Milkyway Chemical: The Infrastructure of China's Industrial DNA

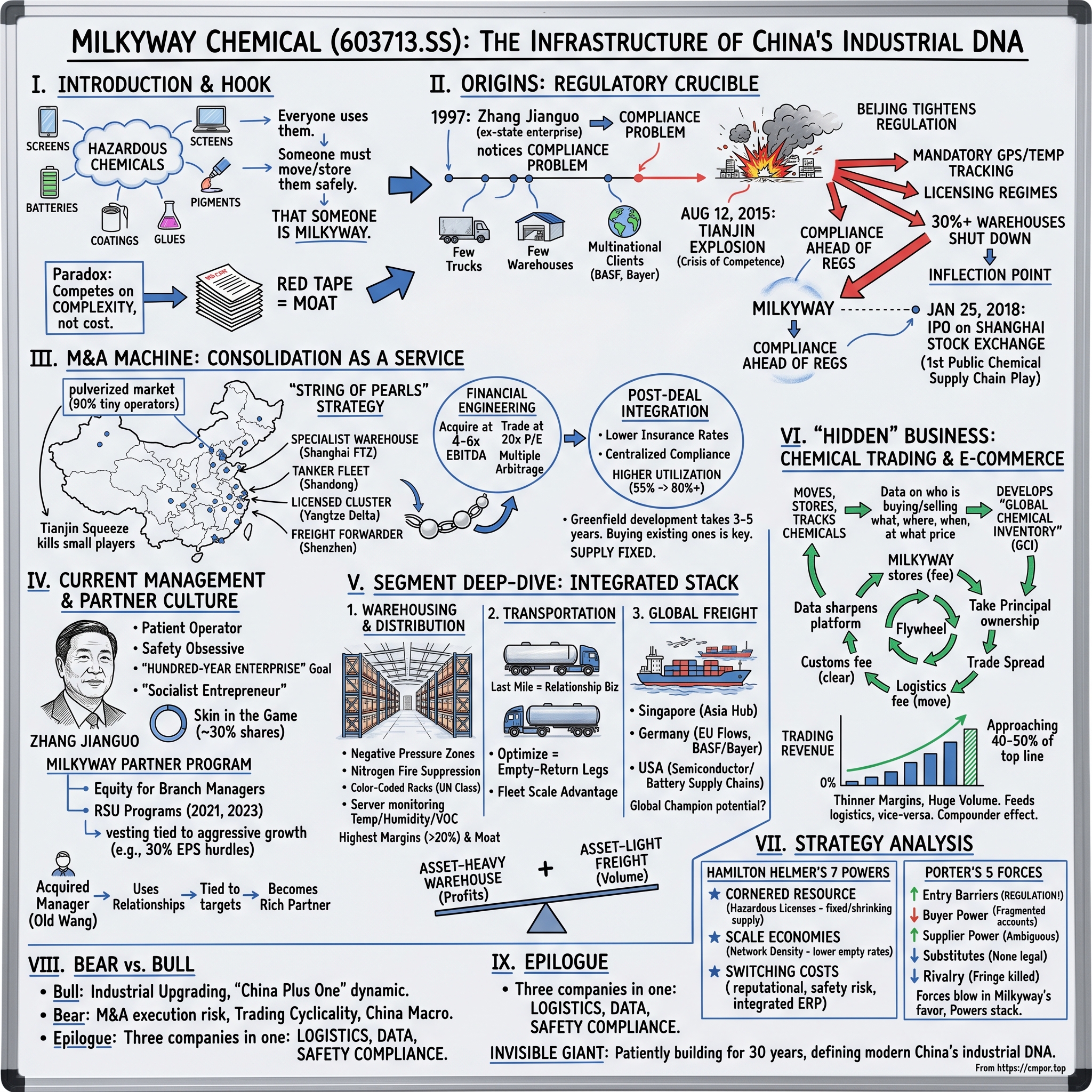

I. Introduction & The "Invisible Giant" Hook

Look around the room you are sitting in right now. The glossy screen you are reading this on. The lithium cells in the battery humming beneath the keyboard. The flame-retardant coating on the polyester carpet. The epoxy glue holding the laminate to the desk. The titanium dioxide pigment making the wall paint bright white. Every single one of those things, not long ago, was a hazardous chemical. A barrel of something corrosive, flammable, reactive, or toxic sitting in a warehouse somewhere in Shanghai, Ningbo, Tianjin, or Houston. Someone had to drive it. Someone had to store it at precisely the right temperature. Someone had to fill out the United Nations dangerous-goods declaration, log it into customs, escort it past the port authority, and deliver it, intact, to a factory where a technician in a bunny suit would crack the seal.

That someone, increasingly often in China, is Milkyway.

This is the strange paradox that sits at the heart of the Milkyway Chemical story. Most logistics companies compete on cost per ton-kilometer. They race to the bottom, squeezing pennies out of diesel, squeezing minutes out of dispatch, squeezing drivers out of their lunch breaks. Milkyway competes on something almost opposite: complexity. The more regulated the cargo, the more forms to file, the more permits required, the more safety officers on payroll, the better the business gets. In an industry where everyone else views red tape as a cost, Milkyway views it as the moat. Every new safety rule from the Ministry of Emergency Management is, for Milkyway, a gift from the government — a slow-moving asset write-down for every pickup-truck chemical hauler in the country, and a slow-moving asset write-up for the 500,000-plus square meters of licensed warehouse space Milkyway already owns.

The question Acquired listeners will find themselves asking throughout this episode is simple: how did a regional freight forwarder, founded in the late 1990s by a former state-enterprise logistics manager in Shanghai, end up as the consolidator-in-chief of China's $60-billion chemical logistics industry, a listed public company trading on the Shanghai Stock Exchange, and the behind-the-scenes operating partner to giants like BASF, Dow, Sinopec, and CATL?

The short answer is that Zhang Jianguo — Milkyway's founder, chairman, and still its largest individual shareholder — understood something earlier than almost anyone else in China: that the chemical industry was the bloodstream of the country's industrial economy, and that the bloodstream was being pumped through a completely unregulated cardiovascular system.

The longer answer is what we are going to spend the next two hours unpacking. We will trace Milkyway from its origins as a company with a handful of trucks in the suddenly booming Yangtze River Delta, through the regulatory earthquake of August 2015 that we still believe is the single most important event in the company's history, into its 2018 IPO, and then into what we will argue is the most interesting chapter: the string-of-pearls roll-up of fragmented regional operators that turned a freight forwarder into what increasingly looks like the "Amazon of Chemicals" for Chinese industry. Along the way we will dig into the hidden business that almost nobody talks about — the trading and e-commerce segment that is now a rapidly growing slice of revenue — and we will run the whole thing through Hamilton Helmer's 7 Powers and Porter's 5 Forces to see, honestly, what kind of moat this company actually has.

Let us start where every good industrial story starts. With a fire.

II. Origins: The Regulatory Crucible

The year is 1997. Shanghai is still a place where a foreigner walking down Nanjing Road stops traffic. The Pudong skyline, which today looks like someone spilled a box of neon Legos across the Huangpu River, is mostly empty farmland. The Chinese chemical industry — ethylene, caustic soda, PVC, the boring backbone commodities that would, within a decade, become the largest in the world — is exploding. Multinationals are landing in China like paratroopers. BASF is breaking ground in Nanjing. Bayer is scouting Shanghai. And absolutely nobody, at any professional level, knows how to move their stuff.

Zhang Jianguo was thirty-something at the time, a logistics manager trained inside the state system, watching all of this unfold. The story Milkyway's early employees tell — and we cannot fully verify every detail, so treat this as company lore — is that Zhang spent a sleepless night after watching a truck driver tip a drum of solvent into the gutter during a late-night delivery, because the warehouse he was supposed to deliver to had closed for the night and he wanted to get home. That small, deeply illegal moment is supposedly when Zhang realized: this industry does not have a logistics problem. It has a compliance problem dressed up as a logistics problem.

He founded Milkyway (天津市大田集团 in its earliest ancestor form, before rebranding to Milkyway's current corporate structure) as a specialist freight forwarder. For the first decade, it was unglamorous. A few trucks. A few warehouses. A growing rolodex of multinational clients who wanted to move isocyanates and phenols without reading about their cargo in tomorrow's newspaper. The company grew at the pace of Chinese GDP, which is to say, fast enough to matter, slow enough not to get noticed.

Then, at 11:34 p.m. on August 12, 2015, everything changed.

A warehouse at Ruihai International Logistics, inside the Port of Tianjin, exploded. The cause was a batch of nitrocellulose that had been improperly stored, in the wrong part of the facility, next to materials it should never have touched. The initial blast was measured at roughly the equivalent of three tons of TNT. The second blast, thirty seconds later, registered at twenty-one tons. It cratered the warehouse district, killed 173 people, shattered windows for kilometers, and was seen, literally, from space.

For China's political leadership, the Tianjin explosion was not just a tragedy. It was a crisis of competence. How could a facility storing sodium cyanide and ammonium nitrate operate in violation of multiple national safety codes, inside one of the country's most strategic ports, without anyone stopping it? The answer, painful but obvious, was that the entire hazardous-chemical logistics industry in China was operating on a nod-and-a-wink basis. Mom-and-pop operators. Overlapping and poorly enforced regulations. Local officials who could be persuaded to look the other way.

That ended in a matter of months. Beijing unleashed one of the most aggressive regulatory tightenings in the history of Chinese industrial policy. New licensing regimes. Mandatory GPS tracking on every chemical tanker. Mandatory real-time temperature monitoring on Class 6 materials. Mandatory driver re-certifications. Warehouses that had operated for twenty years without a safety inspection were suddenly required to produce documentation that, in many cases, had never existed. By some industry estimates, more than thirty percent of the country's chemical warehouses were shut down, or forced into expensive retrofits, within three years of Tianjin.

For Milkyway, this was not a disaster. It was the inflection point of the entire business. Zhang, almost alone among his competitors, had already been investing in compliance ahead of the regulation — hiring safety officers, getting licensed for Class 3 flammables, building GPS tracking into dispatch before it was required. When the regulatory hammer came down, Milkyway did not have to retrofit. It just had to answer the phone, because every multinational in the country was calling.

The company transitioned, in the phrase that longtime observers use, from "a company with trucks" to "a company with licenses." And in a country of 1.4 billion people where central authority had just declared that it would no longer tolerate amateurism in industrial safety, a company with licenses was sitting on a gold mine.

On January 25, 2018, Milkyway Chemical Supply Chain Service Co., Ltd. listed on the Shanghai Stock Exchange under the ticker 603713. It was the first publicly listed "chemical supply chain" pure-play in China. The IPO was modest by American standards — raising a few hundred million renminbi — but the significance was enormous. Milkyway now had a war chest, a public currency, and a listed stock price that could be handed to sellers in M&A transactions. Which brings us to the real story.

III. The M&A Machine: Consolidation as a Service

Picture a map of China, and imagine sprinkling salt over it. Every grain is a chemical warehouse. There are, depending on how you count, somewhere between fifteen and twenty thousand of them — ranging from a giant Sinopec-owned tank farm to a guy named Old Wang who has a corrugated-steel shed outside Wuxi with three licenses tacked to the wall and a nephew who drives the forklift. For decades, this was the shape of Chinese chemical logistics. Ninety percent of the market — ninety — was handled by operators with fewer than five trucks or one warehouse. The industry was not just fragmented. It was pulverized.

This is important, because it explains why the post-Tianjin regulatory squeeze was existential for most of Milkyway's competitors but transformational for Milkyway itself. When the Ministry of Emergency Management raised the bar on safety systems, insurance requirements, and driver certifications, it did not affect a big compliant operator and a small uncompliant operator in equal measure. It killed the small operator. A safety officer costs the same whether you have three trucks or three hundred. Insurance premiums scale, but compliance costs do not. For Old Wang outside Wuxi, it was no longer economic to stay in business. For Zhang Jianguo in Shanghai, the price of Old Wang's warehouse had just collapsed.

Milkyway called its acquisition playbook the "String of Pearls," and the metaphor is apt. The strategy was not to buy one giant competitor and try to digest it — that is how logistics roll-ups fail, and there is a graveyard of cautionary tales from the American trucking industry to prove it. Instead, Milkyway targeted regional champions, one city at a time. A specialist bonded-warehouse operator in the Shanghai Free Trade Zone. A tanker fleet in Shandong servicing the petrochemical complex at Qingdao. A licensed warehouse cluster in the Yangtze Delta. A freight forwarder in Shenzhen with relationships into the Greater Bay Area. The Starway acquisition, folded in during the post-IPO years, gave the company meaningful expansion into international freight — not just domestic Chinese chemical logistics, but the cross-border piece that connects Chinese factories to Rotterdam, Hamburg, Houston, and Singapore.

The financial engineering underneath these deals is the part that long-term investors need to understand, because it is where a meaningful portion of the company's value has been created. Milkyway has historically acquired regional operators at somewhere between four and six times EBITDA, sometimes lower when the seller is distressed. Milkyway itself has traded at multiples that, depending on the year and the mood of the Shanghai market, are dramatically higher — twenty times earnings or more at various points. The delta between those two numbers is the classic "multiple arbitrage" that has driven everyone from Warren Buffett's early conglomerate plays to Danaher's lifetime of roll-ups. Buy private assets at a private-market multiple, bolt them onto a public platform at a public-market multiple, and watch the value appear out of thin air.

But the multiple arbitrage, while nice, is not actually the interesting part. The interesting part is what happens to the acquired business after the deal closes. Imagine Old Wang's warehouse — three licenses, two forklifts, one safety officer who doubles as the accountant. The day after Milkyway closes the deal, three things happen. First, the insurance gets renegotiated at Milkyway's group rate, often cutting premiums in half. Second, the safety officer stops being a cost center and becomes a node in a centralized compliance system that Milkyway runs from its Shanghai headquarters. Third, Old Wang's warehouse, which previously ran at fifty-five percent utilization because he only had relationships with local buyers, now gets filled to eighty or ninety percent with freight dispatched from Milkyway's national routing system.

That is where the real money is made. Milkyway is not just buying assets at cheaper multiples. It is buying under-utilized assets and immediately making them more productive. It is buying compliance-burdened assets and immediately pooling the compliance. It is buying geographically isolated assets and immediately connecting them to a national network.

The efficiency question — did Milkyway overpay? — matters here. The honest answer is that for individual deals, we have seen quarters where the integration was rocky and the return on invested capital lagged guidance. But the counterfactual is instructive. Greenfield development of a licensed hazardous-chemical warehouse in China, post-Tianjin, takes three to five years. You need permits from provincial safety authorities, environmental impact assessments, fire-code review, local zoning, and in many cases explicit sign-off from the Ministry of Emergency Management. Even if you have the capital, you do not have the time. Buying a licensed facility is often the only way to expand inside a relevant planning horizon. And critically, many local governments have simply stopped issuing new licenses in dense industrial corridors. The supply of legal warehouse capacity is, in the strictest sense, fixed. Milkyway is not building new pearls. It is buying existing ones, because there may not be many more to make.

This shift in supply dynamics is what turned the M&A machine from a growth strategy into something closer to a moat. Every deal makes the remaining addressable pool smaller and the platform's bargaining position stronger. Which, naturally, leads to the question of who is actually running the machine.

IV. Current Management & The "Partner" Culture

Zhang Jianguo does not look, on the surface, like the kind of entrepreneur Western tech reporters write cover stories about. There is no Stanford engineering degree, no Silicon Valley sabbatical, no signature turtleneck. He is, by most accounts, a quiet, almost ascetic operator in his sixties who still shows up at company events wearing a safety vest. People who have sat across the table from him in deal negotiations describe him with a single word that keeps recurring: patient.

That patience has a philosophical basis. Zhang has spoken publicly, especially in Chinese-language business media, about building what he calls a "hundred-year enterprise" — a phrase that in the Chinese business context carries a meaningful cultural weight. It is not marketing. It is a reference to an older tradition, one that predates the Shenzhen gold rush and the Alibaba IPO, of industrial lineages that are built to outlast their founders. Zhang has said in interviews that he wants Milkyway to still be operating, safely, in 2097, which is the company's centennial. He has also described himself, using language that would strike Western ears as strange, as a "socialist entrepreneur" — meaning, roughly, that he sees the company's work as embedded in the broader national project of industrial upgrading rather than as a pure wealth-creation exercise.

Whether you take that at face value or read it as politically adaptive signaling in a country where political adaptation matters, the operational consequence is consistent: Zhang is obsessive about safety. Employees describe internal meetings where a single lost-time incident across the entire national network — not a fatality, not even a serious injury — triggers hours of root-cause review and a cascade of protocol updates. For a logistics company moving Class 3 and Class 6 materials across a country of 9.6 million square kilometers, a culture of safety is not an HR poster. It is the product.

Zhang's skin in the game is substantial. He and his affiliated entities controlled roughly thirty percent of the company's shares at the time of IPO, and while the precise number has moved around with follow-on offerings and the various incentive programs, he has remained the single largest individual shareholder. This matters in a way that Anglo-American investors sometimes under-appreciate when looking at Chinese companies. In a market where founder lock-ups, VIE structures, and opaque corporate governance can create real alignment problems, Zhang has consistently operated with the long-horizon posture of someone who plans to still own a material chunk of the business twenty years from now.

The second piece of the management story, and arguably the more interesting one for students of organizational design, is Milkyway's Partner Program. The problem Zhang was solving is deeply structural in fragmented logistics. When you acquire a regional operator — say, Old Wang's warehouse — you are not just buying a building. You are buying relationships. Old Wang knows the local shippers, the local port officials, the local truckers. If Old Wang gets frustrated with his new corporate overlords eighteen months in, he can walk out the door, take his relationships with him, and start a competing operation two blocks away. The logistics industry in every country in the world is littered with examples of exactly this pattern.

Milkyway's answer was to stop thinking of branch managers as employees and start thinking of them as partners. Through a series of RSU programs — most meaningfully launched in 2021 and expanded in 2023 — Milkyway began allocating equity to branch managers and key regional operators tied to performance targets. The structure, details of which the company has disclosed in its annual reports and proxy-equivalent filings, ties vesting to aggressive earnings-growth milestones, with reported thirty-percent EPS-growth hurdles in certain tranches. If you are Old Wang and your warehouse hits its numbers, you are a rich man. If it doesn't, you are not. And critically, you cannot monetize the equity without staying in the tent.

Underneath the culture layer sits the operational plumbing. Milkyway's "Control Tower" — a centralized operations system run out of Shanghai that tracks, in real time, every truck, every driver, every temperature-controlled drum, and every port transit in the network — represents the company's transition from a founder-led, hustle-driven organization to something closer to an industrial SaaS platform. The Control Tower is, in Zhang's own telling, what makes the Partner Program work, because it gives the center the ability to trust but verify. A branch manager in Guangzhou cannot cut corners without the Shanghai system flagging it within minutes. A truck that veers off its authorized route triggers an automated alert. A drum that spends too many hours outside its temperature spec gets quarantined.

This is the culture that Milkyway has built heading into the current chapter of its story. Disciplined at the top, incentivized at the edges, monitored in the middle. Which sets the stage for understanding the segment mix that has emerged from all of this effort.

V. Segment Deep-Dive: The Integrated Stack

Walk into one of Milkyway's flagship chemical warehouses — the company operates more than half a million square meters of licensed storage space across its national network — and you realize that calling this facility a "warehouse" is like calling a modern data center a "room with computers." It is technically accurate and meaningfully wrong.

The floor is treated with a specific chemical-resistant coating that has itself been tested, certified, and logged. The ventilation system is designed to create negative pressure in specific zones so that vapors from a potential leak flow away from ignition sources. The fire-suppression system is not water — water would make things worse for many of the chemicals stored here — but a nitrogen-based system keyed to the specific cargo profile. The pallet racks are color-coded by United Nations hazard class. The drums are spaced with prescribed distances between materials that should never touch, because if they did, the warehouse would no longer exist. Workers wear chemical-resistant suits and breathing apparatus rated for specific exposure profiles. A room-sized server stack monitors temperature, humidity, and VOC concentration every thirty seconds.

This is segment one of Milkyway's integrated stack, and it is the foundation of the entire business. Warehousing and distribution contribute the highest operating margins in the portfolio — typically north of twenty percent on a segment level — and, crucially, they contribute the moat. A customer choosing Milkyway is not really choosing a warehouse. They are choosing the certainty that their dimethylformamide will arrive at the pharmaceutical plant in Suzhou next Tuesday at a specific temperature, with full documentation, with customs clearance pre-filed, and with full insurance coverage if something goes wrong.

The second segment is transportation. Milkyway moves hazardous cargo across the mainland with a fleet that is a mix of owned, leased, and partner-operated vehicles, with a strong skew toward specialized tankers for liquid chemicals. Two features of this segment are worth understanding. First, the "last mile" of chemical logistics is far harder than the last mile of e-commerce. A package from Alibaba arrives at your door. A drum of sodium hydroxide arrives at a factory loading dock that has its own safety protocols, its own receiving manifests, and its own hazardous-materials officer who will refuse delivery if paperwork is incomplete. This makes the last mile a relationship business, and Milkyway's dominance in specific industrial clusters — like Changshu for specialty chemicals, or Ningbo for petrochemicals — reflects years of painstaking relationship-building at individual factory gates. Second, the economics of specialized tanker fleets are driven almost entirely by empty-return-leg optimization. A tanker that delivers benzene to Nanjing cannot simply reload with, say, ethanol for the return trip; the cleaning protocols between incompatible cargoes are expensive and, in some cases, prohibited. Milkyway's scale means it can route empty tankers to the nearest compatible loading opportunity. A three-truck operator cannot.

The third segment is global freight, and this is where Milkyway starts to look less like a Chinese logistics company and more like a contender on the international stage. The company has expanded into Singapore, which is the natural regional hub for chemical trading in Asia; into Germany, specifically to service flows into and out of the European Union with multinational chemical customers like BASF and Bayer; and into the United States, where the emergence of China-sourced specialty chemicals for American semiconductor and battery supply chains has created new cross-border flows. The unanswered question is whether Milkyway is building toward a "mini-Maersk for chemicals" — an integrated global ocean, port, warehouse, and inland operator — or whether it will remain primarily a Chinese champion with global reach. The difference matters for the long-term margin and return profile, because global ocean freight is a very different business from Chinese domestic warehousing.

The segment financials explain why the mix matters so much. The warehouse business is asset-heavy, capital-intensive, and margin-rich. The freight forwarding business is asset-light, capital-efficient, and margin-thin. Combining the two inside one company creates a portfolio that generates both the returns on assets that justify the capital spending and the revenue velocity that justifies the platform scale. It is, in a way, the same structural insight that made Amazon Web Services and Amazon Retail work together — one side provides the profit pool, the other side provides the volume that keeps the infrastructure full.

And yet, for all the elegance of the logistics stack, the real plot twist of the Milkyway story is what happens when a company that already moves, stores, and tracks chemicals decides that it might as well start buying and selling them too.

VI. The "Hidden" Business: Chemical Trading & E-Commerce

Here is a thought experiment. You run the largest specialized logistics network for hazardous chemicals in China. Every day, across your half-million square meters of warehouse space, millions of kilograms of raw materials, intermediates, and finished chemicals pass through your fingertips. You know, with precision unmatched by any market participant, who is selling what, who is buying what, at what prices, in what volumes, to which end markets. You know which factory in Zhejiang is running low on a specialty solvent. You know which trader in Shanghai has inventory sitting idle. You know, in effect, the supply and demand curves for thousands of individual chemicals in real time.

Why on earth would you not trade?

That is the logic behind what is, in our view, the most underappreciated development in Milkyway's recent history: the emergence of the company's chemical trading and digital commerce business, which the company refers to internally as the Global Chemical Inventory, or GCI. The transition from moving chemicals to actually buying and selling them is, in one sense, a subtle strategic pivot. In another sense, it is the most consequential business model change in the company's history.

The mechanics are straightforward. Milkyway, through its trading affiliates, takes principal positions in chemical inventory. It buys from producers, holds stock in its own warehouses, and sells to end customers. The margins on trading are thinner than margins on logistics — trading, in any industry, is a spread business — but the volume can be enormous. More importantly, the trading business feeds back into the logistics business, and vice versa, in ways that compound.

Consider the flywheel. Milkyway stores a chemical on behalf of a producer, earning a warehousing fee. Seeing the inventory sit, and knowing a downstream buyer who needs exactly that chemical, Milkyway proposes to take principal ownership of the cargo, earning a trading spread. It moves the chemical through its own transportation network, earning a logistics fee. It clears the chemical through customs using its own bonded facilities, earning a customs fee. It reports the transaction back into its data platform, sharpening its understanding of real-time supply and demand. Next time a similar trade opportunity appears, it has even better information. The flywheel spins.

The trading segment has grown, by multiple years of company reporting, at compound annual rates well north of fifty percent, and in some recent years has approached a meaningful fraction of total revenue — pushing toward forty to fifty percent of the top line, up from essentially zero a few years earlier. This is a dramatic revenue-mix shift for any industrial company to absorb. It raises legitimate questions that long-term investors must engage with: Is this a structural margin accretion or dilution? Is this a growth engine or a working-capital trap? Does the trading business actually create durable value, or is it just leveraging the logistics network for lower-quality revenue?

The honest answer to each of these is "it depends on how you measure." Trading revenue is gross, which means it comes in big and can make headline growth look more impressive than the economic reality. Gross margin percentages go down as the trading mix goes up, because trading inherently runs thinner. But absolute gross profit can grow meaningfully if the trading volume is large enough, and the incremental return on invested capital can be excellent if the trading inventory is already sitting in Milkyway's warehouses for logistics reasons anyway — that is, if the marginal cost of trading activity is close to zero.

The flywheel framing also has a competitive dimension that is worth sitting with. Why can Milkyway play this game better than a pure-play chemical trader? Because a pure-play trader does not own the warehouses, does not move the trucks, and does not see the data. Why can Milkyway play this game better than a pure-play logistics company? Because a pure-play logistics company does not have the balance-sheet appetite, the commercial relationships, or the market-information advantage to take principal positions. The intersection of the two capabilities is, if you are Milkyway, an extremely defensible space. And if you are a competitor trying to replicate it, you have to build both sides of the business from scratch, which — given the post-Tianjin regulatory moat on the logistics side — is, in a practical sense, close to impossible.

That, more than anything else, is what transforms the Milkyway story from a "roll-up in a fragmented industry" narrative into something closer to a platform narrative. The roll-up bought the real estate. The platform makes the real estate sing. Which is the natural setup for running the whole thing through the strategic frameworks that long-term investors in this kind of business care about.

VII. Strategy Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is, in our view, the most useful strategic lens for thinking about durable competitive advantage, and Milkyway gives us an unusually clean example of how the powers stack. Let us walk through the three that matter most here, and note the ones that do not.

The first is Cornered Resource. In Helmer's framework, a cornered resource is preferential access to a coveted asset that can, independently, drive significant value. For Milkyway, the cornered resource is crystal clear: the hazardous-chemical warehouse license. In the post-Tianjin regulatory environment, local authorities across most of coastal China have significantly slowed, and in some cases effectively stopped, issuing new licenses for hazardous-material storage in dense industrial corridors. The existing license stock, in the geographies that matter most for the chemical industry — the Yangtze Delta, the Pearl River Delta, the Bohai Rim — is a fixed or shrinking supply. Milkyway owns a large and growing share of that fixed supply. No amount of capital, talent, or determination can replicate this in a reasonable planning horizon. Someone could try to buy every remaining independent license holder, but Milkyway is buying them first. This is as pure a cornered-resource power as you will find in Chinese industry.

The second is Scale Economies. This one is more subtle in logistics than in, say, semiconductor fabrication, but it is real. The key scale advantage for Milkyway is network density. The more routes Milkyway runs, the lower the empty-return rate on specialized tankers, because there are more opportunities to find compatible reverse-leg cargo. The more warehouses Milkyway operates in a given region, the better it can dynamically balance utilization across the network. The more shippers it serves, the sharper its forecasting gets, and the less safety stock it needs to hold. Every incremental unit of scale makes the network more efficient, which in turn makes it more attractive to the next incremental customer. This is classic network-scale economics, and it compounds particularly well in a business where the marginal cost of adding a new cargo to an existing route can be very close to zero.

The third is Switching Costs. If you are BASF, Dow, Bayer, or Covestro, and you have integrated your enterprise resource planning system with Milkyway's compliance and tracking platform, the cost of switching to an unproven vendor is not measured in renegotiating a rate card. It is measured in potential regulatory exposure, customs documentation continuity, real-time tracking integration, and, most importantly, the absence of the one thing you cannot afford: a safety incident. Chemical multinationals will cheerfully pay a premium to keep running with a trusted, compliant logistics partner, because the downside of a vendor failure is a cover-of-the-newspaper disaster. Switching costs in this industry are not transactional. They are reputational. And reputational switching costs are the stickiest kind.

The other four powers in Helmer's framework — Counter-Positioning, Branding, Process Power, and Network Economies in the classic user-to-user sense — are either less relevant or only partially present in the Milkyway case. We will not force them.

Run the same business through Porter's 5 Forces and the picture sharpens further. Barriers to entry are extraordinarily high, because regulatory licensing in the post-Tianjin environment is now the binding constraint, and greenfield capacity is slow or impossible to add. Buyer power is structurally low, because the buyers — chemical producers and end-user factories — are enormously fragmented across tens of thousands of accounts, and none of them individually can squeeze Milkyway. Supplier power is ambiguous, because Milkyway's "suppliers" in a classical sense are a mix of truckers, port operators, and its own acquired subsidiaries; in most cases, Milkyway is more the price-setter than the price-taker. Substitutes are minimal, because the alternative to compliant hazardous-material logistics is, in most cases, illegal and increasingly unacceptable to regulators. And competitive rivalry is surprisingly muted inside Milkyway's core segments, because the regulatory environment has systematically killed off the fringe competition that would have kept margins under pressure in an earlier era.

Put differently, this is an industry where Porter's forces are mostly blowing in Milkyway's favor at once, and the 7 Powers are stacking. That is the kind of configuration that shows up rarely in any industry, anywhere in the world, and it is why the company deserves the attention long-term investors have started to pay it.

Of course, powerful frameworks on a slide are easy. Reality is always messier, which is why the next step is to stress-test the story from both sides.

VIII. Bear vs. Bull & The Playbook Lessons

Let us take the bull case and the bear case seriously, not as a rhetorical device but as the actual stress test that any long-horizon holder needs to run on this name.

The bull case starts with the upgrading of the Chinese chemical industry itself. For decades, the Chinese chemical sector was a commodity engine — ethylene crackers, bulk PVC, caustic soda, the boring ton-chemistry that fed construction and consumer goods. Going forward, the center of gravity is shifting dramatically toward specialty and fine chemicals: electronic-grade solvents for semiconductor fabs, ultra-pure electrolytes for lithium batteries, advanced pharmaceutical intermediates for a growing domestic innovative-drug industry, high-performance coatings for electric vehicles. These categories are harder, smaller-volume, higher-value, and crucially, significantly harder to move safely. A ton of bulk methanol is a rounding error in a tanker. A kilogram of a semiconductor-grade photoresist component is a precision-logistics problem. The chemicals of the 2030s are more dangerous, more temperature-sensitive, more documentation-heavy, and more insurable-risk-heavy than the chemicals of the 2000s. Milkyway is the only scaled, listed, specialized player positioned at the intersection of all of these trends.

Layer on top the "China Plus One" dynamic that has reshaped global supply chains in the post-pandemic, post-trade-tension era. Multinationals are not leaving China so much as they are duplicating capacity outside China — a factory in Vietnam here, a tolling arrangement in Thailand there, a new facility in Mexico or in India. But the raw materials for many of those facilities still flow out of Chinese production. The logistics layer connecting Chinese specialty chemical producers to a multi-country Asian and global industrial footprint is precisely the layer Milkyway has been building. The bull case argues that Milkyway's international expansion is not a vanity project — it is the emerging arterial system for "Chinese inputs, global assembly."

The bear case, fairly stated, is that execution risk in M&A never fully disappears. Every acquisition introduces new people, new procedures, new facilities, and new failure points. If one acquired subsidiary has a major safety incident — and in a network of hundreds of facilities operating across thousands of cargo types, the base-rate probability is never zero — the reputational damage flows to the entire Milkyway brand. The very feature that makes Milkyway's moat powerful — that customers outsource their safety risk to the logistics vendor — is the same feature that creates concentrated fragility. A single catastrophic event could, in theory, undo a decade of brand-building.

The second bear-case strand is the cyclicality of the trading segment. Chemical prices are volatile. When methanol prices drop thirty percent in six months, as they have in past cycles, a trading book carrying methanol inventory takes real hits. The logistics side of Milkyway is relatively insulated from chemical-price volatility — a warehouse charges rent whether the product inside has appreciated or depreciated — but the trading side is directly exposed. As trading grows as a share of revenue and gross profit, the consolidated earnings profile becomes more cyclical, not less. Investors who thought they were buying a stable infrastructure play may need to recalibrate toward a hybrid infrastructure-plus-merchant model.

A third bear-case strand, and one that we think deserves more attention than it typically gets, is the broader Chinese macro overhang. Milkyway is a China-domiciled, Shanghai-listed company whose fortunes are tied to the trajectory of Chinese industrial production, Chinese regulatory continuity, and Chinese capital-markets openness to foreign investors. A persistent slowdown in Chinese manufacturing would pressure volumes. A shift in regulatory priorities — say, an aggressive environmental push that reclassifies certain core chemicals as restricted — could change the terrain. This is not a prediction, just a reminder that Milkyway is a play on Chinese industrial policy as much as it is a play on Chinese logistics.

On the second-layer diligence side, a few items are worth flagging without overweighting. The company has been a regular issuer of equity-linked incentive programs, which is governance-positive for alignment but modestly dilutive for existing shareholders; a careful reading of the share-count trajectory is appropriate. The capital intensity of acquiring licensed warehouse space has, at times, pushed leverage higher than the asset-light perception of a logistics company would suggest. And the company's financial disclosure is governed by the Shanghai Stock Exchange's reporting regime, which for non-Chinese investors can require more effort to parse than the SEC equivalent.

Three playbook lessons emerge from putting all of this together. First, regulated monopolies can be built. The post-Tianjin regulatory environment did not create Milkyway's business — Zhang did — but it gave Milkyway the structural gift of an ever-scarcer license pool. Investors looking for durable businesses should pay attention to industries where government mandates are tightening the supply of a necessary input, and where one operator has positioned ahead of the wave. Second, the platform pivot is the real alpha. The logistics business is good. The logistics-plus-trading platform is dramatically better, because it captures multiple spreads on the same physical flow. The moment a company can credibly say that its trading volume improves its logistics data, and its logistics data improves its trading decisions, the competitive moat has migrated from physical to informational. Third, "boring" businesses become "tech" businesses at scale. A single tanker is a truck. A thousand tankers coordinated by a real-time control tower, routed by a demand-forecasting algorithm, and funded by a trading book that takes principal positions, is a technology platform wearing a logistics costume. The aggregator's advantage in the internet era has a direct analog in specialized physical industries, and Milkyway is a textbook case.

For ongoing monitoring, we would zero in on two, possibly three, key performance indicators. The first is warehouse utilization rate across the licensed storage footprint. This is the cleanest single read on the health of the core moat business — a rising utilization rate says the network is pulling more volume through existing assets, which is exactly what a platform should do. The second is the revenue mix between logistics and trading, and the incremental gross margin each contributes. Watch whether trading is growing in a way that is accretive to absolute gross profit or merely to headline revenue, because those are very different outcomes. The third, slightly softer KPI, is the company's disclosed safety incident rate. In this industry, a drift in safety metrics is the earliest possible warning sign that something in the operational culture has slipped. Catch it late and the damage is measured in headlines.

Which brings us, finally, to the question that all great business stories eventually pose about themselves: what, actually, is this company?

IX. Epilogue

Stand back from the details — the trucks, the warehouses, the licenses, the trading books, the acquisitions, the control tower, the RSU program, the partner culture — and ask the simplest possible question about Milkyway. What kind of company is this?

The honest answer is that it is three companies at once, wearing the costume of one.

It is a logistics company, obviously. Moving hazardous material from producer to consumer is the visible work, and the revenue from that work still makes up the majority of the top line. A logistics company is how Milkyway was born, and a logistics company is, in the most mechanical sense, what it remains.

But it is also, increasingly, a data company. The Control Tower is a data platform. The trading book is a data play, leveraging asymmetric information about supply and demand across the Chinese chemical industry. The safety-monitoring system is a data asset that gets more valuable with every drum, every truck, every kilometer it processes. The moat over time will shift from pure physical infrastructure to the combination of physical infrastructure and the informational layer on top of it. This is the pattern that played out in global logistics with companies like Maersk, in retail with Amazon, in payments with Visa. Physical scale begets data scale begets network effect.

And underneath both of those, Milkyway is a safety-compliance company. This is the deepest truth of the business, and the one that most directly reflects Zhang Jianguo's founding intuition. Customers do not hire Milkyway because its trucks are faster or its warehouses are prettier. They hire Milkyway because its drivers have been certified, because its facilities have been inspected, because its documentation will stand up in court, and because its safety record is the cleanest available. In an industry where the downside risk is measured in casualties and criminal liability, the upside of a compliant vendor is difficult to over-state.

Zhang has been consistent, in every public setting where he has spoken about the company's future, that the hundred-year horizon is what matters. The quarterly results fluctuate. The Chinese macro cycle fluctuates. The chemical price curve fluctuates. But the underlying drift, as he sees it, is unmistakable: China's industrial economy is moving up the value chain, its regulatory standards are tightening further rather than loosening, and the number of operators capable of serving the resulting demand at scale is shrinking. If Milkyway simply continues doing what it has been doing — buying licensed capacity, integrating it onto a national platform, extracting trading spreads from the resulting information advantage, and never, ever compromising on safety — the compounding effect over decades can be significant.

Whether that patience pays off is the question every long-term holder has to live with. Patient capital is always easy in theory and hard in practice, because the market will offer plenty of reasons to lose faith along the way. There will be quarters when the trading book takes mark-to-market hits on falling chemical prices. There will be acquisitions that integrate poorly. There will be macro cycles in Chinese industrial production that drag on volumes. And there will always be the haunting low-probability, high-consequence tail risk of a major safety incident somewhere in the network, which is the only event that could materially break the story.

But for investors willing to look past those near-term gyrations and think about what the Chinese chemical industry will need in 2035, 2045, or beyond, Milkyway presents a rare and specific kind of opportunity: a business with a cornered resource, a scaled platform, genuine switching costs, a coherent management culture, a founder with skin in the game and a hundred-year mindset, and a structural tailwind from industrial upgrading that shows no sign of reversing. Few companies in any market, anywhere in the world, score that high on that many dimensions at once.

The invisible giant, it turns out, has been sitting in plain sight all along — inside the drum, behind the warehouse door, on the manifest that nobody ever reads. The industrial DNA of modern China runs through systems like Milkyway's, quietly, at two in the morning, in the monitoring room of a Shanghai control tower, where a screen glows with the status of ten thousand shipments in motion, and where a founder who once lost sleep over a single spilled drum is still, at sixty-something, patiently building the company he has been describing for thirty years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube