Asymchem Laboratories: The Green Chemistry Engine of Global Pharma

I. Introduction & Episode Roadmap

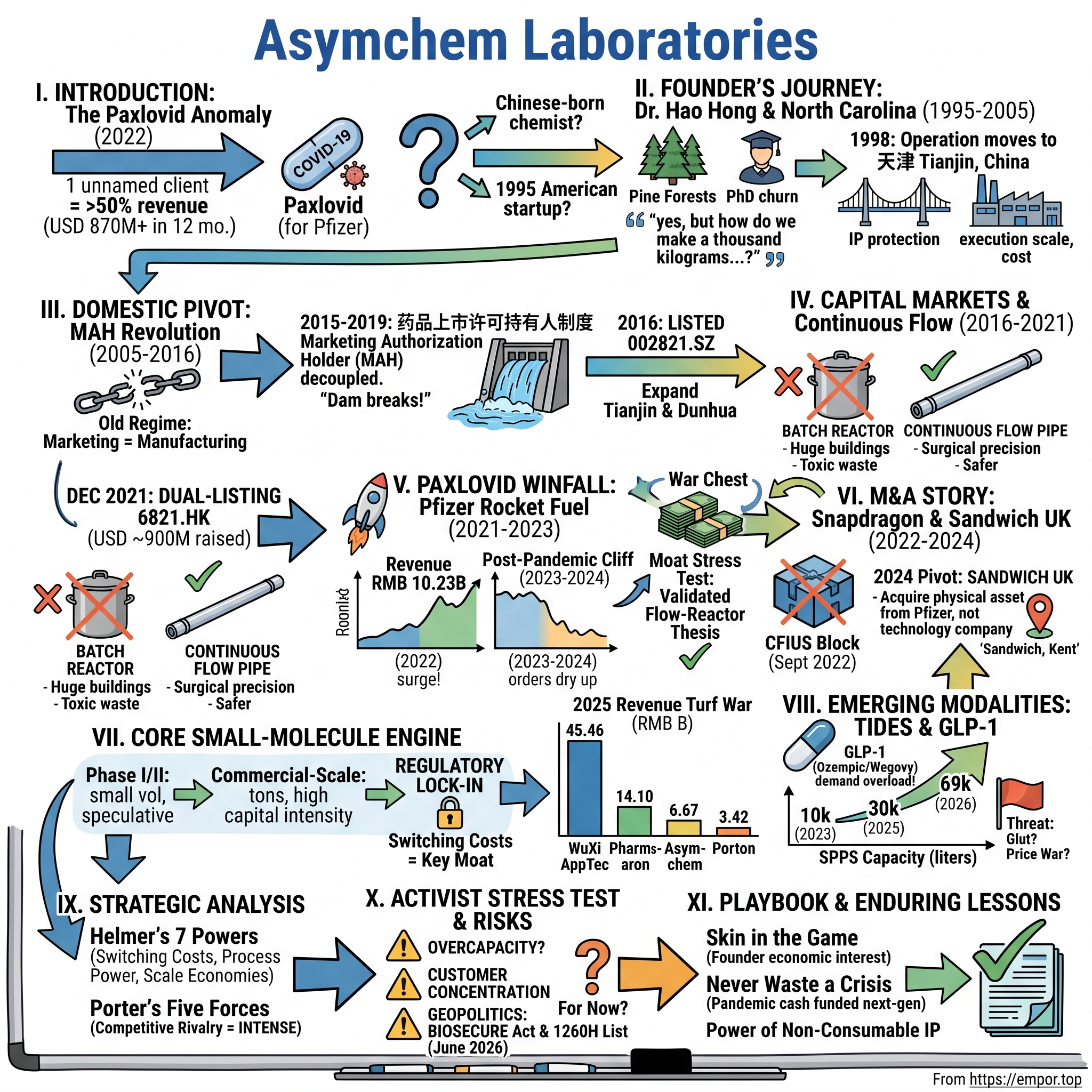

In the spring of 2022, a curious anomaly rippled through the financial filings of a company most Western investors had never heard of. A mid-sized Chinese chemical manufacturer, headquartered in the industrial sprawl of Tianjin, reported that a single unnamed "large multinational pharmaceutical company" had become responsible for more than half of its entire business. The customer was anonymized in the prospectus language, referred to only as a major overseas client. But the timing, the chemistry, and the sheer scale gave it away. The customer was 辉瑞 Pfizer. The product was Paxlovid, the oral antiviral that became the most rapidly deployed novel small-molecule drug in pharmaceutical history. And the company quietly cranking out hundreds of metric tons of its active ingredient was 凯莱英 Asymchem Laboratories (Tianjin) Co., Ltd.[^1]

Here is the part that should make any business historian sit up: this firm, which generated over USD 870 million in revenue from that one customer in twelve months, did not begin life in China at all. It was founded in 1995 in the woods of North Carolina's Research Triangle Park by a Chinese-born chemist with a post-doctoral pedigree and a conviction that the future of drug manufacturing belonged to whoever could make molecules cleaner, faster, and cheaper than the incumbents. How does a tiny American startup laboratory become the high-tech, low-waste backbone of a pandemic-defining blockbuster — and then use that windfall to position itself for the next gold rush in human medicine?

That is the story we are telling today. The company trades under two tickers: 6821.HK on the Hong Kong Stock Exchange and 002821.SZ on the Shenzhen Stock Exchange, a dual-listed structure that itself tells a story about straddling two financial worlds.8 Its market capitalization sits in the rough neighborhood of USD 3–4 billion — a fraction of the giants it competes against, yet it punches well above its weight on a single dimension: process technology.

A word on what Asymchem actually is, because the acronym soup of the drug industry hides more than it reveals. Asymchem is a CDMO — a Contract Development and Manufacturing Organization. When a biotech or a Big Pharma company invents a new molecule but does not want to build a factory to make it, they hire a CDMO. The CDMO figures out how to manufacture the compound at scale (the "development" part) and then actually produces it under regulatory-grade conditions (the "manufacturing" part). Think of it as the contract chip foundry of the pharmaceutical world — the TSMC to the drug industry's fabless designers. Asymchem does this primarily for small-molecule drugs: the classic pills and capsules built from precisely arranged carbon, hydrogen, oxygen, and nitrogen atoms.

Here is our roadmap. We will trace the founder's improbable journey from a North Carolina bench chemist to the architect of a multi-billion-dollar enterprise. We will explain the regulatory earthquake in China that turned Asymchem from a pure exporter into a domestic powerhouse. We will dig into the Paxlovid windfall — the single most consequential contract in the company's history — and the inevitable cliff that followed. We will war-game the competitive chessboard against the towering 药明康德 WuXi AppTec and the fast-following 康龙化成 Pharmaron. We will dissect the blocked American acquisition that taught Asymchem a brutal geopolitical lesson, and the European pivot that answered it. And we will scrutinize the bet that now defines the company's future: a frantic, capital-intensive race to build peptide manufacturing capacity for the GLP-1 weight-loss revolution. Throughout, we will keep one question front of mind — not whether management says it will win, but what evidence actually supports the claim, and what could prove it wrong.

It begins with a chemist who decided he could do it better.

II. The Chemistry of the Founder: Dr. Hao Hong & the Founding of Asymchem (1995–2005)

Picture the Research Triangle Park in the mid-1990s. Tucked between Raleigh, Durham, and Chapel Hill, it was the closest thing the American South had to a science campus paradise — pine forests, low-slung labs, and a steady churn of PhDs flowing out of Duke, UNC, and NC State. It was here, after a post-doctoral stint at the University of Georgia, that 洪浩 Dr. Hao Hong made a living as a process chemist. And process chemistry, it should be said, is an unglamorous craft. Discovery chemists get the headlines for inventing new drug molecules. Process chemists are the ones who answer the deflating follow-up question: yes, but how do we make a thousand kilograms of it without blowing up the plant or generating a swimming pool of toxic waste?

Hong was, by all accounts, very good at this unglamorous craft. And in 1995 he made the leap that defines every founder story — he decided the people he worked for were leaving value on the table, and he could capture it himself. He founded Asymchem in North Carolina with a deceptively simple proposition: sell high-end process chemistry services to Western pharmaceutical innovators who would rather outsource the headache.

To understand why this was a smart bet, you have to understand what was happening to Big Pharma's business model in the late 1990s. For most of the 20th century, the great drug houses — Merck, Pfizer, GSK, Eli Lilly — were vertically integrated cathedrals. They discovered molecules in-house, ran the clinical trials in-house, and built sprawling manufacturing complexes in New Jersey and Indiana to produce the finished goods in-house. But two tectonic shifts were underway. First, drug discovery was migrating outward, to nimble venture-funded biotech startups who could chase risky science the lumbering giants avoided. Second, drug manufacturing was increasingly seen not as a core competency but as a cost center to be outsourced — a function you could hand to a specialist who did nothing else and did it cheaper. The CDMO industry was being born out of this great unbundling, and Hong had positioned himself directly in its path.

But Hong saw a flaw in his own setup almost immediately. North Carolina was wonderful for one thing: proximity to customers. American pharma executives could drive over, tour the lab, and trust that the chemistry was being done to Western standards. What North Carolina could not provide was cheap, abundant chemical-engineering talent and the raw physical footprint — the land, the reactors, the plant labor — needed to scale a chemical operation from grams to tons. Those things were expensive in the United States and getting more so.

So Hong did something that, in hindsight, looks visionary, but at the time was a genuine gamble with his young company's survival. In 1998, he moved the operational guts of Asymchem — the actual chemistry and manufacturing — to 天津 Tianjin, China, while keeping the commercial front-end and customer relationships rooted in the United States. This was the founding architecture of the entire enterprise, and it is worth naming plainly: Western intellectual-property protection and customer trust, paired with Chinese execution scale and cost. American clients got an American-facing partner they could sue, audit, and rely on. The molecules got made by a deep bench of Chinese engineers at a fraction of the Western cost.

It is tempting to romanticize this as foresight, and partly it was. But it was also a structural arbitrage that dozens of firms would later copy — most famously WuXi, founded the same era. What separated Asymchem from a commodity labor-arbitrage shop was Hong's insistence, even in these lean early years, that the company's edge had to be technological, not merely cheap. He was a chemist first and a businessman second, and he kept steering capital toward process innovation — finding shorter, higher-yielding synthetic routes — rather than simply adding cheap reactor volume. That instinct would not pay off for nearly two decades. But it was the seed of everything that came later.

For now, though, Asymchem was a minnow. Through the early 2000s it was a small, export-only operation, almost entirely dependent on a handful of Western clients, with revenue that would barely register on a Big Pharma balance sheet. Its fortunes were bound to a question it could not yet answer: what would happen if China's own pharmaceutical industry ever woke up?

III. The Domestic Pivot: Decoupling and the Chinese MAH Revolution (2005–2016)

For its first two decades, Asymchem lived an oddly bifurcated life. Its body was in China; its wallet was in the West. Well over 90% of its revenue came from American and European multinational pharmaceutical companies. A visitor to the Tianjin plant in, say, 2012 would have found Chinese chemists in Chinese lab coats making molecules destined almost entirely for clinical trials and pharmacy shelves in Boston, Basel, and London. The home market — the enormous, fast-growing Chinese pharmaceutical sector right outside the factory gates — was almost irrelevant to the business.

Why? The answer reveals something fundamental about how innovation gets strangled or unleashed by regulation. China's domestic pharma industry in this era was vast but technologically shallow. It was dominated by generic-drug manufacturers competing on price in a brutal commodity scrum. Genuine homegrown biotech innovation — companies inventing genuinely new molecules — was virtually nonexistent. And there was a specific, almost bureaucratic reason for this drought, one that would take an act of the state to fix.

Under the old Chinese regulatory regime, a drug's marketing approval was welded to its manufacturing license. In plain terms: if you invented a new drug in China, you could not simply hire a factory to make it. You had to own the factory. The marketing authorization and the production license were a single, inseparable bundle. For a cash-strapped biotech startup with a promising molecule and no money, this was a death sentence. Before you could ever sell a pill, you had to raise enough capital to build and validate an entire manufacturing plant — a redundant, capital-destroying requirement that funneled scarce money into concrete and steel instead of science. It is hard to imagine a policy more perfectly designed to suffocate a domestic innovation ecosystem. And it meant a CDMO like Asymchem had almost no domestic customers, because Chinese drug developers structurally could not outsource.

Then came the earthquake. In 2015, the Chinese government launched a pilot program for what is called the 药品上市许可持有人制度 Marketing Authorization Holder (MAH) system, later formalized nationally in the 2019 revision of the Drug Administration Law. The reform did one elegant thing: it decoupled the right to market a drug from the obligation to manufacture it. Under the MAH system, a Chinese biotech could hold the marketing authorization for its own molecule while contracting the actual production out to a third party. The factory requirement vanished. Suddenly, a venture-backed startup in Shanghai could focus its capital on discovery and trials, and simply rent the manufacturing.

For the Chinese CDMO industry, this was the equivalent of a dam breaking. An entire category of customer that had been legally impossible now sprang into existence overnight. And Asymchem was extraordinarily well positioned to catch the flood. It already operated FDA-inspected, Western-standard facilities — the kind of high-quality, regulatorily-credible plants that the new wave of ambitious Chinese biotechs wanted their molecules made in. The domestic contracts that began flowing in were not low-margin generic work; they were higher-value innovation projects. Asymchem had spent twenty years building a Ferrari for export customers, and the MAH reform suddenly filled the domestic highway with drivers who wanted to rent it.

The company moved quickly to capitalize. In November 2016, Asymchem listed on the Shenzhen Stock Exchange under the ticker 002821.SZ. The timing was deliberate. The capital raised was channeled straight into scaling up — expanding the flagship plants in Tianjin and building out a major new manufacturing base in 敦化 Dunhua, in Jilin province. Management was, in effect, betting that both ends of the business would boom simultaneously: the established Western export engine and the newly unlocked domestic market. It was preparing for a two-front expansion.

What this period really demonstrates is a recurring theme in Asymchem's history: the company's biggest inflection points have often come not from its own brilliance but from external structural shifts it was lucky and ready enough to ride. The unbundling of Big Pharma created the export opportunity in the 1990s. The MAH reform created the domestic opportunity in the 2010s. The discipline was in being prepared — having the FDA-grade plants already built when the rules changed. But an honest investor should note the corollary: a business this leveraged to regulatory and structural tailwinds is also exposed when those winds reverse. That lesson was still years away. For now, freshly capitalized and riding two booms, Asymchem turned its attention to building a genuine, defensible technological moat.

IV. Capital Markets and Scaling Up: The Dual-Listing Play (2016–2021)

If you want to understand what makes Asymchem different from the dozens of other Chinese CDMOs that sprang up to chase the same opportunity, you have to spend a moment in a chemistry lab — specifically, at the difference between a batch reactor and a continuous flow reactor. Stay with us, because this is the heart of the company's competitive claim.

The traditional way to manufacture a drug molecule is batch chemistry, and the mental model is your kitchen. You have a giant pot — except instead of a stockpot it is a steel-and-glass reactor vessel the size of a small room. You dump in your starting chemicals, you heat and stir, you wait for the reaction, you cool it down, you drain it, you clean the vessel, and you do it all again for the next step. It is how humans have made chemicals for centuries. It works. But it has ugly properties at scale: the vessels are enormous and require huge buildings, they consume tremendous energy heating and cooling massive volumes, they generate large quantities of solvent waste, and — most dangerously — some reactions release so much heat or are so violently reactive that you simply cannot run them safely in a giant pot. The bigger the pot, the harder it is to control the temperature evenly throughout, and the more catastrophic the failure if it runs away.

继续流化学 Continuous flow chemistry inverts the entire concept. Instead of a giant pot, imagine a long, thin, temperature-controlled pipe — sometimes thinner than a drinking straw. The chemicals flow through this pipe continuously, reacting as they travel, and the finished product streams out the far end in a steady river. Because the reaction happens in a tiny cross-section at any given instant, you can control temperature and mixing with surgical precision. Reactions that are too dangerous or too finicky to run in a batch pot become tractable. You can run them around the clock. And critically, scaling up does not mean building a bigger, scarier pot — it can mean running the same little pipe for longer, or running several in parallel. The technical jargon for the advantage is superior "mass transfer and heat transfer," but the intuition is simple: a thin pipe is just a far better-behaved place to do violent chemistry than a giant vat.

Hong, the process chemist at heart, made continuous flow — alongside 生物催化 biocatalysis, the use of engineered enzymes to run reactions that would otherwise require harsh chemicals and many steps — the central pillar of Asymchem's strategy. Rather than competing as the cheapest batch shop, Asymchem positioned itself as the premium, high-technology alternative: the CDMO you hired when your molecule was too complex, too dangerous, or too inefficient to make the old way. By 2021, the company had built out continuous manufacturing capability spanning the full range from milligrams in early development to metric tons in commercial production. The pitch to a Western pharma client was compelling: bring us your ugliest, most heat-sensitive, most multi-step synthesis, and we will make it cleaner, safer, and with less waste than anyone else. A published case study of this approach — a scalable flow biocatalytic process developed for the AstraZeneca cancer drug ceralasertib — would later appear in the peer-reviewed literature, lending outside credibility to what might otherwise sound like marketing.1

It was on the strength of this story, and at the absolute peak of the global biotech funding mania, that Asymchem executed the financial move that gave it its second ticker. In December 2021, the company completed a dual-listing on the Hong Kong Stock Exchange under 6821.HK. It priced its H-shares at HK$388.00 each and raised net proceeds of approximately HK$6.85 billion — gross proceeds of roughly HK$7.15 billion, or close to USD 900 million — in one of the largest healthcare IPOs in Hong Kong that year.28 The debut itself was lukewarm; the stock slipped on its first trading day as the broader biotech bubble was already beginning to deflate.9 But the strategic logic of the raise was sound and forward-looking.

The cash was explicitly earmarked for three purposes: globalizing the R&D and manufacturing footprint, pushing into non-small-molecule "emerging businesses" — chiefly peptides and biologics — and building a financial buffer against the rising US–China trade friction that any China-exposed executive could see gathering on the horizon. In other words, even at the moment of its greatest capital-markets triumph, management was already telegraphing the two themes that would dominate the next five years: diversify the modalities, and hedge the geopolitics. What no one could have known in December 2021 was that within weeks, a single customer was about to hand Asymchem a sum of money so large it would dwarf the entire IPO — and reshape the company's trajectory overnight.

V. The Paxlovid Windfall: Pfizer's Rocket Fuel and the Post-Pandemic Cliff (2021–2023)

In late 2021, the world was desperate for a pill. Vaccines had blunted COVID-19, but there was still no convenient oral treatment for people who got infected. Then Pfizer's Paxlovid arrived, and the demand was instantaneous and astronomical — governments wanted to buy tens of millions of courses, immediately. There was just one problem, and it was a problem Pfizer could not solve alone: the active pharmaceutical ingredient in Paxlovid, nirmatrelvir, is a genuinely nasty molecule to manufacture. It requires a long, complex synthesis with steps that are exactly the kind of heat-sensitive, hard-to-control chemistry that batch reactors struggle with. Pfizer needed a manufacturing partner who could make enormous quantities of this difficult compound, fast, to Western regulatory standards. It needed exactly the kind of company Hong had spent twenty-six years building.

The contracts that resulted were staggering. Beginning in late 2021 and into early 2022, Asymchem subsidiaries signed a series of supply contracts with the unnamed "large overseas pharmaceutical company" for the API and intermediates of a small-molecule innovative drug. The combined value of these large orders came to roughly RMB 9.3 billion — on the order of USD 1.46 billion — an amount that contemporaneous industry coverage noted was about three times the company's entire prior-year revenue.3 Let that sink in: a single customer, on a single product, placed orders worth triple everything Asymchem had sold to everyone the year before. The IPO that had just raised nearly USD 900 million was, suddenly, the smaller windfall.

The 2022 financial results that followed look less like an annual report and more like a lottery ticket cashing in. Total revenue surged 121% to RMB 10.23 billion — roughly USD 1.5 billion. Of that, the Paxlovid-linked "large orders" contributed approximately RMB 5.91 billion, more than 57% of the entire company's sales.[^1] The company delivered something in the range of USD 870 million worth of these complex APIs in twelve months. For a firm that had been a respected-but-mid-sized specialist, this was a transformation in scale that normally takes a decade, compressed into a single fiscal year.

But here is the part that matters for understanding the business, as opposed to just gawking at the numbers. Delivering that volume of nirmatrelvir on that timeline was not something a company could fake or improvise. It was the single most demanding proof point in Asymchem's history, and it validated the entire continuous-flow thesis in the most public way imaginable. The reason Asymchem could make the molecule at that speed and scale — when traditional batch chemistry would have buckled under the heat-transfer and mass-transfer demands — was precisely the flow-reactor technology Hong had been quietly investing in for years. The pandemic became an unplanned, billion-dollar live demonstration that the company's core technical claim was real. When evaluating a company's "moat," investors usually have to take management's word. Here, the moat ran a stress test in front of the entire industry and held.

The windfall also transformed the balance sheet. The Paxlovid orders generated immense free cash flow, leaving Asymchem with a large cash stockpile and essentially zero net debt. This is the single most important fact in the modern Asymchem story, and we will return to it repeatedly: the company emerged from the pandemic not just larger, but liquid and unleveraged, with a war chest it had not had to borrow.

And then, as everyone knew it must, the music stopped. COVID-related demand evaporated. Paxlovid orders dried up. Total revenue fell back to RMB 7.83 billion in 2023, and then further to RMB 5.80 billion in 2024 as the last of the pandemic backlog washed out of the numbers.[^5]4 On a headline basis, this looked like a company in steep decline — revenue nearly halving in two years. A naive reading of the chart would suggest a business falling apart.

The more important question, and the one management spent its 2023 and 2024 earnings communications trying to redirect investors toward, was the trajectory of the underlying base business — revenue excluding the one-time COVID orders. Stripped of the pandemic distortion, that core business continued to grow at a healthy clip, with management pointing to underlying growth in the mid-20s-percent range.4 Now, this is exactly the kind of "adjusted" framing that warrants skepticism, because every management team in the world prefers the metric that flatters it. But in Asymchem's case the framing is structurally defensible: the COVID orders were genuinely, explicitly one-time, disclosed as such from the start, and the base-business growth was independently visible in the segment data. The cliff was real, but it was a cliff the company had told investors to expect.

What separated Asymchem's handling of the hangover from some peers is what it did with the cash. Rather than the classic CDMO mistake — over-building generic capacity at the peak and then eating massive overcapacity write-offs when demand normalized — Asymchem deployed its pandemic windfall to fund, entirely from internal cash and debt-free, its transition into the next generation of drug modalities. The crisis cash became the growth capital. Whether that bet pays off is the central open question of the rest of this story. But first, the company had to learn a hard lesson about where it was, and was not, allowed to spend its money.

VI. The M&A and Capital Deployment Story: CFIUS, Snapdragon, and the UK Sandwich Pivot (2022–2024)

Flush with pandemic cash and convinced that continuous flow was the future, Asymchem went shopping in early 2022 for the most logical target imaginable. In February 2022, it agreed to acquire Snapdragon Chemistry, a Massachusetts-based company that was, alongside Asymchem itself, one of the genuine pioneers of continuous flow manufacturing in the Western world. The price was USD 57.94 million.56 On paper, it was a beautiful fit: Snapdragon's flow-chemistry expertise slotted directly into Asymchem's own capabilities, and the deal would have given the Chinese firm a credentialed American development beachhead, offering customers a seamless path from preclinical process R&D through commercial manufacture on US soil.

It is worth pausing on the discipline of the price, because it tells you something about how management thinks. At roughly four to five times Snapdragon's revenue, the valuation was conservative by the standards of the moment. In 2021 and early 2022, at the apex of the biotech bubble, specialized high-growth CDMO technology assets were routinely changing hands at six to eight times sales or more. Asymchem, sitting on a mountain of cash that would have tempted a less disciplined acquirer into overpaying for a trophy, instead negotiated a price that looks almost frugal in context. This is a data point in favor of management's capital discipline — a theme worth tracking, because plenty of companies that strike disciplined deals on the way up abandon that discipline once the checkbook is open.

The deal never closed. In September 2022, Asymchem and Snapdragon announced they were abandoning the acquisition.7 The reason was the Committee on Foreign Investment in the United States — CFIUS — the interagency body empowered to block foreign takeovers of American assets on national-security grounds. CFIUS objected to a Chinese company acquiring continuous-flow manufacturing IP, and the two firms could not agree on mitigation terms that would satisfy the US Treasury.1011 The deal died. Within roughly a year, Snapdragon was acquired instead by Cambrex, an American CDMO, for a comparable valuation — the asset Asymchem wanted went to a buyer Washington found acceptable.12

The lesson was harsh and unambiguous, and management appears to have internalized it completely: for a Chinese company, acquiring US-based technology assets was no longer a viable path, full stop. No matter how disciplined the price or how clean the strategic logic, the geopolitical veto was now a structural reality of the landscape. A lesser management team might have kept ramming its head against that wall, or sulked and hoarded the cash. Asymchem did something more interesting. It redirected the same strategic impulse — establish a Western footprint, acquire credible capability outside China — but routed it around the geopolitical blockade.

The answer came in 2024, and it was elegant. In May 2024, Asymchem announced it would take over Pfizer's small-molecule API pilot plant and part of the development laboratories at Discovery Park in Sandwich, Kent, in the United Kingdom.13 This was the company's first manufacturing footprint in Europe. And the structure of the deal was a study in capital-efficient, geopolitically-savvy dealmaking. Consider the contrasts with the failed Snapdragon approach.

First, instead of buying a technology company — the kind of IP-rich target that triggers national-security reviews — Asymchem acquired a physical asset: a fully-built, already-compliant manufacturing site. There was no proprietary American flow-chemistry IP to seize; there was a permitted, GMP-grade British facility. Second, it bought the site directly from a long-standing customer, Pfizer, the very company whose Paxlovid orders had filled Asymchem's coffers — a relationship that smoothed the entire transaction. Third, the deal came with people: Asymchem retained a substantial group of the site's existing scientists and operators, many of them legacy Pfizer chemists who had faced redundancy, with the site expected to employ roughly 100 individuals by the end of 2024.1415 The development labs began operating in June 2024 and the API pilot plant came online that August.1617

The economic logic was compelling. By acquiring an existing, fully-permitted plant rather than building a greenfield site from scratch, Asymchem skipped an estimated three years of regulatory certification and spent a fraction of what a comparable new-build would have cost — greenfield builds of this type can run well north of USD 80 million. More importantly, the Sandwich site is a geopolitical hedge dressed up as a manufacturing facility. It gives nervous Western clients a non-China location where their molecules can be developed and made, a hands-on answer to the "what's your China contingency?" question that every pharma procurement officer now asks. Whether 100 people in Kent can become a material manufacturing alternative to the vast Chinese plants is an open question — the site is, for now, a clinical-scale development and pilot facility, not a commercial-tonnage powerhouse. But as a signal of strategic adaptability, and as an option on a de-risked Western footprint, it was bought cheaply and shrewdly. The contrast between the blocked American tech-grab and the successful British asset-purchase is, in miniature, the entire lesson Asymchem learned about operating as a Chinese company in a fracturing world.

With the geopolitical hedging underway, it is worth stepping back to the engine that actually pays for all of it — the small-molecule business that remains, windfalls and pivots aside, the beating heart of the company.

VII. The Core Small-Molecule Engine: Scale, Economics, and the Global CDMO Turf War

Strip away the pandemic noise, the peptide ambitions, and the geopolitical drama, and what is Asymchem at its core? It is a small-molecule CDMO. That cash-cow business still drives roughly 75–80% of the company's normalized revenue and profit.4 Everything else — the emerging modalities, the European sites — is either an outgrowth of, or a bet funded by, this engine. So it pays to understand exactly how the money works, because the unit economics of CDMO contracts are unusual and they explain almost everything about the company's strategic behavior.

A CDMO relationship typically begins early, when a drug is still in clinical trials, and it follows a distinctive arc. In the early phases — Phase I and Phase II, when a molecule is still being tested for safety and efficacy in small groups of patients — the volumes are tiny, the work is highly collaborative and customized, and the margins are attractive. But it is also speculative: roughly nine out of ten drugs that enter clinical trials never make it to market. The CDMO is, in effect, running a portfolio of early-stage bets, knowing most will fizzle.

The magic happens when a drug actually gets approved and moves to commercial-scale manufacturing. Now the volumes explode — from kilograms to tons — and the economics flip to high capital intensity with powerful operating leverage. But the truly valuable property emerges from regulation. When a drug is approved, the exact manufacturing process — the specific plant, the specific route, the specific reactors and quality controls — is written into the regulatory filing submitted to the FDA or its equivalents. The CDMO's process becomes part of the drug's legal identity.

This creates what is, in our view, Asymchem's single most important moat: switching costs. Once Asymchem's process is baked into an approved drug's regulatory dossier, moving production to a different CDMO is brutally expensive and slow. The new manufacturer has to be re-validated, the process has to be re-filed, and the drug-maker faces one to two years of regulatory work and millions of dollars in validation costs — all while risking a supply interruption of a product that is generating revenue every single day. In the language of business strategy, this is a textbook high-switching-cost moat, and it is the reason commercial-stage CDMO revenue is so sticky and predictable. The customer is, for practical purposes, locked in for the life of the drug. The flip side, which a careful investor must hold in mind, is that this same lock-in means winning new commercial molecules is everything — the installed base is durable, but growth depends on continually feeding the front end of the funnel with early-stage projects that survive to approval.

Now, the competitive battlefield. The Chinese CDMO/CRO landscape is dominated by a clear hierarchy, and seeing the 2025 revenue figures side by side clarifies exactly where Asymchem sits. At the top looms 药明康德 WuXi AppTec, the titan, which reported full-year 2025 revenue of RMB 45.46 billion and dominates across both laboratory research services and manufacturing.18 It is in a different weight class entirely — roughly seven times Asymchem's size. The clear number two is 康龙化成 Pharmaron, with 2025 revenue of RMB 14.10 billion, strong in research services and growing in manufacturing.19 Then comes Asymchem itself, with 2025 revenue of RMB 6.67 billion — not a generalist giant but a focused, pure-play CDMO specialist.4 And trailing in its shadow is the most direct comparable, 博腾股份 Porton Pharma Solutions, at RMB 3.42 billion in 2025, a company that has struggled to scale out of Asymchem's wake and recently swung back to a slim profit after a difficult stretch that included losing a major Novartis contract.20

The strategic takeaway from these numbers is important and easy to miss. Asymchem is not trying to be WuXi. It is not chasing the full-spectrum, discovery-to-commercial, do-everything model. It is a specialist that competes on a specific axis: process technology. And critically, it no longer wins primarily on labor-cost arbitrage — that game has commoditized, and a domestic price war has broken out in Chinese small-molecule CDMO work, compressing margins for everyone. Asymchem's actual claim to differentiation is that its flow chemistry and engineered enzymes let it compress synthetic routes — taking a synthesis that might require twelve chemical steps and re-engineering it down to five. Fewer steps means higher yield, less waste, lower cost, and faster delivery. For a Big Pharma client, a shorter route is not a marginal nicety; it can be the difference between a drug being economical to manufacture or not. That is the value Asymchem is really selling, and it is a more defensible position than "we are cheaper." Whether it is defensible enough to escape the industry-wide price war is the question its margins will answer over the next several years.

That technological edge is also, conveniently, the same toolkit Asymchem is now betting will let it win an entirely new and larger market.

VIII. Emerging Modalities: GLP-1, the "TIDES" Explosion, and Future Materiality

Every great growth story needs a second act, and Asymchem's is hiding inside an unglamorous acronym: TIDES. The term refers to peptides and oligonucleotides — two classes of larger, more complex molecules that sit between traditional small-molecule pills and full-blown biologic drugs. At Asymchem, this business lives in the segment it calls Chemical Macromolecules. And the reason it has gone, in the space of a couple of years, from a rounding error to the center of the bull case can be summarized in two letters and a number: GLP-1.

GLP-1 receptor agonists are the weight-loss and diabetes drugs that have become the defining pharmaceutical phenomenon of the decade — semaglutide (Ozempic and Wegovy), tirzepatide (Mounjaro and Zepbound), and a pipeline of next-generation dual- and triple-agonist follow-ons. Many of these blockbusters are, chemically, peptides: chains of amino acids that must be synthesized link by link. The demand for them has overwhelmed global manufacturing capacity, and the innovators who own them — chiefly 诺和诺德 Novo Nordisk and Eli Lilly — cannot make enough on their own. That supply gap is precisely the opening a peptide CDMO is built to fill.

The standard way to make these peptides is Solid-Phase Peptide Synthesis, or SPPS. The intuition is almost like beadwork: the growing peptide chain is anchored to a tiny solid bead, and amino acids are added one at a time, each in its own reaction cycle, until the full sequence is built — then the finished peptide is cleaved off the bead. It is reliable but reagent-hungry and, at commercial scale, capacity-constrained by the sheer volume of synthesis "resin" you can run. Which is why the key operating metric for this business is, bluntly, liters of SPPS capacity — and why Asymchem has been pouring its pandemic cash into a frantic capacity build-out.

The trajectory management has laid out is aggressive. Capacity stood at roughly 10,250 liters at the end of 2023, expanded toward 21,000 liters by the end of 2024, and is targeted to reach roughly 30,000 liters in 2025, with stated ambitions of around 44,000 liters by the end of 2025 and as much as 69,000 liters by the end of 2026.[^5]21 In other words, the company is planning to multiply its peptide manufacturing capacity several-fold in three years. This is not a tentative toe in the water; it is a full-bodied capital commitment.

And the revenue has begun to follow. In 2024, the Chemical Macromolecules segment generated approximately RMB 1.226 billion — around 21% of total company revenue, a share that has grown precisely because the COVID-distorted small-molecule numbers were shrinking at the same time.[^5] In the first half of 2025, the segment reached RMB 756 million, up more than 51% year over year, with management projecting the full-year figure to roughly double.22 This is no longer a novelty line item. It is a genuine, material growth engine, and the most credible answer to the question of what replaces the Paxlovid revenue.

The technological angle is what makes the bet more than a generic capacity play. Asymchem has married its continuous-flow expertise to its synthetic-biology platform — an AI-driven enzyme-engineering system it brands as STAR — to develop what it has described as the world's first commercial-scale process for a GCG/GLP-1 dual-agonist peptide, improving yields and lowering raw-material costs relative to conventional synthesis.[^25] The idea is to do for peptides what flow chemistry did for small molecules: use smarter process technology to make a hard, expensive synthesis cheaper and cleaner than rivals can.

Now for the sober counterweight, because this is where independent analysis has to push back on the narrative. A multi-fold capacity expansion is a bet, and bets can go wrong in specific, identifiable ways. If the GLP-1 innovators bring more manufacturing in-house than expected — and both Lilly and Novo have announced enormous internal capacity investments — the merchant CDMO market could be smaller than the headlines imply. If competitors expand capacity even faster (and WuXi's TIDES revenue, at RMB 11.37 billion in 2025, is already far larger than Asymchem's entire peptide business and growing 96% a year, while Switzerland's Lonza is also pouring in capital), the result could be a peptide glut and a brutal price war that destroys the very margins this expansion is meant to capture.18 Building 69,000 liters of capacity is only a good idea if there are enough committed orders to fill it. The capacity numbers are management targets; the demand to fill them is, as yet, a forecast. That tension — proven technology versus unproven demand at scale — is the crux of the investment debate, and it leads naturally into a more formal strategic dissection.

IX. Strategic Analysis: Porter's 5 Forces, Hamilton's 7 Powers, and the Tech Edge

Let us put Asymchem on the strategist's dissecting table and apply two of the standard frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — not as an academic exercise, but to pressure-test exactly where the company's advantages are real and where they are merely asserted.

Start with Helmer's 7 Powers, taking the three that genuinely apply. The first and strongest is switching costs, which we have already met as the company's primary moat. Once Asymchem's manufacturing process is written into an approved drug's NDA or BLA regulatory dossier, the customer is locked in by the prohibitive time, cost, and supply risk of re-validating and re-filing with a different manufacturer. This is high, durable, and genuinely defensible — but, crucially, it only switches on at the commercial stage. For the large pool of early-clinical projects, switching costs are low and customers shop around freely. So the power is real but concentrated in the back half of the funnel.

The second is process power — proprietary know-how embedded in how the company operates that rivals cannot easily replicate. This is Asymchem's distinctive claim and the one most central to its self-image: the continuous-flow chemistry technology and the synthetic-enzyme library, which management describes as containing on the order of 300,000 biocatalysts developed through its STAR AI platform.[^25] The Paxlovid execution and the peer-reviewed ceralasertib process lend this claim outside credibility.1 But process power is also the hardest power to verify from the outside and the most vulnerable to erosion — flow chemistry is no longer exotic, competitors are investing in the same techniques, and the enzyme-library figure is a company-supplied number. The honest assessment: process power is probably real and probably an advantage, but it is a lead, not an unassailable monopoly.

The third is scale economies, which we would rate as only moderate. Asymchem's manufacturing complexes in Tianjin, Dunhua, and elsewhere give it real purchasing leverage over raw chemical intermediates relative to a sub-scale competitor like Porton. But against WuXi, which is seven times its size, Asymchem is the one at the scale disadvantage. So scale cuts both ways depending on which rival you hold it up against.

Now Porter's Five Forces, focusing on the two that matter most. Bargaining power of buyers is a tale of two phases, mirroring the switching-cost dynamic: high during early clinical work, when customers can take their project anywhere, and low-to-moderate once a drug is commercialized and the regulatory lock-in kicks in. Competitive rivalry is the force to worry about, and it is intense. The Chinese CDMO space is crowded, and a price war has already broken out in domestic small-molecule work, squeezing gross margins across the industry. Asymchem's strategic response — leaning on its high-tech flow chemistry and its TIDES segment to protect margins — is essentially an attempt to escape the commodity rivalry by competing on technology instead of price. The threat of new entrants is muted by the capital and regulatory barriers to building credible GMP capacity, and the threat of substitutes is more of a long-term modality-shift question than a near-term force.

The synthesized verdict: Asymchem's defensibility rests overwhelmingly on the combination of regulatory switching costs (durable but back-end-loaded) and process power (real but contestable). It is a good position — better than a pure cost-arbitrage shop — but it is not an impregnable fortress. The advantage has to be continuously re-earned by staying technically ahead, because the moment the technology lead narrows, the company is exposed to the same vicious rivalry pummeling everyone else. That is precisely the kind of vulnerability a skeptical investor would press on.

X. The Activist Stress Test & Current Risk Radar

So let us play that skeptic deliberately. If a short-seller or an activist investor built a presentation arguing that Asymchem is overvalued and over-extended, what would the slides say? Steelmanning the bear case is the best way to understand what could actually break the story.

The first slide would be titled overcapacity. The bear would point straight at the peptide build-out and ask the uncomfortable question: is the planned expansion toward 69,000 liters a disciplined response to real demand, or a bubble inflated by GLP-1 hype? The argument writes itself. The GLP-1 innovators, Lilly and Novo, are spending tens of billions building their own internal manufacturing. Competitors with deeper pockets — WuXi, with a peptide business already several times Asymchem's size, and Lonza — are racing to add capacity at the same time.18 If the merchant market turns out smaller than hoped while everyone's new capacity comes online at once, the result is a glut, and gluts produce price wars that vaporize margins. A company that has spent its precious pandemic cash building reactors it cannot fill would have converted a windfall into a stranded asset. This is the single most important risk to monitor, and it is not hypothetical — it is the base-rate outcome of capacity arms races throughout industrial history.

The second slide would read customer concentration. Asymchem's modern history is, in large part, the story of a few enormous contracts. The Paxlovid orders alone were once 57% of revenue. The bear's point is sharp: a business that can be made by a single blockbuster can be unmade by the loss of one, and the post-pandemic revenue cliff was a vivid demonstration of exactly that fragility. The burden is on management to prove it has genuinely broadened its client base and is not simply waiting for the next mega-contract to paper over the gap. The diversification of the base business is encouraging on this front, but concentration risk in a contract-manufacturing business never fully disappears — by definition, a few large commercial molecules will always dominate the revenue.

And then there is the slide that overhangs every Chinese CDMO: geopolitics, and specifically the BIOSECURE Act. After years of legislative limbo, the BIOSECURE Act was signed into law on December 18, 2025, as part of the FY2026 National Defense Authorization Act.2324 In broad strokes, it moves to prohibit federal agencies from contracting with, or funding companies that use the equipment or services of, designated Chinese "biotechnology companies of concern." The law named specific firms of concern, with WuXi AppTec the most prominent target. And the screws tightened further in June 2026: on June 8, 2026, the US Department of Defense published its updated Section 1260H list of "Chinese military companies," and WuXi AppTec was added to it — a designation that compounds its BIOSECURE exposure and sent a chill through every Western client relying on Chinese CDMOs.25

Here is where Asymchem's position becomes genuinely interesting, and where the analysis must be precise rather than alarmist. Asymchem is not named on the BIOSECURE list of concern, and it is not on the 1260H list. That distinction is, at this moment, a real competitive asset. As Western clients scramble to de-risk away from the explicitly blacklisted WuXi, some of that displaced work flows to Chinese CDMOs that retain the cost and capability advantages but carry no formal designation. Asymchem sits, for now, in a "China-plus-one" sweet spot — Chinese execution economics without the named-entity stigma — and the Sandwich UK site gives it a tangible non-China option to wave at nervous procurement officers.

But the bear's rejoinder is devastating in its simplicity: for now. Asymchem remains a Chinese company, fully exposed to the same decoupling currents that just engulfed its larger rival. The 1260H list is reviewed and reissued annually, and the next major review is due by late 2026. There is no structural guarantee that Asymchem stays off it. The company is currently a beneficiary of geopolitical fragmentation; it could become a victim of it with a single bureaucratic stroke, and an investor has essentially no ability to handicap that political outcome. This is an unhedgeable, binary risk sitting underneath an otherwise fundamentally-driven story — and any honest assessment has to weight it heavily.

XI. Playbook: Business & Investing Lessons

Step back from the risk radar and ask what this whole arc teaches — about management, about incentives, and about how a durable business gets built. Start with incentives, because at Asymchem they are unusually well-aligned, and alignment is the first thing a long-term investor should check.

Consider the founder. 洪浩 Dr. Hao Hong is disclosed to hold a substantial total economic interest in the company he founded — on the order of 36–40%, combining a small direct stake of roughly 4% with a much larger indirect interest of around 32% held through the Delaware-incorporated Asymchem Laboratories, Inc., the vestige of those North Carolina origins.26 His reported annual compensation is modest by global-pharma-executive standards at around CN¥7.35 million. The structural point matters more than the precise figures: the overwhelming majority of Hong's wealth is tied to the share price, not to his salary. He does not get rich from a paycheck; he gets rich if the stock compounds. That is the kind of skin-in-the-game alignment investors should want from a founder-led company, and it is a meaningful contrast to professionally-managed firms where executives are insulated from the stock.

The second key figure is Ms. Rui Yang, the co-CEO, whose story is a quiet testament to the company's internal culture. She joined Asymchem in 1999 — when it was still a struggling minnow — and rose, over more than two decades, from office manager to co-chief executive. Her economic interest is structured through a management vehicle, AsymCore, and she is incentivized under a 2025 Restricted Share Incentive Scheme that ties equity vesting to aggressive growth targets specifically defined on the non-COVID base business.26 That last detail is a small but telling governance choice: by anchoring management's incentive compensation to base-business growth rather than headline revenue, the board structurally prevented executives from being rewarded for the Paxlovid windfall they did not really earn, and forced them to focus on the durable engine. It is the kind of incentive design that suggests the board is actually thinking about alignment rather than rubber-stamping a comp plan.

Now the credibility check, assessed through behavior over time rather than rhetoric. The evidence is, on balance, favorable. Management showed capital discipline by refusing to overpay for Snapdragon even with cash burning a hole in its pocket; it pivoted quickly and pragmatically when CFIUS blocked that path, rather than wasting years fighting an unwinnable battle; it then deployed capital into a cost-efficient European asset and into the GLP-1 capacity build — all of it funded from internal cash, debt-free. And it handled the post-pandemic revenue cliff with relative transparency, telling investors from the outset that the COVID orders were one-time and keeping the narrative focused on base-business growth. A management team that consistently does roughly what it said it would do, across a blocked deal, a revenue cliff, and a strategic pivot, has earned a degree of benefit of the doubt. The caveat, as always, is that the biggest test of capital discipline is still in progress: the peptide expansion is the largest bet the company has ever made with its own money, and the verdict on whether it was disciplined or reckless will not be in for years.

Two broader lessons fall out of the Asymchem story for founders and operators. The first is the power of non-consumable IP. Asymchem built its business around proprietary, hard-to-replicate process technology — flow chemistry and biocatalysis — rather than around trying to discover and own drugs itself. Drug discovery is a lottery; the picks-and-shovels business of manufacturing other people's molecules, when armed with genuine technical differentiation, is a steadier and more cash-generative model. The company sells a capability that gets more valuable with each drug it helps make, not a single product that can fail in a trial. The second lesson is the oldest one in business, freshly demonstrated: never waste a crisis. Asymchem took a once-in-a-generation pandemic windfall and, instead of dividending it all away or sitting on it, converted it into the funding for an entire next-generation growth platform — debt-free. Whether that platform succeeds is unresolved, but the discipline of recycling a windfall into the future is exactly what separates enduring companies from one-hit wonders.

For the investor trying to track this company going forward, the noise of headline revenue — still distorted by the COVID base effect — is the wrong thing to watch. Two or three things actually matter. The growth rate of the base small-molecule business, ex-COVID, is the truest read on the health of the core engine. The revenue ramp and utilization of the TIDES/peptide segment is the read on whether the big bet is paying off or producing stranded capacity. And, sitting above the fundamentals, the geopolitical designation status — whether Asymchem stays off the BIOSECURE and 1260H lists — is the binary that could override everything else. Track those, and you are tracking the real Asymchem.

XII. Epilogue & Outro

As of mid-2026, Asymchem stands at an inflection that its founder could scarcely have imagined in that North Carolina lab thirty-one years ago. The company has guided for a robust 19%–22% revenue growth trend for the full year 2026, a return to top-line expansion driven by the commercialization of new peptide projects and the integration of the Sandwich UK site — a trajectory that, notably, roughly matches the growth pace WuXi has guided for its own continuing operations, suggesting the broader Chinese CDMO sector has digested the COVID hangover and re-entered a growth phase.418 The headline numbers are finally clean of the pandemic distortion; from here, growth has to come from the base business and the new modalities, which is exactly as it should be.

There is a tidy symmetry to the whole arc. Asymchem began as a bet that the best place to do chemistry was wherever the best combination of trust, talent, and cost happened to be — Western customer relationships, Chinese execution. Three decades later, the company is making the same bet in reverse, planting a flag back in the West at a former Pfizer site in Kent, hedging the very geography that made it. The constant through it all has not been a country or a customer; it has been a conviction that superior process technology — making molecules cleaner, shorter, cheaper — is a durable source of advantage in an industry that runs on chemistry. The Paxlovid windfall was, in a sense, the universe handing Hong a billion-dollar receipt for a thesis he had been quietly building since 1995.

Whether that thesis carries the company through its next chapter is genuinely uncertain, and we have tried to be honest about why: the peptide bet could glut, the customer concentration could bite, and the geopolitical designation could flip from tailwind to existential threat with a single annual review. Those are real risks, not rhetorical ones. But the story of how a process chemist's insistence on doing the unglamorous work better turned a tiny export lab into the green-chemistry engine behind one of history's fastest drug launches is, regardless of where the stock goes from here, a genuine triumph of high-end chemical engineering — and a case study in being prepared when the world's structural winds happen to shift in your favor.

If you loved this episode, share it with a friend.

References

-

Development of a Scalable Flow Biocatalytic Process for the Synthesis of Ceralasertib — ACS Organic Process Research & Development, 2022-07-25 ↩↩

-

Asymchem Announces Shares Listing on the Hong Kong Exchange — PR Newswire, 2021-12-10 ↩

-

The 9.2 Billion New Crown Special Medicine Orders Stunned the CDMO Leader — ECHEMI, 2022 ↩

-

Asymchem Acquires Snapdragon Chemistry — PR Newswire, 2022-02 ↩

-

China CDMO Asymchem snaps up Snapdragon for $58M — Fierce Pharma, 2022-02 ↩

-

Snapdragon Chemistry and Asymchem Abandon Planned Acquisition — PR Newswire, 2022-09-09 ↩

-

Asymchem Laboratories – HK$7.15 Billion IPO — Cooley, 2021-12-15 ↩↩

-

Chinese Drugmaker Asymchem Slips in Hong Kong Trading Debut — Bloomberg, 2021-12-10 ↩

-

Asymchem terminates acquisition of US firm Snapdragon, citing CFIUS hurdle — Reuters, 2022-09-12 ↩

-

US Treasury Department derails Asymchem's acquisition of Snapdragon — C&EN, 2022-09 ↩

-

Snapdragon rebounds with a deal to be acquired by Cambrex — C&EN, 2022 ↩

-

Asymchem Expands Global Footprint with Acquisition of Former Pfizer Manufacturing Facility in Sandwich, UK — Business Wire, 2024-05-29 ↩

-

Asymchem Secures Former Pfizer Sandwich, UK, Development and API Pilot Plant Manufacturing Facilities — Business Wire, 2024-05-21 ↩

-

Axed Pfizer workers rehired as new Chinese firm moves in — Kent Online, 2024 ↩

-

Asymchem's Sandwich, UK Facility Initiates Pilot Operations — Business Wire, 2024-06-12 ↩

-

Asymchem Inaugurates Its First European Small Molecule Development and API Pilot Plant Site at Discovery Park — Business Wire, 2024-08-02 ↩

-

WuXi AppTec Beat Full-Year Guidance and Achieved Record Performance in 2025 — PR Newswire, 2026-03-23 ↩↩↩↩

-

Pharmaron Lifts Revenue and Cash Flow in 2025 Despite Profit Dip — TipRanks, 2026 ↩

-

Porton Corporation (300363) 2025 Annual Report Commentary — Futubull, 2026 ↩

-

Asymchem Unveils Its Fully Integrated TIDES Commercial Supply Matrix — PR Newswire, 2026 ↩

-

Asymchem (002821): Rapid Growth in Emerging Businesses with Orders and Capacity — Futubull, 2025 ↩

-

Biosecure Act Signed into Law — Latham & Watkins, 2025-12-19 ↩

-

WuXi AppTec Added to DoD's 1260H List: The BIOSECURE Act Clock Is Running — Holland & Knight, 2026-06 ↩

-

Asymchem Laboratories (Tianjin) Co., Ltd. (6821.HK) Stock Analysis & Ownership — Simply Wall St ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube