Shanghai Putailai: The Architect of the Battery Interior

I. Introduction: The Most Important Company You've Never Heard Of

Walk into any auto show in 2026—Shanghai, Munich, Detroit—and the marquee names roll off the tongue the way they always have. BYD's Yangwang supercars draw crowds with their tank-turn party trick. CATL's booth is a temple to gigawatt-hour abstractions, all glass and white light. Tesla, as usual, skips the show entirely and lets its absence do the marketing. Yet buried in the spec sheet of nearly every high-performance electric vehicle on that floor is a supplier most visitors have never heard of, and most investors couldn't pick out of a lineup.

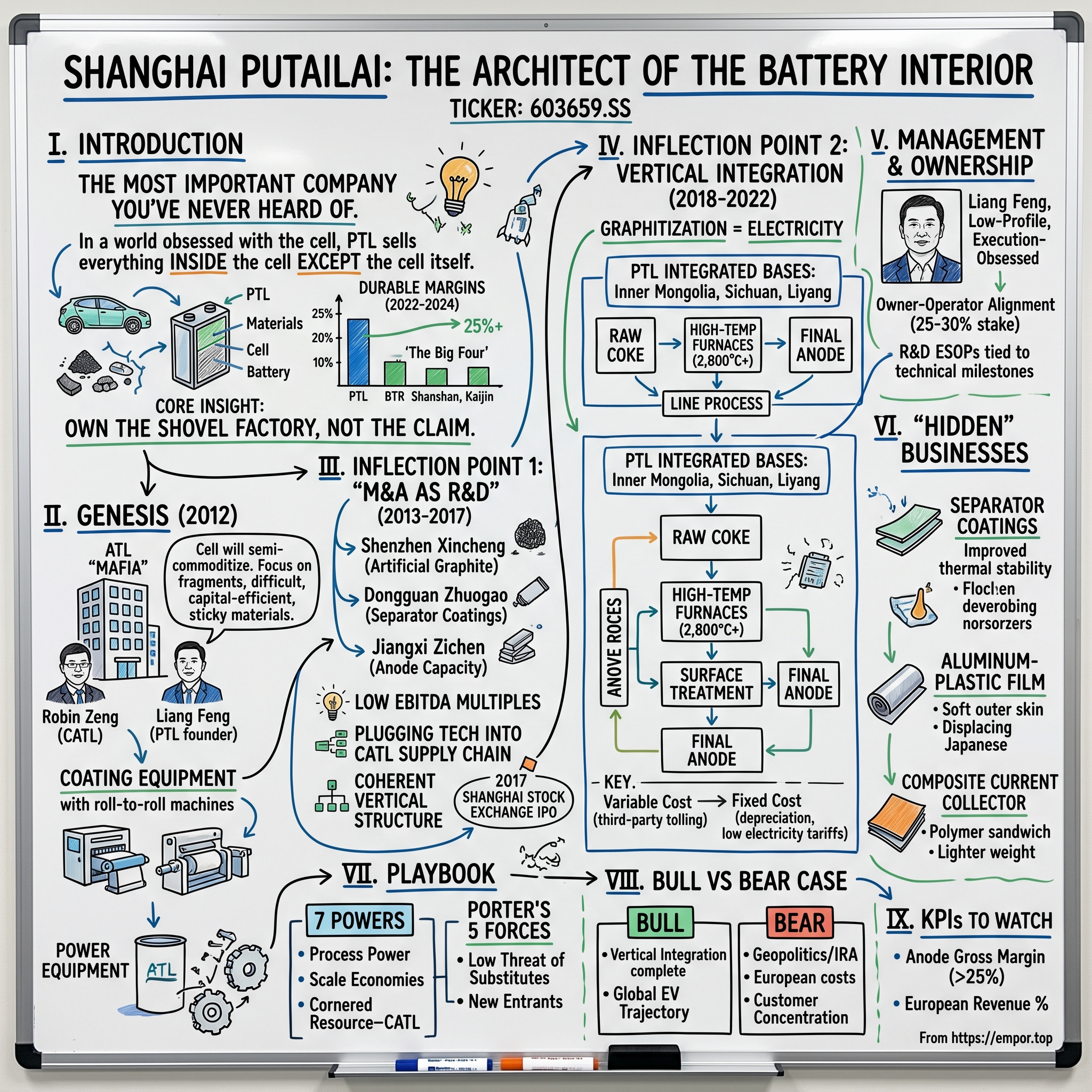

That supplier is Shanghai Putailai New Energy Technology Co., Ltd.—known in the industry simply as PTL, or by its Chinese name, Putailai. The ticker is 603659.SS. The company is twelve years old. It has never made a battery cell, never assembled an EV, never stamped a hood. And yet, in the economic anatomy of the lithium-ion battery, it occupies a position that is, by some measures, more enviable than CATL's. PTL makes the anodes. It makes the equipment that makes the anodes. It makes the coatings, the separators' separator coatings, the aluminum-plastic films that sheathe pouch cells, and now the next generation of copper current collectors that could strip 5% to 10% of the weight out of a finished battery pack. In a world obsessed with the cell, PTL sells everything inside the cell except the cell itself.

The "why now" is straightforward and, for a long-term investor, urgent. Anode producers across China were caught in a brutal margin compression between 2022 and 2024, with industry gross margins collapsing from the high twenties into the low teens as graphitization capacity flooded in and customers squeezed. PTL came out the other side with gross margins still above 25% in its anode segment—a gap of ten to fifteen percentage points over BTR, Shanshan, and Kaijin, the other three members of what the Chinese industry calls the "Big Four" anode houses. That gap is not an accident, not a pricing trick, and not a subsidy artifact. It is the mechanical output of a strategy that founder Liang Feng began building in 2012 and that only fully bore fruit a decade later.

This is the story of how a quiet capital allocator with deep roots in the ATL family built a roughly ten-billion-dollar market capitalization by solving problems no one wanted to solve. It is the story of how a company bet the farm on graphitization furnaces in Inner Mongolia at the exact moment the industry thought graphitization was a commodity. It is the story of an "M&A as R&D" playbook that looks, in hindsight, as shrewd as anything Silicon Valley ever ran. And it is, above all, the story of a simple insight: in a gold rush, you don't always want to own the claim. Sometimes you want to own the shovel factory, and the conveyor belt, and the power plant that runs the smelter, and the proprietary coating that makes the shovels last longer than anyone else's.

II. The Genesis: The ATL Mafia and the 2012 Pivot

Every great Chinese battery story, it turns out, begins in the same building. In the early 2000s, a Hong Kong-headquartered company called Amperex Technology Limited—ATL—sat in a low-rise office park in Dongguan, supplying lithium-polymer cells to a then-obscure customer in Cupertino called Apple. ATL's founder, Robin Zeng, would eventually split off the company's EV battery unit in 2011 and name it Contemporary Amperex Technology Limited—CATL. The alumni of that single hallway—engineers, operations leaders, supply-chain negotiators, materials specialists—went on to seed what industry insiders now affectionately call the "ATL Mafia." Liang Feng was one of them.

Liang is an unusual figure in Chinese industrial history. He does not have the bombastic entrepreneurial persona of a Wang Chuanfu at BYD or a Li Bin at NIO. He is not a Ph.D. in electrochemistry like Robin Zeng. By training and temperament, Liang is a capital markets person who understood batteries because he had lived inside the ATL ecosystem and watched, from a financial seat, how hard it was to actually build a cell to the tolerances Apple demanded. When he looked at the lithium-ion supply chain around 2011 and 2012, he did not see what everyone else saw—which was a coming EV explosion and a once-in-a-generation cell opportunity. He saw something more interesting. He saw the pit crew.

The insight Liang Feng carried into the founding of Putailai in 2012 was this: the cell itself was going to become, in time, a semi-commoditized product. Dozens of Chinese firms were already lining up to build cell capacity. The Japanese incumbents—Panasonic, Sony, Sanyo—were deep-pocketed and technically formidable. The Koreans—LG Chem, Samsung SDI—were about to pour billions into the space. If you wanted to play that game, you needed to write checks with a lot of zeros and hope that scale arrived before you ran out of money. But the materials that went into the cell, and the specialized coating, winding, and stacking machines that assembled the cell, were a different story. Those businesses were fragmented, technically difficult, capital-efficient, and structurally sticky. Once you qualified into a customer's bill of materials, you stayed there, because re-qualifying a new anode chemistry or a new coating machine took eighteen months of hell that no procurement officer wanted to sign up for.

Putailai was founded in Shanghai with that thesis etched into its DNA. The company's first business was not anode materials at all—it was coating equipment, the large roll-to-roll machines that spray electrode slurry onto copper and aluminum foil at the heart of every cell line. It was a deliberate starting point. Selling machines to ATL and, later, to CATL put Putailai in the room during every cell-line expansion. It gave Liang Feng's team a real-time view of which materials those customers were buying, which suppliers were failing qualification, and which sub-segments of the bill of materials were priced richly enough to be worth attacking.

That view, in turn, set up the next decade of moves. Because by late 2013, Putailai's team had mapped the entire interior of a pouch cell—anodes, separators, aluminum-plastic film, binders, conductive additives—and had a list of small, technically strong, capital-starved Chinese companies they could buy to own those positions. The pit crew, it turned out, had been sitting in plain sight the whole time.

III. Inflection Point 1: The "M&A as R&D" Strategy, 2013–2017

There is a particular flavor of Chinese industrial deal-making that Western investors often miss. It is not the splashy cross-border megadeal of the early 2010s, when companies like ChemChina were writing checks for Syngenta. It is not the IPO-and-roll-up strategy that private equity imported from the U.S. It is something quieter: a small, listed or pre-listed Chinese company buying a technically gifted but capital-constrained counterpart for what looks, in hindsight, like a rounding error, and then plugging that acquired firm into a much larger customer's supply chain. Putailai turned this into an art form between 2013 and 2017.

The first major move came in 2013, when Putailai acquired Shenzhen Xincheng Graphite Co. Xincheng was a small, scrappy anode material producer that had been supplying artificial graphite into the consumer electronics battery market. It had customers. It had a working recipe. It did not have the capital to scale, and it did not have a pathway into the EV cell makers who were just beginning to place serious orders. Putailai's pitch to Xincheng's management was simple: you bring the chemistry, we bring the capital and the ATL/CATL relationship. The deal was executed at what industry sources described as a low single-digit multiple of EBITDA—a valuation that would be unthinkable seven years later, when comparable anode assets would trade at 20 to 30 times earnings in the 2021 bull market.

The second move, in 2014, was the acquisition of Dongguan Zhuogao—a specialist in the coating of electrode materials onto foils, which complemented Putailai's existing equipment business by giving it a direct hand in the application process itself. Then came Jiangxi Zichen, which expanded anode capacity. Then Ningde New Energy-related coating assets. Each deal was small by Western standards. Each was executed at a sensible price. And each one slotted a new piece of the puzzle into an increasingly integrated picture.

What's striking about this period is how un-Silicon-Valley the strategy was. There was no narrative about platforms or network effects. There was no valuation arbitrage play, no SPAC, no storytelling dressed up as strategy. Liang Feng and his team were doing the industrial-era equivalent of buying a chain of specialty welding shops so they could build better bridges. The genius was in the targeting: every acquired company had either a defensible process recipe, a qualified customer position, or both. And because Putailai was paying cash-and-stock at modest multiples, each acquisition was accretive almost from day one.

The contrast with Western conglomerate M&A of the same era is instructive. GE Power was paying massive premiums for Alstom in 2015 on promises of synergy that never materialized. Valeant Pharmaceuticals was doing roll-ups at frothy prices that later imploded. Putailai was doing the opposite: buying below replacement cost, integrating aggressively, and using its ATL-seeded customer relationships as the distribution layer. The technical due diligence was done by engineers who had worked next to the target's engineers for years. There was no "synergy slide." There was, instead, an honest assessment of what each shop could make and what Putailai could get that shop to ship once it had capital and customer access.

By the time Putailai listed on the Shanghai Stock Exchange in November 2017, the company had transformed itself from a coating-equipment specialist into a diversified battery materials and equipment platform with a coherent vertical structure. The IPO raised the public profile of the company, gave it access to a currency for further M&A, and put Liang Feng's ownership stake on the map. It also did something more important and less noticed at the time: it signaled to the market that Putailai was entering a new phase. The M&A-as-R&D chapter was closing. The next chapter would require tens of billions of renminbi in capital expenditure. And for that, the company would need the kind of balance sheet that only a public listing could support.

The smart money reading the 2017 prospectus should have noticed one line in particular: a reference to plans for "integrated graphitization capacity" in western China. Almost no one did. They would, within five years.

IV. Inflection Point 2: The Vertical Integration Gamble, 2018–2022

To understand why Putailai's next move was so audacious, you first have to understand what an anode actually is, and why the business of making one is really the business of selling electricity.

A lithium-ion battery has two electrodes: a cathode, usually some mix of nickel, cobalt, manganese, and lithium, and an anode, which in the overwhelming majority of cells on the road today is made of graphite. Specifically, it is made of artificial graphite—a synthetic material produced by baking petroleum coke or needle coke at temperatures exceeding 2,800 degrees Celsius in specialized furnaces for days at a time. That baking process is called graphitization. And graphitization, as any chemical engineer will tell you, is a euphemism for "enormous, sustained electricity consumption." Roughly half of the total cost of producing an artificial graphite anode is the cost of the electricity that feeds the graphitization furnaces.

For years, the Chinese anode industry lived with a strange bifurcation. The big-name anode houses—BTR, Shanshan, Putailai, Kaijin—did the front-end material processing and the final product finishing, while outsourcing the graphitization step to third-party job shops clustered in Inner Mongolia, Sichuan, and Yunnan, where electricity was cheap. This was fine in a steady-state market. But it meant that the anode producers' margins were hostage to two things they did not control: the spot price of petroleum coke, and the contract price of graphitization tolling. When both moved against them at the same time—as happened in 2021, when Chinese coke prices spiked and graphitization tolling rates nearly doubled—anode producers got squeezed from both ends. Industry gross margins for pure anode makers fell into the high single digits. Some quarters were close to cash breakeven.

Liang Feng had seen this coming. Starting in 2018, Putailai began pouring capital into its own integrated graphitization bases. The first major facility was in Xinghe, Inner Mongolia—a windswept, coal-adjacent corner of the autonomous region where industrial electricity tariffs were among the lowest in China and where the grid had substantial excess capacity from the buildout of nearby renewables. The facility was designed not just to do graphitization tolling for Putailai's own anode production but to integrate the entire flow: raw coke processing, high-temperature graphitization, surface treatment, and final sizing, all under one roof. The company then replicated the model with further capacity in Sichuan, in Liyang, and in additional Inner Mongolia phases.

The scale of the capital commitment was the thing that separated Putailai from its peers. Between 2019 and 2022, the company committed tens of billions of renminbi to integrated graphitization and anode capacity—numbers that, relative to its own revenue base at the time, were jaw-dropping. BTR, the market leader by volume, was also integrating, but more slowly and with a more conservative balance sheet posture. Shanshan was distracted by corporate restructuring and a strategic shift into polarizers. Kaijin was smaller and more dependent on joint-venture capital. Putailai went all in.

The logic was simple and brutal. In a commodity-exposed materials business, the only durable advantage is being the lowest-cost producer. By owning its graphitization, Putailai converted a variable cost—third-party tolling fees that moved with the market—into a fixed cost, its own depreciation and electricity contracts. In a down cycle, when tolling rates collapsed, the in-house assets would look no better than the market. But in an up cycle, when tolling rates spiked, Putailai's margins would hold while competitors' collapsed. And in the long run, the company's effective cost per ton of finished anode would sit ten to fifteen percent below the industry average, permanently.

That is exactly what happened. When the 2022 capacity wave finally broke over the anode industry in late 2023 and 2024—when new graphitization capacity from every major player and a dozen minor ones came online and tolling rates collapsed by more than half—the other three Big Four anode houses watched their gross margins compress into the mid-teens and, in some quarters, into the low teens. Putailai's anode gross margins held above 25%. The reason was not that the company had a secret recipe for graphite. It was that the company had spent four years and an enormous amount of capital buying permanent access to cheap electricity in Inner Mongolia.

This is the Putailai that investors are looking at in 2026. The vertical integration gamble is no longer a gamble. It is, in the Helmer parlance, a Process Power that has crystallized into durable unit economics. The capital has been deployed. The assets are depreciating on schedule. And the harvest phase, in theory, has just begun.

V. Management & Ownership: The Liang Feng Era

There is a scene that people who have worked with Liang Feng describe with some amusement. It is an investor meeting, circa 2020, in the Putailai headquarters on Shanghai's Tianyaoqiao Road. A large Western institutional shareholder has flown in a delegation. They want to understand Putailai's equipment business, its materials roadmap, its plans for Europe. Liang Feng enters the room, greets the guests politely, sits down, and spends the next ninety minutes saying almost nothing. His CFO and head of strategy handle the substantive answers. Liang Feng listens, occasionally nods, occasionally asks a short, technically precise question. When the meeting ends, he shakes hands and leaves. One of the Western analysts, packing up his laptop, turns to his colleague and says, "I have no idea what just happened."

What just happened is that the investor met the real Liang Feng—a low-profile, execution-obsessed, near-media-phobic operator who believes that the company's output is the story and that everything else is a distraction. In an industry where flamboyant founders like William Li of NIO and He Xiaopeng of XPeng have turned their Weibo accounts into quasi-investor-relations platforms, Liang Feng is a deliberate anomaly. He rarely gives interviews. He does not participate in industry-ceremony self-congratulation. When he does appear in print, it is usually in a tightly scripted annual report letter or in the prepared remarks of a company event.

This matters for two reasons. First, because owner-operator alignment is a measurable thing, and it is unusually strong at Putailai. Liang Feng, through direct and indirect holdings, controls a meaningful stake in the business—commonly cited in the 25% to 30% range, depending on how one accounts for related-party vehicles. His personal wealth is overwhelmingly tied to the equity performance of 603659.SS, and his time horizon—judging by the capital allocation decisions the company has made since 2018—is measured in decades, not quarters. The Inner Mongolia graphitization plants do not pay back in two years. They pay back over a cycle, and only a founder with long tenure and skin in the game would have signed those checks with the conviction Putailai did.

Second, because the executive bench below Liang Feng looks different from the typical Chinese industrial company. The "ATL Mafia" culture that seeded the company in 2012 has been deliberately preserved, with a steady rotation of senior engineers and operations leaders moving between Putailai's subsidiaries to cross-pollinate technical know-how. The company's R&D-heavy employee stock ownership plans have become something of an industry benchmark for how to retain specialized talent in a market where top battery engineers can be poached by CATL, BYD, or any one of a dozen venture-backed start-ups for a fifty-percent raise. Putailai's ESOPs vest over multi-year horizons and are tied to concrete technical milestones, not just stock price performance. That structure has held the core team together through several brutal industry cycles.

The executive style that has emerged from all of this is what Hamilton Helmer might call process-oriented leadership. Putailai does not make bold prognostications about being the world's largest anode producer, or about beating BTR on volume, or about capturing forty percent of the global market. The company simply reports, quarter after quarter, on capacity additions, new customer qualifications, and gross margin trends. In a noisy industry, the company's silence is itself a signal. Investors who have held the stock through its full history—from the 2017 IPO through the boom, the bust, and the recovery—have come to recognize that the absence of drama is usually good news.

The risks on the governance side are worth naming honestly. Concentration of control at a single founder is always a double-edged sword: it enables long-term thinking but creates key-person risk. Related-party transactions inside any large Chinese industrial group deserve ongoing scrutiny, and Putailai is not exempt from that baseline vigilance. The company's affiliated holdings, its joint ventures, and its supply arrangements with customers who are themselves shareholders of group entities all require careful reading of the annual report. But in the decade since listing, Putailai has not triggered the kind of governance flashpoints that have marred other Chinese industrials. The disclosures have been reasonably thorough. The auditor relationship has been stable. The numbers have tied out.

Perhaps the best summary of the Liang Feng era is this: the man has built something close to a ten-billion-dollar company by, apparently, not trying very hard to be famous. He has instead focused on the boring problems—furnace yield, coating uniformity, copper foil thinness—and let the compounding do its work. It is a style that would be familiar to any reader of Charlie Munger.

VI. The "Hidden" Businesses: Beyond Anodes

If all Putailai did was make the world's lowest-cost artificial graphite anode, it would still be a good business. But it would not be the business it has become. The company's second, third, and fourth acts—its equipment division, its aluminum-plastic film operation, its separator coatings, and its nascent composite current collector unit—are what turn Putailai from a single-product commodity champion into a diversified platform for the interior of the battery. Each of these lines has a distinct competitive structure, and each deserves its own look.

Start with equipment. Putailai, through its subsidiary and affiliates, is one of the two largest suppliers of coating machines and automated production lines to CATL and to several other top-tier cell makers. This is the business the company was originally founded on in 2012, and it remains the least understood part of the story. Coating machines are the thousand-ton, precision-engineered roll-to-roll monsters that lay the electrode slurry down on copper foil for the anode and on aluminum foil for the cathode. Each machine is custom-engineered for a specific chemistry, a specific thickness, and a specific line speed. A modern gigafactory might use fifty to eighty such machines. They are expensive, they are sticky, and the margin structure for the top suppliers is considerably richer than the materials business. Putailai's equipment business has historically run at gross margins well above the company average. It also operates as an intelligence network: every machine Putailai installs in a CATL factory is a real-time read on what that factory is about to make and in what volumes.

The aluminum-plastic film business is a different kind of jewel. Aluminum-plastic film—often called pouch film—is the soft, laminated outer skin of a pouch battery cell. It has to be thin, chemically inert, impermeable to moisture, and structurally robust enough to survive a decade of charge cycles. For years, this market was dominated by Japanese suppliers—Showa Denko, Dai Nippon Printing—who held proprietary lamination technology and extracted high margins from Chinese pouch cell makers. Putailai methodically built up a domestic alternative through a series of acquisitions and R&D investments, and has been steadily taking share from the Japanese incumbents in segments ranging from consumer electronics to EV pouch cells. The business is smaller than anodes in revenue, but it is structurally high-margin and strategically important: it is one of the few places in the battery supply chain where a Chinese champion is displacing an entrenched Japanese one, rather than the other way around.

Separator coatings are the third hidden gem. A separator is the thin polymer membrane that sits between the anode and the cathode in every lithium-ion cell, preventing short circuits while allowing ions to pass through. In modern high-energy-density cells—especially those using high-nickel cathodes or silicon-enhanced anodes—the separator is coated with ceramic or polymer layers to improve thermal stability and prevent dendrite formation. That coating is often applied by third-party specialists using proprietary chemistries, and Putailai has built a strong position there. The interesting strategic point is that as battery chemistry moves toward higher energy density—toward silicon-blended anodes and toward nickel-rich cathodes—the complexity and value of the separator coating increases. Putailai's coating technology is, in effect, a leveraged play on the continued evolution of battery chemistry. If the world standardizes on simpler chemistries, the business is less special. If the world keeps pushing the energy-density frontier, Putailai's coatings become more valuable.

And then there is the composite current collector. This is the part of the Putailai story that most excites the analysts who have studied the company closely, and the part that is hardest to evaluate because the commercial ramp is still early.

A current collector is the thin metal foil—copper on the anode side, aluminum on the cathode side—that carries electrons out of the active material and into the external circuit. In a conventional cell, the anode's current collector is a sheet of pure copper foil, typically around six microns thick. Copper is dense. It is also expensive. In the weight of a finished battery pack, the current collectors can account for ten to fifteen percent of the total mass. If you could replace most of that copper with something lighter, you would reduce pack weight, improve energy density, and cut cost.

This is what composite current collectors do. Instead of a pure copper foil, the composite design uses a thin polymer film—polypropylene or polyethylene terephthalate—sandwiched between two ultra-thin layers of copper. The polymer provides structure; the copper provides conductivity. The resulting foil can weigh less than half of a pure-copper foil while maintaining, or even improving, certain safety characteristics. Because the polymer core is non-conductive, a composite foil is inherently more resistant to internal short-circuiting during puncture or deformation—a meaningful safety improvement. For the reader who is not a battery engineer, the analogy is roughly this: imagine replacing a solid steel beam with a fiberglass beam plated in a microscopically thin layer of steel. You keep most of the electrical properties, you shed a huge amount of weight, and you pick up mechanical forgiveness.

Putailai was one of the first Chinese firms to commit serious capital to composite current collectors, building out production lines and qualifying product with multiple tier-one cell customers. The commercial adoption of composite foil has been slower than the most aggressive analyst projections from 2022 and 2023, largely because the production economics require high yields at sub-micron copper-plating thickness and because battery makers are conservative about qualifying new current collector designs. But the direction of travel is clear. If composite current collectors achieve meaningful penetration in the EV cell market over the next three to five years, Putailai is positioned to be one of the primary beneficiaries. And if they do not, the capital at risk is manageable relative to the company's overall balance sheet.

Taken together, these four business lines—anodes, equipment, aluminum-plastic film, and composite current collectors—give Putailai a diversified exposure to the entire interior of a lithium-ion cell that no other company in the world quite matches. Each line has its own competitive dynamic. Each has a different margin structure. And each one tends to do better in a slightly different scenario, which provides natural hedging within the portfolio.

VII. The Playbook: 7 Powers & Porter's 5 Forces

To evaluate whether Putailai's moat is real or imagined, it helps to run the company through two of the more rigorous frameworks investors use—Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. The exercise is not academic. It forces you to articulate exactly why this company should be able to keep its gross margins where they are, when the industry's structural gravity is pulling them down.

Under Helmer's framework, the first and most important power Putailai has is Process Power. This is the power that comes from proprietary operational know-how that cannot be easily copied, even by a competitor who has studied the playbook. Putailai's graphitization process—the specific thermal profiles, the feedstock selection, the crucible loading patterns, the furnace scheduling that achieves high yield at low energy consumption—has been refined over more than a decade, and it lives in the heads of hundreds of engineers in Inner Mongolia, Sichuan, and Jiangsu. A new entrant building a greenfield graphitization plant would take three to five years to reach Putailai's current yield curve, and during that time would run at a meaningful cost disadvantage. Process Power compounds quietly. It does not look like a moat from the outside. It looks, from the outside, like slightly-better margins that people assume must be temporary. They are not.

The second power is Scale Economies. Putailai's integrated production bases in Inner Mongolia and Sichuan are sized to the demand of CATL, LG, and the other tier-one cell customers the company serves. Fixed costs—depreciation, central administration, R&D—are spread over a volume base that few competitors can match. In a business where electricity contracts are negotiated partly on committed volume, Putailai's scale translates directly into a lower per-kilowatt-hour input cost. This is the kind of scale advantage that is visible in the unit economics and that widens, rather than narrows, as the company grows.

The third power is Cornered Resource, and it is the most debated one for Putailai. The "resource" in question is the relationship with ATL and CATL—the shared DNA, the personal networks, the years of co-development, the embedded position on qualified supplier lists. Some investors will tell you that this is not really a cornered resource because it is not legally exclusive; CATL buys anodes from BTR, from Shanshan, and from Kaijin as well. That is true. But the depth of the Putailai-CATL relationship—the fact that Putailai's equipment lives on CATL's production floors, that the two companies have co-developed product specifications across multiple generations, and that Putailai's Jiangsu and Sichuan facilities were sited in part to serve CATL's own nearby plants—creates a switching cost that is hard to see on a spreadsheet but very real in practice. It is not a pure cornered resource in Helmer's strictest sense, but it is closer to one than most competitive relationships in this industry.

Where Putailai is weakest on the Helmer framework is in Branding and Counter-Positioning. The company has no consumer brand and does not need one. And while its vertical integration strategy counter-positioned it against tolling-based competitors during a specific window, most of the industry has since copied the strategy, blunting the counter-positioning edge.

Now Porter. Bargaining Power of Buyers is high, and would be higher if not for qualification switching costs. CATL, LG Energy Solution, Samsung SDI—these are among the most powerful procurement organizations in industrial history. They squeeze every supplier. But they cannot squeeze indefinitely, because swapping out a qualified anode supplier mid-product-cycle risks cell performance and safety, and no cell maker wants to take that risk. The result is that Putailai's customers push hard on price at every contract cycle but rarely walk away. Over time, the company has also worked to diversify its customer base internationally, particularly into Korean and, increasingly, European cell makers, which dilutes concentration risk.

Bargaining Power of Suppliers is moderate. The key inputs—needle coke, petroleum coke, specialty polymers, copper—are commodities with their own price cycles. Putailai's scale gives it some leverage, but it is not a price setter in any of these markets. The company mitigates this by holding strategic inventory, by signing multi-year supply contracts where possible, and by vertical integration into the highest-cost input, which is electricity for graphitization.

Threat of Substitutes is, somewhat counterintuitively, low in the near-to-medium term and potentially favorable in the long term. Silicon-based anodes have been discussed as the "next chemistry" for years. In practice, silicon is almost always blended into a graphite anode matrix rather than replacing it outright, because pure silicon anodes swell and crack during cycling. Moving to silicon-blended anodes does not reduce the need for Putailai's products; it increases the need for specialized coating and binder chemistries that sit adjacent to Putailai's core competencies. Lithium-metal and solid-state batteries are further out on the horizon and would, at scale, reduce graphite demand—but the timelines are measured in decades, not years, for cost-competitive deployment.

Threat of New Entrants is real but bounded. Plenty of new anode capacity has come online in China in the past three years, which is exactly what compressed industry margins during the 2023-2024 downturn. But new entrants without integrated graphitization, without tier-one customer qualification, and without the cost structure Putailai enjoys have found that adding capacity is the easy part and making money on that capacity is the hard part. The industry has effectively been in a shakeout, and Putailai's cost position means it is usually on the right side of that shakeout.

Intensity of Rivalry among existing competitors is high. The Big Four anode houses compete aggressively on price, on new product introductions, and on customer-specific technical roadmaps. This rivalry is what prevents any single player, including Putailai, from earning outsized monopoly profits. It also, paradoxically, is what reinforces Putailai's position, because in a rivalry-intense industry, the low-cost producer with the most diversified product mix tends to be the survivor.

The integrated picture, then, is a company with two durable powers—Process Power and Scale Economies—one contingent but valuable power in the form of its CATL relationship, and a Porter-type environment that is tough but navigable. It is not a monopoly. It is not even close. But it is a very good business.

VIII. The Bear vs. Bull Case

Every good investment thesis has a mirror image. Here is Putailai's.

The bull case is straightforward. The vertical integration phase is effectively complete. The capital has been spent, the assets are built, and the depreciation schedule is predictable. From here, incremental revenue drops through to gross profit at a margin structure that the rest of the industry cannot match. The anode segment should continue to earn 25% or better gross margins through the cycle, while competitors oscillate in the 10% to 18% range. The equipment business continues to throw off high-margin cash and provides privileged information about cell industry capacity additions. The aluminum-plastic film business displaces Japanese incumbents and grows into a larger, stickier profit pool. And the composite current collector business, if it reaches mass adoption, becomes a second major growth engine that could rival anodes in economic importance over the next decade.

The macroeconomic backdrop supports this view. Global EV adoption, despite the occasional slowdown in one market or another, is continuing a secular trajectory that will require more battery capacity in every year of the next decade than the year before. Energy-storage-system deployments are scaling even faster, with grid-scale storage emerging as a structural market that most investors underweighted until very recently. Every marginal gigawatt-hour of cell capacity requires anodes, separators, aluminum-plastic films, coating machines, and current collectors. Putailai sells all of them.

The bull case also leans on a simple mathematical observation. Putailai trades at a multiple that implicitly assumes the company's structural margin advantage is temporary. If the market is wrong about that—if Process Power and Scale Economies are actually durable—then the current earnings are the floor of a multi-year earnings power that the consensus has not yet priced. This is the classic Helmer-style moat mispricing, and it is the reason long-only institutional investors with a decade-plus time horizon have been accumulating positions through the 2023-2024 downturn.

Now the bear case, which is serious and deserves to be taken seriously.

The largest bear argument is geopolitical. Putailai is a Chinese company selling into a battery supply chain that is increasingly bifurcating along geopolitical lines. The U.S. Inflation Reduction Act, signed in August 2022, created a framework of tax credits that explicitly exclude components produced by "foreign entities of concern"—a category that, in practice, includes most Chinese battery material suppliers. European regulators have been less categorical but are moving in a similar direction through the Critical Raw Materials Act and various supply-chain-resilience initiatives. A meaningful share of the global EV market is, in effect, being walled off from Chinese materials suppliers.

Putailai's response has been to build an international footprint. The company has announced and progressed facilities in Sweden and has explored other European locations, with the intent of serving European cell makers with European-produced anodes. This is a strategically necessary move, but it is economically difficult. European electricity is vastly more expensive than Inner Mongolian electricity. European labor is more expensive. European regulatory compliance is slower and more costly. A ton of artificial graphite produced in Sweden will be more expensive than a ton produced in Xinghe, possibly by a meaningful margin. The question is whether European cell makers and their automaker customers are willing to pay the premium for local supply—and the early evidence suggests that some are, some aren't, and the margin structure of Putailai's European operations is unlikely to match the Chinese business for many years.

The second major bear argument is cyclicality and capacity risk. The battery materials industry has a long history of boom-and-bust cycles driven by capacity additions that lag demand signals by eighteen to twenty-four months. Putailai has navigated the latest cycle exceptionally well, but nothing prevents a new capacity wave from reappearing in 2027 or 2028, particularly if several Chinese competitors decide simultaneously to push into the higher-margin coated separator or composite current collector segments. The company's margin structure is not immune to industry supply shocks; it is more resilient, not bulletproof.

The third bear argument is technological disruption. The assumption that graphite remains the dominant anode material for the next decade is a reasonable one, but it is not a certainty. Aggressive scenarios for silicon-anode penetration could, in theory, erode graphite demand faster than consensus expects. Solid-state battery commercialization—if and when it happens—changes the separator and electrolyte picture in ways that could affect several of Putailai's business lines. These are tail risks rather than base-case concerns, but a long-term investor has to carry them honestly.

A fourth, more subtle concern is customer concentration. Putailai's revenue is disproportionately tied to a small handful of top-tier cell makers, and within that handful, CATL is the largest single customer by a considerable margin. This concentration is what has enabled the company's scale and its cost structure. It is also a source of vulnerability: any serious deterioration in the Putailai-CATL relationship, or any strategic move by CATL to in-source more of its materials, would have a meaningful impact on Putailai's volumes. There is no public evidence of such a deterioration, and the interlocking nature of the two companies' operations makes a sudden rupture unlikely. But concentration is concentration, and it deserves to be monitored.

The integrated reading, for a long-term fundamental investor, is that the bull and bear cases are not symmetric. The bull case rests on durable, observable operating advantages that are unlikely to disappear quickly. The bear case rests on macro and regulatory forces that could, in principle, damage the business but have so far not done so at a scale that offsets the operating story. How those two cases resolve over the next decade will depend on factors—geopolitics, technology adoption curves, energy prices—that no one can forecast with confidence.

IX. KPIs to Watch and Myth vs Reality

If you were going to watch only a handful of metrics to judge how the Putailai story is unfolding over the next several years, which ones would matter most? For this company, three stand out above all others.

The first is the anode segment gross margin. This single line item is the cleanest real-time read on whether Putailai's structural cost advantage is holding up against industry capacity additions and competitor catch-up. When this number is above 25%, the moat is intact. When it drifts into the low twenties, the industry is applying pressure. When it falls below twenty, the bear case is strengthening. No other metric captures so much of the story in so little space.

The second is the customer-and-geography mix, particularly the ramp of European revenue as a percentage of total sales. This is the measure of whether the company is successfully executing its geopolitical diversification. Growth in European revenue, without severe margin damage, is the signal that Putailai can maintain its platform position as the global battery industry bifurcates. Stagnant or margin-destroying European growth is the signal that the geopolitical bear argument is winning.

The third is the commercialization of composite current collectors, measured both in revenue contribution and in customer qualifications. This is the call option embedded in the stock. If composite current collectors are still less than five percent of revenue three years from now, the option was worth less than the market was pricing. If they cross ten to fifteen percent of revenue and begin to show the margin profile that early analysis suggested they could earn, then Putailai's earnings power in the late 2020s is materially higher than consensus currently assumes.

With those KPIs in hand, it is worth pausing to fact-check a few consensus narratives about this company—the myth-versus-reality exercise that separates the prepared investor from the crowd.

Myth number one: "Putailai is just another Chinese anode maker." Reality: the company is a diversified materials and equipment platform with four distinct business lines, each with its own competitive dynamic. Treating Putailai as a commodity anode pure-play misses most of the investment case.

Myth number two: "The CATL relationship is the whole story." Reality: the CATL relationship is important—perhaps the single most valuable intangible asset the company owns—but it is not the entire story. The equipment business, the aluminum-plastic film business, and the emerging composite current collector business would be meaningful standalone operations even without CATL. The relationship amplifies, rather than defines, the overall value proposition.

Myth number three: "Vertical integration is a commodity strategy that everyone can copy." Reality: everyone can announce vertical integration. Very few can execute it at Putailai's cost structure, because the relevant Process Power—yield optimization, feedstock selection, furnace operations—lives in the accumulated experience of engineers who have been running these lines for a decade. New entrants will spend years catching up, and some will never fully catch up.

Myth number four: "The U.S. IRA kills the Chinese anode industry." Reality: the IRA constrains Chinese anode suppliers in the North American market specifically. The global market for batteries is not, and will not be, exclusively North American. Europe, Southeast Asia, the Middle East, Latin America, and China itself—which is by far the largest EV market on the planet—remain addressable. The IRA is a headwind, not an extinction event, and Putailai's European buildout is a rational response to it.

And finally, a brief second-layer diligence aside. Any long-term investor in Putailai should periodically check for changes in the auditor relationship, for material related-party transactions within the broader group structure, for shifts in the disclosure of graphitization electricity contracts, and for any indication that the company is pushing capacity additions ahead of demand signals in a way that could presage a cycle mistake. None of these flags have been waving red in recent disclosures, but they are the places where an industrial company of this scale would first show stress, and they deserve periodic review.

X. Conclusion & Final Reflections

There is a particular kind of business that rewards patient, careful reading of annual reports—the kind where the important things are almost never in the headline and are often not even in the press releases, but instead live in the footnotes of the capital expenditure disclosures, the electrical capacity announcements from Inner Mongolia provincial authorities, and the incremental procurement qualifications that show up as brief paragraphs in supplier filings. Putailai is that kind of business.

What Liang Feng and his team have built over the past fourteen years is a textbook example of how to construct a durable industrial moat without ever making noise. The company did not invent the lithium-ion battery. It did not invent the artificial graphite anode. It did not even invent vertical integration as a strategy; steel, chemicals, and semiconductors have been running that playbook for a century. What Putailai did was recognize, earlier than almost anyone else in its industry, that the economics of the lithium-ion anode were really the economics of electricity, and that whoever owned the integrated flow from coke to finished anode at the lowest cost per kilowatt-hour would eventually own a durable margin advantage. Then the company spent a decade executing that insight with a single-mindedness that even its largest competitors have struggled to match.

There is a lesson embedded in this story for anyone trying to understand the broader energy transition. The public imagination of the transition is dominated by the visible things—the Teslas and BYDs on the road, the gigafactory openings, the headline-grabbing EV launches. Those are real and important. But underneath every visible car and every visible factory is an invisible supply chain of specialized materials, specialized equipment, and specialized processes, and a surprising amount of the economic value of the transition is captured not at the visible layer but at the invisible one. The winners at the invisible layer will not be household names. They will be companies most consumers have never heard of, run by executives who prefer not to be interviewed, operating in industrial parks in places most travelers will never visit. Putailai is one of those companies.

The final thing worth saying, and the thing that matters most for any investor trying to frame this story at a high level, is this: the hardest investment question is not usually "Is this a good business?" The hardest question is "Is this a good business that the market has already fully priced?" On that question, different investors will arrive at different answers, and this article has not tried to answer it. What the article has tried to do is lay out, as clearly and honestly as possible, what kind of business Putailai is, how it got to where it is, what the levers are that will determine where it goes next, and what the real risks look like. The arithmetic of whether any of that is adequately reflected in 603659.SS's current trading range is a question every reader will have to work out for themselves, using their own time horizons, their own cost-of-capital assumptions, and their own tolerance for the particular blend of operational excellence and geopolitical exposure that Putailai represents.

In the quiet rooms of Shanghai where Liang Feng sits through investor meetings and says almost nothing, there is probably a small satisfaction in having built a company that the market struggles to describe in a single sentence. Putailai is an anode maker and an equipment supplier and a film specialist and a coating innovator and a current-collector pioneer. It is a story about capital allocation, about M&A discipline, about vertical integration, about the physics of electrons moving through graphite, and about the long patience it takes to turn chemistry and process expertise into durable economic value. It is, in the end, exactly the kind of company that built the great industrial economies of the twentieth century—and exactly the kind of company that will build the electrified economies of the twenty-first.

The shovels, as it turns out, were always worth more than the gold.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube