NEC: The 125-Year-Old Startup

I. Introduction: The "Invisible" Giant

Walk into a police station in Birmingham, England, and the software that pulls up a suspect's criminal history, cross-references it with CCTV footage, and flags a match against a national database runs on code written by a company most Brits have never heard of. Fly through Frankfurt Airport and the face that unlocks your boarding gate is verified by the same company's algorithm. Somewhere in the Pacific Ocean right now, a cable-laying ship is threading fiber optic lines across the seabed, connecting entire continents to the internet, and the prime contractor is, once again, this same company.

That company is NEC Corporation.

For most people outside Japan, NEC is a faded memory: the logo on a bulky CRT monitor from 1997, or a flip phone that a Japanese exchange student once pulled out at a college party. The brand feels like a relic. And that perception gap between what NEC was and what NEC has become is precisely what makes this story worth telling.

Today, NEC is the operating system for the United Kingdom's police force. It processes the social security payments for nearly every citizen of Denmark. Its facial recognition technology has been ranked number one by the U.S. National Institute of Standards and Technology repeatedly since 2009, with a false non-match rate so low it borders on science fiction. It is one of only three companies on Earth capable of building a submarine cable from scratch, end to end. And it was the prime contractor for the spacecraft that flew to an asteroid, scooped up samples, and brought them back to Earth.

None of this happened by accident. What NEC executed over the past decade is one of the rarest and most difficult maneuvers in corporate strategy: the conglomerate pivot. Not a spin-off here and a divestiture there, but a fundamental rewiring of what the company is, what it sells, and how it makes money. NEC went from a hardware-heavy, Japan-centric conglomerate bleeding cash and shedding businesses to a software-driven, globally expanding digital architect with improving margins and a growing base of institutional investors who are paying attention for the first time in decades.

The old NEC rallying cry was "C&C," Computers and Communications, a vision articulated by legendary CEO Koji Kobayashi back in 1977. The new rallying cry is "Social Value Creation," which sounds like corporate jargon until you realize it describes something very specific: NEC wants to be the company that governments trust to run their most sensitive digital infrastructure. Not Amazon Web Services. Not Microsoft Azure. Not Huawei. NEC. The thesis is sovereignty, and in a world fracturing along geopolitical lines, that bet is looking increasingly prescient.

But to understand how a 125-year-old Japanese company pulled this off, you have to go back to the very beginning, to a time when Japan was desperately trying to catch up with the West, and a young engineer who had worked for Thomas Edison came home with a plan.

II. Roots: Western Electric and The Sumitomo Bond

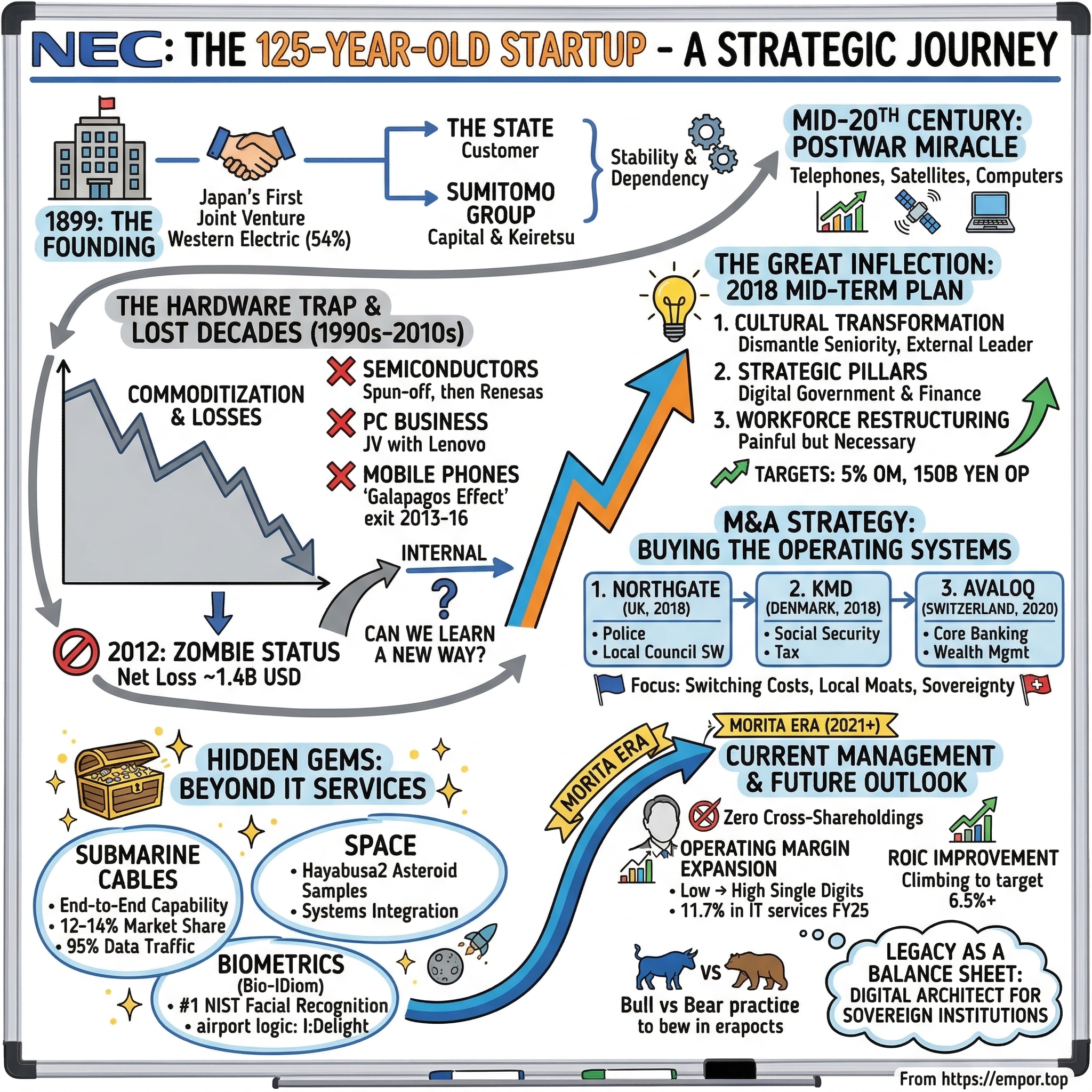

In the summer of 1899, in a modest office in Tokyo's Mita district, a 33-year-old engineer named Kunihiko Iwadare sat across from W.T. Carleton, the head of Western Electric's Tokyo branch. The two men were finalizing the paperwork for what would become Japan's first joint venture with foreign capital. Western Electric, the manufacturing arm of Alexander Graham Bell's AT&T empire, would hold a 54 percent ownership stake. Iwadare, who had spent years in the United States, including a stint working under Thomas Edison himself, would run the operation. The company would be called Nippon Electric Company, Limited.

The founding DNA matters here because it explains everything that followed for the next century. NEC was not born as a scrappy startup tinkering in a garage. It was born as a telecommunications equipment provider, purpose-built to supply the Japanese government's telegraph and telephone networks with switching equipment and transmission gear. From day one, the company's customer was the state.

That relationship crystallized when Japan's telephone system was nationalized and eventually organized under Nippon Telegraph and Telephone, NTT, the "Ma Bell" of Japan. NEC became one of a handful of companies in the "NTT Family," a group of favored suppliers who received preferential contracts in exchange for joint R&D. By the mid-twentieth century, NTT was responsible for more than half of NEC's total revenue. This was a blessing and a curse. The blessing was stability: NEC had a guaranteed customer with deep pockets and a mandate to build out Japan's telecommunications infrastructure. The curse was dependency: NEC's strategic muscles atrophied because the biggest customer always came back.

The other formative relationship was with the Sumitomo Group. In 1919, NEC began its association with one of Japan's oldest keiretsu conglomerates. By 1932, under government pressure during Japan's shift toward economic nationalism, Western Electric's stake was transferred to Sumitomo interests. NEC became a core member of the Sumitomo family, which meant access to patient capital from Sumitomo banks, cross-shareholdings with Sumitomo companies, and a cultural ethos that prioritized long-term survival over short-term profit.

This patience would prove essential. Over the next several decades, NEC rode Japan's postwar economic miracle, building telephone exchanges, microwave relay systems, and eventually satellites and computers. The company survived currency crises, oil shocks, and trade wars that would have killed a Western firm operating quarter to quarter. The Sumitomo safety net meant NEC could invest in R&D at levels that seemed irrational by Western standards, spending through downturns when American competitors were cutting.

But patience can also become complacency. And by the time the twenty-first century arrived, the very relationships that had built NEC, the NTT dependency, the keiretsu cushion, the government contracts, would become the chains that nearly dragged it under. Because the world was about to change, and NEC was not ready.

III. The Hardware Trap and The Lost Decades

Picture the NEC of 1985. The company is the number one semiconductor manufacturer on the planet, a title it would hold for eight consecutive years through the early 1990s. Semiconductor revenue alone hit 2.1 billion dollars in 1985. That same year, the top three chip makers in the world were all Japanese: NEC, Toshiba, and Hitachi. Six of the global top ten were Japanese. American executives in Silicon Valley were genuinely panicked. Congressional hearings were held. Trade restrictions were imposed. Japan Incorporated, as the Western press called it, seemed unstoppable, and NEC was its flagship.

The C&C vision that CEO Koji Kobayashi had articulated in 1977, the convergence of computers and communications, was not just a tagline. It was a prophecy. Under Kobayashi's leadership from 1964 to 1984, NEC's sales grew from 270 million dollars to eight billion dollars, with 35 percent coming from overseas. The company made everything: mainframe computers, personal computers, semiconductors, telecommunications equipment, satellites. It was a vertically integrated technology empire, and for a brief, shining moment, it looked like the future.

Then the world shifted, and NEC's empire began to crack.

The semiconductor business, once the crown jewel, was commoditized by South Korean and Taiwanese competitors who could manufacture DRAM chips at lower cost. NEC responded by merging its chip operations, first spinning off NEC Electronics in 2002, then merging it with Hitachi and Mitsubishi's joint venture to form Renesas Electronics in April 2010. The DRAM business was even more painful. NEC and Hitachi had combined their DRAM operations into a joint venture called Elpida Memory back in 1999. By February 2012, Elpida filed for bankruptcy with liabilities of 448 billion yen, roughly 5.5 billion dollars, making it the largest Japanese bankruptcy since Japan Airlines. Micron Technology eventually acquired the remains for about 2.5 billion dollars. NEC's chip empire, the thing that had made it the envy of Silicon Valley, was gone.

The personal computer business followed a similar trajectory. NEC had dominated the Japanese PC market for decades with its proprietary PC-98 series, but as the industry standardized around the IBM-compatible architecture, NEC's market share eroded. In January 2011, NEC announced a joint venture with Lenovo, with the Chinese company holding 51 percent. NEC received 175 million dollars in Lenovo shares. By July 2016, Lenovo acquired the remaining stake for approximately 195 million dollars. The PC business that had once defined NEC in the minds of Japanese consumers was now a subsidiary of a Chinese company.

And then there were the mobile phones. This is where the "Galapagos Effect" hit hardest. Japanese mobile phones, known as garakei, had evolved in splendid isolation, loaded with features like mobile payments, TV tuners, and high-resolution cameras years before the iPhone existed. But they ran on proprietary platforms tied to Japanese carrier specifications, particularly NTT DoCoMo's i-mode system. When Apple's iPhone and Google's Android platform arrived, the Galapagos phones could not compete globally. NEC exited the smartphone market in July 2013 and stopped developing new models entirely by March 2016. Another business, gone.

The cumulative effect of these losses hit bottom in fiscal year 2012, when NEC posted a net loss of approximately 110 billion yen, about 1.4 billion dollars, driven by deferred tax asset write-downs and restructuring charges. Operating income was a skeletal 7.1 billion yen. The dividend was suspended. The company announced ten thousand job cuts, seven thousand in Japan and three thousand overseas. Interest-bearing debt stood at nearly 693 billion yen with a debt-to-equity ratio above one.

In the investment community, NEC had acquired the most damning label a company can receive: zombie. A company that was not quite dead but was not really alive either, kept breathing by patient banks and cross-shareholdings, shuffling forward without strategic direction. The realization was dawning inside NEC's headquarters in Minato, Tokyo, that "making things" was no longer the path to "winning things." The hardware era was over. The question was whether a company with a 115-year-old culture could learn an entirely new way of doing business.

The answer, improbably, was yes. But it would take a new plan, a new set of leaders, and a willingness to break taboos that most Japanese corporations would never touch.

IV. The Great Inflection: The 2018 Mid-Term Plan

On January 30, 2018, NEC's president and CEO Takashi Niino stood before a room of analysts and journalists in Tokyo and unveiled what he called the "Mid-Term Management Plan 2020." The name was deliberately boring. Japanese corporate plans always have boring names. But the content was anything but.

Niino, who had taken the top job in 2016, had spent two years studying why NEC kept losing ground. His diagnosis was blunt: the company was organized to optimize internally rather than compete externally. Business units operated as fiefdoms. Decision-making was slow. Talent was allocated by seniority, not by skill. And the revenue mix was lethally skewed toward low-margin hardware businesses in a shrinking domestic market. The plan he unveiled was designed to reverse all of this, simultaneously.

The financial targets were ambitious for a company that had been barely profitable: revenue of three trillion yen with an operating profit of 150 billion yen, a five percent operating margin. For context, NEC's operating margin at the time hovered around two to three percent. Niino was asking the company to nearly double its profitability in three years.

But the real revolution was cultural. In April 2018, NEC did something almost unheard of for a major Japanese corporation: it created a "Culture Transformation Division" and hired an external professional to lead it. This was not a consulting engagement or an offsite workshop. This was a permanent organizational unit with a mandate to dismantle the seniority-based systems that had governed NEC for over a century.

The old system worked like this: you joined NEC out of university, you were assigned to a division, and you rose through the ranks based primarily on tenure. Compensation was tied to years of service. Promotions were predictable. Risk-taking was discouraged because failure was punished while mediocrity was tolerated. The system produced stability but not innovation, loyalty but not urgency.

Under the new plan, executive compensation was restructured into three components: a base salary, a short-term performance bonus tied to measurable business outcomes, and a medium-to-long-term stock-based incentive tied to total shareholder return and return on invested capital. For a company where executives had historically been paid modest fixed salaries regardless of performance, this was a cultural earthquake. The message was clear: NEC would reward results, not tenure.

The plan also identified two strategic pillars that would define NEC's future: Digital Government and Digital Finance. These were not randomly chosen. They were selected because they represented markets where NEC had existing relationships and technical capabilities, but where the company had never pursued the global opportunity aggressively. Japanese government IT was a mature business for NEC. European government IT was a greenfield opportunity. Japanese banking software was a known quantity. Global wealth management technology was a different league entirely. The plan was to take what NEC knew how to do domestically and scale it internationally through targeted acquisitions.

The workforce restructuring was painful but necessary. Approximately three thousand positions were eliminated in Japan, primarily in back-office functions and hardware-related roles, expected to improve earnings by about 24 billion yen annually. This was not the blunt-instrument layoffs that American companies execute routinely. In Japan, where lifetime employment had been a social contract, cutting three thousand jobs from a company like NEC was a signal that the old rules no longer applied.

What made the 2018 plan different from the dozens of previous NEC "restructuring plans" that had come and gone was its specificity. It did not just say "we will grow internationally." It named the markets. It did not just say "we will improve profitability." It set margin targets by segment. And most importantly, it backed the words with actions, because within months of the announcement, NEC went shopping.

V. M&A Strategy: Buying the Operating Systems

The first phone call went to Cinven, the London-based private equity firm. The target was Northgate Public Services, a British software company that most people have never heard of but that quietly runs some of the most critical digital infrastructure in the United Kingdom. When a police officer in England or Wales pulls up a suspect's criminal record, the software is Northgate's. When a local council processes housing benefit applications, the backend is Northgate's. When a court issues a warrant, the workflow management system is Northgate's. The company was not glamorous, but it was deeply, structurally embedded in the British public sector.

NEC acquired Northgate in January 2018 for 475 million pounds, approximately 670 million dollars. The implied valuation was roughly twelve times EBITDA, a price that looked rich for a UK public sector software company but made strategic sense when viewed through the lens of switching costs. Governments do not change their criminal records management system on a whim. The implementation cycles are measured in years, the data migration challenges are enormous, and the political risk of a failed transition is career-ending for the civil servants involved. Once Northgate was in, it was in for decades. NEC was not buying software. It was buying a franchise, and it rebranded the business as NEC Software Solutions to signal that this was the template for the company's future.

The second acquisition came in December 2018, and it was even more audacious. KMD, Denmark's largest IT company, was acquired from Advent International and Sampension for eight billion Danish kroner, approximately 1.2 billion dollars. KMD was to Denmark what Northgate was to the UK, but broader. The company processed social security payments, tax filings, municipal administration, and healthcare records for Danish citizens. In one of the world's most digitized societies, where virtually every interaction between citizen and state runs through software, KMD was the plumbing.

The strategic logic was identical to Northgate but amplified. Denmark was not just a customer. It was a proof of concept. If NEC could demonstrate that it could operate the digital backbone of one of the most advanced welfare states on Earth, it could credibly bid for similar contracts across Scandinavia, the Benelux countries, and eventually across the European Union. KMD was a beachhead.

The third and largest acquisition landed in October 2020, when NEC announced the purchase of Avaloq from Warburg Pincus and other shareholders for 2.05 billion Swiss francs, approximately 2.2 billion dollars. If Northgate and KMD were about Digital Government, Avaloq was about Digital Finance. The Swiss company provided core banking software to more than 150 wealth management firms and private banks across over thirty countries. Its platform handled transaction processing, portfolio management, and regulatory reporting for institutions that managed trillions of dollars in assets.

The price was steep, roughly seventeen times EBITDA, a significant premium over what NEC had paid for Northgate. But the logic held. Avaloq's customers were private banks and wealth managers, institutions that are pathologically resistant to changing their core technology platforms. A migration from Avaloq to a competitor would take two to three years, cost tens of millions of dollars, and carry execution risk that no risk committee would voluntarily approve. The switching costs were not just high. They were prohibitive.

Across these three acquisitions, NEC deployed approximately four billion dollars in roughly two years. By the standards of Japanese corporate M&A, this was breathtaking. Japanese companies have a well-documented history of overpaying for foreign assets, often driven by empire-building rather than strategic logic. The 1990s were littered with cautionary tales. But NEC's acquisitions were different in important ways. First, the multiples were reasonable by the standards of global software M&A. American acquirers were routinely paying twenty to thirty times EBITDA for SaaS companies during this period. NEC's prices looked downright disciplined by comparison. Second, each acquisition was targeted at a specific strategic thesis: switching costs and local moats. These were not businesses that NEC could have built from Tokyo. The relationships, the regulatory knowledge, the institutional trust, all of it had to be bought.

The critical question for investors was whether NEC could actually integrate these businesses. Japanese companies acquiring European software firms is a notoriously treacherous combination, with cultural mismatches, management departures, and value destruction being the historical norm. NEC's approach was to let the acquired companies operate with significant autonomy, keeping local management in place while gradually integrating sales channels and cross-selling opportunities. It was a patient strategy, and it was working. By 2025, the European businesses were contributing meaningfully to both revenue and, more importantly, to the margin expansion that NEC had promised investors.

The acquisitions revealed something else about NEC's evolving strategy. The company was not trying to compete with the hyperscalers, with AWS or Azure or Google Cloud. Instead, NEC was positioning itself as the alternative for customers who, for reasons of sovereignty, regulation, or geopolitics, could not or would not entrust their most sensitive data to an American or Chinese technology platform. This was not a niche. It was a growing market, and NEC had just bought its way to the front of the line.

VI. Hidden Gems: Submarine Cables, Space, and Biometrics

Fourteen thousand meters below the surface of the Pacific Ocean, in the hadal zone where sunlight has never reached and the pressure would crush a human body like an aluminum can, a fiber optic cable sits on the ocean floor. It carries terabits of data per second between continents, handling everything from financial transactions to streaming video to military communications. That cable was manufactured, transported, and laid by one of only three companies on the planet with the end-to-end capability to do so: SubCom, an American firm; Alcatel Submarine Networks, which the French government acquired from Nokia in January 2025 for 375 million dollars to ensure it remained under sovereign control; and NEC.

The submarine cable business is one of those industries that sounds obscure until you realize it underpins virtually all of modern civilization. More than 95 percent of intercontinental data traffic travels through undersea cables. The market is estimated at roughly 32 billion dollars and projected to grow to 44 billion by 2030, driven by the insatiable demand for data capacity and the construction of new routes to connect emerging markets and data centers. NEC commands roughly 12 to 14 percent of global market share, with particular strength in transpacific routes connecting Asia to the Americas.

What makes this business strategically important is the barrier to entry. Building submarine cables requires specialized ships, proprietary manufacturing facilities for the cables and repeaters, deep expertise in ocean surveying and route planning, and the ability to manage projects that span thousands of kilometers and multiple years. A new competitor cannot simply decide to enter this market. The capital requirements are enormous, the technical knowledge is accumulated over decades, and the customer relationships with governments and telecommunications carriers are deeply entrenched. Chinese competitors HMN Tech, formerly Huawei Marine Networks, and Hengtong are growing but face restrictions from Western governments concerned about security. NEC, as a Japanese company allied with the West but not American, occupies a uniquely advantageous position.

Then there is space. On December 6, 2020, a capsule the size of a kitchen pot parachuted into the Australian outback, carrying samples from an asteroid named Ryugu that orbits the sun roughly 300 million kilometers from Earth. The spacecraft that collected those samples, Hayabusa2, was built by NEC as the prime contractor. NEC designed and manufactured the spacecraft bus, the structural and electrical backbone of the entire vehicle, along with the communications system and the mid-infrared camera. The ion engines that propelled Hayabusa2 across the solar system, four xenon thrusters generating a combined thrust roughly equivalent to the weight of a one-yen coin, were also coordinated by NEC.

The space business does not move the needle on NEC's income statement in isolation. But it serves a purpose that transcends quarterly earnings. It is a demonstration of systems integration capability at the highest possible level of complexity. When NEC tells a government customer that it can manage a multi-year, multi-billion-dollar digital infrastructure project, the unspoken credential is: we built the spacecraft that went to an asteroid and came back. That is a calling card that no PowerPoint presentation can match.

But the true crown jewel of NEC's technology portfolio is its biometrics business, and specifically its facial recognition technology. NEC has ranked number one in the National Institute of Standards and Technology's Face Recognition Vendor Test multiple times since 2009, most recently in April 2025 with a false non-match rate of 0.07 percent when searching a database of twelve million faces. To put that in perspective, the system correctly identifies the right person 99.93 percent of the time, a level of accuracy that exceeds what most humans can achieve when comparing photographs.

The platform is called Bio-IDiom, and it goes beyond faces. It combines facial recognition with iris scanning and fingerprint identification in a multimodal biometric suite. When face and iris recognition are used together, the false positive rate drops to less than one in ten billion, a number so small it approaches the theoretical limits of biometric authentication.

The commercial applications are already deployed at scale. Star Alliance, the world's largest airline alliance, launched NEC's I:Delight facial recognition platform at Frankfurt and Munich airports in December 2020, with Lufthansa and SWISS as the first adopters. The system allows passengers to move through check-in, security, and boarding using only their face, no passport, no boarding pass, no physical interaction. The plan is to extend the system to all 26 Star Alliance member airlines, and it is already deployed at approximately 80 airports worldwide.

The segment economics tell the story of NEC's transformation. The company's IT Services segment, which includes the European acquisitions and the domestic enterprise business, generated revenue of roughly two trillion yen in fiscal year 2025 with an adjusted operating profit margin of 11.7 percent, up about two percentage points year over year. The Social Infrastructure segment, which houses the submarine cable and space businesses along with domestic public sector work, posted adjusted operating profit of 60.5 billion yen, nearly double the prior year's 32.9 billion. The overall company reached adjusted operating profit of 287.2 billion yen, meaningfully ahead of the 300 billion yen target that was supposed to be hit in fiscal year 2026.

The operating margin expansion from the low single digits to the high single digits and beyond is the single most important financial trend at NEC. It reflects the shift from hardware, where margins were thin and competition was brutal, to software and services, where switching costs protect pricing power and recurring revenue creates predictability. For a company that was posting losses just over a decade ago, reaching nearly 300 billion yen in operating profit represents a transformation that few analysts would have predicted.

VII. Current Management: The Morita Era

Takayuki Morita became president and CEO of NEC on April 1, 2021, and his biography reads like a deliberate counterpoint to every stereotype about Japanese corporate leadership. Born in the early 1960s, Morita graduated with a law degree from the University of Tokyo, Japan's most prestigious university, and joined NEC in 1983. But unlike most of his contemporaries who spent their entire careers within a single business unit, rising slowly through the ranks of a domestic division, Morita spent six years in the United States and built his career in corporate strategy and M&A.

This matters because of what it signals about NEC's intent. Previous NEC presidents were typically engineers or sales executives who had risen through the telecom equipment or computing divisions. They understood the technology and the domestic customer relationships, but they were not deal-makers and they were not globalists. Morita was both. Before becoming CEO, he served as Chief Global Officer from 2016, where he oversaw NEC's international expansion strategy, and then as CFO from June 2018 to April 2021, the precise period when the three European acquisitions were executed. Morita did not inherit the M&A strategy. He architected it.

His track record includes involvement in more than forty M&A transactions over his career, ranging from the semiconductor and flat panel display spin-offs that cleaned up the old NEC to the Lenovo joint venture that exited the PC business to the Northgate, KMD, and Avaloq acquisitions that defined the new NEC. This is a CEO who views capital allocation as his primary tool for value creation, a mindset that is common in American boardrooms but rare in Japanese ones.

Under Morita, NEC's approach to shareholder engagement has shifted dramatically. The company adopted a "zero cross-shareholdings" policy, unwinding the web of reciprocal equity stakes with other Sumitomo Group companies that had historically insulated NEC from market discipline. Cross-shareholdings are a defining feature of the Japanese keiretsu system, and dismantling them is a statement that NEC intends to be judged by its financial performance, not protected by its corporate relationships.

The investor base has responded. International institutional investors now hold approximately 30 percent of NEC's share registry, up from much lower levels a decade ago. Morita has actively courted this constituency, conducting regular roadshows in New York, London, and Singapore, and making the case that NEC deserves to be evaluated as a global software and services company, not as a Japanese hardware conglomerate trading at a "Japan Discount."

The "NEC 2025" mid-term management plan, announced in May 2021, set fiscal year 2026 targets of 3.5 trillion yen in revenue, 300 billion yen in adjusted operating profit representing an 8.6 percent margin, and a return on invested capital of 6.5 percent. The company effectively hit the profit target a year early, posting 287 billion yen in adjusted operating profit and 311 billion yen on a non-GAAP basis in fiscal year 2025. ROIC reached approximately 6.6 percent, up from below five percent just five years earlier.

Morita conducts monthly virtual town halls that reach over ten thousand employees, an unusual practice for a Japanese CEO and a deliberate effort to communicate directly with the workforce rather than through the traditional cascade of division heads and department managers. He frames the transformation not as cost-cutting but as repositioning, arguing that NEC's future lies in being indispensable to governments and financial institutions, not in manufacturing commoditized hardware.

The executive compensation structure that was introduced under the 2018 plan has been refined under Morita. Short-term bonuses are explicitly linked to annual performance targets from the mid-term plan. Medium-to-long-term incentives are tied to total shareholder return and ROIC, metrics that align management interests with those of outside shareholders. For a company that historically paid its executives modest fixed salaries with minimal performance linkage, the transformation in incentive design is as significant as the transformation in business mix.

The question that sophisticated investors ask about Morita is whether one leader can truly change the culture of a 125-year-old organization with over a hundred thousand employees. The evidence so far suggests that the answer is conditional: Morita can change the incentives, the organizational structure, and the capital allocation priorities. Whether the cultural change reaches the middle management layers, where most of the day-to-day decisions are made, remains the open question. Japanese corporate culture is famously resistant to top-down mandates, and the true test of the Morita era will be whether the transformation survives his eventual departure.

VIII. The Playbook: 7 Powers and 5 Forces

To understand NEC's competitive position, it helps to step back from the financials and apply two of the most powerful frameworks in business strategy: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. These frameworks reveal not just what NEC is doing, but whether what it is doing is defensible.

Start with switching costs, which Helmer identifies as one of the most durable sources of competitive advantage. NEC's entire acquisition strategy was designed to buy switching costs. When the Danish government runs its social security system on KMD's platform, the cost of switching to a competitor is not just financial, it is existential. The data migration would take years. The risk of errors in benefit payments affecting millions of citizens is politically unacceptable. The institutional knowledge embedded in KMD's customization of the platform for Danish regulations cannot be replicated by a foreign competitor unfamiliar with the specifics of Danish welfare law. The same logic applies to Northgate in UK policing and Avaloq in private banking. These are not products that customers evaluate annually. They are infrastructure that becomes load-bearing over time, and the longer a customer uses them, the harder it becomes to leave.

The second power NEC possesses is what Helmer calls a cornered resource: a proprietary asset that competitors cannot replicate. NEC's Bio-IDiom biometric platform, and specifically its facial recognition algorithms, qualifies. The algorithms were developed over decades of research at NEC's Central Research Laboratories, trained on proprietary datasets, and refined through real-world deployment at scale. The NIST number-one ranking is not just a marketing badge. It reflects a measurable, tested superiority in accuracy that competing algorithms have not matched. Biometric algorithms are not commodities. The differences in accuracy between the top-ranked and tenth-ranked systems are operationally meaningful, especially in high-security applications where false positive rates must be extraordinarily low. NEC's lead in this area is a genuine cornered resource.

The third power is scale economies in the submarine cable business. The fixed costs of maintaining a fleet of cable-laying ships, operating specialized manufacturing facilities, and employing the ocean engineering expertise required to plan and execute submarine cable projects are enormous. These costs are spread across a limited number of projects each year, creating a natural oligopoly. A new entrant would need to invest billions of dollars before laying a single kilometer of cable, and even then would lack the track record that governments and carriers require before entrusting a billion-dollar infrastructure project to an unproven supplier. NEC's position as one of three global players gives it pricing power and project flow that smaller competitors cannot match.

Now apply Porter's Five Forces to NEC's primary markets. The threat of new entrants is low in Digital Government and submarine cables, moderate in biometrics where Chinese companies are investing heavily, and high in generic enterprise IT. The bargaining power of buyers is significant in Japan, where NTT remains a dominant customer, but lower in European government contracts where switching costs create lock-in. The bargaining power of suppliers is generally low, as NEC has diversified its technology stack and does not depend on any single vendor for critical components. The threat of substitutes is the most interesting force to analyze.

The substitute that keeps NEC's strategists awake at night is the hyperscalers: Amazon Web Services, Microsoft Azure, and Google Cloud. These companies have the technical capabilities, the financial resources, and the sales organizations to compete for government IT contracts anywhere in the world. And in many cases, they are winning. But NEC has identified a structural barrier that limits the hyperscalers' reach: sovereignty.

Governments increasingly do not want their most sensitive data, tax records, criminal justice information, social security files, biometric databases, sitting on servers controlled by an American corporation subject to American laws. The CLOUD Act, passed by the U.S. Congress in 2018, gives American law enforcement the ability to compel U.S. technology companies to produce data stored overseas. For a European government evaluating whether to put its citizens' tax records on AWS, this is not an abstract legal concern. It is a fundamental question of national sovereignty.

NEC's positioning as a "Sovereign Cloud" partner addresses this concern directly. As a Japanese company, NEC is not subject to American data access laws. As a company with no ties to the Chinese government, it does not trigger the security concerns that have led Western nations to ban Huawei and restrict other Chinese technology firms. NEC occupies a geopolitical sweet spot: allied with the West but not American, trusted by democracies but not beholden to any single power. In a world where digital sovereignty is becoming a strategic priority for governments from Brussels to Canberra, this positioning is enormously valuable.

The competitive rivalry in NEC's core markets is moderate. In Digital Government, the primary competitors are Accenture, Capgemini, and local champions in each market. In Digital Finance, the competitors include Temenos, FIS, and Finastra. In biometrics, the competitors include Idemia, Thales, and increasingly Chinese firms like SenseTime and Megvii. In submarine cables, the competition is limited to SubCom and ASN. None of these markets are winner-take-all. They are fragmented, relationship-driven, and characterized by long sales cycles and high barriers to switching. This is the kind of competitive environment where patient, long-term players with strong local relationships thrive, and NEC has been playing this game for 125 years.

IX. Bear vs. Bull Case

The bear case against NEC is rooted in a fundamental question: can a 125-year-old Japanese company, with over a hundred thousand employees and a culture forged in the seniority-based traditions of the keiretsu system, truly move at the speed required to compete in global software markets?

The skeptics point to the NTT dependency. While NEC has diversified its revenue base significantly, NTT remains a major customer, and the relationship carries risk in both directions. NTT invested 596 million dollars for a 4.8 percent stake in NEC in June 2020, deepening the financial ties between the two companies. On one hand, this signals commitment and provides NEC with a stable anchor customer. On the other hand, it raises questions about whether NEC can truly operate as an independent, globally competitive company when its largest domestic customer is also a significant shareholder with its own strategic agenda.

There is also the integration risk. NEC has spent four billion dollars acquiring three European software companies in rapid succession. The history of Japanese companies acquiring Western businesses is littered with failures: Nomura's acquisition of Lehman Brothers' European operations, NTT's acquisition of Dimension Data, Toshiba's acquisition of Westinghouse Nuclear. In each case, cultural mismatches, management departures, and strategic confusion destroyed value. NEC's approach of granting autonomy to acquired companies mitigates some of this risk, but it also limits the potential for synergies and creates governance challenges. Managing a Danish software company from Tokyo is not easy, regardless of how enlightened the head office may be.

The margin expansion story, while impressive, also faces headwinds. NEC's operating margins, while improving, remain below those of pure-play software companies. Achieving consistent double-digit operating margins will require continued portfolio optimization, which may mean additional divestitures of lower-margin hardware businesses. Each divestiture carries execution risk and may face internal resistance from employees and managers who have built their careers in the divested units.

And then there is the technology risk. NEC made a significant bet on Open RAN, the initiative to disaggregate the hardware and software components of 5G cellular networks, allowing operators to mix and match equipment from different vendors rather than relying on integrated systems from Ericsson, Nokia, or Huawei. NEC was initially ranked as the number two Open RAN vendor globally, invested heavily in partnerships with Rakuten Mobile, NTT DoCoMo, Vodafone, and Telefonica, and established a Center of Excellence in the UK. But in late 2024 and into 2025, NEC effectively retreated from the 4G/5G base station hardware market, classifying it as non-core. Its global market share in base stations remained below one percent despite the investment. This was a humbling reminder that ambition and capability do not always translate into market share, and that competing against entrenched incumbents in a capital-intensive hardware market remains enormously difficult even for a company of NEC's resources.

The bull case is built on three pillars.

First, NEC owns the plumbing of the digital state in Europe and Japan, and that plumbing is getting more valuable, not less. The global trend toward digital government is accelerating, driven by citizen expectations for online services, the need for efficiency in aging societies with shrinking workforces, and the lessons of the COVID-19 pandemic, which exposed the fragility of paper-based and legacy government systems. Japan's Digital Agency, established in September 2021 specifically to modernize the country's fragmented government IT infrastructure across roughly 1,700 municipalities running incompatible systems, represents a multi-decade domestic tailwind for NEC as one of the primary incumbent IT providers to the Japanese public sector.

Second, the sovereignty thesis is gaining momentum. The geopolitical fracturing of the technology landscape, with the United States, China, and Europe increasingly pursuing independent digital infrastructure strategies, creates a structural demand for technology providers that are trusted but not aligned with any single superpower. NEC's Japanese identity is an asset in this context, not a liability. The French government's decision to acquire Alcatel Submarine Networks from Nokia to keep it under sovereign control demonstrates that this is not a theoretical concern but a policy priority for major democracies. NEC is positioned to be the "Sovereignty as a Service" provider for governments that want digital infrastructure without strategic dependency.

Third, the biometrics business has the potential to become a platform in its own right. As border security, airport automation, and digital identity verification become standard requirements for governments worldwide, NEC's number-one-ranked technology gives it a competitive advantage that is difficult to replicate. The addressable market for biometric identity solutions is growing rapidly, and NEC's combination of proven accuracy, real-world deployment at scale, and a reputation for reliability makes it a natural partner for governments and regulated industries.

For investors tracking NEC's ongoing transformation, two key performance indicators deserve close attention above all others. The first is operating profit margin, particularly in the IT Services segment, which captures the impact of the European acquisitions and the shift from hardware to software. Margin expansion in this segment is the clearest signal that the transformation is delivering sustainable value, not just revenue growth. The second is ROIC, return on invested capital, which management has explicitly adopted as a core performance metric and which captures both the profitability of the business and the discipline of capital allocation. ROIC improvement from below five percent to the mid-single digits has been meaningful, but the trajectory matters more than the absolute level. If ROIC continues to climb toward and beyond management's targets, it will validate the thesis that NEC's acquisitions are generating returns above their cost of capital.

X. Epilogue and Final Reflections

In 2024, NEC celebrated its 125th anniversary. Most companies that reach this milestone do so by looking backward, publishing glossy commemorative books filled with sepia-toned photographs and nostalgic essays about the founder's vision. NEC used the occasion to look forward, framing the anniversary not as a celebration of heritage but as a starting point for the next phase of transformation.

The lesson of NEC's story is deceptively simple: legacy is not a death sentence. It is a balance sheet. The same institutional relationships that created NEC's NTT dependency also gave it the patient capital to survive crises that would have killed a leveraged Western company. The same keiretsu structure that slowed decision-making also provided the cross-functional integration capabilities that NEC now deploys on submarine cable projects and spacecraft missions. The same Japanese corporate culture that resisted performance-based incentives also produced the engineering discipline and attention to quality that earned NEC the number-one ranking in biometric accuracy.

The old label was "the IBM of Japan," and like IBM, NEC spent years struggling with the transition from hardware to services. But where the comparison breaks down is in the endgame. IBM became a consulting and hybrid cloud company, essentially following its existing enterprise customers up the stack. NEC became something different: a digital architect for sovereign institutions, a company that builds the physical cables that connect continents, the biometric systems that verify identities at borders, and the software platforms that process tax returns and social security payments for entire nations.

Whether NEC can sustain this transformation through the next business cycle, the next CEO transition, and the next wave of technological disruption is an open question. The cultural change is real but incomplete. The margin expansion is impressive but not yet at levels that command premium valuations. The sovereignty thesis is compelling but untested at scale outside of a few European markets.

What is not in question is that NEC has executed one of the most dramatic corporate pivots of the twenty-first century, transforming itself from a company that the market had written off as a zombie into one that sits at the intersection of some of the most powerful secular trends in global technology: digital government, data sovereignty, biometric identity, and undersea connectivity. For a company founded in 1899 to supply telephone equipment to the Japanese government, the journey from Kunihiko Iwadare's modest office in Mita to the ocean floor of the Pacific and the surface of an asteroid is a story that deserves to be told.

And it is a story that is still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube