Fanuc Corporation: The Yellow Giant of the Global Factory Floor

I. Introduction & The Yellow Paradox

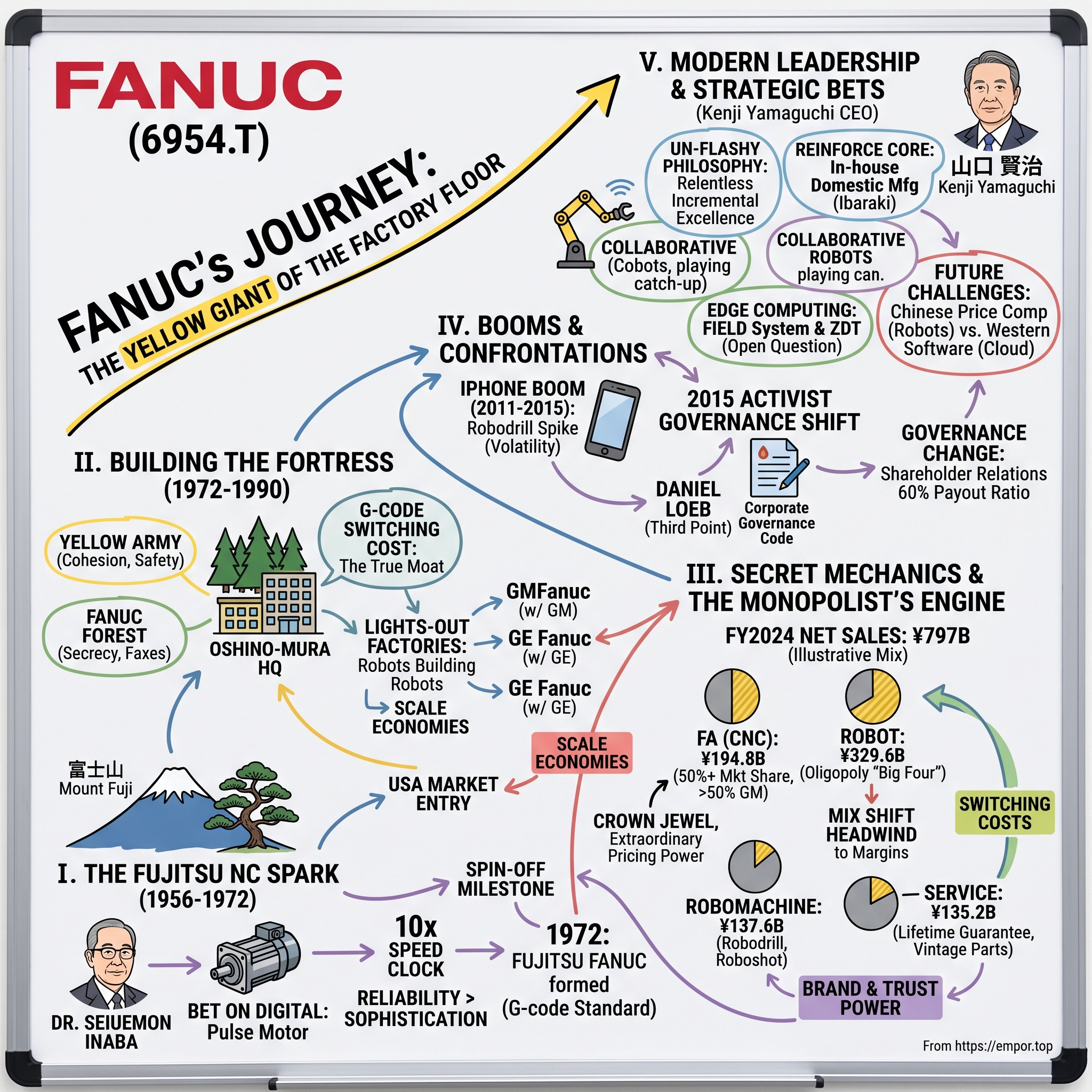

Drive west out of Tokyo for roughly two hours, past the last of the suburban sprawl and up into the pine forests that ring the base of 富士山 Mount Fuji, and you arrive somewhere that does not look quite real. In the village of 忍野村 Oshino-mura, hidden behind a screen of trees, sits a sprawling corporate campus where everything—every single thing—is painted the same shade of yellow. The office buildings are yellow. The factories are yellow. The delivery trucks, the forklifts, the coveralls on the workers, the robotic arms bolted to the assembly lines, even the fire hydrants: all of them wear the identical, unmistakable hue that the industrial world simply calls "Fanuc Yellow."

This is the headquarters of ファナック株式会社 FANUC Corporation, and it is arguably the most important company that the average person has never heard of. Walk through any modern factory on earth—an automotive plant in Bavaria, a smartphone assembly line in Shenzhen, an aerospace machine shop in Ohio—and you will find Fanuc's fingerprints everywhere. Its computer numerical control (CNC) systems are the "brains" that tell metal-cutting machine tools exactly where to move, down to the micron. Its robots are the "muscles" that weld, paint, and lift on assembly lines. If Fanuc were to vanish overnight, an alarming fraction of the world's automated manufacturing would simply grind to a halt, because there is no easy substitute waiting in the wings.

For a company that shuns publicity to the point of near-invisibility, the financial results are startling. Listed on the Tokyo Stock Exchange under the code 6954, Fanuc sits among the largest companies in Japan by market value.11 In the fiscal year ended March 2025 (which the company labels FY2024), it generated roughly ¥797 billion in net sales, and for decades it ran operating margins that flirted with 40%—numbers that belong to a dominant software business, not a maker of heavy steel machinery.3[^14] How does a physical hardware manufacturer earn software-like economics?

That is the paradox this story tries to unravel. How did a small, chronically underfunded research team inside the telecommunications giant 富士通株式会社 Fujitsu Limited grow into a near-monopoly over the digital controls of global industry? How did a single, famously autocratic founder build a culture so obsessed with speed and precision that it manufactured its own moat? How did an American activist investor crack open the most secretive company in Japan in 2015? And—the question that matters most for anyone looking forward rather than backward—how is today's management navigating a world of collaborative robots, edge-computing software, and a wave of heavily subsidized Chinese competitors who are learning, quickly, how to build a cheaper yellow box? Let's start where the yellow began.

II. Dr. Seiuemon Inaba & The Fujitsu NC Spark (1956–1972)

In the mid-1950s, Japan was a poor country. The factories that had survived the war were running worn-out prewar machinery, and the government's Ministry of International Trade and Industry—the legendary 通商産業省 MITI that would orchestrate so much of the postwar miracle—had concluded that if Japan was going to compete with the West in manufacturing, it could not simply copy American machines. It would have to leapfrog into the coming age of automated, computer-controlled production. Numerical control—the idea of driving a machine tool with coded instructions rather than a skilled human hand on a crank—was the frontier.

Into this bet walked a young mechanical engineer named 稲葉 清右衛門 Dr. Seiuemon Inaba. A University of Tokyo graduate who had joined Fujitsu in 1946, Inaba was handed a small, poorly funded team and an enormous mandate: build Japan's first practical numerical control system.2 He was, by every account, a difficult and relentless man—impatient, blunt, contemptuous of excuses—and those traits would eventually harden into a corporate religion. But in 1956 he was simply an engineer with a problem to solve and almost no resources to solve it with.

Here Inaba made the decision that arguably created the company. Western pioneers—General Electric, Bendix, the machine-tool establishment—were chasing numerical control through analog servo systems: continuous electrical signals, delicate feedback loops, expensive and finicky. Inaba bet the other way. He bet on digital, and specifically on translating digital pulses directly into mechanical motion. His team developed an electro-hydraulic pulse motor, a device that took discrete electronic pulses from a controller and converted each one into a precise, repeatable increment of physical rotation.1 Think of the analog approach as steering a car by continuously nudging the wheel and watching the road; the digital pulse approach was more like a staircase, where each step is exact, countable, and impossible to misread. It was cruder in theory but far more rugged, far cheaper, and far harder to break—exactly the qualities a cash-strapped factory floor needed.

In 1956, Inaba's team successfully ran the first numerical control system developed in the Japanese private sector.1 It was not elegant by Western standards, but it worked, it kept working, and it did not require a PhD to operate. That combination—reliability over sophistication—would become the entire Fanuc design philosophy, and it is worth pausing on why it mattered strategically. A factory owner does not buy the most advanced machine; he buys the one that will still be running at 3 a.m. on a Sunday when a shipment is due Monday. Inaba understood, decades before it became fashionable business-school language, that in industrial equipment durability is the product.

For sixteen years the operation grew inside Fujitsu, expanding from automating a single machine to automating whole production lines. But a fast-moving factory-automation market did not fit comfortably inside a giant telecom bureaucracy. So in 1972, Fujitsu spun the division out as an independent company, Fujitsu Fanuc—the acronym standing for Fujitsu Automatic Numerical Control.1 Inaba, now Executive Director and soon the unquestioned boss, was finally free of his corporate parent.2

What he did with that freedom set the tone for everything that followed. Inaba installed a culture of almost theatrical urgency. The most famous artifact was the 10倍速時計 ten-times-speed clock he mounted in the research labs—a clock whose second hand swept around the dial ten times faster than real time, a permanent visual scold reminding his engineers that, in his words, engineering without speed was meaningless. It was equal parts management theory and psychological pressure, and it captured the man perfectly: this was not going to be a gentle, consensus-driven Japanese company. It was going to be an empire run at a sprint. The question was where to build it.

III. Oshino-Mura: Building the Yellow Fortress (1972–1990)

Inaba's answer was to disappear. In the early 1980s—the company completed the headquarters move in 1984—he pulled Fanuc out of the Tokyo suburbs and relocated the entire operation, executives, laboratories, factories and all, to a vast wooded site at the foot of Mount Fuji in Oshino-mura.1 The official rationale was focus: away from the noise and the poaching and the endless meetings of Tokyo, engineers could concentrate. The unofficial rationale was control. A company hidden in a forest is a company whose secrets stay in the forest.

The isolation quickly became mythology, and the mythology had a color. Everything was painted yellow, and over the years the choice acquired layers of meaning that the company was happy to let accumulate. The practical origin was safety—yellow is the most visible color on a chaotic factory floor, the color of caution tape and warning signs. But inside Fanuc it grew into something closer to a uniform for a movement. Employees became known, admiringly and a little uneasily, as the 黄色い軍団 Yellow Army. The color signaled cohesion, energy, and total identification with the company. You did not merely work at Fanuc; you were absorbed into it.

The secrecy went further than paint. For decades Fanuc was famous for banning internal email, on the theory that electronic messages leak and paper does not, forcing communication back onto fax machines and physical documents that never left the building.[^8] To competitors, the "Fanuc Forest" was a black box. To the press, it was a source of endless fascination and almost no access. And to Inaba, it was exactly the point: a company nobody could see was a company nobody could copy.

But the deepest moat Fanuc built in these years was not physical at all—it was linguistic. Fanuc standardized its CNC controllers around Gコード G-code, the programming language that tells a machine tool how to move. And as Fanuc came to dominate the Japanese machine-tool market and then exported aggressively, an entire global generation of machinists learned their craft on Fanuc controllers, Fanuc keyboard layouts, and Fanuc's particular dialect of G-code. This is the crucial move to understand, because it is where the software-like economics come from. A machine shop that has trained fifty operators on Fanuc controls, written thousands of part programs in Fanuc's syntax, and built its whole workflow around Fanuc's quirks cannot simply switch to a Siemens or a Heidenhain controller. Doing so would mean retraining every operator, rewriting every program, and eating the downtime while the shop relearns how to work. In the language of strategist Hamilton Helmer, this is a textbook switching cost: the customer is locked in not by a contract but by the sunk cost of human habit. The interface became the moat, and it was a moat measured in careers, not dollars.

Then Inaba did something that took Fanuc's cost advantage into a different universe: he pointed the robots at themselves. The Oshino factories were designed to run "lights-out"—overnight, in the dark, with robotic arms assembling other robotic arms and CNC units, human beings barely required.[^8] "Robots building robots" was a marketing slogan, but it was also a genuine manufacturing revolution. Extreme automation drove down unit costs, eliminated the variability of human assembly, and produced a level of quality consistency Western rivals struggled to match. This is Helmer's scale economies power in its purest form: the more Fanuc built, the cheaper and better each unit became, and no smaller competitor could climb the same curve.

The one thing Inaba would not do was let his tightly held technology out of his hands. To crack open Western markets protected by trade barriers and local-content politics, he avoided acquisitions—which would have diluted control and leaked intellectual property—and reached instead for joint ventures with the biggest industrial names in America. In 1982 he formed GMFanuc Robotics, a 50-50 venture with General Motors that rapidly seized the North American automotive-robot market; Fanuc bought out GM's half a decade later.1 In 1986 he paired with General Electric to form GE Fanuc Automation, targeting CNC and industrial controls in North America—a partnership that ran until an amicable dissolution in 2009, with Fanuc keeping the core CNC business.1 Each deal followed the same logic: borrow the partner's distribution and political cover, keep the crown-jewel technology in the forest. By 1990, Fanuc was no longer a Japanese supplier. It was becoming the invisible standard beneath global manufacturing—and to see why that standard printed money, you have to open up the black box.

IV. The Monopolist's Engine: Secret Mechanics of CNC

To understand why Fanuc earns what it earns, you have to understand what a CNC system actually is, because the marketing word "controller" badly undersells it. Imagine a high-end metal-cutting machine—a five-axis milling machine that carves a jet-engine turbine blade out of a solid block of titanium. The CNC is the entire nervous system of that machine. It is the computerized brain that reads the part program and decides what happens next; it is the software and the motion-control algorithms that translate "cut this curve" into thousands of precisely timed commands; and it is the high-torque servo motors—the muscles—that actually move the cutting head through space. Fanuc makes all three, tightly integrated into one proprietary package. A rival selling only the controller, or only the motors, is selling a component. Fanuc sells the whole nervous system, and it sells it to the machine-tool builders—firms like ヤマザキマザック Yamazaki Mazak and DMG森精機 DMG Mori—who bolt it inside the machines they in turn sell to the world.

That distinction shows up starkly in the segment economics. Look at how the roughly ¥797 billion of FY2024 revenue split across Fanuc's four businesses.3 Factory Automation—the pure CNC, servo, and laser business—was the smallest reporting segment at about ¥194.8 billion, roughly a quarter of sales. Yet it is the crown jewel, because Fanuc's global share of the CNC market is variously estimated in the region of 50% or higher, a level of dominance that translates into extraordinary pricing power and gross margins believed to sit well above 50%.[^11]10 This is the business that historically pulled Fanuc's whole-company operating margin up toward 40%.

The largest segment tells a different story. ROBOT—the heavy industrial arms that weld car bodies, lift pallets, and spray paint—was about ¥329.6 billion, over 40% of sales.3 But here Fanuc does not enjoy a near-monopoly; it operates in a global oligopoly, the industry's so-called "Big Four," slugging it out against Japan's 安川電機 Yaskawa Electric, Switzerland's ABB, and Germany's KUKA (now owned by China's 美的集団 Midea Group). Robots are fiercely competitive, more commoditized, and structurally lower-margin than CNC. The remaining revenue came from ROBOMACHINE, at about ¥137.6 billion—Fanuc's family of standardized machine tools sold under the Robodrill, Roboshot, and Robocut brands—and Service, at about ¥135.2 billion, covering maintenance, spare parts, and retrofits worldwide.3

Service deserves its own spotlight, because it is where Fanuc's trust moat becomes a business model. Fanuc promises to service and repair its products for as long as a customer keeps using them—not for a warranty period, but effectively forever, even for machines that are forty years old. To honor that promise, the company warehouses a staggering, deliberately maintained inventory of vintage semiconductors and obsolete mechanical parts, so that it can fly a technician out with the exact right component within hours. Consider what that does to the mind of a factory owner. When a machine tool goes down, the cost is not the repair bill; it is the thousands of dollars per minute of a frozen production line and missed customer deliveries. A supplier who guarantees to get you running again, on any machine, at any age, has effectively de-risked the entire purchase decision. In Helmer's terms this is brand and trust power, and it is worth more than any spec sheet: it lets Fanuc charge a premium on the initial sale precisely because the buyer knows he will never be stranded.

Now for the uncomfortable part, the one investors have to sit with. That gorgeous 40%-margin history belonged to an era when the tiny, super-profitable CNC business drove the company. Today the biggest contributor is the lower-margin robot segment, and that mix shift has dragged consolidated operating margins down into a range closer to the high teens and low twenties—operating income in FY2024 was about ¥158.8 billion on ¥797 billion of sales, a roughly 20% margin.3 There is nothing wrong with a 20% industrial margin; most manufacturers would kill for it. But an investor who anchors on Fanuc's legendary 40% past is anchoring on a business mix that no longer exists. The company is growing its revenue by leaning into its least differentiated, most competitive segment—and that is a structural headwind to profitability that no amount of yellow paint can hide. It is also, as the next chapter shows, a business that can boom and bust with terrifying speed.

V. The iPhone Boom & The Cyclicality of Robomachine

In 2011, a machine called the Robodrill—Fanuc's compact, absurdly fast vertical machining center, a workhorse designed to mill small metal parts at high speed—suddenly became one of the most sought-after industrial products on earth. The reason was sitting in hundreds of millions of pockets.

When Apple moved the iPhone away from plastic and toward the machined aluminum unibody—the cold, seamless metal shell that became the phone's signature—it created a manufacturing problem of unprecedented scale. Each of those enclosures had to be carved out of a solid billet of aluminum, and carved to tolerances measured in fractions of a hair's width, at a rate of hundreds of millions of units a year. Apple's contract manufacturers, above all 鴻海精密 Hon Hai / Foxconn, needed CNC milling machines—not dozens, not hundreds, but tens of thousands of them. And the machine that fit the job, small and fast and reliable, was the Fanuc Robodrill.

Between roughly 2011 and 2015, Apple and its suppliers placed sudden, colossal orders, and Fanuc's Yamanashi factories scrambled to produce thousands of Robodrills a month. It was a gusher. The Robomachine segment threw off enormous cash, and Fanuc's earnings spiked. But this is where the story turns into a cautionary tale about the seductions of a mega-customer, because a boom driven by one company's product-design cycle is a boom you do not control.

When Apple's casing designs stabilized, or when it shifted a process, or simply when the existing installed base of Robodrills was enough to meet demand, the orders did not taper. They fell off a cliff—collapsing by half or more, effectively overnight. Fanuc experienced the full double-edged sword of serving a capital-equipment cycle attached to consumer-electronics fashion: explosive on the way up, brutal on the way down, and almost impossible to forecast. For investors, the lesson embedded in the Robomachine segment is precisely the one the smartphone boom taught: this is a genuinely volatile business, and while it is material—around 17% of FY2024 revenue—it should never be mistaken for the durable core.3 The recurring, compounding cash flows of CNC and Service are the ballast; Robomachine is the sail that fills and luffs with every gust from Cupertino. That volatility, and the enormous pile of cash it periodically deposited on Fanuc's balance sheet, would soon attract exactly the kind of attention Fanuc had spent forty years avoiding.

VI. The Activist Confrontation: Daniel Loeb & The 2015 Governance Shift

By late 2014, Fanuc had a problem that most companies would envy and most shareholders would resent: it was drowning in its own cash. Decades of fat margins and iron discipline had left roughly ¥1 trillion—on the order of $8 billion—sitting idle on a balance sheet with essentially no debt.57 The dividend payout ratio hovered around 30%, buybacks were nonexistent, and management's justification was the same one Inaba had given for forty years: Fanuc needed a "war chest" to survive the multi-year downturns that periodically gutted the industrial cycle. It was a prudent answer. It was also, to a certain kind of investor, an irresistible target.

Fanuc made itself irresistible in another way, too: it was, by design, one of the least shareholder-friendly companies in the developed world. It had no investor relations department, no email address for shareholders, no quarterly conference calls. Western fund managers who made the pilgrimage to Yamanashi were, by widespread account, received coldly if at all. In an era when Japanese corporate governance was becoming a live political issue, Fanuc was the perfect villain—or, from the other side, the perfect opportunity.

Enter Daniel Loeb, the combative founder of the American hedge fund Third Point, who built a significant stake and went public with his campaign in early 2015.5 His timing was surgical. Prime Minister 安倍晋三 Shinzo Abe had just introduced a new Corporate Governance Code and a companion stewardship code, explicitly designed to push Japanese companies toward higher returns on equity and more respect for outside shareholders. Loeb was not a lone foreign raider making unreasonable demands; he was pushing on a door that the Japanese government itself had just unlocked. His asks were pointed: create a real shareholder-relations function, roughly double the dividend payout, deploy the idle cash into buybacks, and add independent directors to the board.57

What happened next genuinely shocked corporate Japan. In March 2015, then-CEO 稲葉 善治 Yoshiharu Inaba—the founder's son—did not dig in. He capitulated, and did so almost completely.6 Fanuc announced it would create its first-ever shareholder-relations department. It committed to a consolidated dividend payout ratio of 60%, double the prior policy, as the cornerstone of its capital-return framework. It launched a large share buyback and began appointing independent directors.6 The company that had banned email and hidden in a forest was, seemingly overnight, holding earnings calls and talking to the very Western investors it had spent decades ignoring. Domestic Japanese institutions, newly emboldened by the governance code, had quietly lined up behind Loeb, and once that happened the outcome was never really in doubt.

It is tempting to file this away as a clean win for shareholder capitalism, and in the near term it was: capital discipline improved, the stock re-rated, and billions in trapped cash began flowing back to owners. But a skeptical long-term investor should hold a second thought alongside the first. The same cash that Loeb pried loose was cash that could, in principle, have funded a decade of aggressive software and platform R&D at exactly the moment when Western rivals like Siemens and Rockwell Automation were beginning to build cloud-based "digital twin" ecosystems around their hardware. Fanuc's engineering culture, brilliant at squeezing microns out of a servo motor, has never been a natural software house. Whether the post-2015 emphasis on returning cash came at the expense of the platform investments Fanuc would need for the next war is a question the company has not been forced to answer—yet. And the man now tasked with answering it inherited both the fortress and the new rules of engagement.

VII. Modern Leadership: Kenji Yamaguchi's Strategy & Capital Allocation

In April 2019, 山口 賢治 Kenji Yamaguchi became Chief Executive Officer of Fanuc, with Yoshiharu Inaba stepping back toward the chairman's role.8 If you were designing the ideal Fanuc CEO in a laboratory, you would probably produce something close to Yamaguchi. He is not a hired-gun outsider brought in to shake things up; he is a lifer, a University of Tokyo–trained engineer who joined Fanuc in 1993 and spent his entire career inside the robot development and production organization, becoming a development team leader by 2000 and rising to president in 2016 before adding the CEO title.89 He is, in other words, culturally native to the "strict preciseness" of Inaba's Fanuc—but he came of age professionally in the post-2015 world where shareholders get a phone call back.

Yamaguchi's public philosophy is revealingly un-flashy. In interviews he returns again and again to a single theme: that organizations are built on people, that only employees who take genuine pride in their products can make good products, and that engineers should get out of the lab and onto the customer's factory floor to feel where a machine is hard to use.8 It is a manufacturing purist's creed, not a Silicon Valley visionary's, and it tells you how he thinks the company wins: not through grand strategic pivots, but through relentless, incremental excellence in the core.

On capital allocation, the behavior largely matches the words, which is itself worth noting—management credibility is proven over cycles, not press releases. Through the wild swings of 2020 through 2026, Fanuc has held to the 60% payout policy it adopted under duress in 2015, honoring the post-activist settlement rather than quietly walking it back once the pressure lifted.[^12] Yamaguchi has consistently declined the temptation of large, expensive, dilutive acquisitions—the roll-up path that so many industrial peers chose—preferring to plow capital into domestic manufacturing capacity, such as the heavily automated Ibaraki-prefecture facilities, to lock down supply-chain security and keep production in-house.[^11] For an investor, this is a coherent and disciplined record; the flip side is that a company allergic to M&A also forgoes the fastest route to acquiring the software capabilities it lacks.

His alignment with shareholders is real but modest. Company disclosures put Yamaguchi's personal holding in the tens of thousands of shares—material to him, but a rounding error against the market capitalization, and nothing like a founder's stake.[^12] Compensation leans on performance-linked bonuses tied to metrics like return on equity and operating margin, which keeps management pointed at capital efficiency rather than empire-building.[^12] This is the profile of professional, institutional management—competent and accountable—rather than an owner-operator betting his own fortune on the outcome.

Where Yamaguchi is placing his strategic bets is telling. The first is collaborative robots—"cobots"—the CR series, designed to work safely alongside humans rather than caged behind safety fences. The logic is demographic: aging, shrinking workforces in China, Japan, Germany, and the United States make automation less a luxury than a necessity, and cobots extend automation to smaller shops that could never justify a traditional caged robot cell. The competitive challenge is that this fast-growing niche was pioneered by focused specialists like Universal Robots (owned by Teradyne), and Fanuc is the incumbent giant playing catch-up in a category it did not invent.

The second bet is software, and here Fanuc has planted its flag firmly against the prevailing wind. Rather than chase the Western industrial-cloud model, it built the FIELD system—FANUC Intelligent Edge Link and Drive—a platform that performs analytics at the "edge," on-premise, on the factory floor itself, instead of uploading sensitive production data to a public cloud.[^11] Its showcase application, Zero Down Time (ZDT), monitors thousands of connected robots and predicts mechanical failures before they occur, converting Fanuc's install base into a stream of higher-margin service and feeding the very lock-in the whole company is built on.[^11] The pitch to a security-conscious manufacturer is genuinely compelling. The open question—the one that will take years to resolve—is whether "edge, on-premise, and proprietary" turns out to be a durable strategic choice or a comfortable way of avoiding a cloud-software fight Fanuc is not sure it can win.

VIII. Strategic Analysis: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Strip away the yellow paint and the Mount Fuji mystique, and what does Fanuc's competitive position actually look like under a cold analytical lens? Two frameworks—Hamilton Helmer's 7 Powers and Michael Porter's Five Forces—map the terrain well, and the honest reading is that Fanuc's moat is very deep in one business and merely decent in another.

Start with Helmer's switching costs, which are Fanuc's single most valuable asset and among the strongest in all of industrials. The G-code standard, the muscle memory of hundreds of thousands of machinists trained on Fanuc interfaces, and the mountains of existing part-programs written in Fanuc's syntax mean that ripping out a Fanuc CNC in favor of a Siemens or Mitsubishi controller is a training and re-engineering nightmare that most shops will simply refuse to undertake. Scale economies rank next: the lights-out, vertically integrated "robots building robots" factories give Fanuc a unit-cost position no sub-scale competitor can match on equivalent volume. Then brand and trust power, embodied in the lifetime "service first" guarantee that makes buying a Fanuc the safe choice for any risk-averse plant manager. And finally a moderate cornered resource: sixty-plus years of proprietary, hard-won motion-control algorithms and motor designs that cannot be reverse-engineered from a data sheet. Note what is missing from this list—there is no meaningful network effect and no counter-positioning, and the cornered-resource advantage is eroding as talent and know-how diffuse globally.

Porter's Five Forces sharpen the picture further. The threat of new entrants is very low: the capital intensity, the decades of R&D, and above all the global service network required to credibly promise lifetime support form a barrier that no startup can vault. Supplier power is very low, because Fanuc's obsessive vertical integration—making its own motors, castings, and circuit boards—means it depends on almost no one. So far, so dominant.

The forces that bite are on the demand side and the rivalry side. Buyer power is moderate but rising: a giant automaker like トヨタ Toyota, GM, or Tesla buys enough robots to negotiate hard, and—more ominously—Chinese factory owners are increasingly willing to accept a "good enough" domestic CNC at a fraction of Fanuc's price. Substitutes are a low-to-moderate threat today: open-source, PC-based motion controllers exist and are improving, but they still lack the ruggedness, reliability, and lifetime-support network that define the Fanuc value proposition. And competitive rivalry is genuinely bifurcated—moderate and comfortable in CNC, where Fanuc's share is enormous, but high and margin-eroding in robots, where ABB, Yaskawa, KUKA, and a swarm of hungry Chinese manufacturers are all fighting for the same welding and handling applications. The strategic conclusion writes itself: Fanuc's fortress is the CNC business, and the robot business—the segment management is growing fastest—is where the walls are thinnest. Which is exactly the tension a bull and a bear will fight over.

IX. The Investor Stress Test: Bull & Bear Cases & Key KPIs

Picture two seasoned investors arguing over Fanuc across a table. Both know the company cold. They reach opposite conclusions, and the gap between them is the whole game.

The bull leans on structural inevitability. The developed and developing world alike are running out of factory workers—China's workforce is aging and shrinking, Japan's more so, and Germany and the United States face chronic shortages of people willing to weld and machine for a living. Against that backdrop, factory automation stops being a discretionary capex line and becomes a non-negotiable survival tool, and Fanuc sells the picks and shovels. On top of that secular demand sits the shock absorber: an installed base of well over a million robots and millions of CNC systems worldwide, throwing off high-margin service revenue that keeps cash flowing even when new-equipment orders freeze in a recession.[^11] And behind it all stands a fortress balance sheet—effectively no debt, a disciplined 60% payout returning cash to owners through the cycle.[^12] The bull's thesis, in a sentence: you are buying the toll road of global manufacturing, and the toll road is not going anywhere.

The bear does not dispute the demand story; the bear disputes who captures it. The most serious argument is Chinese localization. Backed by heavy state subsidies and a national-champion industrial policy, domestic Chinese CNC and robot makers are closing the quality gap faster than Fanuc's admirers would like to admit, and they are selling at prices reportedly 30% to 50% below Fanuc's. China is roughly a quarter or more of Fanuc's revenue, so this is not a peripheral market—it is the growth market, and if Fanuc gets designed out of it on price, both its growth and its precious scale economics deteriorate together.10 The second bear point is cyclicality: a prolonged freeze in electric-vehicle capital spending hits the robot segment directly, since so many robot orders ride on automotive welding and assembly lines. The third is the software worry raised earlier—if the industrial world consolidates around cloud-native, software-defined automation platforms controlled by Siemens or Rockwell, Fanuc's proudly on-premise, edge-first FIELD system could find itself an island. The bear's thesis, in a sentence: the moat is real, but it is being attacked at its two weakest points—Chinese price competition in robots and Western software integration in the cloud—precisely as management leans the revenue mix toward the more contested businesses.

Notice that the recent numbers do not settle the argument; they merely reload it. In the fiscal year ended March 2026, Fanuc's net sales rose about 7.6% to roughly ¥857.8 billion, with operating income near ¥183.8 billion and net income up about 13% to roughly ¥166.5 billion, as a post-inventory-correction recovery in demand—including, notably, renewed Chinese robot orders and a fast-emerging growth story in India—flowed through the results.4 The bull reads that as the toll road reasserting itself; the bear notes that leaning on Chinese robot demand is precisely the exposure in question. Both are right, which is why the case has to be tracked, not assumed.

So what should an investor actually watch? Three things, and only three. First, the consolidated operating margin: because the whole story of Fanuc is a mix shift from ultra-high-margin CNC toward lower-margin robots, the margin is the single cleanest gauge of whether pricing power and product mix are recovering or bleeding. Second, the FA-versus-ROBOT revenue mix: watch whether the crown-jewel CNC business is holding its own or being outgrown by the more commoditized robot segment, because that ratio is the margin story in leading-indicator form. Third, Service segment revenue growth: this is the purest measure of whether Fanuc is successfully monetizing its enormous, compounding global install base—the annuity that is supposed to make the whole cyclical machine durable. Get those three right over the next several years and you will know, well before the headline EPS does, whether the fortress is holding or quietly being flanked.

X. Epilogue & Key Playbook Lessons

Step back from the segment tables and the activist drama, and Fanuc's rise reads like a masterclass in a single, unfashionable idea: that extreme focus, relentlessly applied for decades, can build a hardware business with the economics of software. A cash-strapped team inside a telecom company made an early, contrarian bet on digital control; a difficult, brilliant founder wrapped that bet in a culture of speed, isolation, and yellow paint; and the whole edifice came to rest on a moat made not of patents or capital but of human habit—the machinists of the world quietly learning to think in Fanuc's language.

There are durable lessons here for anyone studying great businesses, and they are worth stating plainly rather than as slogans.

The first is that the interface is the moat. Fanuc's most valuable asset was never the physical controller; it was control of the G-code programming interface that human operators had to learn. Owning how the customer's people work is far stickier than owning what the customer buys, because retraining people is the switching cost no CFO wants to authorize.

The second is that "service first" can be a pricing strategy disguised as a customer-service policy. By promising to maintain its products essentially forever, Fanuc removed the single biggest fear in a factory owner's purchase decision—being stranded with dead equipment—and a de-risked buyer will pay a premium on day one. Lifetime support is not a cost center; it is what makes the initial sale defensible at a high price.

The third cuts against the grain of an M&A-obsessed corporate era: you do not have to buy your way to greatness. Fanuc built one of the highest-margin industrial franchises on earth almost entirely through organic R&D and deep vertical integration, proving that a cohesive, tightly controlled company can out-earn the roll-ups. The same discipline, of course, is now its dilemma—the software capabilities it may need are the kind most easily bought, and Fanuc's whole identity resists buying them.

And the fourth, delivered by Daniel Loeb in 2015, is that even a fortress must eventually answer to its owners. The most operationally secure empire in Japanese industry still had to open its books, return its cash, and learn to pick up the phone. Capital efficiency is not optional forever, however wide the moat.

Where all of this leaves Fanuc today is genuinely unresolved, and that is the honest place to end. The company enters the second half of the 2020s with its CNC monopoly intact, its balance sheet unbreakable, and its service annuity compounding—yet facing a Chinese challenge to its growth engine and a software question it has chosen to answer on its own contrarian terms. The yellow giant has been underestimated before, most recently by everyone who assumed a secretive forest company could never change. Whether its next act rewards or punishes that history is the wager investors are now being asked to make.

References

-

FANUC founder Dr. Seiuemon Inaba passed away — International Federation of Robotics, 2020-10 ↩↩

-

FANUC Financial Results and Financial Announcements (FY ended March 2025 segment data) — FANUC Corporation ↩↩↩↩↩↩

-

Consolidated Annual Financial Results for the Year Ended March 31, 2026 — FANUC Corporation, 2026-04 ↩

-

Third Point targets Fanuc to push for corporate governance reform — Financial Times, 2015-02-11 ↩↩↩

-

Robotic giant Fanuc vows to double payout ratio, yield to investor pressure — The Japan Times, 2015-03-12 ↩↩

-

Hedge fund billionaire Loeb targets secretive Japanese robot maker — Bloomberg, 2015-02-13 ↩↩

-

Take pride in products! Interview with Kenji Yamaguchi, President and CEO of FANUC — SEISANZAI Japan, 2019 ↩↩↩

-

Tokyo Stock Exchange Corporate Profile & Listing Details — Japan Exchange Group ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube