Daikin Industries: The Invisible Giant of Global Climate Control

I. Introduction & Episode Roadmap

Consider the scale first, because it is genuinely difficult to hold in the mind. In the fiscal year ended March 2026, Daikin's consolidated net sales crossed ¥5 trillion for the first time in its history, reaching ¥5,015 billion — roughly $33 billion — an increase of about 6% over the prior year, with operating profit of about ¥415 billion and net income of ¥275 billion.[^2] The company operates in more than 170 countries, and by most industry estimates commands somewhere in the mid-teens of global HVAC market share — a fragmented industry in which "mid-teens" makes you the undisputed leader.2 It has done this while eclipsing the iconic American names that effectively invented the category: Carrier, whose founder Willis Carrier built the first modern air conditioner in 1902, and Trane, the century-old Wisconsin institution. The pupil has quietly outgrown the masters. Listed on the Tokyo Stock Exchange under the code 6367, Daikin is one of the largest components of Japan's blue-chip indices, yet it carries none of the household recognition of a Sony or a Toyota — a testament to how thoroughly a company can dominate an essential global industry while remaining invisible to the people it serves.[^9]

But market share is the least interesting number in this story. The interesting number is a structural one that no competitor can replicate. Daikin is the only global HVAC company that is vertically integrated from organic chemistry all the way to mechanical engineering. Carrier, Trane, Lennox, and the Chinese giants 美的 Midea and 格力 Gree all buy their refrigerant — the working fluid that actually does the cooling — from chemical companies like Honeywell, Chemours, or Arkema. Daikin synthesizes its own. It runs a specialty-chemicals division that makes fluorocarbons and fluoropolymers for semiconductors, EV batteries, and aerospace, and it uses that chemistry to design the mechanical guts of its machines around the thermodynamics of the fluids flowing inside them. It does not just build the box. It formulates the blood that runs through it.

That dual-engine structure — chemicals and hardware, developed together over ninety years — is the spine of everything that follows. This article walks through six acts. First, the chemical-hardware origin in pre-war Osaka, where the two competencies were forged in the same fire. Second, the 1982 invention of Variable Refrigerant Volume, the product that created an entire commercial category and, with a single trademark, permanently branded every competitor as an imitator. Third, the great North American acquisition offensive under Noriyuki Inoue — the OYL/McQuay deal of 2006 and the audacious $3.7 billion bet on Goodman in 2012. Fourth, the counterintuitive decision to give away a patent portfolio for free, which turned Daikin's R-32 refrigerant into a global standard. Fifth, the 2024 generational handover and the newly minted FUSION 30 strategic plan, which asks whether a hardware company can reinvent itself as a seller of "solutions." And finally, the bull-and-bear stress test: the PFAS "forever chemicals" liability that hangs over the chemicals crown jewel, the Chinese property slump, the European heat-pump hangover, and the American "inverterization" wave that could be Daikin's single largest growth opportunity of the decade.

It helps to understand why HVAC is such an underrated business to dominate. Air conditioning is not a fashion product with fickle demand or a technology product with winner-take-all dynamics. It is a slow, physical, recurring, globally essential industry — closer to cement or elevators than to smartphones. Growth is steady rather than explosive, tied to construction cycles, temperature, urbanization, and rising incomes in the developing world. The barriers to a credible global player are enormous: you need decades of installed base, a trained service network, brand trust with contractors, regulatory approvals in every jurisdiction, and the capital to run factories on multiple continents. That combination makes the industry structurally consolidated at the top and forbidding to new entrants — which is exactly the kind of terrain in which a patient, well-run incumbent can compound for a very long time. Daikin is the incumbent that compounded best.

The competitive field, however, is not sleepy. On one flank sit the Western applied-systems giants — Carrier, now an independent company after spinning out of United Technologies, and Trane Technologies, both formidable in large commercial and institutional cooling. On another sit the Japanese and Korean electronics-adjacent players, Mitsubishi Electric, LG, and Samsung. And on the most dangerous flank sit the Chinese volume champions, 美的 Midea and 格力 Gree, whose vast domestic scale and aggressive pricing make them the low-cost disruptors of the industry. Daikin sits above all of them by revenue, but "above" in a fragmented industry is a lead measured in a few points of share, not a monopoly — a distinction that matters enormously to the investment case.

The throughline is a question worth keeping in mind: is Daikin's dominance the product of a genuinely durable moat, or of a long run of good execution in a cyclical, capital-intensive business now facing its most crowded competitive field ever? The answer, as usual, is some of both — and the work is in figuring out how much of each.

II. Osaka Origins: Radiators, Chemicals, and the Dual-Engine DNA (1924–1970s)

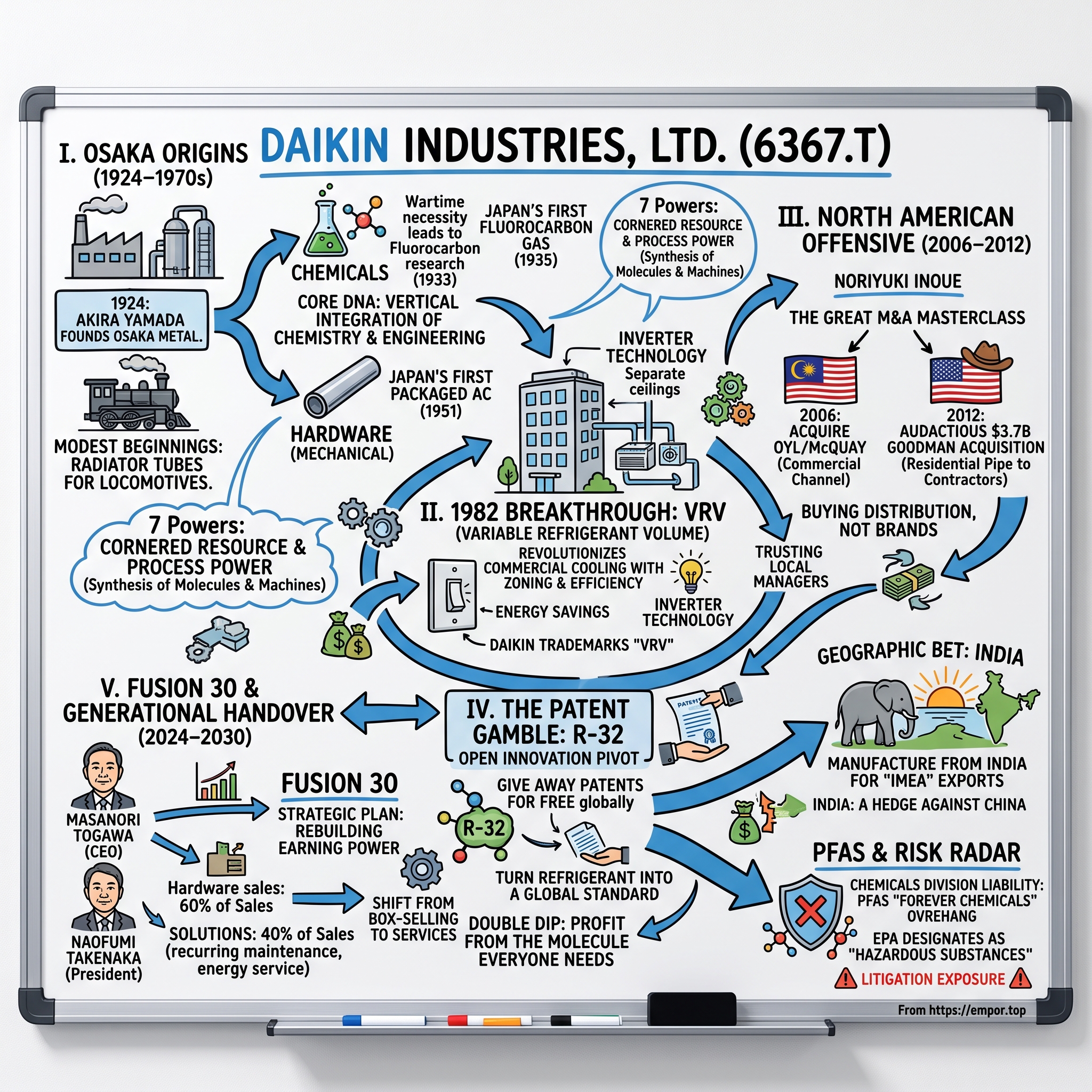

In 1924, in an Osaka still rebuilding its industrial base, a metalworker named 山田晁 Akira Yamada founded a small workshop called Osaka Kinzoku Kogyosho — Osaka Metal Industries.7 Its first product line was almost comically distant from climate control: radiator tubes for the steam locomotives that were then stitching Japan together. It was a machine shop that made metal tubes hot. The pivot to making air cold would take decades, and it would come through a detour into chemistry that no ordinary radiator manufacturer would ever have taken.

Picture the setting. Osaka in the 1920s was the "Manchester of the East," the smoky industrial heart of a Japan racing to catch the West, its canals crowded with barges and its skyline thickening with factory chimneys. Into that ferment stepped Akira Yamada, a metalworker with no particular reason to believe his radiator-tube shop would outlast the decade, let alone the century. The company that became a $30-billion global champion began, like most great industrial firms, as a modest bet by a practical man solving a mundane problem — how to make better metal tubes for the machines of his moment. What separated it from the thousands of similar workshops that vanished was a single willingness, a few years later, to walk through a door that had nothing to do with metalworking.

That detour was driven by the least romantic of catalysts: military demand. In the 1930s, Japan's armed forces needed refrigeration — for provisions, for submarines, for the machinery of a mobilizing empire — and they needed the fluorocarbon refrigerants that made modern cooling possible. These chemicals were largely controlled by American firms, and a militarizing Japan wanted its own supply. Yamada's firm took up the challenge. It began fluorocarbon research in 1933, and in 1935 it succeeded in manufacturing fluorocarbon gas for the first time in Japan.8 In 1938, it delivered the "Mifujirator," Japan's first fluorocarbon-based refrigeration unit, to the Kure Naval Arsenal for use aboard submarines.8 Long before Daikin ever sold a comfort cooling product to a consumer, it had learned to make the molecules that cooling depends on.

This is the origin of the "dual engine," and it is worth dwelling on why it mattered so much, because it is the single most path-dependent fact in the company's history. Everywhere else in the world, air-conditioning developed as a mechanical industry — pumps, coils, compressors — that purchased its refrigerant as a commodity input from the chemical industry. In Japan, at this one firm, the two disciplines grew up in the same building, taught by the same wartime necessity. The mechanical engineers and the chemists ate in the same canteen. When the war ended and Japan's military-industrial complex was dismantled, most of Yamada's contemporaries lost their reason to exist. Daikin had two.

The mechanical leap came in 1951, when the company — applying its refrigeration know-how to civilian comfort — launched Japan's first packaged air conditioner. Post-war Japan was hot, humid, crowded, and beginning its miracle of reconstruction; the demand for cooling in offices, trains, and eventually homes would prove enormous. In 1963, reflecting how central air conditioning had become to its identity, the company was renamed, and it would eventually settle on Daikin Industries, Ltd. — "Dai-kin" a contraction of Osaka Kinzoku, the metalworks it had started as.7

The chemicals side, meanwhile, kept advancing in parallel, developing fluoropolymers like Neoflon that would later become the foundation of a high-margin specialty business feeding the semiconductor and chemical-processing industries. It is worth pausing on what fluoropolymers actually are, because they explain why the chemicals division became both a crown jewel and, later, a liability. Fluoropolymers are plastics in which the carbon backbone is armored with fluorine atoms, giving them almost supernatural resistance to heat, chemicals, friction, and electricity. That is why they line the inside of semiconductor-fabrication equipment, insulate wiring, seal EV battery systems, and coat aircraft components — applications where failure is catastrophic and ordinary plastics dissolve or degrade. The same fluorine-carbon bond that makes these materials so useful also makes them nearly indestructible in the environment, which is the entire basis of the "forever chemicals" problem that would surface decades later. Daikin, in other words, spent the twentieth century mastering exactly the chemistry that the twenty-first century would learn to fear.

In the language of Hamilton Helmer's 7 Powers framework — a lens this article will return to — what Osaka Metal accidentally built in the 1930s was a Cornered Resource and the seed of Process Power. A cornered resource is preferential access to something valuable that rivals cannot get on equal terms; process power is an advantage embedded in an organization's way of working that competitors cannot copy quickly even if they understand it. Daikin's in-house command of fluorochemistry was both. It meant that when the company later designed compressors and heat exchangers, it could optimize the machine and the fluid together, as a single system, rather than designing a box to fit whatever refrigerant the chemical suppliers happened to offer. Western manufacturers, structurally divorced from the chemistry, could not. That is a subtle edge, invisible on any spec sheet, and it would take another thirty years and an energy crisis to fully reveal its value.

That revelation arrived in the 1970s, when the price of oil quadrupled and the entire logic of the industry inverted overnight.

III. The 1982 Breakthrough: Variable Refrigerant Volume (VRV)

Resource-poor Japan imported nearly all of its energy, and the oil shocks of 1973 and 1979 hit it harder than almost any other industrial nation. Electricity prices spiked; the government imposed strict energy-conservation mandates; and suddenly the defining question for an air-conditioning company was no longer "can it cool the room?" but "how little power can it use doing so?" For most of the world's manufacturers, this was a headache. For a company that could co-engineer its refrigerant and its machine, it was an opening.

The problem with conventional commercial air conditioning, then as now in much of the United States, was that it was fundamentally a blunt instrument. A large central system chilled air and blew it through a building via enormous ducts, running full-blast or not at all — the thermostat equivalent of a light switch with only "on" and "off." Cooling an entire floor to serve three occupants in a corner office was routine, and wasteful. The ductwork itself devoured ceiling space and construction budget. In the dense, vertical, space-starved commercial real estate of Japan and Asia, this Western model fit badly.

In 1982, Daikin launched its answer: the Variable Refrigerant Volume system, or VRV.7 To understand why it was revolutionary, skip the acronym and picture the plumbing. Instead of chilling air centrally and pushing it through ducts, VRV pipes refrigerant directly to many small indoor units scattered through a building, each serving its own zone. The breakthrough was the word "variable." Using an inverter — an electronic controller that continuously varies the speed of the compressor motor rather than cycling it fully on and off — the system modulates exactly how much refrigerant flows to each unit, moment by moment, room by room. The analogy is a dimmer switch replacing a light switch, or a car with a smoothly variable accelerator replacing one with only "floored" and "stopped." Empty rooms get almost nothing; the crowded conference room gets more; the compressor loafs along at partial power instead of slamming between extremes. The energy savings were dramatic, and in an era of conservation mandates, decisive.

Here the dual-engine DNA paid off in a way rivals struggled to match. Continuously modulating refrigerant flow puts unusual demands on the fluid and on the compressor's behavior across a wide operating range — precisely the kind of system-level optimization a company that made both could tune more tightly than one assembling third-party parts. The inverter itself is worth understanding, because it is the piece of the story that quietly connects Daikin to the semiconductor age. An inverter is a bank of power electronics that converts incoming AC power into a form whose frequency — and therefore the motor's speed — can be varied continuously. This is the same fundamental technology that would later make electric vehicles and industrial robots possible, and it embeds real semiconductor and control-software content into what looks like a simple metal box. It is also expensive, which is why cheap markets resisted it: an inverter air conditioner costs more up front and pays the buyer back over years in lower electricity bills. In a country with expensive, imported energy, that trade was obvious. In a country with cheap energy, it was not — a divergence that would shape the industry's geography for forty years.

Consider what the inverter did to the economics of the machine. A conventional compressor is like a sprinter who can only stand still or run flat out; to hold a room at a steady temperature it lurches between full power and off, overshooting and undershooting, wasting energy at every switch and wearing itself out in the process. An inverter-driven compressor is a distance runner who settles into an efficient cruising pace and adjusts it smoothly. The result is not only lower energy use but quieter operation, more stable temperatures, and longer equipment life. Bundle that inverter with the zoning of VRV and you had, in 1982, a system that was a full generation ahead of the ducted, single-speed norm that still dominated the American market — and would keep dominating it for decades, for reasons that had nothing to do with the technology and everything to do with the price of electricity.

Then came the masterstroke that had nothing to do with engineering. Daikin trademarked the term "VRV." When competitors inevitably reverse-engineered the concept over the following years, they found themselves legally barred from calling their products by the name the market had learned. They were forced to coin a generic substitute — VRF, Variable Refrigerant Flow — and to this day the entire category carries a name that quietly concedes Daikin got there first. It is one of the cleaner examples of branding power in industrial history: not a consumer logo, but a category-defining word that permanently frames every rival as the imitation and Daikin as the original. Walk into a commercial HVAC tender in Singapore or Dubai and "VRV" still functions as the premium reference point.

VRV conquered Japan, then Asia, then the space-constrained commercial buildings of Europe. But it left one enormous market curiously untouched. The United States, with its cheap energy, sprawling low-rise buildings, and entrenched culture of ducted "unitary" systems, remained a stubborn holdout — still buying simple, single-speed, on/off central units decades after the rest of the developed world had moved toward inverters and zoning. For Daikin, America was simultaneously the industry's largest prize and its most glaring blind spot: a country that had barely heard of the company's signature technology. Closing that gap could not be done with a better product alone. It would require buying a way in.

IV. The Inoue Expansion: The Great M&A Masterclass (1994–2012)

In 1994, a Daikin lifer named 井上礼之 Noriyuki Inoue became the company's fourth president, and he would go on to define it for the next three decades.[^8] Inoue was not an engineer; he was a management thinker, and his signature doctrine — 人を基軸にする経営, "People-Centered Management" — held that a company's durable advantage lived in the judgment and initiative of its people rather than in any single technology. In practice, that philosophy translated into an unusually decentralized, entrepreneurial approach to global expansion: hire and trust local managers, adapt to local markets, and grow by absorbing others rather than by imposing a rigid Osaka template on the world. It was a bet on human capital that would be tested most severely on the terrain where Daikin was weakest — North America.

The first move was oblique. Rather than attack the US market head-on, Daikin bought its way in through Malaysia. In 2006, it acquired OYL Industries, a Malaysian-listed conglomerate, for roughly ¥230 billion — about $2.1 billion at the time.6 OYL looked like an odd trophy until you examined what sat inside it: McQuay International, a respected American maker of large "applied" commercial chillers — the industrial-scale cooling plants that serve hospitals, data centers, and skyscrapers — plus the AAF air-filtration business and a low-cost Asian manufacturing base. In one stroke, Daikin acquired a genuine commercial sales-and-service channel in the United States and a foothold in the applied segment, complementing the ductless expertise it already dominated. It was a lateral entry: not the mass residential market yet, but the professional, engineered end of it.

The main event came in 2012, and it is the deal that Daikin skeptics and admirers still argue about. The target was Goodman Global, a Houston-based manufacturer that was, in almost every respect, Daikin's opposite. Goodman made high-volume, low-cost, no-frills ducted residential air conditioners — the workhorse boxes of the American suburb. It was unglamorous, unfashionable, and owned by the private-equity firm Hellman & Friedman, which had been shopping it. A premium Japanese technology company buying a "cheap, low-tech American distributor" struck much of Wall Street as a category error.

There was drama in the timing. Daikin had been prepared to buy Goodman in 2011 for roughly $4 billion, but the deal was aborted in the chaos following the March 2011 Tōhoku earthquake and tsunami, which threw Japanese corporate finances and priorities into disarray. A year later, with a cooler head and a weaker seller, Daikin closed the transaction at a disciplined $3.7 billion — a price representing roughly ten times EBITDA, and notably below what it had been willing to pay before the disaster.[^5] The restraint is itself a data point about the company's capital discipline: it walked away, waited, and paid less.

Did Daikin overpay for a commodity box-maker? The bear reading at the time was that it did. The bull reading — which the subsequent decade has largely, though not entirely, vindicated — was that Daikin was not really buying factories or brands. It was buying a distribution network that money could not easily rebuild. Goodman's crown jewel was its vast, independent chain of company-owned distribution stores, which sold directly to the tens of thousands of small HVAC contractors who actually install American home systems. This bypassed the traditional manufacturer-rep model and put Daikin in direct contact with the installer base — the true decision-makers in a market where the homeowner almost never chooses the brand. What Daikin acquired, in effect, was a pipe into the American home.

To grasp why that pipe was worth so much, you have to understand how the American residential HVAC market actually works, because it is nothing like buying a television. When a family's air conditioner dies in July, they do not research brands; they call a contractor, and they buy whatever that contractor recommends and can install that afternoon. The contractor, in turn, stocks and installs the brand whose distributor is nearby, whose parts are available, whose margins are good, and whose systems they already know how to commission and repair. Distribution proximity and contractor loyalty, not consumer preference, decide the sale. Goodman had spent decades building exactly that — hundreds of stores stocking parts and equipment within easy reach of the independent contractor. A rival could match Goodman's product in a year; matching its distribution footprint and contractor relationships would take a decade and a fortune. Daikin bought the decade.

There is a deeper strategic point here about Inoue's people-centered philosophy in action. A more arrogant acquirer would have descended on Goodman, replaced its management, and imposed Japanese processes on a Texan culture — and likely destroyed the very network it had paid for. Daikin did close to the opposite. It retained Goodman's leadership and salesforce, respected the low-cost culture that made the business work, and treated the acquisition as a channel to be fed rather than a colony to be governed. Over the following years it consolidated Goodman's scattered plants into the single, massive Waller campus, improving efficiency without gutting the distribution model. This restraint is the hard part of M&A that spreadsheets never capture: knowing what not to change. It is also the clearest real-world demonstration of what "people-centered management" meant beyond the slogan.

The integration strategy revealed the discipline behind the thesis. Daikin did not force-merge Goodman into the parent or paper over the low-cost brand with premium pricing. It kept Goodman's cost base intact, consolidated manufacturing into an enormous new facility in Waller, Texas — the Daikin Texas Technology Park, one of the largest factories in North America — and then used Goodman's distribution pipe to gradually push higher-margin inverter compressors and ductless systems into a market that had never bought them at scale. In 2022, it renamed the combined US business Daikin Comfort Technologies, quietly retiring the arm's-length posture and signaling that the American operation was now core rather than adjunct.3[^16] The Goodman brand survived at the value end; the Daikin brand rose above it. Two decades of patient channel-building had turned the industry's most conspicuous blind spot into one of its largest growth engines.

But hardware and distribution were only half of Inoue's game. The other half was being played in the chemistry lab, and it involved giving away the store.

V. The Open Innovation Pivot: The R-32 Patent Gamble

Every so often a company does something that looks, on first glance, like corporate self-sabotage, and turns out on closer inspection to be a chess move three turns deep. Daikin's decision to hand its refrigerant patents to competitors for free is one of those.

Start with the regulatory wall. The refrigerants that made modern air conditioning possible have a dark environmental side: many are extraordinarily potent greenhouse gases. The industry workhorse of the 2000s, R-410A, has a Global Warming Potential — a measure of heat-trapping capacity relative to carbon dioxide — roughly two thousand times that of CO₂. Under the Montreal Protocol's Kigali Amendment, the world agreed to phase such high-GWP refrigerants down. The industry needed a replacement, and it needed one fast.

Daikin's answer was R-32, difluoromethane, a single-component refrigerant with about one-third the global warming potential of R-410A, better energy efficiency, and lower cost.4 There was one catch, and it was the reason the industry had hesitated for years: R-32 is classified A2L — mildly flammable. Conservative safety regulators, building-code committees, and rival manufacturers balked at putting a faintly flammable gas into millions of homes. The technology was ready before the world's rulebooks were.

This is where Daikin made its unconventional move. Rather than hoard its substantial R-32 patent estate and extract licensing fees, it did the opposite. In 2011 it granted free access to 93 of its R-32 patents to companies in emerging economies, to encourage adoption where the climate impact of cheap air conditioning would be greatest. In 2015 it widened the offer globally. And in 2019 it issued a formal Patent Non-Assertion Pledge, a binding promise not to enforce its basic R-32 patents against anyone building equipment with the refrigerant — a portfolio that by the early 2020s spanned hundreds of patents.4 It voluntarily removed every legal reason for a competitor to avoid the technology it had pioneered.

Why would any company do this? Because Daikin had grasped a piece of platform game theory that the rest of the industry had not. A refrigerant is not a product; it is a standard. Its value compounds with universality — shared servicing knowledge, interchangeable components, harmonized safety codes, contractor familiarity. By eliminating licensing friction, Daikin engineered R-32 into the global default before rival chemistries promoted by Honeywell or Chemours could lock in, effectively winning a standards war by refusing to charge tolls on the road it had built. More than a hundred million R-32 units have since been deployed worldwide.

The move rhymes with famous open-standards gambits from other industries — the decision to make a technology free precisely so that it becomes ubiquitous, at which point the sponsor profits from an adjacent, harder-to-replicate position rather than from licensing fees. Tesla's decision to open its patents to spur electric-vehicle adoption is the closest recent analogue. What made Daikin's version unusually shrewd is that its adjacent position was not a network or a brand but a molecule — a physical input that every adopter must keep buying. When you open-source software, the marginal copy is free forever. When you "open-source" a refrigerant standard, every unit ever built still needs to be filled and, eventually, refilled with a chemical that only a few companies can manufacture at scale. Daikin gave away the blueprint and kept the quarry.

There is a counter-narrative worth stating honestly, because promotional accounts of the R-32 pledge tend to skip it. Daikin's altruism was also self-interest of a defensive kind: several of the alternative low-GWP refrigerants being promoted by chemical rivals were proprietary blends that would have shifted the industry's value toward those rivals and away from Daikin. Pushing a simple, single-component, hard-to-patent-around molecule that Daikin could produce cheaply was a way of steering the transition onto terrain where Daikin was strong and its chemical competitors were not. The pledge was generous, genuinely accelerated climate-friendlier cooling, and was also a masterful act of competitive positioning. Those things are all true at once, and an independent reading holds them together rather than choosing the flattering one.

The genius, though, is in the double-dip, and it circles straight back to the dual engine. When a competitor builds an R-32 air conditioner using Daikin's freely pledged mechanical patents, it still has to fill that machine with the refrigerant itself — and Daikin's chemicals division is one of the world's top-tier producers of the R-32 chemical. The pledge gave away the low-margin patent tolls in order to inflate demand for the high-margin molecule that only a handful of firms, Daikin foremost among them, can make at scale. Rivals were invited to build the cars for free, on the condition that many of them would keep coming back to buy the fuel. It is the clearest single demonstration of why owning both the chemistry and the machine is worth more than the sum of its parts — and, as later sections will show, it is also the reason the chemicals division has become the company's most complicated asset, because the same fluorine chemistry that makes it valuable is now squarely in the crosshairs of environmental regulators.

That tension — chemistry as crown jewel and chemistry as liability — now sits on the desk of a new generation of leadership.

VI. Modern Leadership: Inside Daikin's Current Command Center

For sixty-seven years, one man was woven into the fabric of Daikin. Noriyuki Inoue joined the company in 1957, ran it as president from 1994, remained its chairman and guiding intelligence long after, and in June 2024, at the age of 89, finally stepped back to become Honorary Chairman.[^8] Few executives in modern corporate history have shaped a single institution for so long. His departure was less a retirement than the closing of an era, and it raised the question that hangs over every founder-scale personality: how much of the company's success was the system he built, and how much was simply him?

The succession had been staged carefully, which is itself a mark of governance seriousness. 十河政則 Masanori Togawa, who had served as CEO since 2011 and steered the company through the pandemic and the supply-chain convulsions that followed, moved into the role of Representative Director, Chairman, and CEO.[^8] 竹中直文 Naofumi Takenaka was appointed Representative Director, President, and COO, taking day-to-day operational command. The structure keeps an experienced hand on strategy while handing the operating controls to the next generation — a deliberate, un-dramatic transition of the kind Japanese governance tends to do well and Western succession dramas often do badly.

Yet the very smoothness of the handover raises the governance question a skeptical investor should ask of any long-dominant founder-figure. Inoue ran or oversaw Daikin for the better part of five decades, and the retention of a long-serving CEO into the chairmanship, followed by an internally promoted president, is textbook Japanese continuity — reassuring for strategic stability, but the opposite of the independent, external-check-heavy board structure that Anglo-American governance prizes. There is no evidence of dysfunction here; Daikin's execution record argues the culture works. But an activist would note that a board this internally cultivated is unlikely to be the source of hard challenges to management's own plan — which puts more weight on external investors to supply the scrutiny, particularly around capital allocation and the credibility of margin targets. Continuity has served Daikin's shareholders well for thirty years. Whether it also produces the pointed self-examination that a "rebuild our earning power" moment demands is a fair thing to watch.

On the evidence of behavior over time, the credibility of this management team rests on a mixed but broadly favorable record. The top line tells a story of relentless growth: consolidated net sales climbed from just under ¥4 trillion in the year ended March 2023 to ¥4.4 trillion, then ¥4.75 trillion, and finally past ¥5 trillion in the year ended March 2026 — three consecutive record years and a roughly 26% increase over three years.[^2] Net income has tracked a similar upward path, reaching ¥275 billion in the latest year.[^2] For a business of this scale in a mature industry, sustained high-single-digit top-line growth is a genuinely strong result, and it reflects real demand for the product across cycles and geographies.

The blemish is on profitability, and management has been candid enough to name it. Operating margin has hovered in the 8-to-9% range rather than climbing, which is why FUSION 30 opens with the confession that its predecessor plan missed its margin and return targets.5 A company can grow revenue by chasing volume in low-margin markets or by absorbing input-cost inflation it cannot fully pass on — and some of both happened over this period, as copper, aluminum, and freight costs whipsawed and as growth came partly from price-competitive regions. Togawa's tenure delivered a long run of record sales and steady, if unspectacular, operating margins through a decade that included a pandemic, a semiconductor shortage, and violent swings in raw-material and freight costs. Capital allocation has been recognizably Japanese: conservative, reinvestment-heavy, and unusually disciplined about mergers — the willingness to walk away from Goodman in 2011 and pay less a year later is the template. Daikin has consistently prioritized plowing cash into R&D and into regional manufacturing under a "local production for local consumption" doctrine, rather than juicing earnings per share with aggressive buybacks. For long-term investors this is mostly a virtue, though an activist would fairly note the flip side: a balance sheet run conservatively and a shareholder-return policy that has historically been modest relative to the cash the business throws off. A skeptic's question — is management being disciplined or simply under-distributing? — is a legitimate one to keep on the table.

The honest place to test management, though, is not the good years but the recent stumble, and the financials point straight to it. The company is best understood as three businesses of wildly different size. The Air Conditioning segment is the empire: it accounts for well over 90% of sales and is the undisputed engine of corporate value. The Chemicals segment is small — a low-single-digit share of revenue — but historically a high-margin specialty jewel, supplying fluoropolymers and fluorochemicals to semiconductor, EV-battery, and aerospace customers. And a residual "Other" segment houses hydraulics, defense, and oil-hydraulic equipment. In the year ended March 2025, that structure produced roughly ¥4.75 trillion in total sales, with air conditioning contributing the overwhelming majority and chemicals a small but richly profitable sliver.[^2]

What matters is what happened next. In the year ended March 2026, even as total sales pushed past ¥5 trillion to a record, the chemicals division went into reverse: revenues rose modestly but profit fell sharply, hammered by weak semiconductor demand and a slow recovery in the automotive sector, with a specific hit to sales of PFA — a high-value fluoropolymer used in chip-making equipment.[^2] Management framed this on its results briefing as a cyclical downturn in end-markets rather than a structural break. That framing is plausible; semiconductor capital spending is famously cyclical. But it is exactly the kind of claim an independent analyst should mark to watch, because the chemicals division's troubles are not only about the chip cycle. They are also about fluorine — and fluorine is now a regulatory battlefield. Which is precisely why the company has staked its next five years on shifting the center of gravity away from selling boxes and molecules, and toward selling something stickier.

VII. The "FUSION 30" Playbook: Shifting from Box-Selling to Solutions

Every five years, Daikin publishes a strategic management plan under the "FUSION" banner, and on May 12, 2026, alongside its record results, it unveiled the newest one: FUSION 30, covering the fiscal years 2026 through 2030.1 What makes this plan more interesting than a typical corporate roadmap is that it opens with something close to an admission. The prior plan, FUSION 25, hit its top-line sales targets but missed on profitability — operating margin and return on equity both fell short of goal.5 FUSION 30's stated organizing theme is blunt: "rebuilding our earning power."1 A company that has just crossed ¥5 trillion in sales is telling its investors that growth alone is no longer the point; profit per unit of that growth is.

The numeric targets put teeth on the rhetoric. Daikin is aiming for roughly 6% average annual sales growth, an operating margin of 10% by FY2028 rising above 12% by FY2030, and return on equity of 12% by FY2028 climbing to 15% by FY2030.[^4] To gauge the ambition, anchor on the starting point: the year ended March 2026 delivered an operating margin of roughly 8.3%. Lifting that to 12% while growing the top line at 6% a year is not a rounding exercise — it implies a meaningful re-engineering of the business mix, and it is a promise the market will hold management to, precisely because the last plan came up short on this exact metric.

The centerpiece of that re-engineering is the pivot from hardware to "solutions." In plain terms, Daikin wants to sell fewer one-time boxes and more ongoing relationships: multi-year maintenance and service contracts, energy-performance agreements where Daikin is paid for the efficiency it delivers, IoT-enabled building management, and "air-as-a-service" arrangements where a customer buys guaranteed indoor climate rather than the equipment that provides it. The plan targets expanding this solutions business to 40% of total sales by FY2030.1 The strategic logic is sound and familiar from other industries: hardware sales are cyclical and increasingly commoditized by low-cost Chinese competitors, whereas service revenue is recurring, higher-margin, and stickier — it raises customer lifetime value and smooths the brutal cyclicality of equipment demand. It is the same "razor-to-blades," "product-to-platform" migration that has reshaped software, elevators, and aircraft engines.

The elevator analogy is the most instructive, because it is the closest cousin to Daikin's situation. Companies like Otis and Schindler discovered long ago that the money in elevators is not in selling the elevator but in the decades of mandatory maintenance contracts that follow — a captive, recurring, high-margin annuity attached to a piece of installed equipment that legally and practically cannot be left unserviced. Air conditioning has the same shape: every unit Daikin has ever sold is a piece of equipment that needs servicing, monitoring, refrigerant, and eventual replacement, and the company that installed it has the inside track on all of it. Daikin's installed base, built over decades, is therefore a vast latent annuity that it has historically under-monetized. The solutions push is, at bottom, an attempt to finally harvest that annuity — to turn a century of boxes sold into a stream of services rendered. If the company has one genuinely underpriced asset, it may be this installed base.

The independent question is whether Daikin can actually execute it, because selling solutions is a genuinely different business from manufacturing them. It demands digital platforms, service organizations, data capabilities, and sales cultures that a century-old manufacturing company does not automatically possess, and every industrial firm now chases the same recurring-revenue dream with mixed success. Moving from 28% to 40% of a growing sales base in five years is aggressive, and "solutions" is a soft enough category that investors should watch how the company defines and reports it — the risk being that low-margin maintenance contracts get relabeled to hit a headline percentage. The target is a management claim, not yet a proven capability, and it deserves to be tracked as such.

Alongside the solutions pivot sits a striking geographic bet: India. Daikin is repositioning India from a market it manufactures for into a market it manufactures from — building out mega-capacity, including a large facility at Sri City, to serve not only India's booming domestic demand but to export to East Africa, the Middle East, and Latin America. This is the "IMEA" theme (India, Middle East, Africa) at the heart of FUSION 30's growth agenda.1

The domestic prize is real, and its scale is easy to underestimate. Air-conditioning penetration in Indian households remains in the single digits to low double digits — a fraction of the near-universal ownership in China, Japan, or the United States — even as incomes rise, cities swell, and heatwaves grow more severe and more lethal. That gap between where penetration is and where a hot, urbanizing, middle-income country's penetration eventually goes is one of the largest structural demand pools left in the consumer-durables world, and Daikin holds a leading position at the premium residential end of it. The India logic is thus a two-for-one: capture a domestic market in the early innings of a multi-decade adoption curve, and simultaneously turn Indian factories into a low-cost export base for the wider tropical world.

There is also a defensive rationale that management is careful not to over-advertise: India is a hedge against China. For years, China was the growth engine of the global air-conditioning industry and a major profit center for Daikin's premium multi-split business. With Chinese property demand now structurally impaired, the company needs a new volume engine that is not correlated to Chinese real estate — and a manufacturing base outside China as global supply chains fragment along geopolitical lines. India answers both needs at once. Whether the export ambition materializes at the scale the plan implies is an open question, and India has humbled many foreign manufacturers with its logistics, tariffs, and price sensitivity. But the direction of travel is clear, and it points at the structural moat that all of this ultimately rests on.

VIII. The 7 Powers of Daikin: Mapping the Moat

Strip away the narrative and ask the cold question a long-term investor must ask: why can't a competitor simply do what Daikin does? The honest answer is that in some respects they can — this is a competitive, cyclical, capital-intensive industry with formidable rivals — but in three specific respects the barriers are real and worth naming precisely, using Helmer's framework as the scalpel.

Scale Economies (Power #1). As the world's largest HVAC manufacturer, Daikin buys steel, copper, aluminum, and electronic components — the physical bulk of an air conditioner — at volumes no rival can match, and spreads its enormous R&D budget across more units than anyone else. In a business where the bill of materials is dominated by industrial commodities, purchasing scale translates fairly directly into cost position. The caveat is important, though: scale in HVAC is regional, not purely global. A factory in Texas does not lower the delivered cost of an air conditioner in Poland, which is precisely why Daikin runs its "local production for local consumption" network. Its scale advantage is therefore a patchwork of strong regional positions rather than one monolithic global cost curve, and in China specifically, domestic giants Midea and Gree enjoy scale of their own.

High Switching Costs / Channel Lock-In (Power #2). This is the most underappreciated and arguably the strongest of Daikin's powers, and it hinges on a peculiarity of the industry: the customer almost never chooses the brand. The homeowner or building manager defers to the contractor who installs and services the system, and the contractor's choice is governed by what they are trained, tooled, and comfortable with. Daikin has spent decades exploiting this through "Daikin Academies" that certify tens of thousands of installers worldwide in its proprietary VRV piping, diagnostic software, and controllers. Once an installer has invested the time to master Daikin's ecosystem — its tools, its fault codes, its commissioning software — switching to a rival means re-training, re-tooling, and re-learning at real cost. Daikin has, in effect, cornered the channel rather than the customer. This is a genuine, behaviorally grounded moat, and it is why Goodman's distribution network was worth $3.7 billion: distribution and installer relationships, not factories, are the scarce asset.

Cornered Resource (Power #3). The vertical integration of the chemicals division — the ability to synthesize its own fluorochemicals and fluoroelastomers and to co-optimize the machine with the fluid — remains the structural feature no competitor possesses. It is a real edge in R-32 economics and system design. But intellectual honesty requires flagging that this cornered resource has become double-edged: the very fluorine chemistry that competitors cannot replicate is the chemistry that global regulators are now moving to restrict. A cornered resource that regulators are trying to outlaw is a more ambiguous asset than it looks on a strategy slide.

It is worth war-gaming the rivals directly, because the competitive threat differs by flank. The most existential long-run challenge comes from China. Midea and Gree enjoy colossal domestic scale, vertically integrated component manufacturing, and a willingness to compete on price that compresses margins wherever they show up. In the commodity end of the global residential market — the simple, low-feature units sold in price-sensitive emerging economies — the Chinese players are formidable and gaining, and they are the reason Daikin cannot simply defend the low end and must keep migrating upmarket toward premium systems and services. The Western giants, Carrier and Trane, are a different kind of competitor: strong in large applied and commercial systems, disciplined on price, and increasingly focused, like Daikin, on the recurring-service and controls layer. They are less a threat to Daikin's existence than a matched pair of peers fighting over the same premium commercial and institutional customers. And the Korean and Japanese electronics players — LG, Samsung, Mitsubishi Electric — compete hard in ductless and residential but lack Daikin's chemical integration and its depth in applied commercial systems.

The strategic conclusion is that Daikin's defensible ground is the premium, engineered, service-attached end of the market, and its exposed flank is the commoditizing low end where Chinese scale wins. Much of FUSION 30 can be read as an explicit acknowledgment of exactly this: retreat is not the plan, but the growth and margin ambitions are concentrated in "high-profit domains," solutions, and applied systems — precisely the terrain where Chinese price competition bites least and Daikin's moats bite most.

Run the same analysis through Porter's Five Forces and the picture sharpens. Rivalry is intense and intensifying, with Midea, Gree, Carrier, Trane, LG, and Mitsubishi Electric all formidable. Buyer power is fragmented and blunted by the contractor-channel lock-in described above — a structural advantage. Supplier power is where Daikin is unusual: by making its own refrigerant, it has partially internalized what is a key supplier for everyone else. Threat of substitutes is low — there is no substitute for climate control in a warming world, and decarbonization is turning heat pumps into a growth category. And barriers to entry are high for a credible global player: distribution, brand, installed base, and regulatory approvals take decades to assemble. The composite verdict is a business with a genuinely defensible position, but not an unassailable one — a leader that must keep running, not a monopolist collecting rent. Which sets up the real debate: from here, does Daikin win, and what could break the case?

IX. The Investment Story Spine: Bull vs. Bear & Risk Radar

The bull case

The bull case rests on two waves, one American and one global, that could power Daikin's next decade.

The first is what the industry calls US "inverterization." Recall that America remained, for decades, the developed world's great holdout — still buying cheap, single-speed, on/off central units while the rest of the planet moved to efficient variable-speed inverter systems. That is now changing, pushed by tightening federal efficiency standards and a slow consumer shift toward lower energy bills. Daikin is arguably better positioned than any competitor to profit from this transition, because it owns both the pipe and the product: Goodman's distribution network reaches deep into the American contractor base, and Daikin's inverter and ductless technology is exactly what that base will increasingly be required to sell. On its investor communications, management has repeatedly pointed to regaining ducted-unitary share in the Americas and converting that legacy customer base toward higher-value inverter systems as a central growth thesis.[^2]12 If it works, Daikin captures a structural upgrade cycle in the world's largest and most profitable HVAC market — selling the same customers a more expensive, higher-margin machine.

The size of the US prize deserves emphasis, because it is what makes the Goodman bet potentially transformational rather than merely sound. North America is the largest and among the most profitable HVAC markets on Earth, and it has been the slowest to adopt the efficient technology Daikin has sold everywhere else for forty years. That is not a mature market to defend; it is an under-penetrated one to convert. Each home that swaps a single-speed unit for an inverter system is a customer trading up to a more expensive, higher-margin machine — and Daikin, through Goodman's stores, sits at the exact point of sale where that decision is made. The bull case is not that Daikin gains American share by winning a price war; it is that the whole market is being pulled upmarket toward the products Daikin was built to make, and Daikin already owns the distribution to serve it. If even a meaningful fraction of the US installed base converts over the next decade, the revenue and mix implications are large.

The second wave is decarbonization and electrification. Governments across Europe and beyond have been subsidizing heat pumps to displace gas boilers, and Daikin's Altherma line is a leading premium brand in that transition. In a world serious about cutting building emissions, the electric heat pump is the central technology, and Daikin sells it at scale. The mechanism is elegant: a heat pump is simply an air conditioner that can run in reverse, moving heat into a building in winter as efficiently as it moves heat out in summer, and because it moves existing heat rather than burning fuel to create it, it can deliver several units of warmth for each unit of electricity — a physics advantage that no gas boiler can match. As electricity grids decarbonize, the heat pump becomes the obvious way to heat a building without emissions, and Daikin's decades of refrigerant-cycle expertise transfer directly. The long-term structural tailwind — a warming climate driving cooling demand in emerging markets, and climate policy driving heat-pump demand in developed ones — is as favorable a backdrop as an industrial company could ask for. The caveat, developed below, is that policy-driven demand is fickle, and Europe has just demonstrated how quickly a subsidy-fueled boom can turn into a glut.

The bear case and risk radar

The bear case is where an independent analysis earns its keep, because the risks here are specific, material, and in one case potentially enormous.

The PFAS "forever chemicals" time bomb. This is the single most serious overhang, and it strikes at the crown jewel. Daikin's high-margin chemicals division depends on per- and polyfluoroalkyl substances — PFAS, the "forever chemicals" prized for their performance and notorious for their environmental persistence. The regulatory vise is tightening globally. In April 2024, the US EPA finalized a rule designating the two most prominent PFAS compounds, PFOA and PFOS, as "hazardous substances" under the CERCLA "Superfund" law — a designation that can expose manufacturers and users to sweeping cleanup and remediation liability.10 Compounding the shift, Daikin's rival 3M announced it would exit all PFAS manufacturing by the end of 2025, and reported completing that exit — a move that both validates the reputational and legal risk and, paradoxically, could hand market share to producers like Daikin that remain in the business.9 That is the double edge: staying in PFAS may mean more volume, but also escalating litigation exposure, soil and water remediation liabilities, and heavy R&D costs to develop next-generation replacement chemistries. For a segment prized precisely for its high margins, a large, hard-to-quantify legal tail is exactly the kind of risk that markets struggle to price and tend to punish. Investors should watch the segment's disclosures closely for any provisions, reserves, or litigation commentary.

The reason PFAS cuts so deep is that it threatens the most profitable part of the company at the moment that part is already weak. The chemicals division earns its keep precisely because its high-performance fluoropolymers command premium prices in demanding applications — chip-making, batteries, aerospace — where there is no cheap substitute. But "no cheap substitute" and "regulators want it banned" are a dangerous combination. If restrictions tighten, Daikin faces a three-front problem simultaneously: legal and remediation liabilities for past and present production, the R&D expense of inventing next-generation non-PFAS or lower-persistence alternatives that match the performance customers depend on, and the competitive question of who is left standing to supply a shrinking-but-essential market. The optimistic reading is that a rival's exit leaves Daikin as one of few qualified suppliers of materials the semiconductor and defense industries genuinely cannot do without — a position of pricing power. The pessimistic reading is that Daikin is holding a bag of legal risk that 3M chose to put down. Both readings depend on regulatory and litigation outcomes that are, by their nature, unpredictable, which is exactly why this belongs at the top of the risk radar rather than buried in a footnote. An independent analyst cannot size this liability from the outside; the honest posture is to flag it as material, unquantified, and worth monitoring in every disclosure the company makes.

China's structural property slump. Daikin's most profitable Chinese business has long been premium multi-split systems for high-end residential apartments — a business tightly coupled to high-end property development. With China's real estate sector in a prolonged, structural downturn, that engine has cooled, and management has acknowledged softening residential demand in China as a drag on the air-conditioning segment.[^2] This is not a passing weather event; it is a secular headwind tied to the unwinding of China's property model, and it removes a pillar that used to be reliably high-margin.

The European heat-pump hangover. The same subsidy-driven boom that powers the bull case has proven volatile. In several European markets, governments have trimmed or wobbled on heat-pump subsidies, and the economics of heat pumps versus gas boilers swing with the ratio of electricity to gas prices. The result over the past couple of years has been a boom-then-glut pattern: a subsidy-fueled surge, an inventory overhang, and a slowdown in adoption. It is a reminder that policy-driven demand is only as durable as the policy, and that a growth story dependent on subsidies carries the risk built into every subsidy.

The activist stress test

What would a skeptical long/short investor or activist actually press management on? Three things. First, portfolio complexity: does the small, now-troubled, legally exposed chemicals business — plus a grab-bag "Other" segment of hydraulics and defense — belong inside an air-conditioning champion, or is it a source of "diworsification" and hidden liability that a sum-of-the-parts case would separate? Second, capital allocation and shareholder returns: a conservatively run balance sheet and historically modest payout invite the question of whether discipline has tipped into under-distribution, especially now that management is explicitly promising to "rebuild earning power." Third, accountability on the profitability miss: FUSION 25 fell short on margin and ROE, and the credibility of FUSION 30's even more ambitious targets depends on management explaining why this time is different with something more concrete than a new slogan. None of these is disqualifying. All of them are fair, and all of them are things a serious owner should keep pressing.

The net of the spine is that Daikin wins from here if the US inverter upgrade and global electrification tailwinds compound faster than the PFAS liability, the China property drag, and the margin-execution risk erode the story. That is a live contest, not a settled one — which is exactly why a small number of indicators are worth watching above all others.

X. Epilogue & What to Watch

Boil a company this sprawling down to what actually moves the thesis, and three indicators do most of the work. You do not need to calculate them; you need to watch which way they move.

1. The Solutions business share of AC sales. This is the master gauge of whether the strategic pivot is real. FUSION 30 stakes its "rebuilding earning power" promise on lifting solutions to 40% of sales by 2030.1 Track the trajectory — and watch how management defines the category. Steady, transparently reported progress would signal a genuine migration toward recurring, higher-margin revenue; a number that jumps suspiciously via reclassification, or stalls, would signal the opposite.

2. North American inverter conversion. The largest single growth lever is Daikin's ability to convert Goodman's legacy customer base from cheap single-speed boxes to premium inverter systems, and to keep regaining ducted-unitary share in the Americas.[^2] This is where the $3.7 billion distribution bet either compounds or plateaus. It is the clearest test of whether Daikin can turn its structural advantage into pricing power in the market that matters most.

3. Chemicals segment margin and PFAS provisions. Watch the profitability of the chemicals division and, crucially, any disclosure of legal reserves, remediation costs, or litigation related to PFAS. This is the line where a cyclical semiconductor downturn and a potentially structural regulatory liability are tangled together, and separating the two will tell you whether the crown jewel is merely having a bad year or facing a permanent re-rating.

Step back, and the shape of the whole becomes clear. Daikin is a masterclass in compounding an unlikely set of advantages: a chemical competency stumbled into by wartime necessity, a category-defining product locked in by a single trademark, a distribution empire assembled through patient and disciplined M&A, and a standards war won by the counterintuitive act of giving intellectual property away. It built a durable global position not through any one brilliant stroke but through a century of stacking edges that individually look modest and collectively became formidable. The quiet giant of climate control now faces its most crowded competitive field and its most complex risk in the fluorine chemistry that made it special. Whether it proves to be a serene compounder riding decarbonization and inverterization for another decade, or a great industrial franchise whose chemicals liability and margin ambitions outrun its execution, will not be settled by any single earnings report. It will be settled slowly — in the drift of a margin, the conversion of a contractor, and the ruling of a regulator on a molecule.

XI. Outro & Resources

The themes that define Daikin recur across its century: the fusion of chemistry and machinery into a single competitive organism; the discipline to buy channels rather than build them, and to walk away when the price is wrong; the willingness to play long games, whether trademarking a category or gifting a patent portfolio to win a standard; and now the harder, unproven task of turning a manufacturer into a service company while defending a chemicals franchise under regulatory siege. For readers who want to pressure-test the numbers behind the narrative, the primary sources below — Daikin's investor materials, results briefings, and the FUSION 30 plan documents, read against independent filings and reporting — are where the story can be verified, quarter by quarter, as it continues to unfold.

- Daikin Investor Relations portal and IR library, for results materials, integrated reports, and briefing transcripts.11

- The FUSION 30 Strategic Management Plan and its presentation deck, for the full target set and segment strategy.1[^4]5

- The financial results briefings, for segment-level performance and management's live framing of North America, China, Europe, and chemicals.[^2]

References

-

Daikin Formulates Strategic Management Plan "FUSION30" — Daikin Industries, Ltd., 2026-05-12 ↩↩↩↩↩↩

-

Daikin Industries, Ltd. (6367.T) Company Profile and Financial Market Data — Reuters ↩

-

Goodman Global Renamed Daikin Comfort Technologies — Daikin Industries, Ltd., 2022-03-15 ↩

-

R-32 Patent Non-Assertion Pledge Portal — Daikin Industries, Ltd. ↩↩

-

Strategic Management Plan "FUSION" — Daikin Industries, Ltd. ↩↩↩

-

Daikin Industries Acquires O.Y.L., McQuay — ACHR News, 2006 ↩

-

Chronology / Corporate History — Daikin Industries, Ltd. ↩↩↩

-

History of Daikin Innovation (Fluorocarbon gas first manufactured in Japan, 1935) — Daikin Industries, Ltd. ↩↩

-

PFAS Stewardship: 3M to exit PFAS manufacturing by end of 2025 — 3M ↩

-

PFAS Year-End Review: EPA finalizes PFOA/PFOS as CERCLA hazardous substances (April 2024) — Miller Nash LLP ↩

-

Daikin Investor Relations Portal — Daikin Industries, Ltd. ↩

-

Daikin Outlines U.S. Growth Strategy at J.P. Morgan Industrials Conference — Daikin North America ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube