Bank of Chengdu: The "Western Growth" Engine

I. Introduction & The "So What"

Picture the skyline of Chengdu at dusk. A city of sixteen million people, draped in neon, with the scent of Sichuan peppercorn drifting from a thousand hotpot restaurants into humid evening air. Look east from the new Tianfu central business district and you see cranes—still, in 2026, hundreds of them—hovering over a city that has been under permanent reconstruction for three decades. Look west and you see the beginnings of the Longquan mountains, where Intel built the largest chip packaging plant in Asia and where Foxconn cranked out the iPads that ended up on kitchen counters in Cleveland and Copenhagen.

Now, somewhere in the middle of that panorama, on a corner of Qingjiang Middle Road, sits a building most foreign visitors will never notice. It is the headquarters of Bank of Chengdu. From the outside, it is unremarkable—glass, concrete, Chinese state-enterprise austere. From the inside, it houses one of the strangest and, arguably, most impressive financial stories in modern Chinese capitalism.

Here is the setup. When most global investors think of Chinese banks, they conjure the Big Four: ICBC, CCB, Agricultural Bank, Bank of China. They imagine state-owned behemoths financed by household savings, stuffed with policy loans, trading at perennial discounts to book value because nobody believes the book value. The assumption is that Chinese banking is where capital goes to die.

That assumption is wrong—at least at the edges. Because hidden in the Sichuan basin, shielded by a ring of mountains and a ring of political protection, is a regional bank that has quietly delivered return on equity in the high teens for years, an NPL ratio under 1%, and a market capitalization that more than tripled since 2019. This is not a bank that grew by recklessly chasing loan volume or leveraging up the balance sheet. It is a bank that grew by becoming, in the phrase its chairman uses over and over, "deeply plowed" into its home soil.

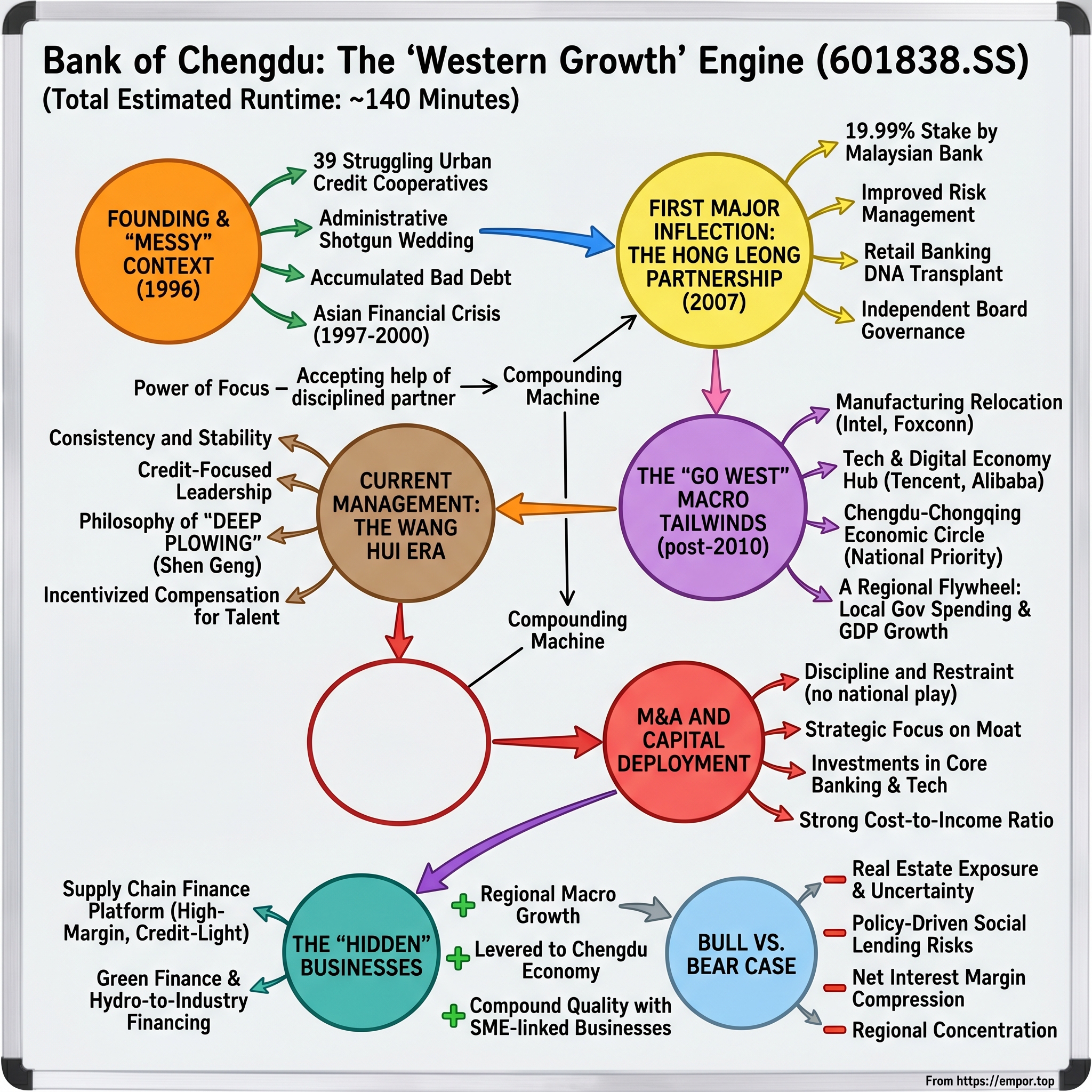

This is the story of how Bank of Chengdu, born as an administrative shotgun wedding of 39 struggling urban credit cooperatives in 1996, became one of the most admired city commercial banks in China. It is the story of a Malaysian bank's improbable stake, a state-owned parent that actually behaved like a patient capital allocator, and a chairman named Wang Hui who turned a regional utility into something resembling a compounding machine.

More than that, it is a story about the Chinese economy's single most important geographic migration since Deng Xiaoping opened the southern coast: the move west. Beijing decided, around 2010 and with redoubled conviction by 2021, that the next phase of national development would not be another Pearl River Delta. It would be the Chengdu-Chongqing Economic Circle. That policy decision reshaped a half-dozen provinces. And it handed a small city bank on Qingjiang Road a tailwind that has not yet run out.

The roadmap for the next two hours walks through all of it. The messy 1990s consolidation. The near-death experience of the early NPL crisis. The game-changing 2007 minority investment by Malaysia's Hong Leong Bank that functioned less like a capital raise and more like a DNA transplant. The macro surge that transformed the Sichuan interior into what Chinese media now call the "fourth pole" of the national economy. The management philosophy of Wang Hui and his team. The hidden supply chain finance business growing at a pace that regional banks should not be able to sustain. And finally, the bull and bear cases, the Porter forces, the Helmer powers, and the question any investor must answer: is Bank of Chengdu a generic regional lender riding a cyclical wave, or is there something structurally different here?

Let's find out.

II. Founding & The "Messy" Context

The year is 1996. Bill Clinton is running for reelection. China's GDP is still smaller than Italy's. And in Chengdu, provincial officials have a problem.

Scattered across the city are 39 small urban credit cooperatives—institutions that took deposits and made loans, mostly to local collectives and small businesses, but with capital ratios that made actuaries weep and loan books that nobody, not even the managers, fully understood. These cooperatives had been set up in the 1980s as experimental units of the planned-economy reform. By the mid-1990s they had accumulated so much bad debt and so little governance that the central government decided they were, in polite Chinese bureaucratic language, "a systemic risk at the urban level."

The solution was administrative. Gather them up. Fold them together. Stamp a new name on the merged entity and give it a charter as a proper joint-stock commercial bank. On December 30, 1996, Chengdu City Cooperative Bank opened its doors, the product of a shotgun wedding of those 39 cooperatives. It was the standard playbook the People's Bank of China deployed across dozens of Chinese cities that decade—Beijing City Commercial Bank (which became Bank of Beijing), Shanghai City Commercial Bank (Bank of Shanghai), Nanjing, Ningbo, Hangzhou. A generation of "city commercial banks" was born not out of entrepreneurial ambition but out of regulatory necessity. They inherited the deposits. They also inherited the skeletons.

Call it what it was: these banks were, in their earliest years, garbage bins for local bad debt. The cooperatives that merged into Chengdu City Cooperative Bank had funded textile factories that would never reopen, small traders who had vanished, state-affiliated ventures whose only ongoing activity was accumulating interest arrears. The new bank's opening balance sheet was, by any honest accounting, deeply impaired.

What happened next nearly killed it. The late 1990s were brutal for Chinese banking. The Asian Financial Crisis in 1997 exposed the rot in every corner of the financial system. By 2000, the central government was grappling with NPL ratios across the entire banking sector that some Western analysts estimated at 30–40%. Nobody really knew. The big state banks were recapitalized through a series of extraordinary interventions—the creation of the four asset management companies, the transfer of problem loans at face value to what were effectively national bad banks, and, later, massive equity injections from the central Huijin fund.

City commercial banks were not so lucky. They were too small to be individually rescued. Many simply limped. Some were quietly merged out of existence. Chengdu City Cooperative Bank spent its first decade doing two things simultaneously: honoring deposits and trying, often desperately, to clean its loan book. This was not a bank growing; this was a bank surviving.

And yet—here is where a story starts to form—something valuable came out of that ordeal. In a bank that nearly failed, risk management becomes a religion rather than a department. The culture that emerged from those years, a bone-deep fear of hidden credit rot, is exactly the culture that would later produce an NPL ratio that became the envy of the industry. Fragility, in small doses and survived, breeds discipline.

By 2005, the bank had cleaned itself up enough to warrant a proper rebranding. It became Bank of Chengdu Co., Ltd., shedding the "cooperative" label and signaling, at least on letterhead, its transition to a modern commercial bank. But everyone who knew the institution understood it still needed something more. It needed capital. It needed governance. It needed, frankly, a grown-up in the room.

That grown-up arrived in 2007, speaking Malaysian-accented Mandarin.

III. The First Major Inflection: The Hong Leong Partnership

Imagine a meeting in a private dining room in Kuala Lumpur in early 2007. On one side of the table sits Quek Leng Chan, the billionaire Malaysian-Chinese patriarch behind the Hong Leong Group, a family conglomerate that had grown from a tin-trading company into one of Southeast Asia's most formidable financial empires. On the other side, a delegation from Sichuan—provincial officials, bank executives, a translator. On the wall, a map of Chinese cities shaded by GDP growth rates. And in Quek's hands, the pitch deck for a stake in a bank most of his international banking peers had never heard of.

Quek had been looking for a foothold in China for years. Every major global bank had one by 2007—HSBC took 19.9% of Bank of Communications, Citigroup grabbed a slice of Pudong Development Bank, Royal Bank of Scotland and Temasek bought into Bank of China, Goldman Sachs was in ICBC. The deals were eye-watering, oversubscribed, and valued at multiples the foreigners would soon wish they had never paid. Quek, characteristically, wanted something different. He did not want a Big Four bank where he would be one voice among many passive foreign strategics. He wanted a regional bank where a 19.99% stake—conveniently just under the 20% threshold that triggered tighter regulatory treatment—would actually mean something.

He found it in Chengdu.

The deal closed in 2007. Hong Leong Bank Berhad, Malaysia's fifth-largest bank by assets, paid for its 19.99% stake and landed two board seats. The headline price was, by the standards of the era, not dramatic. Chinese banks were trading at nose-bleed premiums to book value at the time. Hong Leong got a more reasonable entry, in part because Bank of Chengdu was regional and unglamorous, and in part because Quek was a harder negotiator than a large foreign institutional investor racing to get any China exposure before year-end.

But the real significance of the deal was never the price. It was what Hong Leong brought beyond the cash.

Start with risk management. Hong Leong had one of the most conservative, tightly-run credit cultures in Asian banking. It had survived the 1997 Asian crisis not by being lucky but by being stingy—tight underwriting, industry concentration limits, collateral discipline. Its management sent teams of auditors, credit officers, and operations specialists to Chengdu to help the local team build genuine, non-cosmetic risk frameworks. For a bank that had spent its first decade crawling out from under legacy bad debt, the arrival of a partner whose entire corporate identity was built on "don't lend to people who won't pay you back" was, for lack of a better word, formative.

Then retail banking. Chinese city commercial banks in 2007 were, almost universally, corporate lenders. They financed local SOEs, provincial infrastructure, real estate developers, and medium-sized industrial borrowers. Retail deposits existed but retail lending—credit cards, consumer finance, wealth management—was practically nonexistent. Hong Leong in Malaysia had a thriving retail franchise. It brought branch design standards, service protocols, product templates, and the institutional muscle memory of how to run a consumer bank. Not all of it translated. A Malaysian branch in Petaling Jaya is not a Chengdu branch in Jinjiang District. But the scaffolding it gave Bank of Chengdu—how to think about retail as a profit center, how to segment customers, how to price products—was a decade ahead of most of its city-bank peers.

Governance was perhaps the most underappreciated piece. For the first time in its history, Bank of Chengdu had a truly independent institutional shareholder sitting on the board, asking uncomfortable questions in imperfect Mandarin about related-party lending, provisioning adequacy, and strategy coherence. This was governance arbitrage at its finest. In a Chinese banking system where many regional banks were captive to their local governments, the presence of Hong Leong forced a more commercially rational discussion at every board meeting.

Was the deal a success for Hong Leong? Over time, unambiguously yes. It turned out to be one of the most profitable inbound minority investments in modern Chinese banking, measured in unrealized value creation from entry cost to eventual book value. The combination of Bank of Chengdu's later IPO, its subsequent earnings growth, and its rising valuation multiples made that 2007 stake a multi-bagger. More than that, it was strategically durable in a way that most of the big-bank foreign strategic stakes were not. HSBC, Goldman, RBS, and Temasek all trimmed or exited their Chinese bank stakes during the post-2008 global crisis, often at losses. Hong Leong stayed. It remains a major shareholder today.

For Bank of Chengdu, the Hong Leong deal was the moment the bank stopped being a local government utility and started becoming a commercially driven franchise. The transition was not instantaneous—cultures do not change in a quarter—but by the time the bank IPO'd on the Shanghai Stock Exchange in 2018, the institutional DNA it had inherited from those Kuala Lumpur boardroom meetings was fully embedded.

That DNA was about to meet the most powerful tailwind in Chinese economic geography.

IV. The "Go West" Macro Tailwinds

There is a moment, around 2010, when something shifted in Chinese economic policymaking that is still underappreciated by foreign investors. For three decades, the growth model had been unambiguous: coastal. Shenzhen, Shanghai, Tianjin, Xiamen, Guangzhou. Export-led manufacturing, concentrated in the coastal provinces, financed by coastal banks, moving goods through coastal ports. The interior was agricultural, demographically aging, politically important but economically secondary.

Then the wages on the coast got too high. Rising labor costs, rising land costs, rising compliance costs pushed coastal manufacturers to look inland. At the same time, central policymakers recognized that sustainable national development required rebalancing. The "Open Up the West" (西部大开发) campaign had been formally announced years earlier, but it was in the post-2008 stimulus era that the policy moved from slogan to infrastructure.

Enter Chengdu. A city that had always been consequential—Sichuan is China's most populous inland province, Chengdu is its capital, and the region's food production alone gives it civilizational weight—suddenly found itself at the intersection of three massive forces. First, manufacturing relocation. Intel announced a major chip assembly and test facility in Chengdu in 2003 and expanded it repeatedly through the 2010s. Foxconn followed, building enormous assembly operations. Texas Instruments, Dell, and Lenovo all set up major operations in the greater Chengdu area. By the middle of the 2010s, a meaningful share of the world's iPads was made in Sichuan.

Second, tech. Chengdu positioned itself aggressively as a software and digital economy hub. The city had long attracted engineering talent—Sichuan University, University of Electronic Science and Technology of China (UESTC), Southwest Jiaotong University collectively graduate tens of thousands of engineers each year—and starting around 2012, a wave of domestic tech companies opened Chengdu operations centers. Tencent, Alibaba, ByteDance, Huawei all have major presences. Gaming studios cluster in a way that has earned Chengdu the informal label of China's game development capital.

Third, and most important, policy. In 2020, the Chinese central government designated the Chengdu-Chongqing Economic Circle as a national strategic priority—the official phrasing was placing it on par with the Beijing-Tianjin-Hebei region, the Yangtze River Delta, and the Greater Bay Area. That designation, formalized further in the "Chengdu-Chongqing Dual-City Economic Circle" outline published in October 2021, was the single most important policy development for Bank of Chengdu in its history. It did not just imply more infrastructure spending. It implied that Beijing had decided the region was to become the fourth great pole of the Chinese economy, alongside the three established coastal clusters.

What does that mean in practice for a bank?

It means a flywheel. Local government infrastructure spending flows through the provincial investment platforms, many of which bank with—and borrow from—Bank of Chengdu. That spending attracts companies. Those companies hire workers. Those workers deposit salaries. Those deposits fund more lending. And because the Chengdu government is simultaneously the bank's anchor shareholder (via the Chengdu Communications Investment Group) and one of its largest customer cohorts, the flywheel is politically reinforced.

For the better part of a decade, Chengdu was the fastest-growing major Chinese city by almost any metric an investor would care about. GDP growth consistently exceeded the national average. Population grew. Fixed-asset investment grew. Retail consumption grew. In a Chinese economy that had obviously decelerated from its pre-2013 pace, Chengdu kept expanding at a rate that looked like 2007 instead of 2020. Bank of Chengdu's balance sheet expanded with it. Total assets doubled, then doubled again. Loan growth ran well ahead of the industry.

The interesting analytical question is whether this tailwind is durable or cyclical. The bear view treats the Chengdu-Chongqing surge as a one-off, financed by state investment, vulnerable to the same real estate deceleration that has bedeviled other regional economies. The bull view treats it as structural—a fundamental rebalancing of Chinese economic geography that will unfold over two or three decades and that has only played out halfway. Both views find evidence. The infrastructure buildout has clearly peaked in absolute spend. But the private economy now runs on rails that were built a decade ago, and in 2026, Chengdu's economy looks more diversified—more weighted to services, tech, advanced manufacturing, consumer brands—than it has ever looked.

That diversification matters because a regional bank's fate is inseparable from the regional economy's fate. A bank that rode a pure infrastructure cycle would now be facing headwinds. A bank embedded in a broadening, maturing regional economy has something closer to a compounding opportunity.

Which raises the next question: who is running this bank, and how are they allocating capital against that opportunity?

V. Current Management: The Wang Hui Era

Chinese bank CEOs have a reputation. It is not flattering. The stereotype, rooted in genuine observation, is of a revolving door of politically connected executives whose primary skill is navigating municipal Party politics, whose tenure is short, whose strategic horizon is the next provincial meeting, and whose real career ladder leads either up into the banking regulatory apparatus or sideways into a different state enterprise.

Wang Hui does not fit the stereotype. He runs Bank of Chengdu as its chairman, and he has been doing so for years. Consistency is the first thing to note about the management of this bank. While peer institutions have cycled through chairmen and presidents at a pace that makes strategic continuity difficult, the top of the house at Bank of Chengdu has remained remarkably stable. In an industry where leadership rotation is often the single biggest drag on execution quality, that stability is not a detail. It is a strategic asset.

Wang's background is unusual for a Chinese bank chairman. He is, by training and early career, a credit person, not a retail banker or an investment banker. He spent years inside the bank and the broader Sichuan financial system before rising to the top. What that means in practice is that when credit cycles turn, Wang is not reading about them in a briefing memo. He has lived through them. This shows up in the way the bank communicates. Its annual reports and investor presentations spend an unusual amount of time on asset quality, sector exposures, vintage analysis, and forward-looking provisioning. The tone is of a credit officer explaining to other credit people why the book is safe. That tone permeates the culture.

The management philosophy is captured in a two-character Chinese phrase that shows up in almost every speech and letter to shareholders: shen geng (深耕), which translates roughly as "deep plowing." The metaphor is agricultural—you do not plow many fields shallowly; you plow your own field deeply. In strategic terms, it is a refusal to chase the shiny object. Bank of Chengdu does not try to become a national bank. It does not aggressively open branches in cities it does not understand. It does not buy distressed regional banks just to pad asset growth. It stays in Sichuan and a few carefully chosen adjacent markets, and within those markets it tries to be the best at what it does.

This is, quietly, a radical posture in Chinese banking. Peer city commercial banks have, over the past decade, pursued a range of strategies—some tried to build national consumer finance platforms, some chased interbank-funded asset growth, some got into trust products or shadow-banking-adjacent structures, some bought cross-regional branch networks. Many ran into trouble. The most public failures, including a handful of small-bank collapses and take-overs that required regulatory intervention, came from banks that stretched outside their native competence. Bank of Chengdu did not stretch. It compounded.

Incentives reinforce the philosophy. In a financial system where compensation at state-adjacent banks has historically been compressed—capped, politically constrained, often stagnant—Bank of Chengdu has run a more performance-linked comp structure than many of its state-owned peers. It has been willing to pay for talent, especially risk and technology talent poached from the Big Four banks. Why would a credit officer at ICBC jump to a regional bank in Chengdu? Because the autonomy is higher, the decision-making is faster, and the upside is genuinely tied to bank performance. This has allowed Bank of Chengdu to build benches of mid-level and senior-level talent that punch above the weight its balance sheet would suggest.

Behind management sits the shareholder base, and this is where the story gets politically interesting. The largest shareholder is Chengdu Communications Investment Group, a municipally owned investment platform. Also present is Hong Leong. Also present is a constellation of strategic and financial shareholders, plus public float. The key point is this: the state-owned anchor shareholder has, over the years, behaved like an unusually patient principal. It has not extracted value through related-party dealing in ways that would show up in disclosures. It has not forced policy lending that would degrade the book. It has, broadly speaking, let management run the bank.

Some of that restraint is probably ideological—Chengdu's municipal leadership has, over multiple administrations, taken pride in being a reform-minded, market-oriented city government, and they view Bank of Chengdu as a showcase. Some of it is probably practical—a well-run bank generates dividends, and dividends are useful to a state owner. And some of it is probably the legacy effect of Hong Leong's presence on the board, which makes egregious interference harder.

The combination is a rare thing in Chinese state-linked enterprise: a stable anchor shareholder willing to let a talented operating team take a five-to-ten-year view, with an international strategic investor holding them accountable on governance. That is the substrate on which the rest of the story rests.

Now, the question any thoughtful investor asks about a regional bank with these tailwinds is: how have they actually deployed capital? Are they compounding quality, or are they just growing the balance sheet?

VI. M&A and Capital Deployment

Here is a test for any Chinese city commercial bank. It is 2015. Interest rates are declining. Real estate is booming. The regulator is easing cross-regional expansion rules. Your peers are announcing acquisitions, opening new city branches, launching consumer finance subsidiaries, and marketing wealth management products that your credit team privately suspects are mispriced. The public equity market is rewarding growth. What do you do?

Most banks grew. Bank of Chengdu, largely, did not.

The discipline shows up in the M&A track record. While some peers made bold acquisitions of village banks, rural commercial banks, or struggling city commercial banks in other provinces, Bank of Chengdu's inorganic footprint has been deliberately modest. It has invested in a set of village banks in Sichuan, extending its reach into smaller counties where the demographic and economic growth story complements the urban core. It has participated in local financial infrastructure—consumer finance joint ventures, financial leasing arms, small-loan platforms—but always in ways that reinforced the core commercial bank rather than diluting management attention.

What it has emphatically not done is a "national" play. There is no Bank of Chengdu flagship branch in Shanghai's Lujiazui competing with everyone else for trophy corporate clients. There is no aggressive loan originator in the Pearl River Delta. There is no flashy tie-up with an internet giant to launch a nationwide consumer finance product. The discipline is almost severe. The strategic message is: we know our moat ends at the Sichuan border, with a small bleeding edge into Chongqing and a handful of adjacent markets. We will not walk off the edge.

Why does this matter? Because the single most common way Chinese regional banks destroy capital is by stretching into markets where they have no information advantage. A bank's core competitive edge is asymmetric information about its borrowers. In its home market, a regional bank knows the local developers, the local manufacturers, the local SOEs, the local professional class. It knows which neighborhood has declining foot traffic and which export sector has rising orders. Its relationship managers are recycled into new roles and carry institutional memory. Outside its home market, none of that applies. A regional bank in an unfamiliar region is, in credit terms, worse than a national bank. It has the cost structure without the information.

Bank of Chengdu grasped this. And it freed up capital and management attention to do something much more valuable: invest in its digital stack.

This is the less-visible part of the capital deployment story, and it is possibly the most important. Rather than blowing money on prestige acquisitions, the bank has poured investment into technology—core banking modernization, mobile app development, an in-house data and analytics capability, and most importantly, a supply chain finance platform (which we will discuss shortly) that would have been impossible to build without substantial IT spend.

The best way to see the results is in the cost-to-income ratio. Among the top-tier city commercial banks—Ningbo, Nanjing, Jiangsu, Hangzhou, Beijing, Shanghai, Bank of Chengdu—the cost-to-income ratios cluster in a narrow range, generally in the mid-to-upper 20s to low 30s. Bank of Chengdu has historically been at the efficient end of that cluster. What that translates to is: for every yuan of revenue, fewer yuan go to overhead and more drop to pre-provision profit. In a banking sector where net interest margins have been compressed by policy-driven rate cuts, cost discipline is the difference between a bank that grows earnings and a bank that watches them erode.

There is a deeper point about capital allocation here. Banks, especially Chinese banks, are frequently evaluated on asset growth. It is an obvious metric because it is so easy to measure. But asset growth without return is value-destructive, and sometimes worse than that—it consumes capital that must be raised dilutively, it accumulates credit risk that shows up in a downturn, and it gives management an excuse to avoid doing the harder work of improving margins and efficiency. The good operators in banking, globally, are the ones who grow at or below their capital generation rate while improving return on equity. They compound rather than sprint.

Bank of Chengdu's return on equity has consistently run at levels that peer Chinese banks struggle to match—regularly in the high teens, sometimes testing twenty percent—while maintaining asset quality. That is not a bank that is winning by growing the book fastest. That is a bank that is winning by growing the book smartest.

The flip side of that discipline is that the bank has stayed small enough—and focused enough—to benefit from a couple of hidden business lines that investors covering the sector from 30,000 feet tend to miss entirely.

VII. The "Hidden" Businesses

There is a conference in Chengdu that happens every spring, hosted by Bank of Chengdu and attended by a rotating cast of manufacturing executives, logistics operators, commodity traders, and the occasional regulator. To a casual observer, it looks like a typical industry gathering with banquets and speeches. To an informed observer, it is one of the bank's most important customer development events. Because the topic is not traditional corporate lending. It is supply chain finance, and it is possibly the single most overlooked growth engine on the income statement.

Start with the context. Supply chain finance, globally, is a boring-sounding but important business line. The idea is this: in a typical manufacturing supply chain, a big anchor buyer (say, an auto assembler, or a major electronics OEM, or a big retailer) places orders with hundreds or thousands of upstream suppliers. Those suppliers produce goods, deliver them, and then wait—often for 60, 90, or 120 days—for the anchor to pay. During that waiting period, the suppliers have capital tied up in receivables. They would like to be paid sooner. A bank can step in, buy the receivable (or lend against it), take on the credit risk of the anchor (which is usually very creditworthy), and collect a fee or spread for providing the liquidity.

It is a straightforward business in theory. In practice, it is a technology and information game. To do it at scale, a bank has to integrate with the anchor buyer's procurement system, verify invoices in real time, price receivables accurately, monitor counterparty behavior, and manage a portfolio of exposures that may involve thousands of small suppliers. That requires software, data pipes, and relationship depth. It is, in other words, the kind of business that a mid-sized regional bank with a strong local relationship base and meaningful tech investment can do well, and that a Big Four bank often does badly because its systems are built for scale rather than granularity.

Bank of Chengdu has been building this business for years. Around the core anchor buyers in Sichuan's manufacturing economy—auto parts, electronics, machinery, consumer goods—the bank has built out a digital supply chain finance platform that connects into anchor ERP systems, automates invoice-based lending, and serves thousands of small and medium-sized suppliers. The segment has grown at rates regional banks normally cannot sustain—the kind of growth that in a Silicon Valley context would get a company a software multiple, not a bank multiple.

The strategic genius of the business is threefold. First, it is high-margin. Spreads on supply chain finance, especially to smaller suppliers, are meaningfully higher than on large corporate loans. Second, it is credit-light. The ultimate risk sits with the anchor buyer, which is typically a high-quality corporate, not with the fragmented supplier base. That means the bank can grow the book without degrading asset quality. Third, it is relationship-reinforcing. Suppliers who get financed through the platform often migrate into the bank's broader SME ecosystem—deposits, payments, FX, payroll. This is a customer acquisition channel dressed up as a credit product.

The second hidden business is green finance, and the narrative here is even more interesting. Sichuan has two resources the rest of China badly wants: hydroelectric power and rare earth minerals. The province's western mountain ranges generate enormous quantities of hydropower, particularly during the wet season, and have been underutilized for decades because the interior grid could not absorb them and the transmission infrastructure to the coast was limited. Beijing has been steadily building out that transmission, and Sichuan has been positioning itself as a destination for energy-intensive industrial activity that can plug directly into clean hydroelectricity. The phrase that gets used is "hydro-to-industry"—using the province's green power endowment to attract aluminum smelting, silicon materials production, data centers, advanced manufacturing, and, increasingly, computing infrastructure for artificial intelligence.

Financing that transition is a major lending opportunity, and it happens to be explicitly encouraged by regulatory policy. China's green finance framework offers preferential treatment to banks that originate qualifying green loans—in capital weightings, in policy rate access, and in political optics. A regional bank that can stake out an early, credible position in green infrastructure lending in a province that is becoming a national green energy hub is building exactly the kind of franchise that compounds over a decade.

Bank of Chengdu has been leaning into this aggressively. Green loan balances have grown rapidly, a disproportionate share of the book is tied to hydroelectric-powered industrial activity, and the bank's green finance narrative has become a key part of its equity story. The market is, in the analytical consensus, still underpricing this lever. Regional green finance at scale is a business that did not meaningfully exist five years ago. It is now a category, and Bank of Chengdu is one of a handful of regional banks in China that can credibly claim category leadership in its home market.

Step back and look at the revenue mix. Corporate banking remains the largest single segment, reflecting the bank's heritage. Retail banking is growing, helped by an expanding urban middle class and better digital infrastructure, but remains smaller than at peers with longer retail histories. Financial markets—interbank activity, bond investment, treasury—generates a meaningful share of the pie, reflecting Chinese banking's broader structure where investment securities now compose a large share of most bank balance sheets. Inside the corporate segment, though, the mix is shifting. Traditional large-corporate lending is flat to declining as margins compress and the government tightens local government financing vehicle exposures. What is growing is the SME-linked, supply-chain-finance-adjacent, green-tilted segment. That mix shift matters because it is explicitly moving the bank toward higher-margin, lower-correlated, less policy-vulnerable revenue.

All of which sets up the strategic analysis. What kind of competitive position is Bank of Chengdu actually building?

VIII. The Playbook: 7 Powers & 5 Forces

Great businesses can be analyzed through two complementary frameworks, and great regional banks in particular reward the exercise. Let's walk through both.

Start with Hamilton Helmer's 7 Powers—the framework that asks what structural advantages a business enjoys that competitors cannot easily replicate.

The first power, and the most obvious for Bank of Chengdu, is Cornered Resource. In this case, the cornered resource is the set of deep, non-replicable relationships with Chengdu's municipal government, its local state-owned enterprises, and its anchor private enterprises. These are not casual business relationships. They are generations-deep. Relationship managers at the bank have worked with the same corporate clients for ten or fifteen years. The bank has financed the same families of developers across multiple cycles, the same industrial conglomerates across multiple capex programs. When a major local infrastructure project is being structured, Bank of Chengdu is not just on the call—it is often drafting the term sheet. The Big Four banks cannot replicate this with a branch opening and a marketing campaign. They do not have the local memory. And other city commercial banks from outside the province cannot replicate it at all.

The second power is Scale Economies, but of a specific regional kind. In banking, scale operates at two levels. National scale matters for technology spend, for wholesale funding access, for treasury operations—and the Big Four banks dominate there. Regional density matters for information, for distribution, for operating efficiency per unit of market. Bank of Chengdu has more branches per square kilometer in the Sichuan basin than any other bank, more relationship managers covering more customers, and a denser physical and informational presence. The result is that its marginal cost of serving a new customer is lower, and its information about that customer is better, than any peer. Lower customer acquisition cost and better credit information translate directly into lower NPLs and higher returns.

The third power worth considering is Switching Costs, and here the case is more modest. Banking relationships are stickier than most consumer services—payroll, supplier payments, and working capital lines do not get moved on a whim—but switching costs in banking are not as dramatic as in enterprise software or medical devices. The bank benefits from some stickiness but should not be overvalued on it.

Counter-Positioning is an interesting dimension. Bank of Chengdu's decision to stay regional, while peers tried to go national, looks in retrospect like a counter-position. Going national required scale the bank did not have and diluted the informational edge in its home market. Staying regional meant it could underwrite better, serve more deeply, and grow more profitably. If peer banks now tried to imitate the "deep plowing" strategy, they would have to disassemble what they have built, which their own incentives and career structures make nearly impossible.

The other powers—Network Effects, Branding, Process Power—apply marginally. There is no true network effect in traditional banking, though the supply chain finance platform edges in that direction. Branding matters locally but is not a wide moat. Process power is real but modest.

Now apply Porter's Five Forces to understand the industry structure.

Threat of New Entrants is low to moderate. Regulatory barriers in Chinese banking are high—you cannot open a new commercial bank in a province without extensive regulatory approval and capital. But fintechs and large tech companies (Ant, WeBank, MyBank) have encroached on parts of the retail and SME space. The encroachment is real but bounded—regulators have pulled back on some of the more aggressive fintech expansion, and the core commercial banking activities remain heavily protected. For a regional player in its home market with government relationships intact, the practical entry threat is low.

Bargaining Power of Suppliers (depositors and wholesale funders) is a relevant lens. Chinese household depositors have historically been captive to banks, with limited alternatives and policy-anchored deposit rates. That has been slowly eroding as wealth management products, money market funds, and digital deposit substitutes have proliferated. Bank of Chengdu, because of its dense local footprint and sticky local deposit base, has one of the better funding structures among city commercial banks—deposit costs that are lower than peers who rely more on interbank funding. Supplier power is moderate and slowly rising; the bank's position against it is relatively strong.

Bargaining Power of Buyers (borrowers) is mixed. Large corporate clients, especially state-owned ones, have meaningful bargaining power—they can and do shop their credit needs among multiple banks, squeeze margins, demand capital markets services at cost. The Big Four banks compete aggressively for large-corporate business. But SMEs and smaller suppliers, which are Bank of Chengdu's growing emphasis, have limited bargaining power. They are underserved by the Big Four. They are too small to access capital markets. They need a bank that knows them. In that segment, buyer power is low, and pricing is better. This is one of the core strategic reasons the bank's revenue mix is shifting toward SME-linked business.

Threat of Substitutes is where bank executives should lose sleep. Bond markets, direct lending platforms, private credit funds, and securitization channels have all taken share from traditional bank lending in many markets. In China, the substitutes are still developing. Corporate bond issuance is growing but dominated by large borrowers. Shadow banking has been aggressively reined in by regulators. Fintech lending platforms exist but have had their wings clipped. For now, substitute pressure on a regional bank focused on relationship-heavy, information-intensive lending is manageable. Over a longer horizon, it will matter more.

Rivalry Among Existing Competitors is intense in Chinese banking overall but, again, regionally differentiated. In Sichuan, the competitive set is Bank of Chengdu, a handful of Big Four branch networks (which are effective but not locally dominant), a few other Sichuan-based city banks (which are smaller), and rural commercial banks (which serve different segments). The rivalry is real but not ruinous. Margins have compressed but not collapsed. Market share shifts slowly. This is not a commoditized, price-war industry structure at the local level—it is more like an oligopoly with entrenched positions.

The synthesized view is of an industry where the structural forces are moderate, not extreme, and where a well-positioned regional operator with a cornered resource and scale density can generate persistent excess returns. Bank of Chengdu is not protected by a wide moat in the classical sense—no one is, in banking—but the combination of advantages it has assembled in its home market is durable.

Which means the investment case turns less on the competitive position and more on the macro environment and execution.

IX. Bull vs. Bear Case

Take the bear case first, because it is the one any serious investor needs to examine, and because it is real.

The central bear argument is real estate. Chinese banks, almost universally, have sizable exposure to real estate—both directly, through loans to developers and mortgages to homebuyers, and indirectly, through land-backed local government financing vehicles and infrastructure projects whose cash flows depend on land sales. The Chinese real estate market has been in a multi-year deceleration, marked by the defaults of several large developers, declining sales volumes, and a national policy shift away from property as the primary growth engine. For a regional bank in a city where real estate has been a major economic driver, the concern is that hidden NPLs in the real estate complex could emerge as defaults ripple through the system.

Bank of Chengdu's disclosed real estate exposure has been managed carefully, and its asset quality has held up better than peers through the cycle so far. But the honest investor should assume some uncertainty. The bank's NPL ratio is reported at industry-leading low levels. Special mention loans and stage-two loan balances, which can be leading indicators of future NPL formation, have been watched by analysts. The regulatory environment has favored loan forbearance and restructuring in ways that may mute reported asset quality metrics relative to economic reality. If real estate deterioration is worse than disclosed—industry-wide, not bank-specific—the provisioning cushion could be tested.

A second bear argument is policy. Chinese regional banks are perpetually vulnerable to policy shifts that require them to take on social lending responsibilities at the expense of returns. Directives to lend to small businesses at preferential rates, to support struggling local SOEs, to fund local infrastructure projects at below-market pricing—these are features, not bugs, of the Chinese banking system. In any given year, new directives can compress margins, distort portfolio construction, or force loan growth that management would not have chosen. Bank of Chengdu, as an institution embedded in a municipal government ecosystem, is exposed to this risk continuously. The bank has managed it well historically, but the risk does not go away.

A third bear argument, less discussed but important, is net interest margin compression at the industry level. Chinese policy rates have been declining. The loan prime rate has been cut repeatedly. This squeezes the spread between deposit costs and loan yields, and it is a headwind that every Chinese bank faces. Bank of Chengdu's margin has compressed along with the industry. The question is whether it can compress further before meaningfully dragging on earnings. The structural answer—lower margins, partially offset by volume growth and mix shift to higher-margin segments like supply chain finance—looks workable but not painless.

A fourth argument is concentration. The bank's fate is tied to the fate of Sichuan and particularly Chengdu. If the Chengdu-Chongqing macro story disappoints, if manufacturing relocation stalls, if the next decade looks nothing like the last, a regional bank with all its eggs in one basket is more vulnerable than a national bank. This is the trade-off of the "deep plowing" strategy. It works brilliantly when the home market is great. It amplifies the downside when the home market stumbles.

Against all of that, the bull case rests on several legs.

First, the macro. The bull case argues that the Chengdu-Chongqing integration is the next decade's version of the Pearl River Delta growth story. The Pearl River Delta took twenty years to mature into what it became. Chengdu-Chongqing is, on that arc, somewhere around year eight or ten. The tailwind is structural, not cyclical. The base case is that the regional economy continues to outperform the national economy, that the emerging industries (tech, advanced manufacturing, biotech, AI infrastructure) compound, and that the region's role as the "fourth pole" becomes a durable feature of Chinese economic geography.

Second, the bank-specific story. Bank of Chengdu is the most levered, highest-quality way to play the Chengdu macro. It has the densest branch network, the deepest relationships, the best asset quality, the best cost structure. If the macro plays out, the bank is the obvious beneficiary. If the macro stalls, the bank is still better positioned than peers.

Third, the hidden growth engines. Supply chain finance at the rate it is growing, green finance with explicit policy tailwind, SME lending with structurally better margins—these are all businesses whose contribution to the P&L is still relatively young. Extrapolated forward, they suggest mix shift that improves both growth and returns.

Fourth, governance and management. The bank is run by an operator who has been there long enough to matter, with a shareholder structure that supports long-term decision-making, and a culture that has consistently avoided the worst mistakes of regional banking. That is not a moat in the Porter sense, but it is a quality of management that compounds.

Fifth, valuation. Chinese banks broadly trade at discounts to tangible book. Bank of Chengdu, because of its superior returns, trades at a higher book multiple than Big Four peers but often at a lower earnings multiple than the truly top-tier regional names like Ningbo or Nanjing. For investors who want exposure to the Chengdu macro and are willing to underwrite the governance story, the valuation is not asking for heroic assumptions.

On balance, the bank sits at an interesting intersection. It is not a pure macro play, because its execution has been consistently differentiated. It is not a pure alpha story, because its fate is genuinely tied to a regional economy. It is both—which means the investor underwriting it is taking two bets simultaneously, and they had better be comfortable with both.

The metrics to watch are the things that would either confirm or invalidate the thesis. For a bank like this, there are a small number of KPIs that matter disproportionately. First, the NPL ratio and its leading indicators (special mention loans, stage-two loan balances, overdue-but-not-NPL balances). If asset quality breaks, everything else stops mattering. Second, loan growth in the core corporate and SME segments—specifically the supply chain finance book and the green finance book. That is where the thesis lives. Third, cost-to-income ratio, as a proxy for operating discipline and the payoff from technology investment. If those three lines compound well, the bank compounds.

X. Conclusion & Reflections

Walk back through the story and what stands out is how much of Bank of Chengdu's success is explained by things that Bank of Chengdu did not do.

It did not try to become a national champion. It did not chase cross-regional acquisitions. It did not pile into off-balance-sheet wealth management products in the mid-2010s the way half the industry did. It did not build a shadow-banking adjacent business that would later require writedowns. It did not, when the Chinese banking zeitgeist demanded growth, abandon the discipline that its early near-death experience had instilled. It stayed in Sichuan. It stayed focused. It stayed conservative on credit. And it quietly, patiently, compounded.

There is an Acquired-style observation lurking in that. The hardest thing in business, and arguably the hardest thing in banking, is to do less than you could. A bank that can grow at 20% a year through aggressive expansion, if the capital allocation team is disciplined enough to grow at 10% a year instead—accepting slower growth to avoid hidden credit mistakes—is doing something deeply against human nature and against most incentive structures. That kind of discipline is rare. It is usually explained, when it exists, by a combination of culture, personality, and shareholder alignment. At Bank of Chengdu, all three seem present.

The Hong Leong partnership of 2007 deserves reexamination as a broader lesson in financial sector investing. What made it successful was not the headline price or the regulatory packaging. It was the transfer of institutional capability—risk management, retail banking templates, governance culture—from a disciplined regional operator in one market to an undermanaged regional operator in another. This is the model that rarely works when large foreign banks buy into large Chinese banks (the capability transfer is diluted across a huge organization), and that works much better in smaller, more focused pairings. It is a lesson in selecting partners, structuring minority stakes, and understanding what value creation looks like in financial services cross-border investing.

The macro lesson is about Chinese economic geography and the patient way government-directed development actually shows up in corporate outcomes. A decade ago, Chengdu was an ambitious regional capital. Today, it is a legitimate fourth pole of the Chinese economy, with a diversified industrial base, a growing tech cluster, and a population that continues to expand even as many Chinese cities are shrinking. That transition was policy-driven but also real—companies moved, people moved, infrastructure got built, productive capacity materialized. A bank embedded in the right place benefited from a tailwind that was obvious in hindsight but required a long-horizon bet in real-time.

The philosophical question remains: is Bank of Chengdu a generic bank or a compounding machine? The evidence of the last decade supports the compounding machine interpretation. Return on equity persistently in the high teens, asset quality better than peers, cost efficiency better than peers, and a mix shift toward higher-margin segments. The risk is that past performance, especially in banking, is not always destiny. Credit cycles exist. Macro slowdowns happen. Policy shifts can change the rules of the game overnight. The prudent view acknowledges all of this while observing that the bank has earned more credibility than most for navigating the risks.

The final lesson, and the one that generalizes beyond this specific company, is the power of focus. Bank of Chengdu is, in 2026, one of the most admired regional banks in China not because it did more than its peers but because it did less of what they did. It refused to chase prestige. It refused to chase scale without return. It refused to leave its home market. It knew, with a clarity unusual in any industry, exactly where its moat ended—and it refused to cross the line.

For long-term fundamental investors trying to understand Chinese financial services, or regional banking anywhere, or the general question of how quality compounds in mature industries, Bank of Chengdu is worth studying. Its story is not about a breakthrough product, a technological revolution, or a dramatic turnaround. It is about a bank that was handed a messy legacy in 1996, survived the sector's near-death experience, accepted the help of a disciplined minority partner, rode a historic macro tailwind, and stayed humble enough to play only the hand it was dealt.

Those are, quietly, the ingredients of most great long-term financial services franchises. And on the corner of Qingjiang Middle Road in Chengdu, at dusk, with the cranes still visible on the horizon, the bank continues to do what it does. Deeply. Patiently. Plowing its own field.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube