.9 billion in 2024, estimated at $10.5 billion in 2025, and projected to reach $24.7 billion by 2030.

So the question isn’t whether nucleic acid medicine matters. It’s whether Nitto’s edge—precision manufacturing, process control, and the willingness to invest through long learning curves—translates cleanly from the demanding world of displays into the even more complex world of pharmaceutical production.

Because if it does, this won’t be a side bet.

It’ll be Nitto’s next empire.

VII. The "Global Niche Top" Strategy: Nitto's Unique Competitive Playbook

Japanese strategy phrases can sound opaque to Western ears, but Nitto’s “Global Niche Top” idea is worth decoding—because it’s basically a plain-English description of how the company has won for decades.

The logic is simple: don’t try to be a giant in every market. Instead, pick narrow pockets inside growing markets where proprietary technology creates real separation, then take the leading share there. Become the supplier customers can’t replace, not the brand everyone recognizes.

That mindset shows up in what Nitto calls “Sanshin,” or “three new.” It’s a recurring push in three directions: develop new products, find new applications for existing products, and create new demand where none existed before. It can read like corporate language on paper, but in practice it’s a disciplined way to keep reusing the same underlying technology platforms—adhesion, coating, polymer chemistry—into the next adjacent opportunity.

Nitto has also put numbers around where it wants this to go. In its “2030 Ideal State” vision, it set targets that include reaching a 50% Niche Top sales ratio and having 40% of sales come from products certified under its PlanetFlags/HumanFlags framework by fiscal year 2025.

PlanetFlags and HumanFlags are Nitto’s internal attempt to connect ESG to the actual business, not just the annual report. Under the system, products are assessed by whether they meaningfully contribute to environmental sustainability (PlanetFlags) or human well-being (HumanFlags). If they qualify, they’re certified—and Nitto tracks how much of its revenue comes from those certified products.

The key point is that this isn’t just vague “green” messaging. By turning ESG into a certification system with targets, Nitto creates internal pressure. Product teams have to think about environmental and social impact at the design stage, and products that can’t make a credible case risk losing priority when resources get allocated.

At the company level, Nitto says it puts ESG at the core of management, aiming to solve social issues while creating economic value. It has organized its efforts around three focus domains—Power & Mobility, Digital Interface, and Human Life—where it believes its technologies can overlap and compound into “essential” products.

And hovering behind all of this is a structural advantage that makes Nitto’s playbook easier to execute: its keiretsu ties. As a member of the Mitsubishi UFJ Financial Group (MUFG) keiretsu, Nitto benefits from relationship-based business building and more patient capital than a typical standalone public company under constant quarterly pressure. That doesn’t guarantee success—but it does make it far more plausible to place long-horizon bets, like scaling oligonucleotide manufacturing, and stay the course long enough for the market to catch up.

VIII. The Modern Era: Three Focus Domains (2018–Present)

When Nitto turned 100 on October 25, 2018, it didn’t celebrate by looking backward. It used the anniversary to draw a map for the next century—organizing the company around three focus domains: Power & Mobility, Digital Interface, and Human Life.

Power & Mobility is Nitto planting its flag in two of the biggest physical transitions happening in the world: electrified transportation and renewable energy. This is where the company’s unsexy superpower—adhesion—shows up in very modern places, like battery assembly. And it’s also where Nitto’s membrane technologies matter, in applications like water purification and gas separation. As EVs scale and grid batteries become infrastructure, the premium shifts to materials that can survive high voltages, extreme temperatures, and relentless duty cycles without failing.

Digital Interface is the evolution of the business Nitto is already famous for inside the industry. Displays are still the center of gravity, but the category is getting bigger and stranger: augmented reality, virtual reality, and more advanced human-machine interfaces. Screens aren’t just on phones and TVs anymore—they’re everywhere, from car dashboards to appliances to industrial equipment. And the more contexts displays appear in, the more demand rises for high-performance optical films that keep images bright, readable, durable, and efficient.

Human Life is the domain with the biggest narrative tension, because it’s where Nitto is asking investors to believe the same company that mastered optical films can also become critical infrastructure for healthcare. It includes the pharmaceutical and medical businesses: oligonucleotide manufacturing, drug delivery patches, and diagnostic materials. It’s a continuation of the same strategy—become an “invisible essential”—but in a market where quality, regulation, and reliability are even less forgiving.

Leadership-wise, Nitto has leaned heavily on continuity. Hideo Takasaki had served as President, Chief Executive Officer, Chief Operating Officer, and Representative Director since April 2017. He joined the company in April 1978, previously served as President of Nitto Europe NV, and earned his undergraduate degree from Meiji University. He’s the archetype of the Japanese corporate leader: decades inside the organization, deep operational context, and a steady hand at the top. That kind of continuity can be a strength—but it also invites the obvious question in fast-shifting markets: can the organization adapt quickly enough?

By 2024, Nitto was signaling that it understood the need to evolve the operating model. It announced new executive roles—Chief Strategy Officer and Chief Information Officer—effective April 1, 2024. CFO Shuhei Aramaki would take on the CSO role, and CTO Masanori Honda would serve as CIO, with the explicit goal of strengthening strategic planning and digital transformation. Read between the lines and it’s clear: the old structure that worked for decades of materials manufacturing isn’t automatically built for a world where digital capabilities, data, and speed matter across everything from production to customer engagement.

That same modernizing push shows up in sustainability, too. Nitto’s 2030 greenhouse gas targets were certified as Science Based Targets (SBT), and the company received SBTi certification in 2024—positioning its emissions goals within an internationally recognized framework.

Then it went a step further and turned the ambition into a physical asset. Nitto completed construction of the group’s first CO2 zero-emission factory at its Tohoku Plant in Osaki City, Miyagi Prefecture, with operations slated to begin in the second half of fiscal 2024. The factory is designed to make maximum use of in-house renewable energy, and Nitto aims to reach net zero CO2 emissions through measures including producing and storing green hydrogen using surplus solar power. It is also working on a system described as Japan’s first to generate steam with boilers fueled by 100% hydrogen, using hydrogen gas produced from liquefied hydrogen.

What makes the Tohoku initiative especially telling is how it ties sustainability back to the life sciences bet. The Tohoku Plant, which began operating in March 1977, manufactures oligonucleotide therapeutics-related products such as NittoPhase. The newly completed factory at the site is positioned as the latest facility for these products, built to increase NittoPhase production under the concept of a “sustainable factory friendly to humans and the environment.” In other words, Nitto is trying to scale the healthcare future it’s betting on—without building it on yesterday’s emissions footprint.

IX. Playbook: Business & Investing Lessons

Nitto’s century-long run isn’t an accident. It’s a case study in how to build durable advantage in the materials world—an industry where products look simple, customers are ruthless, and mistakes show up fast.

The "Invisible Essential" Model

Some of the best businesses don’t win by being famous. They win by becoming a component that no one notices until it fails.

That’s Nitto in displays. Its polarizing films are literally invisible to consumers; their entire job is to make the screen work. But that “invisible” status is exactly what makes them strategically valuable. If you’re Apple or Samsung, you don’t casually swap polarizer suppliers. Qualification takes months, and if anything goes wrong, the defect isn’t hidden inside the device—it’s staring back at the customer from the screen.

The same pattern shows up even more strongly in life sciences. Oligonucleotide synthesis depends on validated manufacturing processes that regulators review and approve. Once a pharmaceutical company has qualified Nitto as a manufacturer, changing suppliers isn’t a sourcing decision—it’s a revalidation project. That can take years and cost millions.

Platform Technology Leverage

Nitto’s superpower isn’t one product. It’s a set of foundational capabilities—adhesion, coating, and polymer synthesis—built over more than a hundred years and carried from market to market.

So when Nitto moves into something new, like automotive displays or transdermal drug delivery patches, it isn’t starting from zero. It’s bringing the same deep, hard-earned process knowledge and applying it to a new set of requirements.

That advantage is reinforced by sustained R&D. Nitto invests around ¥50 billion a year in research and development, roughly 5% of revenue. In advanced materials, that kind of consistent spending matters because the compounding is real: better tools, better yield, better performance, deeper know-how—and a gap that gets harder to close each year.

Adjacent Market Expansion

From electrical insulation to tape, from tape to polarizing films, from films to oligonucleotide manufacturing: this is not random diversification. It’s adjacency stacking—each step close enough to leverage what Nitto already knows, but large enough to open up a new profit pool.

The key is that these were technology adjacencies, not just market adjacencies. Nitto didn’t move into pharmaceuticals simply because healthcare was growing. It moved because its polymer chemistry and precision manufacturing discipline translated into the kind of controlled, repeatable processes pharma demands.

That capability has been recognized externally, too. Nitto Denko Corporation was named one of the "Clarivate Top 100 Global Innovators 2024"—an annual list of the world’s most innovative companies and research institutions compiled by Clarivate Analytics. The program began in 2012, making 2024 its 13th year, and Nitto was selected for the 11th time.

It’s not a branding award. Clarivate’s selection is based on patent and intellectual-asset data—measuring things like patent volume, influence, success rate, global reach, and rarity. In other words, it’s a quantitative signal that Nitto’s innovation engine isn’t just active. It’s consistently world-class.

X. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

Threat of New Entrants: LOW

Polarizing film looks like a commodity until you try to make it. In reality, the global market is highly consolidated, dominated by a small set of Asian manufacturers, because the entry ticket is enormous: heavy R&D, sophisticated manufacturing facilities, and the ability to run them at high yield.

Even if a new entrant can build a plant, they still run into the real barriers. Nitto has more than a century of accumulated polymer chemistry and process know-how, and it has deep, long-standing customer relationships with major display makers like Samsung, LG, and BOE. Then comes qualification: customers don’t “test” polarizers the way they test a new accessory. They validate them over long cycles, because one mistake shows up as a visible defect on the screen. In practice, that makes “unproven supplier” a non-starter.

Bargaining Power of Suppliers: MODERATE

Nitto relies on specialty chemical inputs, but it has reduced supplier leverage through vertical integration in key areas. It also benefits from long-term supplier relationships supported by keiretsu ties, which tends to stabilize pricing and availability.

That said, not every input is equally easy to lock down. Some raw materials, particularly those used in oligonucleotide synthesis, remain potential points of vulnerability if supply tightens or pricing spikes.

Bargaining Power of Buyers: MODERATE-HIGH

Nitto sells into concentrated customer bases—major display and electronics manufacturers with huge purchasing volume and real negotiating leverage. That concentration naturally pushes buyer power up.

But there’s a counterweight: switching costs. In display and electronics supply chains, changing a critical materials supplier is a qualification-heavy engineering effort, not a quick sourcing swap. Buyers can pressure on price, but they can’t easily walk away without cost and risk. The competitive set matters here too: rivals like Sumitomo Chemical and SAMSUNG SDI hold meaningful share, backed by their own vertical integration and strong positions in consumer electronics supply chains.

Threat of Substitutes: LOW-MODERATE

OLED has reduced some LCD polarizer demand, and that substitution pressure is real. But Nitto has adapted its portfolio to serve OLED as well; NPF (Nitto Polarizing Film) is designed for displays such as OLED and LCD.

Meanwhile, in pharma, the picture is different. Nucleic acid medicines are distinguished by their mechanism of action—targeting gene expression—so they don’t have direct “drop-in” substitutes in the way a component material might.

Industry Rivalry: MODERATE

Competition is intense, but structured. The top end of the market is contested by capable incumbents like Sumitomo Chemical and SAMSUNG SDI. At the same time, Chinese manufacturers including Ningbo Shanshan and HONY have been gaining share through aggressive pricing, typically with lower gross margins.

So rivalry is rising, especially on price. But the critical limiting factor remains the same: matching Nitto’s quality, consistency, and yield at scale is still extremely hard, which keeps the fight from collapsing into a pure commodity market.

Hamilton's 7 Powers Analysis

Scale Economies: STRONG

Nitto’s scale shows up in two places that matter. It’s the largest producer of polarizing film globally, and it describes Nitto Avecia as the operator of the largest oligonucleotide manufacturing site in the world. That kind of scale improves procurement leverage, spreads fixed costs, and makes continuous manufacturing improvement easier to fund—and harder for smaller competitors to match.

Network Effects: WEAK

This is a classic B2B materials business. More customers don’t inherently make the product more valuable to other customers, so Nitto doesn’t benefit from network effects in the way software platforms do.

Counter-Positioning: STRONG

Decades of manufacturing expertise are difficult to replicate, especially for newer competitors trying to climb the yield-and-quality curve.

More interestingly, the life sciences push has shades of counter-positioning. Many traditional chemical companies would have to cannibalize existing businesses—and tolerate years of losses—to pursue the oligonucleotide opportunity as aggressively as Nitto has been willing to do.

Switching Costs: STRONG

Nitto lives in industries where switching is painful. In semiconductors and displays, long qualification cycles create lock-in, and materials are embedded into customer production lines. Changing suppliers becomes an engineering project with real operational risk.

In pharmaceutical manufacturing, switching costs can be even higher. Regulatory approvals and validation requirements mean that changing a manufacturing partner can trigger revalidation work—turning “supplier change” into a major program.

Branding: MODERATE

Nitto isn’t a consumer brand, and it doesn’t need to be. But within OEM and manufacturing circles, its reputation for quality and reliability is a real asset.

In pharmaceuticals, the Nitto Avecia name also carries weight with drug developers evaluating contract manufacturers, where credibility and execution track record matter as much as price.

Cornered Resource: STRONG

Nitto’s cornered resource is not a single patent or molecule. It’s a stack of proprietary technologies—adhesion, coating, polymer synthesis—built and refined over more than a century.

On the Avecia side, experience matters in a very specific way: process knowledge accumulated across a huge range of oligonucleotide work. Avecia’s experience handling more than 1,200 oligonucleotide sequences—now more than 1,500—represents know-how that isn’t easily bought or rushed.

Process Power: VERY STRONG

If you had to pick one “unfair advantage” that explains Nitto across generations, it’s process power.

This is the embedded organizational ability to manufacture at extreme precision: producing defect-free optical films at scale, maintaining pharmaceutical-grade cleanliness in synthesis operations, and hitting yields and consistency that competitors struggle to sustain. It’s the kind of advantage that compounds quietly—one improved process step at a time—until the gap becomes very hard to close.

XI. Bull vs. Bear Case

Bull Case

The optimistic view of Nitto starts with a simple observation: it already owns one of the most important choke points in modern electronics, and it’s trying to buy its way into another one in medicine.

In displays, Nitto Denko maintained more than a 25% global revenue share in LCD polarizing films in 2024. What’s remarkable isn’t just the size of that lead—it’s the durability. This is a market that’s been fought over for decades, and Nitto’s position has held.

And the end markets haven’t stopped expanding. Screens are proliferating beyond phones and TVs into cars, AR/VR devices, and industrial and commercial settings where readability and reliability matter. Even in mature categories, that shift toward “more displays per person” keeps demand for high-performance optical films relevant.

The LCD display polarizing film market itself was valued at about $4.3 billion in 2024 and is projected to grow to roughly $6.1 billion by 2032. That’s not hypergrowth—but it is steady expansion in a category where the leader tends to keep compounding through scale, yield, and customer lock-in.

The bigger potential upside, though, is life sciences—because the market may not be fully crediting what it would mean for Nitto to become a default manufacturer for nucleic acid medicines. The oligonucleotide contract manufacturing market is projected to grow around 20% annually through 2030, and Nitto has been investing ahead of that curve. If oligonucleotide therapeutics keep moving from rare diseases into broader indications like cardiovascular disease and cancer, manufacturing capacity and execution become the bottleneck. In that world, being the leading contract manufacturer isn’t a nice-to-have—it’s strategic real estate.

Financially, the bull case is helped by the fact that Nitto hasn’t been starving the core business to fund the future. In fiscal 2024, it reported profit attributable to owners of the parent of ¥137.2 billion, up from ¥102.7 billion the year before. It also set new records in operating profit and operating profit margin, and revenue exceeded ¥1 trillion for the first time. The story there is discipline: growing while sustaining strong profitability, even as it funds long-horizon bets.

Bear Case

The pessimistic view is less about whether Nitto is good—and more about whether the world stays kind to its two biggest profit engines.

Start with displays. Chinese manufacturers have been gaining share in polarizing film through aggressive pricing. Historically, Nitto has defended itself with quality and consistency. But the risk is straightforward: if competitors close the quality gap to “good enough” while staying meaningfully cheaper, Nitto’s premium pricing power starts to crack. That doesn’t require Nitto to lose all its share; it only requires margins to compress in a business that funds everything else.

Then there’s execution risk in pharma. Nitto’s Human Life segment posted operating losses for the second consecutive year in fiscal 2024. The main issue wasn’t that the market went away—it was that growth in oligonucleotide therapeutics came in slower than expected. That’s exactly the danger of building capacity ahead of demand: if adoption takes longer, the investment phase stretches, losses extend, and the timeline to profitability moves out.

And there are structural headwinds in the broader display ecosystem. Smartphone penetration is saturated in developed markets, and TV replacement cycles have lengthened. Automotive displays are a real growth pocket, but the volumes are smaller than consumer electronics. If consumer demand weakens for an extended period, the pressure shows up where it hurts most: Nitto’s core Optronics segment.

Key Performance Indicators to Watch

Investors monitoring Nitto should focus on three metrics that best reveal whether the moat is holding and whether the next act is actually arriving.

1. Optronics Segment Operating Margin

This is the cleanest signal for pricing power and manufacturing performance in polarizing films. If margins trend down, it’s a warning that competition or mix is pressuring the business. If margins hold steady or improve, it suggests Nitto is still earning a quality premium.

2. Human Life Segment Revenue Growth Rate

This is the heartbeat of the oligonucleotide bet. Sustained double-digit growth would suggest the market is accelerating and that Nitto’s investments are landing with customers. Flat or declining growth would imply the ramp is slower than management expected—and that losses could linger.

3. Niche Top Sales Ratio

This is Nitto’s own scoreboard: the share of revenue coming from categories where it holds the number-one position. If the ratio rises, the strategy is working—new niches are being found and owned. If it falls, it can signal erosion in existing strongholds or a failure to create the next set of “invisible essentials.”

The Nitto Denko story is ultimately about a rare kind of power: becoming invisible and indispensable at the same time. For more than a century, Nitto has embedded itself so deeply into its customers’ products that switching suppliers becomes a risk few can tolerate.

Now the company is trying to do it again—this time in pharmaceuticals.

Whether that translation works will decide if Nitto’s second century is merely a continuation of excellence in materials, or the beginning of a whole new empire built on manufacturing the next generation of medicine.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube