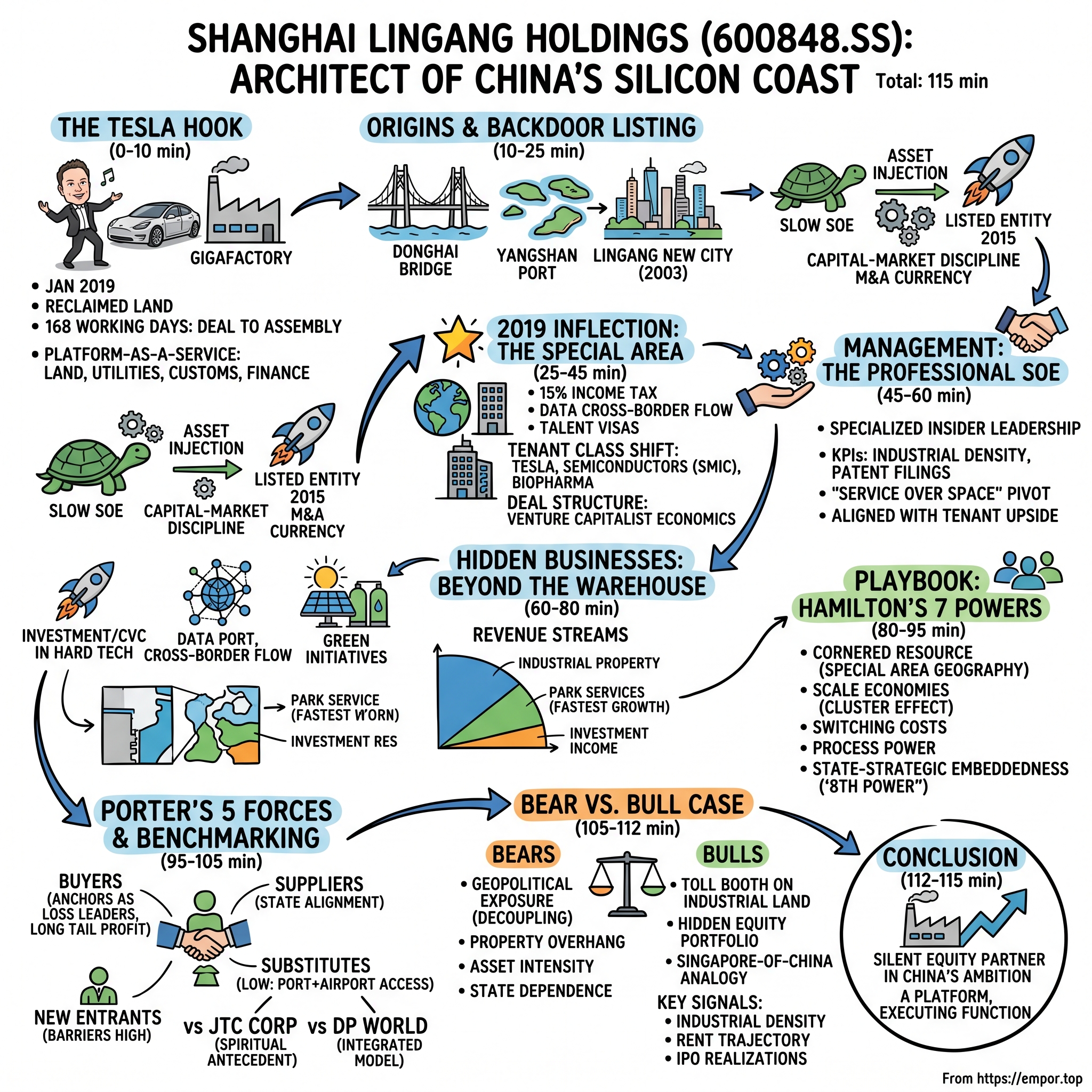

Shanghai Lingang Holdings: The Architect of China's Silicon Coast

I. The Hook: The Tesla Giga-Factor (0:00 – 10:00)

January 7, 2019. A flat, reclaimed plain of damp earth south of Shanghai, where the Yangtze silt meets the East China Sea. The wind off Hangzhou Bay carried the salt of a coastline that, just two decades earlier, had been ocean. On a small stage, surrounded by hard-hatted officials and the bewildered stares of a Chinese press corps that had never quite seen anything like this, Elon Musk began to dance.

It was not an elegant dance. It was the awkward, jubilant shuffle of a founder who had just been handed something almost no foreign executive had ever received in the People's Republic: a fully-licensed, wholly-owned factory site, approved for construction in a matter of weeks rather than years. Behind him, the red banners read "Shanghai Gigafactory — Tesla." In front of him, a stretch of barren industrial plots that, on Google Maps, still looked like a half-finished jigsaw puzzle.

Then came the statistic that defied every manufacturing textbook on earth. From the signing of the land transfer to the first Model 3 rolling off the line, Tesla needed just 168 working days. To put that in perspective, Tesla's Nevada Gigafactory had taken years of permits and litigation before a single battery was pressed. Volkswagen's factories in Tennessee had broken ground only to stall for environmental reviews. And here, on a field that had been literally dredged out of the Pacific, a foreign carmaker went from signed deal to final assembly in less than a single orbit of the moon.

How did a wasteland 75 kilometers from the Shanghai city center — a place so remote that Shanghainese taxi drivers used to refuse the fare — become the only patch of ground on earth capable of compressing a global auto factory's birth cycle into half a year? The answer was not in Tesla. It was not even in Beijing. The answer sat, listed on the Shanghai Stock Exchange under the ticker 600848, buried within the dense financial footnotes of a company most western investors had never heard of: Shanghai Lingang Holdings Co., Ltd.

Here is the insight most observers missed in 2019, and which has only grown louder by 2026. Lingang Holdings is not a real estate company, despite what its balance sheet suggests. It is not even a developer in the traditional sense. What Lingang actually operates is one of the most ambitious "Platform-as-a-Service" businesses ever constructed in the physical economy — a vertically integrated stack that bundles land, utilities, customs clearance, tax arbitrage, supply-chain proximity, financing, visa processing, and equity capital into a single offering. If Amazon Web Services rented you compute by the hour, Lingang rented you a country by the acre.

The Tesla deal was the moment this thesis became visible to the outside world. But by the time Musk was dancing in the mud, Lingang had already spent two decades laying down the physical and institutional rails. What followed would not just reshape Shanghai's industrial geography. It would become the template the entire Chinese state would replicate for its most strategic industries — semiconductors, biopharma, artificial intelligence, hydrogen, and data. And it would turn a once-sleepy state-owned developer into the quiet landlord of what planners in Beijing now call the "Silicon Coast."

To understand the future of Chinese manufacturing, you have to understand one company. And to understand that company, you have to begin not in 2019, but in the reedy coastline of 2003, when a young city planner named Wu Hui was handed a blank map of the sea and told to design a city.

II. Origins & The "Backdoor" Evolution (10:00 – 25:00)

The myth of Lingang starts, appropriately enough, with a blank spot on a map. In the late 1990s, Shanghai had a problem. The Port of Shanghai, then the busiest in mainland China, had outgrown the Huangpu River. Waters at the existing docks were too shallow for the monstrous new Post-Panamax container ships that were redrawing global trade routes. Ningbo-Zhoushan to the south was already pulling ahead. Busan and Singapore loomed as ever-present threats. The city needed a deep-water port, and fast.

There was just one problem: there was no deep water near Shanghai. The Yangtze River dumped so much sediment into the East China Sea that the entire coastline for a hundred kilometers was a shallow, silty shelf. The only natural deep-water channel within reach of the city was 32 kilometers offshore, around a cluster of rocky islands called Yangshan. So Shanghai, in an act of civil-engineering hubris that still startles visitors, decided to build a bridge.

The Donghai Bridge, completed in 2005, remains one of the longest sea-crossings on earth. It connected mainland Shanghai to the Yangshan archipelago, instantly creating a deep-water port out of thin water. But a port needs a hinterland — warehouses, bonded logistics, trucking yards, worker housing. So on the mainland end of the bridge, planners designated a new zone of reclaimed land called Lingang New City, literally "the city facing the port."

This is where the corporate ancestry begins. The Shanghai Lingang Economic Development Group, the state-owned parent of today's listed entity, was formally founded in 2003 to master-plan, develop, and operate this reclaimed coastal zone. The mandate was simple on paper, epic in reality: take a hundred-plus square kilometers of silt, drain it, build roads, wire up power, lay fiber, zone it for industry, and hand turn-key parcels to manufacturers. The group was explicitly modeled, in internal memos, on Singapore's JTC Corporation — the government-linked industrial estate builder that had spent the 1960s and 70s turning a swampy backwater called Jurong into the petrochemical engine of Southeast Asia.

For the first decade, Lingang Group operated the way any Chinese SOE developer of that era operated. Slow, paternalistic, financed by policy bank loans at low but patient rates. Tenants were mostly heavy industry — shipbuilding yards, wind-turbine assembly, steel-related workshops. Revenue trickled. Returns on capital, measured against the enormous land-reclamation costs, were unflattering. By the mid-2010s, Lingang was, by most accounts, a respected but unremarkable state-owned developer. Competent. Patient. But not the kind of company that moved equity markets.

What changed was a piece of financial engineering that, in retrospect, looks like the single most consequential moment in the company's history: the 2015 backdoor listing.

The mechanics matter here. In Chinese capital markets during the 2010s, the China Securities Regulatory Commission maintained notoriously tight control over direct IPOs. Queues for approval could stretch for years. A faster path existed — the "reverse merger" or "backdoor listing," where a private or unlisted state asset would inject itself into an existing, listed shell company, instantly gaining public-market status. The shells were often sleepy, poorly performing, but tradable. The trick was finding one.

Lingang Group found theirs in Shanghai Songjiang Industrial Investment Co., a dull listed vehicle that had been plodding along under the 600848 ticker. In 2015, Lingang Group engineered a massive asset injection into Songjiang, effectively swapping its prized industrial-park assets in the Lingang and Songjiang districts into the shell and taking majority ownership. Overnight, the listed company transformed from a minor industrial holding into one of the flagship industrial-park developers on the Shanghai Stock Exchange. The ticker stayed 600848. Everything else changed.

Why did this matter beyond plumbing? Three reasons, and each one reshapes how investors should read the company today.

First, capital-market discipline. A sleepy SOE can operate for decades on patient policy-bank loans and never care about quarterly earnings. A listed company, even a state-controlled one, has analysts, minority shareholders, Northbound connect flows, and a stock price that publicly marks its management every single trading day. The moment 600848 started reporting, management's horizon collapsed from "the next Five-Year Plan" to "the next earnings call." That discipline — subtle, grinding, but relentless — pushed Lingang toward asset-light services, higher-margin revenue streams, and the cultivation of tenants who could themselves IPO and create value back to the platform.

Second, a currency for M&A. Public shares gave Lingang Holdings a tradable instrument to acquire new assets from the parent group. Between 2015 and 2020, the listed entity would repeatedly tap equity markets — via directed share issuances, asset swaps, and rights offerings — to absorb additional industrial parks from the parent. In essence, the listing turned the company into a rolling-up machine for the parent's development pipeline.

Third, and most subtly, a signaling device. By putting the Lingang name on the Shanghai exchange, the state was effectively saying: this is not just a regional industrial zone, this is an investable thesis. Money, both Chinese and foreign, could now express a view on the Lingang project by owning the stock. And when the big announcement came in 2018, they did.

The pre-2015 Lingang was a landlord. The post-2015 Lingang was something stranger — a curator of industries, with a public balance sheet, a professional investor base, and a mandate to compound. It still owned the warehouses. But increasingly, the warehouses were becoming almost incidental to the real business.

Which set the stage, in turn, for the largest tail event in the company's history: a line in a speech, delivered on a stage across the city, that would more than double the size of its sandbox overnight.

III. The 2019 Inflection Point: The "Special Area" (25:00 – 45:00)

November 5, 2018. The China International Import Expo at the Shanghai National Exhibition Center. Xi Jinping stood at the podium and delivered the keynote. Toward the end, almost as an aside, he made three announcements. One concerned launching a science and technology innovation board. One concerned elevating the Yangtze Delta integration to a national strategy. And one concerned something called the "Lingang Special Area."

The line was short. Roughly translated: Shanghai will, on the basis of the existing Free Trade Zone, add a new piece of land, called the Special Area, which will implement more open and flexible policies. That was it. No details. No map. No tax schedules. Just the announcement that a new zone would be carved out, somewhere in Shanghai, with rules more liberal than anything else on the Chinese mainland.

Traders who understood the implications immediately started scanning for the beneficiary. The ticker they found was 600848.

On August 6, 2019, the State Council released the implementation plan for the China (Shanghai) Pilot Free Trade Zone Lingang New Area. The geographic footprint was 119.5 square kilometers of core area, with the potential to expand to 873 square kilometers. The policy package was unlike anything previously granted in mainland China: a 15% corporate income tax rate for qualifying advanced industries (compared to the standard 25% on the mainland), streamlined customs and bonded zone treatment, eased data cross-border flow rules, simplified foreign-exchange management, preferential visa and talent policies, and more permissive industry-access lists for foreign investors.

In one stroke, Beijing had effectively created a domestic Singapore. And the master-developer of that Singapore, the listed vehicle that owned most of the developable land within its boundaries and held exclusive rights to a chunk of its utilities, logistics, and data infrastructure, was 600848.

The stock reacted accordingly. Between the November 2018 announcement and mid-2019, shares of Lingang Holdings approximately tripled off the bottom, then consolidated. But the real story was operational, not financial. The Special Area designation did three things to Lingang's business that mattered far more than any single quarter's results.

First, it changed the tenant class. Before 2019, Lingang had attracted mostly domestic and mid-tier foreign manufacturers. After 2019, the list became a who's-who of geopolitically sensitive industries. Tesla came first, in January 2019 — technically pre-Special Area, but negotiated under the same liberalizing logic. Then came the semiconductor cluster: SMIC's most advanced fab investments, Zhongxin Guoji, and a host of equipment and materials suppliers. Then came biopharma majors, including joint ventures with Roche and Johnson & Johnson spin-offs. Then came civil aviation, with COMAC — the state aircraft maker — expanding its Lingang assembly footprint for the C919 narrow-body. Artificial intelligence labs, hydrogen research facilities, and a new generation of commercial aerospace startups followed.

Second, it changed the deal structure. Traditional industrial parks in China charge rent. Lingang, emboldened by the Special Area mandate, began increasingly bundling land, services, and equity. In other words, tenants could lease land at preferential rates in exchange for granting Lingang investment rights in future funding rounds. This was a quiet but radical change — a shift from landlord economics to venture capitalist economics, with the company's own industrial zone serving as a deal-flow funnel that no other GP in China could replicate.

Third, it unlocked a wave of asset injections from the parent. Between 2019 and 2023, Lingang Holdings absorbed a string of additional properties and platforms from Lingang Group, financed largely through directed share issuances. These included additional industrial plots, logistics parks, and increasingly, stakes in operating companies such as venture capital funds, data center operators, and hydrogen infrastructure platforms. Each injection expanded the scope of the listed company from pure real estate into a multi-segment industrial platform.

Here the question every value investor asks: did Lingang overpay? The honest answer is that this question is almost unanswerable with traditional real estate math. Cap rates on industrial property in comparable Chinese tier-one markets during 2019-2023 hovered in the 5-6% range. The implied yields on some of Lingang's experimental plots — especially those zoned for hard-tech or cross-border data — were notably lower on a pure-rent basis. But the "industrial yield," defined as the total economic capture of the platform including equity gains, service fees, and tax-sharing arrangements, was arguably several multiples higher. Lingang was effectively willing to accept a thin rent coupon if it came with a fat equity kicker.

Compare this to the broader Chinese property sector during the same period. By 2021-2022, the "Three Red Lines" deleveraging campaign had effectively triggered what many observers called a Lehman-scale crisis in Chinese property. Evergrande defaulted. Country Garden wobbled. Even previously rock-solid names like Vanke saw credit spreads widen dramatically. Within the industrial sub-sector, the once-celebrated China Fortune Land Development — a private-sector industrial park developer that had expanded aggressively outside its home market — collapsed under its debt load. By 2021 it was effectively a restructuring story.

Lingang, by contrast, sailed through. Its debt was predominantly onshore, denominated in RMB, and held by policy banks and state-backed financial institutions with long time horizons. Its tenant base skewed heavily toward industrial rather than residential, which meant it was not exposed to the collapse in home-buyer confidence. And critically, its ultimate shareholder — the Shanghai municipal state — had both the balance sheet and the strategic incentive to backstop it if needed. Investors effectively got exposure to a booming industrial thesis without the leverage-related tail risk that was vaporizing returns across the rest of the Chinese property complex.

This is why, by the time one looked at the company on any metric that mattered by 2024-2025, it had become something genuinely distinct from the rest of its peer group. And the architects of that distinction — the management team that translated the policy tailwind into operating results — deserve their own chapter.

IV. Management: The Professional SOE (45:00 – 60:00)

To understand how Lingang runs, you have to first unlearn what you know about Chinese state-owned enterprises. The stereotype — cigarette-stained conference rooms, sclerotic decision-making, executives rotated between chairmanships as a form of political housekeeping — has some truth in certain corners of the SOE universe. It is not, however, what visitors encounter when they walk into Lingang's headquarters tower near the Dishui Lake district.

The dominant impression is of a mid-sized private-equity firm or a top-tier regional bank. Open floor plans. A visible analytics team running dashboards on tenant performance. Investment memos circulating among staff in their thirties. Calendars booked with due-diligence meetings for venture deals. And at the top of it, the current chairman, Weng Kaining, a figure whose public-facing persona sits somewhere between a veteran municipal planner and a specialized infrastructure fund manager.

Weng's biography reads like a study in the grooming of a modern Chinese SOE executive. His career had been spent largely inside the Shanghai industrial-zone ecosystem, with postings across planning, asset management, and investment functions. He was not a political appointee parachuted in from an unrelated ministry. He was, by the standards of Chinese SOE leadership, an insider specialist — someone who had spent years understanding the specific operating logic of industrial parks before being asked to run one.

The management style that has emerged under his tenure and that of his executive peers departs sharply from the old SOE template in three ways.

First is the performance architecture. Lingang management, according to disclosures and investor communications, is evaluated on a matrix of indicators that explicitly includes industrial density (output per square meter of leased land), tax revenue generated per acre of zoned land, and "incubation success" — the rate at which tenants hit development milestones, including IPOs. This is closer to the KPI set of a venture studio or a BRT-style (business resource team) asset manager than to a traditional developer. A Western real estate investor reading this should pause on that word "incubation." It implies that a not-insignificant portion of management compensation is tied to how well their tenants succeed as companies. Lingang is aligned with the upside of its tenants in a way that a standard industrial REIT simply is not.

Second is the service posture. Inside the company, there is a phrase that staff repeat often, and which has shown up in multiple management interviews: the pivot from "renting space" to "providing services." In practice, this manifests as dedicated customer success teams assigned to major tenants, concierge-style regulatory support for foreign firms navigating Special Area rules, in-house legal and tax advisory to help tenants optimize their use of the 15% incentive regime, talent-visa coordination, and even HR support for attracting PhD-level researchers to the district. The closest analog in the Western economy would be something like a Class-A life-sciences campus operator that bundles lab-share, instrument-share, and regulatory help alongside the lease — except that Lingang does it at the scale of an entire industrial ecosystem.

The signature anecdote that captures this mindset, widely recounted by founders who negotiated with Lingang, goes roughly like this. A semiconductor startup founder came in to discuss leasing a plot. He had his rent-per-square-meter offer prepared. The Lingang dealmaker waved away the sheet. "Don't tell us how much rent you can pay," he said. "Tell us how many patents you will file." The story may be apocryphal at the edges, but it captures a real operational reality. Lingang doesn't price its space purely by market rent. It prices by strategic fit, and for the strategically valuable tenants, the "rent" is often partially denominated in promised R&D output, technology transfer, or supply-chain anchoring.

Third is the shareholding and accountability structure. The controlling shareholder remains the Shanghai municipal state, via the Lingang Group parent and associated SASAC-linked entities. As of the most recent disclosures, state-related entities hold the majority of the equity. But the float is genuinely public, and notably, the company has seen rising participation from institutional investors via the Stock Connect programs. Northbound flows — foreign capital investing into mainland stocks through the Hong Kong connect — have periodically represented a non-trivial share of the trading activity, and while those flows have been volatile with geopolitical tides, their sustained presence has had a disciplining effect on the IR function, the English-language disclosure quality, and the company's willingness to engage with international analysts.

None of this makes Lingang a private company. It is decidedly not. When Beijing signals a strategic priority — say, the development of a particular semiconductor process node, or the buildout of hydrogen-refueling corridors — Lingang responds with the kind of speed and capital deployment that no pure private-sector landlord could match. But the crucial point is that the company has absorbed a set of private-sector management practices, KPI frameworks, and incentive structures that allow it to execute those priorities with something close to commercial efficiency. It is, to borrow a term used by one of its own investor day presenters, a "professional SOE."

That professional posture becomes most visible not in the rent roll but in the surprising range of businesses that now sit under the Lingang umbrella — businesses that most investors, at first glance, would never associate with a company officially classified in the real estate sector.

V. The "Hidden" Businesses: Beyond the Warehouse (60:00 – 80:00)

Walk the perimeter of Lingang's core industrial zone today and you see something that, at first glance, resembles any advanced manufacturing cluster — glass-and-steel fabs, logistics yards, ring roads, and the occasional showcase R&D campus. Look closer, and you start to notice things that don't belong in a standard industrial park. A row of hydrogen refueling stations along the trunk road. A low, windowless building ringed by fiber cables and labeled simply "Data Port." An office tower whose signage reads "Lingang Venture." A solar-paneled rooftop extending unbroken for kilometers across warehouse after warehouse.

These are the "hidden" businesses — the parts of Lingang Holdings that don't show up in the consolidated property rent line but that, taken together, are increasingly shaping the long-term earnings profile of the company.

Start with the investment arm. Over the last several years, Lingang has quietly built out one of the more active corporate venture capital platforms in China, concentrated in what the state calls "hard tech" — semiconductors, new energy, advanced materials, hydrogen, AI infrastructure. The structure is typical of industrial-park-linked VC arms: Lingang co-invests alongside state-backed funds such as the National Integrated Circuit Fund (the famous "Big Fund"), municipal innovation funds, and private GPs. Its edge is not capital — there is plenty of capital chasing Chinese hard tech — but rather pipeline. Because Lingang is the physical landlord of hundreds of hard-tech tenants, it has an informational advantage that a purely financial investor can only dream of. It sees which fabs are hitting yield targets before the data hits the market. It sees which AI labs are poaching talent and which ones are losing it. It sees which startups are expanding their cleanroom footprint — the single most reliable leading indicator of a semiconductor company's next revenue inflection.

The investment income from this activity shows up in Lingang's financials primarily as fair value changes in financial instruments and as gains on disposals when portfolio companies IPO or get acquired. In any given year the number can be lumpy. But the cumulative build, especially as more of the Special Area tenant cohort has begun reaching public-market scale on the STAR Board, has become material to the earnings profile. Investors who model Lingang purely as a real estate company tend to underestimate this income stream precisely because it is non-recurring by GAAP definition and therefore often stripped out of core earnings estimates.

Next, the data layer. In 2021, Shanghai formally launched the Lingang International Data Port — an initiative explicitly designed to take advantage of the Special Area's more permissive cross-border data flow policies. In practical terms, this meant designating Lingang as a zone where certain categories of data could move between domestic and international servers under a streamlined regulatory regime, subject to compliance with security reviews. For foreign multinationals operating in China, this is an enormous concession. The standard playbook outside the Special Area requires domestic data localization with onerous export approval processes. Inside, qualifying firms can operate data infrastructure that functions as a bridge between the mainland and international networks.

Lingang Holdings is building and operating physical infrastructure to support this — including bonded data center capacity, high-performance network cabling, and compliance-layer services. In a country where the rest of the technology sector faces ever-tightening data export rules, owning the one legitimate on-ramp is a moat no other mainland developer possesses. It is the closest thing China has to a "free data zone," and it sits on Lingang's ground.

Now layer in the green initiatives. Lingang has aggressively rolled out distributed rooftop solar across its industrial portfolio. Millions of square meters of warehouse roofing owned or controlled by Lingang represents one of the densest solar-deployable surfaces in coastal China, and the economics of rooftop solar — where the tenant factories become both host and captive offtaker — are genuinely attractive. The company has also moved into hydrogen infrastructure, with hydrogen refueling stations serving logistics fleets in and around the port and the airport cargo zones, and partnerships with hydrogen vehicle manufacturers and fuel-cell companies based within the zone. The hydrogen play is still early-stage by any reasonable standard — global hydrogen economics remain challenging — but it gives Lingang credible exposure to what Beijing's 2060 carbon-neutrality pathway has identified as a core technology.

Now the segment breakdown. Lingang's revenue does not cleanly fit into one bucket. Broadly, the company reports revenue across industrial property leasing and sales, park and management services, and investment-related income. The leasing and sales line is the largest and most visible, representing traditional industrial park development revenue. The park services line — which includes property management, utilities, logistics support, and increasingly, digital and regulatory services to tenants — has been the fastest-growing segment on a percentage basis in recent years, consistent with management's "service over space" pivot. And the investment income line, while volatile, periodically contributes meaningfully to the bottom line on years when portfolio company exits cluster.

What this breakdown reveals, if you stand back from the segment labels, is a company that is quietly transforming itself from a property business into something that looks more like a diversified industrial platform — part landlord, part service provider, part investor, part utility operator, part digital infrastructure. Each of these businesses on its own would be a middling operation. Stacked on top of the same tenant base, they compound. Every new tenant who signs a lease is a potential services customer, a potential portfolio investment, a potential solar offtaker, a potential data-port user. The moat is not in any single layer. The moat is in the stacking.

Which means the right framework for understanding Lingang's competitive position is not a conventional real estate analysis. It is, instead, something closer to the kind of power analysis that technology investors have spent the last decade applying to the platform businesses of the digital economy.

VI. Playbook: The Hamilton 7 Powers Analysis (80:00 – 95:00)

Hamilton Helmer's 7 Powers framework was built, famously, to explain why some businesses earn durable, outsized returns while others slip back to the mean. The seven — Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power — are usually mapped onto technology and consumer-facing names. Applying them to a Chinese industrial-park developer sounds, on its face, almost silly. And yet, when you work through the list, Lingang scores on more of them than almost any comparable real estate operator in the world.

Begin with the most concentrated power: Cornered Resource. A cornered resource in the Helmer sense is preferential access to a coveted asset that independently enhances value. Lingang's cornered resource is not simply land — lots of Chinese developers have land. Its cornered resource is a specific geography where the laws of China are literally different. Inside the Lingang Special Area, the corporate tax rate for qualifying industries is 15%, compared to 25% elsewhere. Foreign-exchange rules are more permissive. Data can cross borders. Talent visas are fast-tracked. Bonded customs regimes are streamlined. No other developer on the mainland can offer this bundle, because no other developer controls land inside the Special Area boundary. The sovereign has drawn a line on a map and granted the company inside that line privileges that cannot be arbitraged by a competitor building across the street.

Next, Scale Economies, manifested here as the cluster effect. Semiconductors are the textbook case. A chip designer in Lingang benefits from being within a short drive of its fabricator, its packaging facility, its equipment suppliers, its materials vendors, and the EDA-tool providers who service them. The physical proximity reduces shipping costs, shrinks feedback loops between design and production, and makes it vastly easier to poach — and retain — the specialized engineering talent that concentrates where the cluster concentrates. Once a critical mass of fabs, design houses, packagers, and suppliers have all chosen the same zone, the marginal tenant has an overwhelming economic reason to follow them. The same dynamic applies to electric vehicles, where Tesla's anchor presence has attracted a halo of battery, motor, and software suppliers who now treat Lingang as their default deployment site. And the same to biopharma, where an increasingly complete stack of CROs, CDMOs, regulators, and hospitals has concentrated within the district.

Now Switching Costs. Consider what happens when a tenant — say a gigafactory operator, or a semiconductor fab — has committed to a plot of Lingang land. They have installed clean rooms. They have certified local suppliers. They have trained a workforce of thousands. They have negotiated customized utilities. They have written their multi-year ERP and MES systems to assume a particular port, a particular customs regime, a particular set of Chinese labor and tax rules. Unwinding that to move across provinces is not merely expensive; it is close to impossible without absorbing years of lost production. The gravity of the supply chain, once established, becomes a binding constraint. The economic term is switching cost. The practical term is "you are never leaving."

Process Power is less obvious but arguably real. Lingang has, over two decades, built what is effectively a proprietary playbook for rapidly provisioning industrial sites — from land reclamation to utility hookup to regulatory permitting — at speeds that others simply cannot match. The 168-day Tesla build is the headline, but the same rapid-deployment muscle has been exercised on dozens of other projects. This is organizational knowledge, embedded in teams, workflows, and relationships with municipal authorities. It is hard for a competing zone to copy in the short term because it is not codified anywhere — it lives in people and routines.

Network Economies and Branding are more mixed. Lingang has some weak version of each — its brand among Chinese hard-tech founders is genuinely valuable, and its tenant network creates some "more users, more valuable" dynamics — but neither reaches the strength of the first three powers. Counter-Positioning does not really apply; Lingang is not undercutting incumbents with a novel business model in the way the term is usually used.

But here is where Helmer's framework needs a Chinese-characteristics addendum. Students of Chinese policy economics have increasingly begun to describe an eighth power: the ability to synchronize corporate strategy with national planning. Call it Government Alignment or, in its most developed form, State-Strategic Embeddedness. Lingang has this in an almost unique dose. When Beijing articulates a strategic industry in the Five-Year Plan, Lingang doesn't need to lobby, compete, or bid. The zone is, by design, one of the default landing pads for whatever Beijing has decided matters. When the 14th Five-Year Plan emphasized "indigenous innovation" in semiconductors, Lingang was already receiving fab investments. When hydrogen was elevated as a strategic technology, hydrogen refueling stations were already going up on Lingang's ground. When cross-border data flows became a policy priority, the Data Port was already pilot-operating.

This eighth power has genuine, defensible economic value. It allows Lingang to effectively front-run policy, deploying capital into favored industries before the incentives are fully legislated, capturing first-mover advantages within the zone. And it cuts both ways — it means that when priorities shift, Lingang can also shift faster than pure-commercial peers. A private-sector developer in Suzhou or Hefei, reading the tea leaves of Beijing's planning documents, still has to raise capital, negotiate with municipal officials, secure land, and win permits. Lingang, by contrast, often gets briefed by the same officials designing the plan.

None of these powers are absolute. Every one of them has a stress scenario in which it degrades — geopolitical isolation, a domestic property crisis that forces forced asset sales, a shift in central government priorities away from the Shanghai coastal model. But the stacking of multiple powers, several of them genuinely unique, gives Lingang a competitive position that, in the traditional real estate lexicon, simply does not have a comparable.

And the comparables, when you go looking for them, force you outside the Chinese mainland entirely.

VII. Porter's Five Forces & Competitive Benchmarking (95:00 – 105:00)

The standard Porter's Five Forces analysis gets interesting for Lingang because most of the arrows point in directions that feel counterintuitive for a real estate company.

Bargaining Power of Buyers. On paper, a marquee tenant like Tesla or SMIC holds enormous power. They represent hundreds of thousands of square meters of footprint, thousands of jobs, and magnetism for hundreds of suppliers. Lingang, rationally, is willing to give up enormous concessions to land them — below-market rents, expedited land transfers, tax holidays, preferred utility rates, and equity sweeteners. In the language of retail, these anchor tenants are loss leaders. But the economic mechanic is that these losses get recouped many times over through the hundreds of small and mid-sized suppliers, service providers, and satellite firms who show up in the anchors' wake. These smaller tenants have almost no bargaining power — they are there because Tesla or SMIC is there, and they pay something much closer to full market rates on shorter lease terms. The marginal economics of the platform come almost entirely from the long tail, subsidized by the gravitational pull of the anchors.

Bargaining Power of Suppliers. For a traditional developer, suppliers are contractors, engineering firms, and material providers. For Lingang, the key input is effectively land — land that comes from the municipal government under master-plan arrangements, often via the parent group. Here the "supplier" and the "customer" (the state) are effectively the same entity, which is both a strength (aligned incentives, low friction) and a vulnerability (political pricing risk if priorities shift). In utilities and infrastructure inputs, the company uses a mix of SOE-linked providers and private contractors, with limited individual supplier power.

Threat of New Entrants. Extremely low within the footprint of the Special Area. The geographic and regulatory boundary of the zone is fixed. A competing developer cannot simply buy adjacent land and offer the same regulatory package. The state decides who gets the tax rate, who gets the data port access, who gets the customs regime, and the state has designated Lingang. Outside the Special Area, the threat is higher — other coastal and inland cities have been building their own industrial parks, and some, like Suzhou Industrial Park or Hefei's integrated-circuit cluster, have become genuine alternatives for specific industries. But none offer the full Special Area bundle.

Threat of Substitutes. This is perhaps the most interesting force. The question is: can a company that might otherwise have chosen Lingang instead locate elsewhere — either within China or offshore? Suzhou has a strong biotech and electronics base. Shenzhen has the Qianhai zone and an unmatched consumer-hardware supply chain. Hefei has been the winner in display and specific semiconductor segments. Xiongan, outside Beijing, was the original state-directed new city. Internationally, Vietnam, India, Mexico, and others have courted the same global supply chains that once automatically defaulted to China.

But two things distinguish Lingang's moat against these substitutes. The first is infrastructure — specifically, the combination of the Yangshan deep-water port and Pudong International Airport, both accessible to the Lingang district via the Donghai Bridge in the case of the port and via short-haul ground transport in the case of the airport. Few other Chinese industrial zones can claim similar access to both a top-five-globally container port and a top-five-globally air cargo hub within the same logistics catchment. For industries where export velocity and just-in-time import of advanced components matter, this is genuinely hard to substitute. The second is the sovereign policy package — the 15% tax rate, the data port, the customs regime. No Chinese substitute inland can match the full bundle. The closest peer within China in terms of regulatory experimentation is Hainan Free Trade Port, which has a different industrial focus (consumer goods, tourism, services rather than advanced manufacturing).

Rivalry Among Existing Competitors. This looks different from typical industrial-park rivalry because Lingang, within its Special Area footprint, has no true existing competitor. Outside the footprint, it competes as one industrial developer among many — a serious player but not dominant. The mental model is closer to a monopolist on its home turf competing with a broader field on road games.

Which brings us to the international benchmarking. If Lingang is not really a normal Chinese developer, what is it most comparable to? Two names come up repeatedly in analyst work on the company.

Singapore's JTC Corporation is the spiritual antecedent. JTC was founded in the 1960s to turn Jurong into a petrochemical hub, and in the decades since has evolved into the master-developer of Singapore's industrial real estate, operating as a statutory board with a government mandate and commercial discipline. Lingang was explicitly modeled on JTC's template, and the operational similarities are obvious — a single state-backed entity that master-plans, builds, and operates industrial land, bundling policy, infrastructure, and services. The key difference is scale and industrial mix. JTC's portfolio is national-Singapore scale; Lingang's is Special Area scale but embedded in the much larger Chinese manufacturing economy. The industrial mix has also diverged, with JTC historically weighted toward chemicals and precision engineering while Lingang has moved aggressively into EVs, semiconductors, biopharma, and data.

Dubai's DP World is the second comparison, though it is imperfect. DP World is primarily a port operator with industrial zone adjacency (JAFZA), whereas Lingang is primarily an industrial zone operator with port adjacency. Still, the integrated logistics-plus-zone business model shares structural DNA, and both have benefited from sovereign support as strategic national champions.

The honest assessment is that Lingang is arguably the most scaled version of this template globally — in part because it sits on top of the Chinese manufacturing base, which remains the largest in the world. Whether it is the most efficient "Industrial OS" in the world is a harder claim to validate, given the difficulty of comparing gross metrics across different regulatory and cost structures. But on the measures that matter — time-to-deploy, tenant mix quality, and policy flexibility — it is at or near the global frontier.

That frontier position, however, does not make the investment case a slam dunk. And any serious analysis has to sit with the bear side of the argument as seriously as the bull.

VIII. Bear vs. Bull Case (105:00 – 112:00)

Start with the bear case, because it is the one investors underweight.

The first and most structural bear concern is geopolitical exposure. Lingang's entire thesis depends on China remaining integrated enough with global capital flows, technology partnerships, and supply chains for the Special Area to be a useful bridge. If the trajectory of U.S.-China decoupling accelerates — and by 2026 there has been no shortage of signals pointing in that direction, from semiconductor export controls to investment-screening regimes to tariff escalations — the class of tenants that Lingang most values (foreign multinationals seeking China onshoring, Chinese firms seeking international access) could shrink. A world in which Western companies are affirmatively discouraged or prohibited from operating advanced manufacturing in Special Areas would not destroy Lingang's business, but it would meaningfully alter its highest-margin segments.

Specifically, the Data Port initiative is exquisitely exposed to geopolitical swings. Cross-border data flow is already one of the most politically charged corners of the U.S.-China relationship. If either side further restricts data movement, the Data Port's value proposition erodes. The regulatory permission granted by Beijing is effectively worthless if Western regulators counter with their own blocks.

The second bear concern is the Chinese property overhang. Although Lingang has been insulated so far by its industrial focus and state-backed balance sheet, it is not entirely divorced from the broader real estate cycle. A prolonged downturn in Chinese industrial demand — say, from a hard landing in domestic consumption or a global manufacturing recession — would pressure rents and occupancy even in premium zones. The industrial segment has been the last domino to fall in the Chinese property deleveraging; the question is whether it ever falls at all, and if so, how Lingang's rent roll holds up under stress.

The third is interest rates and asset intensity. Industrial park development is capital-intensive. Lingang holds billions of yuan in investment properties on its balance sheet, financed through a mix of policy-bank loans, corporate bonds, and equity. In a rising-rate environment — and Chinese rates have been anomalously low by global standards but are not immune to change — the weighted average cost of capital on the portfolio rises, and fair-value marks on investment properties can compress. The asset-heavy nature of the business means that any incremental growth requires incremental capital, which means either dilution, leverage, or slower growth.

The fourth, more qualitative concern is dependence on state signaling. Lingang's success is tightly coupled to sustained central government support for the Special Area model. That support has been robust through 2026. But political priorities evolve, and a reallocation of focus — say, toward a different coastal node, or toward inland-first industrial strategy — could dull the relative advantage. This is the classic risk of being too aligned with any single sovereign narrative.

Now the bull case, which is in some ways the mirror image.

The primary bull thesis is that Lingang is not, in its essence, a real estate company at all. It is a toll booth on the most productive industrial land in the world. Every Tesla delivered out of the Shanghai gigafactory, every chip fabricated at a Lingang-based fab, every biologic manufactured at a Lingang CDMO generates some economic output that, through rent, services, tax-sharing arrangements, utilities, data infrastructure, or equity interests, flows back in some form to Lingang's platform. As the industrial base within the Special Area expands and matures, the toll booth revenue compounds mechanically, with relatively little incremental capital required once the underlying infrastructure is built.

The second bull argument is the hidden equity portfolio. Lingang's accumulated venture investments across its tenant base — semiconductors, AI, hydrogen, biopharma — sit on the balance sheet at cost or fair-value marks that, in many cases, substantially understate the economic reality. As the STAR Board and Hong Kong connect IPO markets have matured, and as a new cohort of Lingang-incubated companies has approached public listing, the realization events on these portfolio stakes have, on select years, meaningfully added to earnings. The long-tail value of this portfolio, if Beijing's hard-tech ambitions play out, could be several multiples of the current visible mark.

The third bull argument is the Singapore-of-China analogy. Over decades, Singapore's GDP per capita grew not because Singapore had special natural resources but because it had a sovereign commitment to industrial sophistication, efficient regulation, and selective openness. Lingang, as a zone, is a conscious attempt to replicate that trajectory in microcosm. If the experiment succeeds on the scale that Beijing clearly intends, the company behind the ground will compound in a way more reminiscent of a sovereign wealth platform than a normal listed developer.

Synthesizing bull and bear, the investor's real question is not whether Lingang's business is high-quality — on most measures, it is. The real question is about the path dependency of Chinese policy and geopolitics over the next five to ten years. In a benign scenario, where China remains engaged with global capital and technology flows while continuing its industrial upgrading, Lingang is arguably one of the most attractive platform-economy businesses in emerging markets. In an adverse scenario — severe decoupling, sanctions targeting specific Chinese industrial zones, a domestic credit event that spreads into industrial property — the business remains solvent, thanks to state backing, but compounds far more slowly.

This is why, for an investor watching this name, the most useful practice is not to forecast every line item but to track a very small number of signals that actually move the underlying thesis. And here the KPIs genuinely narrow to a short list.

The first is industrial density — effectively, how much industrial output, tax revenue, or employment Lingang's zone generates per square meter of developed land. This is the best single measure of whether the "service over space" pivot is working. A company compounding on density is compounding on ability to attract and retain higher-quality tenants, which is the core of the thesis. The second is occupancy and rent trajectory across the industrial park segment, the most traditional property metric, which remains essential as a sanity check on the base business. The third is investment income realizations from the venture portfolio, especially the frequency and scale of IPO-related exits among Lingang-incubated tenants — a leading indicator of whether the equity flywheel is actually producing harvestable returns at scale. Everything else is noise around these three.

IX. Conclusion & Final Thought (112:00 – 115:00)

Zoom out. The coastline south of Shanghai, in satellite photos from 2015, looked like a half-drawn sketch — roads ending in silt, warehouses scattered across muddy fields, the thin grey line of the Donghai Bridge reaching out over empty water toward the faint silhouette of Yangshan. In photos from 2026, the same coastline looks like someone turned on "infinite money" in a city-builder game. Gleaming fabs. Aircraft assembly hangars. Data center complexes throwing off visible heat signatures in infrared. Hydrogen stations along the trunk roads. The Dishui Lake district with its arcing waterfront. A Tesla gigafactory running three shifts. Supplier clusters radiating outward in concentric rings.

Somewhere in the middle of all this — on a balance sheet listed under ticker 600848 — sits the company that, quietly and without the name recognition of its flagship tenants, curated the entire project. Lingang Holdings is the physical manifestation of what Beijing calls its "dual circulation" strategy — the attempt to build an economy that is simultaneously deeply integrated with global supply chains and strategically self-sufficient in critical technologies. It is the landlord of that ambition, the service provider, the investor, the utility, the data broker, and the silent equity partner in hundreds of its tenants' journeys.

To understand the future of Chinese manufacturing, one has to understand the companies building the hardware — Tesla, SMIC, COMAC, and their peers. But to understand why all those companies found themselves in the same muddy field south of Shanghai on the same timeline, you have to understand the ground underneath them. And to understand the ground, you have to understand the company that built it, stitched it to a sovereign policy package, and turned it into a platform.

The final thought, for any investor thinking about what kind of business they are looking at, comes back to the 2019 image. Elon Musk, dancing in the mud. One hundred and sixty-eight working days. A scene that almost no other economy on earth could have produced, engineered by a listed state-owned developer most of the world had never heard of. That was not a miracle. It was a platform, executing its function, in real time, in public, for anyone patient enough to see it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube