The Japan Steel Works, Ltd.: The Metallurgy of Modern Choke Points

I. Introduction & The Strategic Paradox

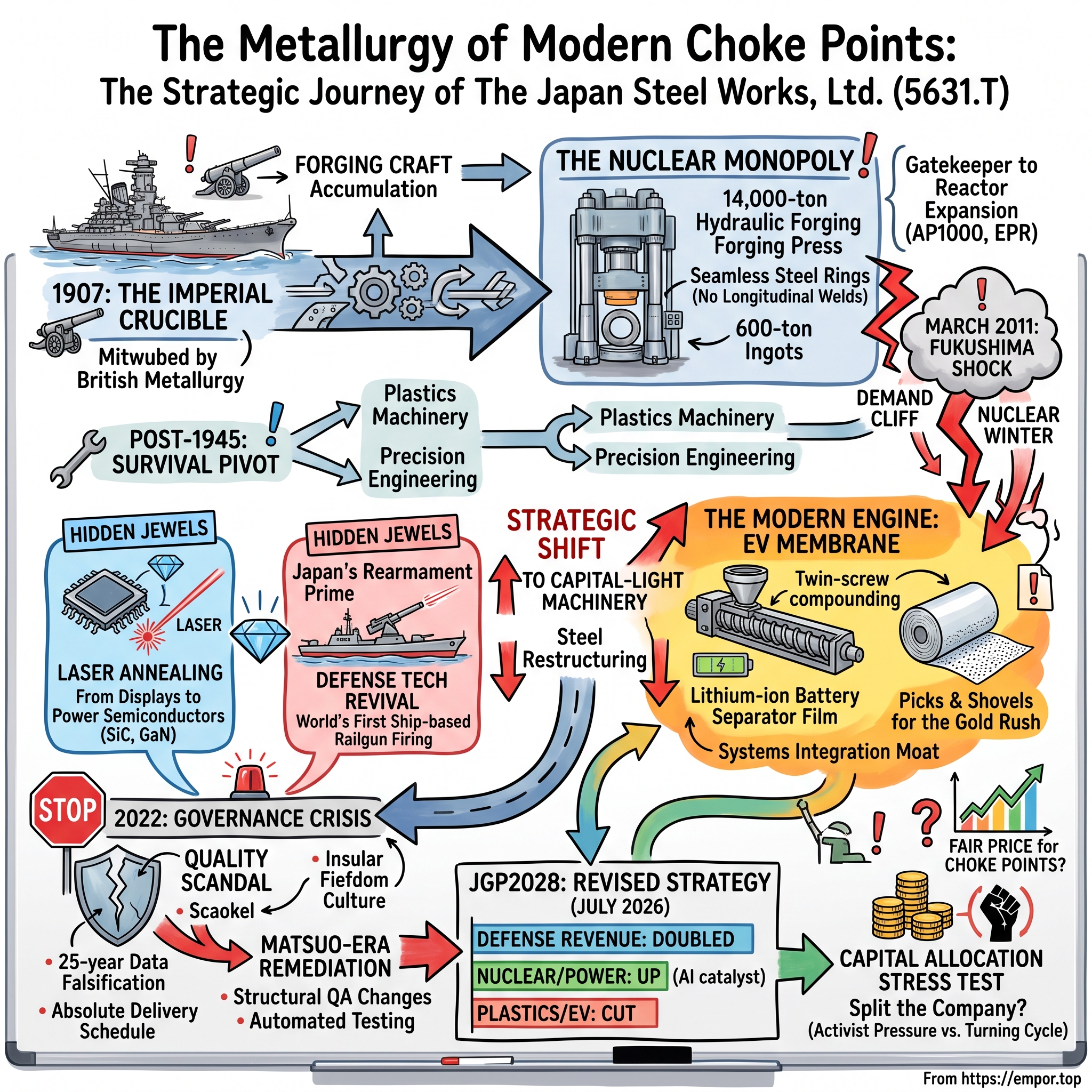

Start with a single, almost absurd sentence, and let it sit for a moment. The same company that forged the 46-centimeter main gun barrels for the battleship 戦艦大和 Yamato — the largest naval guns ever mounted on a warship — is today the world's leading supplier of the machines that manufacture the wafer-thin plastic membrane inside your electric vehicle's battery. Between those two facts lies more than a century of Japanese industrial history, two lost wars, a nuclear renaissance, a nuclear winter, a corporate fraud that reached back a quarter of a century, and a live-fire railgun test on the open ocean.

株式会社日本製鋼所 The Japan Steel Works, Ltd. — trading in Tokyo as 5631.T on the Prime Market of the 東京証券取引所 Tokyo Stock Exchange — is not a large company by the standards of Japanese industry. It reported consolidated net sales of ¥274.9 billion for the fiscal year ended March 31, 2026, roughly $1.8 billion, with operating profit of ¥25.3 billion.[^1] Toyota does that much revenue in a bad long weekend. And yet JSW sits astride several of the most unforgiving choke points in the modern industrial economy — the kind of narrow passes where, if the company stumbled, entire downstream industries would feel it.

Consider the three of them, because they are the spine of this whole story.

The first is the nuclear foundry. At its 室蘭製作所 Muroran Plant in Hokkaido, JSW operates a colossal 14,000-ton hydraulic forging press capable of shaping a single, seamless steel ring — the pressure-vessel section of a nuclear reactor — from a 600-ton ingot, with no longitudinal weld seams anywhere in the wall. For decades it was the only facility on Earth that could do this at scale, and the World Nuclear Association still describes Muroran as holding a unique global position in ultra-heavy nuclear forgings.[^9]

The second is the EV membrane. JSW is, by its own account and by most industry estimates, the global leader in the 二軸混練押出機 twin-screw compounding extruders and film-stretching lines used to manufacture リチウムイオン電池セパレータ lithium-ion battery separator film — the porous plastic sheet that keeps a battery cell from short-circuiting into a fire.[^6]

The third is the rearmament prime. JSW is Japan's sole domestic manufacturer of large-caliber gun barrels and tank cannons, and in October 2023 it was the industrial hand behind the world's first firing of an electromagnetic railgun from a ship at sea.3

How does one modestly sized engineering company end up holding all three? The honest answer — the thread we will pull for the rest of this article — is that JSW never really sold products. It sold process: the accumulated, hard-won, decades-deep ability to manipulate metal and polymer under extreme pressure, temperature, and precision. Guns, reactors, plastic extruders, and semiconductor lasers are just different customers for the same underlying craft. A company that grasps this about itself can survive the death of its core business not once but twice, because the craft outlives the object it happens to be applied to. That is the quiet superpower running underneath a hundred and nineteen years of Japanese industrial history.

There is a reason this matters for how you should read the numbers. JSW is a company where the income statement badly understates the strategic position. A $1.8 billion revenue base looks like a mid-cap regional industrial; the choke points it controls look like something an antitrust lawyer would flag. The gap between those two pictures — small financials, outsized strategic footprint — is exactly the space in which both the bull case and the bear case live, and it is why the stock has been such a puzzle for investors to price.

But this is not a hagiography, and JSW is not a company you can admire uncritically. The same metallurgical mastery that built the moats also bred an insular factory culture that, in 2022, was revealed to have been falsifying quality-inspection data for roughly a quarter of a century — including on nuclear and defense components. The same asset-heavy legacy that anchors the story is why the stock has spent years trading at a conglomerate discount, drawing the attention of a Tokyo market regulator and a rising tide of Japanese shareholder activism. This is a story of extraordinary industrial capability shadowed by governance failure and capital-allocation questions that remain, in 2026, unresolved.

Here, then, is the roadmap for the episode. We will trace JSW from an imperial weapons works midwifed by British arms makers, through the improbable civilian monopoly it built in nuclear forgings, into the near-death experience of the post-Fukushima "nuclear winter" and the frantic pivot to capital-light machinery. We will sit inside the twin-screw extruder and the battery separator line that became the company's new engine, tour the two hidden jewels of laser annealing and railgun defense, and then confront the 2022 quality scandal that nearly poisoned the well of trust the whole enterprise drinks from. Finally we will put the capital allocation and the activist pressure through a hard, skeptical stress test — because the most interesting thing about JSW in 2026 is not what it makes, but whether the market will ever pay a fair price for it.

So let us go back to where the metal was first poured — in the twilight of the samurai era, with British warship-builders as midwives.

II. The Imperial Crucible: Battleships and British Metallurgy

In 1907, Japan was a nation in a hurry and afraid of being late. It had shocked the world two years earlier by destroying the Russian fleet at Tsushima, but the humiliating truth inside that victory was that many of its best warships had been built in British yards. A rising empire that had to import its battleships did not control its own destiny — and the men running Meiji-era Japan understood this with the particular intensity of people who remembered when Commodore Perry's black ships had forced the country open.

The answer, incorporated on November 1, 1907, was a joint venture of a distinctly turn-of-the-century kind: Japanese capital married to British arms expertise. The 三井グループ Mitsui Group, through its Hokkaido Colliery & Steamship arm, joined forces with two of Britain's great defense conglomerates — Sir W.G. Armstrong, Whitworth & Co. and Vickers, Sons & Maxim — to create The Japan Steel Works. The logic was elegant. Mitsui brought coal, capital, and a Hokkaido industrial base; the British brought the metallurgical know-how to forge gun barrels and armor plate that Japan could not yet make itself. It was technology transfer at the barrel of a naval cannon, and it was precisely how a follower nation escaped dependency.

There is a subtlety worth pausing on, because it explains the DNA of the whole company. Armstrong Whitworth and Vickers were not passive financial investors; they were the two firms that, along with a handful of German houses, defined the state of the art in naval ordnance and armor. When they took equity in a Japanese venture and seconded their metallurgical methods, they were transferring the single hardest-to-copy body of knowledge in early-twentieth-century heavy industry — how to make steel that survives the physics of a naval gun. Japan had cheap labor and coal; what it lacked was exactly this tacit craft. The 1907 structure was, in effect, a licensing deal denominated in know-how rather than royalties, and JSW spent its first decades absorbing that knowledge until it no longer needed the teachers. The teachers, for their part, got a foothold in a fast-arming Pacific customer. Both sides understood the bargain.

The location mattered as much as the partners. The founders anchored the enterprise at Muroran, a deepwater port on Hokkaido's southern coast, close to coal fields and iron sand and blessed with a harbor deep enough to float out the heaviest finished forgings. That choice — proximity to raw material, deepwater logistics, room to build ever-larger presses — would compound for the next hundred years. A modern forged reactor component can weigh hundreds of tons; you cannot truck it down a mountain road. It has to be born beside deep water and lifted onto a ship. Muroran, chosen in 1907 for battleship logistics, turned out to be the ideal cradle for nuclear forgings sixty years later — a piece of pure path dependence that no competitor could retroactively acquire. Muroran was not just a factory; it was the physical embodiment of a capability that could not be relocated on a spreadsheet.

For the first four decades, JSW's customer was the Imperial Japanese Navy, and its craft climbed toward a terrible apex. The company forged heavy armor plate and the enormous gun barrels for Japan's capital ships, culminating in the 46cm main guns of the Yamato and 戦艦武蔵 Musashi — 18.1-inch weapons firing shells that weighed more than a small car, mounted on the largest battleships ever built. To make such a barrel is to solve a metallurgical problem of the first order: a tube of steel that must contain a controlled explosion, thousands of times, without fatiguing, cracking, or drifting out of tolerance. The skill required to do that reliably is not a blueprint you can photocopy. It lives in the hands and judgment of master forge operators, and it accumulates slowly.

It is worth naming what that craft actually is, because the same word recurs through every later chapter: forging. Casting is pouring molten metal into a mold and letting it freeze; forging is taking solid, glowing-hot metal and pounding or pressing it into shape while it is plastic. Forging aligns the internal grain of the steel, closes microscopic voids, and produces a part far stronger and more uniform than a casting of the same alloy — which is exactly why the most safety-critical components in the world, from crankshafts to reactor vessels to gun barrels, are forged rather than cast. To forge a giant part well is to control temperature, force, and timing across a mass of metal that behaves differently at its core than at its surface. JSW's founders bought that discipline from the British; its workers spent a century deepening it.

Then, in 1945, the customer vanished and the mission was outlawed. Under the Allied Occupation, Japan's military manufacturing was banned outright, and a company built to arm a navy that no longer existed faced a stark choice: liquidate, or find something else to forge. This was the existential crisis that, in retrospect, taught JSW its founding lesson about reinvention — the first of two times the ground would fall away beneath it. Management chose to survive by redirecting the one asset the occupation could not confiscate — the metallurgical craft itself. If JSW could forge a gun barrel that withstood the pressures of firing, it could forge steel for the peaceful machines of a rebuilding industrial economy: rolling-mill rolls, ship components, power-plant rotors, chemical-plant vessels. In the postwar decades it also branched, almost improbably, into machinery — building on the precision-engineering habits of the ordnance shop to make plastics-processing equipment, a seed that would flower into the company's modern core. The pivot from ordnance to industry was not a marketing decision. It was a survival reflex, and it planted the seed of everything that came after. The question was what peacetime application would demand the very heaviest, most exacting forgings — the ones only Muroran's presses could make. In the 1960s, the answer arrived, and it glowed.

III. The Nuclear Monopoly: The 14,000-Ton Forging Press

Here is the engineering problem that made JSW indispensable, and it is worth slowing down to feel its weight, because the entire nuclear moat rests on it.

A nuclear reactor pressure vessel is, in essence, a giant steel thermos — a thick-walled cylinder that holds the radioactive core, the coolant, and enormous pressure and heat, for sixty years, while being continuously bombarded by neutrons. Over decades, that neutron radiation makes steel brittle, a slow poisoning called embrittlement. And the most vulnerable place in any welded steel structure is the weld itself — the seam where two plates are joined. A traditional pressure vessel is rolled from flat plate and welded up the side with long vertical seams, and every one of those longitudinal welds is a potential crack initiation point degrading year after year under radiation.

JSW's answer was audacious in its simplicity: don't have a seam. Forge the entire cylindrical wall of the reactor vessel as one continuous, seamless steel ring, so there is no longitudinal weld to embrittle in the first place. It is the difference between a barrel made of staves and a barrel carved from a single block of oak — one has joints that can fail, the other does not.

To do that, you need to take a steel ingot the size of a small house — up to 600 tons — heat it to roughly 1,200°C until it glows a workable orange, and then squeeze it into shape with a press exerting thousands of tons of force. JSW built exactly such a machine at Muroran: a 14,000-ton hydraulic forging press, one of the largest on the planet, fed by ingots that only a handful of foundries in the world could even cast cleanly at that size.[^9] The economic point is subtle but decisive. The barrier here is not merely the press — capital, in the end, can buy a press. The barrier is the tacit knowledge wrapped around it. A 600-ton ingot does not deform predictably; it has internal segregation, thermal gradients, a personality. Training a master forge operator who can read the steel's resistance through the hydraulic controls — who knows by feel when to press and when to wait — takes years, and it cannot be downloaded. This is what the strategist Hamilton Helmer would call a cornered resource: a uniquely valuable asset, in this case a fusion of scale and human craft, that rivals cannot readily replicate.

There is a second, even scarcer input hiding inside this story: the ingot itself. Before you can forge a 600-ton seamless ring you must first cast a clean ingot of that size — and casting steel at that scale without ruinous internal segregation, where heavier elements sink and lighter ones float as the mass slowly solidifies over days, is its own black art. JSW poured these giants in-house, controlling the whole chain from molten steel to finished forging. Vertical integration here was not a strategy-deck buzzword; it was a physical necessity, because no merchant supplier could hand you a flawless 600-ton ingot on demand. Each link in the chain — clean melt, sound ingot, skilled forging, precise heat treatment, exhaustive inspection — was a place a rival could fail, and JSW had spent decades not failing at any of them.

For decades, no competitor could match it. France's Framatome, South Korea's 두산 Doosan, and China's 中国一重 China First Heavy Industries could forge nuclear components, but not single-piece ultra-heavy rings at Muroran's scale and quality — and so the whole world's ambition to build large reactors ran, at least partly, through a single plant in Hokkaido. At the peak of the 2000s "nuclear renaissance," when utilities from the United States to China were planning fleets of new reactors, JSW's order book for ultra-heavy forgings stretched out roughly five years. Customers did not negotiate on price so much as queue for a slot; the company supplied components destined for Westinghouse's AP1000 and Areva's EPR reactor designs, and its historical share of the largest reactor forgings was often cited near 80%.

Sit with the economics of that position for a moment, because it is genuinely rare. When a customer must wait five years for your product, you have priced very differently than a company competing for next quarter's order. A slot in Muroran's queue was itself a scarce, tradable asset — utilities reserved capacity years ahead of pouring concrete on a reactor site, because losing the slot meant losing the reactor's schedule. That is pricing power in its purest form: the supplier sets terms, and the customer's alternative is not a cheaper rival but no reactor at all. For a window in the mid-2000s, JSW arguably held one of the most enviable single-asset monopolies in all of heavy industry. The tragedy — and the lesson — is how completely that windfall depended on a single downstream industry continuing to believe in its own future.

Think about what that meant strategically. JSW had become a gatekeeper to the physical expansion of nuclear power worldwide — a tollbooth on an industry measured in the trillions. It was, on paper, one of the most enviable competitive positions in global heavy industry: a genuine near-monopoly on an irreplaceable input, protected by physics, capital, and craft all at once. The trouble with being the single indispensable supplier to one industry, of course, is that your fortunes are welded to that industry's fate. And on an afternoon in March 2011, that fate cracked open off the coast of northeastern Japan.

IV. The Fukushima Shock & The Decadelong Nuclear Winter

At 2:46 p.m. on March 11, 2011, the seafloor off Tōhoku lurched, and a magnitude-9.0 earthquake sent a tsunami over the seawalls of the Fukushima Daiichi nuclear plant. The meltdowns that followed did not just devastate a stretch of Japanese coastline; they detonated the global business case that JSW had spent half a century building. Within days, the psychology of an entire industry inverted. Nuclear power went, in the public mind of much of the developed world, from the clean-energy future to an unacceptable risk — and the order book that had stretched five years into the future began, in slow motion, to evaporate.

The numbers behind the collapse were brutal in their logic. Japan progressively idled all of its commercial reactors for safety review. Germany announced an accelerated exit from nuclear power entirely. Utilities everywhere froze or cancelled new-build plans. For JSW, whose Steel and Engineering segment had been tooled and staffed for a high-volume future of ultra-heavy nuclear and thermal-power forgings, this was the worst kind of shock: a demand cliff hitting a fixed-cost, capital-intensive business. A forging press does not care whether it is busy; its depreciation and its maintenance and its skilled workforce cost roughly the same whether the order book is full or empty. When volume fell, that fixed-cost base flipped from an advantage into structural losses, asset write-downs, and painful restructuring of the Muroran workforce.

This is the first and most important investing lesson buried in JSW's history, and it is worth stating plainly: a cornered resource is a double-edged sword. The very concentration that made JSW indispensable to nuclear power made it hostage to a single, systemic, unforecastable industry shock. A moat around one castle is worthless if the entire kingdom is abandoned.

There is a psychological dimension to this collapse that investors underrate. For a proud engineering organization, the Fukushima shock was not only a financial event; it was an identity crisis. Muroran had spent half a century believing it was the indispensable heart of the company — the crown jewel, the reason JSW mattered on the world stage. Suddenly its order book was hollowing out and head office was talking about downsizing the very furnaces that had defined the firm's self-image. That kind of internal wound matters, because as we will see, the insular, defensive, "the schedule is sacred" culture that eventually produced a quality scandal grew in a division under existential pressure, told for a decade that it was a shrinking legacy problem to be managed rather than a jewel to be protected. Strategy and culture are not separate stories here; they are the same story.

Management's response was to shift the company's economic center of gravity away from heavy steel and toward capital-light machinery — a business where the value is in engineering and controls rather than in tons of forged metal and giant presses. The distinction is fundamental to how an investor should value JSW. A forging business consumes enormous capital, carries heavy fixed costs, and swings violently with the industrial cycle; a machinery business sells engineered systems, ties up far less capital per yen of revenue, and can grow by winning designs rather than by pouring more steel. Shifting weight from the former to the latter is, in effect, an attempt to raise the entire company's return on capital and to dampen its cyclicality — the two things the market punishes JSW for lacking.

Two moves defined the pivot. In 2008, JSW had formed a capital alliance with the plastics-molding-machine maker 株式会社名機製作所 Meiki Co., Ltd.; in 2020, it fully merged Meiki in, deepening its injection-molding portfolio. And in 2015, it acquired South Korea's SM Platek to reach mid-market twin-screw extruder demand across broader Asia. Neither deal was enormous, but together they signaled the direction: build out the machinery businesses that could grow without a 14,000-ton press attached. Read as capital allocation, these were sensible, disciplined, un-flashy bolt-ons — the opposite of the trophy acquisitions Japanese industrials sometimes make to look busy. They bought capability and market access in the segment JSW wanted to grow, at prices that never threatened the balance sheet.

The result, over the following decade, was a reweighting of the whole company. The Industrial Machinery Products business — extruders, molding machines, film lines, lasers — grew to drive the clear majority of group revenue, while the legacy Steel and Engineering division was downsized, rationalized, and reframed. It was no longer the engine. It became something closer to a long-dated option: a business kept alive and clean, waiting for the possibility that energy security and climate policy might one day revive demand for exactly the heavy forgings the world had just walked away from. Whether that option ever pays off is a live question we will return to. But first, we need to understand the business that actually became the engine — the unglamorous, deeply strategic world of industrial plastics.

V. The Modern Engine: Plastics Compounding and the EV Boom

Say the words "plastics machinery" to an investor and watch their eyes glaze. That reflex is exactly why JSW's core business is so poorly understood — and, arguably, so persistently underpriced. Because what happens inside a modern twin-screw compounding extruder is not the crude melting of plastic pellets. It is closer to precision cooking at industrial scale, and it sits at the heart of some of the most demanding materials in the economy.

Picture two intermeshing screws, turning inside a heated barrel, each zone held to an exact temperature and shear profile. Into that barrel you feed a base polymer plus a recipe of additives — reinforcing glass fibers, flame retardants, colorants, stabilizers, conductive fillers. The screws knead the mixture with just enough energy to disperse everything uniformly without degrading the polymer, and out the other end comes a compounded resin with engineered properties: a plastic strong enough for a car bumper, or heat-resistant enough for an engine bay, or biodegradable, or electrically conductive. Get the shear and temperature slightly wrong and you have ruined an expensive batch. JSW's TEX series of twin-screw extruders is widely regarded across the chemical industry as a gold-standard machine for exactly this reason: it is the difference between a chef's knife and a butter knife. Industry estimates put JSW's share of the high-performance end of this market at roughly 40%.[^6]

The separator: the most critical plastic you have never heard of

Then the electric-vehicle era arrived and handed JSW a second, faster-growing use for the same core competence: the separator film.

The separator is the least glamorous and most quietly critical component in a lithium-ion battery. It is an ultra-thin porous plastic membrane — often thinner than five microns, a fraction of a human hair — that sits between the anode and the cathode inside every cell. Its job is a paradox: it must be porous enough to let lithium ions pass freely through it (or the battery won't work), yet mechanically strong and thermally stable enough to keep the two electrodes from ever touching (or the battery shorts, overheats, and can catch fire). Manufacturing that membrane at scale, at consistent sub-five-micron thickness, at high yield, is a genuinely hard problem in polymer processing — and JSW builds the extrusion-and-stretching lines that do it. The company reported in 2021 that it was expanding extruder capacity specifically to meet surging demand for battery-separator equipment, and it has consistently claimed the leading global share in these high-volume separator lines.[^6]

It helps to understand how a separator is actually made, because the process is where JSW's edge lives. There are two broad routes — "wet" and "dry" — but both hinge on the same trick: you extrude a polymer film and then stretch it, biaxially, pulling it in two directions at once so that it thins out and develops a controlled network of microscopic pores. Control the polymer melt, the extrusion, the stretching ratio, and the temperature profile, and you get a membrane that is uniformly porous, uniformly strong, and uniformly thin across a roll that may be kilometers long. Lose control for a fraction of a second and you get a pinhole — and a pinhole in a battery separator is a latent fire. The machine that must never let that happen is precisely a high-precision extrusion-and-stretching line, and building the best of those is the same discipline as building the best compounding extruder. This is why JSW could walk into a brand-new industry and lead it: it was not learning a new business, it was applying an old mastery to a new film.

Here is the strategic elegance, and it echoes the whole JSW story: the separator business is the plastics-extrusion craft pointed at a new megatrend. The same mastery of shear, temperature, and film uniformity that makes a good engineering resin makes a good battery membrane. The customer changed from a chemical company to a battery-materials company; the underlying process IP did not. And the demand behind it is enormous in scale — every EV battery, every grid-storage installation, every laptop and phone contains separator film, and the megatrend of electrification means the world needs vastly more of it each year. JSW does not sell batteries or even separators; it sells the picks and shovels that make the separators, which is historically one of the more attractive places to stand in a gold rush.

Who does JSW fight for this? The competitive set is real and capable. Germany's Coperion, now owned by the U.S. group Hillenbrand, and the German precision-extruder maker Leistritz compete hard in compounding; domestically, 住友重機械工業 Sumitomo Heavy Industries and others contest parts of the machinery market. JSW's claimed edge is not any single component but systems integration and scale: it does not merely sell an extruder, it designs, builds, and controls the entire multi-story automated production line, tuned end-to-end. For a separator maker such as 旭化成 Asahi Kasei or China's Senior, that integration is the switching cost — once your whole line, its control software, and your process recipes are built around a JSW system, ripping it out for a rival is expensive and risky.

There is also a competitive threat worth naming that JSW's marketing will not: China. Chinese machinery makers have moved up the value chain in separator and extrusion equipment, and they compete on price with a domestic battery industry that is itself the largest in the world. JSW's defense is quality, precision, and the switching cost of an installed integrated line — but that is a defense, not an impregnable wall, and the margin trajectory of the machinery segment is the number that will reveal whether the wall is holding. If a JSW extruder commands a durable price premium over a competent Chinese line, the moat is real; if the premium erodes, the business drifts toward commodity economics no matter how sophisticated the engineering.

The honest analytical caveat is that "leading global share" in separator equipment is largely a company-reported claim, hard for an outside investor to independently audit, and the separator market itself has cooled with the broader EV slowdown — a vulnerability the company itself acknowledged in 2026, as we will see, by cutting its own plastics-machinery target. What is not in doubt is that industrial machinery, not steel, is now the profit engine of this company, generating the clear majority of both revenue and operating profit.[^2] And within that engine sit two smaller businesses that may matter more to the next decade than their current revenue suggests.

VI. The Hidden Jewels: Laser Annealing and Defense Tech

Every diversified engineering company has a drawer of technologies that look like footnotes until, one day, they don't. JSW has two, and both trace — of course — back to the same theme of process mastery applied to a new frontier.

The first is light. For years JSW has been a quiet leader in excimer laser annealing, or ELA — a technology developed to make high-end smartphone displays. The problem ELA solves is this: to build the fast, high-quality transistors that drive an OLED screen, you need the silicon film on the glass to be crystalline rather than amorphous, but you cannot simply bake the whole panel because the glass would melt. ELA fires precisely shaped ultraviolet laser pulses that melt and recrystallize a whisker-thin surface layer of silicon in nanoseconds, leaving the substrate cool. It is surgical heating with light. JSW's machines became essential kit for premium display fabs.

The strategically interesting move is that JSW is repointing that same laser-annealing craft at power semiconductors — the silicon carbide (SiC) and gallium nitride (GaN) chips that manage electricity in EV inverters, fast chargers, and industrial power grids. These wide-bandgap materials handle high voltages and high temperatures far more efficiently than ordinary silicon, wasting less energy as heat, which is why they are becoming the beating heart of electrified everything. Their manufacture, however, is finicky — and one persistent problem is activating dopants and repairing crystal damage in the wafer without heating the whole thing to temperatures that would wreck it. Localized laser annealing, firing precisely dosed pulses at just the surface, is one of the ways to do it, and it is exactly the craft JSW spent years perfecting for displays. This is a premium, supply-constrained, high-margin niche in the semiconductor supply chain, and it is a genuinely credible adjacency — the same "process, not product" logic that carried JSW from gun barrels to reactors applies here in miniature. The caveat for investors is proportionality: it remains a small contributor today, an option on a trend rather than a proven profit center, and JSW competes against far larger semiconductor-equipment specialists with deeper customer relationships. It belongs on the watch list, not yet in the valuation — and management, to its credit, presents it that way rather than inflating it into a headline.

Here a useful myth-versus-reality check is in order, because outsiders routinely misfile JSW. The consensus caricature is "a Japanese steelmaker" — a sleepy, cyclical, commodity metals-basher. The reality is nearly the inverse: the majority of revenue and profit comes from precision machinery, lasers, and electronics-adjacent equipment, and the "steel" division is now the smaller, optional part of the company. Investors who anchor on the word "steel" in the name — and on the low-multiple mental model that word triggers — are pricing a company that no longer exists. That mispricing is either the opportunity or the trap, depending on whether you believe the machinery moat is durable and the steel-and-defense inflection is real.

The defense revival and the railgun on the water

The second hidden jewel is far louder, and it is enjoying the strongest tailwind in the whole portfolio. JSW never fully left the defense business it was born into. It remains Japan's sole domestic prime for large-caliber gun barrels and naval gun mounts, and it makes the main cannon for the Ground Self-Defense Force's Type 10 tank. For decades, in pacifist postwar Japan, this was a stable but strategically capped franchise — a modest, low-growth line item constrained by a tiny defense budget and a ban on arms exports.

That constraint is now lifting. In response to a sharply deteriorating regional security environment, Japan committed to a historic build-up, targeting defense spending of roughly 2% of GDP — a near-doubling of the budget — and it has relaxed its long-standing arms-export restrictions. For the country's sole heavy-ordnance prime, that is a structural change in the size of the addressable market, not a cyclical bump.

There is a further, less obvious reason the defense franchise is strategically valuable to JSW beyond its growth: it is a sole-source, domestic, government-backed business that no foreign competitor can enter. Japan will not buy its tank cannons or its naval gun barrels from abroad for reasons of security and industrial sovereignty, and it cannot realistically stand up a second domestic supplier for such specialized, low-volume ordnance. That makes JSW a protected monopoly in its home defense market — the mirror image of the fiercely contested separator business. The catch, as ever with a monopoly built on a single buyer, is that the customer is a government whose spending moves on political and budget cycles, not on JSW's timetable.

Nowhere is JSW's defense-tech ambition more vivid than the electromagnetic railgun. A railgun replaces gunpowder with electromagnetic force, using a massive current to accelerate a projectile along conductive rails to hypersonic speed — the holy grail being a cheap, deep-magazine defense against hypersonic missiles. The physics is brutal: passing enough current to hurl a projectile to Mach 6-plus generates forces and heat that erode the rails after a handful of shots, and the U.S. Navy spent more than a decade and hundreds of millions of dollars before shelving its own program, defeated largely by that barrel-life problem. That Japan — through the Ministry of Defense's 防衛装備庁 Acquisition, Technology & Logistics Agency (ATLA), with JSW as the industrial hand — got a railgun to fire repeatably from the deck of a ship at sea is a genuine engineering milestone, not a press release. In October 2023, ATLA and the Maritime Self-Defense Force conducted what was reported as the world's first firing of a railgun from a ship at sea, launching a 40mm projectile at roughly Mach 6.5.3 The current prototype runs on around five megajoules of charge energy with an ambition to scale toward twenty. JSW has spoken openly of the goal of turning this into a hypersonic-missile defense for the 2030s.[^7]

The reason a railgun is such a coveted capability is economic as much as military. An interceptor missile that shoots down an incoming hypersonic weapon can cost millions of dollars per shot, and a saturation attack can simply exhaust the defender's magazine. A railgun fires a comparatively cheap metal slug and can, in principle, keep firing as long as it has power — deep magazine, low cost per shot. If it works at scale, it changes the arithmetic of missile defense. That "if" is doing enormous work, and an investor should treat the railgun exactly as the technology it is: a high-variance option, not a line in the model.

An investor should hold two thoughts at once here. The railgun is a genuine, world-leading technical achievement and a marker of JSW's engineering depth. It is also, today, a research program funded out of modest R&D budgets — the kind of prototype work measured in single-digit billions of yen — not a production revenue stream. Its value is optionality on a defense-procurement wave that may or may not materialize in the 2030s. Which brings us to the shadow over all of it — because a defense and nuclear supplier lives or dies on one thing above all, and in 2022 JSW was caught having quietly corroded it for a quarter of a century.

VII. The Governance Crisis: Inside the 2022 Quality Scandal

On May 9, 2022, JSW issued the kind of disclosure that makes a defense ministry and a nuclear regulator sit up straight. Its subsidiary Japan Steel Works M&E, Inc. — the heavy-forgings unit at the heart of Muroran — had been falsifying, fabricating, and manipulating the results of material tests and product inspections.[^4] Reuters reported the same day that the company was investigating data falsification affecting turbine and other components.1 This was not a single rogue batch. When the special investigation committee of external attorneys reported back on November 14, 2022, the scale was staggering: inappropriate conduct spanning power-generation products, cast and forged steel, plates and pipes, and — most alarming — nuclear energy products and ordnance, with cases stretching back roughly a quarter of a century.[^5]

How a proud forge faked its own certificates

The breakdown was chilling in its specifics. The misconduct touched on the order of twenty nuclear-related components and a handful of defense-ordnance cases, alongside hundreds of instances across the broader product range.[^5] France's nuclear safety regulator separately flagged irregularities affecting nuclear equipment JSW had supplied, underscoring that this was not a purely domestic problem — the contaminated trust reached into reactors abroad.

How does a company forge seamless reactor rings that the world depends on, and simultaneously fake the paperwork that certifies them? The investigation painted Muroran as an insular fiefdom governed by an "absolute delivery schedule" culture. When a multi-ton, multi-million-dollar forging cooled slightly out of dimensional or mechanical tolerance, the choice on the factory floor was stark: scrap a fortune in steel and blow the delivery date, or quietly adjust the test-equipment outputs so the part passed. Too often, for too long, workers chose the keyboard over the scrap heap. The rot was possible precisely because quality assurance reported up through the same factory management that owned the delivery schedule — the fox guarding the henhouse.

This is the third great lesson of the JSW story, and it is a devastating one for anyone who believes reputation alone protects a franchise. A quality culture built on trust, without tamper-proof systems, is fragile under delivery pressure. JSW's prestige — a century of forging the world's most demanding steel — was exactly what let the fraud hide in plain sight for so long. Nobody audits the firm everyone already trusts. The engineering excellence and the governance failure were not opposites; they grew in the same insular soil.

It is worth situating this in the wider context of corporate Japan, because JSW was not an isolated bad apple. The 2010s and early 2020s produced a grim procession of quality-data scandals at some of the country's most respected manufacturers — falsified inspection records surfacing across steel, materials, and components makers. The pattern was strikingly consistent: a revered manufacturing culture, a shop floor under relentless delivery and cost pressure, inspection processes owned by the same people responsible for shipping on time, and a deference to hierarchy that made whistle-blowing nearly unthinkable. JSW's fraud was a particularly dangerous instance of a systemic national weakness, not a uniquely Japanese-Steel-Works villainy. That framing matters for investors, because it means the fix is not "hire better people" — it is "build systems that make the fraud impossible even for pressured people," which is a harder and more capital-intensive undertaking.

The response has become the redemption arc of the current management. Toshio Matsuo, who took over as president in April 2022 in the very thick of the crisis, chose transparency over the reflexive corporate instinct to minimize. He inherited the scandal rather than caused it, which gave him both the freedom and the obligation to be brutal about it. Rather than a controlled internal review, JSW commissioned an independent external investigation by outside attorneys and published its findings, and Matsuo committed to a structural remediation with three planks: decoupling quality-assurance reporting lines from factory-floor management so QA answers to the center rather than to the schedule; investing in automated testing equipment to strip human data entry — the exact point of tampering — out of the loop entirely; and re-inspecting and re-validating affected products with customers and regulators to re-establish that the parts already in service were, in fact, safe. On the earnings and briefing circuit that followed, management's framing was notably un-defensive: the misconduct was presented as a governance failure of the company's own making, to be fixed by systems, rather than blamed on a few individuals.

For investors, the credibility test is not whether Matsuo apologized; every Japanese executive apologizes. It is whether the systems changed, because culture reverts and systems endure. On that score the record so far is encouraging in form — full disclosure, external investigation, structural QA changes — but it is the kind of claim that can only be validated by the absence of a recurrence over many years. A single repeat would be close to fatal for the nuclear and defense franchises, which live entirely on certification. That existential stakes-of-trust reality is exactly why the next question — how management deploys capital and defends its legitimacy — carries such weight.

VIII. Capital Allocation & The Activist Stress Test

Every few years a Japanese industrial company publishes a mid-term plan, and investors have learned to read them with a skeptical eye, because the graveyard of Japanese corporate history is full of confident three-year targets quietly abandoned in year two. JSW's plan is called JGP2028, and what makes it worth taking seriously is less the targets themselves than what management did to them in the summer of 2026 — because the revision reveals which parts of the story management actually believes.

First, the base rate. In the fiscal year ended March 2026, JSW grew net sales roughly 11% to ¥274.9 billion and lifted operating profit about 11% to ¥25.3 billion, with net profit of ¥19.2 billion.[^1] Those are respectable, not spectacular, numbers — mid-single-digit-billions of dollars in revenue growing at a double-digit clip, a roughly 9% operating margin, and a return on equity around 9.5%.[^1] The equity ratio near 49% signals a conservatively financed balance sheet — arguably too conservative, which is precisely the kind of lazy-balance-sheet feature that draws activists who see under-levered equity as trapped capital.[^1] The forecast for the year ahead pointed to further top-line growth toward ¥310 billion, with earnings expected to be broadly flat — a signal that management is buying growth now and expecting the profit to follow later rather than immediately.

The original JGP2028, unveiled in 2024, set out clear FY2028 destinations: net sales of ¥400 billion, operating income of ¥40 billion, and a 10% operating margin, funded by a large step-up in investment weighted heavily toward growth, with capital expenditure scaling up sharply versus the prior plan and much of it aimed at expanding twin-screw extruder capacity.[^3] On shareholder returns, the plan committed to a consolidated dividend payout ratio of 35% or more and a minimum dividend-on-equity (DOE) of 2.5% — a floor designed to keep payouts from collapsing in a down year, and a nod to the market's demand for capital discipline.[^3] For the fiscal year just closed, the company delivered on the payout commitment, lifting the annual dividend to ¥92 per share at a 35.2% payout ratio.[^1] The DOE floor is a subtle but meaningful commitment: by tying the minimum dividend to equity rather than to earnings, JSW promises to keep returning cash even in a year when profits dip — reassuring for income investors, and a small piece of evidence that the board has internalized the capital-discipline critique rather than merely nodding at it.

Then, on July 7, 2026, JSW updated the plan — and the re-mix is the most revealing document in this entire story. The headline ¥400 billion revenue target held, but the engines driving it were swapped around under the hood. The defense revenue target was doubled to roughly ¥100 billion, riding the national build-up and export liberalization. The nuclear and power-components target was raised to around ¥80 billion, explicitly citing demand from AI data centers hungry for firm, carbon-free electricity. And crucially, the plastics and EV-related machinery target was cut — revised down by tens of billions of yen — in candid acknowledgment of the EV slowdown.2 The operating margin target was nudged up to 10.0% and ROE to a 10–11% range, with a further capital-expenditure commitment of around ¥30 billion at Muroran to expand power-generation component capacity.2

There is a genuinely fascinating detail buried in the nuclear upgrade: the demand catalyst is artificial intelligence. Management explicitly tied the raised nuclear-components target to power demand from AI data centers.2 The logic is that the electricity appetite of large-scale AI computing is reviving interest in firm, carbon-free baseload power — which means nuclear, both life-extension of existing reactors and new small modular reactors. A company that forges reactor vessels is, improbably, a second-order beneficiary of the AI boom. Whether that thesis holds is unproven — data-center power can also be met by gas, renewables, and storage, and SMRs remain largely pre-commercial — but it is a striking example of how the energy transition keeps handing JSW's dormant heavy-forging asset new potential customers.

Read the re-mix as an analyst, not a cheerleader. It is, on the positive side, a mark of honesty: management cut the fashionable EV number rather than defend a target the market would have laughed at, and it leaned into defense and nuclear where the evidence genuinely turned. Cutting your own headline growth target is not a natural act for a management team, and doing it openly is a real, if modest, credibility signal — the kind of behavior an investor should weight more heavily than any amount of upbeat narrative. On the cautious side, it is also a bet that two politically driven, lumpy, government-dependent demand streams — defense procurement and nuclear revival — will reliably backfill a consumer-driven growth market that just disappointed. Government demand is real but slow, subject to budget cycles and political weather, and it does not compound like a winning commercial product; a defense order can be delayed a year by a budget fight, and an SMR program can slip a decade. The plan is more credible than most Japanese mid-term plans precisely because management has already been willing to revise it downward where reality demanded. It is not, however, derisked, and the gap between a ¥400 billion target and the roughly ¥275 billion the company earned in FY2026 is a large distance to travel in a few years on the back of order books that have not yet fully materialized.

And this is where the skeptics — increasingly, activists — enter the frame. JSW has long traded at a conglomerate discount, and the reason is structural. Bolt a high-growth, high-return machinery business (extruders, separator lines, semiconductor lasers) onto a capital-heavy, cyclical, scandal-scarred steel-and-defense business, and the market refuses to pay a machinery multiple for the whole. The consolidated entity gets valued closer to its heaviest, ugliest part. For years the stock languished around or below a price-to-book ratio of 1.0 — the threshold that, since 2023, the Tokyo Stock Exchange has explicitly pressured listed companies to fix, demanding that sub-1.0-PBR firms lay out concrete plans to improve capital efficiency.

A brief primer on why price-to-book is the metric that matters here, since it drives the whole activist logic. Book value is, roughly, the accounting net worth of the company — assets minus liabilities. When a stock trades below one times book, the market is effectively saying the company is worth less alive, run by current management, than the sum of the capital sitting inside it — a quiet vote of no confidence in how that capital is being deployed. For an asset-heavy firm like JSW, stuffed with land, presses, and factories carried on the books, a sub-1.0 PBR is a standing invitation to anyone who thinks the parts are worth more than the whole. In 2023 the Tokyo Stock Exchange turned that invitation into semi-official policy, publicly pressing chronically sub-1.0-PBR companies to publish concrete plans to raise their capital efficiency or explain themselves — a uniquely Japanese piece of regulatory nudging that has supercharged shareholder activism across the market.

The activist thesis: sum-of-the-parts

The activist thesis writes itself: split the company. Carve out the high-ROE Industrial Machinery division and let it trade on its own merits, freeing it from the cyclical steel-and-defense anchor. Divest non-core assets, unwind Japan's traditional cross-shareholdings — the web of mutual equity stakes Japanese firms hold in their business partners, which tie up capital and blunt accountability — and return the trapped value to shareholders. The math the activist points to is simple and uncomfortable: if the machinery business alone, valued on a machinery multiple, is worth more than the entire company's current market capitalization, then the steel-and-defense division is being assigned a negative value by the market, which is absurd for a business that is actually inflecting upward. Japan's activism wave — documented in 2026 as intensifying against exactly this profile of low-PBR, cash-rich, structurally complex industrials — has companies like JSW squarely in its sights. A meaningful slice of the register sits with institutional custodians; a large block is held in the name of The Master Trust Bank of Japan, the country's dominant trust-bank nominee (a custodial vehicle holding shares on behalf of others, not a beneficial owner in its own right), and behind such nominees increasingly sit domestic trust banks and foreign institutions willing to vote for change rather than defer to management.

The counter-argument management can make is not trivial: the "conglomerate" here shares a genuine technological root — process metallurgy and precision manufacturing — and the steel/nuclear/defense side, whatever its optics, is precisely what is now inflecting upward. Splitting at the moment defense and nuclear finally turn could destroy the option just as it comes into the money, and there are real operational synergies — shared metallurgy, shared plant, shared engineering talent — that a clean carve-out would sever. That tension — unlock value now versus keep the portfolio whole to harvest a turning cycle — is the central unresolved capital-allocation debate around JSW in 2026, and it has no clean answer.

How should an investor weigh management's credibility in the middle of that debate? On the evidence so far, the Matsuo-era record leans positive but is not yet proven. In its favor: the team inherited a scandal and chose radical disclosure over cover-up; it set out a concrete, numeric mid-term plan rather than vague aspiration; and — the single most telling behavior — it revised that plan by cutting its own fashionable EV target while raising the ones the evidence supported, which is the opposite of the overpromise-and-hope pattern that erodes trust in so many management teams. Against it: the ¥400 billion revenue destination remains a long way from today's base and rests heavily on government demand the company does not control; the capital-efficiency problem (a chronic sub-1.0 PBR and a conservative balance sheet) has been acknowledged more than it has been solved; and the ultimate test of the quality remediation — years without a relapse — simply has not had time to run. The honest verdict is that management has earned the benefit of the doubt on candor and lost none of it on execution yet, but the hardest promises are the ones still outstanding. What the whole saga does yield, unambiguously, is a set of lessons that generalize well beyond one Japanese forge.

IX. The Playbook: Key Lessons for Founders and Investors

Strip away the battleships and the railguns, and JSW's century leaves three durable lessons that generalize far beyond heavy industry.

Lesson 1: A cornered resource is a double-edged sword. JSW's 14,000-ton press and its irreplaceable metallurgical craft gave it something close to an absolute monopoly in ultra-heavy nuclear forgings — and then Fukushima demonstrated the fatal flaw of that position. When your unique asset serves essentially one end-market, you are not diversified; you are concentrated in a way that looks like strength right up until the market you serve disappears overnight. The time to build the second engine is before the crisis, when the first engine is still roaring and nobody thinks you need it. JSW built its machinery business under duress, after the shock; the more valuable version of that lesson is to build it beforehand.

Lesson 2: The asset is the process, not the product. The through-line from 46cm gun barrels to seamless reactor rings to sub-five-micron battery membranes to semiconductor laser annealing is not any single product — it is the underlying mastery of manipulating materials under extreme, precisely controlled conditions. Companies that understand their real asset is a transferable process capability can ride from one dying vertical to the next emerging one. Companies that think their asset is the product they happen to sell today tend to die with that product. JSW has survived a hundred years and two obsolete core businesses precisely because it kept recognizing the process, not the object, as the crown jewel.

Lesson 3: Quality culture without systems is a liability disguised as an asset. The 2022 scandal is the dark mirror of Lessons 1 and 2. The same deep, proud, insular craft culture that produced world-beating forgings also produced two decades of falsified inspection data, because trust-based quality controls have no defense against sustained delivery pressure. Reputation is not a control. Digital, tamper-proof, automated verification is. Any investor evaluating a "prestigious engineering firm" should ask a cold question: what stops a stressed operator on the night shift from adjusting a number? If the only answer is "our people wouldn't do that," the honest translation is "we have no control at all."

These lessons converge on a single investment question: from here, does JSW win, and what breaks the case?

X. The Investment-Story Spine: Bull vs. Bear Case

Let us wargame it properly, because the bull and bear here are unusually well-matched, and the truth is that both are partly right.

The bull case rests on three engines finally pointing the same direction. The EV-and-grid megatrend, even in a slowdown, still needs ever-thinner, higher-quality separator film, and JSW's line-integration position gives it durable pull; batteries are not going away, and grid-scale storage is a second demand pool sitting behind the automotive one. The nuclear franchise — long dead — is being revived by an unexpected patron: the AI data-center boom, whose bottomless appetite for firm, carbon-free power has put small modular reactors (SMRs) and large-reactor life-extension back on the table, and JSW's Muroran forging capability is now, in management's telling, both irreplaceable and cleaned of its compliance sins.2 If SMRs commercialize at anything like the scale their backers hope, the demand for exactly the kind of high-integrity forgings JSW makes would return — and JSW would face far less competition than in the 2000s, since a generation of the nuclear-winter years saw rivals exit or under-invest. And the defense build-up hands JSW a stable, high-margin, domestic government revenue stream with a decade-long runway and a doubled internal target to match.2 Three secular tailwinds, one company, all cited in the July 2026 plan revision — that is a genuinely rare alignment, and it is the crux of why the stock has begun to attract attention after years in the wilderness.

The bear case is equally concrete, and it starts with the same three engines viewed from the short side. The EV slowdown is not hypothetical; JSW itself cut the plastics target for exactly that reason, and a prolonged battery-demand slump — or a shift toward battery chemistries and cell architectures that need less or different separator film — could stall the order book that anchors the machinery growth story. The nuclear revival is a thesis, not a backlog: SMRs remain largely pre-commercial, big-reactor new-build is slow and politically fraught, and data-center power may simply be met by cheaper, faster options. Defense demand, for all its tailwind, depends on a government budget that could be trimmed by the next fiscal crisis or the next dovish administration. Input-cost inflation — high-grade scrap, alloys, and above all the electricity that heavy forging devours — can compress margins in the legacy steel and defense divisions faster than pricing can catch up. And hanging over everything is compliance risk: any repeat of the 2022 falsification, in a business whose entire value proposition is certification, could trigger de-certification by nuclear regulators or the defense ministry and vaporize the two franchises the bull case depends on. The scar tissue is real, and it is thin. The bear does not need all of these to break; any one of the three growth engines stalling while capex stays elevated would leave JSW with idle capacity and a disappointed market.

Five forces and 7 Powers

Run it through Michael Porter's five forces and the picture sharpens. Barriers to entry are extraordinarily high in the two heavy franchises — you cannot casually build a 14,000-ton press or a certified defense supply chain — and high but more contestable in machinery, where German rivals compete hard. Buyer power is significant: JSW's customers are giant utilities, battery makers, and a single national defense ministry, all capable of squeezing. Supplier power runs through raw steel and energy, where JSW is a price-taker. Substitutes are the quiet threat — renewables plus storage substituting for nuclear, sodium-ion or solid-state chemistries reshaping separators. Rivalry is most intense precisely in the growth business. The uncomfortable read is that JSW's strongest competitive positions sit in its slowest, most cyclical markets, and its most contested positions sit in its fastest-growing ones.

Through Hamilton Helmer's 7 Powers, the standouts are cornered resource (Muroran's forging craft, the deepest and most durable power JSW holds), switching costs (a separator maker rebuilt around a JSW line does not lightly change), and a dose of scale economies in systems integration and, on the defense side, a process power rooted in a century of ordnance know-how that no new domestic entrant could replicate. Notably absent are network effects and any consumer-style brand as a pricing lever — and JSW's brand power among engineers was, if anything, negative after 2022, a moat that had to be repaired rather than exploited. A company whose competitive edge rests on trusted certification does not want its brand associated with falsified certificates, and rebuilding that intangible is slow, unglamorous work that will not show up cleanly in any single quarter's numbers.

A few second-layer diligence overlays round out the picture, the kind of things that do not appear in the headline story but matter to a careful owner. On capital allocation discipline, the swing factor is the sharp step-up in capital expenditure under JGP2028: aggressive capex after a period of restraint is exactly where "growth investment" can quietly curdle into "diworsification" and idle capacity, so the execution rate bears watching. On governance and ownership, the post-scandal board changes and the rising weight of institutional and foreign holders behind the trust-bank nominees have made the register more activist-friendly than it was a decade ago, which cuts toward eventual portfolio action. On balance-sheet optionality, JSW carries the classic Japanese-industrial features — an under-levered balance sheet, land and cross-shareholdings carried at historical cost, and non-core assets that could be monetized — all of which are latent value an activist would push to unlock and all of which also flatter the sub-1.0-PBR arithmetic. None of these is a thesis on its own; together they describe a company sitting on more stored, unexpressed value than its market price admits, guarded by a management team whose willingness to release it is the open question.

So the "why win / why not" verdict is honestly balanced. JSW wins from here if — and only if — the nuclear and defense inflections are real and durable, the separator franchise re-accelerates as EV demand normalizes, the semiconductor-laser option matures, and, underneath it all, the post-scandal quality systems hold without a single serious relapse. It loses if EV weakness proves structural, if government demand disappoints on timing or budget, if input costs outrun pricing, or if trust breaks again. Management's July 2026 candor — cutting the fashionable number, leaning into the turning ones — is a point in its favor on credibility. It is not proof of execution.

The three KPIs that will settle the argument

For an investor who wants to track whether the thesis is being validated rather than merely asserted, three KPIs cut through the noise:

- Industrial Machinery operating margin. This is the single best readout of pricing power against low-cost competitors and of whether the growth investments are earning their keep. Rising margins mean the systems-integration moat is holding; eroding margins mean it is a commodity fight.

- Defense-segment backlog and order conversion. The railgun and advanced-artillery programs are prototypes today; the number that matters is whether R&D contracts convert into firm, multi-year procurement orders. Backlog growth is the leading indicator that the defense tailwind is real money, not press releases.

- CapEx execution and capital-efficiency (ROE / PBR) trajectory under JGP2028. With capital expenditure scaling up sharply, the test is whether that spending translates into high-yielding revenue and a re-rating above book value — or into idle capacity and a persistent conglomerate discount that eventually forces the activists' hand.

The deepest irony of The Japan Steel Works is that a company born to make the tools of the last century's wars now sits at the intersection of this century's defining industrial contests — batteries, nuclear power, semiconductors, and the militarization of the Pacific. It has the rarest kind of industrial capability, and the hardest kind of governance history to live down. Whether the metallurgy of these modern choke points finally earns the market's respect, or remains trapped inside a discounted, complicated, asset-heavy holding company, is the question the next several years will answer.

References

-

Japan Steel Works investigates data falsification on turbine parts — Reuters, 2022-05-09 ↩

-

The Japan Steel Works Revises Mid-Term Plan Upward, Targeting ¥400 Billion in Revenue by FY2029 on Defense and Nuclear Power Demand — BigGo Finance, 2026-07-07 ↩↩↩↩↩

-

Japan Performs First Ever Railgun Test From Ship at Sea — Naval News, 2023-10-17 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube