3Peak Inc.: The Art of Analog and the Great Decoupling

I. Introduction: The "Black Magic" of Analog

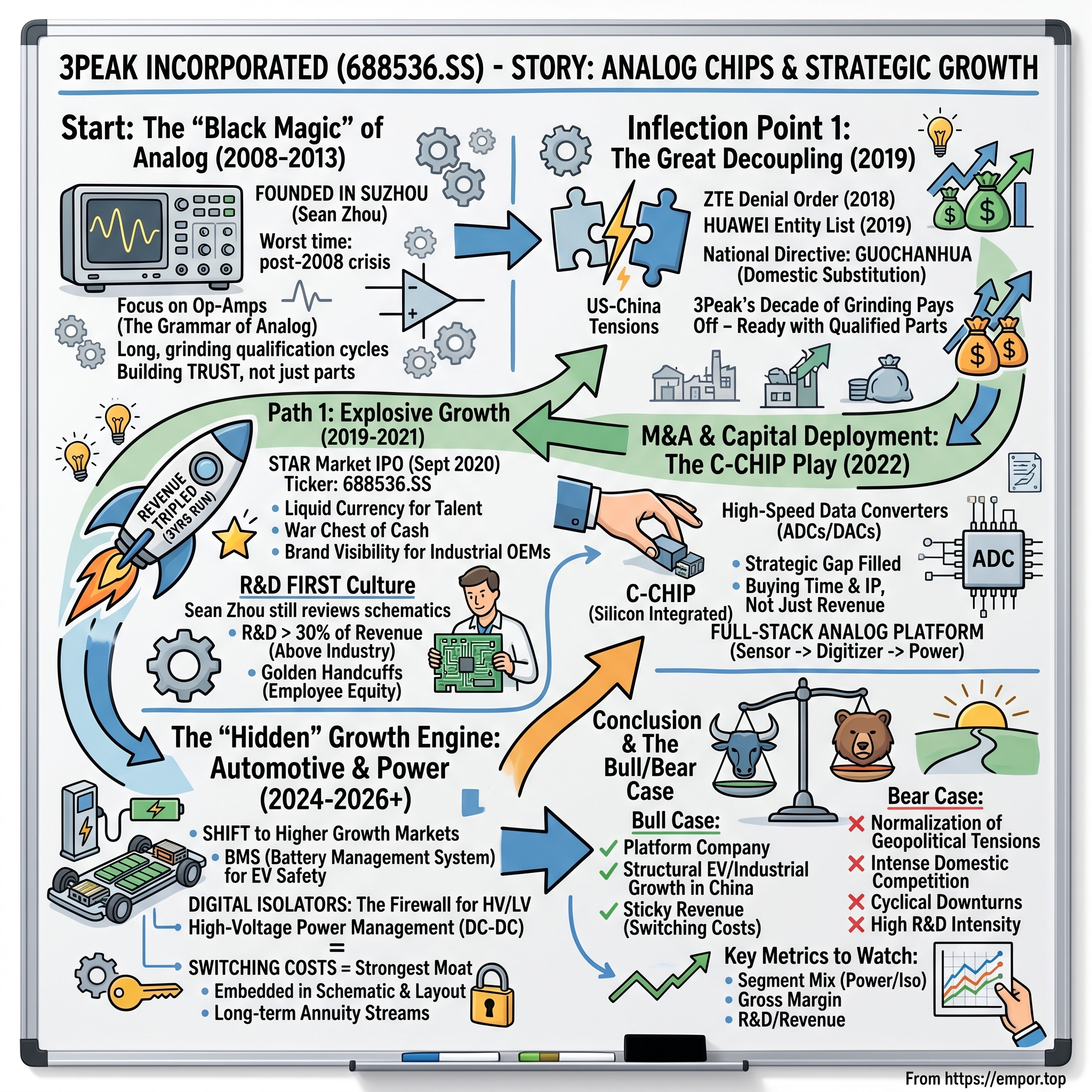

Picture a cleanroom on the outskirts of Suzhou in the summer of 2023. Fluorescent light bounces off epoxy floors, and a group of engineers in bunny suits is hunched over a lab bench. On the oscilloscope in front of them is a squiggle. Not a clean square wave, not a pretty sine—just a squiggle. A signal that has just traveled through a copper trace no wider than a human hair, survived crosstalk from a 400-volt power rail sitting a few millimeters away, and emerged with 24 bits of precision intact. To the casual observer, this is a boring Tuesday. To the analog engineers, this squiggle is the culmination of eight years of design work, three failed tape-outs, and one very uncomfortable meeting in which the CEO asked why a single operational amplifier had taken longer to qualify than most consumer apps take to go from concept to IPO.

Welcome to analog semiconductors. Welcome to 3Peak.

In an industry that celebrates the relentless march of Moore's Law, where every eighteen months the transistor count doubles and digital chips get exponentially smaller and faster, analog is the stubborn cousin who refuses to join the party. Analog chips are the translators between the physical world—temperature, voltage, pressure, sound, light—and the digital world where computation happens. They do not care about three-nanometer transistors. The laws of physics that govern them were written by Maxwell, Kirchhoff, and Ohm, not Mead and Conway. And the expertise to design them well is arguably the single most defensible moat in all of semiconductors.

3Peak Incorporated, listed in Shanghai under the ticker 688536, is not a household name even within technology circles. It has no consumer-facing product, no branded chip on the back of your phone, no logo anyone would recognize. And yet, tucked inside Huawei base stations, BYD electric vehicle inverters, Mindray medical imaging systems, and a thousand industrial automation cabinets across Asia, 3Peak's signal-chain and power-management chips are quietly doing the real work. They are measuring, amplifying, isolating, and converting—turning the analog mess of the physical world into the clean digital bits that AI models and cloud servers feast upon.

This is the story of how a twelve-person startup founded in the long shadow of the 2008 financial crisis became one of the most strategically important semiconductor companies in China. It is a story about the art of analog design, about the patience required to compete against Texas Instruments and Analog Devices—giants with fifty years of institutional knowledge and twenty-year-old product catalogs that still print money. It is a story about what happens when geopolitical tectonic plates shift and a low-cost alternative suddenly becomes a national necessity. And it is a story, above all, about timing. About a company that spent its first decade grinding through obscurity, building a catalog nobody cared about, and then woke up one morning in 2019 to find that the world had rearranged itself around them.

We will trace 3Peak from its founding to its STAR Market IPO, through its most important acquisition, and into its current pivot toward a full-stack analog platform. We will discuss Zhixue "Sean" Zhou, the chairman who still reviews schematic pages personally. We will examine the hidden growth engine inside the income statement. And we will frame all of it through the lens of the investor frameworks—Hamilton Helmer's 7 Powers, Porter's Five Forces, and the quieter question of whether domestic substitution is a tailwind or a trap.

Let's begin where every good semiconductor story begins. In a room with too few engineers and too much ambition.

II. The Founding & The Analog Moat

In 2008, the world was on fire. Lehman Brothers had just collapsed, credit markets had frozen, and in Shenzhen, venture capital was evaporating faster than a water droplet on a 300-degree hot plate. It was, on paper, the worst possible moment to start a semiconductor company. Fabless chip startups need years of burn before revenue, patient capital for mask sets that can cost millions per tape-out, and a customer base willing to qualify parts that might not ship in volume for half a decade. None of those things existed in abundance in late 2008.

Which is exactly when Zhixue Zhou—most Western colleagues simply called him Sean—decided to do it anyway. Zhou had spent more than a decade as an analog designer in the United States, working at the kind of companies that treat analog IC design as a form of applied art. He had absorbed the mantra that defines the industry: digital is science, analog is magic. He had watched experienced designers stare at a datasheet for an hour, then sketch a topology on a napkin that would survive twenty years of production. And he had concluded that the mainland Chinese semiconductor industry—for all its ambition around DRAM and mobile processors—had almost nothing in the way of indigenous analog capability.

The founding team was small. A handful of engineers, most with US analog backgrounds, setting up shop in Suzhou because the cost of living and the engineering talent pool around Shanghai Jiao Tong and Fudan made it viable. The first office was unremarkable. The first product line was even more unremarkable: operational amplifiers. Op-amps. The most boring, commoditized, utilitarian chip in the analog catalog. Texas Instruments had been selling op-amps for fifty years. Analog Devices had built an empire on them. Why on earth would a Chinese startup start there?

The answer is instructive. Op-amps are the grammar of analog electronics. Every signal-conditioning circuit, every sensor interface, every voltage reference, every ADC driver starts with an op-amp somewhere. If you can build a portfolio of precision op-amps that actually work across temperature, supply voltage, and load conditions—and you can get industrial customers to trust them—then you have earned the right to sell everything else in the catalog. Op-amps are the foot in the door. They are also, critically, the chips where the bar is highest: a 24-bit precision amplifier does not tolerate sloppy layout, sloppy device modeling, or sloppy testing. If you can ship a good op-amp, you can ship almost anything.

So 3Peak spent its first five years doing something that looked remarkably unglamorous from the outside: building one op-amp family, then another, then another, and grinding through the qualification cycles of industrial customers. Power-meter makers. Factory automation vendors. Medical device companies. These were not flashy design wins. There were no press releases. An industrial customer in China would take a 3Peak op-amp, qualify it for six months, design it into a product that would not ship for another two years, and then use it for the next decade. The design-in cycle was long, brutal, and cumulative.

Why did this matter? Because analog is not a business where you win by being cheaper or faster. You win by being trustworthy over a very long period of time. A circuit designer at a Tier-1 industrial OEM does not care that your chip is three cents cheaper. She cares that it will not fail in her customer's factory at 85 degrees Celsius in year seven of a ten-year product life. Every cycle of qualification, every design that ships without returns, every application note that happens to answer the question she is about to ask—all of it compounds into what insiders call tribal knowledge. It is the knowledge that says: when you drive a long cable in a noisy factory, use a 200-ohm isolation resistor in series with the op-amp output. Nobody writes that down in a textbook. You either know it, or you learn it the hard way when your customer's product fails in the field.

3Peak spent those lean years accumulating the kind of tribal knowledge that does not show up on a balance sheet. By the time the company began to approach one hundred million renminbi in revenue around 2014, it had something that mattered more than scale: credibility. A few hundred qualified SKUs in production. A reputation for being reachable—their field engineers would take a phone call from a 50-person customer in Chengdu, which TI's field team in Dallas would not. A willingness to help customers solve problems that fell slightly outside the chip itself.

None of this was visible in 2014. What was visible was a small, unremarkable fabless analog company with a strange name and a niche product line, competing in a segment the Chinese domestic press barely wrote about. The newly minted consumer chip companies—the ones chasing the mobile phone boom—got all the attention. 3Peak got the long, grinding design-ins.

That obscurity, as it turned out, was the best thing that could have happened to them. Because by the time the world changed, they were ready.

III. Inflection Point 1: The Great Decoupling

The phone call came in the spring of 2019, though different people at the company remember the exact moment differently. Some remember it as a trickle. Others as a flood. What nobody at 3Peak disputes is that, in the span of a few quarters, their business went from niche to strategic. From alternative to essential.

Rewind briefly. In the summer of 2018, the United States Commerce Department placed ZTE on a denial order, effectively cutting off the Chinese telecom equipment maker from American semiconductor suppliers. ZTE nearly collapsed within weeks. The message to every boardroom in China was unambiguous: your supply chain is a national security dependency, and the political weather just turned. Then came May 2019, when Huawei was placed on the Entity List. Huawei was not a middling telecom company. It was the crown jewel of Chinese industrial capability, the company that had almost single-handedly built 5G infrastructure across half the planet. And the US government had just told its suppliers they could not sell to it.

What followed inside Chinese OEMs over the next eighteen months is difficult to overstate. Every procurement team at every industrial, automotive, telecom, and medical equipment company in China was ordered to build a second supply chain. Not a theoretical one. A real one. Every Texas Instruments part number on every bill of materials was audited, and someone—often a mid-level engineer with a stopwatch and too much coffee—was told to find a domestic replacement that would pin-compatibly drop in. The industry coined a term for this: guochanhua, loosely "domestic substitution." It became a directive at levels of the government and the enterprise that were not accustomed to receiving engineering directives.

Here is where 3Peak's decade of quiet grinding suddenly paid off. Most of the flashy domestic analog startups founded in the 2015–2018 boom had chased consumer applications, because that is where volumes were. They had almost nothing in their catalogs that looked like an ADI or TI industrial-grade op-amp, instrumentation amplifier, or precision voltage reference. 3Peak had hundreds. The qualification work was already done. The datasheets matched up. The parts actually worked.

Revenue accelerated in a way that would have seemed fanciful just two years earlier. A company that had spent a decade getting to roughly 100 million renminbi in annual revenue suddenly found itself closing deals it had previously lost on price. Procurement teams that had politely declined to qualify 3Peak in 2017 were now cold-calling them. The company's top-line roughly tripled in 2019, then tripled again in 2020, then tripled again in 2021, crossing one billion renminbi in revenue on a base that had been measured in the double-digit millions just a few years earlier. For context, this is the kind of revenue acceleration that analog companies essentially never experience. Analog businesses are famous for their slow, steady compounding. 3Peak had, through no particular marketing genius of their own, hit an inflection that analog legends at TI or ADI had not seen in their lifetimes.

The company moved to capitalize on the moment. In September 2020, 3Peak listed on the Shanghai Stock Exchange's STAR Market, the then-new technology board created specifically to host strategically important hard-technology companies. The IPO priced at 90 yuan per share, opened well above that, and closed the first day at multiples of the offering price. The float was small by design, which amplified the volatility, but the signal was unmistakable: 3Peak was not just a company. It was a policy-aligned platform that the state-linked investor base wanted to own.

The STAR listing matters for reasons that go beyond the capital raised, which was large but not unusual by 2020 Chinese IPO standards. It gave 3Peak three things. First, a liquid currency—listed shares—with which to hire and retain engineering talent in a market that had suddenly become the most competitive analog-talent market in the world. Second, a war chest of cash that would, within two years, fund the acquisition that reshaped the company's product line. Third, a visible brand inside the halls of Chinese industrial enterprises. An OEM that might have hesitated to design a niche part from an unlisted startup into a ten-year industrial product could now point to the 688536 ticker and say: these people are here to stay.

There is a subtle story worth noting. The substitution tailwind was not uniform. Consumer and handset applications were relatively easy to substitute, because the design cycles were short and the performance requirements forgiving. Industrial applications were harder because the qualification cycles were longer, but once you won, you were in for a decade. Automotive applications were the hardest of all because of AEC-Q100 qualification and functional safety requirements. 3Peak played all three, but the real strategic gold was in industrial and, increasingly, automotive. That is where the durable revenue lived. And that is where the company began to pivot capital and headcount in 2021 and 2022.

But the substitution wave would not last forever. And the smarter voices inside 3Peak knew it. Which brings us to the man who had been patiently laying the groundwork for what came next.

IV. Management & The "R&D First" Culture

Most founder-CEOs of hot Chinese semiconductor companies, by the time their stock has gone up tenfold, have become minor celebrities. They appear on conference stages. They pose for profile pieces in Caixin. They give keynotes at the Shanghai Semiconductor Exhibition. Sean Zhou, by contrast, is rarely seen. He shows up at the annual shareholder meeting, answers questions in a flat, engineering-calibrated monotone, and retreats back to his office in Suzhou. His public interviews, when they exist at all, tend to be technical. His LinkedIn presence is minimal. He is, by the standards of the industry, almost invisible.

That is by design, and it tells you something about how the company is run.

Zhou is a designer, not a marketer. People who have worked closely with him describe a CEO who still reads schematic review packets, still asks questions about process corners and temperature drift during design reviews, and still flags layout choices in top-level blocks. This is not a CEO who has drifted upward into the strategic empyrean. This is a CEO who believes that if the schematics are right, the strategy will follow. Whether that belief is fully defensible in a company that is now selling into dozens of end markets is a question we will come back to. For now, take it as a fact of the management culture.

Zhou's shareholding sits in the mid-teens as a percentage, giving him enough economic skin to align with outside shareholders without dominating the cap table. Around him is a core founding and early-hire group who together hold meaningful equity positions, many through employee stock ownership vehicles that vest over multi-year periods. The 3Peak equity incentive structure has evolved in recent years into what the industry sometimes calls golden handcuffs: four-to-five-year vesting schedules on restricted stock, with performance-linked accelerators tied to revenue and R&D milestones. The explicit purpose is to discourage talent poaching from competitors like SG Micro, Silan, or the newer analog entrants backed by state industry funds. In an industry where a senior analog designer can move across town for a 50 percent raise, the retention math matters.

The R&D headcount tells a story of its own. At last published disclosure, research and development employees accounted for roughly three-quarters of the total workforce. R&D spending as a percentage of revenue has consistently exceeded what industry veterans consider the high end for mature analog companies. Texas Instruments spends about 10 percent of revenue on R&D. Analog Devices, roughly 20 percent across cycles. 3Peak has run well above that, at times pushing above 30 percent. The optics of this are not flattering to near-term margins. The strategic logic is that a company competing against fifty-year-old catalogs has to run faster for longer just to close the gap. Some shareholders have found this difficult to swallow, particularly during the recent downturn. Management has been firm: the R&D budget is the moat.

There is also a cultural artifact worth describing, which management sometimes refers to as "zero defects." In analog, a part that fails in the field—particularly one that fails subtly, causing a customer's system to produce wrong readings rather than obvious failure—can be catastrophic. A bad op-amp on a medical imaging board can degrade a diagnostic image. A failed digital isolator in an electric vehicle can compromise safety. 3Peak institutes a level of internal testing and design review that, by all accounts, goes beyond what the Chinese analog industry average looks like. The company hired from the automotive playbook early, importing concepts like Design FMEA and functional-safety process flows into a workforce that had grown up on consumer timelines. That cultural transplant has not been painless. It has also, in the view of customers who have audited 3Peak's quality processes, been the single most important factor in winning industrial and automotive design-ins.

The transition Zhou is currently attempting is from founder-led design boutique to institutionalized semiconductor company. This is the transition at which, historically, many analog startups have failed. The pattern is familiar: the founders are brilliant, the first 200 products are gorgeous, but the systems needed to run a 2,000-SKU portfolio across dozens of end markets—product line management, quality systems, volume production discipline, global sales coverage—are a different capability altogether. 3Peak has been visibly building this layer since the IPO. Senior hires from TI, ADI, and Maxim have appeared in product-line and operations roles. The Suzhou R&D center has been augmented with design offices in Shanghai and Beijing. The investor communications team, once nonexistent, now fields institutional calls.

Whether this transition will be successful is, frankly, not yet decidable. The last two years have included a significant analog downcycle, which has pressured margins and tested the company's cost discipline. Revenue declined meaningfully from the 2022 peak before stabilizing. Margins compressed. Management held the R&D budget flat in renminbi terms, which meant R&D as a percentage of revenue spiked uncomfortably. Shareholders grumbled. Zhou held the line.

A reasonable investor who has watched the analog industry for a long time will recognize the posture. This is what TI did through the dotcom bust. This is what ADI did through the 2008 crisis. You do not cut R&D in an analog downturn, because the products you do not design during the downturn are the products you do not sell during the recovery. Whether Zhou can sustain this discipline through multiple cycles, and whether the culture will hold as the company scales, is the most important management question on the table.

Because the next phase of 3Peak's story is not going to be built primarily inside the walls in Suzhou. It is going to be built through acquisition.

V. M&A and Capital Deployment: The C-CHIP Play

For the first fourteen years of its existence, 3Peak did not acquire anyone. This is unusual. Analog in the United States is practically defined by M&A; the industry's modern structure was shaped by ADI buying Linear Technology, Maxim merging into ADI, Microchip buying Microsemi, and so on. The playbook is so entrenched that the default assumption about a well-capitalized analog company is that it will use its cash to buy adjacent catalogs. 3Peak ignored the playbook and grew organically through its first decade, then through its IPO, and then for another two years beyond that.

Why? Two reasons, both characteristic of Zhou. First, he was skeptical that Chinese analog companies were mature enough to buy from. Most of them, in his view, had thin product lines, immature processes, and teams that had not yet earned the right to be acquired. Second, he was—and is—worried about the integration problem. Analog engineering cultures are idiosyncratic. Bolting two of them together rarely produces a sum greater than the parts. The failed integrations in the US analog industry, from the inside, are legend.

What finally moved the needle was a specific strategic gap: high-speed data converters. Data converters—analog-to-digital converters (ADCs) and digital-to-analog converters (DACs)—are the single highest-value class of chips in the analog world, and high-speed converters are the crown jewels. They are the chips that digitize radar, radio front-ends, and medical imaging signals at gigahertz rates. A company that can build competitive high-speed ADCs has, by extension, demonstrated mastery of the hardest corner of analog. Texas Instruments and Analog Devices dominate this space globally. 3Peak, for all its strength in signal-chain and precision products, did not have a credible high-speed ADC line. The gap in the portfolio was visible to every major customer. It was also the specific gap that made 3Peak a "partial platform" rather than a "full platform" supplier.

The answer was Silicon Integrated, known as C-CHIP. C-CHIP was a smaller, specialized Chinese analog company with a focused portfolio in high-speed converters and radio-frequency front-end products. It had the team, the IP, and the process relationships to ship competitive high-speed ADCs. It had also, critically, gone through multiple rounds of private financing and had the sort of sophisticated cap table that could be cleanly rolled up. The acquisition, completed in stages, landed around the hundred-million-dollar-equivalent range for the control stake, with the exact structure disclosed in the filings but not simple to reduce to a headline number.

Did 3Peak overpay? The honest answer is that the pure revenue multiple looked high by the standards of how Western buyers typically value analog targets. But three things mitigate that framing. First, Western multiples for high-speed data converter companies, when they trade at all, are nosebleed multiples—because the IP is rare and the competitive set is tiny. Second, the price tag included not just the existing product portfolio but the engineering team itself. In analog, a good high-speed converter team of thirty engineers has taken, in some cases, a decade to assemble. You cannot recreate it with a greenfield hiring budget. Third, 3Peak was not buying future cash flows on a DCF basis. It was buying time. Every year that 3Peak did not have a competitive high-speed ADC line was a year during which full-portfolio competitors could foreclose them from the highest-value sockets. From that angle, paying a premium to collapse the time horizon was not irrational. It was, arguably, the only credible option.

There is a deeper strategic logic. Prior to the acquisition, 3Peak was a signal-chain company with a growing power-management business. It sold parts. After the acquisition, the company could pitch itself as a full-stack analog partner—a vendor that could walk into a customer's system architect and have a credible conversation about the entire analog signal path, from sensor to digitizer to power delivery to isolation. The competitive relevance of this is profound. TI and ADI have always sold on platform rather than on part. A customer design team that uses TI for the op-amp, the ADC, and the power rail has lower total integration risk than one that mixes vendors. Until the C-CHIP acquisition, 3Peak could not credibly make the same platform pitch. After it, they could—at least in the target verticals.

The integration has not been frictionless. Bringing a second engineering culture into Suzhou required organizational rearrangement, and several key C-CHIP hires departed during the first 18 months, which is typical. But the product roadmap came through, and the first co-designed products under the combined engineering team hit production in 2024. Those products are now being qualified into high-end industrial and defense-adjacent sockets, some of which have historically been all but unreachable for domestic suppliers.

What this says about capital allocation going forward is interesting. 3Peak's cash position remains substantial post-IPO, and management has signaled openness to further selective M&A, particularly in areas where organic development would take five or more years—RF front-ends, isolated gate drivers, specialized power products for automotive. The operative words are "selective" and "strategic." Zhou has repeatedly emphasized that the company will not do acquisitions simply for accounting purposes or to pad the revenue line. Whether that discipline holds over time, as the company gets larger and the temptation to buy growth increases, is another open question.

Meanwhile, the acquired capabilities were being deployed into a growth vector that, as of 2026, is larger and faster-moving than anyone at the original signal-chain business would have predicted.

VI. The "Hidden" Growth Engine: Automotive & Power

There is a particular kind of meeting that happens inside every electric vehicle company when the first sample batch of a new power module arrives from manufacturing. The engineers wheel it onto a bench, hook it up to a dyno, and run the test sequence. And if you are watching carefully, you will notice that one of the first things they check is not the torque curve or the thermal performance. It is the noise floor on the battery management system. Because in an EV, the single most valuable thing in the car—the battery pack—is also the most dangerous if managed badly. And a battery management system that reports a wrong cell voltage by ten millivolts is not an inconvenience. It is a recall.

This is the world 3Peak has been quietly entering for the last three years.

If you opened 3Peak's income statement in 2019, the picture was dominated by signal-chain products—op-amps, comparators, voltage references, the bread-and-butter of industrial analog. Power management was a small line item. Isolation was almost nonexistent. By 2024, the picture had changed. Power management and isolation had grown faster than the company as a whole, with both segments turning in well above-average growth rates while the core signal-chain business, larger and more mature, compounded more slowly. The strategic implication is significant: the growth engine of 3Peak is no longer what the public market narrative—the "Chinese TI"—would suggest. It is, increasingly, what the "Chinese ADI" or even the "Chinese Silergy" narrative suggests.

Let's take these two segments in turn, because they represent very different market dynamics.

Power management first. The power management integrated circuit market in China has a peculiar structure. At the low end—commodity DC-DC converters, linear regulators, LED drivers for consumer applications—it is brutally competitive, with dozens of domestic suppliers and shrinking margins. 3Peak largely avoided this end of the market. At the high end—power for automotive, industrial, and communications infrastructure—the market is much more attractive, with fewer players, longer qualification cycles, and margins that can reach mid-50s on a gross basis. 3Peak aimed here. The company's high-voltage DC-DC converters, buck controllers, and increasingly its isolated gate drivers are finding their way into EV powertrains, charging infrastructure, and industrial motor drives.

Now isolation. If there is one chip category in modern vehicles that almost nobody outside the industry knows about, but that is absolutely critical to the future of electrification, it is the digital isolator. Here is why. Inside every modern EV, you have two electrical domains that cannot talk to each other directly. On one side, you have the high-voltage domain: the 400-volt or 800-volt battery pack, the traction inverter, the onboard charger. On the other side, you have the low-voltage domain: the 5-volt and 12-volt world of the microcontroller, the CAN bus, the ADAS computer. A stray voltage from the HV side touching the LV side will, at minimum, destroy a bunch of silicon. At worst, it will electrocute a person.

The digital isolator is the firewall. It is a chip that passes digital signals across a capacitive or inductive barrier without any direct electrical connection. Analog Devices and Texas Instruments dominate this market globally, and until recently, essentially no Chinese EV maker had a credible domestic isolator supply. When 3Peak rolled out its isolator family and started qualifying it into automotive and industrial customers in 2022 and 2023, it was pushing on an open door. Every Chinese EV OEM wanted a second source. Every industrial automation vendor wanted to localize. 3Peak was among the first domestic suppliers with a competitive, automotive-grade isolator portfolio.

The battery management system opportunity is an even larger wedge. A single EV battery pack can contain hundreds of lithium cells, and every one of them needs to be monitored for voltage, current, and temperature. The chips that do this—battery management ICs—are a concentrated category dominated by a handful of players. 3Peak's entry into BMS represents a structural long-term play. These sockets, once won, last for the entire life of a vehicle platform, which in Chinese EV land is typically five to seven years. The company is not going to win every platform. But winning even one significant platform with a major OEM is a multi-year annuity stream.

Why is all of this so much more interesting than the core signal-chain business? Two reasons. First, automotive and power are structurally higher-growth end markets than general industrial. The global vehicle parc is electrifying, and the analog content per vehicle in an EV is two to three times that of an internal combustion vehicle. Second, these sockets have higher switching costs. Once a 3Peak digital isolator is qualified into a BYD or NIO electrical architecture, it stays there for the generation. Rewinning that socket is extremely expensive for a competitor, because it requires requalification, requalification, and another requalification.

There is a flip side. Automotive customers are more demanding, more price-sensitive in volume, and far less forgiving of quality issues. A single field failure in an automotive application can cost a chip supplier tens of millions of dollars in recall exposure and years of reputational damage. 3Peak has been deliberate about how fast it enters automotive specifically because of this risk profile. Management has repeatedly emphasized that the company will not chase volume at the expense of quality. That posture has kept growth in these segments slightly slower than the maximum achievable rate, but it also keeps the tail risk in check.

The near-term operating question is simple. Can power and isolation continue to outpace signal-chain by roughly 2x, as management has implicitly guided? If yes, the segment mix of 3Peak shifts materially over the next three years, and the company's growth profile starts to look less like an industrial-cycle play and more like a long-dated structural growth story tied to Chinese electrification. If no, then the story reverts to whatever happens in the general industrial cycle, which has been mediocre for the last eighteen months.

The answer depends, in significant part, on whether 3Peak's competitive position holds up. Which means we need to talk about frameworks.

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

The reason to apply frameworks to a company is not to tick a checklist. It is to force yourself to ask the questions that the narrative obscures. For a company like 3Peak, where the bullish narrative of "domestic substitution" is easy and the bearish narrative of "geopolitical normalization" is also easy, the frameworks matter because they force specificity. What exactly is the moat? Where exactly is it thin? And what would it take to break it?

Let's walk through Hamilton Helmer's 7 Powers with some honesty.

Switching costs are the strongest power 3Peak has, and they are stronger than most investors appreciate. Once an analog chip is designed into an industrial or automotive system, it is physically embedded in the schematic, the layout, and the bill of materials. Replacing it requires board-level rework, requalification under all operating conditions, customer approval, and—in regulated industries—regulatory recertification. The total cost of switching a qualified industrial analog chip is, anecdotally, in the range of several hundred thousand dollars per design, and the time cost is measured in quarters, not weeks. For a chip that costs a few dollars, this math almost never makes sense absent a failure. Which is why, once a socket is won, revenue from that socket is remarkably durable. This is the core of the analog moat, and it is the single best argument for owning analog companies over digital ones.

Cornered resource in 3Peak's case is the analog engineering talent pool, particularly in Suzhou and Shanghai. There are a genuinely small number of analog IC designers globally—estimates put the population at a few tens of thousands, and the subset capable of leading a new product from concept to qualification at maybe 10 percent of that. 3Peak's hiring footprint in the Chinese analog talent ecosystem is significant, and the retention structure, with its multi-year vesting schedules, is explicitly designed to lock in the most productive engineers. This is not an infinite cornered resource—analog designers do move jobs, and new ones are being trained at Chinese universities—but it is a meaningful one, and it compounds with every year of retained team cohesion.

Counter-positioning is more subtle. 3Peak's counter-positioning is not against TI directly. It is against TI and ADI's inability to provide concierge-level support to mid-sized Chinese customers. A Chinese industrial OEM doing roughly $100 million in annual revenue is, to TI's global sales organization, a rounding error. TI will ship them chips, but TI's top field engineers will not fly to Chengdu to help them debug a power integrity issue on Monday morning. 3Peak will. Whether this counter-positioning survives as 3Peak scales is a real question. The company is rapidly adding customers, and maintaining concierge-level engagement across a much larger base is hard. But in the current moment, and particularly for the long tail of mid-sized customers, it is a real source of competitive advantage.

Scale economies are not yet a major power for 3Peak. The company is still well below the scale of TI or ADI, and the advantages of massive scale—internal 300mm wafer capacity, deeply amortized fixed costs, global distribution infrastructure—remain tilted decisively in favor of the incumbents. This is one of the real structural vulnerabilities in the 3Peak story, and we will return to it in the bear case.

Network economies, branding, and process power are either not applicable or weakly present. Analog chips do not have network effects. Branding matters modestly in B2B contexts but is not a dominant power. Process power—the accumulated way the company does things—exists at 3Peak but is not yet uniquely differentiating against global competitors.

Now Porter's Five Forces, applied to 3Peak's industry positioning.

Threat of substitutes: low. The laws of physics require analog chips in any system that touches the real world. The long-running fantasy that digital SoCs will "absorb" analog functionality has largely not panned out, because the precision, power, and voltage handling requirements of serious analog work are not compatible with deep-submicron digital processes. Analog is a structural, permanent category.

Bargaining power of buyers: moderate, and improving for 3Peak. In a commodity analog context, buyers have significant power because there are many substitutes. But in industrial and automotive sockets where 3Peak has become a sole-source or near-sole-source domestic supplier, buyer power weakens substantially. Some of 3Peak's most profitable sockets are, by design, ones where the customer would prefer not to disclose the supplier publicly.

Bargaining power of suppliers: moderate. 3Peak is fabless and depends on foundry partners—primarily Chinese foundries like SMIC and HuaHong, with some use of TSMC and GlobalFoundries for certain processes. Foundry capacity for the specialty analog processes that 3Peak uses is not particularly constrained today, but it can tighten quickly in cycles. The dependency on SMIC specifically is worth watching given its own geopolitical exposures.

Threat of new entrants: high in theory, lower in practice. Chinese state investment funds have poured capital into new analog startups over the last five years, and dozens of new entrants have launched product lines. Very few of them have the catalog depth, the qualification base, or the engineering cohort to seriously contest 3Peak's core sockets. The effective threat is higher in the hot new product categories—gate drivers, isolation, BMS—where 3Peak itself is a recent entrant, than in the established signal-chain categories where 3Peak's design-ins are entrenched.

Industry rivalry: intense in commodity analog, more benign in precision industrial and automotive. The market is not one homogeneous space; it is a collection of sub-markets with very different competitive dynamics, and 3Peak has mostly positioned itself in the better sub-markets.

Put it all together and the picture that emerges is not simple. 3Peak has a real moat, grounded in switching costs and talent, supplemented by counter-positioning at the mid-market. It does not yet have scale economies on par with the incumbents. Its moat is deepest in industrial and automotive, thinner in consumer and commodity. The question is how all of this will look as the competitive environment evolves.

Which brings us to the pivot the company is currently executing.

VIII. Inflection Point 2: The Multi-Product Pivot

There is a phrase that you hear more and more often inside 3Peak in 2026: "from hundreds to thousands." It refers to the SKU count, and it describes a deliberate strategic shift that is, quietly, one of the most important things happening at the company.

For most of its history, 3Peak's catalog was narrow. Focused. The company would pick a product category—precision op-amps, for instance—build a family, ship it, and move to the next. The total SKU count through 2021 hovered around 500. That is a respectable catalog for a focused specialist, but it is nowhere near the 100,000+ SKU catalogs of TI or ADI. The narrow catalog was a feature, not a bug: 3Peak's engineering bandwidth was finite, and it was directed at depth, not breadth.

Starting in 2022, and accelerating through 2024 and into 2026, the strategy has changed. The company has been systematically expanding across adjacent product categories, and the SKU count has climbed into the multi-thousands. Power management families have multiplied. Isolation products have expanded. Interface chips—RS-485, CAN, LIN—have been added. Clock and timing products. Specialty converters. The catalog is broadening, and with it, the surface area against which 3Peak can compete.

Why is this pivot happening now? Three reasons.

First, the substitution tailwind has matured. In 2019 and 2020, the game was to replace a specific TI or ADI part that a Chinese OEM already had in a design. The list was finite. The strategy was defensive. By 2024, most of the easily substitutable parts had been substituted. To grow from here, 3Peak needs to be on the original bill of materials for new designs, not just a drop-in replacement for old ones. That requires breadth. A customer architecting a new EV platform does not want to use seven different vendors for seven different analog categories if she can use two. The full-platform pitch requires a full-platform catalog.

Second, the acquisition of C-CHIP made the platform pitch finally credible. With high-speed data converters in the portfolio, 3Peak could say, without caveats, that it covered the entire signal path. That opened conversations with system architects that had previously been off-limits.

Third, the domestic competition is not standing still. SG Micro, Silan, AnalogySys, and a constellation of state-backed analog startups are all expanding their own catalogs. The risk of sitting still and being outflanked by a competitor with a broader portfolio is real. If 3Peak remained narrow, it would be structurally disadvantaged in multi-product platform pitches against competitors who were broadening.

The execution risk here is substantial. A company that has built a culture around depth is now being asked to execute on breadth. The discipline required to launch multiple new product families in parallel, without sacrificing quality on any of them, is a completely different organizational muscle. Management has reorganized the company into product-line business units to support this, but whether the transition will be smooth is not yet clear. Some of the early new-category products have taken longer than planned. Some have required respins. This is normal for category expansion, but it does mean that the next two years will be a period of investment without commensurate revenue, and margins will reflect that.

The second part of the pivot is geographic. Historically, more than 90 percent of 3Peak's revenue came from Chinese customers. The company has begun to invest in international sales infrastructure, particularly in Southeast Asia and India, where local OEMs are increasingly open to Chinese analog suppliers. The logic is straightforward: at some point, the Chinese domestic market alone will not be enough to drive double-digit growth, and the company will need to sell globally to sustain its trajectory. The question of whether international customers will trust a Chinese analog vendor, in a world of ongoing technology tensions, is genuinely open. Early signs from the Indian and Southeast Asian markets have been encouraging; the Western market remains, for now, essentially closed.

The honest assessment of the pivot: it is the right strategy, and it is the only viable path to 3Peak becoming a genuinely global analog platform rather than a Chinese-market specialist. The execution will take three to five years, and the near-term financials will reflect the investment. Patient shareholders who trust management's ability to execute category expansion will be rewarded if the strategy works. Impatient shareholders may find the margin trajectory frustrating.

And this is where we arrive at the bull-bear debate.

IX. Conclusion & The Bull/Bear Case

Every investment thesis is a bet about which force will dominate over a long horizon. For 3Peak, the question is whether the structural reshaping of the global semiconductor supply chain—which has so dramatically favored the company over the last five years—will continue, or whether the forces will reverse, or whether something more nuanced and interesting happens in the middle.

Let's lay out the cases.

The bear case, in its clearest form, goes like this. 3Peak's extraordinary revenue growth from 2019 through 2022 was overwhelmingly driven by the "domestic substitution" tailwind: Chinese OEMs being politically required, or economically motivated, to swap Western analog chips for Chinese alternatives. That tailwind is not permanent. If, at some point in the next five years, US-China technology tensions ease materially, Chinese OEMs will face less pressure to maintain domestic suppliers, and some of them will return to the cheaper, deeper-catalog, higher-scale incumbents. TI and ADI have not stopped innovating. TI's 300mm wafer fab strategy gives it structural cost advantages that no Chinese fabless company can match. ADI's catalog depth from the Linear Tech and Maxim integrations is formidable. If the political weather changes, the "low-cost domestic alternative" pitch reverts to being a low-margin pitch.

The bear case is also attentive to cyclicality. Analog is a cyclical industry, and the last two years have reminded everyone that the up-cycle of 2021 was not sustainable. Inventories at customers, capacity at foundries, and pricing in end markets all move in cycles. 3Peak's financials during the recent downturn have shown that the company is not immune; revenue declined from peak, margins compressed, and operating leverage worked in reverse. A prolonged analog downturn, coinciding with a normalization of US-China trade tensions, would be the worst-case scenario.

There are also narrower risks worth naming. Concentration in key customers—particularly those in the Chinese telecom and EV sectors—means that a single customer's downturn can move 3Peak's line. Dependence on SMIC and other Chinese foundries creates a second-order geopolitical exposure; if SMIC itself is further constrained by US export controls, 3Peak's capacity access tightens. The category expansion into automotive creates new quality-related tail risks that the company has historically not faced at scale. And the R&D spend, while strategically correct, is consuming free cash flow at a rate that some investors find uncomfortable.

Now the bull case, which is different than a simple inversion of the bear case.

The bull case starts with the observation that 3Peak is not, or is no longer, simply a Chinese substitution play. It is increasingly a platform company. Once a 3Peak chip is designed into a Huawei base station, a BYD inverter, or a Mindray medical imager, it stays for ten years. And the platform sell—the ability to cross-sell power management, isolation, data converters, and signal-chain into a socket originally won with an op-amp—is a multiplier that the single-product narrative misses. Every new design-in is not just a revenue point; it is a foothold from which three, five, or ten additional products can be sold.

Second, the bull case recognizes that Chinese industrial modernization is a structural force with decades of runway ahead. China is in the middle of a major industrial productivity transition: EVs, automation, renewable energy, advanced medical devices, and increasingly AI-adjacent industrial systems. Every one of these segments consumes more analog content per unit than the segments they replace. 3Peak is positioned squarely in the path of this build-out. Even if the geopolitical overlay moderates, the underlying industrial demand does not.

Third, the bull case points to the moat. Switching costs in analog are, as discussed, durable. The designs 3Peak won during the substitution wave of 2019–2022 are embedded in products that will ship for the next decade. That revenue base is remarkably sticky, regardless of what happens to new design-in momentum.

Fourth, the bull case takes the platform expansion seriously. If the company can execute the pivot from 500 to 2,000+ SKUs, and can transition from a signal-chain specialist to a full-stack analog vendor, then the long-term earnings power of the business is meaningfully higher than where current margins suggest, because the SG&A and R&D fixed costs are leveraged over a larger catalog. The math of analog platforms is that the first billion of revenue is painful and the fifth billion is very profitable. 3Peak is still on the early side of that curve.

Put the two cases together, and the honest read is that 3Peak is a company with a real moat in its core sockets, a credible strategy for growth adjacencies, a capable founder-CEO, and a structural tailwind from Chinese industrialization—with exposure to a geopolitical variable that could cut either way, cyclical risk in the short term, and execution risk on the platform pivot.

A few themes for a long-term investor to watch. Among the dozens of line items in the quarterly report, three data points are disproportionately informative.

The first is segment mix, specifically the share of revenue from power management and isolation combined. This is the leading indicator of whether the pivot to automotive and industrial electrification is working. If that combined share is growing year over year, the strategy is on track. If it plateaus, the bear case grows louder.

The second is gross margin. 3Peak's gross margin is the real-time report card on whether the catalog expansion is capturing higher-value sockets or drifting into commodity. The company's margin profile through the recent downturn has been compressed, but stabilization and recovery in the mid-to-high fifties is the signal that the premium-end positioning is holding.

The third is R&D intensity, measured as R&D expense as a percentage of revenue. This is a counterintuitive KPI because a falling ratio is often bad news: it either means revenue is outgrowing the R&D budget (good) or it means management is cutting R&D to prop up margins (very bad). Watching the absolute renminbi spend on R&D, alongside the revenue trajectory, tells you what kind of company 3Peak is becoming. A company that sustains high absolute R&D through cycles is one that will still have a moat ten years from now.

Myth versus reality for a moment. The market narrative on 3Peak is "Chinese TI." This is a useful shorthand, but it is wrong in two important directions. TI is a digital-cost-advantaged analog giant with massive internal wafer capacity and a 60-year catalog; 3Peak is neither cost-advantaged in the TI sense nor remotely as deep. In the other direction, the narrative understates the degree to which 3Peak is evolving into a platform play across signal chain, power, and isolation. The more accurate analog would perhaps be "Chinese mid-cap ADI," but even that is imperfect. What 3Peak actually is, as of 2026, is a company roughly twelve to fifteen years into a thirty-year build-out, with a real moat in its core and a high-variance pivot into its next phase.

As a closing observation, it is worth stepping back from the company itself. 3Peak is not just a chip company. It is a bet on a specific vision of how the global technology economy reorganizes over the next generation. In one future, the global technology supply chain partially decouples into parallel ecosystems, and companies like 3Peak become the analog backbone of the Chinese-aligned ecosystem, with durable moats, high returns, and stable geopolitical demand. In another future, the decoupling reverses, efficiency wins, and the global incumbents regain share in Chinese end markets. In the most likely future—which is probably some messy middle—both ecosystems persist, 3Peak wins within its core geography and selected export markets, and the company's long-term earnings trajectory is a function of Chinese industrial demand more than of geopolitics. Investors who want to hold 3Peak are, implicitly, taking a view on which of these futures is more likely.

What the company itself will do, meanwhile, is what it has always done: keep hiring analog engineers, keep qualifying parts, keep winning sockets one design review at a time. Zhou will keep reviewing schematic pages. The cleanroom in Suzhou will keep running. And somewhere, on some obscure oscilloscope in some customer's lab, another squiggle will emerge—clean, precise, 24 bits of signal pulled out of a noisy physical world. The art of analog does not scale linearly, does not double every eighteen months, and does not make for dramatic press releases. It compounds quietly, one decade at a time. Which, for the right kind of investor, might be exactly the point.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube