Ping An Insurance: The Chinese Giant's Tech Transformation

I. Introduction & Episode Thesis

Picture this paradox: In 1988, thirteen employees crammed into a 200-square-meter office in Shenzhen, sleeping on mattresses between desks, cycling through humid streets to pitch insurance policies door-to-door. Their annual premium target? A seemingly impossible 5 million yuan. Fast forward to today—that scrappy startup has metamorphosed into a trillion-dollar colossus employing over 300,000 people, serving 230 million customers, and running four tech unicorns that Wall Street salivates over.

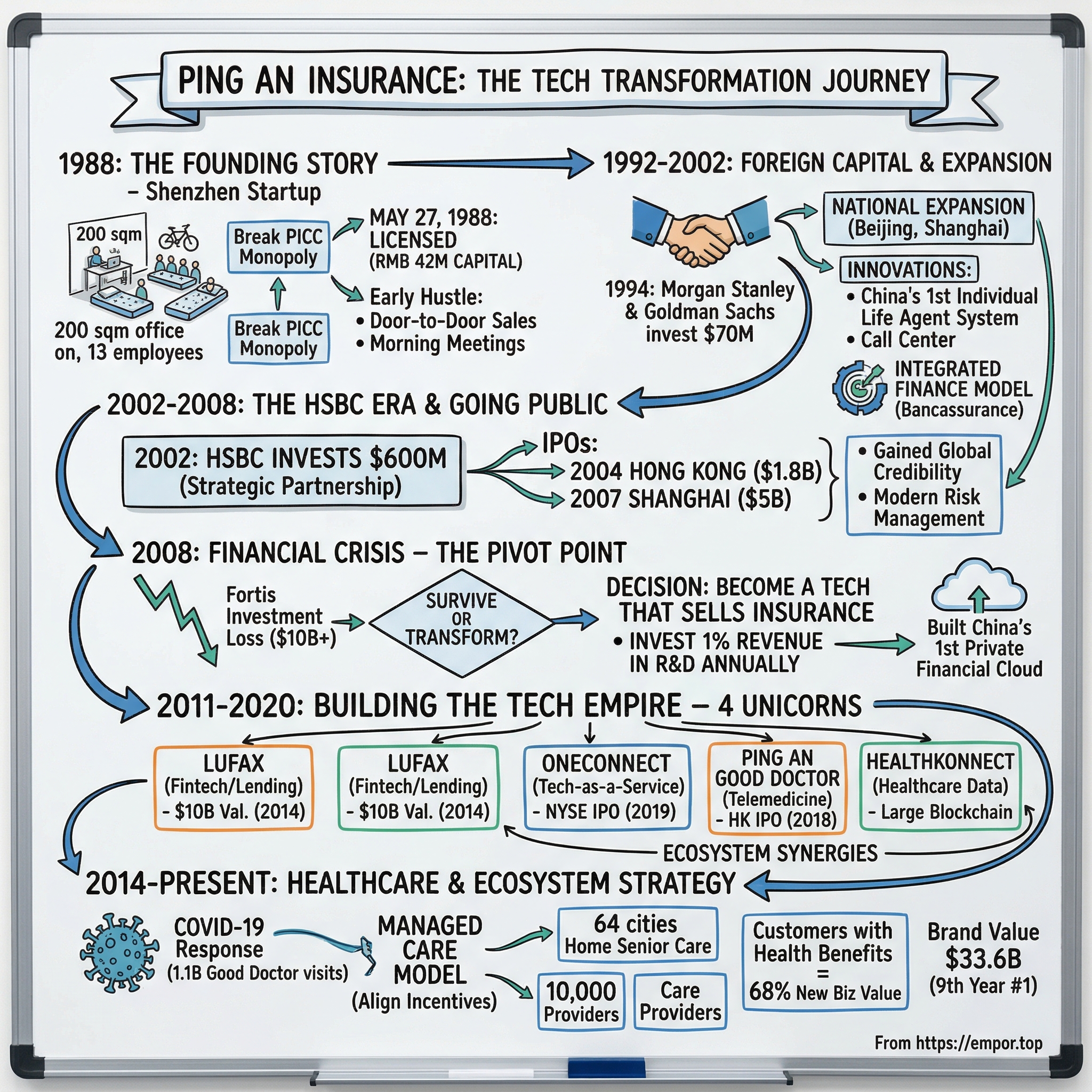

This is the story of Ping An Insurance—a company that shouldn't exist, at least not in its current form. When Peter Ma Mingzhe fought for two years to get China's first joint-stock insurance license, he wasn't just breaking a state monopoly. He was architecting what would become the most audacious transformation in financial services history: from a regional insurer to China's sixth-largest company, from paper policies to AI-powered healthcare, from copying Western models to exporting fintech to the world. The company was founded in 1988 and is headquartered in Shenzhen. It is ranked as China's 6th largest company. In 2024, Ping An ranked 29th on the Forbes Global 2000 list and 53rd on the Fortune Global 500 list. With revenue reaching RMB1,141 billion ($161 billion) in 2024 and a brand value of $33.6 billion, Ping An stands as the world's most valuable insurance brand for nine consecutive years.

But here's what makes this story extraordinary: Unlike Western financial giants who bolt on technology as an afterthought, Ping An decided in 2008—right as Lehman Brothers collapsed—to become a technology company that happens to sell insurance. Today, the company invests 1% of its revenues into R&D each year, employing over 21,000 technology developers and over 3,000 scientists, with patent applications totaling 53,521—more than most Silicon Valley unicorns combined.

The roadmap ahead traces an improbable journey: from challenging China's insurance monopoly in 1988, to courting foreign capital in the 1990s, to surviving the Asian Financial Crisis, to the HSBC partnership that changed everything, through the 2008 pivot that redefined the company, to building four tech unicorns from scratch, and finally to the audacious healthcare ecosystem play that could redefine insurance globally. This isn't just a story about China's financial liberalization—it's about how a company from Shenzhen wrote the playbook for financial services in the 21st century.

II. The Founding Story: China Opens Up (1988–1992)

The year was 1986, and Peter Ma Mingzhe faced an impossible task. The 31-year-old deputy manager at Shekou Industrial Zone's social insurance company had been given a mandate that would have made seasoned executives laugh: break the iron grip of the People's Insurance Company of China (PICC), which had monopolized Chinese insurance since 1949. Ma didn't just need to create a company—he needed to convince Communist Party officials that competition in insurance wasn't capitalism run amok, but rather a necessary evolution for China's economic reform.

Ma's secret weapon wasn't capital or connections—it was Yuan Geng, the legendary reformer who ran Shekou Industrial Zone like a capitalist experiment within socialist China. Yuan had already pushed boundaries by introducing labor contracts and performance-based pay in state enterprises. When Ma approached him with the insurance idea, Yuan saw an opportunity to test another reform thesis: could financial services competition improve economic efficiency without threatening socialist principles?

The licensing battle that followed reads like a bureaucratic thriller. For nearly two years, Ma shuttled between Shenzhen, Beijing, and various provincial capitals, armed with feasibility studies and reform theories. PICC executives lobbied hard against the application, arguing that insurance required national scale and that competition would fragment risk pools. Party conservatives worried about ideological implications—wasn't insurance fundamentally about private property protection, anathema to socialist ideals?

Ma's breakthrough came through a clever reframing. He positioned Ping An not as a competitor to PICC but as a "supplement" serving the special economic zone's unique needs—joint ventures, foreign enterprises, and private businesses that PICC struggled to understand. He emphasized that Shekou's experimental status made it the perfect testing ground for financial reform. If it failed, the damage would be contained; if it succeeded, the model could spread.

On May 27, 1988, after 21 months of negotiations, the approval finally came through. Ping An Insurance Company was born with RMB 42 million in founding capital—51% held by Shekou Social Insurance Company and 49% by China Merchants Bank Shenzhen Trust Company. The name "Ping An" (平安) meaning "safe and well" was personally chosen by Yuan Geng, who believed insurance should provide peace of mind, not just financial compensation.

The early office painted a picture of startup scrappiness that would make Silicon Valley garage stories seem luxurious. The company's first headquarters occupied just 200 square meters on Zhaoshang Road in Shekou—roughly the size of a two-bedroom apartment. Six to eight employees slept in a cramped dormitory; several others simply slept under their desks. The Shenzhen Branch of China Merchants Bank, taking pity on these insurance pioneers, donated an old van that served as both transportation and mobile office.

But the real challenge wasn't infrastructure—it was market education. In 1988, most Chinese citizens had never heard of commercial insurance. The concept of paying money for protection against events that might never happen seemed absurd to people emerging from decades of planned economy where the state theoretically provided all social protection. Ma's team had to become evangelists, educators, and salespeople simultaneously.

The sales strategy was pure hustle. Ping An staff would cycle through Shenzhen's dusty streets in the subtropical heat, knocking on every factory door, every shop front, every construction site. They carried flip charts explaining insurance concepts in simple terms. One early employee recalled drawing pictures to explain how premiums worked, using rice bowls and chopsticks as props. The annual target seemed impossible: RMB 5 million in premiums, just one-thousandth of PICC's national volume, but still a mountain for a company starting from zero.

Ma instituted daily morning meetings at 7 AM where the team would practice pitches, share rejection stories (there were many), and psyche each other up for another day of door-knocking. He created a culture of radical transparency—everyone's daily sales figures were posted on a board, creating peer pressure but also peer support. The first major breakthrough came when they convinced a Hong Kong-invested toy factory to buy a property insurance policy. The premium was just RMB 5,000, but the team celebrated like they'd won the lottery.

What distinguished Ping An from PICC wasn't just hunger—it was innovation born from desperation. PICC operated through state-owned enterprise channels, essentially mandatory insurance bundled with other government services. Ping An had no such advantages, forcing them to actually compete on service. They offered faster claims processing (weeks instead of months), simpler policies (written in plain Chinese rather than bureaucratic jargon), and most radically, they actually marketed to individuals rather than just enterprises.

The individual life insurance model, virtually non-existent in China at the time, became Ma's obsession. He studied Taiwanese and Hong Kong insurance companies, inviting advisors to train his team. In 1992, Ping An launched China's first individual life insurance agent system, recruiting housewives, retirees, and unemployed youth to sell policies on commission. PICC executives mocked it as "American-style pyramid selling," but within months, Ping An's army of agents was generating more premium volume than traditional corporate channels.

By 1992, Ping An had expanded beyond Shekou to all of Shenzhen, then to Guangdong province. Premium income reached RMB 418 million, nearly 100 times the original target. The company that started in a cramped office now employed over 3,000 people. More importantly, they had proven that insurance competition could work in China, setting the stage for national expansion.

The founding period established cultural DNA that would define Ping An for decades: a relentless work ethic born from underdog status, an openness to foreign ideas combined with Chinese pragmatism, and most critically, an innovation mindset that saw regulatory constraints not as barriers but as problems to solve creatively. When Western consultants later studied Ping An's culture, they found something unique—not quite Silicon Valley's "move fast and break things," nor Japanese corporate discipline, but rather what one advisor called "entrepreneurial socialism with Chinese characteristics."

As 1992 drew to a close, Deng Xiaoping's famous Southern Tour endorsed deeper market reforms, specifically praising Shenzhen's experiments. For Ping An, this was vindication and opportunity rolled into one. The scrappy regional insurer was about to go national, but Ma knew that scaling required something the company desperately lacked: capital and expertise. The solution would come from an unexpected source—Wall Street investment banks eager to bet on China's financial future.

III. Foreign Capital & Early Expansion (1992–2002)

The meeting at the Peninsula Hotel in Hong Kong would change everything. It was late 1993, and Peter Ma sat across from a team of Morgan Stanley bankers who couldn't quite believe what they were hearing. Here was a Chinese insurance company—barely five years old, operating in a communist country where private property rights were still evolving—asking Wall Street to become shareholders. The Morgan Stanley team had seen ambitious pitches before, but this was different. Ma wasn't just selling equity; he was selling a vision of China's financial future.

"You don't understand," Ma told the skeptical bankers through his interpreter, his passion breaking through language barriers. "In ten years, China will have the world's largest middle class. They'll need insurance for their homes, their cars, their children's education. PICC thinks like a government department. We think like a business. That's why we'll win."

The timing was fortuitous. China had just amended its company law to allow foreign investment in financial institutions, though with strict limitations. Ma had lobbied for this change, arguing that Chinese financial companies needed foreign expertise to modernize. But he was also playing a deeper game—foreign shareholders would provide political protection against domestic rivals who wanted to crush the upstart competitor.

Goldman Sachs joined the conversation in early 1994, creating an unusual dynamic—two Wall Street rivals potentially investing in the same Chinese company. Ma masterfully played them against each other, not just on valuation but on value-add. He demanded that any investment include technology transfer, management training, and help building modern risk assessment systems. This wasn't just about money; it was about transformation.

The negotiations stretched for months, complicated by Chinese regulations that limited foreign ownership to 24.9% combined. Every term sheet had to be vetted by multiple government agencies. Ma spent more time in Beijing's regulatory corridors than Shenzhen's headquarters, wearing out shoe leather and building relationships with officials who would prove crucial later.

In October 1994, the deal closed: Morgan Stanley and Goldman Sachs each took 6% stakes, investing a combined $70 million. It was the first foreign investment in a Chinese financial institution, making headlines from Hong Kong to New York. The Financial Times called it "a watershed moment for China's financial opening." PICC executives were furious, privately lobbying to reverse the approval.

But Ma wasn't done. That same year, the company was renamed "Ping An Insurance Company of China," signaling national ambitions. The foreign capital enabled rapid expansion—by 1995, Ping An had branches in Beijing, Shanghai, and 10 other major cities. Premium income surged to RMB 8.7 billion, making it China's second-largest insurer with 5% market share.

The foreign influence went beyond capital. Morgan Stanley sent Peter Sands (later CEO of Standard Chartered) to conduct a three-month diagnostic of Ping An's operations. His report was scathing—risk controls were primitive, IT systems were fragmented, and actuarial models were guesswork. But rather than being defensive, Ma embraced the criticism, hiring Western consultants to rebuild core functions from scratch.

The transformation was remarkable to witness. The company's Shanghai office became a laboratory for Western insurance practices adapted to Chinese realities. They introduced computerized underwriting when most Chinese companies still used paper ledgers. They built China's first insurance call center, shocking an industry where customer service meant waiting in line at a state office. They even launched television advertising—unprecedented for a financial company—with the tagline "Insurance is love," repositioning insurance from bureaucratic necessity to family responsibility.

The real strategic coup came in 1995-1996 when Ma pushed into adjacent financial services. Ping An Securities was established in 1995, becoming one of China's first integrated financial groups. The acquisition of ICBC Pearl River Delta Financial Trust Joint Company, renamed Ping An Trust, added asset management capabilities. Wall Street advisors pushed back—focus on insurance, they argued. But Ma understood something they didn't: Chinese customers wanted one-stop financial services, not product specialists.

The integrated finance model, or "bancassurance" as Europeans called it, was Ma's obsession. He studied models from Allianz to AXA, but ultimately created something uniquely Chinese. While Western companies cross-sold through separate divisions, Ping An built unified customer databases and shared branch networks. A customer buying car insurance might be offered a credit card; a trust client might be pitched life insurance. It was messy and inefficient at first, but it created customer stickiness that pure-play competitors couldn't match.

Cultural transformation proved harder than strategic expansion. The company was essentially running two parallel organizations—the old guard from the Shekou days who valued relationships and hustle, and the new hires from universities and foreign companies who spoke the language of ROE and risk-adjusted returns. Ma instituted "Friday Forums" where employees could debate strategy and air grievances. He famously kept an open office where any employee could walk in with ideas or complaints.

The Asian Financial Crisis of 1997-1998 tested everything. Foreign investors panicked as Asian currencies collapsed. Several demanded board seats to protect their investments. Chinese regulators, spooked by the crisis, tightened rules on financial conglomerates. Competitors spread rumors that Ping An's foreign ownership made it vulnerable to capital flight.

Ma's response was masterful. He invited regulators to examine Ping An's books, demonstrating that foreign investment had actually improved risk management. He published full financial statements—unprecedented transparency for a Chinese financial institution. Most cleverly, he positioned Ping An as a national champion, a Chinese company using foreign expertise to compete globally. The narrative shifted from "foreign-influenced" to "internationally competitive."

By 2000, the strategy was vindicated. Ping An's premium income reached RMB 67.8 billion. The company had 25 million customers and 200,000 employees and agents. More importantly, it had built capabilities—in technology, risk management, and customer service—that PICC and other state-owned insurers couldn't match.

The period also saw Ma's leadership style fully emerge. Unlike traditional Chinese executives who ruled through hierarchy, or Western CEOs who managed through processes, Ma created what one McKinsey consultant called "entrepreneurial orchestration." He set aggressive goals but gave teams freedom to achieve them. He demanded performance but tolerated failure if lessons were learned. He was equally comfortable discussing actuarial models with PhDs and sharing meals with entry-level sales agents.

One story captures his approach: In 1999, the life insurance division was struggling with lapse rates. Rather than issuing top-down directives, Ma spent a week working as a sales agent, cold-calling customers who had cancelled policies. He discovered the real issue—policies were too complex and agents oversold benefits. Within months, Ping An simplified its products and retrained its entire sales force.

As the new millennium arrived, Ping An faced a crucial decision. The foreign shareholders were pushing for an IPO to realize returns. Chinese regulators were encouraging consolidation to create national champions. International expansion beckoned as China prepared to enter the WTO. Ma knew Ping An needed a transformational partner, someone who could provide not just capital but global expertise and credibility. That partner would come from an unexpected place—Hong Kong, in the form of the British banking giant HSBC.

IV. The HSBC Era & Going Public (2002–2008)

The Mandarin Oriental ballroom in Hong Kong was packed with journalists on October 9, 2002. HSBC Chairman John Bond stood next to Peter Ma, announcing what the Financial Times would call "the deal of the decade"—HSBC was investing $600 million for a 10% stake in Ping An, with rights to increase to 19.9%. The British banking giant, with its 137-year history in Asia, was betting big on China's insurance future. But this was more than a financial transaction; it was a marriage of colonial-era banking wisdom and Chinese entrepreneurial energy that would transform both companies.

The courtship had been anything but smooth. HSBC initially wanted management control, proposing a 51% stake that would make Ping An a subsidiary. Ma refused, leading to six months of stalemate. The breakthrough came when HSBC's Asia-Pacific CEO, David Eldon, spent a week at Ping An's Shenzhen headquarters, sleeping in the company guesthouse and eating in the employee canteen. He emerged convinced that Ping An's culture and local knowledge were too valuable to subordinate to Hong Kong control.

The final structure was ingenious. HSBC took a large equity interest in Ping An in 2002, becoming the single largest shareholder while accepting limits on board control. They would nominate directors and provide technical assistance but couldn't dictate strategy. Ma later called it "strategic partnership without strategic surrender"—a model that would influence Chinese corporate governance for decades.

HSBC's impact was immediate and profound. They brought something money couldn't buy—credibility with international investors and regulators. When Ping An executives traveled abroad, doors that had been closed suddenly opened. European insurers who had dismissed Ping An as a Chinese upstart now took meetings. Rating agencies upgraded their assessments. Most crucially, HSBC's involvement signaled to Chinese regulators that Ping An was ready for the global stage.

The technical assistance was transformative. HSBC sent teams to upgrade Ping An's risk management, introducing concepts like Value at Risk (VaR) and Economic Capital that were alien to Chinese insurance. They rebuilt the treasury function, teaching Ping An how to manage billions in premiums across currencies and asset classes. The bancassurance expertise was particularly valuable—HSBC had been cross-selling insurance through bank branches since the 1960s.

But the real game-changer was HSBC's push for Ping An to become a true financial conglomerate. In 2003, Ping An Insurance (Group) Company of China was established, creating a holding company structure that could own banks, not just insurance and securities businesses. This wasn't just corporate reorganization—it was architecting for ambition.

The banking expansion started modestly. In 2003, Ping An acquired Fujian Asia Bank, a tiny lender with just 13 branches. HSBC executives were skeptical—why buy a marginal player in China's most competitive sector? Ma's answer was prescient: "Insurance companies are asset gatherers, banks are asset deployers. We need both sides of the balance sheet." The 2005 acquisition of Shenzhen Commercial Bank, creating Ping An Bank, proved the thesis. Within three years, Ping An Bank's assets grew five-fold through insurance company deposits and customer referrals.

The IPO preparations began in 2004, with HSBC playing quarterback. The challenge was staggering—explaining to international investors a Chinese conglomerate structure that didn't fit any Western template. Ping An wasn't just an insurer like AIG, nor a bancassurer like Allianz, nor a pure bank like HSBC itself. It was something unique—a financial ecosystem adapted to Chinese customer behavior where the same family might need insurance, banking, investments, and trust services from a single provider.

The roadshow was grueling. Ma and his team visited 200 institutional investors across 23 cities in 15 days. The pitch deck ran 300 pages, covering everything from actuarial assumptions to Communist Party governance. Skeptics questioned everything—could Chinese risk management handle complex derivatives? Would regulators allow true competition? How real were the reported numbers?

On June 24, 2004, Ping An listed on the Hong Kong Stock Exchange, raising $1.8 billion at HK$10.33 per share. It was Hong Kong's largest IPO that year, with demand exceeding supply by eight times. The stock jumped 28% on the first day, making paper billionaires of early employees who had received stock options—still rare in Chinese companies.

But Ma wasn't satisfied with Hong Kong success; he wanted Shanghai listing to tap domestic capital. This required another level of regulatory navigation. The China Securities Regulatory Commission had concerns about connected party transactions, requiring two years of negotiations and restructuring. HSBC's reputation again proved crucial—their endorsement carried weight with Beijing officials wary of financial conglomerate risks.

The Shanghai IPO on March 1, 2007, was even more spectacular. Ping An raised $5 billion at RMB 33.80 per share, the world's largest insurance IPO at that time. Domestic demand was extraordinary—retail investors queued overnight at bank branches to submit applications. The lottery allocation meant some investors received just 100 shares despite applying for thousands. The stock doubled on the first trading day, creating a market value exceeding $100 billion.

The dual listing transformed Ping An's capabilities. Suddenly flush with capital, the company went on an acquisition spree. They bought 4.99% of Fortis, the Belgian-Dutch financial giant, for €1.8 billion—China's largest overseas financial investment. They acquired Shenzhen Development Bank for $3.3 billion, gaining a nationwide banking network. They even explored buying a U.S. insurer, though regulatory concerns killed that deal.

HSBC's influence extended beyond transactions to transformation. They pushed Ping An to adopt International Financial Reporting Standards (IFRS), making it the first Chinese insurer with truly comparable global accounts. They introduced Solvency II concepts years before Chinese regulators mandated them. Most importantly, they helped build an international talent pipeline—by 2007, Ping An had over 200 executives with Western financial experience.

The cultural fusion was fascinating to observe. Ping An's headquarters became a babel of languages—Mandarin, Cantonese, English—with translation booths in major meeting rooms. HSBC executives learned to navigate Chinese business dinners with their elaborate toasting rituals, while Ping An managers mastered PowerPoint presentations and Excel modeling. One HSBC advisor recalled teaching VaR models in the morning and learning tai chi from Ping An colleagues at lunch.

The governance structure evolved into something unique—neither purely Western nor traditionally Chinese. The board included independent directors from Harvard Business School and Bank of England, alongside Chinese officials and entrepreneurs. Audit committee meetings could last eight hours, with HSBC-nominated directors drilling into risk exposures that Chinese companies typically kept opaque. Ma later said this governance discipline, though painful, saved Ping An during the coming financial crisis.

By early 2008, the partnership had exceeded all expectations. Ping An's market value reached $140 billion, making it Asia's most valuable insurer. HSBC's stake, increased to 16.8% through follow-on investments totaling $1.7 billion, was worth over $20 billion on paper. The company had 50 million customers, 400,000 employees and agents, and operations in 20 countries.

The model seemed unstoppable—Chinese growth powered by Western expertise, local knowledge enhanced by global best practices. Investment bankers were already pitching the next phase: acquisitions in Europe and America, a London listing, maybe even challenging AIG as the world's largest insurer. But storm clouds were gathering. The U.S. subprime crisis was metastasizing into global financial contagion. Lehman Brothers was wobbling. And Ping An's aggressive expansion had created vulnerabilities that would soon be exposed.

The 2008 financial crisis would test everything—the HSBC partnership, the conglomerate model, Ma's leadership, and ultimately, Ping An's survival. But paradoxically, this near-death experience would catalyze the company's most dramatic transformation yet: from financial conglomerate to technology company. The crisis that almost destroyed Ping An would ultimately save it, forcing a pivot that would define its next decade.

V. The 2008 Financial Crisis: Pivot Point

The phone call came at 3 AM Shenzhen time on September 15, 2008. Lehman Brothers had filed for bankruptcy. Peter Ma, already awake and monitoring Bloomberg terminals, knew this was the moment everything would change. Within hours, Ping An's stock price would crater 40%. The Fortis investment—€1.8 billion spent just months earlier—would become essentially worthless as the Belgian-Dutch giant collapsed. Paper losses would exceed $10 billion. But in that darkest moment, Ma made a decision that would transform Ping An from a traditional financial services company into something entirely different: a technology company that happened to sell insurance.

The immediate crisis was existential. In early 2008, Ping An had agreed to take a 50% share in Fortis Investments, a subsidiary of Fortis, which had taken over ABN AMRO Asset Management as a result of the split up of ABN AMRO in late 2007; the deal was canceled in October 2008. The planned expansion into European markets evaporated overnight. Domestic customers, spooked by global financial contagion, began withdrawing deposits from Ping An Bank. Insurance sales collapsed as Chinese families hoarded cash. The stock price fell from HK$82 to HK$25 in six weeks.

The board meetings during this period were brutal. HSBC, dealing with its own crisis, wanted Ping An to hunker down—cut costs, reduce risk, survive. Some Chinese directors pushed for government bailout, arguing Ping An was too big to fail. International investors demanded asset sales to shore up capital. Everyone expected Ma to announce layoffs and retrenchment.

Instead, Ma called an emergency strategy session in October 2008 that would become legendary within Ping An. For three days, the top 100 executives sequestered themselves in a Shenzhen hotel, mobile phones confiscated, discussing a single question: "What if this crisis isn't ending something, but beginning something?"

Ma's thesis was contrarian but compelling. The financial crisis had exposed the brittleness of traditional financial models—overleveraged banks, opaque derivatives, misaligned incentives. But it had also accelerated digital adoption. Chinese consumers, unable to visit bank branches during crisis volatility, were turning to online services. Mobile phone penetration was exploding. E-commerce was taking off. Maybe, Ma argued, technology wasn't just a tool for financial services—maybe it was the future of financial services.

The pivot started with a simple but radical decision: while competitors cut budgets, Ping An would invest 1% of revenue—about $500 million annually—into technology R&D. Not IT infrastructure or back-office systems, but genuine innovation—artificial intelligence, blockchain, cloud computing. The board was skeptical. HSBC executives called it "reckless" given capital constraints. But Ma persisted with an argument that resonated: "The companies that win after crisis aren't those that cut deepest, but those that invest smartest."

The first project was almost absurdly ambitious: build a unified technology platform serving all Ping An businesses—insurance, banking, investments—with a single customer view. Every consultant said it was impossible. Legacy systems were incompatible. Regulatory requirements differed across sectors. The project would take years and might fail entirely. Ma green-lit it anyway, appointing Jessica Tan, a McKinsey alumna with a MIT degree, to lead the transformation.

What happened next surprised everyone. Young Chinese engineers, many educated abroad but returned home during the crisis, flocked to Ping An. They were attracted not by insurance but by the technical challenge—building financial technology at unprecedented scale. The Shenzhen headquarters transformed from insurance offices to something resembling a Silicon Valley campus, with coding marathons, hackathons, and algorithm competitions.

The cultural transformation was jarring. Traditional insurance executives who had spent careers analyzing mortality tables suddenly worked alongside 25-year-old data scientists building neural networks. Morning meetings that once reviewed sales figures now discussed API architectures and machine learning models. The dress code relaxed—ties disappeared, hoodies appeared. One veteran recalled: "It felt like a different company invaded and took over."

But Ma understood something crucial: transformation required protection from quarterly pressures. He created Ping An Technology, a separate subsidiary with its own P&L, freed from insurance regulatory constraints. He hired Chen Xinying, a former IBM executive, promising him startup autonomy within a corporate giant. Most importantly, he set expectations with investors—this was a 10-year transformation, not a quick fix.

The results were initially invisible externally but revolutionary internally. By 2010, Ping An had built China's first private financial cloud, processing millions of transactions previously handled by paper. They developed facial recognition systems for customer authentication when most banks still required physical signatures. They created AI models for claims assessment, reducing processing time from weeks to minutes.

The smartphone revolution accelerated everything. In 2011, when smartphones were still luxury items in China, Ma made another contrarian bet: mobile-first for everything. Not mobile as a channel, but mobile as the primary interface. Every service had to work perfectly on a 4-inch screen with 3G connectivity. Executives who protested complexity were overruled. "The customer doesn't care about our internal complexity," Ma said repeatedly.

The ecosystem strategy emerged from this digital foundation. If customers were living digital lives, why shouldn't Ping An serve all their needs? Not just insurance and banking, but healthcare, real estate, automotive services. The board worried about focus dilution. Regulators questioned scope creep. But Ma saw inevitability: "Amazon started selling books. Alibaba started connecting buyers and sellers. Platform economics trump product economics."

The numbers validated the strategy. By 2011, while Western financial giants were still deleveraging, Ping An's technology investments were paying off. Online sales exceeded offline for the first time. Customer acquisition costs dropped 60% through digital channels. Claims processing accuracy improved from 78% to 95% through AI assistance. The company that almost collapsed in 2008 was now worth more than before the crisis.

HSBC's relationship evolved during this period. Initially supportive of the transformation, they grew concerned about capital allocation. HSBC spent $1.7 billion to build up a 15.6 percent stake in China's second-largest insurer in 2002 and 2005, but a sale has been widely expected as part of its three-year recovery plan in the wake of the 2008 financial crisis and regulatory reforms. They needed capital for their own recovery and questioned Ping An's technology spending. The partnership that had defined Ping An's previous era was fraying.

The philosophical divergence was stark. HSBC saw technology as operational efficiency—cutting costs, improving margins. Ping An saw technology as strategic transformation—new business models, new revenue streams. When HSBC executives visited Ping An's new innovation lab in 2011, filled with 3D printers and virtual reality headsets, one reportedly asked: "What does this have to do with insurance?" The Ping An executive's response: "Everything and nothing."

But the real validation came from an unexpected source: the Chinese government. In 2012, Beijing announced its "Internet Plus" strategy, encouraging traditional industries to embrace digital transformation. Ping An, which had started its pivot four years earlier, was perfectly positioned. They became the poster child for China's financial technology ambitions, hosting delegations from ministries and state-owned enterprises studying their transformation.

The crisis-driven transformation also created internal entrepreneurs. Engineers who joined to build systems started proposing business models. The idea for Lufax, a peer-to-peer lending platform, came from a team frustrated with bank lending inefficiency. The concept for Good Doctor, a telemedicine platform, emerged from data scientists analyzing health insurance claims. These weren't top-down initiatives but bottom-up innovations enabled by technology infrastructure.

By 2012, Ping An was unrecognizable from its pre-crisis incarnation. The company employed more software engineers than insurance actuaries. Patent applications exceeded 1,000 annually. Technology subsidiaries were approaching unicorn valuations independently. The financial conglomerate had become a technology platform that happened to offer financial services—exactly as Ma had envisioned in that October 2008 strategy session.

The transformation lessons were profound. First, crisis creates opportunity for fundamental reinvention, not just incremental improvement. Second, technology transformation requires cultural transformation—you can't digitize a traditional mindset. Third, patient capital and long-term thinking enable bets that quarterly-focused competitors can't make. Finally, in platform economics, ecosystem breadth matters more than product depth.

As 2012 ended, Ping An stood at another inflection point. The technology foundation was built. The cultural transformation was complete. The ecosystem vision was clear. Now came the audacious next step: spinning out technology subsidiaries as independent unicorns, competing not just with insurers and banks but with Alibaba, Tencent, and Silicon Valley. The four unicorns strategy—Lufax, OneConnect, Good Doctor, and HealthConnect—would test whether a 25-year-old insurance company could birth the next generation of technology giants.

VI. Building the Tech Empire: The Four Unicorns (2011–2020)

The conference room on the 47th floor of Ping An's Shenzhen headquarters was silent as Gregory Gibb, the former McKinsey partner who had just joined as CEO of Lufax, finished his presentation. It was January 2011, and he had just proposed something that sounded insane: build a peer-to-peer lending platform that would eventually rival banks, despite having no banking license, no branches, and no deposit base. Peter Ma broke the silence: "If we don't disrupt ourselves, someone else will disrupt us. Approved."

That moment launched Ping An's most audacious strategy yet—creating independent technology companies that would compete in the open market, not just serve internal needs. The plan was to build four unicorns, each addressing massive market inefficiencies in Chinese financial services and healthcare. It was corporate venture building on steroids, with a twist: these wouldn't be mere subsidiaries but independent entities that could IPO separately, creating value beyond Ping An's traditional insurance multiple.

Lufax came first, born from a simple observation: small businesses and individuals couldn't get loans from traditional banks, while savers earned negligible returns on deposits. The platform would connect them directly, using technology to assess risk and facilitate transactions. Gibb recruited talent from Goldman Sachs, Google, and Alibaba, creating a culture clash that energized innovation. The early days were chaotic—regulators didn't understand the model, customers didn't trust online lending, and traditional Ping An executives worried about reputation risk.

The breakthrough came through trust innovation. Lufax didn't just match lenders and borrowers; it provided guarantees through Ping An's balance sheet, essentially using the insurance company's credibility to bootstrap a new business model. By 2012, transaction volume exceeded RMB 1 billion monthly. By 2014, Lufax had raised $500 million from external investors at a $10 billion valuation, making it the world's largest fintech unicorn at the time. The OneConnect story began differently. Founded in December 2015, it emerged from Ping An's recognition that their internal technology capabilities could solve industry-wide problems. By June 2020, OneConnect had served all of China's major banks, 99% of its city commercial banks and 53% of its insurance companies. The value proposition was compelling—smaller financial institutions couldn't afford to build AI, blockchain, or cloud infrastructure themselves, but they desperately needed these capabilities to compete. OneConnect would provide technology-as-a-service, essentially democratizing financial technology.

The early traction was explosive. Regional banks that had never heard of machine learning were suddenly using AI for credit scoring. Insurance companies still processing claims on paper adopted automated settlement systems. By 2018, OneConnect was processing 10 billion transactions annually, with 99.99% uptime—better reliability than most Silicon Valley giants.

OneConnect was listed on the New York Stock Exchange in 2019, raising $312 million despite a difficult IPO market. The roadshow was challenging—American investors struggled to understand why a Chinese insurance company was selling technology to competitors. But the numbers spoke: 3,700 financial institution clients, $350 million in revenue, and growth rates exceeding 50% annually.

Ping An Good Doctor, launched in 2014, attacked an even bigger problem: China's broken healthcare system. With 1.4 billion people served by just 3 million doctors, Chinese patients faced hours-long waits for minutes-long consultations. The platform would connect patients with doctors online, using AI for initial diagnosis and triage. Ma's vision was breathtaking in scope—not just telemedicine, but a complete healthcare ecosystem including drug delivery, health management, and insurance integration.

The skeptics were numerous and vocal. Doctors worried about liability. Patients doubted online diagnosis. Regulators had no framework for digital healthcare. But Jessica Tan, who led the initiative, had a secret weapon: Ping An's 200 million insurance customers who desperately needed better healthcare access. She offered the service free to Ping An policyholders, creating instant scale that attracted doctors and built trust.

The AI capabilities were genuinely innovative. The platform's diagnostic assistant was trained on 300 million medical records, achieving accuracy rates comparable to experienced doctors for common conditions. By 2017, Good Doctor had 190 million registered users and 1,000 in-house doctors providing 24/7 consultations. Daily consultations exceeded 530,000—more than most hospital systems handle monthly.

The IPO in Hong Kong in May 2018 raised $1.1 billion, the largest global healthcare technology IPO at the time. The stock jumped 4.6% on the first day, valuing the company at $7.5 billion. But more important than the financial success was the model validation—a four-year-old startup from an insurance company was now China's largest digital healthcare platform.

The fourth unicorn, HealthKonnect (the healthcare data platform), was the most ambitious yet least visible. Launched in 2016, it aimed to solve healthcare's fundamental problem: data fragmentation. Patient records were scattered across hospitals, clinics, and insurers with no interoperability. HealthKonnect would create a unified health data platform, using blockchain for security and AI for insights.

The technical challenges were staggering. Chinese hospitals used hundreds of different record systems, many paper-based. Privacy regulations were strict but inconsistent. The platform needed to handle billions of records while maintaining millisecond response times. The team, led by former Microsoft and Alibaba engineers, built one of the world's largest healthcare blockchains, processing 30 million blocks daily by 2019.

The ecosystem synergies among the four unicorns created competitive moats that pure-play competitors couldn't replicate. Lufax users were offered Good Doctor consultations. OneConnect's AI models were trained on Lufax's lending data. HealthKonnect's patient insights improved Ping An's insurance underwriting. Good Doctor's diagnosis data enhanced HealthKonnect's algorithms. It was platform economics at its most sophisticated—each business strengthened the others.

The cultural transformation required to birth these unicorns was profound. Ping An created "garage rules"—startup teams could ignore corporate policies if they conflicted with innovation speed. Failed projects were celebrated if lessons were learned. Engineers could spend 20% of time on personal projects, some of which became major products. The Shenzhen campus added basketball courts, sleep pods, and a 24-hour cafeteria—Silicon Valley perks with Chinese characteristics.

The talent war was intense. Ping An competed with Alibaba, Tencent, and ByteDance for the same engineers. Ma's solution was unique: offer not just competitive compensation but meaningful mission. "Alibaba sells things, Tencent connects people, we save lives," became the recruiting pitch. The company sponsored AI competitions, partnered with universities, and created China's largest financial technology internship program.

By 2020, the four unicorns strategy had exceeded all expectations. Lufax launched its IPO on the New York Stock Exchange, the 5th largest IPO in the US that year. Combined, the four unicorns were valued at over $100 billion—more than many traditional insurers globally. They employed 50,000 people, served 500 million users, and generated $10 billion in revenue. The insurance company had successfully birthed a technology empire.

But the real validation came from competitors. AXA, Allianz, and MetLife all launched similar initiatives, explicitly citing Ping An as inspiration. Chinese banks created technology subsidiaries. Even the government launched initiatives to encourage traditional companies to build tech platforms. The model Ma had pioneered—traditional company as tech incubator—became the template for digital transformation globally.

The lessons were clear: First, internal capabilities can become external businesses if the market need is large enough. Second, independent subsidiaries with startup culture can thrive within corporate structures if given sufficient autonomy. Third, ecosystem synergies can create competitive advantages that standalone companies can't match. Finally, traditional companies shouldn't fear cannibalizing existing businesses—if you don't disrupt yourself, someone else will.

As 2020 began, Ping An faced new challenges. Regulatory scrutiny was intensifying. The P2P lending crisis had damaged fintech's reputation. COVID-19 was spreading. But these challenges would actually accelerate Ping An's next transformation: from financial services provider to healthcare company. The pandemic that shut down the world would open up Ping An's biggest opportunity yet.

VII. Healthcare & Ecosystem Strategy (2014–Present)

The emergency room at Shenzhen People's Hospital was chaos. It was February 2020, peak COVID-19 panic, and hundreds of worried citizens with minor symptoms were overwhelming the system, preventing genuinely sick patients from getting care. In a makeshift command center, Ping An Good Doctor's crisis team worked around the clock, their platform handling 1.1 billion visits in just three months—10 times normal volume. While the pandemic devastated traditional businesses, it validated Ma's decade-long healthcare bet in ways no business plan ever could.

The healthcare vision had actually started years earlier, born from a simple insight: China's insurance claims data revealed a healthcare system in crisis. Diabetes rates were exploding. Cancer diagnoses came too late. Chronic diseases consumed 70% of medical spending but received minimal preventive care. Ma saw opportunity where others saw intractable problems—if Ping An could fix healthcare delivery, it could reduce insurance costs while creating massive new revenue streams.

The strategy went far beyond telemedicine apps or wellness programs. Ping An envisioned nothing less than reimagining healthcare delivery for 1.4 billion Chinese citizens. This meant building physical clinics, training AI doctors, creating health management protocols, and most audaciously, implementing a "managed care" model that aligned incentives across patients, providers, and payers—something even America's HMOs struggled to achieve.

The first piece was digital infrastructure. By 2015, Good Doctor had evolved from simple online consultations to comprehensive health management. The platform's AI assistant could handle 2,000 diseases, achieving 90% accuracy for common conditions. But the real innovation was the hybrid model—AI for initial screening, human doctors for complex cases, creating efficiency impossible with pure human or pure AI approaches.

The numbers were staggering. By 2019, before COVID-19, Good Doctor was handling 700,000 daily consultations with just 1,500 in-house doctors—each doctor effectively serving 467 patients daily through AI augmentation. Traditional hospitals averaged 30 patients per doctor per day. The platform had contracted with 50,000 external specialists who could be consulted for complex cases, creating China's largest virtual hospital network.

Physical infrastructure came next. Ping An opened One-Minute Clinics in shopping malls and office buildings—unmanned booths where patients could consult AI doctors, get basic tests, and receive medications. Over 1,000 clinics were deployed by 2020, handling 3 million consultations annually. Each clinic cost $15,000 to build but generated $50,000 in annual revenue—a payback period under four months.

The home healthcare push was even more ambitious. As of 30 June 2024, Ping An's home-based senior care services covered 64 cities across China with over 120,000 customers entitled to the benefits. This wasn't just meal delivery or nurse visits but comprehensive care coordination—medication management, rehabilitation services, chronic disease monitoring, emergency response. The platform connected 10,000 care providers through a single app, creating accountability and efficiency unprecedented in home healthcare.

The managed care model adaptation for China required delicate innovation. Unlike America's HMOs that restricted patient choice, Ping An created incentive alignment through technology and convenience. Patients who used Good Doctor for primary care received insurance discounts. Doctors who achieved better outcomes earned bonuses. Hospitals that reduced readmission rates got preferential referrals. The system rewarded health, not just treatment.

The integration with insurance was seamless and powerful. When a Ping An policyholder reported symptoms on Good Doctor, the system automatically checked their coverage, suggested in-network providers, and even pre-authorized treatments. Claims were processed in real-time—patients never saw bills. This convenience drove adoption: insurance customers who used Good Doctor had 20% lower claims costs and 30% higher retention rates.

The chronic disease management programs showed particular promise. Ping An created "digital twins" for diabetes patients—AI models that predicted complications based on continuous glucose monitoring, lifestyle data, and genetic markers. Patients received personalized intervention plans updated daily. Early results were remarkable: 40% reduction in hospitalizations, 25% improvement in HbA1c levels, and paradoxically, higher patient satisfaction despite more intensive management.

COVID-19 accelerated everything. In January 2020, Good Doctor launched a free COVID-19 consultation service that handled 10 million consultations in the first month alone. The platform's AI was quickly trained on COVID-19 symptoms, achieving 96% accuracy in identifying high-risk cases requiring hospital care. While hospitals were overwhelmed, Good Doctor provided calm, professional guidance to panicked citizens from their homes.

The pandemic response showcased capabilities competitors couldn't match. Ping An leveraged its insurance data to identify high-risk populations for proactive outreach. Its logistics network delivered medications to locked-down communities. Its financial services provided emergency loans to affected families. The ecosystem approach—impossible for standalone healthcare companies—saved lives while building unshakeable customer loyalty.

The eldercare ecosystem emerged as the next frontier. China's aging tsunami—400 million citizens over 60 by 2040—represented both crisis and opportunity. Ping An had unveiled premium health and senior care communities in five cities as of December 31, 2024, which are currently under construction. The communities in Shanghai and Shenzhen are scheduled to open for business in the second half of 2025. These weren't traditional nursing homes but integrated communities combining residential living, medical care, and lifestyle services, all connected through Ping An's technology platform.

The business model innovation was clever. Customers could purchase eldercare community residency through insurance products, essentially pre-funding retirement care while healthy. This created predictable revenue streams, reduced sales costs, and aligned everyone's interests in keeping residents healthy. Early pre-sales exceeded expectations, with Shanghai's 800-unit community selling out despite construction being years away.

The healthcare strategy's impact on insurance was transformative. Customers entitled to service benefits in the healthcare and elderlycare ecosystem accounted for over 68% of Ping An Life's new business value in 2024. Customers weren't buying insurance anymore; they were buying into a healthcare ecosystem with insurance included. This repositioning drove premium growth even as traditional insurers struggled.

The technology investments were massive but strategic. Ping An spent $2 billion annually on healthcare R&D, filing over 10,000 healthcare-related patents. They built China's largest medical AI training facility, with 100 petabytes of anonymized health data. They partnered with Harvard Medical School and Mayo Clinic for clinical validation. The goal wasn't just Chinese leadership but global healthcare innovation.

The regulatory navigation required for healthcare was even more complex than financial services. Healthcare touched national security, social stability, and personal privacy. Ping An executives spent countless hours in Beijing, explaining their model to skeptical officials. The breakthrough came when they positioned themselves not as disrupting public healthcare but as supplementing it—reducing pressure on overwhelmed public hospitals while improving population health.

Competition emerged from unexpected quarters. Alibaba launched Alibaba Health. Tencent invested in WeDoctor. JD.com created JD Health. But Ping An's advantages were structural—insurance customer base providing immediate scale, claims data enabling better risk prediction, and most importantly, aligned incentives where Ping An profited from keeping people healthy, not just treating illness.

International expansion beckoned. Southeast Asian countries with similar healthcare challenges—large populations, insufficient infrastructure, rising chronic disease—were natural markets. Ping An partnered with local insurers in Thailand, Indonesia, and Malaysia, licensing technology while adapting to local regulations. The vision was ambitious: become Asia's healthcare platform, not just China's.

The recent AI integration took capabilities to another level. In February 2025, Ping An Healthcare and Technology announced that its artificial intelligence model and its platform designed for doctors now have built in access to DeepSeek's model. This partnership with China's leading AI company enabled diagnostic capabilities approaching specialist physician levels for complex conditions.

By 2024, the healthcare ecosystem had become Ping An's growth engine and competitive moat. Healthcare services revenue exceeded $5 billion. Good Doctor served 400 million users. The platform handled 1 billion annual consultations. More importantly, healthcare wasn't a separate business but the glue binding insurance, banking, and investment services into an integrated life services platform.

The strategic lessons were profound. First, healthcare requires patient capital—Ping An invested for a decade before significant returns. Second, ecosystem approaches can solve problems that vertical integration cannot. Third, technology enables new business models, not just operational efficiency. Finally, addressing societal challenges creates both purpose and profit.

As Ping An entered its fourth decade, healthcare had transformed it from a financial services company that happened to offer health insurance into a health services company that happened to offer financial products. The transformation Ma envisioned in 2008—from traditional insurer to technology company—was complete. But new challenges loomed: regulatory scrutiny, competitive pressure, and the ultimate question of succession as Ma approached retirement.

VIII. Leadership Transition & Modern Era (2020–Present)

The announcement came via a simple press release on July 1, 2020, but its implications reverberated through Asian financial markets: Peter Ma Mingzhe, the only CEO Ping An had ever known, was stepping down from day-to-day operations while remaining chairman. In his place, three co-CEOs would share responsibilities—a structure that management consultants said would never work. Yet this unconventional transition would prove to be Ma's final masterstroke, ensuring continuity while enabling transformation in an era of unprecedented regulatory and competitive challenges.

The three co-CEOs represented different facets of Ping An's evolution. Jessica Tan, the MIT-trained technologist who had built the healthcare ecosystem, would oversee technology and innovation. Xie Yonglin, a banking veteran who had transformed Ping An Bank from also-ran to digital leader, would manage traditional financial services. Yao Bo, the insurance lifer who understood Ping An's cultural DNA, would handle insurance and investments. Together, they embodied Ping An's past, present, and future.

The transition had been meticulously planned for years. Ma had studied succession failures at other Chinese companies where founder departures created chaos. He implemented a "shadow cabinet" system where potential successors ran parallel organizations, proving capabilities before promotion. The co-CEO structure wasn't compromise but design—forcing collaboration while preventing any single person from undoing Ping An's ecosystem model.

The immediate challenge was navigating China's regulatory tsunami. The Ant Financial IPO cancellation in November 2020 signaled Beijing's determination to rein in fintech giants. P2P lending platforms were being shut down. Data privacy laws were tightening. The "common prosperity" agenda questioned excessive profits. Ping An, with its fingers in every financial pie, was squarely in regulatory crosshairs.

The co-CEOs' response was masterful. Rather than resistance or retreat, they embraced "regulatory alignment." Lufax voluntarily withdrew from P2P lending before being forced, taking a $2 billion writedown but preserving reputation. They open-sourced OneConnect's blockchain platform, positioning it as financial infrastructure rather than proprietary advantage. They pledged $15 billion for "common prosperity" initiatives, funding rural healthcare and education.

The data governance transformation was particularly impressive. New regulations required data localization, algorithm transparency, and user consent. Ping An rebuilt its entire data architecture, creating what they called "privacy-preserving AI"—models that could learn from data without accessing individual records. The investment exceeded $500 million, but it positioned Ping An as the compliance gold standard while competitors scrambled.

The strategic focus also shifted subtly but significantly. While Ma had pursued growth at all costs, the new leadership emphasized quality and sustainability. "From scale to value" became the mantra. Agent numbers were reduced but productivity increased. Product portfolios were simplified. Marginal businesses were shut down or sold. The goal wasn't to be biggest but best—highest margins, lowest risk, strongest moat.

The cultural evolution was fascinating to observe. Ma's charismatic leadership style—inspirational speeches, bold visions, personal interventions—gave way to systematic management. The co-CEOs instituted "OKRs" (Objectives and Key Results) across all divisions. They created "tiger teams" for cross-functional initiatives. They even hired McKinsey to redesign organizational structure—unthinkable under Ma's entrepreneurial reign.

The biggest test came in 2023 with the HSBC proxy battle. In May 2023, HSBC defeated a proposal, backed by its largest stakeholder Chinese insurer Ping An, to consider spinning off its Asia business into a Hong Kong-listed entity. Ping An, now HSBC's largest shareholder after years of accumulation, pushed for value creation through restructuring. The proposal's defeat was embarrassing but revealing—Ping An had evolved from junior partner seeking Western expertise to activist investor demanding strategic change.

The technology strategy under new leadership became more focused but no less ambitious. Rather than building everything internally, they embraced partnerships. The DeepSeek collaboration for AI was just the beginning. They partnered with Microsoft for cloud infrastructure, with Ethereum for blockchain protocols, with Toyota for autonomous vehicle insurance. The philosophy shifted from "not invented here" to "best in class wherever it comes from."

The international expansion strategy also matured. Rather than acquisitions or greenfield operations, Ping An focused on technology licensing and joint ventures. They signed deals with banks in Japan, insurers in India, and healthcare providers in Vietnam. The model was asset-light but impact-heavy—earning fees while avoiding regulatory complexity and capital requirements.

The generational challenge was acute. Ping An's workforce had grown to 600,000, with stark divides between digital natives and insurance veterans. The co-CEOs instituted "reverse mentoring" where young employees taught executives about social media and cryptocurrency. They created "Ping An University" offering degrees in fintech and health-tech. They even launched internal competition shows where employees pitched new business ideas, with winners getting funding and autonomy.

The numbers under new leadership impressed skeptics. Despite regulatory headwinds and COVID-19 disruption, operating profit grew steadily. Net profit attributable to shareholders of the parent company rose 47.8% year on year to RMB126,607 million in 2024. Revenue reached RMB1,141,346 million, an increase of 10.6% YoY. Customer satisfaction scores reached all-time highs. Employee engagement improved despite organizational changes.

The innovation pipeline remained robust. Ping An launched China's first parametric insurance products, automatically paying claims based on external triggers like earthquakes or flight delays. They created "embedded insurance" integrated into e-commerce and ride-sharing platforms. They even experimented with "DeFi insurance" using smart contracts, though regulatory concerns limited deployment.

The ESG (Environmental, Social, Governance) transformation under new leadership was substantial. Ping An achieved an AA rating in MSCI ESG rankings in 2024, securing the top spot in the Asia-Pacific multi-line insurance and brokerage industry for the third year in a row. They committed to carbon neutrality by 2030, divested from coal investments, and launched green insurance products. The social initiatives were equally impressive—free insurance for gig workers, microfinance for rural entrepreneurs, AI doctors for underserved communities.

The succession planning for the next generation was already underway. The co-CEOs identified high-potential leaders in their 30s and 40s, rotating them through different businesses and geographies. They created a "founders program" where entrepreneurial employees could propose and lead new ventures. They even recruited talent from ByteDance and Pinduoduo, bringing fresh perspectives to a maturing organization.

Ma's role as chairman evolved into elder statesman and chief visionary. He focused on long-term strategy, government relations, and what he called "impossible projects"—moonshots like using satellite data for agricultural insurance or blockchain for international remittances. His presence provided continuity and confidence while allowing new leadership operational freedom.

The competitive landscape had transformed dramatically. Traditional insurers like China Life had digitalized aggressively. Tech giants like Tencent and Alibaba had financial licenses. International players like AXA and Allianz were expanding in Asia. New entrants with innovative models emerged monthly. The moats that had protected Ping An were eroding.

But the new leadership's response revealed confidence, not concern. They welcomed competition as validation of their model. They open-sourced non-core technologies to shape industry standards. They created venture funds to invest in potential disruptors. Most cleverly, they positioned Ping An as the platform that enabled others' success rather than competing directly.

The 2024 performance demonstrated the transition's success. New business value for life insurance grew 34%. The combined ratio for P&C insurance improved to 98.3%. Banking ROE exceeded 11%. Technology subsidiaries achieved profitability. The company that skeptics said would stumble without its founder was thriving under collective leadership.

As 2025 began, Ping An stood at another crossroads. The co-CEO structure had worked but wouldn't last forever. The regulatory environment remained uncertain. Competition was intensifying. Technology was evolving rapidly. But the company had proven something important: successful succession wasn't about finding another Peter Ma but about evolving beyond dependence on any single leader.

IX. Playbook: Lessons from the Ping An Story

The Harvard Business School case study writers who descended on Ping An's Shenzhen headquarters in 2019 expected to find a typical emerging market success story—copy Western models, execute with Chinese efficiency, profit from scale. Instead, they discovered something far more interesting: a company that had written an entirely new playbook for financial services in the digital age. The lessons from Ping An's journey weren't just about insurance or China; they were about how traditional companies could transform themselves into technology platforms while navigating regulatory complexity and competitive disruption.

The "Integrated Finance" Model: One Customer, Multiple Products

The conventional wisdom in financial services was specialization—be the best at one thing. Ping An rejected this, building what they called "integrated finance"—one customer accessing all financial services through a single relationship. This wasn't the failed "financial supermarket" model of 1990s America but something more sophisticated: products that reinforced each other, data that improved all decisions, and convenience that created stickiness.

The execution required overcoming massive technical and organizational challenges. Different products had different systems, regulations, and economics. The solution was elegant: a single customer identifier across all businesses, shared data lakes with privacy protection, and most importantly, aligned incentives where divisions were rewarded for cross-selling, not just individual product performance.

The results validated the model. Customers with multiple products had 90% retention rates versus 60% for single-product customers. Customer acquisition costs dropped 40% through cross-selling. Most importantly, lifetime value increased 3.5x as customers deepened relationships over time. The model worked because it solved a real customer problem—managing financial life was complex, and Ping An simplified it.

Technology as Core Competency, Not Add-On

The 1% revenue rule—investing 1% of total revenue in R&D annually—seemed modest compared to pure technology companies spending 15-20%. But for a financial services company generating $150 billion in revenue, this meant $1.5 billion annually, more than most Silicon Valley unicorns' entire valuations. This wasn't IT spending on servers and software but genuine R&D—AI research, blockchain development, quantum computing experiments.

The organizational structure was crucial. Technology wasn't a support function reporting to operations but a profit center with its own P&L. Engineers weren't cost centers but revenue generators. Innovation wasn't a department but a company-wide mandate with every employee expected to contribute ideas. The culture shift was dramatic—actuaries learned Python, bank tellers suggested app features, insurance agents became data analysts.

The intellectual property strategy was particularly clever. While competitors outsourced technology to vendors, Ping An built proprietary capabilities and patented aggressively—53,521 patent applications by 2024. These patents weren't defensive but offensive, creating barriers to competition and licensing opportunities. When OneConnect went public, investors weren't buying insurance distribution but technology IP.

Building Ecosystems vs. Products

Ma's insight that "platform economics trump product economics" drove Ping An's ecosystem strategy. Rather than selling insurance policies, they sold membership in a life services ecosystem. Rather than offering bank accounts, they provided financial management platforms. Rather than competing on price, they competed on convenience and comprehensiveness.

The ecosystem construction followed a pattern. First, identify a massive customer pain point (healthcare access, financial complexity). Second, build or acquire point solutions (Good Doctor, Lufax). Third, integrate solutions into seamless experiences. Fourth, add adjacent services that increase engagement. Finally, monetize through multiple revenue streams—direct fees, insurance premiums, data insights, platform taxes.

The network effects were powerful. Each new service made existing services more valuable. Each new customer reduced unit costs for all customers. Each new data point improved AI models for everyone. Competitors could copy products but couldn't replicate ecosystems without similar scale, capabilities, and patience.

Patient Capital and Long-Term Thinking

In an industry obsessed with quarterly earnings, Ping An's long-term orientation was revolutionary. The healthcare ecosystem took 10 years to achieve profitability. Technology subsidiaries burned billions before breaking even. New market entries required 5-7 years to achieve scale. Yet Ping An persisted where others would have pivoted or quit.

This patience was enabled by ownership structure and expectation management. With no controlling shareholder demanding immediate returns, management could invest for decades. By consistently communicating long-term strategy and delivering on promises, they earned investor trust. The virtuous cycle was self-reinforcing—patient capital enabled long-term bets, which created competitive advantages, which generated superior returns, which attracted more patient capital.

The time horizon affected every decision. Hiring focused on potential over experience. Partnerships prioritized strategic value over immediate economics. Investments targeted transformation over optimization. The question wasn't "what delivers returns this quarter?" but "what positions us to win in 2030?"

Navigating Regulatory Complexity

Operating in China's regulatory environment—where rules changed frequently, enforcement was inconsistent, and political winds shifted suddenly—required unique capabilities. Ping An developed what insiders called "regulatory kung fu"—not fighting regulations but flowing with them, turning constraints into advantages.

The approach had several elements. First, proactive engagement—briefing regulators before launching products, not after. Second, compliance excellence—exceeding requirements to build credibility. Third, strategic alignment—positioning initiatives as supporting government priorities. Fourth, rapid adaptation—changing direction quickly when policies shifted. Finally, patience—accepting that some initiatives would take years to approve.

The regulatory relationships became competitive advantages. When P2P lending was banned, Ping An had already exited. When data privacy laws tightened, Ping An was already compliant. When "common prosperity" became priority, Ping An had already launched inclusive finance initiatives. Competitors scrambled while Ping An sailed smoothly forward.

Culture as Strategy

The cultural transformation from traditional insurer to technology company wasn't just organizational change but strategic necessity. The famous "kill the not-invented-here syndrome" campaign symbolized deeper shifts—from hierarchy to meritocracy, from risk avoidance to intelligent risk-taking, from Chinese insularity to global perspective.

The mechanisms were deliberate and systematic. Performance reviews weighted innovation equally with execution. Failure analyses focused on learning, not blame. Town halls where any employee could question executives built transparency. Stock options aligning employee and shareholder interests created ownership mentality. The result was a culture that attracted top talent and enabled rapid adaptation.

The East-meets-West fusion created unique advantages. Chinese entrepreneurial energy combined with Western management discipline. Local market knowledge enhanced by global best practices. Relationship-based business development supported by data-driven decision making. The hybrid model proved more robust than pure Eastern or Western approaches.

The Innovation Factory Model

The four unicorns strategy demonstrated that large companies could be successful venture builders. The key was treating internal ventures like external startups—separate teams, independent funding, entrepreneurial culture, and most importantly, freedom to cannibalize existing businesses.

The selection criteria were strict. Ventures needed to address billion-dollar markets, leverage Ping An's unique assets, achieve standalone viability, and create ecosystem synergies. The execution followed Silicon Valley practices—MVP development, rapid iteration, pivot readiness, growth hacking. But unlike Silicon Valley, failures weren't career-ending but learning experiences.

The incentive alignment was crucial. Venture teams received phantom equity providing upside if successful. Core business units were compensated for customer referrals and data sharing. The parent company accepted short-term earnings dilution for long-term value creation. Everyone won when ventures succeeded.

Lessons for Global Financial Services

Ping An's playbook offers lessons beyond China. First, digital transformation requires cultural transformation—you can't digitize analog mindsets. Second, platforms beat products in customer acquisition and retention. Third, ecosystems create moats that pure financial returns cannot. Fourth, technology is becoming the business, not just enabling it. Finally, winners will be those who solve customer problems, not those who sell financial products.

The execution challenges are real. Building ecosystems requires massive capital, patient investors, technical capabilities, and regulatory navigation skills. Cultural transformation takes years and faces internal resistance. Platform economics are different from product economics, requiring new metrics and mindsets. Not every company can or should follow Ping An's path.

But the strategic insights are universal. Customers want solutions, not products. Technology enables new business models, not just efficiency. Ecosystems create value that vertical integration cannot. Long-term thinking beats quarterly optimization. And most importantly, in a world of infinite choice and zero switching costs, customer experience is the only sustainable competitive advantage.

X. Bear vs. Bull Case & Valuation Discussion

The debate at the Sohn Investment Conference in Hong Kong was getting heated. On one side, a Tiger Global partner argued Ping An deserved a technology multiple—after all, its tech subsidiaries alone were worth $100 billion. On the other, a seasoned value investor from Edinburgh insisted it was still an insurance company with fancy apps, deserving traditional financial valuations. This encapsulated the fundamental tension in valuing Ping An: Is it a tech company that happens to sell insurance, or an insurer with tech subsidiaries? The answer determines whether it's dramatically undervalued or fairly priced.

The Bull Case: The Hidden Tech Giant

The bullish argument starts with sum-of-the-parts math that seems almost too obvious. Lufax went public at a peak valuation exceeding $30 billion. OneConnect reached $7 billion. Good Doctor hit $15 billion. The unlisted HealthKonnect could be worth $10-20 billion based on comparable health tech valuations. Add these up and the tech subsidiaries alone approach $70-100 billion—nearly Ping An's entire market capitalization.

But the bull case goes deeper than arithmetic. Ping An's core insurance business generates $15-20 billion in annual operating profit with stable growth. Applying a conservative 10x multiple (below global insurance peers) yields $150-200 billion. The banking business earns $5 billion annually; at book value, it's worth another $50 billion. Add the tech subsidiaries and you get $300+ billion in value versus a market cap often below $150 billion—a 50% discount.

The ecosystem moat argument is even more compelling. No competitor can replicate Ping An's integrated platform. Building Good Doctor from scratch would take a decade and billions in losses. Replicating OneConnect's 3,700 financial institution relationships would be nearly impossible. The data advantage—billions of insurance claims, banking transactions, and health records—creates AI capabilities that improve exponentially with scale.

The growth trajectory supports premium valuations. Healthcare services are growing 30% annually in a market expanding from $1 trillion to $3 trillion by 2030. Digital financial services penetration in China remains below 50%, suggesting years of growth ahead. The international expansion into Southeast Asia opens 600 million new potential customers. If Ping An captures even 10% of these opportunities, revenues could double.

The technology transformation deserves recognition. With 21,000 engineers and 53,521 patents, Ping An invests more in R&D than most Silicon Valley unicorns. Their AI diagnostic tools match specialist physicians. Their blockchain processes millions of transactions daily. Their cloud infrastructure handles Black Friday-level traffic every day. This isn't an insurance company with apps; it's a technology platform that happens to originate through insurance.

Chinese government support provides tailwinds. The "Healthy China 2030" initiative aligns perfectly with Ping An's healthcare ecosystem. Digital finance initiatives favor established players over disruptive startups. The Greater Bay Area integration benefits Shenzhen-based companies. Unlike tech giants facing regulatory crackdowns, Ping An operates in encouraged sectors with government blessing.

The financial fortress provides downside protection while enabling upside optionality. With $1.6 trillion in assets and regulatory capital well above requirements, Ping An can weather any crisis. The diversification across insurance, banking, and technology reduces concentration risk. The recurring premium income provides stable cash flows funding growth investments. This isn't a speculative tech bet but a profitable giant with venture options.

The Bear Case: The Conglomerate Discount is Deserved