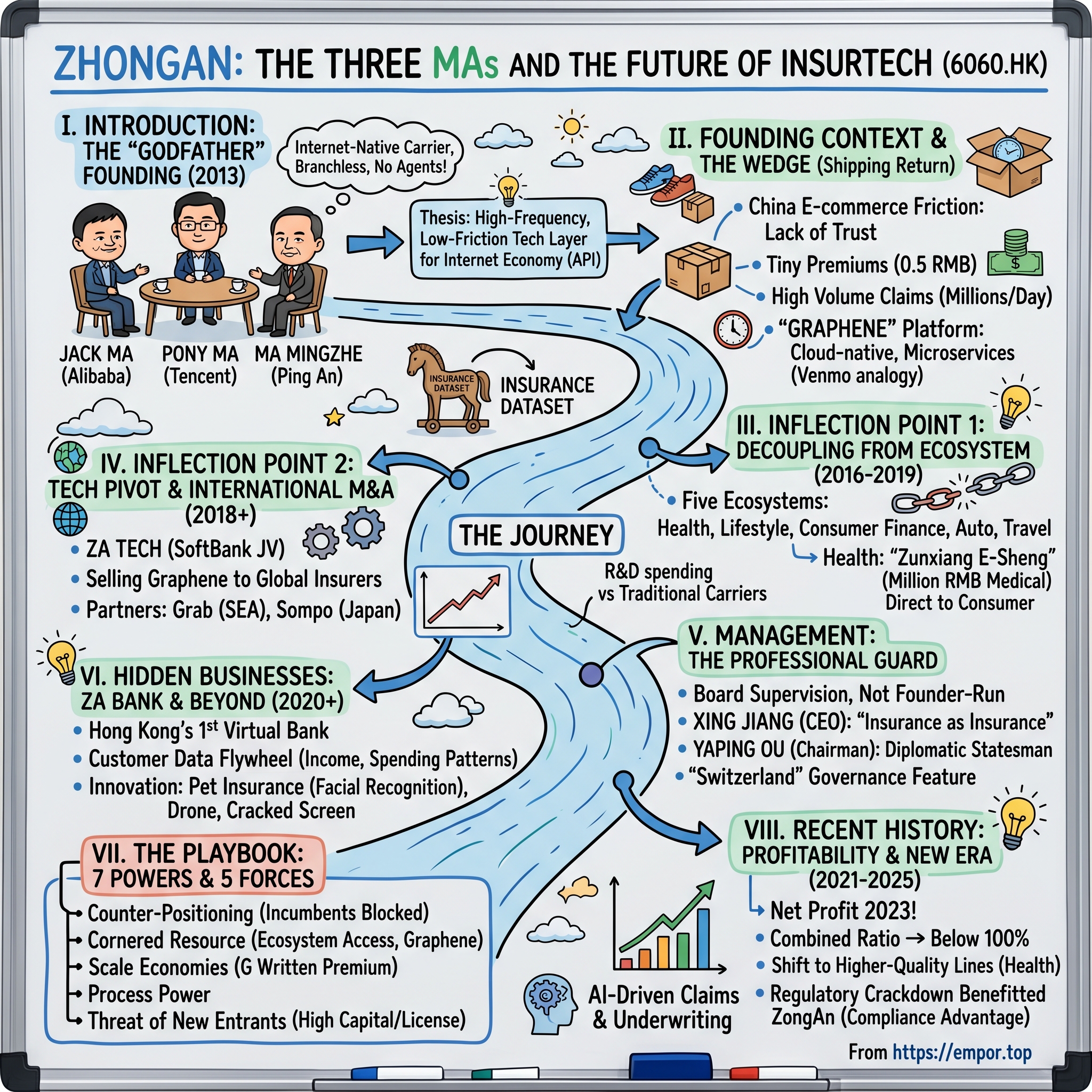

ZhongAn: The Three Mas and the Future of Insurtech

I. Introduction: The "Godfather" Founding

Picture a conference room in Shanghai in the autumn of 2013. The three most powerful men in Chinese business are all in the same room, which, if you know anything about Chinese corporate dynamics, almost never happens. Jack Ma, the irrepressible English teacher turned e-commerce czar of Alibaba, is the loudest voice. Pony Ma, the famously reticent engineer behind Tencent and WeChat, watches quietly from across the table. And Ma Mingzhe, the buttoned-up, fiercely competitive founder of Ping An Insurance, who built a financial services empire from a small Shenzhen outpost in 1988, is already thinking about capital ratios and solvency margins.

They are not merging their companies. They are not swapping equity. They are, of all things, creating an insurance company together. No offices. No agents. No paper. Just an internet-native carrier that would live inside the Alipay checkout button, the WeChat wallet, and the Ping An app.

It was audacious for two reasons. First, three fiercely competitive empires were agreeing to ride the same horse. Second, the regulators of the China Insurance Regulatory Commission—a body that had never before approved a purely online, branchless insurance carrier—signed off on it. On November 6, 2013, the license was granted. The company was called Zhong An Online Property & Casualty Insurance, and it opened for business with a total registered capital of just over one billion yuan.

The thesis that animates this entire story is deceptively simple. ZhongAn is not really an insurance company, not in the way Aetna or Allianz or even Ping An is an insurance company. It is a high-frequency, low-friction technology layer for the internet economy. It is what happens when you take the core actuarial and risk-pricing machinery of insurance, compress it into an API, and drop it into every digital transaction that touches a Chinese consumer.

That framing matters because it explains almost every decision ZhongAn has made in the years since. The decision to sell micro-policies for pennies. The decision to run a cloud-native core system when every incumbent ran mainframes. The decision to launch a virtual bank in Hong Kong. The decision to export its technology stack to Japan, Singapore, and Southeast Asia rather than hoard it as a competitive advantage.

Here is the roadmap for this episode. We start with the wedge—the now-famous shipping return insurance that turned ZhongAn from a curiosity into a claims-processing juggernaut overnight. Then we trace the two great pivots: first, the decoupling from the founding ecosystems into a direct-to-consumer health and lifestyle brand; second, the pivot from technology consumer to technology vendor. We examine the management structure, which is quietly one of the more interesting governance experiments in Chinese finance. We go deep into the "hidden" businesses, particularly ZA Bank, the first licensed virtual bank in Hong Kong. And then we zoom out to the strategic frameworks—Hamilton Helmer's 7 Powers and Porter's 5 Forces—to understand whether the moat is real, or whether ZhongAn is just a clever feature hitching a ride on two giants.

Because here is the question that hangs over the entire story. When you are born from the loins of Alibaba, Tencent, and Ping An, are you a company, or are you a joint venture that has been allowed to pretend to be a company? The answer, which ZhongAn has spent twelve years trying to prove, turns out to be more interesting than either. Let's begin at the beginning.

II. Founding Context & The Wedge: The Shipping Return Era

To understand why a shipping return insurance policy was one of the most elegant business ideas of the last two decades, you have to understand what Chinese e-commerce actually felt like in 2011 and 2012. Taobao, Alibaba's consumer-to-consumer marketplace, was exploding in gross merchandise value. But every transaction carried a tax—not a literal one, but a psychological one. The buyer did not trust the seller. The seller did not trust the buyer. And the courier, well, nobody trusted the courier.

If you bought a pair of shoes for forty-five yuan on Taobao and they arrived too small, you had a choice. Either you kept shoes that didn't fit, or you paid another fifteen yuan to ship them back. On a forty-five yuan purchase, that is a thirty-three percent tax on being dissatisfied. And for sellers, returns were a nightmare in reverse—arguments over who bore the shipping cost destroyed seller ratings, which destroyed their ranking in Taobao search, which destroyed their business.

Alibaba had tried everything to solve this. Buyer protection programs. Escrow through Alipay. Seller rating systems. Each of these reduced friction but none removed it. What was needed was a financial instrument—an insurance policy—that would pay the buyer the shipping cost automatically if they returned the item. Essentially, underwrite the psychological cost of a bad purchase.

The problem was that no traditional insurer would touch it. The premium was tiny—typically half a yuan to a yuan per policy, about eight to fifteen U.S. cents. The administrative cost of writing, underwriting, and settling a traditional insurance policy was many multiples of that. A legacy insurer's core system, usually some vintage mainframe running COBOL or early Java stacks, might be able to process a few hundred claims per hour. Taobao was generating millions of transactions per day, and on Singles' Day—the November 11th shopping festival invented by Alibaba—tens of millions in a single day.

This was the wedge. ZhongAn's first product, "shipping return insurance," sold for as little as 0.5 yuan and paid out a reimbursement of up to a few dozen yuan if the buyer returned the goods. The unit economics were laughable by traditional standards—margins so thin that any manual intervention would incinerate them. But that was precisely the point. ZhongAn did not have a single manual process. Every policy was underwritten by algorithm, issued by API call, and settled via Alipay directly into the buyer's account, usually within minutes.

The volume was unprecedented. In ZhongAn's first full year of operation, it underwrote hundreds of millions of policies. By 2016, the company was reportedly issuing billions of policies annually, most of them shipping-related, each one a micro-event generating a data point about a consumer, a seller, a SKU, a logistics route, and a return behavior. ZhongAn was, in effect, building the largest consumer-behavior-meets-financial-transaction dataset in China, one forty-cent policy at a time.

The technology that made this possible was branded internally as "Graphene," a cloud-native, microservices-architected core insurance platform that the company built from scratch. The name was deliberate—graphene is the thinnest, strongest material known to materials science, and ZhongAn wanted to convey that its stack was both lightweight and load-bearing. Unlike legacy insurers who treated their IT as a cost center, ZhongAn treated it as the product.

For a listener who doesn't think about insurance technology for a living, here is a simple analogy. Imagine the difference between writing a check by hand, and Venmo. A traditional insurer's policy administration is the handwritten check—slow, costly, requires a human at every step. Graphene was Venmo. The value of the individual transaction is trivial, but the volume and velocity create an entirely new financial instrument class.

And this is what the founders understood that most people missed. The shipping return policy was not a business in the conventional sense. It was a Trojan horse for something much larger—a computational layer that, once built, could price, issue, and settle risk on almost any microtransaction in the digital economy. That realization would, within four years, take ZhongAn from an experimental venture funded by three billionaires to the first Chinese insurtech to list on the Hong Kong Stock Exchange.

III. Inflection Point 1: Decoupling from the Ecosystem

There is a moment in every platform-born company when the founders look at their revenue mix and feel a cold knot in their stomachs. For ZhongAn, that moment came sometime in 2015, two years into operations, when the reality of their dependence became impossible to ignore. In the year leading up to the Hong Kong IPO, the company's prospectus disclosed that a staggering share of gross written premiums flowed through the Alibaba and Tencent ecosystems. Shipping return alone accounted for a huge chunk of policies, and shipping return only existed because Taobao existed.

If Jack Ma woke up one morning and decided that Ant Financial—as it was then called—should start its own captive insurer, ZhongAn's business would evaporate overnight. If Pony Ma decided WeChat Pay should own the lifestyle insurance layer, same problem. Even the small portion funneled through Ping An's ecosystem was dependent on the goodwill of Ma Mingzhe, who had competing priorities in his own P&C operation. The three godfathers had given birth to ZhongAn, and in principle they could also strangle it in its crib.

The strategic response, which unfolded roughly from 2016 through 2019, was one of the more interesting pivots in Chinese internet finance. ZhongAn's leadership—initially Chairman Yaping Ou and a rotating cast of CEOs including Chen Jin and later Xing Jiang—began to articulate an internal doctrine of "five ecosystems." Lifestyle consumption, consumer finance, health, auto, and travel. The idea was that while Alibaba and Tencent would always be critical distribution channels, ZhongAn would build its own brand in verticals where consumer trust—not platform access—was the binding constraint.

The most consequential of these ecosystem moves was health. In 2016, ZhongAn launched "Zunxiang E-Sheng," or "Personal Health," a million-RMB medical expense cover that, in one stroke, established ZhongAn as a retail consumer brand. The product was brilliant. For a premium that could be as low as a few hundred yuan a year for a young policyholder, you got a high-deductible medical insurance policy with an annual cap of one million yuan (around 140,000 U.S. dollars) for major medical expenses. In a country where the state medical system covers only the basics and serious illness bankrupts families, this was transformative.

But the product was only half the story. The real innovation was distribution. ZhongAn sold Zunxiang E-Sheng directly through its own app, through WeChat public accounts the company controlled, and through a mini-program inside WeChat. Consumers did not experience it as "ZhongAn sold through Tencent." They experienced it as "I bought this from ZhongAn." That subtle shift—from embedded product to trusted brand—changed the valuation logic of the entire company.

By 2018 and 2019, health insurance was catching up to lifestyle as a proportion of total gross written premium. By 2020 and 2021, health had overtaken lifestyle entirely in many quarters, and the company was widely recognized as the leader in online medical insurance in China, competing with Taikang Online, Ping An Health, and a field of state-owned insurers that had been slow to adapt.

There is a second dimension to this decoupling worth lingering on. When ZhongAn sold policies through Alibaba, Alibaba took a platform fee. When ZhongAn sold a policy directly, there was no fee. Unit economics on health and other direct-to-consumer products were structurally better than on the embedded wedge products. This is the insurance version of the classic internet playbook—build audience on someone else's rails, then migrate them onto your own.

For investors, this period was when ZhongAn stopped being a "feature" and started being a "company." The narrative shifted from "interesting insurtech experiment backed by Three Mas" to "largest digital insurer in China with a diversified product portfolio." It also set up the next question, which became the defining issue of the 2017-2020 period. If you have built the best insurance technology stack in China, should you keep using it yourself, or should you start selling it to everyone else? That question would take ZhongAn into a global pivot that almost nobody saw coming.

IV. Inflection Point 2: The Tech Pivot & International M&A

In a conference room in Hong Kong sometime in 2018, Xing Jiang and a small cross-functional team sat down with executives from SoftBank's Vision Fund. On the table was an idea that, if you squinted, looked like the most audacious strategic expansion in the history of Asian insurance, and if you squinted differently, looked like a company that had run out of things to do in China and was hunting for a second act.

The idea was ZA International, later rebranded ZA Tech, a joint venture that would take ZhongAn's "Graphene" cloud-native insurance core and sell it to insurers around the world. Not just license it. Actually deploy it, operate it, and capture a share of the resulting premiums. SoftBank came in with capital, and the joint venture moved aggressively across Southeast Asia and into Japan.

You have to appreciate the pivot here. In 2016, ZhongAn Technologies was carved out as a separate unit inside the company whose mandate was essentially to productize the internal stack. By 2018, the plan was to take that productized stack, joint-venture it with the largest technology investor in the world, and sell it as a SaaS-in-a-box to other insurance markets. The premise was that Southeast Asia, Japan, and parts of Europe were roughly where China had been in 2013—high smartphone penetration, low insurance density, legacy carriers stuck on mainframes, and no digital-native challenger.

The customer list that ZA Tech assembled by 2020 reads like a who's who of Asian digital commerce. Grab in Singapore and across Southeast Asia, which used ZA Tech's stack to power its embedded insurance offerings for drivers and riders. Sompo in Japan, a century-old Japanese P&C giant that, astonishingly, chose a seven-year-old Chinese company's technology to underpin its digital transformation. NTUC Income in Singapore. Various partners in Thailand, Malaysia, and Vietnam.

The capital-light nature of this business model was crucial. ZA Tech did not take on the insurance risk. It sold the plumbing. The actual premium sat on Grab's or Sompo's books, subject to their capital and solvency rules. ZA Tech took a SaaS or transaction-based revenue stream. In the language of investors, it was the shovels-not-gold play, and it had the potential to turn ZhongAn from a China-only insurer into a global infrastructure company.

Benchmarked against global peers, ZhongAn's commitment to technology is easy to identify in the financials, even if some of the specific ratios fluctuate year to year. The company has disclosed research and development spending consistently in the high single-digit to low double-digit percentage of gross written premium range, a level that would be considered either heroic or reckless at a traditional carrier. AXA and Allianz, the European incumbents ZhongAn is most often compared with on scale, spend a far smaller share of premium on technology. For ZhongAn, the R&D line is not a cost center. It is the product line.

The natural question every investor asks is whether ZhongAn overpaid for this international growth. The answer, as of 2025 and early 2026, is ambiguous. ZA Tech did not scale as fast as the most bullish scenarios projected. Insurance is a heavily regulated industry, and selling "insurance-in-a-box" to a Japanese carrier with 150 years of legacy systems is a multi-year implementation cycle, not a SaaS six-week onboarding. Revenue contribution from international technology services to ZhongAn group remained a minority of total income through 2024, and the joint venture's profitability profile has been lumpy.

But the strategic optionality is what matters. By being an early technology vendor to Sompo, Grab, and others, ZhongAn has embedded itself in a network of relationships that would be very expensive to replicate. The comparison you sometimes hear is to Stripe or Adyen—payment rails that started with a core market and expanded globally by becoming the default infrastructure for their category. Whether ZhongAn becomes the Stripe of insurance is an open question, but the fact that it is an actual question, not a marketing slogan, is itself a significant development.

What makes this pivot especially interesting is what it says about management's willingness to redefine the business. Most insurers never make the leap from operator to vendor. They protect their technology as a source of competitive advantage. ZhongAn instead treated technology like venture capital—something that compounds in value the more customers it serves, not the more it is hoarded.

That willingness to rewrite the identity of the company is a recurring theme, and it leads directly to the question of who actually runs ZhongAn and how they think.

V. Management: The Professional Guard

If you visit ZhongAn's headquarters in Shanghai today, you will not find a founder-CEO who can fit the origin story on a single slide. You will not find a Jack Ma character giving motivational speeches to thousands of employees. What you will find is something that, in the context of Chinese tech, is almost unusual. A professionally managed, board-supervised insurance technology company whose senior leadership is drawn from a mix of traditional financial services and technology executives, and whose largest shareholders sit on the board but do not run the day-to-day.

The current Chief Executive Officer, Xing Jiang, is the defining figure of the present era. Jiang came up through the insurance and financial services side, with roles at Ping An group companies, and joined ZhongAn during the critical transition years. His leadership style, as colleagues and market participants have described it in Chinese financial press, emphasizes underwriting discipline, capital allocation, and what he has publicly called "insurance as insurance," not insurance as a loss leader for technology. That phrase—insurance as insurance—captured a deliberate pivot away from the 2017-2019 mindset that tolerated underwriting losses in pursuit of growth.

The Chairman, Yaping Ou, has been a stabilizing presence through the company's various inflection points. Ou's profile is less that of a founder-visionary and more that of a senior statesman of the Chinese financial sector. He came from an investment and financial services background, and has served as the long-running figurehead connecting the company's institutional shareholders to its executive team. The combination of a detail-oriented CEO on operations and a diplomatic Chairman on governance is, in some ways, exactly what an insurance company needs, and not what a pure tech company might naturally gravitate toward.

This structural hybrid—professional management layered on top of a three-godfather founding coalition—is ZhongAn's unique governance experiment. Ant Group retains a significant minority stake. Tencent retains a significant minority stake. Ping An retains a significant minority stake. None of them alone controls the company. And because each of them is a potential competitor in adjacent verticals, none of them can push ZhongAn too hard in a direction that would only benefit itself. This is what some Hong Kong analysts have called the "Switzerland" feature of ZhongAn—neutral, useful to all three, beholden to none.

Incentives, however, are where things get interesting. ZhongAn operates in the low single-digit to mid-teens price-to-earnings world of insurance when its underwriting is profitable, and in the high revenue-multiple world of technology when investors focus on the Graphene and ZA Tech narratives. Managing employees across both worlds is a real challenge. Insurance executives typically get paid via steady salaries and long-dated bonuses tied to combined ratios and return on embedded value. Technology executives typically get paid through equity that vests over four years and compounds with the stock.

ZhongAn has attempted to bridge this through its employee share ownership schemes, including restricted share unit plans and share award programs that align management and technical staff with long-term share price performance. The company has disclosed employee incentive plans in its annual reports, though the specific structures and vesting schedules have varied over time. The honest read is that it is easier to say "insurance plus technology" in a strategy deck than to compensate people who actually work at the seam.

One specific second-layer diligence point worth flagging. The ownership structure means that any material event at Ant Group, Tencent, or Ping An—regulatory actions, strategic pivots, or ownership changes—creates a second-order effect at ZhongAn. When Ant Group's IPO was suspended in November 2020 and the company was subsequently restructured under regulatory pressure, ZhongAn's narrative around ecosystem distribution was affected. That episode did not fundamentally impair the business, but it was a reminder that three shareholders, each themselves exposed to Chinese regulatory and political risk, sit at the top of the cap table.

For a long-term investor, the question is not "is management good?"—they are credentialed and disciplined—but "is the governance structure stable?" And the answer, based on more than a decade of track record, appears to be that yes, the Switzerland logic holds. The three Mas, or their successor institutions, continue to benefit from a shared portfolio asset more than they would benefit from unwinding it. That equilibrium has held through CEO transitions, regulatory crackdowns, and a pandemic. It is not guaranteed to hold forever, but it is the single most important thing to watch for anyone underwriting this company.

Which brings us to the parts of ZhongAn that most investors don't fully price because they are hidden inside the group structure.

VI. Hidden Businesses: ZA Bank & Beyond

On March 24, 2020, in the middle of a global pandemic, a new digital bank opened its doors in Hong Kong. Or rather, it opened its app. ZA Bank, a wholly-owned subsidiary of ZhongAn's international technology arm, became the first of Hong Kong's eight newly licensed virtual banks to go fully live for customers. Within days, it was offering a demand deposit rate of 1% and above, at a time when traditional Hong Kong banks were paying closer to nothing, and it signed up tens of thousands of customers in its first weeks.

The first obvious question, and the question every analyst asked, was this. Why is an online property and casualty insurance company from Shanghai running a digital bank in Hong Kong?

The answer reveals a lot about how ZhongAn's leadership thinks about the adjacency between finance and data. Insurance underwriting, in its modern form, is fundamentally a data problem. The better your view of a customer's financial life—their income stability, their savings behavior, their spending patterns, their credit profile—the more accurately you can price their risk. Banks have the best view of these things, historically, because they sit in the middle of the cash flow. Insurers have a worse view, traditionally, because they only see the customer at the moment of policy purchase and, if unlucky, at the moment of claim.

By owning a bank, ZhongAn was buying, in effect, a front-row seat to a segment of customers' financial lives. The Hong Kong context was specifically chosen because Hong Kong is a regulatory testing ground—small enough to experiment in, sophisticated enough to generate proof points, and a bridgehead for eventual expansion into Southeast Asia where digital banking licenses were starting to be issued around the same time period.

ZA Bank has since grown aggressively. By 2024 and into 2025, it had become the largest of Hong Kong's virtual banks by customer count, crossed the 800,000 customer mark at various reporting milestones, and built out wealth management, small business lending, and crypto-adjacent services (offering retail investors access to digital asset trading via licensed partners). The bank has also been candid about the capital cost of the journey. Virtual banks in Hong Kong, as a category, burned significant capital in their first five years building scale, and ZA Bank has not been immune. The group has regularly injected additional capital into the HK operations.

The synergy story is partly about customer acquisition cost. For a standalone insurer to acquire a high-quality Hong Kong consumer costs significant money in marketing, broker commissions, and digital advertising. A bank customer who has already downloaded the ZA Bank app and gone through Know-Your-Customer onboarding is, at the margin, cheap to cross-sell an insurance product to. And an insurance customer with a claim history is a very informative input to a bank's credit decisioning. The data flywheel, in principle, compounds.

Beyond ZA Bank, the "Digital Life" segment inside ZhongAn China is a perpetual source of interesting product innovation. Pet insurance underwritten using facial recognition on dogs and cats—yes, really—because pet insurance historically struggles with identity fraud; policyholders switch pets and claim on the new one. Drone insurance for the increasingly common commercial and hobbyist drone market. "Cracked screen" insurance for smartphones, bundled with device purchase and activated via the insured's own phone camera. Delivery insurance for food couriers. Travel disruption insurance for flights, auto-triggering payout if the flight is delayed beyond a threshold, with no claim submission required.

Each of these products, individually, is small. Collectively, they make up the "Digital Life" segment that, along with Consumer Finance insurance (coverage sold with various lending and installment products) and the legacy E-commerce Lifestyle line, represents the non-Health part of ZhongAn's domestic business. What they demonstrate is an almost anthropological commitment to finding new microtransactional insurance moments in the digital economy and underwriting them at scale.

The elegant observation about this cluster of businesses is that none of them, individually, would survive as a standalone product at a traditional insurance company. The distribution cost would swamp the premium. But because ZhongAn has already built Graphene, each new product is a marginal configuration on top of existing infrastructure. The cost to launch a new microinsurance product at ZhongAn is closer to the cost of launching a new SKU at Amazon than the cost of launching a new policy at Chubb.

When you add this all up—a domestic P&C insurer, a digital bank in Hong Kong, a technology SaaS vendor across Asia, and a portfolio of microinsurance product categories that only make economic sense in aggregate—you get a company that does not fit cleanly into any standard financial services taxonomy. That messiness is both the opportunity and the risk, which is exactly what we'll interrogate next through a structured strategic lens.

VII. The Playbook: 7 Powers & 5 Forces

Strategy frameworks are often deployed as post hoc rationalizations, but in ZhongAn's case, Hamilton Helmer's 7 Powers and Porter's 5 Forces genuinely illuminate where the durable economics come from and where the pressure points are. Let's walk through them, and then let's zero in on what matters.

Counter-positioning is the single most powerful moat in the ZhongAn story. Legacy Chinese insurers—PICC, China Life, Ping An's own traditional P&C operation, China Pacific—cannot become ZhongAn without cannibalizing themselves. They employ hundreds of thousands of agents. Those agents are organized into cascading sales hierarchies that pay out commissions multiple layers deep. The moment a legacy insurer routes business primarily through a cloud-native, agentless, direct-to-app channel, it undermines the livelihoods of the very people who have built its distribution. This is the classic incumbent's dilemma. Christensen would call it the Innovator's Dilemma; Helmer calls it counter-positioning. Either way, ZhongAn benefits from the fact that its competitors cannot follow without breaking themselves.

Cornered resource is also genuinely present, though more subtle. The Graphene technology stack, built over more than a decade with hundreds of millions of yuan in annual R&D, is not something that can be cloned in eighteen months. More importantly, the ecosystem access—preferred partnerships or at least deeply integrated technical connections with the Alibaba, Tencent, and Ping An ecosystems—is a resource no other insurer can easily acquire. Competitors like Taikang Online or the insurance arms of JD.com have built similar capabilities, but none with the same three-godfather coverage.

Scale economies are real but nuanced. In insurance, the classic scale economies come from the law of large numbers in risk pooling and from fixed distribution cost amortization. ZhongAn has both, plus a third form that is more technology-like. When Graphene processes billions of policies, the marginal cost of processing policy one billion and one is effectively zero. The per-policy compute cost for a microinsurance product at ZhongAn is likely well under a cent. No legacy insurer can match that, and even a well-capitalized new entrant would take years to get there.

Process power is worth noting. ZhongAn has built institutional muscle around very fast product iteration. A new product category can be designed, priced, approved, and distributed in weeks rather than the quarters or years it takes at a traditional carrier. This is cultural and organizational, not just technological, and it is very hard to replicate.

The remaining 7 Powers—switching costs, network economies, and branding—are partially present but not the dominant moat. Switching costs on a micro-policy are essentially zero; consumers move between insurers easily. Branding is meaningful in the health segment, where ZhongAn has built real consumer trust, but less so in embedded products. Network economies are present through the data flywheel but are not a two-sided network in the classic sense.

Turning to Porter's 5 Forces, the first one—bargaining power of suppliers and distribution channels—is where the real stress test lies. Alibaba and Tencent are not suppliers in the traditional sense, but their platforms function as critical distribution channels for a meaningful share of ZhongAn's premium volume, and they have the power to change terms. The direct-to-consumer pivot discussed earlier was explicitly designed to reduce this force. It has worked to a degree, but the dependence is not zero, and platform dynamics can shift quickly.

Threat of new entrants is probably the single most underappreciated force working in ZhongAn's favor. Chinese insurance regulation has high capital requirements, and the licensing bar for a purely online insurer is extremely high. The fact that ZhongAn received the first such license in 2013 was a specific regulatory moment; it has not been easily repeated. International markets where ZA Tech operates have their own licensing regimes that act as barriers to entry for new competitors. And in Hong Kong, the virtual bank licensing batch from 2018-2019 is, by regulatory intent, not repeating soon.

Bargaining power of customers is low for most products. Microinsurance customers have limited negotiating leverage on a fifty-cent policy. Health insurance customers care more about claim payout reliability than premium shopping; ZhongAn's claim settlement speed, automated for a meaningful share of claims, is a competitive advantage that commands loyalty rather than extracts price sensitivity.

Threat of substitutes depends on the product. For shipping return insurance, Alibaba's own "worry-free return" guarantees are a substitute. For health insurance, state medical coverage plus commercial competitors are substitutes. For virtual bank deposits, HSBC and Standard Chartered are substitutes. Each of these is manageable because ZhongAn competes on features and user experience, not primarily on price.

Competitive rivalry is the complicated one. Within Chinese online insurance, there is real competition from Taikang Online, Ping An Health (a related-party situation given the Ping An shareholding in ZhongAn), and several state-owned insurer online arms. Internationally, ZA Tech competes with Western insurtech vendors like Duck Creek, Guidewire, and a long tail of regional players. The rivalry is intensifying, not diminishing.

Netting it all out, the single most distinctive strategic feature is the combination of counter-positioning against legacy incumbents and regulatory moat against new entrants. That combination is powerful because it means the most natural competitors—both the ones who would use their existing infrastructure to attack, and the ones who would start fresh—are each blocked by different structural factors. Whether the moat deepens over time depends on execution, which brings us to the most recent chapter of the story.

VIII. Recent History: Profitability & The New Era

The narrative arc of ZhongAn from 2021 to 2025 is almost a textbook case of a growth-at-all-costs company learning the discipline of underwriting profit. For several years following the 2017 Hong Kong IPO, the company grew gross written premium aggressively—into the tens of billions of yuan—but posted combined ratios above 100%, meaning it was paying out more in claims and expenses than it was collecting in premiums. Underwriting losses were partly offset by investment returns on the float and by growth in the technology segment, but the core insurance business was, in accounting terms, subsidizing the growth.

In 2020 and 2021, the company began a deliberate pivot. Xing Jiang, along with the board, publicly committed to improving the combined ratio toward and below 100%, even at the cost of slower premium growth. The discipline showed up in several places. Product mix shifted toward higher-quality lines, particularly in health. Underwriting controls tightened on consumer finance insurance, where default-linked products had been hit by the broader Chinese deleveraging cycle. Claims processing automation was further optimized to reduce loss adjustment expense ratios.

By 2023, the fruits of this discipline were visible. ZhongAn reported its first full-year net profit in several years, and the combined ratio had trended to approximately breakeven or slightly better on the domestic insurance business. By 2024 and into 2025, the company consolidated this profitability, though results remained sensitive to specific large events—weather-related claims, a resurgence of claim severity in specific categories, or investment portfolio marks in volatile quarters. The 2024 annual report and the 2025 interim disclosures confirmed the trajectory, and the market rewarded the discipline with a meaningful rerating of the stock off its 2022 lows.

The macroeconomic and regulatory context of this period is a story in its own right. From late 2020 through 2023, the Chinese government's crackdown on the technology and platform economy reshaped the landscape in which ZhongAn operated. Ant Group's IPO suspension in November 2020 and subsequent restructuring was the opening act. Didi, Meituan, and a long list of platform companies followed. In the insurance sector specifically, regulators tightened rules on online sales of certain products, cracked down on mis-selling, and required stricter disclosure and consumer protection practices.

The counterintuitive read, which management has articulated in investor communications and which has proven largely correct, is that the regulatory crackdown helped ZhongAn. Why? Because the smaller, shadier online insurance brokers and platforms—the ones selling through livestreaming, WeChat groups, and aggressive direct marketing—were forced out of the market or brought under tighter supervision. A licensed, well-capitalized, board-governed insurer with a direct relationship to regulators was structurally favored by the new regime. ZhongAn's discipline on compliance and capital looked less like cost and more like competitive advantage.

There have been, of course, challenges. The Chinese property market downturn starting in 2021-2022 created ripple effects across consumer finance, which impacted credit-related insurance lines. The broader Chinese consumer sentiment weakened, which compressed discretionary insurance purchases in certain lifestyle categories. The ZA Tech international business scaled more slowly than initial projections, though it reached meaningful revenue contribution by 2024-2025. ZA Bank required continued capital support through its growth phase.

Looking at the business as it stands in the spring of 2026, the profile is materially different from what it was five years ago. ZhongAn is now, unambiguously, a profitable digital insurer with a diversified domestic premium base, a scaled health insurance franchise, a growing technology export business, and a maturing digital bank in Hong Kong. The combined ratio is disciplined. Solvency is robust. And the forward agenda—AI-driven claims processing at yet higher automation rates, further international expansion of ZA Tech, product deepening in health and wealth management via ZA Bank—is internally consistent with what the company has been building for a decade.

The specific technology frontier worth watching is AI-powered underwriting and claims. By 2024 and into 2025, ZhongAn had publicly disclosed the use of large language model-based systems for customer service, claims triage, and underwriting document processing. The company's willingness to deploy these capabilities at scale, rather than in proof-of-concept mode, is another differentiator. The practical effect is that as AI claims processing expands, ZhongAn's operating leverage expands with it. Each incremental policy can be handled at a lower marginal cost, which is structurally good for combined ratios.

Having walked through the history and the present, the final synthesis question is whether all this adds up to a durable business that can compound shareholder value over the next decade, or whether it remains a strategically interesting but structurally challenged asset. That is the bull-bear debate worth having.

IX. Analysis: Bear vs. Bull Case

The bear case on ZhongAn starts with the observation that you cannot fully escape the fact that insurance, at its core, is a regulated, capital-intensive, commoditized business. Yes, you can wrap technology around it. Yes, you can distribute it more efficiently. But the fundamental economics of insurance—you collect premium, you invest the float, you pay claims, you hope the math works—have not changed in three hundred years. And for a company like ZhongAn to trade at a valuation that reflects technology multiples, the technology segment has to do a lot of the heavy lifting of the story.

The bear would point out that ZA Tech's international business, while strategically interesting, has not grown to the scale where it meaningfully changes group economics. The revenue base remains dominated by Chinese insurance premiums. International SaaS contracts with Grab, Sompo, and others are real, but their total contribution to ZhongAn's top line remains a minority share. If you underwrite ZhongAn purely on the domestic insurance P&L, you get an insurance valuation, and insurance valuations in Asia are not generous.

A second bear point focuses on ZA Bank. Virtual banks in Hong Kong have, as a cohort, absorbed significant capital and not yet produced consistent standalone profitability. ZA Bank is the leader in its category, but leadership in a category that has not yet proven the unit economics is a mixed blessing. The synergy story with insurance is compelling conceptually; the realized cross-sell economics are harder to verify externally. A cautious investor would give ZA Bank modest terminal value until the path to standalone profitability is clearly demonstrated.

Third, the valuation identity crisis is real and not easy to resolve. When the market is bullish on Chinese tech, ZhongAn trades like a tech stock, and the share price runs up on multiples that pure insurance cannot support. When sentiment sours—as it did broadly during 2022-2023—the stock trades back to something closer to an insurer's multiple, and suffers accordingly. This oscillation creates volatility that is painful for investors who cannot time it, and it suggests that the market itself has not made up its mind what kind of company this actually is.

Fourth, and most structural, is the dependence risk. Even with the direct-to-consumer pivot, a large share of gross written premium continues to pass through the ecosystems of Alibaba, Tencent, and the broader Chinese digital commerce infrastructure. If platform terms shift meaningfully—if Ant Group decides to invest in its own captive insurance capabilities, if WeChat channel economics change, if regulatory changes force a repricing of platform distribution—ZhongAn's embedded revenue is exposed.

Now the bull case. The bullish read begins with the observation that ZhongAn is the most efficient insurance manufacturing platform in the world, and that as insurance goes digital globally, it has the longest head start and the most battle-tested infrastructure. Graphene is not a deck; it is a production system that has processed billions of policies. ZA Tech's customer list is not a prospect list; it is a live deployment list at tier-one Asian insurers and platforms. The combined position is not easily replicable.

Bull point two is the counter-positioning moat, which, as argued earlier, is the most durable form of strategic advantage in the Helmer framework. Legacy insurers cannot become ZhongAn without destroying their own distribution models. New entrants face enormous regulatory capital requirements and a decade-long technology build. ZhongAn sits in a strategic space that is structurally protected on both sides.

Bull point three is optionality. ZA Bank, whatever its current profitability profile, gives ZhongAn a financial identity layer that traditional insurers can never build. Every ZA Bank customer is, over time, a richer dataset than any actuary at a 100-year-old insurer has ever seen. If even one of the adjacent opportunities—digital wealth management, cross-border payment-linked insurance for Greater Bay Area consumers, AI-underwritten SME insurance—scales, the economics shift materially. Optionality is hard to price, which means it is often underpriced.

Bull point four is the management and governance stability. In a Chinese corporate landscape where founder-CEOs are, depending on the year, either celebrated or disappeared, a professionally managed insurer with three institutional shareholders and a disciplined board is a rarer and more valuable asset than it looks. The Switzerland logic has held through multiple regulatory cycles, and there is no obvious catalyst that breaks it.

Bull point five, and the one that ties everything together, is that ZhongAn is simultaneously selling the shovels and digging the gold. Most digital platforms either sell infrastructure to third parties, or use infrastructure to serve end customers. ZhongAn does both. That combined model generates information asymmetry—the company knows, from both its vendor relationships and its operator experience, where insurance risk is actually being priced correctly and where it is not. Over time, that asymmetry should translate into superior capital allocation, both within ZhongAn and in selecting which ZA Tech customers to prioritize.

For long-term investors, the three key performance indicators to focus on are these. First, the combined ratio of the domestic insurance business; this is the core profitability metric, and the trajectory toward and below 100% is the single most important number to watch quarter over quarter. Second, the gross written premium growth rate in the health segment specifically; this captures the direct-to-consumer franchise strength and the decoupling from platform dependence. Third, ZA Bank customer growth and net interest margin; this captures the optionality of the non-insurance bet and whether the adjacent businesses are adding value or absorbing it.

Everything else—the international expansion, the AI capabilities, the product mix shifts—shows up eventually in those three numbers. If combined ratio is disciplined, if health premium grows, and if ZA Bank scales toward profitability, the bull case wins. If any one of those three breaks, the bear case has its evidence.

X. Conclusion & Lessons

There is a lesson in ZhongAn's story that is easy to state and hard to internalize. The wedge matters more than the vision. When the Three Mas sat down in 2013, they did not start by trying to insure a factory, a ship, or a corporate liability program. They started by insuring a two-dollar pair of socks. They picked the smallest, highest-frequency, most algorithmically-tractable insurance transaction in the entire digital economy, and they built the infrastructure to do it at enormous scale.

Every strategic move that followed—the health insurance pivot, the technology pivot, the Hong Kong bank, the international SaaS, the AI underwriting—was an expansion vector off that original foundation. Without the shipping return wedge, none of it works. Without the cloud-native core built to support billions of tiny policies, you don't have a tech stack worth selling. Without the consumer data from hundreds of millions of microtransactions, you don't have underwriting insight worth licensing.

There is a second lesson about ecosystems. Being born from three powerful parents can be either a blessing or a curse, and which one it becomes depends on whether the child earns its independence. ZhongAn spent the years from 2016 to 2022 deliberately decoupling from the distribution rails that birthed it, and in doing so, converted platform dependence into ecosystem access. Those are very different things. Platform dependence is a hostage situation; ecosystem access is a relationship. The company that emerged from that transition was strategically stronger than the company that started the journey, even if the top-line growth rate moderated.

A third lesson concerns the willingness to cannibalize one's own technology advantage. Most companies that build strong internal infrastructure hoard it. ZhongAn instead turned it into a product and sold it to competitors, including some of the largest insurers in Asia. That move sacrificed some short-term differentiation but compounded long-term value, because technology platforms at scale are more defensible as networks than as secrets.

And there is a final, bigger lesson about what insurtech actually is. For much of the 2010s, insurtech was a buzzword that venture capitalists sprinkled on pitch decks. Many of the companies that raised capital under that banner did not actually re-architect anything; they were traditional insurance businesses with better websites. ZhongAn is different. It did re-architect the core—the underwriting engine, the claims engine, the product design engine, the distribution engine. It built an insurance carrier where the first principles are computational rather than actuarial. That is what insurtech actually means, and it is why ZhongAn, as of early 2026, remains the defining case study in the category.

The company that the Three Mas birthed in 2013 has grown up. It still carries the features of its parents—Ant Group's product velocity, Tencent's consumer reach, Ping An's financial discipline—but it is now, recognizably, its own thing. What it becomes in the next decade depends on how much of the insurance industry globally follows the trail ZhongAn blazed, and how effectively ZhongAn can be the partner, the competitor, and the template for the next wave of digital insurance.

A company that insures a two-dollar pair of socks by API in 2013, and runs the first licensed virtual bank in Hong Kong by 2020, and sells its core stack to a 140-year-old Japanese insurer by 2022—that is a company worth watching carefully. The story is not finished. In many ways, after twelve years, it is just entering the interesting part.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube