Fujitsu: The Great Pivot and the Ghost in the Machine

I. Introduction & Episode Roadmap

Picture two press conferences, held on the same island nation, roughly a quarter of a century apart, and imagine watching them back to back.

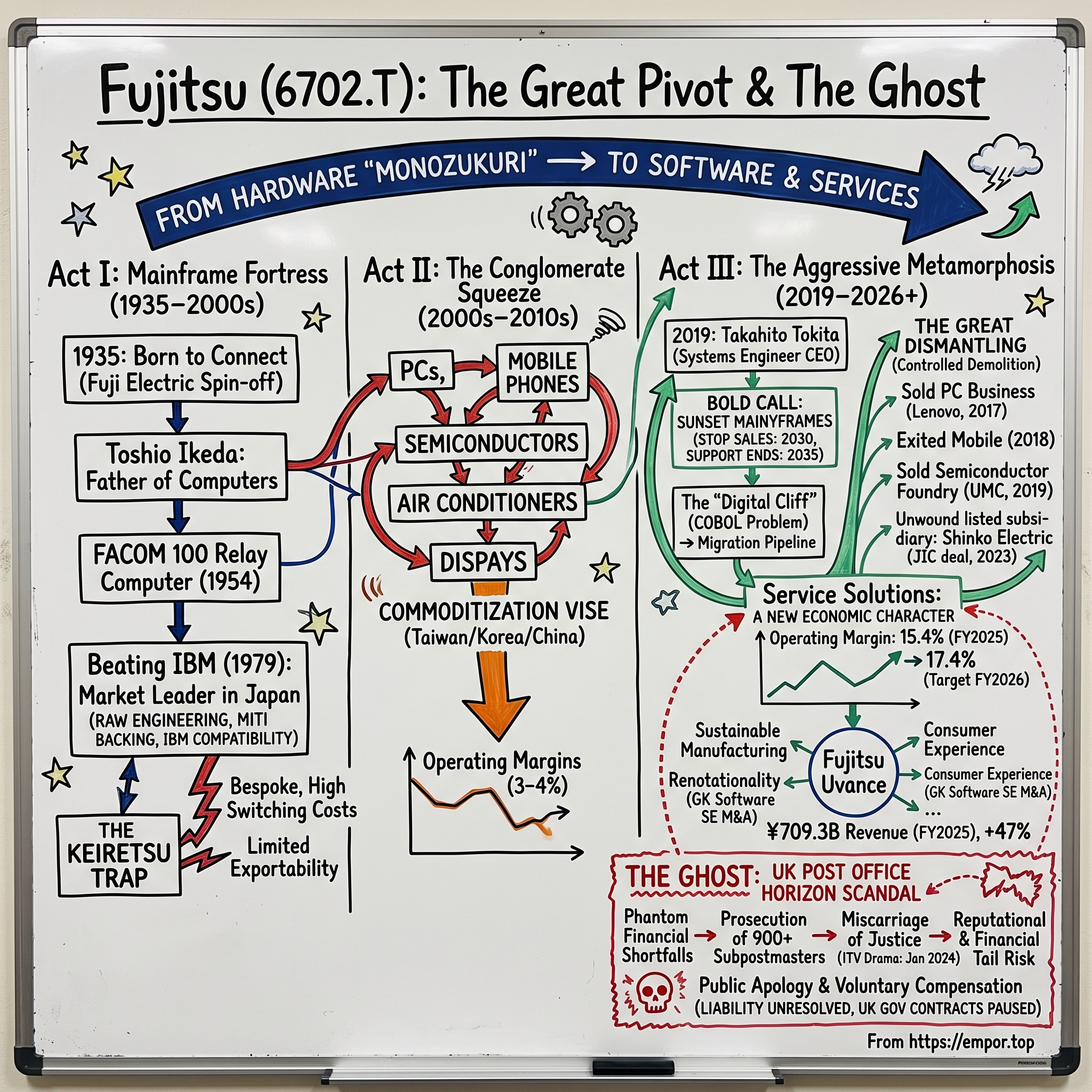

In the first, executives in dark suits stand beside a humming grey cabinet the size of a wardrobe — a mainframe computer, the beating heart of a Japanese bank, a government ministry, a national railway. This is the machine that runs the country. It is proprietary, unfathomably complex, and utterly irreplaceable. The men on stage are proud. They have built the invisible plumbing of modern Japan.

In the second, held in Kawasaki in April 2026, a soft-spoken former systems engineer named Takahito Tokita (時田隆仁) walks investors through a very different story. Fujitsu, the company that built those mainframes, has just reported ¥3,502.9 billion in revenue and — far more importantly — an adjusted operating profit of ¥390.5 billion, up 27.1% year over year, its fourth consecutive record.1 The grey cabinets are being deliberately, methodically killed. Fujitsu has told its customers that it will stop selling mainframes by fiscal 2030 and switch off support in 2035.10 The company that defined Japan's post-war hardware miracle is, on purpose, executing its own founding technology.

That is the paradox at the center of this story. Over roughly two decades, 富士通株式会社 Fujitsu Limited has dismantled almost everything that once defined it — personal computers, mobile phones, semiconductors, air conditioners, chip packaging — and reassembled itself as a high-margin cloud-software and digital-services business. Its core Service Solutions segment now earns a 15.4% operating margin, a number that would have been science fiction for the old conglomerate.1 This is one of the most aggressive corporate metamorphoses in Japanese history: the deliberate destruction of monozukuri (ものづくり, the near-religious craftsmanship of physical making) in favor of software.

And yet, at the precise moment the financial transformation is bearing fruit, Fujitsu is haunted. Buried inside its portfolio is a ghost — a piece of accounting software called Horizon, sold to the United Kingdom's Post Office, that produced phantom financial shortfalls and helped send more than 900 innocent local postmasters to bankruptcy, criminal records, prison, and in at least thirteen cases, suicide.15 It is one of the largest software-induced miscarriages of justice in modern legal history, and it has Fujitsu's name on it.

So here is the spine of the story we are going to unwind. Can an 80-plus-year-old Japanese industrial conglomerate genuinely escape its hardware past and the reputational fallout of a legacy IT catastrophe to become a global cloud-native software titan? The financial engine says one thing. The ghost in the machine says another. Let's start where every great pivot starts — with the thing being pivoted away from.

II. Spin-offs, Siemens, and the Battle with Big Blue

To understand why Fujitsu was so good at building mainframes, you have to understand that Fujitsu was, quite literally, born to build machines that connect things.

The year was 1935. In a Japan racing to industrialize, a company called Fuji Electric spun off its telecommunications division into a new entity: Fuji Tsushinki Manufacturing, a maker of telephone switching equipment.3 The lineage matters, because Fuji Electric itself was a joint venture born in 1923 from an unlikely marriage — Japan's Furukawa Group and Germany's Siemens. The very name "Fujitsu" is a compression of that heritage: Fu from Furukawa, ji echoing the Japanese pronunciation of Siemens (Shiimensu), stitched together into a single corporate identity. From day one, this was a company built at the intersection of Japanese industrial ambition and imported German engineering discipline, making the switchboards that routed a nation's phone calls.

Telephone switching, it turns out, is a wonderful school for computing. Both are about logic gates — relays clicking open and shut, routing signals down one path or another. And in the early 1950s, one eccentric, chain-smoking visionary saw that connection more clearly than anyone else in Japan.

The genius of Toshio Ikeda

Toshio Ikeda (池田敏雄) was not a typical Japanese salaryman. He was an obsessive, a hardware savant who reportedly worked himself to exhaustion, and he became convinced that the switching relays Fujitsu already manufactured could be wired into a calculating machine. In October 1954, his team completed the FACOM 100, a relay-based automatic computer — one of Japan's first practical machines of its kind.4 It was slow and enormous, a room full of clattering electromechanical switches, but it worked. Ikeda had dragged a telephone-parts company into the computer age almost by force of personal will. He would go on to drive Fujitsu's computing strategy for two decades, and inside the company he is remembered as the father of its computer business — the single human decision that changed the entire trajectory of the firm.

Beating Big Blue at home

Here is where the story gets genuinely remarkable. Through the 1960s and 1970s, the global computing world had exactly one sun around which everything orbited: IBM. To compete with IBM anywhere was audacious. To beat it was almost unheard of.

Fujitsu did it in Japan. It leaned on three advantages that compounded together. First, raw engineering — its FACOM M-series mainframes were high-performance machines that could stand toe to toe with IBM's best. Second, industrial policy: Japan's Ministry of International Trade and Industry, MITI, actively backed domestic computing champions against American dominance, and protectionist procurement gave homegrown machines a running start. Third, and most durably, Fujitsu made a strategic bet to build machines compatible with IBM's software ecosystem, so Japanese customers could switch to Fujitsu hardware without abandoning their programs. By 1979, the improbable had happened: Fujitsu edged past IBM to become the market-share leader in Japan's domestic computer market — a feat no other company on Earth had managed.5

The keiretsu trap

But every strategic victory carries the seed of a future constraint, and Fujitsu's did too. To win Japan's banks, utilities, and ministries, Fujitsu did not just sell them boxes. It embedded itself. It wrote bespoke software, customized every deployment, and wrapped its customers inside the dense web of 系列 keiretsu business relationships — the interlocking, long-term, deeply loyal corporate networks that define Japanese commerce. The result was a systems-integration model with switching costs so high they were practically walls. A Japanese megabank running on a Fujitsu mainframe, with decades of custom COBOL code layered on top, was not going anywhere.

That was fabulous for revenue stability and lethal for scalability. Each contract was a snowflake — unique, hand-built, non-repeatable. You could not take a system integration project designed for a Tokyo ministry and resell it in Frankfurt or Chicago. The very intimacy that made Fujitsu unassailable at home made it nearly impossible to export. Fujitsu had built a fortress. It just happened to be a fortress with only one country inside it. And as the twentieth century closed, that fortress was about to be surrounded on every other flank.

III. The Conglomerate Squeeze and the Lost Decades

If the first act of the Fujitsu story is a triumph, the second act is a slow, grinding disappointment — the tale of a company that made too many things, in too many markets, for too little money.

Walk into an electronics store anywhere in Asia in 2005 and you could have bought a Fujitsu laptop, held a Fujitsu-branded mobile phone, watched a display driven by Fujitsu components, and gone home to a room cooled by a Fujitsu General air conditioner. The company had sprawled into a bewildering conglomerate spanning semiconductors, PCs, mobile handsets, display panels, servers, telecom gear, and HVAC. On paper, diversification. In reality, a value trap.

The commoditization vise

The problem was structural and unforgiving. Through the late 1990s and 2000s, hyper-efficient competitors from Taiwan, South Korea, and China turned one hardware category after another into a brutal commodity. Taiwanese contract manufacturers could build a laptop cheaper than Fujitsu could source the parts. Korean giants poured capital into memory chips and displays at a scale that made Japanese margins evaporate. Chinese manufacturers did the same to appliances. In business after business, Fujitsu found itself competing on price in markets where it had no cost advantage whatsoever.

The financial symptom was chronic. For much of this period Fujitsu's consolidated operating margins languished in the low single digits — the 3-to-4% range — a level that signals a company running hard just to stand still. And a chunk of that drag came from its constellation of listed subsidiaries: capital-hungry hardware businesses like the chip-packaging maker Shinko Electric Industries (新光電気工業) and the air-conditioning firm Fujitsu General (富士通ゼネラル), which soaked up cash and reinvestment while the market applied a hefty conglomerate discount to the whole structure. Public investors could see the trap plainly: Fujitsu was a mediocre hardware holding company wearing the costume of a technology leader.

The great dismantling

Somewhere in the 2010s, the internal argument shifted from "how do we fix hardware?" to "why are we still in hardware?" And Fujitsu began, piece by piece, to take itself apart.

In November 2017, it sold a 51% controlling stake in its PC business — Fujitsu Client Computing Limited — to China's Lenovo, folding its laptops into the world's largest PC maker rather than fighting a losing war on price.6 Months later, in early 2018, it agreed to hand its mobile-handset business, FCNT, to the Japanese private-equity firm Polaris Capital Group, exiting the smartphone race entirely.7 Then in 2019 it sold Mie Fujitsu Semiconductor, its chip foundry, to Taiwan's United Microelectronics Corporation (UMC), which took full ownership that October — a quiet admission that Fujitsu could not win the capital arms race of leading-edge chip fabrication.8

Each divestiture told the same truth from a different angle: the traditional Japanese hardware model, in which a national champion made everything itself, was broken. These were not distressed fire sales so much as a controlled demolition — and crucially, activist and institutional investors had begun circling, accumulating stakes and pressing management to go faster, to unwind the cross-shareholdings, to stop apologizing for the conglomerate and simply dismantle it.

What none of these piecemeal exits had yet produced, however, was a positive thesis. Selling off losers is not a strategy; it is triage. The question hanging over Fujitsu at the end of the 2010s was whether anyone at the top could articulate what the company was for once the hardware was gone. In 2019, that person arrived — and he came from an unexpected corner of the building.

IV. Takahito Tokita's Masterclass: Sunsetting the Mainframe

For most of its history, Fujitsu was run by hardware men — engineers who had come up through the physical businesses of building machines. So the appointment of Takahito Tokita as president and CEO in June 2019 was, quietly, a revolution in itself.9

Tokita was not a hardware man. He was a systems-integration lifer — a career spent inside the messy, human, code-and-consulting side of the business, delivering software projects for enterprise clients, and at one point running Fujitsu's Global Delivery organization, the sprawling network of engineers who actually implement systems for customers around the world.9 Where his predecessors thought in terms of factories and product roadmaps, Tokita thought in terms of services, delivery, and margins. Handing him the company was, in retrospect, a signal that the board had decided the future was not something you manufacture. It was something you deliver.

The boldest call in Japanese tech

Then, in February 2022, Tokita's Fujitsu did something that made hardened enterprise-IT veterans put down their coffee. It publicly announced end dates for its own crown jewels. Mainframe manufacturing and sales would cease by fiscal 2030, with support winding down by 2035. UNIX server sales would end even sooner, by the close of fiscal 2029, with support ending in 2034.10

Sit with how radical this was. These mainframes were not a dying side business. They were the load-bearing infrastructure of Japanese banks, insurers, and government agencies — some of the stickiest, highest-switching-cost revenue in the entire technology industry. Announcing a hard sunset was the corporate equivalent of a landlord telling his most reliable, lease-locked tenants that the building would be demolished on a fixed date, so they had better start planning their move. It was a deliberate act of demolishing Fujitsu's own moat — and it only makes sense when you understand the arbitrage underneath it.

The "digital cliff" and the COBOL problem

Japan had a looming crisis that its own government had named the "digital cliff": a vast installed base of aging, proprietary systems running on COBOL, a programming language from the 1960s, maintained by an ever-shrinking population of engineers who understood it — many of them nearing retirement. Tens of thousands of critical business processes were trapped inside code almost nobody alive fully understood anymore.

Here is the analogy that makes it click. Imagine a country's entire financial system running on instruction manuals written in a dead language, maintained by a handful of elderly scholars, with no young readers coming up behind them. That is COBOL in corporate Japan. Every year that passes, the risk of a catastrophic, unfixable failure grows.

Fujitsu's sunset was a way of turning that terror into a business. By setting a firm expiry date on the old machines, Fujitsu forced its most loyal customers to confront the migration they had been deferring for decades — and positioned itself, the company that wrote much of the original code, as the natural partner to lead them off it. To make the grueling work economical, Fujitsu invested in AI-driven tools that can analyze, document, and help translate legacy COBOL into modern languages like Java — work it has pursued in collaboration with IBM, its ancient rival. The strategic logic is elegant: convert an obligation to support dying hardware into a multi-year, high-value migration pipeline. Whether Fujitsu can actually execute thousands of these migrations without a headline-grabbing failure is a separate and very live question — one we will stress-test later.

Cleaning up the balance sheet

The final piece of Tokita's early masterclass was financial housekeeping of the boldest kind. Fujitsu had long held a controlling stake in Shinko Electric Industries, the chip-packaging subsidiary that symbolized everything about the old capital-heavy conglomerate. In December 2023, Fujitsu agreed to sell its roughly 50% stake to a consortium led by the state-backed Japan Investment Corporation (JIC) — a deal that valued Shinko at around ¥685 billion in total and delivered Fujitsu proceeds of ¥285.1 billion for its holding.11 The transaction closed in 2025, with Shinko delisted and Fujitsu's cash beginning to flow in late August.12

This was not just a sale; it was a statement. Unwinding a listed subsidiary that management had tolerated for years demonstrated a genuine commitment to capital efficiency and portfolio discipline — exactly what the activists had been demanding. The proceeds gave Fujitsu a war chest, and how it chose to spend that war chest would become the truest test of whether the transformation was real or theatrical. To judge that, we need to look under the hood of the modern financial engine.

V. The Engine Today: Segment Financials and Fujitsu Uvance

Let's open the books, because the numbers Tokita's Fujitsu now produces are genuinely different in kind from the old conglomerate — and understanding why matters more than memorizing the figures.

For fiscal 2025, the year ended March 31, 2026, Fujitsu reported consolidated revenue of ¥3,502.9 billion, down 1.3% — but that headline decline is misleading in the most important way. The drop came from structural reforms and divestitures shedding low-quality revenue; on an organic basis, the business grew.1 The revenue line went slightly down while the profit line went sharply up, and that divergence is the whole thesis. Adjusted operating profit rose 27.1% to ¥390.5 billion, a fourth straight record.1 Net profit landed at ¥449.4 billion — more than double the prior year — but here honesty is required: a large slice of that was one-time capital gains from selling Shinko Electric and Fujitsu General, not repeatable operating earnings.12 A sophisticated reader separates the two. The operating-profit growth is the signal; the net-profit spike is partly a fireworks display funded by asset sales.

The one segment that matters

Strip away the noise and Fujitsu today is essentially one great business with some legacy attachments. The Service Solutions segment — consulting, systems integration, cloud, and managed services — generated ¥2,346.9 billion in revenue, about two-thirds of the company, and ¥361.4 billion in adjusted operating profit, the overwhelming majority of the total.1 Its operating margin reached 15.4%, up 2.5 percentage points in a single year.1 On the FY2025 earnings call, CFO Takeshi Isobe (磯部武志) attributed the margin gain to "standardization and automation of development work, as well as the benefits of using AI in the development process."2

That margin trajectory is the number to watch obsessively, because it is where the bull and bear cases collide. A services business dragging itself from single-digit conglomerate margins toward the mid-teens is a business genuinely changing its economic character. Management guided to a Service Solutions margin of roughly 17.4% for fiscal 2026 — another two-point jump.2 The remaining Hardware and Device Solutions activities, meanwhile, have been shrunk to their diminished economic weight: low-margin legacy hardware, support, and declining system platforms, kept alive largely to serve the installed base during its long migration off the mainframe.

Fujitsu Uvance: the actual growth engine

Now to the part of the story management most wants you to believe in — and where independent skepticism earns its keep. 富士通ユーバンス Fujitsu Uvance is the brand for Fujitsu's cross-industry, cloud-centric solutions business, and it is growing fast. In fiscal 2025, Uvance revenue reached ¥709.3 billion, up 47% year over year, and it now accounts for roughly 30% of Service Solutions.12 On the earnings call, Isobe noted Uvance was "up 47%" and that, together with modernization work, it had "surpassed the mid-term management plan's goals."2

What actually is Uvance? Strip the marketing and it is an attempt to solve Fujitsu's oldest problem — the snowflake curse of custom, non-repeatable projects — by packaging solutions that can be sold to many customers across industries. It is organized into four vertical, cross-industry offerings (Sustainable Manufacturing, Consumer Experience, Healthy Living, and Trusted Society) sitting on top of three horizontal technology foundations (Digital Shifts, Business Applications, and Hybrid IT). The bet is that a supply-chain solution built for one manufacturer can be resold to the next, converting bespoke consulting engagements into scalable, higher-margin, recurring software-and-services revenue.

To anchor the Consumer Experience vertical in retail, Fujitsu reached for M&A. It pursued the German retail-software specialist GK Software SE through a public takeover launched in 2023 valued at roughly €432 million, and completed the buyout in May 2025, folding GK's point-of-sale and retail cloud platform fully into the group.[^13]13 The strategic logic was to buy immediate, credible SaaS market share in European retail rather than build it slowly from scratch — a reasonable move, though the price paid was a full premium, and whether Fujitsu can globalize a German retail platform is unproven.

The productivity lever — and a caveat

The subtler part of the margin story is internal. Fujitsu has been deploying generative-AI tooling across its own vast engineering workforce to cut the cost of delivering software. In January 2026 it began operating what Tokita described as "a development platform that uses AI to automate processes from requirements definition through implementation and testing."2 The pitch is that AI slashes the grunt work and human-error reworks that plague customized software delivery. It is worth flagging, in the spirit of not simply repeating management's slides: Fujitsu has publicized adoption programs and internal AI tooling, but the precise headcount of engineers using each tool is not consistently disclosed, and productivity claims from any IT-services firm deserve to be verified against actual gross-margin trends rather than taken on faith. So far, the gross-margin trend supports the claim — but it is early. Which brings us to the neighborhood Fujitsu competes in, because margins do not expand in a vacuum.

VI. Competitive Dynamics: The Japanese IT Oligarchy & Hamilton Helmer's 7 Powers

Imagine the Japanese enterprise-IT market as a walled city with a handful of established houses, each controlling ancient, jealously guarded relationships with the banks, ministries, and industrial giants that run the country. Newcomers can raid the outskirts, but the core is divided among a small oligarchy — and Fujitsu is one of its great houses.

The domestic rivals

The scale leader is NTT Data (NTTデータ), whose group revenue runs to roughly ¥4.4 trillion, larger than Fujitsu's entire business and backed by unmatched government and telecom-adjacent relationships thanks to its NTT lineage.19 If Fujitsu is a great house, NTT Data is the royal one. Then there is Nomura Research Institute (NRI, 野村総合研究所), the high-margin aristocrat — smaller in revenue but consistently more profitable, having positioned itself at the lucrative consulting-and-advisory top of the value chain rather than the high-volume systems-integration middle where Fujitsu historically lived. NRI is the benchmark that exposes Fujitsu's ambition: to be seen not as a body shop that writes a lot of code, but as a high-value transformation partner.

Finally, the mirror-image rivals: NEC (日本電気) and Hitachi (日立製作所), fellow former hardware conglomerates undergoing their own parallel pivots to software and services. Watching Fujitsu, NEC, and Hitachi is like watching three aging heavyweights all trying to learn ballet at the same time — each shedding factories, each chasing recurring revenue, each claiming to be the one that will emerge lean and digital. Their simultaneous transformation is itself a risk: they may end up competing away the very margins they are all reaching for.

Seven Powers, honestly applied

The strategist Hamilton Helmer argues that durable competitive advantage comes from a small number of distinct "powers." Run modern Fujitsu through that lens and the picture is genuinely mixed — which is the honest conclusion.

Switching costs — very high, and the true engine of the moat. This is Fujitsu's real power. A Japanese bank whose core systems were built and maintained by Fujitsu over thirty years cannot simply fire it. The proprietary knowledge of that legacy codebase lives inside Fujitsu's engineers. Even the mainframe sunset, paradoxically, deepens this power: the customer must migrate, and the firm that understands the old code is the safest guide off it. Switching costs are why Fujitsu can raise prices on migration work and why its installed base is so defensible.

Scale economies — high, but bounded. Spreading the R&D of the Uvance platform and internal AI toolkits across a very large engineering base does create real operating leverage; that is precisely what the margin expansion reflects. But this scale is overwhelmingly domestic. It is scale within a walled city, not scale across the world.

Counter-positioning — low to medium, and a genuine weakness. Here Fujitsu is on the wrong side. Cloud-native consultancies and global integrators — think Accenture and its Japanese operations — can bid on new, greenfield digital-transformation projects unencumbered by the cost and coordination burden of maintaining a giant legacy customer base. Fujitsu is fast at protecting what it has and structurally slow at chasing what is new. An incumbent defending a fortress rarely moves like a raider.

Brand — a tale of two continents. Inside Japan, the Fujitsu name carries deep institutional trust in corporate and public-sector procurement; it is a safe, respected choice. Outside Japan, that brand power largely evaporates, and — as we are about to see — in one crucial market it has curdled into something actively toxic. Which is the perfect segue into the ghost.

VII. The Ghost in the Machine: The UK Post Office Horizon Scandal

Every acquisition carries hidden cargo. Sometimes it is a synergy. Sometimes it is a time bomb with a 25-year fuse.

In 1998, as part of its long, ultimately frustrated push to become a global player, Fujitsu took full ownership of International Computers Limited (ICL), Britain's national-champion computer company.15 ICL brought engineering talent, a European foothold, and a portfolio of government contracts — including one, won in the 1990s, to build an automated accounting and point-of-sale system for the United Kingdom's Post Office. The system was called Horizon. Fujitsu later rebranded ICL as Fujitsu Services. And for years, Horizon looked like exactly the kind of sticky, blue-chip public-sector contract that global expansion was supposed to deliver.

It was, instead, a catastrophe that would take a human toll almost beyond comprehension.

The phantom shortfalls

Horizon was riddled with bugs. Software errors, data-transmission faults, and reconciliation glitches caused the system to report money missing from local Post Office branches — shortfalls that did not actually exist. To the subpostmasters running those branches, small business owners and pillars of their communities, the screen simply said their tills were short by hundreds or thousands of pounds. Money they had never taken. Deficits conjured by defective code.

What happened next is the part that transforms a technical failure into a moral one. Rather than concede that its software might be at fault, the Post Office — relying on technical evidence and assurances that Fujitsu's systems were reliable — treated the phantom shortfalls as theft. Over roughly fifteen years, more than 900 subpostmasters were prosecuted for theft, fraud, and false accounting.15 Ordinary people were told the computer could not be wrong and that they alone were responsible. Some remortgaged homes to repay money that was never missing. Careers were destroyed, families shattered, reputations obliterated in small towns where everyone knew everyone. People went to prison. The scandal has been linked to at least thirteen suicides.15 It stands as one of the most widespread miscarriages of justice in British legal history — and its root cause was software.

The explosion

For two decades the story simmered in campaign groups, dogged local journalism, and a long-running legal fight led by former subpostmaster Alan Bates. Then, in the first days of January 2024, the British broadcaster ITV aired a four-part drama, Mr Bates vs The Post Office, dramatizing the ordeal. The public reaction was volcanic. Within days the scandal dominated the national conversation, a statutory public inquiry gathered force, and Fujitsu — until then a name most Britons associated vaguely with laptops — became a symbol of institutional cruelty.23

On January 16, 2024, Paul Patterson, co-head of Fujitsu's European business, sat before a committee of MPs and apologized. He acknowledged that Fujitsu had been "involved from the very start" and had "clearly" let the subpostmasters down, framing a contribution to compensation as a moral obligation.[^17] It was a striking public admission from a Japanese company famously careful about liability — and it opened the door to a financial reckoning that is still, in mid-2026, unresolved.

The liability that will not resolve

The financial architecture of the redress is worth understanding precisely, because it is where the risk to shareholders lives. The compensation is being paid, in the first instance, by the UK government, not by Fujitsu. By early 2025, the government had paid out hundreds of millions of pounds to thousands of claimants, against a total redress bill it has estimated in the billions.16 Fujitsu, for its part, has said it will make a "voluntary financial contribution" — but crucially, it has declined to fix a number until the public inquiry publishes its findings, effectively parking the liability off its balance sheet in the meantime.[^17]

That creates a genuine analytical overhang. The eventual contribution could run to several hundred million pounds; it could be more, depending on how the inquiry apportions blame between the Post Office and Fujitsu. Notably, Fujitsu's FY2025 earnings call contained no material discussion of Horizon provisions2 — an absence that itself tells you the company is waiting, not resolving. And there is a second, quieter cost already being paid: Fujitsu voluntarily paused bidding for new UK government contracts, throttling its public-sector growth in one of its most important Western markets. The moat that protects its existing UK work does nothing to help it win new business while the ghost remains unexorcised. For investors, Horizon is the definition of an unquantified tail risk — probably survivable, genuinely material, and entirely dependent on a process Fujitsu does not control.

VIII. Capital Allocation and Management Credibility

Strategy is what a company says. Capital allocation is what it does with the money. And the truest way to judge whether Fujitsu's transformation is real is to watch where the cash from all those divestitures actually goes — and whether management's own incentives are pointed in the same direction as shareholders'.

Follow the money

Fujitsu's post-Shinko war chest could have been squandered a dozen ways — a splashy, overpriced foreign acquisition to buy global relevance; a vanity hardware bet; empire-building. Instead, the pattern so far has been disciplined and shareholder-friendly. On the FY2025 call, CFO Isobe pointed to ¥170 billion of share buybacks executed in fiscal 2025, with a further ¥150 billion planned for fiscal 2026, and a dividend raised to ¥50 per share as profits grew.2 Free cash flow ran to ¥482.6 billion for the year.2 The proceeds from Shinko and Fujitsu General are being cycled into buybacks, domestic data-center and software investment, and bolt-on acquisitions like GK Software, rather than torched on speculative, high-premium deals.2

The analytical read is favorable but not yet fully proven. Returning capital aggressively while a business is genuinely re-rating is exactly what disciplined management should do, and it aligns with the "asset recycling" narrative management has told consistently across recent presentations.22 The skeptic's caveat is that buying back stock and selling assets is the easy part of capital discipline; the hard part is resisting the temptation to make a transformational overseas acquisition to accelerate the global ambitions that Uvance implies. That test has not yet come.

Skin in the game — modest

Does Tokita eat his own cooking? Partly. His direct shareholding is real but far from founder-scale — a holding of around 106,470 shares ties his personal wealth to the stock without making him a controlling owner.18 His pay, however, is structured to align with performance: for fiscal 2024 his total compensation was roughly ¥675 million, with the large majority of it delivered as variable, performance-linked pay rather than fixed salary — a compensation mix weighted heavily toward stock and performance incentives.18 For a Japanese blue-chip, where executive pay has traditionally been modest and seniority-based, that skew toward equity-linked reward is a meaningful governance signal, not a trivial one.

Accountability, forced by crisis

Perhaps the most revealing governance move came in direct response to the ghost. In June 2024, in the thick of the Horizon firestorm, Fujitsu formalized malus and clawback provisions in its executive compensation framework — mechanisms that allow the company to withhold or recover pay from executives in the event of misconduct or material failures.[^21] The charitable reading is genuine structural accountability; the cynical reading is a company bolting the stable door under intense public scrutiny. Both are true at once. What matters for investors is that the mechanism now exists, and that its introduction was, transparently, a crisis-driven reform rather than a proactive one.

Taken together, the capital-allocation record and the incentive structure suggest a management team that is behaving like custodians of a re-rating rather than empire-builders — so far. The word "so far" is doing real work in that sentence, and it should. Which is exactly the mindset to carry into the lessons this whole saga teaches.

IX. Playbook: Business & Investing Lessons

Step back from the ticker and the segment tables, and the Fujitsu story crystallizes into three transferable lessons — the kind that outlive any single quarter.

Lesson 1: The courage of sunsetting. Clayton Christensen's innovator's dilemma describes why great incumbents fail — they cannot bring themselves to kill the profitable, beloved product that made them, so an insurgent does it for them. Fujitsu's decision to announce a hard end date for its own mainframes is a rare, deliberate refusal to fall into that trap.10 It is genuinely counterintuitive: the discipline was not in defending the cash cow but in scheduling its funeral, and using the funeral to sell the migration. The lesson for investors is to prize management teams willing to cannibalize their own heritage before the market does it for them — while remembering that announcing a sunset and surviving the migration are two very different achievements.

Lesson 2: The danger of legacy liabilities in cross-border M&A. The 1998 ICL acquisition was supposed to be Fujitsu's passport to global scale. What it actually imported was a hyper-specialized public-sector software contract that lay dormant for a quarter-century before detonating into a reputational black swan.15 The uncomfortable truth is that no ordinary due-diligence process in 1998 would have priced a scandal that erupted in 2024. Deep, embedded, mission-critical software contracts carry long-tail liabilities that can outlive the executives who signed them — a warning that applies to every acquirer buying its way into a regulated foreign market.

Lesson 3: The real enterprise value of generative AI. The consumer world obsesses over chatbots. Fujitsu's story points at something less glamorous and possibly more valuable: AI as an internal productivity lever, aimed at the grinding, expensive, unglamorous work of documenting undocumented COBOL, translating dead code into living languages, and automating software delivery.2 If the great AI payoff in enterprise IT turns out to be a few points of gross margin extracted from automating legacy migration — rather than a flashy new product — then Fujitsu's margin expansion is a preview of where the actual money is. That thesis is still being proven, but it is a more grounded bet than most AI narratives.

These lessons frame the investment, but they do not settle it. For that, we have to put the bull and the bear in a room together.

X. The Skeptical Investor Stress Test: Bull vs. Bear

Every good story deserves an adversary, so let's war-game the two Fujitsus that could exist five years from now — and be honest that both are plausible.

The bear case

Start with the ghost, because it is the cleanest tail risk. A large legal settlement or a multi-hundred-million-pound contribution to the UK redress fund could take a real bite out of free cash flow, and because the number is hostage to a public inquiry Fujitsu does not control, it cannot be cleanly modeled or hedged.[^17]16 Uncertainty of that kind is precisely what markets dislike most.

The second bear argument is subtler and, for the long term, arguably more dangerous: labor. Fujitsu's entire margin story rests on a large, skilled, domestic engineering workforce — and Japan's population is shrinking. There is an acute and worsening shortage of software engineers, and Fujitsu is now competing for that scarce talent against foreign tech giants and domestic rivals alike. Tokita has been publicly explicit that Fujitsu intends to keep raising wages, and has moved to overhaul the company's traditional lifetime-employment and mass graduate-hiring model to compete for skills.2124 Rising wages are good for society and bad for the exact 15.4% margin the bull case depends on. If AI-driven productivity does not outrun wage inflation, the margin expansion stalls.

The third bear argument is execution. Sunsetting mainframes sounds clean on a slide and is terrifying in practice. Migrating a systemically important bank or utility off decades of custom COBOL is among the highest-risk work in enterprise IT. One high-profile, catastrophic migration failure — the domestic equivalent of a Horizon-scale mishap — could shatter the institutional trust that is Fujitsu's single most valuable asset in Japan. The company is, in effect, defusing thousands of bombs it built itself, and it only takes one.

The bull case

Now flip it. The bull sees a company that has done the hard, unglamorous work of amputating low-margin hardware and is now emerging as something rare in Japan: a genuine pure-play IT-services and software business that can plausibly command premium multiples. The margin trajectory is not a promise; it is already showing up in reported numbers, quarter after record quarter.1

The bull's growth engine is Uvance, compounding at roughly 40-to-50% a year and dragging Fujitsu's revenue mix away from one-off projects toward scalable, higher-margin, recurring solutions.12 If Uvance keeps that pace and marches toward the ¥1 trillion mark, Fujitsu stops looking like a legacy integrator and starts looking like a platform. And beneath it all sits a fortress balance sheet, freshly recapitalized by the Shinko and Fujitsu General exits, funding a sustained program of buybacks and dividend growth that returns cash to owners while the transformation compounds.2

Porter, Helmer, and the verdict that isn't one

Run the whole thing through Porter's five forces and the tension is clear. Rivalry is intense but oligopolistic and civilized — the walled city rewards incumbents. Buyer power is high for new greenfield deals but astonishingly low for locked-in legacy customers facing a migration. Barriers to entry into Fujitsu's core — the intimate, decades-deep knowledge of Japanese institutions' systems — are close to insurmountable, which is why no foreign giant has stormed the fortress. But the threat of substitutes is real and rising: hyperscale cloud platforms and nimble cloud-native consultancies can peel off the modern, greenfield work that represents the future, leaving Fujitsu defending a shrinking-if-lucrative legacy base.

The synthesis, threading Helmer's framework through it, is that Fujitsu's advantage is genuine but asymmetric: enormous switching-cost and scale power at home, weak counter-positioning and brand power abroad, and one radioactive brand liability in the UK. This is a company with a deep, defensible moat around a market it may struggle to grow beyond. Whether that is a great investment or merely a stable one depends entirely on execution against a small number of things you can actually measure.

The three KPIs that matter

Ignore the noise and watch three numbers. First, the Service Solutions adjusted operating margin — the single cleanest gauge of whether the software-led model is real and whether AI productivity is outrunning wage inflation; management has guided it higher still, so the question is delivery.2 Second, Fujitsu Uvance revenue — the proof of whether Fujitsu can convert bespoke consulting into scalable, repeatable growth, with the trajectory toward ¥1 trillion the milestone to track.1 Third, any Horizon-related provision or charge — the moment a real number finally lands on the balance sheet, the tail risk becomes quantifiable, for better or worse.[^17] Everything else is commentary.

XI. Outro & Epilogue

There is a strange symmetry to the Fujitsu story. It began in 1935 as a company that made the switches routing a nation's telephone calls — physical relays, clicking open and shut, connecting one human to another.3 Nearly a century later, it is trying to become a company that makes software route a nation's data and processes, the switches now invisible, living in the cloud. The medium changed utterly; the underlying business — connecting the critical systems of Japanese institutions — is oddly continuous.

What Fujitsu has accomplished is real and rare. It killed its own computers, phones, chips, and appliances, and rebuilt itself around a services engine now throwing off record profits and mid-teens margins.1 Few incumbents anywhere have had the discipline to demolish their own heritage so deliberately. On the financial transformation, the evidence largely supports management's story — with the honest asterisk that the net-profit fireworks were partly asset-sale gains, and the margin gains still have to survive Japan's wage pressures and the execution gauntlet of the mainframe sunset.

And then there is the ghost. Horizon is the part of this story that no amount of margin expansion can fully wash away — a reminder that software is not a neutral tool, that a bug in an accounting system can end lives, and that a contract signed in 1998 can define a company's reputation in 2026. Fujitsu can become Japan's premium digital-transformation champion and still carry that stain; the two are not mutually exclusive, and pretending otherwise would be the kind of investor-relations gloss this story has tried to avoid.

The open question, then, is not whether Fujitsu has changed — it plainly has — but whether it can compound that change into durable, global relevance while defusing both the legacy bombs it built at home and the reputational one it imported from abroad. The switches are being thrown. Whether they route Fujitsu toward a genuinely new future, or merely a more profitable version of its walled-city past, is the story still being written.

References

-

Consolidated Financial Results for FY2025 (Year Ended March 31, 2026) — Fujitsu Limited, 2026-04-28 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Earnings call transcript: Fujitsu Q4 FY2025 sees profitability gains amid revenue dip — Investing.com, 2026-04-28 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Fujitsu's History / Corporate Chronology — Fujitsu Global ↩↩

-

Fujitsu, Lenovo and DBJ Form PC Joint Venture — Lenovo StoryHub, 2017-11-02 ↩

-

Fujitsu and Polaris Reach Share Transfer Agreement on Mobile Phone Business (FCNT) — Fujitsu Global, 2018-01-31 ↩

-

UMC Receives Final Approval for 100% Acquisition of Mie Fujitsu Semiconductor — Business Wire, 2019-09-25 ↩

-

Fujitsu to End Mainframe and UNIX Server Sales in Major Cloud Pivot — Fujitsu Global Press Release, 2022-02-14 ↩↩↩

-

Japan's JIC Agrees to Buy Fujitsu's Chip Packaging Unit Shinko for ¥800 Billion — Reuters, 2023-12-12 ↩

-

Fujitsu to Sell Shinko Electric to JIC in $4.7 Billion Deal — Bloomberg Law, 2023-12 ↩

-

GK Software Becomes a Fujitsu Company — Fujitsu Global, 2025-05-27 ↩

-

Fujitsu Medium-Term Management Plan Update, FY2025 Results — Fujitsu Limited, 2026-04-28 ↩

-

Fujitsu's Role in the Post Office Scandal: Everything You Need to Know — Computer Weekly ↩↩↩↩↩

-

Post Office Horizon Financial Redress and Compensation Data for 2025 — UK Department for Business and Trade / GOV.UK, 2025-01-30 ↩↩

-

Fujitsu FY2025 Slides: Record Profit Margins Offset Revenue Decline — Investing.com, 2026-04-28 ↩

-

NTT DATA Group Financial Results (FY Ended March 31, 2025) — NTT DATA ↩

-

Why Japan's Conglomerates are Unwinding Cross-Shareholdings and Listed Subsidiaries — Financial Times, 2024-03-12 ↩

-

Fujitsu CEO Vows to Keep Raising Wages, With Annual Graduate Hiring Set to End — The Japan Times, 2026-01-13 ↩

-

Fujitsu IR Reference Library — Consolidated Financial Results & Presentations — Fujitsu Limited ↩

-

UK Post Office Horizon IT Inquiry — Official UK Public Inquiry Portal ↩

-

Interview: Fujitsu CEO Vows to Keep Raising Wages — Nippon.com, 2026-01-11 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube