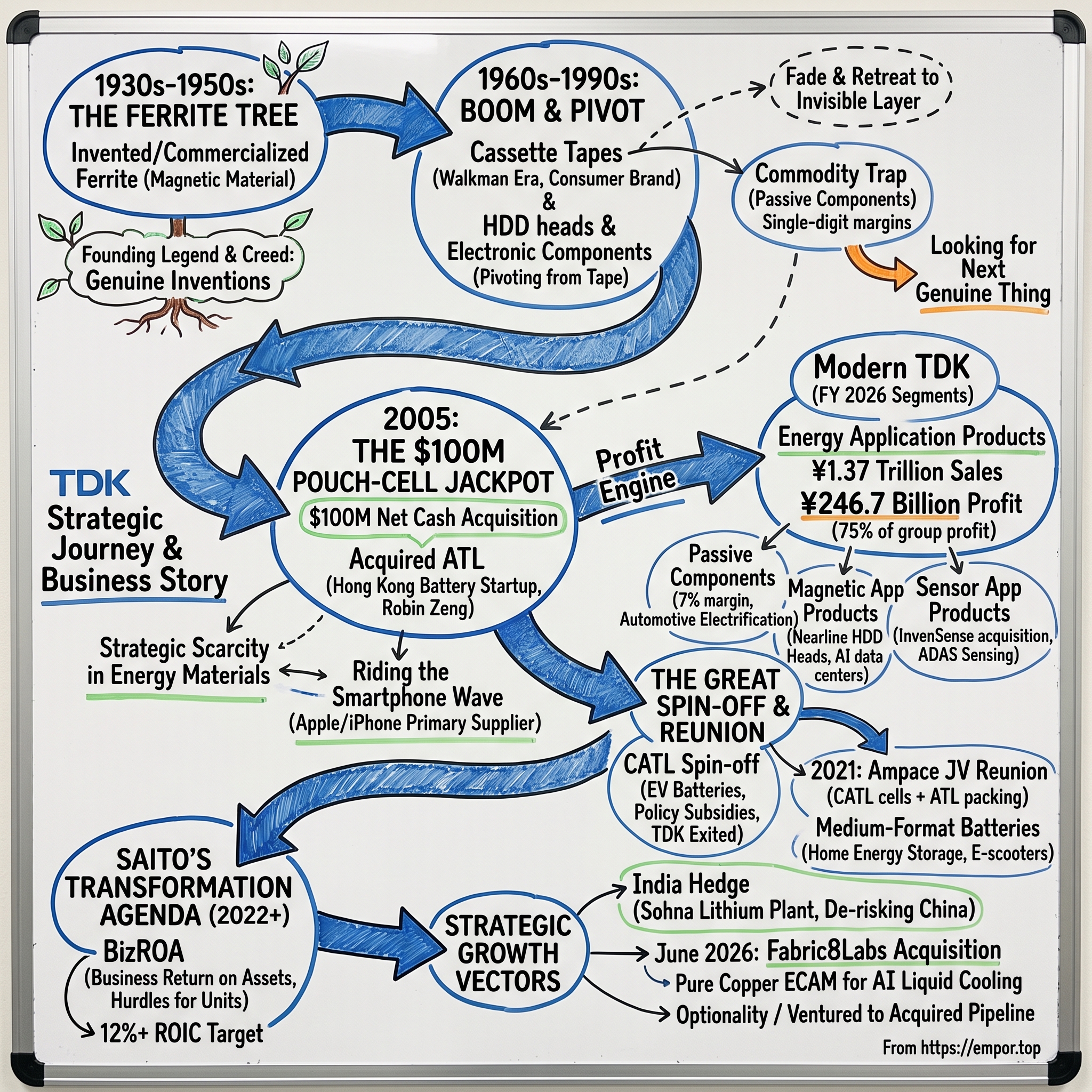

TDK Corporation: The Ferrite Tree, the $100M Pouch-Cell Jackpot, and the AI Thermal Pivot

I. Introduction & Episode Roadmap

Picture the boardroom math on a single acquisition. In 2005, a ninety-year-old Japanese components maker wrote a check for roughly $100 million to buy a little-known Hong Kong battery startup with a plant in Dongguan and about three thousand employees.4 Two decades later, that business — Amperex Technology Limited, or ATL — sat inside a segment generating more than ¥1.37 trillion of annual sales and nearly a quarter-trillion yen of operating profit, powering the batteries inside a huge share of the world's premium smartphones and spinning off, along the way, a company you have almost certainly heard of even if you've never heard of TDK: 宁德时代 CATL, the largest EV battery maker on Earth.96

That is the hook. How did 加藤与五郎 Yogoro Kato's magnetic-materials dream — a company literally founded to commercialize a laboratory curiosity called ferrite — become the quiet electrochemical backbone of the smartphone age? And how did the same firm that made the cassette tapes in your childhood shoebox end up, in June 2026, buying a San Diego startup that 3D-prints pure copper to cool AI data centers?10

The temptation is to file TDK株式会社 TDK Corporation under "legacy Japanese component supplier" — a maker of humble passive parts, the capacitors and inductors and filters that disappear inside every gadget. That framing is wrong, and the misunderstanding is the whole point of this story. Modern TDK is really two companies wearing one logo. One is a materials-science house descended directly from the ferrite discovery: multilayer ceramic capacitors (MLCCs), inductors, magnets, HDD heads, sensors. The other is an electrochemistry titan — the ATL small-battery franchise — that today throws off the lion's share of the group's profit. The interesting investment question is what happens when a cyclical, commoditizing materials business is fused to a spectacularly profitable but customer-concentrated battery business, and whether management can use the cash from the second to reinvent the first.

There is a deeper reason the "boring component maker" label sticks, and it is worth naming up front because it colors how the market prices the stock. TDK's products are, almost by design, invisible. Nobody buys a phone because of the battery brand inside it; nobody specifies the MLCC in their laptop's power circuit. The company lives one or two layers below the surface of every device you own, which means its fortunes are bound to other companies' product cycles and its brand equity — once genuinely famous, in the cassette era — has largely evaporated into anonymity. Anonymity is comfortable when business is good and merciless when a single customer decides to renegotiate. A large part of what follows is the story of how a company got extraordinarily rich by being invisible, and why that same invisibility is the source of its most serious risks.

We should also set the stakes plainly. This is a company whose consolidated sales cleared ¥2.5 trillion in the fiscal year just ended, whose profit is concentrated in one segment to a degree that would make most conglomerates blush, and whose future depends on bets that range from a battery factory in Haryana to a solid-state chemistry still in the laboratory to a copper-printing startup in California.9 The neutral analyst's job is neither to celebrate the ATL jackpot as proof of genius nor to dismiss the transformation as slideware, but to separate what TDK has actually proven from what it is merely promising — and to be honest about which is which.

Before the roadmap, a word on the central myth this piece will test. The consensus story — the one TDK's own investor materials gently encourage — is that the company is a diversified electronics powerhouse riding the great secular waves of electrification, AI, and sensing, with batteries as merely the largest of several growth engines. The reality is starker and, for an investor, more clarifying: TDK is a battery company with a materials-science hobby, and the health of the whole enterprise rests disproportionately on one segment, one dominant customer, and one country. That is not a criticism; single great businesses have made plenty of shareholders rich. But it means the diversification narrative should be treated as an aspiration management is spending money to make true, not as a description of what TDK already is.

Here is the roadmap. We start with the "ferrite tree" and the founding legend that still shapes TDK's self-image. We trace the twentieth-century arc through cassettes and disk-drive heads into the commodity trap that made batteries so appealing. We dwell — because it deserves it — on the ATL jackpot and its complicated, multi-trillion-dollar offspring. We contrast two very different M&A outcomes, the Qualcomm RF360 exit versus the InvenSense purchase. We open the books on the fiscal-year-March-2026 segments. We examine 齋藤昇 Noboru Saito's transformation agenda and his BizROA capital discipline. We look at the India hedge and the Fabric8Labs thermal bet. And we war-game the bull and bear cases with the frameworks sophisticated investors actually use. Let's begin where TDK began — with a magnet nobody knew what to do with.

II. The "Ferrite Tree" and the Founding Legend (1930s–1950s)

In 1930, in a laboratory at the Tokyo Institute of Technology, two researchers — 加藤与五郎 Yogoro Kato and 武井武 Takeshi Takei — synthesized a new class of magnetic material: ferrite, a ceramic oxide of iron that could carry magnetic flux with far lower energy loss than the metal cores then used in transformers and coils.1 It was a genuinely Japanese invention, born of domestic research rather than licensed from the West, and that provenance mattered enormously to what came next. The problem was mundane and familiar to anyone who has watched a university discovery languish: nobody knew how to turn it into a business. It was a powder in search of a factory.

Enter 齋藤憲三 Kenzo Saito, an entrepreneur searching for an industry he could plant in his agricultural hometown to give it something beyond farming. When Saito and Kato met, the chemistry — social as much as chemical — was immediate, and Kato granted Saito the right to commercialize the ferrite technology.1 On December 7, 1935, Saito founded 東京電気化学工業 Tokyo Denki Kagaku Kogyo, the company that would later rename itself with the initials of its founding trade: TDK.2 It is worth pausing on what a wild gamble this was. Saito was not building a better version of something customers already bought. He was betting an entire company on a material that had no established market, no proven demand, and no competitors precisely because no one else believed in it.

It helps to understand what ferrite actually does, because the physics explains the fortune. An ordinary transformer or coil needs a magnetic core to concentrate and guide magnetic flux. Metal cores do this well at low frequencies but bleed energy as heat — "eddy-current losses" — when the current alternates quickly, which is exactly what radio and later electronics require. Ferrite is a ceramic: it conducts magnetism beautifully but electricity poorly, so those wasteful internal currents largely can't form. The practical upshot is a core that stays efficient at high frequencies, which is the enabling ingredient for radios, televisions, and eventually the switching power supplies inside nearly every electronic device. Kato and Takei had, in effect, invented a better building block for the electronic century — and handed a commercialization monopoly to a first-time entrepreneur.

That gamble hardened into a philosophy. Kato's challenge to Saito — the idea that the Japanese should build genuine industries from their own genuine inventions rather than importing and imitating — became TDK's founding creed, later crystallized as the metaphor of the "ferrite tree": a single seed of invention from which an ever-branching family of products would grow.3 It is easy to dismiss corporate origin myths as marketing. But this one has real explanatory power for the company's behavior nine decades later. TDK's repeated pattern — acquire or discover a core material or cell technology, then grow an expanding canopy of applications from it — is the ferrite-tree instinct operationalized. ATL's pouch cell became a "tree." So, management hopes, will its solid-state chemistry.

The post-war decades turned that instinct into an industrial engine. As Japan rebuilt and then boomed, TDK rode the country's ascent from war-ravaged economy to electronics superpower, selling ferrite cores and magnets into the transistor radios, televisions, and telephones that were remaking daily life. The company's culture in this period fused two things that don't always coexist: a genuine reverence for materials research — the belief that owning the fundamental science is the only durable advantage — and an entrepreneurial, almost restless appetite for finding the next application. That combination is what corporate Japan often lacked, and it is why TDK avoided the fate of firms that owned a great invention and then guarded it into irrelevance.

The first branch grew fast. By 1937, joint work between the institute and TDK yielded a manufacturable ferrite core, which was put to use in Japanese wireless communication gear and radios ahead of the rest of the world.1 Wartime demand from the Japanese military for wireless transmitters gave the young company its first high-margin monopoly — a material nobody else could make, sold into an application that could not do without it. That combination, a proprietary material feeding an indispensable use case, is the economic template TDK has chased ever since.

The lesson for a modern investor is not nostalgia. It is that TDK's most durable competitive advantages have always been rooted in materials science that is hard to replicate, and its most painful stretches have come whenever its products drifted toward commodities anyone could make. Hold that tension in mind, because the next fifty years are the story of TDK riding — and eventually being betrayed by — exactly that dynamic. From a wartime coil, the tree grew into the most recognizable consumer brand Japan's electronics industry ever produced.

III. Cassettes, Magnetic Heads, and the 20th Century Boom (1960s–1990s)

For a certain generation, TDK is not a component maker at all. It is a cassette tape. If you owned a Walkman, mixed a tape for someone you liked, or taped songs off the radio, the odds are good you handled a TDK cassette — the D, AD, SA, and MA series that lined record-shop shelves worldwide. TDK popularized the compact audio cassette after 1966, and the same magnetic-coating expertise that came out of the ferrite tree — how to lay a precise film of magnetic particles onto a substrate — carried it into VHS videotape as home video exploded.1 For a components company, this was an extraordinary and slightly accidental gift: a consumer brand with genuine shelf presence, the rare B2B firm whose logo a teenager could recognize.

The cassette business was more than a revenue line; it was a masterclass in consumer marketing that a components firm had no business being good at. TDK segmented its tapes by use case — the everyday D series, the higher-fidelity AD and SA, the premium metal-particle MA for audiophiles — and advertised them like a consumer-goods company, complete with the kind of brand loyalty usually reserved for sneakers or soft drinks. For a brief historical window, a business-to-business materials company had a business-to-consumer brand with real emotional resonance. It is worth remembering that peak, because it is the last time TDK's name meant anything to ordinary buyers. Everything since has been a retreat back into the invisible layer.

But brands built on physical media carry an expiration date written in the technology itself, and TDK's engineers could read it. Magnetic tape was a storage medium; storage was going digital and getting denser. The same skill set that coated tape — the physics of writing and reading magnetic domains — pointed toward a more valuable frontier: the read-write heads inside hard disk drives. Through the 1980s and 1990s, TDK pivoted hard into HDD magnetic heads and into electronic components, above all the multilayer ceramic capacitor, capturing enormous global share in the tiny recording heads that let disk drives keep cramming more data onto spinning platters. A modern HDD head is a marvel — it flies nanometers above a platter spinning thousands of times a minute, reading and writing magnetic bits at a density that would have seemed like science fiction to the cassette engineers. This was the ferrite tree doing what it did best: taking a materials competence and re-rooting it in the next application before the old one withered.

The pivot worked, but it dropped TDK into a harsher neighborhood. Passive components and disk-drive heads are brutally competitive, capital-hungry, and cyclical. Here TDK ran headlong into two formidable domestic rivals that had made the ceramic-and-magnetics business their life's work: 京セラ株式会社 Kyocera and 株式会社村田製作所 Murata. It is worth understanding what an MLCC actually is, because its economics are the whole point. A multilayer ceramic capacitor is a tiny stack of alternating ceramic and metal layers that stores and releases small amounts of electrical charge — the humblest of components, and one that a modern smartphone contains by the hundreds and an electric car by the thousands. They are sold by the billions for fractions of a cent each, which means the game is won on scale, yield, and materials quality, not on any single design. Murata in particular built a fearsome position in MLCCs, out-investing and out-yielding rivals to become the reference producer, and the three-way Japanese scrum — plus waves of lower-cost competition — meant that even a market leader could watch margins evaporate whenever the electronics cycle turned. TDK's passive-components earnings became a sawtooth: feast in the boom, famine in the bust, with heavy factory investment locked in regardless.

That competitive war is still being fought, and it frames how to read TDK's 7% passive-components margin today against Murata's structurally higher one: TDK is a strong number-two-or-three in a business where the leader earns a premium for scale and mix. The company's escape route in passives is not to beat Murata head-on in commodity MLCCs but to specialize where reliability commands a price — the automotive and industrial-grade parts that must survive heat, vibration, and a decade of duty without failing. That is a defensible niche, and the segment's faster-than-sales profit growth this year suggests the mix shift is working, but it is a niche within a business TDK does not lead, which is a very different proposition from the near-monopoly it enjoys in premium pouch cells.

This is the "commodity trap," and it is the single most important thing to understand about why TDK became the company it is today. A commodity trap is what happens when your product is essential but undifferentiated: customers must buy it, but they can buy it from three other people, so all the value leaks to the buyer. TDK had escaped it once, with ferrite, by owning a material no one else could make. By the late 1990s it was stuck in it again — technically excellent, globally scaled, and yet unable to convert that excellence into the fat, stable margins that make investors happy. The magnetic-tape brand was fading, HDD heads faced their own volume peaks, and passive components ground along at single-digit returns.

It is worth dwelling on why the commodity trap is so insidious, because it is the analytical key to TDK's entire modern strategy. A firm in the trap is not failing — it is often the technological leader. It simply cannot capture the value it creates, because the buyer can credibly threaten to walk to a rival, and that threat alone transfers the surplus. The classic escape routes are three: build a genuine technology monopoly (as ferrite once was), achieve a cost position no one can touch (scale economics), or exit the commoditizing product for an adjacent one where differentiation still holds. TDK would eventually try all three. But in the late 1990s the passive-components business offered none of them in abundance, and the disk-drive-head business faced its own eventual volume ceiling as flash memory loomed.

So TDK went looking, as it had in the 1930s, for the next genuine thing — a material and an application defensible enough to break the trap. Management wanted a business with structural scarcity, ideally one tied to a device category about to explode. What they found was not a magnet or a ceramic at all. It was a battery, in Hong Kong, run by a chemist who would go on to build the largest battery company in the world.

IV. The Fateful $100M Jackpot: The ATL Acquisition (2005)

Amperex Technology Limited was founded in Hong Kong in 1999 by a team led by 曾毓群 Robin Zeng (Zeng Yuqun), a chemist with a conviction about a specific, unglamorous technical problem: how to make lithium-polymer pouch cells that were thin, could be shaped to fit a product rather than forcing the product to fit them, and — critically — would not swell, leak, or catch fire.6 The insight was that the winning battery for portable electronics would not be a rigid cylinder like the cells in a flashlight, but a flexible flat pouch that a product designer could slot into any cavity. Getting there safely was hard chemistry, and ATL's early years were a scramble to license and then out-engineer the electrolyte formulations that kept pouch cells stable.

Robin Zeng is worth introducing properly, because he is the human hinge of this entire story and because his ambition explains both the jackpot and its limits. Born in 1968 in rural Ningde, in Fujian province, Zeng trained as an engineer and cut his teeth at a foreign-invested electronics firm before co-founding ATL in 1999 with a conviction that the future of portable power belonged to whoever could tame the polymer lithium cell.6 He was, by every account, relentless, technically fluent, and unwilling to be anyone's junior partner for long — a founder in the fullest sense. TDK bought his company but could not buy his ceiling, and within six years he had engineered his way into building something far larger than the parent that owned him. When you assess TDK's dealmaking, remember that its greatest acquisition came attached to a man who was always going to outgrow the arrangement. That is not a criticism of TDK; it is the nature of buying genius.

By the mid-2000s ATL had a real manufacturing base in Dongguan and roughly three thousand employees, but it was sub-scale and undercapitalized for the tidal wave of demand it sensed was coming.4 TDK, hunting for an escape from the commodity trap and eager to plant a flag in energy materials, saw a fit. Under then-chairman and CEO 澤部肇 Hajime Sawabe, TDK acquired 100% of ATL in 2005 for approximately $100 million, net of cash — a modest sum even then, roughly the price of a mid-sized office building, for a business it framed as an operating base to grow its materials expertise into energy.45 There was no way, in 2005, to model what this would become. The iPhone did not exist. The purchase looked like a sensible, unremarkable bolt-on.

To understand why the pouch cell mattered, picture the two ways to package a lithium battery. The old way is a rigid metal can — a cylinder or a hard prismatic box — strong and safe but geometrically stubborn: the product must be designed around the battery. The pouch cell flips that relationship. It wraps the electrode stack in a flexible laminated foil, so it can be made thin, flat, and shaped to fill whatever awkward cavity a designer leaves for it. The catch is safety: without a rigid can to contain them, pouch cells are less forgiving of the swelling and thermal runaway that lithium chemistry can produce, which is precisely why the electrolyte formulation and quality control that ATL obsessed over were the whole ballgame. Getting a pouch cell to be simultaneously thin, energy-dense, and safe against a customer that would ship hundreds of millions of units was a genuinely hard problem, and solving it repeatedly is the cornered resource TDK actually bought.

Then the smartphone happened. Apple's hardware designers, obsessed with shaving every millimeter and curve, needed batteries that could be molded to the interior geometry of an impossibly thin device — exactly ATL's pouch-cell specialty. ATL's cells went into iPods and then into the original iPhone, and as the smartphone became the defining product of the century, ATL rode shotgun as a primary battery supplier to the most demanding customer in consumer electronics. A $100 million acquisition had, almost by accident of timing, bought TDK a front-row seat to the largest hardware ramp in history. The timing genuinely was luck — TDK did not foresee the iPhone in 2005 — but the positioning was not: management had correctly identified that portable-device energy was a structurally scarce, high-value problem, and had bought the best team in the world at solving it. Luck favored a company that had put itself in luck's way.

Let's be precise about what makes this the "most asymmetric venture jackpot" the outline claims — and where that framing needs a skeptic's asterisk. On the return side, the arithmetic is genuinely staggering: a nine-figure purchase seeded a franchise that, two decades on, anchored a segment doing well over a trillion yen in annual sales.9 Very few corporate acquisitions in any industry have compounded like that. The asterisk is that TDK did not simply buy a finished machine and collect rent. It funded years of capacity expansion, absorbed the capital intensity of battery manufacturing, and — as we'll see — watched the single most valuable part of ATL's future, the EV battery business, walk out the door. The jackpot was real. It was also, in a way TDK could not fully control, shared.

There is also a governance lesson worth extracting for anyone assessing TDK's later deals. The ATL acquisition worked not because TDK micromanaged it into success but because it did the opposite — it provided capital and a stable corporate home while leaving the operating team and its founder largely intact to run the business their way. Japanese acquirers of foreign companies have a mixed-to-poor record precisely because they often smother what they buy. TDK's relative restraint with ATL is a genuine institutional strength, and it is the implicit playbook behind TDK Ventures and the Fabric8Labs deal decades later: find the team, fund the team, don't strangle the team. Whether that light touch survives as the company grows more process-driven under a transformation program is a fair question to hold.

What the ATL deal proves about TDK's strategy is subtle but important: the company's best value creation came not from its own R&D but from its willingness to buy a foreign entrepreneurial team and let it run. That is a very un-Japanese-conglomerate instinct, and it recurs. But buying a founder as brilliant and ambitious as Robin Zeng carries a corollary risk — founders like that rarely stay in someone else's box. Which brings us to the subsidy wall, and the most consequential spin-off in the history of the battery industry.

V. The Great Spin-Off & Reunion: CATL, Ampace, and the Battery Dual-Engine (2011–2021)

By 2011, Robin Zeng was staring at a policy map that made his ownership structure a liability. Beijing was preparing to pour subsidies into electric-vehicle batteries — the single largest industrial-policy bet of the coming decade — but the support was reserved, in practice, for domestically owned Chinese companies. ATL, wholly owned by a Japanese parent, was on the wrong side of that line. The most valuable market on Earth for large-format batteries was about to open, and the Japanese flag on ATL's cap table threatened to lock it out.6

The resolution was elegant and, in hindsight, era-defining. Zeng and a consortium of Chinese investors carved ATL's EV battery ambitions out into a new, Chinese-owned company: Contemporary Amperex Technology Co., Limited — 宁德时代 CATL, named for Zeng's hometown of Ningde in Fujian province.6 TDK retained the small-battery business (phones, tablets, laptops, wearables) inside ATL, took a stake in the new entity, and the two companies established a patent cross-licensing framework so the split did not devolve into litigation.6 CATL then did something few outside China anticipated: it did not merely qualify for subsidies, it used them as a launchpad to become the largest EV battery maker on Earth, supplying automakers worldwide and turning Robin Zeng into one of Asia's wealthiest people.6

TDK later exited its CATL position — a decision that returned cash but, with the benefit of hindsight, meant handing away a claim on what became one of the most valuable industrial companies in the world. This is the part of the jackpot story that a bull glosses over and a bear underlines: TDK owned the seed of the world's dominant EV-battery maker and chose to sell it. The prudent, cash-in-hand logic of that exit is defensible — the political reality was that a Japanese-owned stake could never fully participate in China's EV champion, and monetizing it early de-risked the balance sheet. But the opportunity cost was colossal, and it is the single best illustration of a recurring TDK trait: the company is superb at originating options and only average at holding the biggest ones to their full value. That pattern should temper any assumption that TDK will automatically extract maximum value from its next great find.

For roughly a decade after the split, a clean division of the world held: ATL owned small batteries, CATL owned large EV batteries, and a demilitarized zone sat between them. But markets abhor a clean line. A fat, fast-growing middle emerged — batteries too big for a phone and too small for a car: residential energy-storage systems, e-scooters and e-bikes, power tools, drones, portable power stations. This medium segment had attractive margins and none of the incumbent's home-turf advantages, because neither ATL nor CATL was built precisely for it.

So in 2021, the parent and its famous child reunited to attack the middle together. ATL and CATL announced a business alliance to establish joint ventures under the Ampace banner — 厦门新能安科技 Xiamen Ampace Technology — headquartered in Xiamen and aimed squarely at medium-sized cells and packs.7 The structure is a neat piece of strategic engineering: the venture split into a cell-focused entity, majority-controlled by CATL (roughly 70% CATL / 30% ATL), and a pack-focused entity, majority-controlled by ATL (roughly 70% ATL / 30% CATL).7 Read the ownership split and you can see each parent playing to its strength — CATL's cell chemistry and scale, ATL's packaging and consumer-grade quality control — while sharing the upside of a market neither could optimally serve alone. Ampace went on to become a serious force in global home energy storage, a category that barely existed when ATL and CATL first parted ways.

The medium-battery market Ampace targets deserves a moment, because it is where a lot of the near-term energy growth actually lives. Residential energy storage — the wall-mounted battery that pairs with rooftop solar to bank cheap daytime power for the evening peak — has gone from niche to mainstream across Europe, Australia, and increasingly the United States, and Ampace became a serious global supplier into it. Add e-bikes and e-scooters, cordless power tools, drones, and portable "power station" units, and you have a category with EV-like volume growth but consumer-electronics-like margins, sitting in the exact gap between ATL's phones and CATL's cars. For TDK, this is arguably the most attractive organic growth vector it has, precisely because it leverages both parents' strengths without requiring TDK to win a head-to-head battle against CATL in automotive.

For TDK, this reunion matters because it converts the ATL franchise from a smartphone-dependent story into a broader energy-storage one. The "dual engine" is really becoming a triple: small cells for ICT devices, the medium-battery growth vector through Ampace, and the materials businesses. But it also deepens TDK's entanglement with China — its crown-jewel profit engine is a Chinese-run, Chinese-manufactured operation, joint-ventured with a Chinese national champion. There is a governance subtlety here that an activist would flag: a substantial share of the group's economics runs through joint ventures TDK does not fully control and whose consolidated disclosure is necessarily less granular than a wholly-owned segment's. That is a source of enormous strength and, as we'll see in the bear case, a concentrated geopolitical exposure that no amount of Japanese ownership fully neutralizes. Before we get there, though, TDK made two other big bets in the late 2010s that reveal a great deal about how disciplined — or not — its dealmaking really is.

VI. M&A Strategy: The Qualcomm RF360 Masterstroke vs. InvenSense (2017–2019)

Not every business is worth keeping, and TDK's cleanest strategic win of the decade was a business it decided to walk away from. Radio-frequency filters — the tiny components that let a phone separate the dozens of wireless bands crammed into modern spectrum — are technically demanding but ferociously capital-intensive, and the arms race to keep up with each new cellular standard is a treadmill that never stops. TDK had real RF filter technology; what it lacked was the appetite to fund the treadmill forever.

The answer was a joint venture. In early 2017 TDK folded its RF filter business into RF360 Holdings, a venture with Qualcomm, with an option structure that let Qualcomm buy out the rest. In September 2019, Qualcomm exercised it, acquiring the remaining interest for a total transaction value of approximately $3.1 billion — a figure that included Qualcomm's initial investment, sales-based payments to TDK, and development obligations.[^9] Read through the deal mechanics and the strategy is beautiful in its clarity: TDK extracted billions in cash from a commodity-trending, capital-hungry business, handed the treadmill to a partner better positioned to run it (Qualcomm needed complete RF front-end solutions for its modem franchise), and redeployed the proceeds. This is exactly the kind of unsentimental portfolio pruning that TDK's history of clinging to fading businesses had too often lacked. It is the RF360 exit, more than any acquisition, that shows TDK learning to sell.

The subtlety that makes RF360 genuinely smart, rather than merely lucky, is the recognition of fit — the same asset was worth far more to Qualcomm than to TDK. RF filters are a supporting component; for TDK they were a standalone business that had to earn its own capital, but for Qualcomm they completed an end-to-end radio-frequency front-end that made its modem chips more valuable. When an asset is worth more inside someone else's system than inside yours, selling it to them is not a retreat but an arbitrage. TDK captured that difference in cash. The pattern to internalize is that TDK's cleanest wins come when it correctly identifies that a business it built has become someone else's strategic necessity — and acts on it before the value fades.

The same years produced the counter-example. In May 2017, TDK completed the all-cash acquisition of InvenSense, a US-listed pioneer of MEMS (micro-electro-mechanical systems) sensors — the tiny gyroscopes and accelerometers that tell your phone which way is up — for approximately $1.3 billion, or $13.00 per share.8 The strategic logic was sound: sensors were a natural adjacency, TDK wanted an anchor for a Sensor Application Products segment, and MEMS was a growth category tied to smartphones, automotive, and the coming wave of "sensor fusion" in everything.

But price is what you pay, and TDK paid a premium at the top of the cycle. InvenSense carried the classic vulnerabilities of a merchant MEMS supplier: heavy customer concentration among a handful of giants like Apple and Samsung, and relentless margin compression as sensors commoditized. The uncomfortable comparison writes itself. Where ATL was instant, world-changing accretion for $100 million, InvenSense anchored a segment that, as we'll see, still grinds at single-digit-to-low-double-digit margins nearly a decade later — a payback period measured not in quarters but in a decade-plus of patient integration into higher-value automotive and ADAS sensing. Neither deal was a disaster; the point is the contrast in quality. One acquisition was a lottery ticket that hit; the other was a full-price purchase of a business with a structural buyer-power problem, justified by a strategic-adjacency argument that is still being proven.

It is worth being fair to the InvenSense thesis, because the strategic reasoning was not foolish even if the price was steep. TDK's bet was on "sensor fusion" — the idea that as cars, phones, drones, and industrial equipment sprouted more sensors, the value would migrate from the individual sensor to the integrated package of sensors plus the software that combines their readings into a coherent picture of motion, orientation, and environment. A gyroscope alone is a commodity; a calibrated, software-fused inertial measurement unit designed into a driver-assistance system is not. If that migration plays out, InvenSense's MEMS know-how becomes the anchor of a differentiated automotive-sensing franchise rather than a merchant chip supplier at Apple's mercy. The problem is timing and proof: nine years on, the segment is profitable but still sub-group-margin, which means the thesis is being validated slowly, at best. An acquisition justified by a future that keeps not-quite-arriving is the definition of a long payback, and long paybacks are where invested capital quietly underperforms.

Taken together, RF360 and InvenSense are a Rorschach test for how you read TDK management. The optimist sees a company that has finally learned to buy growth and sell cyclicality. The skeptic notes that the RF360 win was partly luck of having a motivated buyer, and that TDK's willingness to pay a rich multiple for InvenSense at a cycle peak is exactly the behavior an activist would flag. The most useful synthesis is that TDK is a disciplined seller and a sometimes-overpaying buyer — a pattern that argues for watching its acquisition prices closely and giving more weight to its divestitures as evidence of judgment. Which reading is right depends on the numbers underneath the segments — so let's open them.

VII. Modern TDK & Segment Deep Dive (FY March 2026 Data)

On April 28, 2026, TDK closed the books on a record year and, on the earnings call, management walked analysts through a set of numbers that told a single, slightly awkward truth in four parts.9 Strip away nine decades of narrative and here is the hard truth about TDK in fiscal 2026: it is an extraordinarily profitable battery business carrying a collection of good-not-great materials businesses on its back. For the year ended March 31, 2026, TDK reported record consolidated net sales of ¥2,504.8 billion, up 13.6%, and operating profit of ¥272.4 billion, up 21.5%.9 Those are strong numbers. But the distribution of profit inside them is the whole story, and it is lopsided in a way every TDK investor must internalize.

Start with the engine. Energy Application Products — the ATL small-battery franchise plus power supplies and the Ampace-linked energy-storage business — posted net sales of ¥1,370.3 billion, roughly 55% of the group, and operating profit of ¥246.7 billion at an operating margin near 18%.9 Do that arithmetic against the group total and the conclusion is stark: this single segment produced roughly three-quarters of all segment operating profit. TDK's consolidated earnings are, to a first approximation, ATL's earnings with some other stuff attached. When management talks about "record profit," they are overwhelmingly talking about the profitability of shipping billions of small cells into the world's phones, tablets, laptops, and increasingly home batteries. That 18% margin, sustained in a category as competitive as batteries, is the single most important piece of evidence that ATL's pouch-cell franchise still enjoys real pricing power and cost advantage — not commodity economics.

Now the historical core. Passive Components — MLCCs, inductors, and the ceramic parts descended straight from the ferrite tree — generated net sales of ¥593.2 billion but operating profit of only ¥41.8 billion, an operating margin around 7%.9 This is the commodity trap, quantified: a large, technically excellent, globally significant business that converts each yen of sales into a fraction of the profit that batteries do. The bright spot, and the reason this segment is not merely a legacy drag, is automotive electrification. High-reliability ceramic capacitors that survive the heat and vibration of an electric powertrain are a genuinely differentiated, design-in product, and the content of passives per vehicle rises sharply with xEV adoption. Encouragingly, the segment's operating profit grew far faster than its sales this year, a sign that mix and pricing — not just volume — are working in its favor.

The two smaller segments round out the picture. Sensor Application Products — the InvenSense MEMS franchise plus temperature and pressure sensors — did net sales of ¥224.6 billion and operating profit of ¥20.7 billion, a margin near 9%, with profit growing sharply off a low base.9 Nearly a decade after the $1.3 billion purchase, this is finally a real, profitable segment rather than an integration project, though its margins still lag the group and the automotive/ADAS thesis remains a work in progress. And Magnetic Application Products — HDD heads and magnets, the most obviously "legacy" business — surprised to the upside with net sales of ¥262.9 billion and operating profit of ¥27 billion at a margin above 10%, up sharply as demand for high-capacity nearline drives in AI-era data centers breathed new life into a business everyone had written off.9

The magnetics turnaround deserves its own footnote in the investor's mind, because it is a small but real illustration of the ferrite tree's resilience. For fifteen years, HDD heads were the textbook dying business — displaced in laptops and phones by flash memory, a segment you owned only to harvest and shrink. Then the AI buildout created insatiable demand for cheap, high-capacity "nearline" storage in data centers, the tier where hyperscalers park the enormous volumes of data that feed AI training and inference. Spinning disks are still by far the cheapest way to store petabytes, and each new generation of high-capacity drive needs more sophisticated heads. A business everyone had discounted to zero suddenly re-rated on a tailwind nobody was modeling five years ago. The lesson is not that HDD heads are a growth story — they aren't, structurally — but that TDK's habit of keeping a technological foothold in "dying" materials businesses occasionally pays off when the world turns. It also, less charitably, is exactly the kind of business a BizROA framework has to keep honest, lest it become a sentimental holdout.

What does the segment map mean for an investor? Two things. First, the quality of TDK's earnings is concentrated in one place, and any thesis on the stock is really a thesis on ATL's ability to defend its margins. Second, the "boring" materials segments are quietly re-leveraging to two secular tailwinds — vehicle electrification (passives, magnets) and the AI data-center buildout (nearline HDD heads, and soon thermal components) — which is precisely the diversification the battery-heavy profit mix needs. Whether management can accelerate that rebalancing depends on the person now setting capital-allocation policy.

VIII. Saito's Leadership, Incentives, & BizROA

Every CEO inherits a defining problem, and Noboru Saito's arrived gift-wrapped as a triumph. When 齋藤昇 Noboru Saito took over as president and CEO in 2022, he inherited a company with a champagne problem: one business so profitable it obscured the mediocrity of the others. Sharing a surname with founder 齋藤憲三 Kenzo Saito is coincidental, but the symbolic weight of a "Saito" being asked to re-pot the ferrite tree for the AI age is hard to miss. His answer was a program branded the "TDK Transformation," organized around two acronyms that show up in every investor deck: DX (digital transformation of TDK's own operations) and GX (green transformation — riding electrification and energy storage). The branding is standard corporate-Japan fare; what matters is whether the capital discipline underneath it is real.

The most concrete evidence that it might be is BizROA — TDK's internal framework of Business Return on Assets. The idea is to slice the company into cash-flow business units and hold each to a return-on-capital standard rather than letting a strong segment cross-subsidize weak ones forever. Management has described a discipline in which units failing to clear an internal hurdle (in the neighborhood of a 10% return) are placed on an explicit watch for restructuring or exit. This is exactly the mechanism a company with a commodity-trap history needs, because the failure mode of a firm like TDK is not blowing up — it is quietly funding sub-scale, sub-return businesses for a decade because "we've always made them." At the group level, management set a target return on invested capital of 12% or higher, framing roughly ¥130 billion as flexible firepower for strategic investment.9 The RF360 exit and the InvenSense integration are both, in a sense, BizROA verdicts rendered in advance of the framework's formal branding.

On alignment, the structure reads reasonably well on paper: executive pay blends a fixed base with short-term performance-linked bonuses and long-term stock-linked compensation via restricted and performance share units, which at least ties senior management's wealth to the share price and to hitting multi-year targets. Under Saito, TDK also lifted its dividend policy, targeting a payout ratio around 35% of earnings (up from a prior 30%), and raised the actual dividend — to ¥36 per share for fiscal 2026 with guidance toward ¥40 for fiscal 2027.9 For a Japanese industrial long criticized for hoarding cash, a rising payout backed by real free cash flow is a credibility signal, if a modest one.

The most shareholder-visible move was mechanical rather than strategic: a 5-for-1 stock split effective October 1, 2024, cutting the per-share price to widen retail participation on the 東京証券取引所 Tokyo Stock Exchange (6762.T).14 Splits create no value, but in the Japanese context they matter at the margin — a lower board-lot cost genuinely broadens the domestic retail base, and the Tokyo exchange has been pressuring companies to improve liquidity and valuations. Reading the split alongside the higher payout ratio, the fairest interpretation is that TDK is responding, incrementally, to the same governance push that the Tokyo Stock Exchange has aimed at the whole market: return more cash, widen the shareholder base, and narrow the gap between corporate value and market value. These are welcome but modest steps, not a shareholder-return revolution.

A brief diligence aside is warranted on two items a careful analyst would keep in the peripheral vision. The first is currency: as a Japanese exporter with dollar- and renminbi-linked revenues, a meaningful slice of TDK's reported yen growth in strong years reflects a weak yen rather than underlying volume, and the reverse would bite if the yen strengthened — so "record sales in yen" always deserves a mental haircut for translation effects. The second is the joint-venture accounting around Ampace and the battery structure: because material economics run through entities TDK does not wholly own, the consolidated segment disclosure is less transparent than a fully-owned business would be, and investors are to some degree trusting management's characterization of a franchise they cannot fully see through. Neither is a red flag; both are reasons to read the footnotes and the cash flows, not just the headline segment margins.

One nuance is worth flagging on the return targets, because loose reporting often blurs them. TDK operates a group-level ambition — management framed a return-on-invested-capital target of 12% or higher on the FY2026 call — alongside the more granular BizROA hurdle used to police individual business units.9 These are not the same number and should not be conflated: the group target is the promise to shareholders, while the unit-level hurdle is the internal enforcement mechanism that is supposed to prevent weak businesses from dragging the group figure down. A skeptic's question is whether the enforcement has teeth — whether a chronically sub-hurdle unit actually gets sold, or merely gets a restructuring plan and another year. The honest evidence so far is mixed: the RF360 exit shows the willingness exists, but no comparably decisive cut has been forced under the formal BizROA banner during Saito's tenure.

How should an investor grade Saito so far? The honest answer is "promising but unproven." The narrative across recent earnings calls has been consistent — batteries fund the transformation, passives and magnets re-leverage to electrification and AI, capital gets held to a return standard — and consistency of story across quarters is itself a governance positive. Management has also, notably, kept raising guidance through fiscal 2026 rather than setting soft targets it could later beat, and the year delivered record sales and profit against those raised bars, which is the kind of over-deliver-versus-promise behavior that builds credibility over time.9 But the acid test of a capital-allocation framework is what it does in a downturn and whether management will actually shrink or sell an underperforming unit rather than merely narrate discipline. That test has not yet come under Saito, whose entire tenure has coincided with a favorable demand backdrop. The next two moves — a factory in India and a startup in San Diego — are where the transformation stops being a slide and starts spending money.

IX. Strategic Growth Vectors: Sohna (India) and the June 2026 Fabric8Labs Acquisition

For most of its life, TDK's battery empire had a single center of gravity: China. That concentration is efficient and, in the late 2020s, dangerous — which is why the company's most important recent physical bet is a plant not in Guangdong but in Haryana. On September 4, 2025, India's electronics minister inaugurated a state-of-the-art lithium-ion battery plant built by TDK in Sohna, in the National Capital Region, a facility reported at roughly ₹3,000 crore of investment on a large campus, designed to scale toward around 200 million battery packs per year — pitched as roughly 40% of India's mobile-battery requirement — and to employ several thousand people.13[^16] The batteries feed phones, laptops, wearables, and earbuds for the local market.

The project had been telegraphed for two years — reports in late 2023 flagged TDK's intent to build lithium-ion battery capacity in Haryana to serve Apple's India ambitions — so its 2025 opening was the execution of a well-signposted strategy rather than a surprise.[^16] Read past the ribbon-cutting and the strategy is a two-for-one hedge. First, it is an Apple-driven "Make in India" play: as Apple diversifies iPhone assembly out of China, its component suppliers must follow, and a domestic battery-pack base lets TDK stay on the bill of materials as the supply chain regionalizes.[^16] India's production-linked incentive schemes and its electronics-manufacturing-cluster support sweeten the economics, and the local market for phone and device batteries is itself enormous and growing.13 Second, it is a geopolitical insurance policy against exactly the US-China friction that threatens ATL's Chinese manufacturing.

The nuance a careful analyst should hold onto is that a battery "pack" and a battery "cell" are not the same thing, and the distinction is where most of the value and most of the risk live. The cell — the electrochemical heart, with its electrodes and electrolyte — is the hard, high-value, IP-dense part, and it has historically remained anchored in China. A pack is the assembly of cells with protection circuitry and housing; it is genuinely useful local manufacturing but a lower step on the value ladder. If Sohna is initially weighted toward pack assembly with cells still flowing from China, then the geopolitical hedge is partial: a serious disruption to Chinese cell supply would still bite. Building a genuine, deep manufacturing base outside China — cells included — is a multi-year, capital-heavy project, not a switch to be flipped in a crisis. Sohna is a real and meaningful start, and the direction of travel is right, but it is not a completed de-risking, and investors should watch how quickly cell-level capacity actually migrates.

The second bet points at an entirely different frontier. On June 10, 2026, TDK announced a definitive agreement to acquire Fabric8Labs, a San Diego startup, for up to $400 million — an upfront cash payment plus a multi-year earnout.10 Fabric8Labs is the pioneer of Electrochemical Additive Manufacturing (ECAM), and the technology is worth explaining in plain terms because it is the crux of the thesis. Conventional 3D printing melts metal powder with a laser; ECAM instead uses a controlled electrochemical reaction — think of an exquisitely precise, digitally patterned electroplating — to grow structures of pure copper directly, at microscopic resolution, onto semiconductors and thermal components.11 Pure copper is the best affordable conductor of heat there is, and being able to print it into intricate cooling geometries is exactly what the next problem in computing demands.

That problem is AI data-center heat. As accelerator chips pack more transistors into denser racks, air cooling has hit a wall and the industry is racing toward liquid cooling. Fabric8Labs claims its ECAM-enabled cooling structures can pull accelerator temperatures down materially — reductions on the order of several degrees per kilowatt versus competing solutions — which, at data-center scale, translates into real performance and energy savings.11 For TDK, this is the ferrite-tree instinct firing again: buy a differentiated core process, then grow a canopy of high-margin applications (data-center thermal management first, then power and RF components) from it.

The elegant part of the story is provenance. Fabric8Labs was not a random auction win; it was originally spotted and seed-funded by TDK Ventures, the company's corporate venture arm, which nurtured the startup for years before TDK bought it outright.10 That is the scouting-to-acquisition pipeline working as designed, and it is the closest thing modern TDK has to a repeatable version of the ATL magic — find an early-stage team with a defensible process, fund it, then acquire it once the thesis is proven. It is also a deliberate answer to the classic corporate-VC failure mode, in which a big company scatters small checks for innovation theater and never converts any of them into strategic reality. TDK is explicitly trying to run the pipeline the other way: use the venture arm as reconnaissance for full acquisitions in areas its medium-term plan has already prioritized.

The structure of the deal itself signals appropriate caution. Of the up-to-$400 million, a meaningful portion is a multi-year earnout rather than upfront cash, which ties the ultimate price to the technology actually hitting commercial milestones.10 That is the right way to buy a pre-scale startup — you pay the big money only if the thesis proves out. The skeptic's caution nonetheless stands: even a well-structured $400 million is a venture bet, not a sure thing, and the AI-cooling market is crowded with well-funded incumbents and startups all chasing the same liquid-cooling gold rush. Fabric8Labs' claimed advantage — pulling accelerator temperatures down by several degrees per kilowatt versus competing approaches — is a vendor claim that will have to survive contact with real hyperscaler deployments before it becomes revenue.11 It is optionality, not yet a segment, and it should be valued as such: a cheap-ish call option on a large future market, embedded in a company whose earnings today come almost entirely from batteries. Whether TDK can industrialize ECAM at data-center volumes is the open question — and it feeds directly into how we should frame the company's competitive moat.

X. Strategic Playbook (Hamilton Helmer's 7 Powers & Porter's 5 Forces)

Where, precisely, does TDK's advantage live — and how durable is it? Run the company through Hamilton Helmer's 7 Powers and the picture is one of genuine but unevenly distributed moats.

Frameworks can degrade into checklists, so the discipline is to ask not "does TDK have this power?" but "how durable is it, and against whom?" With that lens, the picture is one of genuine but unevenly distributed moats rather than a uniform fortress.

The strongest claim is Cornered Resource. ATL's two decades of patents and process know-how in thin, safe lithium-polymer pouch cells constitute a body of practical knowledge — how to formulate electrolytes and engineer packaging so cells don't swell or ignite in a device pressed against a human body — that competitors cannot simply reverse-engineer from a datasheet. TDK is trying to extend this into a next-generation cornered resource with CeraCharge, its solid-state technology. In June 2024 TDK announced it had developed a material for a solid-state battery reaching an energy density of about 1,000 Wh/L — roughly 100 times the density of its earlier solid-state cells — using an oxide-based solid electrolyte and lithium-alloy anodes, aimed at replacing coin cells in wearables like earbuds and hearing aids.12 The investor's discipline here is to separate proof from press release: TDK was explicit that this was a material-stage breakthrough, with cell design and mass production still ahead.12 It is a promising lab result and a real R&D lead, not yet a shipping product or a proven moat.

Scale Economies are the second power. ATL's multi-billion-unit annual manufacturing footprint — now spanning China and, increasingly, India — creates a unit-cost structure that a subscale entrant cannot match, and in a business where a few percentage points of yield or cost decide who wins Apple's volume, scale is a self-reinforcing advantage. Battery manufacturing is unforgiving in a specific way: the difference between a good producer and a great one is often measured in yield — what fraction of cells come off the line meeting spec — and yield improves with cumulative production experience and process refinement. A player shipping billions of cells simply climbs that learning curve faster and amortizes its enormous plant investment over more units than a challenger can. This is the same dynamic that lets the largest semiconductor foundries stay ahead, and it is why "just build a battery factory" is not a credible threat to ATL from a standing start.

Switching Costs are the third, concentrated in the non-battery segments. Once a specific MLCC or MEMS sensor is designed into an automotive platform, it is locked in for the multi-year life of that vehicle model, because requalifying a safety-relevant component is expensive and slow. That is why the automotive pivot in passives and sensors matters beyond its current margins: it converts cyclical, commoditized parts into sticky, design-in revenue with a longer tail.

Now Porter's Five Forces, which is less flattering. Bargaining power of buyers is high — arguably the defining risk. TDK's largest battery customer (widely understood to be Apple, the perennial "Customer A" of Japanese supplier disclosure) wields enormous leverage: it commands the volume, it can dual-source, and it relentlessly pressures suppliers on cost. An 18% battery margin is impressive precisely because it is earned against the most powerful buyer in electronics — but that same buyer's power is what caps the upside and threatens the downside. Threat of substitutes is moderate: pouch lithium chemistry could eventually cede ground to solid-state or other formats, but TDK's own heavy R&D in solid-state (CeraCharge) and medium-format cells (Ampace) is a hedge against being disrupted by the very transition it is trying to lead. Rivalry is intense in passives (Murata, Kyocera) and rising in batteries (Chinese competitors moving up-market). Supplier power and threat of new entrants are more benign for a player of TDK's scale.

A useful way to hold all of this together is to notice that TDK's powers point in opposite directions on the same business. In batteries, cornered resource and scale economics are strong and getting stronger, but buyer power is extreme; the moat is deep but the toll it can charge is capped by Apple. In passives and sensors, buyer power is more diffuse and switching costs are rising through automotive design-ins, but the underlying products are closer to commodities and rivalry with Murata and Kyocera is relentless; the toll is easier to charge but the moat is shallower. The company does not have one clean competitive position — it has a portfolio of partial ones, which is precisely why the consolidated margin sits where it does and why the investment case is genuinely arguable rather than obvious.

Net it out and TDK's moat is real but asymmetric: deepest in battery materials and manufacturing scale, thinnest exactly where the customer is most powerful. A durable competitive advantage that depends on continuously out-innovating for a single dominant buyer is a strong position and a permanent source of tension. That tension is the heart of the bull-versus-bear debate.

XI. Skeptical Stress Test & Bull vs. Bear Case

Begin with the uncomfortable fact that a short-seller would put on the first slide: over half of TDK's revenue and roughly three-quarters of its segment operating profit come from consumer batteries, and a large share of that flows through a handful of customers led by Apple.9 This is not diversification; it is a magnificent concentration. If Apple squeezes battery margins, dual-sources aggressively, or simply presides over a smartphone market that has plateaued, TDK's earnings engine does not gently decelerate — it stalls, and the moderately profitable materials businesses are not remotely large enough to catch it. Every other argument about TDK is a second-order refinement of this first-order dependency.

The bull case rests on three vectors, each with genuine evidence behind it. The first is GX — the medium-battery growth engine through Ampace, where home energy storage and micro-mobility are expanding fast and where TDK plays through a structure combining ATL's packaging with CATL's chemistry, in a market neither incumbent optimized for.7 This is the most tangible of the three because it is already generating revenue at scale and riding a demonstrable, policy-supported demand curve in residential storage. The second is the AI data-center wave hitting TDK from two directions at once: nearline HDD heads in the magnetics segment, which turned sharply higher this year as hyperscalers bought high-capacity storage,9 and the Fabric8Labs pure-copper thermal bet, which — if it industrializes — opens a high-margin new category precisely as liquid cooling becomes mandatory.10 Management has put a number on this ambition, framing AI-ecosystem-linked sales as heading toward roughly 15% of the group by fiscal 2027, which if achieved would materially diversify the profit base away from the smartphone.9 The third is solid-state optionality: if CeraCharge moves from material to mass-produced cell, TDK could own the replacement for the billions of coin cells in the world's wearables, a category with real volume and, crucially, regulatory tailwinds as jurisdictions tighten rules on disposable button cells.12 Notice that two of these three are still promises, not yet earnings — the discipline for a bull is to size them as options, not to capitalize them as if they were already segments.

The strongest version of the bull case is not any single vector but the compounding machine underneath them: a business throwing off enough cash from batteries to self-fund a portfolio of shots on goal, run by a management team that has shown it can both originate opportunities (TDK Ventures) and prune losers (RF360). If even one of the three vectors becomes an ATL-scale branch of the ferrite tree, the current valuation of the "boring component maker" would look, in retrospect, far too cautious. The bull is really betting on the reinvention process, not on any one product.

The bear case is the mirror image, and it is disciplined rather than alarmist. First, supplier squeeze: Apple has every incentive and growing ability to shift battery volume toward lower-cost Chinese suppliers such as 欣旺达 Sunwoda or 比亚迪 BYD, and even a few points of margin compression on a ¥1.37 trillion segment is billions of yen of profit. The mechanism here is worth stating precisely, because it is the most likely way the bull case erodes: it need not be a dramatic loss of Apple's business, merely the steady, quarter-by-quarter pressure that a dominant buyer applies to a supplier it can credibly replace at the margin. That slow grind shows up as a declining Energy Application margin long before it shows up as lost volume. Second, geopolitical disruption: ATL's manufacturing heart is in China, and any serious escalation in US-China trade or technology restrictions could impair the group's core profit pool faster than the Sohna hedge can compensate — India is a start, not a shield.13 A related, quieter risk is that TDK's most valuable growth vector, Ampace, is a Chinese-domiciled joint venture with a Chinese national champion, which could itself become entangled in trade or investment-screening measures aimed at Chinese battery firms. Third, the slow-payback problem: if the sensor segment cannot lift margins convincingly into the teens, the InvenSense purchase remains a long-dated drag on group returns and a live example of buying growth at too high a price.8

There is also a valuation-and-cyclicality overlay the bear would press. TDK's non-battery segments remain cyclical, tied to electronics and automotive production, and the current record results have coincided with a strong demand environment and favorable currency. A cynic would argue that some of the recent margin expansion in passives and magnetics is cyclical rather than structural, and that a normalized-earnings view would look less flattering than the FY2026 headline. The counter is that the AI and electrification tailwinds are secular, not cyclical — but distinguishing the two requires several more years of data than management or investors currently have.

Push the activist's logic all the way and you arrive at the most provocative question about TDK: why should a spectacularly profitable, scarcity-protected battery business be permanently welded to a portfolio of cyclical, single-digit-to-low-double-digit-margin materials units at all? A sum-of-the-parts sceptic could argue that the battery franchise, valued on its own as a high-margin growth asset, might command a multiple the blended conglomerate never will — the classic "conglomerate discount" argument. TDK's implicit rebuttal is threefold: the materials businesses supply the technological adjacencies (magnets, sensors, thermal components) that keep the company relevant across device cycles; the group's balance-sheet strength and cash generation let it fund long-dated bets like solid-state and ECAM that a pure-play battery maker might not; and BizROA is meant to ensure the laggards either earn their capital or get cut. Whether that rebuttal holds is, again, a question the framework has not yet had to answer under stress. An investor should treat the conglomerate structure as an open governance question, not a settled virtue.

Weighing the two, the intellectually honest position is that TDK is a high-quality operator with a genuine materials-and-electrochemistry edge, tethered to a customer-and-country concentration it cannot fully escape and is only beginning to diversify. BizROA is management's implicit answer to the structure question, but an answer still awaiting its first recession-grade proof. For investors, the debate resolves into a small number of things actually worth watching.

The KPIs that matter most are, first, Energy Application Products operating margin — the single cleanest gauge of whether ATL is holding pricing power against Apple, and the number that most directly drives group earnings. Second, the revenue mix from AI/data-center and non-smartphone applications — management has framed AI-ecosystem exposure as heading toward roughly 15% of sales, and progress against that is the truest measure of diversification away from the smartphone.9 Third, over the longer arc, group ROIC against the ~12% target — the honest scorecard for whether Saito's transformation is compounding capital or merely reshuffling it.9 Track those three and you are tracking the real TDK.

XII. Epilogue & Key Takeaways

The through-line of TDK's ninety years is a company that keeps surviving the death of its own products. Cassettes died; TDK lived. VHS died; TDK lived. Consumer HDDs faded; TDK lived. Each time, the escape route was the same instinct planted in 1935 — take a genuine core competence in materials or electrochemistry and regrow the canopy on a new branch before the old one falls. The ferrite tree was never really about ferrite. It was about the discipline of reinvention.

The second, less obvious lesson is about how TDK reinvents: not primarily through its own labs, but through its willingness to buy and empower outsiders. The company's single greatest value-creation event was purchasing a Hong Kong founder's battery startup for a rounding error and letting him build — even, remarkably, letting him spin off the crown jewel into 宁德时代 CATL and walking away with cash rather than a fight. That same scouting muscle, institutionalized in TDK Ventures, found and funded Fabric8Labs at the seed stage and then brought it home. Corporate venture capital is usually where big companies go to look innovative while learning nothing; TDK has used it, at least twice, as a genuine origination engine for its future.

It is tempting, at the end of a story like this, to render a verdict. The more useful thing is to name the specific evidence that would move the case in either direction over the next several years. Watch whether the Energy Application margin holds near its high-teens level or drifts down under Apple's pressure — that single line is the truest read on whether the cornered resource is still cornered. Watch whether the AI-and-electrification revenue share actually climbs toward management's roughly-15% marker, which would prove the diversification is real rather than rhetorical. Watch whether cell-level manufacturing genuinely migrates to India, converting the Sohna hedge from partial to substantial. And watch what the BizROA framework does the first time a major unit stays below its hurdle through a downturn — that is when capital discipline stops being a slide and reveals itself as either a governance mechanism or a slogan.

Whether that model carries TDK through the next decade is undecided, and honestly assessed it should be. The battery jackpot has already been won and largely booked; the questions now are defensive (can it protect ATL's margins against the world's most powerful buyer and its riskiest single country) and speculative (can solid-state, medium-format storage, and copper-printed cooling become the next ATL-scale branches rather than expensive science projects). The company's own capital-discipline framework is the right tool for the job and remains untested in a real downturn. For a long-term investor, TDK is neither the sleepy component supplier of its reputation nor the invincible compounder its best year suggests. It is a materials-science house that got electrochemistry spectacularly right once, and is now spending that windfall trying to do it again — in front of an audience that has every right to ask for the evidence.

References

-

Discover TDK's History and Milestones — TDK Corporation ↩↩↩↩

-

Venture Spirit Relentlessly Taking on Challenges Drove TDK's 90 Years of Innovation — TDK Corporation ↩

-

TDK Corporation Form 20-F FY2005 (ATL acquisition, ~$100M) — U.S. SEC/EDGAR ↩↩↩

-

TDK buys battery manufacturer for $100M — RCR Wireless News, 2005-06-01 ↩

-

Announcement on Business Alliance and Establishment of Joint Venture with Contemporary Amperex Technology (Ampace) — TDK Corporation, 2021-04-28 ↩↩↩

-

TDK Completes Acquisition of InvenSense ($1.3B) — TDK Corporation, 2017-05-18 ↩↩

-

Earnings Call Transcript: TDK Q4 FY2026 Sees Record Profits — Investing.com, 2026-04-28 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

TDK to Acquire Fabric8Labs, Inc. to Accelerate Data Center Initiatives — TDK Corporation, 2026-06-10 ↩↩↩↩↩

-

Fabric8Labs to be Acquired by TDK Corporation, Accelerating Electrochemical Additive Manufacturing — PR Newswire, 2026-06-10 ↩↩↩

-

TDK Successfully Developed a Material for Solid-State Batteries with 100-Times Higher Energy Density (CeraCharge, 1,000 Wh/L) — TDK Corporation, 2024-06-17 ↩↩↩

-

Union Minister Ashwini Vaishnaw Inaugurates Advanced Lithium-ion Battery Plant in Sohna, Haryana — Press Information Bureau, Government of India, 2025-09-04 ↩↩↩

-

TDK Corp. to Carry Out 5-for-1 Stock Split (effective October 1, 2024) — Moomoo News, 2024 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube