Feytech: The Architect of the Automotive Interior

I. Introduction: The "Invisible" Tier-1 Powerhouse

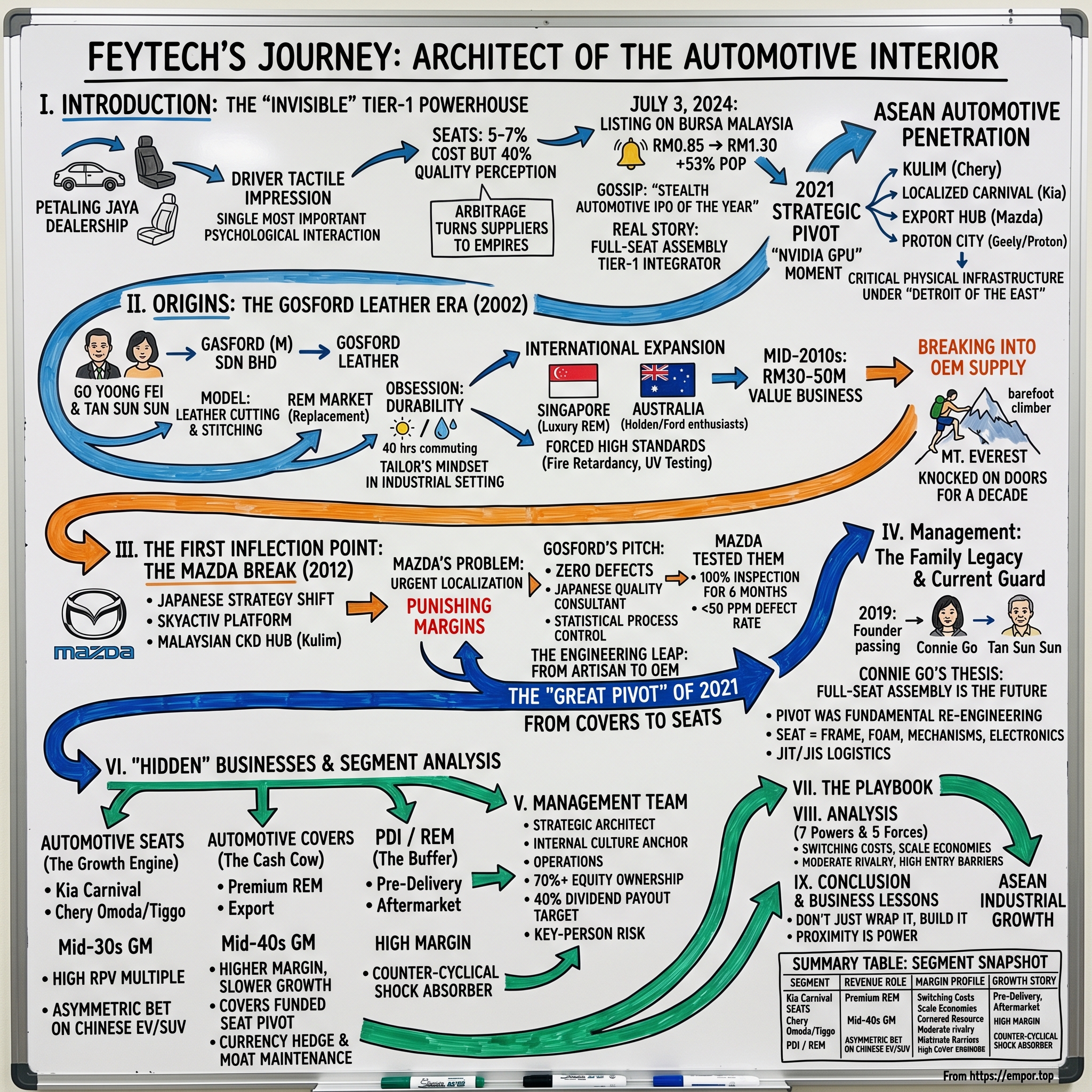

Picture the moment you slide into the driver's seat of a brand-new Kia Carnival at a dealership in Petaling Jaya. The door closes with that satisfying, vault-like thud. You run your palm across the bolstered leather, adjust the headrest, feel the contour of the lumbar support press into the small of your back. That first tactile impression — that's the single most important psychological interaction any driver has with their car. It is also, more often than not in Malaysia, Thailand, and across the ASEAN belt, the handiwork of a company most people have never heard of.

Most car enthusiasts obsess over engines, chassis tuning, infotainment silicon. They argue about torque curves on Reddit and whether the new Skyactiv-Z actually lives up to Mazda's marketing. But sit with a veteran automotive executive long enough, and they will tell you that the physical interface between a human being and a two-ton machine — the seat — is where the real value, and the real margin, quietly lives. Seats account for roughly 5% to 7% of a car's bill of materials, yet they drive something closer to 40% of the customer's perception of quality. That gap between cost and perception is the kind of arbitrage that turns suppliers into empires.

On July 3, 2024, a small Malaysian company called Feytech Holdings Berhad rang the bell on Bursa Malaysia's Main Market, listing at an IPO price of RM0.85 per share and raising roughly RM128 million. In 24 hours, the stock closed at RM1.30, a 53% first-day pop. In the gossip circles of the Klang Valley investment community, it was described as "the stealth automotive IPO of the year." But the real story wasn't the pop. It was what the company had quietly become in the three years prior: a full-seat assembly Tier-1 systems integrator for some of the most important carmakers pushing into Southeast Asia.

For two decades, Feytech — through its predecessor Gosford Leather — had been known as the country's premium leather craftsman. The kind of shop where a Mercedes owner from Bangsar could order a hand-stitched replacement upholstery set. A respectable, solid, artisan business. But artisanship does not usually scale to ringing an exchange bell. Something changed.

In 2021, Feytech made what this episode will argue was its "Nvidia GPU" moment — a single strategic pivot that transformed the ceiling of the business from a capped craft company into a platform that could ride the single biggest manufacturing migration happening in Asia right now: the rerouting of Japanese, Korean, and Chinese automotive production away from China's mainland and into ASEAN.

Malaysia, of all places, has become the quiet beneficiary. Chery opened a CKD (complete knock-down) plant in Kulim. Kia localized the Carnival. Mazda reinforced its Malaysian hub for ASEAN export. Geely's investment in Proton continued to deepen. Each of these required one non-negotiable input: a Tier-1 seat maker willing and capable of building a factory within truck-delivery distance of the assembly line.

The story of how a leather shop became that Tier-1 supplier — how it navigated the death of its founder, engineered a once-in-a-company pivot, and positioned itself as the critical physical infrastructure underneath the "Detroit of the East" — is the story of this episode. It is a story about craftsmanship meeting scale, about the quiet power of geography, and about what happens when a family business decides it no longer wants to be invisible.

Let's rewind to the beginning.

II. Origins: The Gosford Leather Era

In 2002, Malaysia was a country in recovery. The scars of the 1997 Asian Financial Crisis were fading, Proton was still the national automotive champion, and the streets of Kuala Lumpur were filled with aging Iswaras, Wiras, and the occasional imported Toyota Camry showing every mile of its punishment. The car was aspirational, but maintaining one was an exercise in economy. You bought a car, you drove it for a decade, and when the seats cracked and the vinyl flaked off, you took it to a leather shop in a shop-lot somewhere off Jalan Klang Lama and had it reupholstered.

Into this ecosystem stepped a quiet, methodical man named Go Yoong Fei, together with his wife Tan Sun Sun. They founded what was originally registered as Gasford (M) Sdn Bhd, soon rebranded as Gosford Leather. The business model was almost boring in its simplicity: source premium leather, cut it precisely, stitch it meticulously, and sell complete seat cover replacement kits to the REM — Replacement Equipment Manufacturer — market. If your Perdana's seats had given up, Gosford had your answer.

What makes this origin story interesting is not the idea. Half a dozen competitors were doing exactly the same thing. What mattered was Yoong Fei's obsession with a single variable: durability. Malaysian drivers, Yoong Fei observed, were brutal on their seats. The tropical heat turned cabins into ovens. Humidity seeped into every stitch. Long commutes in bumper-to-bumper KL traffic meant the driver's bolster absorbed 40 hours of twisting pressure every week. A cheap leather cover would fail within 18 months. A great one would last the life of the car.

Yoong Fei priced his covers at a premium and backed them with a craftsman's reputation. He traveled personally to suppliers in Italy and Turkey to vet hides. He studied Japanese stitching patterns. Stories within the company still circulate about how he would unstitch a freshly completed cover if he found a single misaligned seam, and make the workshop start again. It was, in many ways, the mindset of a tailor dropped into an industrial setting.

The critical early move — one that would quietly set Feytech apart a decade later — was the expansion beyond Malaysia. By the mid-2000s, Gosford had pushed into Singapore, serving the luxury car aftermarket that catered to Mercedes, BMW, and Lexus owners who wanted their upholstery renewed to concours standards. Shortly after, Australia entered the footprint, driven by demand from the Holden and Ford enthusiast community that still treasured hand-fitted leatherwork.

This international expansion is easy to overlook. But it mattered for two reasons. First, exporting into Singapore and Australia forced Gosford to meet standards that the Malaysian REM market was not yet demanding — fire retardancy ratings, abrasion cycle testing, UV colorfastness. The kind of QC discipline that an OEM contract would later require. Second, it taught the family something about the economics of supplying to markets with very different price points from the same core factory. You could be a craftsman and a scale operator simultaneously, if you were careful about how you segmented your output.

By 2010, Gosford was running a profitable, respected, mid-sized leather business. The kind of company that generated steady mid-teens margins, paid its dues, and was probably worth RM30 million to RM50 million on a private sale. It was a good life. For most founders, this would have been the destination.

But Yoong Fei had been watching something in the background. Every year, Malaysia's passenger car production crept upward. Toyota opened capacity. Honda expanded. Nissan built. And every one of those cars rolled off the line with an interior — seats, covers, trim — that was being imported, in whole or in part, from Thailand or Japan. To someone who had spent ten years becoming a master of cutting and stitching automotive leather, the inefficiency was glaring. The OEMs were paying freight on something that could be made on their doorstep.

The problem, of course, was that breaking into OEM supply was the automotive industry's version of climbing Everest barefoot. You had to convince a Japanese procurement team, notorious for favoring incumbent Japanese suppliers, that a Malaysian leather shop could meet the tolerances, volumes, and audit trails demanded by a modern car plant. For nearly a decade, Gosford knocked on doors. For nearly a decade, the doors stayed shut.

Then, in 2012, one door cracked open. And the company's entire trajectory bent.

III. The First Inflection Point: The Mazda Break

To understand why 2012 mattered, you have to understand what was happening in Japanese automotive strategy at the time. Mazda was a wounded animal. The company had just emerged from the financial crisis of 2008-2009, had been abandoned by its longtime partner Ford, and was betting its entire future on a radical fuel-efficiency platform called Skyactiv. The first car built fully on that platform was the new-generation Mazda 3, launching in Southeast Asia starting in 2013-2014 model years, and Mazda's Malaysian CKD operation in Kulim, Kedah was designated as a regional production hub.

Mazda's problem was urgent. Malaysian localization content requirements meant that a meaningful percentage of each car's value had to be sourced domestically to qualify for favorable tax treatment. Import duties on fully-built Japanese interior components were punishing margins. Mazda needed a local Tier-2 supplier who could produce seat covers to Japanese quality specifications. They did not, frankly, expect to find one.

Gosford's pitch was unusual. Rather than promising lowest cost, Yoong Fei's team promised zero defects. They proposed bringing in a Japanese quality consultant on a retainer basis, implementing the kind of statistical process control usually reserved for Tier-1 suppliers, and offering Mazda's procurement team unrestricted audit access to the factory floor. In exchange, they asked for a long-term cover supply contract on the Mazda 3 and the yet-to-launch CX-5.

Mazda tested them. The story inside Feytech is that for the first six months, every single batch was inspected at 100% before shipment — not by Gosford, but by Mazda's own quality team parked inside the factory. The defect rate reportedly dropped to fewer than 50 parts per million within the first year. For context, a typical REM leather shop would be lucky to hit 5,000 ppm on aftermarket work. The discipline gap between artisan work and OEM work is roughly two orders of magnitude.

This is the engineering leap that gets glossed over in most retellings. Going from hand-cutting leather for 50 retail customers a month to shipping 3,000 identical matched-pair seat covers a month, on time, in Mazda's exact kanban sequence, is not a matter of hiring more people. It is a matter of rebuilding the entire backbone of a company. Gosford invested in computer-controlled cutting beds. It hired industrial engineers. It implemented automotive-grade traceability, so that every cover could be traced back to the hide, the cutter, the stitcher, and the shift in which it was produced. Process sheets replaced tribal knowledge. Yoong Fei, a man who had built his life on personal inspection, had to accept that he could no longer see every piece that left the factory.

The Mazda contract changed the economics. While the REM business had carried unit prices of a few hundred ringgit with gross margins above 40%, OEM covers came with lower unit prices but enormous volumes and multi-year visibility. More importantly, the Mazda relationship became a reference. Within three years, Gosford had added additional OEM relationships — initially as Tier-2 supplier to the seat assemblers, but increasingly with direct procurement conversations. The Malaysian automotive community is small and gossip travels fast. A supplier who did not break under Mazda's ppm audits was a supplier worth looking at.

The more subtle consequence was cultural. Gosford's workforce, previously dominated by skilled manual craftspeople, began to include industrial engineers, quality technicians, and production planners. The language on the shop floor shifted from tailor-speak to lean-manufacturing-speak — takt time, first-pass yield, OEE. Some of the older craftspeople chafed. A few left. Yoong Fei, according to those who worked with him, approached this transition with both sadness and clarity. He understood that a craft shop could not supply Mazda. And he understood that if Gosford remained a craft shop, it would eventually be squeezed by the very OEM migration it was benefiting from.

So by the late 2010s, Gosford had quietly become something different from what it had started as. It was still a leather cover company. But underneath, it had developed the operational muscle of an automotive parts company — disciplined, engineered, auditable. That muscle was about to be tested in a way no one inside the business had anticipated.

In 2019, Go Yoong Fei passed away.

IV. The "Great Pivot" of 2021: From Covers to Seats

There is a period in the life of many founder-led companies when the death or departure of the founder functions as either a death sentence or a forging fire. Gosford entered that period in 2019. For 17 years, Yoong Fei had been the gravitational center of the company — the conscience on quality, the final signature on any major decision, the face that the Mazda procurement team knew personally. His passing left his wife, Tan Sun Sun, holding a roughly one-third stake, and the broader family wrestling with a question that has bankrupted countless Southeast Asian family businesses before it: what now.

The answer, as it emerged over the following 18 months, was neither caretaker continuity nor quiet sale. It was the opposite. It was the most aggressive strategic pivot in the company's history.

The architect of that pivot was Connie Go, Yoong Fei's sister. Connie had spent years inside the business in operational and strategic roles, but after her brother's passing she stepped forward as CEO with a specific thesis: the next 20 years of Malaysian automotive would not be about cover supply. It would be about localized full-seat assembly. And if Feytech did not make that jump now, while it still had the capital and the customer relationships to attempt it, the window would close.

To understand why Connie's thesis was correct, you need to understand the structural difference between a cover and a seat. A seat cover is a textile. It can be manufactured anywhere in the world, packed into a container, and shipped across an ocean to the customer's factory with perhaps four to six weeks of lead time. Margins are decent, but the value-per-unit is modest — somewhere in the range of RM200 to RM400 per vehicle set. A full seat, by contrast, is a 30-kilogram assembly of steel frames, foam padding, adjustment mechanisms, motorized tracks, heating elements, airbag modules, sensors, and the cover wrapped over the top. You cannot ship completed seats efficiently across oceans. They take up too much volume, and the OEM's assembly line needs them delivered in sequenced kits — "Just-In-Time, Just-In-Sequence," or JIT/JIS — exactly when each specific car's body reaches the seat-install station.

This is why the global seat supply industry — dominated by giants like Adient, Lear, Magna, and Toyota Boshoku — is built around a single non-negotiable rule: you build your seat plant within about 40 kilometers of the car plant, and often inside a 2-hour truck window. The physical constraint creates the moat. And the value per vehicle jumps. A full seat assembly carries a revenue per vehicle of roughly RM1,500 to RM3,000 depending on content — four to seven times what a cover alone commands.

Connie's pivot, then, was not cosmetic. It was a fundamental re-engineering of the business. Making seats requires completely different capabilities than making covers: metal frame welding, foam molding, mechanism sub-assembly integration, safety-critical testing (airbag deployment paths, whiplash protection geometry), and JIT/JIS logistics software that hooks directly into the OEM's build schedule. Nothing in Gosford's history had prepared the company for any of this.

The trigger moment came with the Kia Carnival contract. Kia, through its regional assembler, needed a seat supplier for its Malaysian-assembled Carnival — the three-row people-mover that had become a runaway hit with Southeast Asian families who wanted SUV space without SUV fuel bills. Connie and her team made the pitch: Feytech would stand up a dedicated full-seat line near the Kia assembly plant, co-invest in the tooling, and sit inside Kia's JIT/JIS kanban window. Kia said yes.

This moment is the single most important inflection in the company's history, and it is worth pausing on what it actually meant. Before the Carnival contract, Feytech was a Tier-2 supplier — a company that sold components to a seat maker who in turn sold to Kia. Feytech had no direct commercial relationship with the automaker. After the Carnival contract, Feytech was a Tier-1 supplier — selling the full seat system directly to Kia, responsible for the seat performance, warranty, and regulatory certification. Tier-1 status is the automotive industry's equivalent of joining a cartel. There are roughly 200 companies in the world with multi-brand Tier-1 seat integrator status. Feytech became one of them.

The Kia Carnival win cascaded. Chery, the Chinese brand rapidly expanding across ASEAN with its Omoda and Tiggo lines, signed Feytech as a seat partner for its Malaysian CKD program. Mazda, already a trusting incumbent on covers, began discussions to move Feytech up to Tier-1 seat supply on select models. Each new OEM win compounded the capital justification for new capacity — land in Kulim near Kia and Mazda, land in Klang Valley near Proton and Perodua, foam and frame equipment, automated cutting beds, JIS warehouse systems.

The economics changed shape. Seat assembly operates at lower gross margins than premium leather covers — roughly 30% to 35% at the segment level versus 40%-plus on covers — because you pass through the cost of bought-in steel and electronics. But you make it up on volume and on revenue per vehicle. Put simply: covers are a high-margin niche, seats are a scale business. Connie's bet was that Malaysia's automotive production was about to enter a multi-year scale phase, and that the right move was to own the scale game even at the cost of blended margin compression.

The bet has, to this point, aged extremely well. By the time Feytech listed in July 2024, the seat segment had grown to more than half of group revenue, with growth rates compounding at a pace that made the legacy covers business look positively sedate. But the more important legacy of the pivot is not financial. It is that Feytech became a different kind of company — one where geography is a weapon, where customer integration is a wall, and where every new automotive brand opening a plant in Malaysia is a prospective conversation partner.

Pivots of this scale do not happen because of a spreadsheet. They happen because someone decides. And the someone here deserves a section of her own.

V. Management: The Family Legacy & Current Guard

There is a particular kind of Malaysian family business — quiet, disciplined, deeply intertwined with the founder's personal standards — that does not translate well onto a prospectus. Feytech's management, reduced to a paragraph, looks like an ordinary Southeast Asian family-controlled company: husband-and-wife founders, a sibling in the CEO chair, another sibling in operations, combined family ownership well north of 60%. A reader scanning the shareholder register might nod and move on.

But sit with the people who have worked inside Feytech, and a more textured portrait emerges. This is a management team that has absorbed the death of a founder, executed a business-model pivot that reshaped the industrial logic of the company, and taken the business public — all while holding together the cultural fabric that made the original workshop what it was. That is not an ordinary outcome.

Connie Go, the CEO, is the strategic architect. Trained in business and tempered by years alongside her brother in the covers business, Connie has a reputation inside the industry for two things: a near-religious focus on customer proximity, and a willingness to commit capital decisively when the window opens. Colleagues describe her negotiation style as patient but sharply prepared. She reportedly personally attended almost every major OEM site visit during the 2021-2023 Tier-1 transition, making the case in rooms full of Japanese and Korean procurement executives who had not previously dealt with a Malaysian seat supplier. Her case was simple: we will be there, on time, every time, at the specification you demand. The pitch, and the follow-through, worked.

Tan Sun Sun, an Executive Director, holds roughly a third of the equity and serves as the internal culture anchor. She is the surviving spouse of Yoong Fei, and within the company she plays a role that is hard to capture on an org chart. She is the connection to the founding ethos — the reminder, in every operational meeting, that the company was built on craftsmanship standards that could not be relaxed just because the volumes went up. Her management style is understated but, by multiple accounts, formidable. Decisions that might violate the original quality compact do not survive her review.

Go Yoong Chang, also an Executive Director, oversees operations. Running an automotive operations portfolio that spans cover exports to multiple countries, Tier-2 cover supply to OEMs, and full Tier-1 seat assembly across multiple plants is the kind of job that breaks executives in companies ten times Feytech's size. Yoong Chang's reputation is for deep shop-floor presence and an almost unglamorous obsession with plant KPIs — uptime, first-pass yield, delivery adherence. In an industry where customer relationships are won on the golf course but kept on the shop floor, this is exactly the split the company needs.

The family collectively holds more than 70% of the equity post-IPO, which concentrates both alignment and responsibility. The company has articulated a dividend payout target of roughly 40%, which is meaningful not because of the absolute yield it produces but because of what it signals. Committing to pay out 40% of earnings indicates that management believes the cash-generating capacity of the business is durable enough to return capital to shareholders even while funding a capex-intensive expansion into new seat plants. It is a tonal statement as much as a financial one.

What makes the management profile investable, beyond the numbers, is the demonstrated willingness to evolve. Family businesses that make the transition from founder-led craft operations to publicly listed Tier-1 automotive suppliers are rare. Most of them fail, either by preserving craft at the expense of scale or by preserving scale at the expense of the cultural DNA that made the company attractive in the first place. Feytech's leadership has, thus far, threaded that needle. The covers business still runs with the discipline of the Yoong Fei era. The seats business runs on modern lean-production principles. The boundary between them is managed with intention, not accident.

There is, inevitably, key-person risk. Much of the commercial and strategic weight sits on Connie's shoulders. The cultural anchor is concentrated in Sun Sun. Operational execution runs through Yoong Chang. If one of these three were to step back suddenly, the organization would have to redistribute a lot of tacit knowledge quickly. Public company discipline and a growing second-tier management bench mitigate this, but it is the kind of risk that a sober investor keeps in mind with any family-controlled business, regardless of how well things have gone to date.

The post-IPO governance structure has added independent directors with automotive and capital markets experience. Whether that board ends up as real stewardship or as decorative compliance is one of the things that will define the next five years. The early signals are that the family takes outside counsel seriously, particularly on capital allocation, but family businesses that have been right for two decades can develop a gravitational pull that is difficult for independent directors to counterbalance.

Underneath the management question lies the business question: what exactly is the company today, and where is each segment heading?

VI. "Hidden" Businesses & Segment Analysis

On paper, Feytech presents itself as two businesses — automotive covers and automotive seats — with a smaller pre-delivery inspection and replacement-equipment line as a rounding category. The simplicity is slightly misleading. Underneath, the business is a portfolio of distinct customer relationships, each with its own competitive dynamic, margin profile, and growth runway. Understanding them individually is the difference between seeing Feytech as a Malaysian auto parts company and seeing it as a systems integrator positioned at a specific moment in ASEAN industrial history.

Automotive Seats: The Growth Engine. The seats segment accounts for a little over half of group revenue and is the segment that matters most for the forward trajectory. This is where the Kia Carnival contract lives, the Chery relationships live, and where the lion's share of capital expenditure is being directed. Margins are structurally lower than covers — think mid-30s at the gross line — because so much of the bill of materials is pass-through (steel frames, foam chemistry, mechanisms, electronics). But the revenue-per-vehicle multiple more than compensates. Every percentage point of incremental Malaysian passenger car production that goes onto a Feytech-supplied platform converts to outsized revenue growth at the group level.

The hidden story within seats is the Chery partnership. For the casual observer, Chery is just one more Chinese brand making an ASEAN push. But within the Malaysian automotive ecosystem, Chery's arrival has been unusually rapid. Chery's Omoda and Tiggo SUVs have gained meaningful market share since launch, and the brand has been aggressive in localizing production to take advantage of Malaysian incentives. Feytech's positioning as the local Tier-1 seat partner on Chery's Malaysian program is an asymmetric bet on Chinese EV and SUV penetration across ASEAN. Each new Chery model adds to the volume equation. Each new Chery model also deepens the customer relationship, which means Feytech gets first look at future platform decisions.

Automotive Covers: The Cash Cow. The cover segment, the original business, remains a profitable and strategically important line. Margins are higher than seats — closer to the mid-40s at the gross line — reflecting the premium leather heritage and the direct REM pricing power. Growth is slower, but that misses the point. Covers are the business that funded the seat pivot, and covers continue to be the profit engine that supports capital investment into the higher-growth seats segment.

The export footprint of the covers business — Singapore, Australia, and selected other markets — provides two forms of optionality. First, it's a currency hedge, with a portion of revenue coming in foreign currency against a largely ringgit cost base. Second, it's a moat-maintenance mechanism. Continuing to serve premium aftermarket customers in Singapore and Australia keeps the craftsmanship bar high, which in turn keeps the OEM quality reputation intact. The covers segment is, in a sense, the company's living museum — and museums that still earn their keep are valuable things.

Pre-Delivery Inspection / REM: The Buffer. The smallest of the three reported buckets is a mix of aftermarket replacement equipment manufacturing and pre-delivery services. It is small in absolute revenue but structurally useful: it runs on high margins and tends to behave counter-cyclically to new-car production. When new-car cycles slow, aftermarket volumes typically pick up as vehicle owners extend the life of their existing cars. This is not a growth driver. It is a shock absorber on group results, and worth noting precisely because it is usually ignored.

The Real Estate and Capacity Story. Arguably the least discussed but most structurally important part of the Feytech story is the physical footprint. The company operates from multiple plant sites, with a particularly significant concentration in Kulim (strategic to Kia and Mazda) and in the Klang Valley region (strategic to Perodua and Proton). Post-IPO capital deployment included a notable land acquisition in the Proton City area — roughly RM19.9 million for land positioned to serve Proton's Tanjung Malim production hub. Another chunk of IPO proceeds went toward working capital to support the capacity ramp.

This footprint is not glamorous in an investor presentation. But it is the deepest moat the company has. A Tier-1 seat plant is not a fungible asset. You cannot pick it up and move it to a different automotive cluster. Every location is chosen to sit inside a JIT/JIS truck window of a specific OEM. Every new location is a multi-year, capital-heavy commitment that compounds over time. The real estate strategy, in effect, is a strategy of buying toll booths on the most important logistical corridors of Malaysia's automotive map.

None of this works, however, without the right underlying playbook on how capital is deployed and how the corporate structure was designed to support the IPO and the post-listing expansion.

VII. The Playbook: M&A, Capital Deployment, & Benchmarking

Every company, when it lists, goes through a tidying-up exercise that is part corporate hygiene and part public-facing narrative. For Feytech, the tidying-up began in earnest in 2023 and continued through the first quarter of 2024. The key move was a restructuring consolidation that brought the various historical operating entities — Gosford Leather's Malaysian arm, the Singapore business, the Australian business, and Feytech SB, which housed the emerging seat assembly operations — under a single listed holding company, Feytech Holdings Berhad.

This was not a coincidental cleanup. The restructuring served three very specific strategic purposes.

First, it created a unified reporting perimeter that a public market investor could understand. Prior to restructuring, the various parts of the business reported into different corporate structures, with intercompany arrangements that made segment analysis difficult for an outsider. Consolidation made the group economics legible.

Second, it captured value that had been sitting latent in the craft business and redirected it toward the scale opportunity in seats. The covers business had been generating cash for years. Under the new structure, that cash could be allocated explicitly toward the highest-return opportunities in the enlarged group, rather than sitting within a legal silo.

Third, it set up the IPO. The July 2024 listing — priced at RM0.85 per share, raising roughly RM128 million in new primary capital and valuing the group at around RM680 million at issue — gave Feytech a public currency and balance sheet flexibility that a family-owned structure would have struggled to match. Within weeks of listing, the stock re-rated meaningfully, a signal that the public market was viewing the company not as a covers company with a listing overhang, but as a Tier-1 automotive platform with a legacy covers asset.

The use-of-proceeds disclosed at the IPO is worth reading carefully. Rather than earmarking capital for M&A — which would be the pattern for a more financially aggressive playbook — the company allocated proceeds toward what can fairly be called asset-heavy moats: roughly RM19.9 million for land, RM52 million for working capital to support the ramping JIT/JIS seat operations, and additional amounts toward capacity and equipment. This is not a company trying to buy growth. It is a company trying to build capacity precisely aligned with incoming OEM demand.

Benchmarking Feytech against the global seat supply giants is instructive. Adient and Lear are the two largest pure-play automotive seat companies in the world, with revenues in the range of USD 14-20 billion depending on the year and cycle. Their gross margins typically sit in the high single digits to low teens, reflecting the massive commoditized pass-through of their bill of materials and the relentless pricing pressure exerted by their megacap OEM customers — Ford, GM, Stellantis, Volkswagen.

Feytech, operating at a fraction of that scale, reports gross margins in a different universe — 35% to 45% at the segment level. Why? Two reasons. First, the legacy premium leather DNA commands a meaningful premium even when integrated into a seat assembly. Feytech is not competing to supply the cheapest seat in a stripped-down hatchback; it is supplying premium-spec seats into models where the OEM is willing to pay for perceived quality. Second, the ASEAN automotive supply ecosystem is less saturated than North America or Europe. There is pricing power in being one of very few Tier-1 capable seat suppliers in Malaysia, pricing power that Adient has long since lost in Michigan or Ontario.

This margin gap is both a strength and a vulnerability. The strength is obvious: it means the company converts revenue into cash at a rate that a Lear or Adient would envy. The vulnerability is that as ASEAN automotive production scales and attracts more competition from Thai, Chinese, and Japanese seat suppliers willing to set up local operations, Feytech's pricing power will be tested. Whether the margin structure is a durable moat or a temporary rent extracted from a supply-constrained market is one of the most important investor debates around the company.

The company has, thus far, resisted the temptation to deploy IPO proceeds into aggressive M&A. In the Malaysian small-cap industrial space, this is culturally unusual. The peer set is full of companies that IPOed and immediately went on shopping sprees for tangentially-related businesses to justify the capital raise. Feytech's stated deployment priorities — land adjacent to OEM customers, working capital to support the ramp, targeted equipment investment — read as operationally focused rather than financial-engineering focused. For long-term fundamental investors, this ordering usually ends better than its opposite.

The question that remains is how defensible the position Feytech has built actually is, and how it stacks up against the competitive forces arrayed against it. The playbook has been executed well, but the more important question is what the structural endgame looks like.

VIII. Analysis: Hamilton's 7 Powers, Porter's 5 Forces, and the Myth vs Reality

At this point in the episode it helps to zoom out and apply two of the most useful frameworks for evaluating durable competitive advantage: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. The exercise is not academic — it surfaces which parts of Feytech's position are genuinely defensible and which parts might erode faster than the narrative suggests.

Hamilton's 7 Powers Applied to Feytech. Of the seven powers Helmer identifies, three are materially at work in Feytech's business.

The dominant power is Switching Costs. Once an OEM has integrated a Tier-1 seat supplier into its JIT/JIS line, the cost of switching is not just financial — it is operational risk. The seat supplier's logistics system is hooked into the OEM's build schedule. The seat plant has been audited, validated, and certified against the model's safety and quality specifications. Every engineer on both sides knows each other. Ripping out a Tier-1 seat supplier mid-platform is the kind of decision that gets escalated to board level at the OEM, because if anything goes wrong during the transition, an entire assembly line can go dark. In practice, this means that Tier-1 seat contracts tend to run for the full life of a model platform — typically five to seven years — and are often renewed across platform generations.

The second material power is Scale Economies, though in a subtler way than for a megacap seat giant. Feytech does not have cost-per-unit advantages against Adient at a global level. But at the regional level, within Malaysia, the scale advantage is real and growing. Feytech's automated cutting capacity, foam capacity, and integrated assembly lines are meaningfully larger than any local competitor's. A new entrant trying to replicate the footprint would need to spend years and hundreds of millions of ringgit in capex, all while trying to convince OEMs to divert business from an incumbent supplier.

The third power, more nuanced, is Cornered Resource. The specific Tier-1 relationships with Kia, Chery, Mazda, and the growing depth with Perodua/Proton through the Proton City footprint, constitute a resource that competitors cannot easily duplicate. Automotive procurement relationships are not like consumer contracts that can be won with a pricing tweak. They are built over decades, across thousands of audit points, and depend on a history of non-failure. Feytech's cornered resource is essentially twelve years of earned trust, starting from the Mazda break of 2012.

The four powers less applicable here are Counter-Positioning (not particularly relevant to this business), Network Economies (irrelevant for an industrial supplier), Branding (limited, because the end customer sees the automaker's brand, not the seat supplier's), and Process Power (partially applicable through accumulated manufacturing expertise, but not a decisive standalone advantage).

Porter's 5 Forces Applied to Feytech. Porter's framework adds a different layer of analysis, particularly around the dynamics between buyers, suppliers, and substitutes.

Bargaining Power of Buyers: High in theory, moderated in practice. Global OEMs like Kia and Mazda have enormous procurement leverage. But that leverage is constrained by two things: the Malaysian localization requirements that force OEMs to source content domestically, and the absence of a deep bench of alternative Tier-1 seat suppliers in Malaysia. Buyers cannot squeeze Feytech to global Adient-level margins because the market structure will not support it.

Bargaining Power of Suppliers: Moderate. Foam chemistry, steel frames, and electronic components are sourced from specialized suppliers, and commodity price fluctuations (particularly in steel and petrochemicals) directly affect input costs. Feytech passes through most commodity risk through contractual terms with OEMs, but lags and frictions exist.

Threat of New Entrants: Low. The capex, time-to-qualification, and customer relationship requirements form a high entry barrier. A greenfield Tier-1 seat operation in Malaysia would take three to five years to become commercially relevant, and by the time it was qualified, the platforms worth fighting for would already be locked in with incumbents.

Threat of Substitutes: Low in the short run, potentially meaningful in the long run. Autonomous driving and shared mobility could restructure the seating content of vehicles over a 10-to-20-year horizon — more lounge-style interiors, more reconfigurable seating modules, possibly new safety architectures. Feytech's ability to pivot into these content shifts will determine whether it rides the wave or gets displaced by new-form competitors.

Industry Rivalry: Moderate. Within Malaysia, rivalry among Tier-1 seat suppliers is limited by the scarcity of qualified players. Regionally, Thai and Chinese competitors could target Malaysian OEM business if they set up local operations. The rivalry intensity is likely to rise over the next five years, though from a low base.

Myth vs Reality. A few narrative fact-checks worth making.

Myth: Feytech is a leather company. Reality: Feytech was a leather company for 19 years. It is now a systems integrator where leather is one layer of a much more complex product. Valuing it as a textile business materially underestimates both the capex intensity and the customer-relationship moat of the current business.

Myth: The ASEAN auto migration is a fad tied to current geopolitical tensions. Reality: The migration is partially geopolitical but is also structural. Labor cost differentials, ASEAN consumer demand growth, and regional free-trade architecture (RCEP, ATIGA) create durable reasons to build cars in Malaysia, Thailand, and Indonesia even after current tensions cool.

Myth: Family-controlled businesses with 70%+ insider ownership are governance risks. Reality: High family ownership can be either a risk or an alignment vector depending on execution. In Feytech's case, the family has demonstrated, through the pivot and the IPO, willingness to make long-term decisions even when they required cultural discomfort. That is a meaningful signal, though it does not eliminate the structural governance discount that public markets typically apply to high-insider-control companies.

Myth: High margins are proof of a durable moat. Reality: High margins are often proof of a current pricing position, which may or may not be durable. Feytech's 35%-45% gross margins look excellent relative to global seat peers, but a significant portion reflects the premium covers legacy and the supply-constrained Malaysian seat market. As scale increases and regional competition intensifies, margin normalization is a reasonable expectation, not a surprise.

KPIs to Track. For long-term fundamental investors, three metrics cut through the noise better than any others.

First, revenue per vehicle platform. Tracking how Feytech's content-per-vehicle evolves across its active platforms (Carnival, Chery models, Mazda, Perodua/Proton) tells you whether the company is winning more content on existing platforms or being squeezed. Rising content per vehicle is the clearest sign that the Tier-1 transition is deepening.

Second, gross margin by segment. The divergence or convergence between covers margins and seats margins tells you whether the pricing power of the premium leather heritage is holding as volumes scale, or whether pass-through dynamics in seats are eroding the blended profile.

Third, new OEM/platform wins. Every new OEM relationship or new platform qualification extends the moat. Every lost relationship or failed qualification is a structural warning. The list is small enough to track individually.

Taken together, Feytech's competitive position looks like a genuine, if regional, moat — durable for the next five to seven years given platform lifecycles, and with optionality depending on how ASEAN automotive demand evolves.

IX. Conclusion & Business Lessons

Every good business story ends with a lesson, and Feytech's ends with two that extend well beyond automotive.

The first lesson is "Don't Just Wrap It, Build It." For 19 years, Feytech sold the skin. For the last five, it has been selling the body. The jump from covers to seats is not just a product jump — it is a jump up the value chain that multiplies revenue per unit by four to seven times, reorders the customer relationship from Tier-2 to Tier-1, and transforms the ceiling of what the business can become. This pattern — moving from a component inside a system to owning the system itself — is one of the most reliable ways a supplier-side business can escape margin compression and platform dependency. It requires capex, it requires courage, and it usually requires a specific moment when the customer is willing to let you try. Feytech recognized the moment and took it.

The second lesson is "Proximity is Power." In a world that talks endlessly about digital moats, network effects, and globalized supply chains, Feytech is a reminder that some of the most durable competitive advantages are profoundly physical. A seat plant built 30 kilometers from a Kia assembly line is an asset that cannot be replicated by anyone who does not build their own plant at the same distance. Geography, in the automotive supply business, is destiny. The company's quiet but deliberate strategy of acquiring land near the Proton, Kia, Mazda, and Perodua clusters is the building of a physical moat that will take years for any competitor to challenge, and that grows stronger with each new OEM platform that selects a Feytech plant.

Underneath both lessons sits a quieter truth about succession. Feytech did not arrive at this moment because a founder lived to see it. It arrived at this moment because a family, confronted with the death of its patriarch, made harder choices than most families make in that situation. Connie Go's pivot decision in 2021 could have easily been a consolidation decision — tighten up the covers business, harvest cash, pay out dividends, enjoy a respected legacy. It was not. It was a decision to spend capital, stretch the organization, and bet on a larger future that Yoong Fei did not live to see but would, by every account of those who knew him, have recognized as the natural next chapter.

From the outside, Feytech still looks like a modest Malaysian small-cap — a few hundred million ringgit market cap, a handful of OEM customer logos, a business most investors could not pick out of a lineup. But the Malaysian automotive ecosystem it sits inside is one of the most dynamic industrial stages in Asia right now. Chery is building. Kia is localizing. Mazda is reinforcing. Proton, under Geely's hand, is modernizing. Each of these decisions creates demand for exactly the kind of Tier-1 integrator capacity that Feytech has spent the last five years building.

The company is not yet a household name. It may never be one. The end customer, sliding into that Kia Carnival at a dealership in Petaling Jaya, will never know who built the seat that closes so perfectly around their back. But the automotive industry knows. The OEM procurement teams know. And increasingly, the Malaysian capital markets know.

Feytech is not just a leather company. It is not just a seat company. It is the physical infrastructure of the Malaysian automotive dream — the quiet, methodical, family-stewarded Tier-1 that happens to be standing exactly where the road bends toward the next decade of ASEAN industrial growth.

And the most interesting chapter, almost certainly, has not been written yet.

Summary Table: Segment Snapshot

| Segment | Revenue Role | Margin Profile | Growth Story |

|---|---|---|---|

| Automotive Covers | The "Cash Cow" | ~45% (High) | Steady OEM + REM exports. |

| Automotive Seats | The "Growth Star" | ~35% (Medium) | The 2021 pivot; 4x-7x higher revenue/unit. |

| PDI / REM | The "Buffer" | High | Protects against new car cycle slumps. |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube