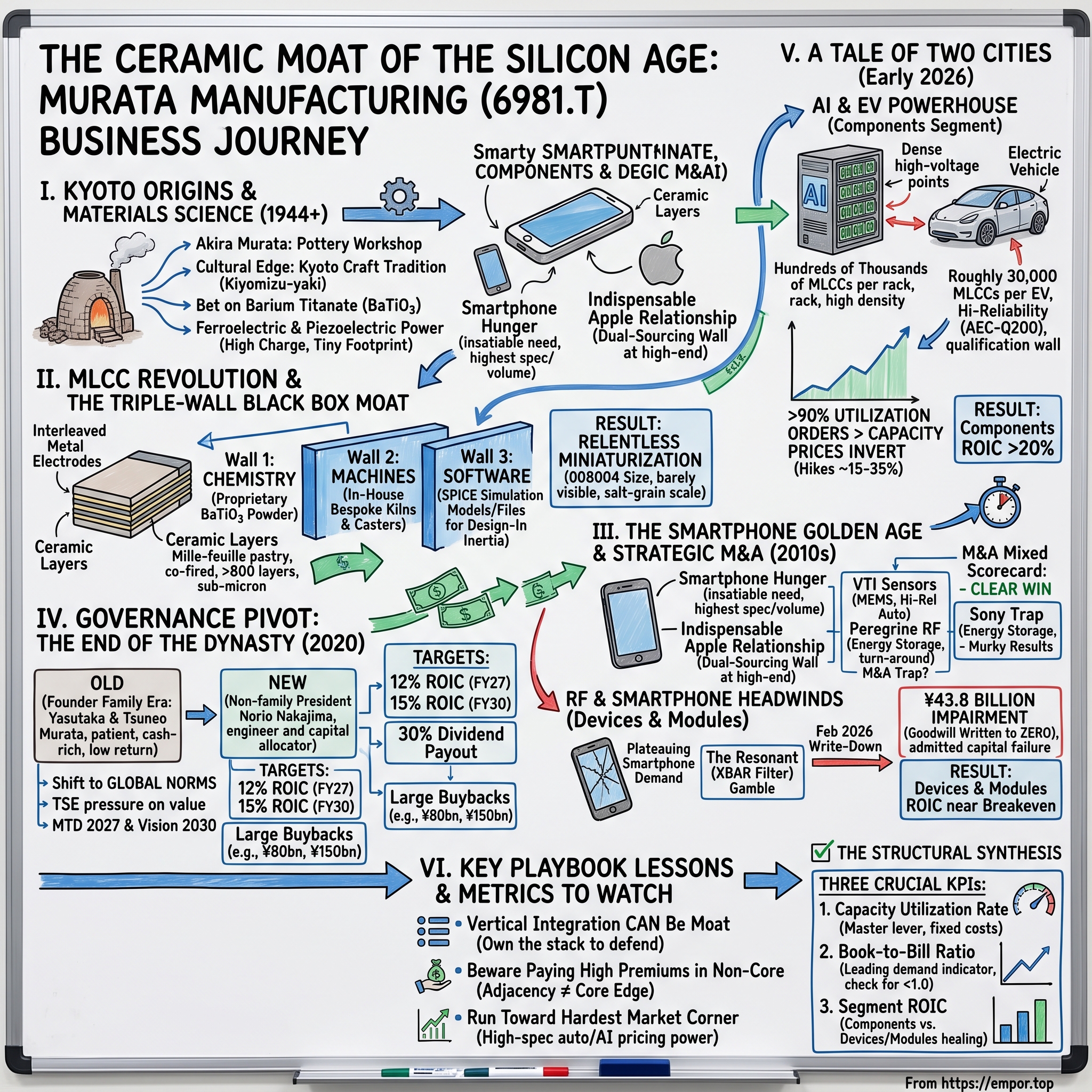

Murata Manufacturing: The Ceramic Moat of the Silicon Age

I. Introduction & Episode Roadmap

Pry the lid off a flagship smartphone and you will find the usual suspects — a processor, a camera stack, a battery. What you will not notice, because they are individually invisible to the naked eye, are the more than a thousand grey specks scattered across the board like electronic gravel. Each is a 積層セラミックコンデンサ multilayer ceramic capacitor, or MLCC: a passive component that stores a whisper of charge, filters noise out of a power line, and smooths the voltage spikes that would otherwise cook a delicate silicon chip. A single high-end handset carries well over a thousand of them.3 An electric vehicle can swallow roughly thirty thousand.22 And an AI server rack — the dense cabinets of GPUs now being bolted into data centers by the millions — can demand hundreds of thousands, with some next-generation Nvidia racks reported to need up to 450,000 MLCCs each.4

These are not glamorous parts. They cost, on average, a fraction of a cent. And yet they sit at a strange and enviable chokepoint in the world economy: nothing digital powers on without them, and one company in Kyoto makes roughly two of every five sold.

That company is 株式会社村田製作所 Murata Manufacturing Co., Ltd. — ticker 6981.T on the Tokyo Stock Exchange, a components maker with a market value north of $30 billion. Murata commands an estimated 40% of the global MLCC market, and by widely-cited industry consensus something closer to half of the high-reliability automotive segment, where a failed capacitor can mean a failed airbag or a stalled powertrain.12

Here is the paradox that makes Murata worth three hours of your attention. It manufactures a physical, passive, seemingly commoditized brick — barium titanate ceramic and metal, fired in a kiln. And yet it earns operating margins that would flatter a software company, and in early 2026 it was raising prices into a shortage rather than defending share on price. How does a firm that literally bakes dirt into capacitors end up with pricing power that looks like a network effect? And, on the other side of the ledger, how did this famously conservative, cautious, engineering-obsessed Japanese icon find itself writing off essentially the entire value of a $300 million American radio-frequency acquisition just four years after buying it?

Consider the sheer improbability of the position for a moment. In an industry — electronics components — that is supposed to be the definition of commoditization, where margins get competed to the bone and yesterday's marvel becomes tomorrow's penny part, Murata has spent eight decades doing the opposite. It grew revenue to a record of roughly ¥1.83 trillion in the fiscal year that ended in March 2026, and earned an operating margin above 15% doing it — and that was a year that included a nine-figure write-down.19 Strip out the one-time charge and the underlying components engine was humming. This is not a company that occasionally makes a good part; it is a company that has industrialized the act of being permanently one process generation ahead of everyone who wants to copy it. The interesting question for an investor is not whether that lead is real — it plainly is — but how long the specific mechanisms that produce it can hold, and what happens to a supply-side champion when its demand runs on cycles it cannot control.

Those two questions — the durable ceramic moat and the expensive silicon misadventure — frame the whole story. Over the next few hours we will trace how a wartime pottery workshop became a materials-science empire; why competitors with billions of dollars still cannot copy Murata's ceramic recipe; how Murata rode the smartphone boom to become one of Apple's most indispensable suppliers; how the founding family finally handed the keys to an outsider in 2020; how the company today lives in two very different cities — a booming AI-and-EV capacitor supercycle on one side, a bleeding smartphone radio business on the other; and finally, we will stress-test the whole thing with Porter's Five Forces, Hamilton Helmer's 7 Powers, and an honest bull-versus-bear reckoning. Throughout, the posture here is that of an independent analyst, not a cheerleader: where management makes a claim, we will ask what evidence backs it and what would prove it wrong. Let us begin where all of it began: in the kilns of Kyoto.

II. Kyoto Origins & The Materials Science of Barium Titanate

To understand Murata you first have to understand Kyoto — not the temple-and-tourist Kyoto, but the quiet industrial Kyoto that produced an improbable cluster of global deep-tech champions. In the same city you will find Murata, 京セラ Kyocera, ニデック Nidec, 任天堂 Nintendo, and 堀場製作所 Horiba. That is a staggering density of world-beating precision manufacturers for one mid-sized inland city, and it is not an accident.

Kyoto's advantage was cultural before it was industrial. For centuries the city was Japan's imperial capital and the home of its most exacting craft traditions — including 京焼 Kiyomizu-yaki, the fine ceramic and pottery work fired in the hills around the Kiyomizu temple. Firing ceramic well is a subtle art: it is about controlling temperature, timing, shrinkage, and the invisible chemistry of a material as it transforms in the heat. A potter learns, by feel and repetition, that a few degrees of kiln temperature or a slightly different clay body changes everything about how the finished piece behaves. Kyoto had, in effect, spent generations building a labor pool and a mindset obsessed with exactly the skill that twentieth-century electronics would suddenly require. When the physics of the transistor arrived, Kyoto's potters were, culturally, halfway to becoming its capacitor engineers.

There is a second, less romantic reason Kyoto bred its cluster of independents. Kyoto was spared the worst of the wartime bombing that flattened Tokyo and Osaka, and it sat outside the dense keiretsu — the interlocking corporate families — that dominated the old industrial heartlands. Kyoto's postwar entrepreneurs were, by necessity and by temperament, outsiders: they built globally-minded, technology-first, fiercely independent firms rather than becoming captive suppliers to a Tokyo conglomerate. That independence bred a distinctive management culture — patient, engineering-led, willing to invest through cycles — that you can still see in Murata, Kyocera, and Nidec today. When people talk about the "Kyoto model" of Japanese business, this is what they mean: less hierarchy, more focus, and an almost stubborn insistence on owning a defensible technical niche rather than chasing scale for its own sake.

Into this setting, in 1944 — wartime Japan, resources scarce, cities bracing for bombing — a young man named 村田昭 Akira Murata set up a small workshop in the Nakagyo ward of Kyoto.5 He was the son of a ceramics dealer, and he was not, at first, making anything you would call high technology. His roughly 150-square-meter factory turned out ceramic components and insulators — humble parts riding on the reputation of Kyoto's fired clay.5 There is no founding legend of a garage epiphany here. What there is instead is a temperament: patient, materials-first, allergic to shortcuts. Akira Murata, who lived from 1921 to 2006, ran the company he founded for decades and imprinted it with a deeply conservative, engineering-first ethos that survives to this day — a belief that the way to win was not to move fastest or shout loudest but to understand the underlying material more deeply than anyone else and to keep the resulting knowledge inside the house.5 He also, crucially, insisted on financial conservatism: a strong balance sheet, low debt, and the patience to invest through downturns when weaker rivals were forced to retrench. That combination — technical obsession plus financial caution — is the recognizable Murata personality, and it explains both the company's greatest strength (a moat built over generations) and its occasional weakness (a caution that, until the 2020 governance change, sometimes shaded into leaving shareholder value on the table). That temperament would harden into corporate doctrine.

The pivot from pottery to electronics came from a single material. In the postwar years Murata began working with barium titanate — chemical formula BaTiO₃ — a synthetic ceramic with two magical properties. First, it is a ferroelectric with an enormous dielectric constant: it can hold hundreds of times more electrical charge in a given volume than the paper, mica, or air that older capacitors relied on. Second, it is piezoelectric, meaning it physically deforms under voltage and generates voltage when squeezed — which made it useful for filters, resonators, and even the fish-finding sonar of Japan's fishing fleets.5 Think of a dielectric as a sponge for electric charge; barium titanate was a sponge that could soak up an astonishing amount of charge while taking up almost no space. That combination — high storage, tiny footprint — is the entire reason the MLCC would eventually be able to shrink to the size of a dust mote while still doing real electrical work.

It is worth dwelling on why this material choice was so strategically consequential, because it set the pattern for everything Murata would later become. A capacitor's job is to store charge; its capacitance depends on three things — the area of the plates, the distance between them, and the dielectric constant of the material sandwiched in between. You can only make plates so large in a shrinking device, and you can only push them so close together before they short out. The dielectric constant is the one lever that lets you cheat physics, and barium titanate's constant is extraordinarily high — and, being a solid ceramic, it can be stacked in wafer-thin layers in a way that liquids and papers cannot. In other words, the moment Murata bet its future on synthesizing and mastering this particular powder, it was implicitly betting that the whole future of miniaturized electronics would be written in ceramic. That bet turned out to be one of the great correct calls in postwar Japanese industry. But it also meant that Murata's destiny would forever be tied to a material that is fiendishly sensitive to impurities, grain size, and firing conditions — which is to say, a material that rewards obsessive process control and punishes everyone who lacks it.

Post-war Japan gave Murata its first great demand wave: radios, then the black-and-white and later color television boom, each set stuffed with ceramic capacitors and filters. Riding that wave, Akira Murata codified the philosophy that still hangs over the company. In its canonical wording, new quality electronic equipment begins with new quality components, and new quality components begin with new quality materials.5 Read it slowly, because it is the strategic thesis of the entire firm: Murata's answer to almost every competitive question would be to go one layer deeper down the stack than its rivals — not to the circuit, not to the component, but all the way down to the chemistry of the powder. That instinct to own the material is what built the moat we turn to next.

III. The MLCC Revolution & The "Triple-Wall" Black Box Moat

Picture the problem an engineer faces every time a chip switches. A modern processor flips billions of transistors on and off, and each flip yanks a tiny gulp of current from the power supply. Multiply that across billions of transistors and you get violent, high-frequency ripples in the voltage — spikes and sags that can crash or destroy the chip. What the chip needs is a local reservoir sitting right next to it, ready to dump charge in a nanosecond to fill a sag and soak up a spike. That reservoir is the MLCC. This is why capacitor count scales relentlessly with chip complexity: every new generation of faster, hungrier, more numerous chips needs more little reservoirs packed closer to it.

An MLCC achieves its capacity through a beautiful piece of geometric brute force. Rather than one big slab of dielectric, you stack hundreds of wafer-thin ceramic layers, interleaving them with metal electrodes like an impossibly fine mille-feuille pastry, then fire the whole stack into a single solid block smaller than a grain of sand. More layers means more capacitance in the same footprint. Murata has pushed high-end designs past 800 stacked layers, each one thinner than a micron — thinner than a red blood cell — co-fired at well over 1,000°C without a single layer cracking, warping, or letting its electrodes drift out of alignment.26

To appreciate how hard that is, picture the manufacturing sequence. You cast the barium-titanate powder into a slurry and spread it into "green tape" only a couple of microns thick — flexible, unfired, and about as forgiving as wet tissue paper. You screen-print electrode patterns of metal onto that tape, stack hundreds of printed sheets in perfect registration, press them into a monolithic block, dice the block into thousands of individual chips, and then fire the whole batch in a kiln. Here is the diabolical part: the ceramic and the metal electrodes shrink by different amounts and at different rates as they sinter, and they are chemically eager to react with each other at high temperature. If any of it goes wrong — a fractionally misaligned layer, a stray void, a temperature gradient across the kiln — the part cracks, delaminates, or simply fails its electrical test, and you throw it away. Doing this at high yield, on parts you cannot even see without magnification, at a rate of trillions of units a year, is the entire game. It is closer to a controlled chemical reaction than to conventional assembly, and it is why "just build a factory" is not a viable competitive strategy.

So here is the trillion-unit question: MLCCs are, technically, an old and open technology. Why haven't lower-cost Chinese and Taiwanese makers simply commoditized Murata's high-end business the way they commoditized so much else in electronics? The answer is what we can call a triple-wall black box moat — three reinforcing barriers, each of which is individually hard and collectively close to insurmountable at the top end of the market.

Wall one, the chemistry. Murata does not buy commercial ceramic powder off a shelf. It synthesizes its own barium titanate in-house and dopes it with a proprietary cocktail of rare-earth and additive elements that stabilize the crystal, prevent it from degrading under voltage and heat, and let it fire at the right temperature.26 Crucially, the exact recipe is a trade secret, not a patent. That is a deliberate choice with teeth: a patent buys you twenty years of protection in exchange for publishing your recipe for the world to read. By keeping the formula unpatented, Murata trades legal protection for permanent opacity. A rival cannot simply read the filing and copy it, because there is no filing — there is only decades of accumulated, undocumented process knowledge locked inside the company.

Wall two, the machines. Stacking sub-micron ceramic sheets in perfect registration and firing them without defects is not something you can buy your way into with a purchase order to an equipment vendor. Murata designs and builds much of its own production machinery — the sheet-casters, the stackers, the sintering kilns — through an in-house machinery division. A competitor buying standard off-the-shelf equipment is, almost by definition, buying the same equipment everyone else has, and therefore cannot reach the yields and tolerances Murata's bespoke line achieves. The machine and the material co-evolve; you cannot copy one without the other.

Wall three, the software lock-in. This is the subtlest and, for investors, the most interesting, because it is the closest thing a passive-component maker has to the switching costs that make software businesses so durable. Murata gives circuit designers free, high-fidelity simulation models — SPICE models and S-parameter files — that describe exactly how each Murata component will behave in a real circuit across temperature, voltage, and frequency. Design engineers build their entire board simulation around these specific parts. Ripping out a Murata capacitor and dropping in a competitor's means re-running weeks of expensive validation to prove the board still behaves. That is a classic switching cost, and it operates precisely where it matters most — at the design-in stage, before a single unit is ordered. Once a Murata part is baked into a validated design that has passed qualification, the customer has every incentive to keep buying it for the life of the product; switching mid-stream saves fractions of a cent per part and risks re-opening a validation nightmare. Inertia, in other words, is monetized.

Notice how the three walls reinforce one another rather than merely stacking. The chemistry is what makes the miniaturization possible; the bespoke machines are what let the chemistry be manufactured at yield; and the simulation models are what get that specific, hard-to-copy part locked into the customer's design so the whole investment pays off in volume. A rival could conceivably chip away at any one wall in isolation — buy better powder, license better equipment, publish its own SPICE library — but it would still face the other two, and it would face all three simultaneously against a company that has been compounding the advantage for seventy years. This is why the phrase "black box" is apt: outsiders can see the inputs (ceramic, metal) and the outputs (a working capacitor), but the transformation in between is opaque, undocumented, and embodied in people and machines that do not leave the building.

The visible trophy of all this is the relentless march of miniaturization. The industry has shrunk case sizes from the once-standard 0805 (2.0 × 1.25 mm) down to 01005 (0.4 × 0.2 mm), and Murata went on to demonstrate the world's first 008004 part — a barely-believable 0.25 × 0.125 mm, smaller than a grain of salt.67 To handle parts that small is itself an engineering feat: they are placed by machines at tens of thousands of units per hour, and a human being who sneezes near an open reel can scatter a fortune of inventory across a cleanroom floor. Each shrink is a fresh gauntlet that leaves slower rivals a generation behind, because reaching the next size down demands thinner green tape, finer powder, and tighter process control all at once — the very things the triple wall protects. That generational lead is not an abstraction; it is exactly what let Murata turn the smartphone, the most demanding high-volume product of the modern era, into a goldmine.

IV. The Smartphone Golden Age & Strategic M&A

The smartphone did something no previous product had done to the capacitor business: it made a mass-market consumer device that was insatiably hungry for the very highest-spec, smallest, most reliable MLCCs on Earth — and then it sold in the billions. A modern high-end 5G phone packs more than a thousand MLCCs into a space that must also hold a battery, a camera array, and a screen.3 The physics of that are unforgiving: to cram a thousand-plus capacitors into a slim handset, you need the smallest cases, the highest capacitance-per-volume, and near-zero failure rates. That is precisely the corner of the market where Murata's triple wall is tallest — and so, as smartphones went vertical, so did Murata.

Being designed into the flagship phones of the world's most demanding customers — Apple foremost among them — was the making of Murata's modern financials. Through the 2010s the company routinely posted operating margins in the range that consumer-hardware suppliers can only dream about, because it was selling scarce, hard-to-make parts into a product with enormous unit volumes and a customer who cared more about reliability than about shaving a tenth of a cent.

The Apple relationship deserves a moment, because it illustrates a subtle point about where power sits in a supply chain. Apple is famous for squeezing suppliers — it dual-sources aggressively, audits costs ruthlessly, and is quite happy to design a partner out of the next generation. Yet for the smallest, highest-capacitance MLCCs, Apple's leverage runs into a wall: there are only a handful of firms on Earth that can make the parts at the required spec and volume, and Murata is the biggest of them. When your product needs a component that only two or three companies can supply, the ruthless-buyer playbook loses much of its bite. The relationship was symbiotic rather than adversarial: Apple's insatiable demand for smaller, better parts pulled Murata's roadmap forward, funding the very R&D and capacity that widened Murata's lead over everyone else. Being Apple's supplier was not just profitable; it was a forcing function that made Murata harder to catch. The dependency, of course, ran both ways — and a concentration of revenue in a single, cyclical consumer product is exactly the vulnerability that would later bite.

But the smartphone was also a trap, and Murata knew it. The business was gorgeously profitable and brutally cyclical. Every capacitance and miniaturization lead is perishable, which meant Murata had to plow enormous sums back into new plants and new process nodes just to stay ahead of Samsung Electro-Mechanics and the Taiwanese and Chinese challengers. High margins and high capital intensity at the same time is an uncomfortable combination: it means you are running hard just to stay in place, and any demand air-pocket leaves you with expensive, underutilized fabs. The cyclicality of that model is a theme we will return to when we reach the two-cities section.

To escape the gravity of a single volatile end-market, Murata went shopping — and its acquisition record is a genuinely mixed scorecard that tells you a lot about the company's edges and its blind spots.

The clear win was VTI Technologies, the Finnish MEMS sensor specialist Murata bought and closed in early 2012, reportedly for around €190 million.10 Rebranded Murata Electronics Oy, it gave Murata a world-class capability in 3D micro-electromechanical sensors — the tiny accelerometers and gyroscopes that sense motion and tilt. This turned out to be a home run precisely because it played to Murata's strengths: high-reliability, physically-engineered components for demanding automotive-safety and even medical applications like cardiac pacemakers, where a false reading can be lethal and the qualification barriers are correspondingly severe. It was, in essence, buying more of what Murata was already great at — precision physical components for applications that cannot tolerate failure — and it gave the company its principal manufacturing foothold outside Japan. The logic of the deal has aged well because the underlying advantage was the same one Murata already possessed: mastery of a hard physical process that customers cannot afford to see fail.

The more ambitious, and more revealing, moves pushed Murata up the stack into active silicon — and here the record turns instructive. In 2014 it acquired San Diego's Peregrine Semiconductor for $471 million, at $12.50 a share, and folded it into a new subsidiary, pSemi.11 By the time of the deal Murata was already Peregrine's dominant customer, so the acquisition was partly a defensive move to lock up a supplier it depended on. Peregrine's prize was RF-on-silicon (RF SOI) switch technology — the guts of the radio-frequency front-end that connects a phone to the cellular network, the part of the phone that decides which of the dozens of frequency bands to talk on. The strategic logic was verticalization: own more of the phone's radio, not just its decoupling capacitors, and ride the same 4G-then-5G content-growth wave from a second position on the board. It was a coherent thesis. But it also planted Murata's flag in active semiconductors — a world of rapid design cycles, ferocious competition from the likes of Qorvo, Broadcom, and Skyworks, and customer concentration in the very smartphone market whose growth was destined to plateau.

Then in 2016 Murata signed a definitive agreement to absorb 索尼 Sony's struggling lithium-ion battery operations, a deal completed on September 1, 2017.1213 The battery business was strategically defensible on paper — energy storage for wearables and IoT devices, a natural adjacency to a components maker whose customers were building ever-smaller connected gadgets — and it came cheaply, because Sony was effectively offloading a money-losing unit. But cheap-and-strategic assets often come with a reason they were cheap: the battery operation arrived with thousands of employees, restructuring baggage, and thin returns that would drag on Murata's consolidated numbers for years, a reminder that turning around someone else's unloved business is rarely as easy as the entry price suggests.

The pattern across these three deals is the analytical takeaway, and it will sharpen dramatically later: when Murata bought deeper into materials and precision physical components — VTI's sensors — it won, because it was extending an advantage it already owned. When it bought into active silicon and volatile, customer-concentrated ecosystems — Peregrine, and later Resonant — the results got murkier, because its materials-and-machines moat simply does not travel into a domain where the competitive game is design speed and software, not ceramic chemistry. Managing that widening, increasingly heterogeneous portfolio — capacitors and sensors and RF silicon and batteries, each with a different competitive logic — would eventually demand a different kind of leadership and a harder-edged capital discipline than a founding family, however capable, had ever been asked to provide.

V. The Governance Pivot: The End of the Dynasty

For seventy-six years, the name on the door and the name in the chairman's seat were the same. Akira Murata founded the company; his eldest son Yasutaka led it; and his second son, 村田恒夫 Tsuneo Murata, ran it as president from 2007 to 2020.14 This is the classic architecture of the Japanese founder-family firm — long horizons, deep institutional patience, and a culture that treats the company almost as a multi-generational stewardship rather than a quarterly earnings machine. Those are real strengths for a business whose core asset is decades of accumulated process knowledge. They are also, to a certain kind of global investor, a governance risk: family control can blur the line between what is good for the company and what is comfortable for the family.

On March 13, 2020, Murata's board announced the change that ended the dynasty. Effective from the shareholders' meeting that June, Tsuneo Murata would step up to Chairman and Representative Director, and 中島規巨 Norio Nakajima — then a senior executive vice president — would become President and Representative Director.14 The company's own release framed it in the neutral language of Japanese corporate ritual, but the wider significance, as the Financial Times reported at the time, was hard to miss: this was, in effect, the first time a non-family professional would run Murata, a deliberate step to strengthen governance as the founding family loosened its grip.15

Who is Nakajima? He is a career Murata engineer and manager, a lifer who rose through the components business rather than a parachuted-in outsider — which matters enormously, because Murata's entire moat is tacit knowledge, and an outsider with no feel for ceramic chemistry or the culture of the factory floor would have been culturally rejected by the organization within a year. This is the crucial distinction that makes Murata's transition different from the celebrity-CEO hirings you sometimes see in Western turnarounds. Murata did not import a management consultant to shake up the engineers; it promoted an engineer and asked him to think like a capital allocator. The DNA stayed; the grammar changed.

And the grammar needed changing, because Murata carried the classic afflictions of the great Japanese industrial. Global institutional investors welcomed the transition precisely because it promised to address the so-called "Japan discount" — the persistent tendency of Japanese companies to trade at lower valuations than comparable Western peers, rooted in habits that destroy shareholder value: hoarding mountains of idle cash on the balance sheet, tolerating chronically low returns on capital in the name of stability, cross-holding shares in customers and suppliers, and communicating with investors in a fog of ritual understatement. For a company as operationally excellent as Murata, these were not fatal flaws — but they were a self-imposed ceiling on the returns shareholders actually received. The broader context helps: this was the era in which the Tokyo Stock Exchange itself began publicly pressuring companies trading below book value to improve capital efficiency, and Japanese corporate governance was, slowly and unevenly, being dragged toward global norms. Murata's 2020 handover was both a company-specific event and a small piece of that much larger national story.

Under Nakajima, Murata put hard, public numbers on itself. Through its Medium-Term Direction 2027 and Vision 2030 frameworks, management committed to a post-tax return on invested capital of at least 12% by fiscal 2027, rising to at least 15% by fiscal 2030, and set a dividend payout target of 30% of profit.16 It went further, tying executive incentives to ROIC and to carbon-reduction targets — a way of signaling that capital discipline and sustainability were now management's problem, not just the board's aspiration. On shareholder returns, the company moved from talk to cash: in 2024 it launched buybacks materially larger than in its cautious past, including an ¥80 billion repurchase announced in April and a ¥150 billion buyback-and-cancellation program shortly after.25 (Note for the record: this is a considerably bigger commitment than the modest buybacks of the family era, and it is the kind of capital-return behavior activists had long wanted from cash-rich Japanese industrials.)

Why does ROIC, specifically, sit at the center of the new framework? Because it is the one metric that a capital-intensive manufacturer cannot fake. A company like Murata can always buy growth — build more fabs, acquire more companies, chase more revenue — but every yen of that growth consumes invested capital, and if the returns on that capital do not clear the company's cost of capital, the growth actively destroys value even as the top line rises. Anchoring the whole organization, and executive pay, to return on invested capital is management's way of saying: we will not grow for growth's sake, and we will not let our engineers' pride in building things override the arithmetic of whether those things earn their keep. For a firm whose history is a story of engineers being handed near-unlimited license to build, that is a genuine cultural shift, and a healthy one.

Here is the analytical caution, though, and it is the neutral-platform point at the heart of how this story should be read: setting a 12% ROIC target and framing incentives around it is a promise, not an achievement, and promises are cheap when the AI cycle is filling your order book. The real test of the framework is not what it does in a boom — anyone can hit return targets when demand outruns capacity — but whether it imposes discipline in a downturn, and whether management is willing to admit, in public and in real time, when its own capital bets have failed. As we will see, a meaningful slice of Murata's invested capital was about to be exposed as value-destroying in the most visible way imaginable, and how the new leadership handled that moment tells you more about its credibility than any target ever could. That admission arrived in early 2026.

VI. A Tale of Two Cities: AI & EV Powerhouse vs. RF & Smartphone Headwinds

By the fiscal year that ended in March 2026, Murata was living a genuine tale of two cities. In one, demand was so hot that customers were queued up begging for capacity; in the other, an entire acquisition was being written down to zero. Both cities showed up in the same set of financial statements, and understanding the tension between them is the key to the whole investment case.

City One: The AI Server and EV Boom

Start with the boom, which lives inside Murata's Components segment — the standard, catalog capacitors and inductors that go into everything. The demand driver here has shifted, almost overnight, from consumer gadgets to industrial infrastructure. A traditional server might use on the order of a thousand capacitors. An AI server built around power-hungry GPUs uses something like 10,000 to 20,000 per unit — and Murata's own investor-day figures for the latest AI baseboards run higher still.1 Scale that up to a full high-density AI rack and the numbers become almost comic: hundreds of thousands of MLCCs per cabinet, with some next-generation racks reported to require up to 450,000.4 The reason is physics, not fashion: the more power a GPU draws and the faster it switches, the more local charge reservoirs it needs packed around it, and AI accelerators are the most power-dense chips ever mass-produced.

The second engine is the car, and it is arguably the more durable of the two because it is less prone to the boom-bust whipsaw of the tech-hardware cycle. Electric and increasingly automated vehicles run high-voltage architectures — often several hundred volts — and every one of those volts has to be filtered and stabilized by capacitors that can survive a decade of heat, vibration, and moisture without failing, meeting punishing standards like AEC-Q200. The reliability bar here is a different universe from consumer electronics: a capacitor that fails in a phone is an annoyance, while one that fails in a braking system or an airbag controller is a recall, a lawsuit, and potentially a fatality. That is precisely why the automotive tier is such fertile ground for Murata — the qualification process is so long, so expensive, and so unforgiving that carmakers, once they have designed in a supplier they trust, are extraordinarily reluctant to switch. A modern EV can use on the order of 30,000 MLCCs, an order of magnitude more than a combustion car of a generation ago, as electric powertrains, battery-management systems, and driver-assistance sensors multiply the number of circuits that need decoupling.22 And critically, these are exactly the high-reliability parts where Murata's moat is deepest and where cheap commodity capacitors simply cannot qualify — the automotive segment is where the third wall, that long qualification gauntlet, is effectively fused to the first two.

The two engines together produce something Murata has rarely enjoyed: demand growth that is structural rather than merely cyclical, and concentrated in exactly the highest-margin corner of the product line. This is the heart of the bull thesis, and it deserves to be stated precisely rather than cheered. The claim is not simply "demand is up." The claim is that the composition of demand is migrating permanently away from consumer gadgets — where content per device is mature and price competition is fierce — toward AI infrastructure and electrified vehicles, where content per unit is exploding and the reliability requirements lock out commodity competitors. If that compositional shift is real and lasting, it changes the character of Murata's earnings, making them both higher and steadier. If it turns out to be a cyclical sugar-high dressed up as a structural shift, the same fixed costs that are producing gorgeous margins today will produce ugly ones tomorrow. That is the single most important open question in the entire investment case, and no one — not management, not the bulls — can yet prove which it is.

The economic consequence of these two engines running at once was visible in Murata's operating posture, and it is worth slowing down to understand why utilization matters so much for a business like this. An MLCC fab is an enormous fixed cost — the kilns, the cleanrooms, the bespoke machinery all have to be paid for whether they run at 60% or 95%. Every incremental unit produced once the plant is built carries a very low marginal cost, so the difference between a plant running at 70% and one running at 95% is not a linear 25% more profit; it is dramatically more, because those last units are almost pure margin. This is the operating leverage that makes component makers so volatile — heavenly on the way up, brutal on the way down. Through the 2025–2026 cycle, by industry reporting Murata's MLCC lines were running at roughly 90–95% utilization, with orders reported to run well ahead of available capacity.18 That is the top of the range, and it means the operating leverage was working entirely in Murata's favor.

The clearest live signal came on the April 2026 earnings call, where management noted the book-to-bill ratio — new orders divided by shipments, the single cleanest leading indicator of demand direction — had risen to 1.24, meaning orders were arriving roughly a quarter faster than the company could ship them.20 When a supplier of a physically scarce, hard-to-copy component is booked past full capacity, the pricing conversation inverts: the buyer, however large, becomes the price-taker. Murata and its peers moved to push through price increases on the tightest AI-server and automotive-grade parts, with trade press reporting hikes in the range of 15–35% on certain high-end capacitor and inductor lines into 2026 — a striking development in an industry whose long-run price trend is relentlessly downward.21 Rising prices in a components business are almost always a signal that demand has genuinely outrun the industry's ability to add supply, because capacity takes years and billions to build. The Components segment did the heavy lifting for the whole company: it grew revenue about 12% to roughly ¥1.16 trillion in the year to March 2026, and — the number that really matters for judging whether that revenue is worth having — earned a pre-tax segment return on invested capital above 20%.19 A 20%-plus ROIC in a supposedly commoditized industry is the whole thesis in a single number: it is the ceramic moat converting physical scarcity into genuine, capital-efficient returns rather than mere revenue.

City Two: The RF Crash and the Resonant Write-Down

Now cross town to the other city, which lives in Murata's Devices & Modules segment — the application-specific products, most notably the radio-frequency (RF) filters and modules that go into smartphones. Here the story is the mirror image. Smartphone unit demand has plateaued, and the segment that Murata had spent a decade and hundreds of millions of dollars building up through active-silicon acquisitions found itself badly exposed.

The clearest wound traces back to 2022. In February of that year Murata agreed to acquire the US filter-technology firm Resonant Inc. for $4.50 per share in cash, roughly $300 million (about ¥33.6 billion) in total.8 The prize was Resonant's XBAR technology, a novel resonator design promising to deliver the ultra-high-frequency filters that 5G, and eventually 6G, radios would need. The price tag raised eyebrows immediately: $4.50 a share was a 266% premium over Resonant's undisturbed price of $1.23, an eye-watering markup that only makes sense if you are certain the technology will become indispensable.9 The deal closed the following month.24

It did not become indispensable on schedule. The 5G RF-filter market proved brutally competitive and slower than hoped, smartphone module demand stayed soft as the handset market plateaued, and the technical synergies Murata had underwritten — folding XBAR into its existing surface-acoustic-wave filter roadmap — arrived slower than the acquisition math required. Under accounting rules, when a business's projected cash flows no longer support the goodwill sitting on the balance sheet, that goodwill must be tested and, if it fails, written down. On February 2, 2026, Murata delivered the verdict: it took an impairment loss of ¥43.8 billion — writing off the entire goodwill associated with the Resonant/SAW-filter business — as part of roughly ¥49.8 billion of one-time charges that cut its quarterly operating profit roughly in half year-over-year, to about ¥37.9 billion for the quarter.17 In dollar terms the write-down was on the order of $275 million at prevailing exchange rates; in plain terms, Murata had essentially admitted that most of what it paid for Resonant was gone.18

How management handled that admission is where the neutral-investor lens earns its keep, and it is worth resisting the urge to resolve it too neatly in either direction. The bear reading is straightforward and, frankly, damning: Murata paid a 266% premium for pre-revenue radio-frequency intellectual property, in an active-silicon domain where it had already stumbled once with Peregrine, and four years later the entire goodwill was zero. That is a textbook case of a superb components company repeatedly overpaying to buy its way into a semiconductor game it does not have a structural edge in — and it happened on the watch of a management team that had just made ROIC discipline its signature promise. An activist would note, pointedly, that the write-down does not undo the cash that left the building in 2022; the money is spent, the technology underdelivered, and the "clean quarter" narrative is at risk of dressing up a capital-allocation failure as a display of virtue.

The more sympathetic reading is about behavior after the mistake, and it is not nothing. Unlike the caricature of the Japanese conglomerate that buries bad news for years and lets zombie assets fester on the balance sheet, Nakajima's team took the full write-down in a single decisive quarter rather than dribbling it out, disclosed it plainly at the February earnings conference, and paired it with a concrete plan to restructure the RF business back toward profitability rather than a vague promise that things would improve. On the merits of crisis management, that is genuinely how you want a management team to behave when a bet goes wrong: recognize it fast, size it honestly, and move on. The credibility question — the one an investor should actually hold in mind — is whether this episode makes Murata more disciplined about its next active-silicon temptation, or whether it is simply the second data point in a pattern of a materials champion that cannot resist reaching for silicon it should leave alone. Which of those two readings you weight more heavily is, frankly, the crux of the entire Murata debate, and it points straight to the playbook lessons the company's history so cleanly teaches.

VII. The Playbook: Core Business & Investing Lessons

Step back from the individual quarters and Murata offers a remarkably clean set of lessons — not because management is infallible, but because its wins and its stumbles rhyme so consistently. Three stand out.

Lesson one: vertical integration can itself be the moat. We live in an era that worships the fabless model — the idea that the smart money designs the product and outsources the dirty, capital-heavy business of actually making it. Murata is the standing counter-example. Because its advantage lives in materials chemistry and mechanical process rather than in a circuit diagram, the messy physical stuff — synthesizing the powder, building the kilns, owning the fab — is not a cost to be shed but the very thing rivals cannot copy. When your secret is tacit process knowledge rather than a blueprint, owning the whole stack is the defense. The fabless playbook would have handed Murata's crown jewels to a contract manufacturer and, with them, the moat.

Lesson two: beware paying high premiums to enter someone else's ecosystem. Murata is the undisputed master of passive components. Every time it has tried to climb up the value chain into active RF silicon — Peregrine, then Resonant — it has bought into a more volatile, more customer-concentrated, faster-moving semiconductor world where its materials-and-machines advantage does not travel. The Resonant write-down is not a random accident; it is the predictable failure mode of a materials company reaching into a domain where its specific edge is neutralized, and paying a growth-stock premium to do it. Adjacency on an org chart is not adjacency in competitive reality.

Lesson three: when a market commoditizes, run toward the hardest corner of it. Standard capacitors are a price war Murata has no interest in winning on cost against Chinese entrants who can accept thinner margins and enjoy state support. So it does the opposite of chasing volume: it aggressively tilts its capacity mix toward the highest-spec automotive and AI-datacenter parts, where qualification barriers are brutal and its triple wall is tallest, and it is content to cede the low end. That is how a company expands margins in a nominally commoditizing industry — not by out-cheaping the cheap players, but by continuously abandoning the commoditized layer for the layer that has not commoditized yet, staying one rung above the rising tide of competition. It is the same instinct as the founder's materials-first philosophy, expressed in portfolio terms: always be where the problem is hardest, because that is where the pricing power lives.

There is a fourth lesson hiding in the first three, and it is the one most relevant to judging the company from here. Murata's durable advantages are all on the supply side — process, scale, switching costs, cornered resources. Its recurring vulnerabilities are all on the demand side — cyclicality, customer concentration, and the temptation to buy growth in markets where its supply-side edge does not apply. A great deal of the Murata investment case reduces to a single tension: an almost unbeatable ability to make things, married to an inability to control who wants them or how much. The company cannot fix the demand cycle; the most it can do is manage its exposure to it, which is exactly what the capacity-mix strategy attempts. Whether that management is durable enough to withstand a determined, well-capitalized competitive assault, and a hard turn in the cycle, is precisely what a structural analysis has to test.

VIII. Structural Analysis: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Let us war-game the business properly, using two lenses. Porter's Five Forces tells us how attractive the industry structure is; Helmer's 7 Powers tells us which specific, persistent advantages Murata holds within it.

Threat of new entrants — very low. Building a competitive high-end MLCC operation is not a matter of capital alone, though the capital bar is already in the billions. It requires custom kiln and machine design, a proprietary powder chemistry refined over decades of trial and error, and years of reliability qualification before an automaker or a hyperscaler will trust your part. Money can buy a factory; it cannot buy the accumulated process knowledge, and it cannot buy back the years. That is the highest wall on the board.

Bargaining power of buyers — moderate, and weaker than it looks at the high end. Yes, Apple and Tesla and the big server makers are enormous, sophisticated buyers with real volume leverage. But the events of 2025–2026 revealed the limit of that leverage: when lines run at 90–95% utilization and orders outrun capacity, even the largest buyer becomes a price-taker, and Murata pushed through double-digit price increases.1821 Buyer power is real in slack markets and evaporates in tight ones — which tells you buyer power in this business is fundamentally a function of the cycle.

Bargaining power of suppliers — low. Because Murata synthesizes its own barium titanate and builds its own machinery, it has deliberately engineered away its exposure to supplier shocks. The company is, to an unusual degree, its own supplier. The residual exposures are raw materials like nickel and palladium for electrodes, and — importantly — energy, which we will flag as a genuine vulnerability in the bear case.

Threat of substitutes — near zero. For the job an MLCC does — enormous capacitance density, high reliability, tiny footprint, low cost, at trillions of units — no alternative technology comes close on that specific combination of attributes. Other capacitor types exist for niche roles, but nothing threatens to displace the MLCC as the default decoupling reservoir on a dense circuit board. That is about as safe as a substitution picture gets.

Competitive rivalry — moderate, and bifurcated. This is the nuance that a casual reading misses. In commodity MLCCs, rivalry is intense: Murata (roughly 40% share) competes with 삼성전기 Samsung Electro-Mechanics (the clear number two, around a quarter of the market), plus TDK, 太陽誘電 Taiyo Yuden, and Taiwan's 國巨 Yageo.123 But in the high-spec automotive and AI-server tier, the field thins to a tight oligopoly where Murata commands premium pricing. The company effectively lives in two different competitive intensities at once, which is precisely why its capacity-mix strategy matters so much.

Now Helmer's 7 Powers, which sharpens the picture into named, durable advantages:

Process Power. This is Murata's signature power in the Helmer sense — an organizational capability, embedded in people and routines and refined over decades, that cannot be bought or quickly replicated. The ability to fire sub-micron ceramic stacks at high yield is the textbook definition.

Scale Economies. Murata's enormous global volume spreads its heavy, ongoing capital spending across trillions of units, driving unit costs below what any smaller rival can reach — and its capex commitments run to the hundreds of billions of yen over multi-year plans, a spend few competitors can match.16

Switching Costs. The SPICE-model design lock-in discussed earlier — engineers building boards around Murata's specific component behavior — is a genuine switching cost operating at the design-in stage.

Cornered Resource. Two candidates: the Kyoto ceramics talent and culture cluster, and the in-house machinery division that builds production equipment no competitor can purchase. Both are resources Murata has access to on preferential terms that rivals structurally cannot match.

It is worth war-gaming the specific competitors, because "Murata has a moat" means little without asking against whom. 삼성전기 Samsung Electro-Mechanics is the most credible threat: it is the clear number two at roughly a quarter of the market, it is backed by the vast resources and vertical integration of the Samsung group, and it has openly declared its intent to take share, particularly in the coveted automotive and high-capacitance tiers.23 TDK and 太陽誘電 Taiyo Yuden are fellow Japanese makers with genuine high-end capability but smaller MLCC scale, each occupying strong positions in particular niches rather than challenging Murata across the board. 國巨 Yageo of Taiwan competes ferociously on the more standardized parts and has grown through acquisition, while a rising cohort of Chinese makers has reached roughly a tenth of the global market — but overwhelmingly at the commodity end, not yet at the automotive-grade tier where the qualification wall stops them.23 The pattern is telling: Murata faces real, resourceful competition, but it is bifurcated. In commodity MLCCs the field is crowded and prices grind lower; in the highest-reliability parts the field thins to two or three names, and Murata sits at the front. The strategic imperative — keep migrating the mix upward, faster than competitors can climb — falls directly out of this map.

What Murata conspicuously lacks, in Helmer's taxonomy, are Network Economies, Branding power in the consumer sense, and Counter-Positioning — its advantages are all on the supply and process side, not the demand side. That matters because it means Murata's moat protects its cost and quality position beautifully, but does nothing to protect it from the demand cyclicality of its end-markets. The moat keeps competitors out; it does not keep the cycle from coming in. An investor who forgets that distinction will mistake a cyclical trough for a broken moat, or a cyclical peak for a permanent re-rating — and both mistakes have been made, repeatedly, by people watching this exact industry.

IX. Bull vs. Bear Case & Key Metrics

Which brings us to the reckoning. Murata is neither the invulnerable compounder its boosters describe nor the overpaying serial acquirer its critics fixate on. It is a company with a genuinely rare supply-side moat riding on genuinely cyclical demand, run by a management team that has just been publicly tested by its own biggest mistake. Here is how to hold both truths at once.

The three KPIs that actually matter

Ignore the noise and watch three numbers. First, capacity utilization — the master switch for operating leverage in a fixed-cost, capital-heavy business. At the reported 90–95% it drives margins up; if it slips toward the 70s in a downturn, those same fixed costs work violently in reverse.18 Second, the book-to-bill ratio, the cleanest leading indicator of demand direction; at 1.24 it signals orders outrunning shipments, and the day it drops decisively below 1.0 is the day the cycle turns.20 Third, segment ROIC, especially the gap between Components (running above 20% pre-tax) and Devices & Modules (barely above breakeven after the RF write-down) — the single best scorecard for whether the troubled RF business is actually healing and whether management hits its promised 12% consolidated ROIC by fiscal 2027.1619

Myth versus reality

Before the two cases, one consensus narrative deserves fact-checking, because it colors how people value the stock. The popular story is that Murata is a "picks-and-shovels" play on AI — a safe, diversified way to own the AI boom without betting on which chip or which model wins. There is truth in that: Murata sells into essentially every AI server regardless of whose GPU is inside, and its parts are genuinely indispensable. But the "safe" framing oversells it. Murata is not a toll road with predictable traffic; it is a cyclical component maker whose fortunes swing violently with capital-spending cycles it does not control, and whose best current customer — AI data-center buildout — is itself the subject of a fierce debate about whether spending is running ahead of returns. If hyperscaler capex pauses, the "picks-and-shovels" narrative will not protect Murata any more than it protected memory makers in past gluts. The reality is a superb, moated business riding a demand wave that is real but not guaranteed to be permanent — which is a very different thing from a safe compounder.

The bull case

With that caveat, the bull case rests on a structural demand shift, not just a cyclical upswing. AI data centers and high-voltage EV architectures, on this view, are not a fad quarter; they represent a durable migration of capacitor demand toward exactly the high-reliability, high-margin parts where Murata's triple wall is tallest and commodity rivals cannot qualify. That mix shift can insulate the company from the mature, plateauing smartphone market that used to define its cycle. Layer on the pricing power that comes from being booked past capacity — a rare and telling thing in this industry — plus a management team now publicly committed to ROIC discipline, a 30% dividend payout, and buybacks an order of magnitude larger than the family era ever countenanced, and you have a plausible path to structurally higher and steadier returns than the boom-bust Murata of the 2010s. The bull's core, falsifiable claim is that the mix shift toward AI and automotive is permanent and the moat is compounding faster than competitors can erode it. The evidence in its favor — 20%-plus component ROIC, a 1.24 book-to-bill, price increases in a deflationary industry, and qualification barriers that visibly keep commodity players out of the best tier — is concrete rather than rhetorical. That is what separates this from a story stock.

The bear case

The bear case does not dispute the moat; it disputes the price, the cyclicality, and the tail risks. Four concerns dominate. Cyclicality dressed as growth: the single biggest risk is that the AI-and-EV demand surge proves more cyclical than structural. Component makers have been fooled before — every glut in history was preceded by a period when everyone was certain demand had permanently re-rated. If AI capex digests, or if the industry (Murata included) over-builds capacity into the current shortage, the same operating leverage that is producing 20%-plus returns today would slam into reverse, and a stock priced for a structural story would re-rate hard. Geopolitics and supply chain: Murata's fabs span Japan, China, and Southeast Asia, and a great deal of the world's final electronics assembly — where its parts actually get consumed — is concentrated in China. Any serious escalation in US–China or China–Taiwan tensions could snarl the logistics that the whole model depends on, and Murata's China exposure cuts both as a manufacturing base and as an end-market. Energy and input costs: firing ceramics in continuous 1,000°C-plus kilns is ferociously energy-intensive, which leaves Murata directly exposed to electricity and gas price shocks — the one meaningful crack in its otherwise supplier-insulated model — as well as to the cost of precious-metal electrode materials. Competitive catch-up: if Samsung Electro-Mechanics, which has openly stated its ambition to take share, or a well-funded Taiwanese or Chinese maker finally cracks the automotive AEC-Q200 barrier at scale, the premium pricing in Murata's best tier would face real downward pressure; the low end has already been substantially ceded to Chinese makers approaching a tenth of the market, and the question is how far up the value chain they can climb.23

And hanging over all of it is the activist's fair question, the one that ties the governance and capital-allocation threads together: after the Resonant write-down, has management truly earned the benefit of the doubt on its next big capital-allocation swing, or was the clean, fast impairment simply competent crisis management applied to a bad decision it should never have made? A skeptic would want to see Murata prove its ROIC discipline by resisting the next shiny active-silicon acquisition, not by writing off the last one gracefully. The company's raised appetite for strategic M&A, disclosed alongside its capacity plans, is either a sign of confident capital deployment or a yellow flag, depending on how much credit you extend — and reasonable investors will disagree.

Step back and the two cases are not really in conflict about the facts; they are in conflict about time horizon and durability. The bull and the bear agree that Murata makes the best MLCCs in the world, that its process moat is genuine, and that AI and EVs are pulling demand toward its sweet spot right now. They disagree about whether that is a permanent re-rating of the business or the top of another cycle, and about whether a management team that just wrote off a $300 million bet has learned discipline or merely learned how to write off bets gracefully. Those are not questions that can be settled by argument; they can only be settled by watching the business over the next several years. That is exactly why the three KPIs matter more than any narrative — they are the instruments that will tell you which story is coming true, quarter by quarter, before the market has fully priced it.

The honest synthesis is that Murata wins from here if — and only if — the AI-and-EV mix shift proves as structural as the bulls claim and the moat holds at the high end, and the case breaks if the cycle turns hard while a competitor finally scales the automotive wall or geopolitics severs the supply chain. The ceramic moat is real, and eighty years of accumulated process knowledge is not something a rival conjures in a business plan; it has simply never protected the company from the one thing it cannot control, which is the demand cycle riding on top of it. That is the enduring shape of the Murata story — a company that solved the problem of how to make something almost no one else can make, and spends every cycle rediscovering that it never solved the problem of controlling who wants it. Watch the utilization rate, watch the book-to-bill, and watch whether that 12% ROIC promise turns into a reported number. Those three will tell the next chapter of the story before any press release does.

References

-

Gabelli Japan Research: Finding Technology Leaders — Gabelli Funds, 2025-04-22 ↩↩↩

-

Murata's Strategic Expansion in AI-Driven MLCC Demand and Global Market Leadership — AInvest, 2025-08 ↩

-

Murata's MLCC for 5G Smartphones (Part 1) — Murata Manufacturing ↩↩

-

How tiny capacitors became the latest AI-driven investor darling — South China Morning Post ↩↩

-

The History of Murata — Murata Manufacturing Co., Ltd. ↩↩↩↩↩

-

MLCC Case Sizes Standards Explained — Passive Components Blog (EPCI), 2026-05-22 ↩

-

008004 size temperature compensation type MLCC, a world-first from Murata — Murata, 2017-02-21 ↩

-

Notice Concerning Conclusion of Agreement to Acquire U.S.-based Resonant Inc. — Murata Manufacturing, 2022-02-15 ↩

-

Goleta 5G filter company Resonant sold to Japanese firm at big premium — Pacific Coast Business Times, 2022-02-15 ↩

-

Murata closed the purchase of VTI Technologies — Business Wire, 2012-01-31 ↩

-

Murata Electronics Completes $471 Million Purchase of Peregrine Semiconductor — EvoNexus, 2014-12 ↩

-

Murata Manufacturing and Sony Sign Definitive Agreement for the Transfer of Battery Business — Murata, 2016-10-31 ↩

-

Notice Regarding the Completion of the Acquisition of Battery Business — Murata, 2017-09-01 ↩

-

Change of President and Representative Director — Murata Manufacturing, 2020-03-13 ↩↩

-

Murata steps up corporate governance as founding family yields control — Financial Times, 2020-03-12 ↩

-

Medium-Term Direction 2027 — Murata Manufacturing Co., Ltd. ↩↩↩

-

Earnings Release Conference (Q3 FY2025), February 2, 2026 — Murata Manufacturing ↩

-

Murata operating profit halved on ¥50 billion impairment — BigGo Finance, 2026-02-02 ↩↩↩↩

-

Consolidated Financial Results for the Year Ended March 31, 2026 — Murata Manufacturing, 2026-04-30 ↩↩↩

-

Earnings Release Conference (Q4 FY2025), April 30, 2026 — Murata Manufacturing ↩↩

-

MLCC Manufacturers Consider Price Increase as AI Demand Outpaces Supply — Passive Components Blog ↩↩

-

Murata Manufacturing (6981): The Best Way To Play MLCC Demand Surge — Macro Ops, 2020-10-21 ↩↩

-

Korean MLCC manufacturers aim to grow market share — Passive Components Blog ↩↩↩↩

-

Murata Completes Acquisition of Resonant Inc. — Murata Manufacturing, 2022-03-29 ↩

-

Murata Manufacturing IR Library — Results & Shareholder Returns — Murata Manufacturing ↩

-

MLCC and Ceramic Capacitors — Passive Components Blog (EPCI) ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube