Komatsu: The Silicon and Steel Giant

I. Introduction & Episode Roadmap

Somewhere in the Atacama Desert of northern Chile, at an altitude where the air is thin enough to make a visitor light-headed, a 400-ton truck the size of a two-story house crawls up a haul road cut into the side of a copper pit. Its payload is worth a small fortune in ore. Its cab is empty. There is no driver reaching for the gearshift, no operator squinting through the dust — just a machine navigating by satellite positioning, obstacle-detection radar, and a private radio mesh that stitches the whole mine into one nervous system. The truck knows where every other truck is. It knows where the shovel is loading. It never gets tired, never takes a smoke break, and never, in nearly two decades of operation, has injured a human being.

Now travel eleven thousand kilometers northwest, to a cleanroom in Veldhoven in the Netherlands, where a lithography machine built by ASML prints circuit patterns onto silicon wafers at dimensions measured in billionths of a meter. At the heart of that machine sits a light source — a deep-ultraviolet excimer laser pulsing thousands of times per second, each flash carving a feature smaller than a virus. Pull the cover off a meaningful share of those light sources and you find a nameplate that has nothing to do with the semiconductor industry's usual cast of characters.

The common thread between the driverless mining truck and the chip-printing laser is a single company: 株式会社小松製作所 Komatsu Ltd., trading as 6301.T on the 東京証券取引所 Tokyo Stock Exchange. Most people know Komatsu, if they know it at all, as "the yellow machines" — the number-two heavy-equipment maker on earth, the permanent silver medalist to Caterpillar's gold. That reputation is accurate and enormously incomplete.

In the fiscal year ended March 31, 2025, Komatsu generated consolidated net sales of ¥4,104.4 billion — roughly $27 billion — with operating income of ¥657.1 billion at a 16.0% margin and net income of ¥439.6 billion.1 Those are the numbers of a large, cyclical, well-run industrial. But underneath them sits a more interesting company than the income statement suggests: a firm that made telematics free two decades before "connected hardware" became a venture-capital religion, that timed a mining acquisition with a discipline its larger rival did not, and that quietly owns one of only two companies on the planet capable of building the lasers modern chipmaking depends on.

This is the story of how a firm founded to save an Ishikawa mining town in 1921 became a study in industrial duopoly, counter-cyclical patience, and the awkward art of running a proud Japanese manufacturer for capital efficiency. The themes to hold onto: the perpetual war with Caterpillar for the earthmoving and mining markets; the KOMTRAX data play that turned steel into software; the contrast between Komatsu's cheap, well-timed purchase of Joy Global and Caterpillar's expensive, top-of-cycle purchase of Bucyrus; the hidden semiconductor option called 株式会社ギガフォトン Gigaphoton; and the April 2025 handover to a finance-native chief executive, 今吉 琢也 Takuya Imayoshi, who inherited a company being told, politely but persistently, to stop sitting on quite so much cash.

II. Company Origins & The Monozukuri Spirit

The origin story does not begin with a bulldozer. It begins with a hole in the ground that had stopped paying.

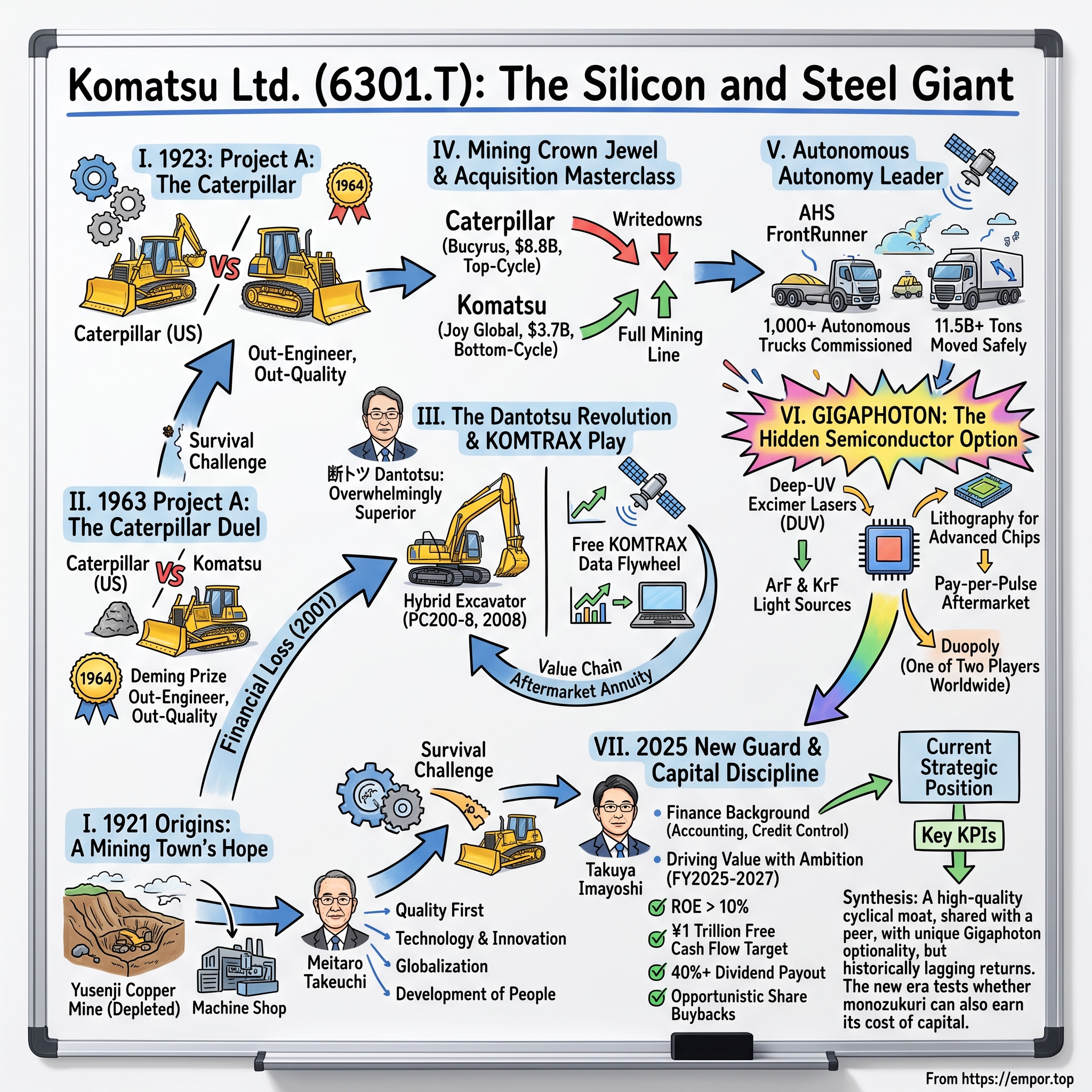

In the years around World War I, the Yusenji copper mine in Ishikawa Prefecture on the Sea of Japan coast supported a cluster of workers and their families. Its owner, the industrialist and politician 竹内 明太郎 Meitaro Takeuchi, had built a machine shop in 1917 to maintain the mine's equipment. As the copper deposit depleted, Takeuchi faced the problem that has haunted every company town in history: what happens to the people when the resource runs out? His answer, in May 1921, was to spin the machine shop off as an independent company — Komatsu Ltd., named for the town of Komatsu — and repurpose it to make cast-steel products and machine tools, giving the mine's dependents somewhere to work.2 The first proper product, a sheet-metal press, followed in 1924.

It is worth pausing on this because founding myths shape corporate DNA, and Komatsu's is unusually explicit about it. Takeuchi's stated principles — quality first, technology and innovation, globalization, and the development of people — were not retrofitted marketing.2 They map with almost eerie precision onto how the company would behave a century later. The Japanese have a word for the ethos: ものづくり monozukuri, literally "the making of things," but connoting a near-spiritual commitment to craftsmanship, to getting the object right for its own sake rather than for the quarter's sake. Monozukuri is easy to romanticize and easy to weaponize as an excuse for over-engineering that customers don't pay for. Komatsu's history contains both the virtue and the trap.

For its first four decades Komatsu was a competent, domestically focused maker of bulldozers and construction equipment — protected, like most of Japanese industry, by a closed home market. Then came the existential shock. In 1963, Japan's Ministry of International Trade and Industry moved to liberalize the earthmoving-equipment sector, and Caterpillar — the American colossus, larger and more technologically advanced — formed a joint venture with 三菱重工業 Mitsubishi Heavy Industries to manufacture inside Japan.3 To contemporaries this looked like a death sentence. Caterpillar's machines were simply better, and now they would be built locally, inside Komatsu's moat.

Komatsu's response became a textbook case in industrial quality. Rather than retreat, management launched what it called "Project A" — a company-wide campaign to raise the quality of its mid-size bulldozers to a level competitors could not match. Engineers pulled apart every weld, every hydraulic line, every fastener. The discipline was rooted in the then-novel gospel of total quality control, and it paid off fast: Komatsu won the Deming Prize, Japan's highest quality honor, in 1964.3 Within a few years the company had not merely survived the Caterpillar-Mitsubishi incursion; it had raised its domestic share and, crucially, made its machines good enough to export — eventually selling into North America, Caterpillar's home turf. The lesson Komatsu internalized was that it could not out-scale Caterpillar, so it would have to out-engineer it. That conviction, born in the 1960s, is the through-line of everything that follows — and it would be tested most severely not by an American rival but by the company's own balance sheet.

III. The Dantotsu Revolution: Rescuing the Company from its First Loss

For a company that had spent eighty years never losing money on a consolidated basis, the number on the page in 2001 was a kind of heresy. The dot-com bust had frozen capital spending, Japan's domestic construction market had been stagnant for a decade, and Komatsu — bloated with product lines, factories, and businesses accumulated in fatter years — posted the first consolidated net loss in its history.

Into that crisis walked 坂根 正弘 Masahiro Sakane, who became president in 2001 and remains one of the most consequential figures in modern Japanese industry.4 Sakane's diagnosis was unsentimental. Komatsu, he judged, could never win a price war against lower-cost competitors, and it could not win by being merely competitive — being 5% better than Caterpillar on ten dimensions was a formula for permanent margin compression. What Komatsu needed was to be so far ahead on a few things that rivals could not catch up for years. He gave the idea a name that became the company's organizing philosophy: 断トツ Dantotsu — a colloquial Japanese term meaning "overwhelmingly superior," the undisputed, incomparable number one.

The Dantotsu program had a hard edge that is easy to lose in the branding. Sakane cut. He exited unprofitable product lines, restructured the sprawling portfolio, and forced a discipline of asking whether each business could plausibly be number one. The philosophy then organized itself into three pillars that Komatsu still uses: Dantotsu Products (machines with advantages competitors cannot replicate quickly), Dantotsu Service (anticipating failures before they strand a customer), and Dantotsu Solutions (optimizing an entire job site rather than selling a single machine). The physical proof point arrived in 2008, when Komatsu launched the PC200-8, the world's first hybrid hydraulic excavator, which captured the energy of the machine's swing rotation and fed it back into the system — a genuine engineering first, not a marketing one.4

But the most durable move Sakane made was almost philosophical in its restraint. Komatsu had developed a telematics system called KOMTRAX — GPS and cellular hardware bolted onto machines to report their location, operating hours, fuel burn, and fault codes back to base. The obvious commercial instinct was to sell it as a premium add-on. Sakane did the opposite: he made KOMTRAX standard equipment, fitted free of charge, first in Japan and then across the fleet globally.5 Giving away hardware that cost real money to install looks, at first glance, like value destruction. It was the opposite, and understanding why is the key to Komatsu's modern moat.

By making telematics free and universal, Komatsu solved the chicken-and-egg problem that kills most connected-hardware plays: the data is only valuable if nearly every machine reports, and customers won't pay upfront for a network whose value only appears at scale. Standardization bought ubiquity, and ubiquity created a flywheel. Customers could suddenly see, in real time, which machines were idling and burning diesel for nothing. Dealers could shift from reactive repair — waiting for a breakdown — to predictive parts replacement, the far more profitable business of selling the right filter or track before the machine failed. And in aggregate, the working-hour data streaming off hundreds of thousands of machines became a macroeconomic signal in its own right. Market commentators came to treat the so-called "KOMTRAX index" of Chinese construction activity as an informal, real-time read on the world's second-largest economy — a leading indicator that construction was slowing or accelerating months before official statistics confirmed it. Whether or not one takes the folklore literally, the underlying point is real: Komatsu built, almost by accident, a proprietary dataset on the pulse of global construction that no competitor could replicate without first giving away the same hardware for a decade. That data advantage is the bridge from Sakane's turnaround to the cash machine that actually pays the bills.

IV. The Core Business Engine: Construction, Mining & Utility

Strip away the lasers and the driverless trucks and the podcast-friendly narrative, and Komatsu is, in accounting terms, essentially one business. In the year ended March 2025, the Construction, Mining and Utility Equipment segment produced net sales of roughly ¥3,798 billion and segment profit of roughly ¥599 billion — well over 90% of consolidated sales and the overwhelming majority of operating profit.6 Everything else — retail finance, industrial machinery, the semiconductor lasers — rounds to a rounding error against it, at least on the top line. So the first question any investor has to answer is: how good is this core business, really, and how defensible?

The industry structure is unusually legible. At the top sits a genuine duopoly for the largest machines: Caterpillar and Komatsu, the only two firms with full-line global scale in both construction and mining. Below them is a regional and niche tier — 日立建機株式会社 Hitachi Construction Machinery, respected especially in large mining excavators; John Deere, strong in the Americas; and Volvo Construction Equipment. And then there is the disruptive tier that keeps Komatsu strategists awake: the Chinese manufacturers, above all 三一重工 Sany Heavy Industry and 徐工集団 XCMG, which rode the Chinese construction boom to enormous domestic volume and then began exporting aggressively priced machines into Southeast Asia, Africa, and Latin America.

Komatsu's response to the Chinese challenge is itself a strategic tell. Rather than fight Sany and XCMG for the low end of the Chinese market on price — a war it could not win against home-court manufacturers with lower cost structures — Komatsu deliberately shifted upmarket and let volume go. The company took a smaller slice of a market it judged to be structurally unattractive, protecting margin over share. On recent earnings calls management has been candid that Chinese demand for construction equipment collapsed with the country's property downturn, and that Komatsu's exposure there is now modest by design. That is defensible portfolio management, but it is also an admission: in the largest single construction-equipment market on earth, Komatsu chose to become a boutique rather than a champion.

The deeper source of durability is not new-machine sales at all — those are violently cyclical, swinging with commodity prices, interest rates, and construction cycles. The durable business is the aftermarket: the parts, service, repairs, and rebuilt components that a machine consumes across a working life of fifteen years or more. Komatsu has spent two decades deliberately expanding this "value chain" business, and company materials describe the aftermarket climbing from roughly a third of the equipment segment toward roughly half of it over the past decade-plus.7 The economics are the whole game. The machine is the customer-acquisition cost — often sold on thin margins to win the placement. The parts and service revenue over the machine's life is the high-margin annuity, and because KOMTRAX tells the dealer exactly what each machine needs and when, Komatsu captures far more of that lifetime spend than it otherwise would.

Put plainly: a Komatsu excavator is less a product than a fifteen-year subscription that happens to be delivered as forty tons of steel up front. The larger the global installed base grows, the larger and steadier the parts annuity becomes, cushioning the brutal swings in new-equipment demand. That is a genuine, evidence-backed advantage — but it is an advantage Caterpillar shares in equal measure, which is why the two giants ultimately fight hardest not over ditch-diggers but over the highest-margin corner of the whole industry: the mine.

V. The Mining Crown Jewel & The Joy Global Masterclass

If construction is the volume business, mining is the profit business, and the difference explains a great deal about how both Komatsu and Caterpillar behave. Mining equipment is a smaller share of unit sales but a disproportionate share of the aftermarket cash flows, because a haul truck grinding ore around the clock in the Pilbara or the Atacama devours parts and rebuilds at a rate no urban excavator can match. Mining is where the margins, the switching costs, and the technological moats all concentrate. It is the crown jewel — and both giants have spent the past fifteen years trying to seize more of it.

Komatsu's technological claim in mining is autonomy, and here the company has a genuine first-mover record rather than a marketing one. It ran its first commercial autonomous-haulage trial in 2008 at Codelco's Gabriela Mistral copper mine in Chile — driverless ultra-class trucks navigating a live pit years before "autonomous vehicles" entered the popular imagination.8 The system, branded FrontRunner, then compounded quietly for nearly two decades. In April 2026 Komatsu announced it had become the first equipment maker to commission its 1,000th ultra-class autonomous haul truck, with customers having moved more than 11.5 billion metric tons of material autonomously — across mines in North and South America, Australia, and Europe, and, by the company's account, without a single autonomy-related operator injury.8 (It is worth flagging that these are company-reported figures; the safety record in particular is Komatsu's own disclosure, not an independently audited statistic.)

Why does autonomy matter so much strategically? Because it converts a machine sale into a systems lock-in. Once a mine has integrated Komatsu's autonomous fleet-management software into its operation — retrained its people, rebuilt its pit design around driverless traffic, wired its haul roads for the radio mesh — switching to a rival's trucks is not a procurement decision, it is a multi-year, multi-million-dollar surgery. That is the mechanism behind mining's fat, sticky margins, and it is why autonomous fleet count is arguably the single best leading indicator of Komatsu's deepening enterprise moat.

Which brings us to the M&A masterclass — or, depending on which company you're rooting for, the M&A cautionary tale. In November 2010, at what turned out to be very close to the peak of the commodity supercycle, Caterpillar agreed to buy Bucyrus International, a storied maker of mining shovels and draglines, for roughly $8.6 billion including debt — paying $92 per share in cash and closing the deal in July 2011 at a total cost near $8.8 billion.9 Caterpillar bought high, financed with debt and equity, and then watched commodity prices collapse over the following years, leaving it to absorb painful mining-related write-downs and restructuring — the same period in which it also took a $580 million charge on an unrelated, fraud-tainted Chinese acquisition.10

Komatsu did the opposite. It waited. In July 2016 — years into the mining downturn, near the bottom of the cycle — Komatsu agreed to acquire Joy Global, the American maker of underground mining machines and P&H electric rope shovels, for about $3.7 billion including debt, at $28.30 per share; the deal closed in 2017 and the business was renamed Komatsu Mining Corp.11 The strategic logic was clean: Joy's underground longwall systems, continuous miners, and surface shovels were almost entirely complementary to Komatsu's surface haul trucks, giving Komatsu a full-line mining offering to match Caterpillar's breadth. The contrast in timing is the point. Caterpillar paid supercycle prices at the top; Komatsu paid distressed prices at the bottom, for an asset that arguably fit better. Whether Komatsu's discipline reflected genius or merely the good fortune of not having a deal ready in 2011 is a fair question — but the outcome, measured in dollars of enterprise value per dollar of mining capability acquired, favored Komatsu decisively. And it is that mining engine, more than anything, that funds the company's most improbable side business.

VI. Gigaphoton: The Hidden Semiconductor Powerhouse

Here is a question that should not have an interesting answer, but does: why does a company that makes bulldozers own a critical link in the global semiconductor supply chain?

The answer runs back to the 1980s, when Komatsu's engineers were doing laser research for industrial applications — combustion analysis, materials processing, the unglamorous physics of making heavy machinery. Excimer lasers, which fire ultraviolet pulses by exciting exotic gas mixtures, turned out to be exactly the light sources the semiconductor industry needed to keep shrinking transistors. The shorter the wavelength of light you print with, the finer the features you can etch onto silicon. In 2000, Komatsu spun that laser expertise into a dedicated company, 株式会社ギガフォトン Gigaphoton, as a 50/50 joint venture with the lighting and optics specialist ウシオ電機株式会社 Ushio Inc.12 In May 2011, Komatsu bought out Ushio's half and made Gigaphoton a wholly owned subsidiary.13

What Gigaphoton makes is the light engine at the heart of a lithography scanner. Modern chip fabrication uses deep-ultraviolet (DUV) excimer lasers — argon-fluoride (ArF) and krypton-fluoride (KrF) sources — to project circuit patterns onto wafers. Think of a lithography machine as the most precise slide projector ever built: it shines light through a patterned mask to print billions of features on a chip, and the laser is the lamp. Without an exquisitely stable, high-repetition-rate light source, the whole apparatus is inert. Gigaphoton is one of only two companies on earth that build these DUV sources at scale. The other is Cymer — acquired by ASML in 2013 — which means the market for the lamps inside the world's chipmaking machines is, effectively, a duopoly, with Gigaphoton supplying laser sources used across lithography systems from ASML, Nikon, and Canon.

This deserves to be sat with, because it inverts the usual story about Komatsu. In its core business Komatsu is the number two, forever chasing Caterpillar. In DUV light sources it is one of only two players in the world — a structurally stronger competitive position than anything in its earthmoving empire. And the business model has a recurring-revenue quality that the cyclical machine business can only envy: excimer laser chambers degrade with use and are serviced on consumption-based contracts, so every wafer exposure a customer runs generates aftermarket revenue for Gigaphoton. It is a "pay-per-pulse" annuity attached to the secular growth of global chip demand.

The catch — and it is a large one for anyone tempted to value Gigaphoton as a hidden tech unicorn — is that Komatsu does not break it out. Gigaphoton sits inside the "Industrial Machinery and Others" segment, a modest slice of total sales that also contains large metal presses and machine tools, and Komatsu discloses neither Gigaphoton's standalone revenue nor its margins. Assertions that it earns "20%-plus tech-company margins" are plausible given the market structure but are not company-disclosed facts; they are inference. What can be said with confidence is that Komatsu owns a scarce, strategically vital asset in the semiconductor value chain, that it is a natural diversifier against the mining cycle, and that its value is almost entirely obscured inside a segment reported as an afterthought. Unlocking or even illuminating that value is one of the more interesting questions facing the company's new leadership.

VII. The New Guard: Takuya Imayoshi, Capital Discipline & Strategy

Corporate leadership transitions in Japan are usually exercises in continuity, and on the surface Komatsu's April 2025 handover looked like one. 小川 啓之 Hiroyuki Ogawa, president since 2019, moved up to chairman; his predecessor 大橋 徹二 Tetsuji Ohashi stepped back to a senior-adviser role; and 今吉 琢也 Takuya Imayoshi took over as president and chief executive.14 The choreography was orderly. The choice of successor was not entirely conventional.

For most of its history Komatsu's top job has gone to men who came up through engineering and the factory floor — the natural aristocracy of a monozukuri company. Imayoshi came up through finance and accounting. He joined Komatsu in 1985 and cut his teeth in the accounting function at the Awazu plant, the company's spiritual home in Ishikawa, before accumulating more than a decade of international experience across the United States and China. That China posting is the biographical detail that matters most. Imayoshi ran Komatsu's China operations through the wrenching downturn in the country's property and construction markets, a period that demanded exactly the un-heroic skills of a finance chief in a crisis: tightening credit to distributors, downsizing capacity, and protecting the balance sheet from the bad-debt contagion that a construction bust can spread through an equipment maker's receivables. A CEO forged in credit control rather than product design is a meaningful signal about what the board thinks the next decade requires.

That signal is reinforced by the strategy Komatsu unveiled alongside the transition. In April 2025 the company launched a new three-year plan, "Driving value with ambition," covering fiscal 2025 through 2027.15 Its financial spine is telling: an ROE target above 10%, explicitly framed as clearing the cost of shareholders' equity; a cumulative free-cash-flow target of ¥1 trillion over three years; a consolidated dividend payout ratio of 40% or more; and a willingness to conduct "opportunistic" share buybacks balanced against financial soundness.15 The strategic pillars emphasize expanding the value-chain (aftermarket) business, pushing harder into Asian and African markets, developing diverse power sources for the decarbonization transition, and — a very 2025 preoccupation — accelerating AI and digital adoption across the company's own operations.

The language of the plan is worth reading skeptically, because it reveals both an ambition and its own limitation. Setting an ROE floor at "above 10%" and celebrating that it clears the cost of equity is, for a company of Komatsu's quality, a strikingly modest bar — the kind of target a firm sets when its actual constraint is not earning power but capital efficiency. Komatsu's management is, in effect, conceding the central critique that activists and analysts have leveled at Japanese industrials for years: that healthy operating margins can coexist with mediocre returns on equity when the balance sheet is stuffed with idle cash and cross-shareholdings. Imayoshi's mandate, read between the lines, is less to make better machines than to make the same machines generate better returns — and the honest verdict on whether he delivers will not be available for years, which is precisely when management credibility is hardest to assess and most worth watching.

VIII. Risk Radar & Activist Stress Test

Every industrial giant carries a portfolio of risks, but the useful exercise is to separate the risks that are merely real from the risks that are material — the ones with a plausible path to actually impairing the business. For Komatsu, three stand out, and none of them is a generic macro cliché.

The first is the yen, and it cuts both ways with unusual force. Komatsu manufactures heavily in Japan and sells to the world, so a weak yen inflates its reported profits: costs are incurred in cheap yen, revenues collected in expensive dollars and Australian dollars. The extraordinarily weak yen of recent years has therefore been a windfall flattering Komatsu's income statement, and management has been transparent that the FY2025 outlook assumes that tailwind reverses — the company guided to lower sales and profit partly on an expected appreciation of the yen (and on U.S. tariff policy), even as underlying pricing and cost programs improve.1 Investors should be careful not to mistake a currency tailwind for operational excellence: a meaningful share of recent margin expansion is FX translation, not durable competitive gain, and it will fade or reverse when the yen strengthens.

The second is geopolitics, most concretely Russia. Following the 2022 invasion of Ukraine, Komatsu suspended shipments to Russia and halted production at its Yaroslavl plant, exiting a market it had spent years building and absorbing the operational cost of rerouting supply chains and writing down its position there.16 The episode is instructive less for its size — Russia was a modest market — than for what it revealed: a globally distributed industrial is a hostage to political ruptures it cannot forecast, and the next such rupture (a Taiwan contingency, a deepening of U.S.–China decoupling, new tariff regimes) could strike a far larger market than Russia.

The third is the capital burden of decarbonization. Mine operators, under pressure from their own investors and regulators, increasingly demand zero-emission haulage, and Komatsu is committing R&D to battery-electric and hydrogen fuel-cell mining trucks — including recent milestones in autonomously operating an electric-drive truck connected to a dynamic trolley line. The technology is real; the near-term return on it is not obvious. Building the machines of the 2030s is a multi-year drag on returns in the 2020s, with genuinely uncertain payback.

Then there is the activist stress test, and here the argument writes itself. A skeptical long/short investor would note that Komatsu's operating margins are perfectly healthy at around 16%, yet its return on equity has historically clustered in the low-to-mid teens — a fraction of Caterpillar's, which in strong years has run several times higher. The gap is not mainly operational; it is structural. Caterpillar runs an asset-lighter dealer model, carries more leverage, and has for years returned enormous cash through buybacks, mechanically boosting per-share returns. Komatsu, in the traditional Japanese mold, has prioritized cash buffers, employment stability, and stakeholder durability over financial leverage. An activist would call that being overcapitalized and under-optimized, and would push management on why a company this good earns returns this ordinary. Management's new plan is, in effect, a pre-emptive partial answer to that critique — which tells you the critique has landed.

IX. Analysis: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip the narrative away and ask the analyst's cold question: where, precisely, does Komatsu's advantage live, and how durable is it? Two frameworks help pin it down.

Start with Hamilton Helmer's 7 Powers. The clearest power Komatsu possesses is switching costs, and it is strongest exactly where it matters most — mining. A mine that has integrated Komatsu's autonomous haulage and fleet-management software into its operations has effectively rebuilt its production process around Komatsu's system; ripping it out means retraining crews, redesigning pit traffic, and re-instrumenting haul roads, at a cost measured in millions and months. That is a real, evidence-backed lock-in, visible in the stickiness of mining aftermarket revenue. The second power is scale economies, expressed through the global dealer and parts-depot network. A mining machine's value collapses if the spare part or the field engineer is a continent away; only Caterpillar and Komatsu maintain service density at genuinely global scale, and a new entrant cannot replicate two decades of depot investment quickly. The third, weaker, power is a cornered resource: Gigaphoton's excimer-laser patents and the scarce engineering talent behind them, one of only two such capabilities in the world. The honest qualifier is that the first two powers are shared almost symmetrically with Caterpillar — they are industry-structural moats more than Komatsu-specific ones — while the genuinely Komatsu-unique power, Gigaphoton, sits in a business too small and too undisclosed to move the whole company's returns.

Now Porter's Five Forces. The threat of new entrants is low: the capital intensity, the safety-critical engineering, and above all the global distribution network are barriers that have kept the top tier of this industry stable for decades — the disruption, when it came, arrived from Chinese incumbents scaling up at home, not from startups. The bargaining power of buyers is moderate-to-high in a specific way: the giant mining houses — Rio Tinto, BHP, Vale — command enormous purchasing power and negotiate hard, but for the very largest, most autonomy-integrated equipment they face a duopoly, which caps how far they can squeeze. The power of suppliers is unremarkable except in the tight semiconductor components Komatsu itself increasingly depends on for its digital systems. Substitutes barely exist — there is no non-machine way to move a mountain. And rivalry is intense — a permanent, disciplined, two-front technology-and-pricing war with Caterpillar that neither side can end and neither can decisively win. The net picture is an industry with excellent structural characteristics shared by two dominant players, in which Komatsu's task is not to build a moat — the moat exists — but to convert it into shareholder returns as efficiently as its rival does. That is the tension the bull and bear cases fight over.

X. Strategic Position: The Bull vs. Bear Case

Before the arguments, the instruments. For all Komatsu's complexity, three KPIs capture most of what a long-term investor needs to track. First, the aftermarket (value-chain) revenue ratio — whether the parts-and-service share of the equipment segment holds around half or higher, because that ratio is the shock absorber that determines how brutal the next down-cycle feels. Second, the autonomous (AHS) fleet count — the cleanest leading indicator of deepening enterprise lock-in in the highest-margin mining business. Third, free cash flow and capital returns measured against the new plan's ¥1 trillion three-year target and 40%-plus payout — the truest test of whether the capital-efficiency conversion is actually happening or is just slideware.

The bull case rests on three legs. The first is the green-metals supercycle: the energy transition requires vast new supplies of copper, lithium, and nickel, and every ton of that metal has to be dug, hauled, and processed by exactly the equipment Komatsu builds. If the electrification of the world is real, Komatsu is a direct, picks-and-shovels beneficiary of the capex boom that must precede it, with autonomy giving it a differentiated position at the premium end. The second leg is the Gigaphoton option — a scarce, duopoly semiconductor asset generating recurring pay-per-pulse revenue, structurally uncorrelated with mining, sitting undervalued and underappreciated inside a cyclical industrial wrapper. The third is the management turn: a finance-native CEO with an explicit mandate and explicit targets to unwind the cash drag, lift ROE above the cost of equity, and raise cash returns to shareholders.

The bear case is the mirror image of each. On the supercycle: commodity capex is famously lumpy and prone to disappointment, mining customers can defer for years, and a green-metals boom that is perpetually "coming" can leave equipment makers waiting through real quarters. On currency: a meaningful chunk of recent reported profitability is a weak-yen translation effect that will dilute export margins when the yen mean-reverts — a reversal management itself has flagged. On competition: Chinese manufacturers, walled out of a contracting home market, are exporting cheap machines into precisely the developing markets — Southeast Asia, Africa, Latin America — that the bull case counts on for growth, eroding Komatsu's share at the volume end even as it retreats upmarket by choice. And on decarbonization: the necessity of funding early-stage, low-return hydrogen and electric development is a multi-year tax on the very returns the new plan promises to lift.

The synthesis is that Komatsu is neither a cheap turnaround nor a hidden growth stock, but a high-quality cyclical whose central question is governance, not competitiveness. Its moat is real and shared with one peer; its cyclicality is unavoidable; its unique optionality (Gigaphoton) is buried; and its returns have lagged not because it makes worse machines but because it has run a more conservative balance sheet. The bull and bear cases ultimately converge on a single empirical test that only time can settle: will a finance-native CEO actually force a proud monozukuri institution to earn its cost of capital and return its surplus cash — or will Japanese corporate gravity reassert itself the moment the cycle turns down?

XI. Epilogue & Outro

Return, at the end, to where the story started — the driverless truck in the Chilean pit and the excimer laser in the Dutch cleanroom. What makes Komatsu genuinely unusual is not that it does both, but that the same institution that was founded in 1921 to give a depleted mining town somewhere to work now automates the largest mines on earth and supplies light sources to the most advanced factories humans have ever built. The thread from Meitaro Takeuchi's cast-steel shop through Sakane's Dantotsu turnaround to Imayoshi's capital-efficiency mandate is a single, stubborn conviction: that a company which cannot out-scale its rival must out-engineer it, and must do so patiently, across cycles measured in decades rather than quarters.

The surprises, for a firm most people file under "old-economy heavy industry," keep coming. It made telematics free before software-enabled hardware was a category. It timed a major mining acquisition with a discipline its larger rival conspicuously lacked. It quietly holds half of a critical semiconductor duopoly inside a segment it barely discloses. And it has kept a fortress balance sheet through a century of wars, busts, and currency shocks — which is precisely the trait that now draws the sharpest criticism, as investors ask whether so much prudence has become a cost of its own.

The open question that will define the next chapter is not whether Komatsu can build extraordinary machines — that much is settled — but whether it can be persuaded to run itself as hard for its owners as it runs its trucks for its customers. On that question, the evidence is still being written, and it will be worth watching the free-cash-flow line, the autonomous fleet count, and the aftermarket ratio to see which way the story turns.

References

-

Consolidated business results for the fiscal year ended March 31, 2025 (U.S. GAAP) — Komatsu Ltd., 2025-04-28 ↩↩

-

Komatsu Limited — Wikipedia (Caterpillar-Mitsubishi joint venture, 1963; Project A; Deming Prize 1964) ↩↩

-

Turning Things Around for Japanese Companies: An Interview with Komatsu's Sakane Masahiro — Nippon.com ↩↩

-

Komatsu Financial Results & Presentation Materials Archive — Komatsu Ltd. ↩

-

Komatsu Annual (Integrated) Reports Archive — Komatsu Ltd. ↩

-

Komatsu becomes first OEM to commission 1,000 ultra-class autonomous haul trucks — Komatsu Ltd., 2026-04-22 ↩↩

-

Caterpillar to buy Bucyrus in $8.6 billion mining deal — Reuters, 2010-11-15 ↩

-

Caterpillar writes off $580 million on China acquisition — Reuters, 2013-01-18 ↩

-

Japan's Komatsu to buy U.S. mining tool maker Joy Global for $2.9 billion — Reuters, 2016-07-21 ↩

-

Komatsu, USHIO join forces in new excimer laser venture — EE Times, 2000 ↩

-

Komatsu Launched New Strategic Growth Plan (FY2025–FY2027) "Driving value with ambition" — Komatsu Ltd., 2025-04-28 ↩↩

-

Komatsu's suspension of shipments to Russia and production in Russia — Komatsu Ltd., 2022-04-08 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube