AirAsia X: The Phoenix of Long-Haul Low-Cost

I. Introduction & The "Impossible" Business Model

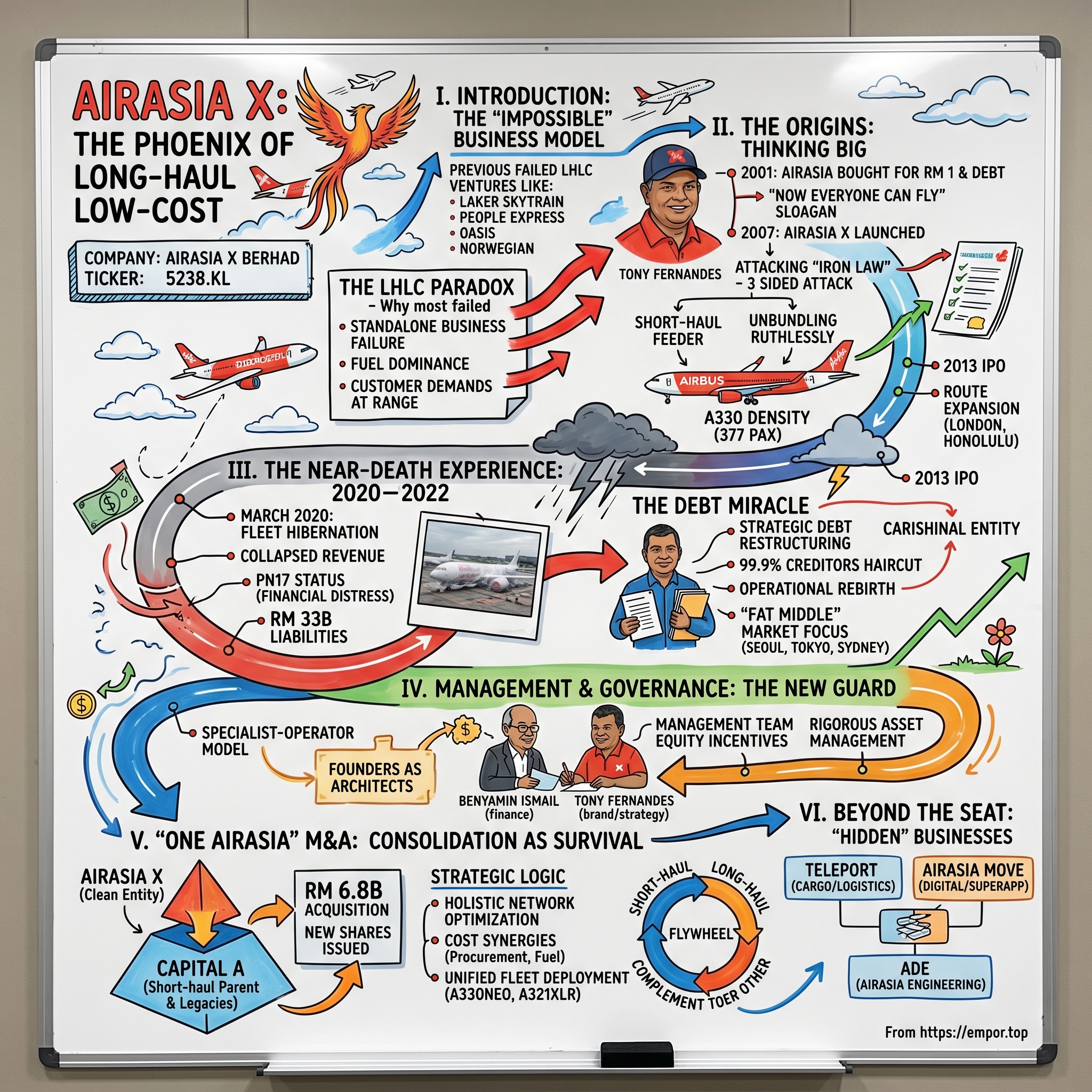

In the summer of 1977, Sir Freddie Laker stood on a tarmac at Gatwick Airport in London, dressed in a somewhat rumpled suit and beaming ear-to-ear, and declared that he was about to change aviation forever. His Skytrain service—one-way tickets from London to New York for just £59, roughly a third of what British Airways charged—was going to democratize transatlantic flight. Five years later, Skytrain was bankrupt. A decade after that, People Express collapsed trying the same trick. Then came Hong Kong-based Oasis, which lasted eighteen months. Then AirAsia X's own first attempt at London. Then Norwegian Air Shuttle, which at its 2019 peak operated 37 long-haul Dreamliners and nearly took down the entire Scandinavian aviation industry with it.

For the better part of five decades, Long-Haul Low-Cost—LHLC, as industry insiders call it with a grimace—was aviation's Holy Grail: eternally promised, never delivered. The mathematics seemed simple enough. If Southwest could crush the legacy carriers on the short-haul Dallas-to-Houston run, and Ryanair could reduce intra-European flying to a bus service in the sky, surely somebody could stretch that playbook across oceans. Every few years, a new ambitious founder would convince credulous investors, order a batch of Boeing 787s or Airbus A330s, and promptly discover the same ugly truth: the economics that make short-haul budget flying work—rapid turnarounds, dense single-aisle configurations, secondary airports—stop working at range. Fuel dominates. Crew rotations demand hotels. Maintenance intervals compress. Customers start wanting meals, baggage, and the ability to actually recline.

And yet today, on April 23, 2026, one airline has not only survived the LHLC graveyard but is absorbing its own parent company in what is shaping up to be Asia's most audacious aviation consolidation in a generation. AirAsia X Berhad, trading under the ticker 5238 on Bursa Malaysia, is executing a roughly RM 6.8 billion acquisition of the entire aviation business of Capital A Berhad—effectively flipping the corporate pyramid upside down. The long-haul subsidiary is swallowing the short-haul parent.

This is a company that, four years ago, was technically insolvent. A company whose planes sat wrapped in protective covers at KLIA for the better part of two years. A company whose creditors were asked—and in a stunning vote, agreed—to accept a 99.9% haircut on approximately RM 34 billion in claims. A company whose stock traded for pennies and whose name appeared on the Malaysian stock exchange's dreaded PN17 list, the regulatory equivalent of a hospice ward.

The thesis of this episode is uncomfortable for orthodox aviation analysts. It is this: the long-haul low-cost model did not fail. What failed were the operators who tried to run it as a standalone business. The version that works—perhaps the only version that works—is the one where a short-haul low-cost giant has already blanketed a region with cheap feeder flights, built a recognizable consumer brand, accumulated the operational muscle memory of running three hundred daily departures, and then uses that infrastructure as a launch pad for wide-bodies. AirAsia X is that version. And it nearly died proving it.

The journey from here traces an arc that would feel implausible in fiction. Tony Fernandes buying a debt-laden national airline for one ringgit in 2001. The audacious launch of "X" in 2007 to run four-hour-plus routes on a budget. The IPO euphoria. The expansion into London, Paris, and Honolulu. The retreat. The pandemic. The hibernation. The debt miracle. And now, the corporate reshuffling that will make AirAsia X the only listed vehicle for one of the world's most recognizable low-cost aviation brands. How this happened, why it matters, and whether the consolidation actually creates the flywheel management promises—that is the subject of the next two hours.

II. The Origins: Thinking Big

Walk into the basement of a nondescript office tower in Kuala Lumpur's Glenmarie industrial estate in the early 2000s and you would have found a thirty-seven-year-old former Warner Music executive named Anthony Francis Fernandes hunched over spreadsheets at 2 AM, running sensitivity analyses on jet fuel prices on a laptop that, by his own account, he could barely afford to keep. He had just mortgaged his house. He had resigned from a senior role at one of the world's biggest record labels. And he had, alongside his business partner Kamarudin Meranun and two other investors, just purchased an airline.

The price they paid has become mythology. One ringgit—roughly a quarter in U.S. currency—for a 51% stake in AirAsia Sdn Bhd, a struggling domestic Malaysian carrier owned by a conglomerate called DRB-HICOM. The catch: the airline came with approximately RM 40 million in debt, two ageing Boeing 737s, and a staff who had not been paid on time in months. Fernandes had no aviation experience. Kamarudin, a former investment banker, had no aviation experience either. Their guiding principle, articulated in dozens of interviews afterward, was that running an airline could not possibly be harder than running a record label at the exact moment Napster was destroying it.

By 2003, AirAsia was profitable. By 2004, it was listed on Bursa Malaysia at RM 1.25 per share. By 2006, it had more than 20 aircraft and was operating across Malaysia, Thailand, and Indonesia through joint ventures carefully structured to navigate the region's patchwork of aviation ownership rules. The slogan—"Now Everyone Can Fly"—was not marketing fluff. For a generation of Southeast Asians who had never boarded a commercial aircraft, who had assumed flying was something rich people did, AirAsia rewired expectations the way Ryanair had done in Europe a decade earlier.

Then came the idea that would break the industry orthodoxy and nearly break the company.

Fernandes and Kamarudin had been studying the route maps obsessively. They saw what aviation strategists had been saying for years: the two-hour window where Southwest economics shine—Bangkok to Singapore, Kuala Lumpur to Jakarta—was lucrative, but finite. The real growth was in the four-to-eight-hour radius. Kuala Lumpur to Seoul. To Tokyo. To Sydney. To Mumbai. These were routes dominated by full-service legacy carriers charging two to three thousand ringgit round-trip. A budget traveler had no option. And crucially, AirAsia's own short-haul network was producing millions of passengers a year who, if offered a cheap onward connection, would happily sleep on the floor at LCCT to get one.

The trick was that nobody had cracked the financial physics. The received wisdom, repeated in Boeing and Airbus sales presentations for thirty years, was that wide-body economics required premium passengers up front to subsidize coach. No premium cabin, no long-haul profit. That was the iron law Freddie Laker had broken himself against.

Fernandes' answer, formalized in 2007 when AirAsia X was carved out as a separate entity, was to attack the iron law from three sides at once. First, exploit the feeder. A passenger flying Jakarta to Melbourne on AirAsia X would not be paying full promotional fares all the way; they would be booked on a combined itinerary where the short-haul leg was essentially marketing. Second, unbundle ruthlessly. Food, baggage, seat selection, priority boarding—every line item became a revenue stream, not a cost. And third, fly the Airbus A330. The A330-300, configured in a punishing 9-abreast economy layout, became the densest wide-body in global commercial aviation. A flagship Cathay Pacific A330 carried around 265 passengers; AirAsia X's version, 377. That roughly 42% density premium was the whole ballgame.

The partnerships followed in rapid succession. Virgin Group took an early stake. Mitsui of Japan invested. Manara Consortium of the UAE came in. An initial public offering in July 2013 raised approximately RM 987 million at an IPO price of RM 1.25 per share, pricing the company at roughly RM 2.7 billion. Tony Fernandes rang the bell at Bursa Malaysia wearing his trademark baseball cap, told reporters that "X" would one day be bigger than the mothership, and announced fresh orders for Airbus A330neos and, later, the narrow-body A321XLR—a plane that would, in theory, let AirAsia X run thin long-haul routes like Osaka to Delhi without wasting capacity.

The flywheel spun beautifully for a while. From 2013 through 2018, AirAsia X added destinations at a breakneck pace. Chengdu. Taipei. Sapporo. Jaipur. Tehran—briefly, before sanctions complicated things. Honolulu, via a politically complex "fifth freedom" arrangement through Osaka. London Stansted, then Gatwick. Passenger numbers climbed toward six million annually. Revenue broke through RM 4 billion.

But the same obsession with route experimentation that made AirAsia X exciting as a growth story also planted the seeds of what came next. Every new long-haul destination required its own regulatory approval, its own marketing push, its own crew training, its own airport handling contracts. Fuel costs were volatile. The Malaysian ringgit was volatile. And management, intoxicated by the brand's success, kept adding frequencies faster than yields could recover. By 2019, analysts covering the stock had started using a particular phrase in research notes: over-extended. Within six months, a virus from Wuhan would prove them catastrophically, generationally correct.

III. The Near-Death Experience: 2020–2022

On March 16, 2020, a team of AirAsia X engineers at Kuala Lumpur International Airport began wrapping the company's Airbus A330s in clear protective film. The process, known in aviation as "long-term parking preservation," is normally reserved for aircraft headed to desert storage facilities in Arizona or the Alice Springs outback. Engines get sealed. Sensors get covered. Fuel gets drained to precise levels. Tires are rotated on a schedule to prevent flat-spotting. What made the KLIA scene surreal was the scale: roughly 24 wide-body aircraft, essentially the entire operating fleet, parked in neat rows alongside the taxiway. By the end of April, AirAsia X was flying almost nothing. By the end of 2020, revenue for the year had collapsed from over RM 4.5 billion the prior year to approximately RM 1.2 billion, and the vast majority of that had been booked in the first quarter before the world shut down.

The hibernation was total in a way difficult to convey even years later. Full-service carriers like Singapore Airlines and Cathay Pacific were pivoting to cargo, ripping out economy seats to stuff freight into passenger cabins. Short-haul low-cost carriers could at least fly scattered domestic routes whenever governments loosened restrictions. AirAsia X had neither option. Its only product was the thing governments had banned: cross-border leisure travel on dense, long-haul, international routings. Its only asset base was a fleet of wide-bodies whose leasing costs continued to accrue whether they flew or not.

By early 2021, the balance sheet had become gruesome. Aggregate liabilities had ballooned past RM 33 billion. Lessors were owed future rentals stretching a decade out. Engine maintenance providers like Rolls-Royce TotalCare had unpaid invoices. Manufacturers were owed progress payments on aircraft orders that AirAsia X could no longer even theoretically take delivery of. The company's auditors issued a going-concern qualification—the accounting profession's way of saying the patient may not survive the night. On October 13, 2020, Bursa Malaysia formally classified AirAsia X as a PN17 company, the status reserved for financially distressed listed entities required to submit a regularization plan.

Into this disaster walked a then-38-year-old former investment banker named Benyamin bin Ismail, who had joined AirAsia X in 2014 after stints at CIMB and Maybank Investment Bank. Benyamin had been involved in the IPO, then moved into various commercial and strategy roles, before being elevated to CEO in May 2020—effectively given the keys to a burning building and asked to rebuild it from inside while the fire continued. A colleague who worked with him during the period described Benyamin in one line: "He learned to find calm by doing very hard math very early in the morning."

The math he ended up doing that year rewrote Malaysian corporate finance. The plan Benyamin, the board, and their advisors at Alvarez & Marsal took to creditors in late 2020 was, on paper, almost comically aggressive. They proposed that essentially all creditors—aircraft lessors, trade vendors, banks, everyone not secured and essential—accept RM 200 million in total settlement for approximately RM 33 billion in outstanding claims. That worked out to roughly 0.5 sen for each ringgit owed. A 99.5% haircut. In more casual reference, management and the business press rounded it to "99.9%" and the figure stuck.

The audacity was the point. Benyamin's team argued that the only realistic alternative was liquidation, in which unsecured creditors would receive approximately zero. Twenty cents on the dollar did not exist. Ten cents did not exist. The only version of this story where creditors recovered anything was one in which AirAsia X survived, and survival required a clean slate. The creditor composition was masterfully handled through the High Court of Malaya. On November 12, 2021, the scheme received court sanction. A handful of aircraft lessors who had held out ultimately came along. By early 2022, AirAsia X had legally extinguished the vast bulk of its pre-pandemic liabilities.

This was not, however, a magic wand. The restructuring also required an operational rebirth. The fleet was cut. Orders for A330neos and A321XLRs were drastically renegotiated. And critically, the new AirAsia X made a strategic choice that defined everything that came after: it walked away from the long-haul routes that had defined the pre-COVID brand. London Stansted—gone. Paris Orly—gone. Honolulu—gone. Jeddah—gone. Even Osaka-Honolulu, the much-celebrated fifth-freedom routing, disappeared from the schedule.

In their place came a relentless focus on what management started calling "the fat middle" of the Asian market: four-to-seven-hour sectors from Kuala Lumpur to Seoul, Tokyo, Shanghai, Delhi, Sydney, Auckland, Almaty. Routes where AirAsia X's density advantage was preserved, where the feeder network from short-haul AirAsia could fill seats at the margin, and where load factors could hit the high 80s consistently. Management had discovered something European LHLC carriers had missed: the magic was not in flying further. The magic was in flying dense wide-bodies exactly long enough to exploit the unit-cost advantage and not one kilometer further.

By mid-2023, AirAsia X was exiting PN17 status. Revenue for the financial year ending December 2023 recovered past RM 2.9 billion. Load factors were above 80%. And for the first time since 2017, the company posted a clean, uncontested operating profit. The stock, which had touched RM 0.04 during the darkest moments, had begun a gradual climb that would eventually see it trade at multiples of its restructuring-era trough. The patient had survived the night. Now came the second, harder question: what to do with the rest of its life.

IV. Management & Governance: The New Guard

There is a photograph circulated internally at AirAsia X headquarters in Sepang that tells the management story more compactly than any organizational chart. It was taken in early 2022, shortly after the court approval of the debt restructuring. Benyamin Ismail stands in the foreground, in a white shirt with the sleeves rolled up, holding a thick printed document. Behind him, slightly blurry, Tony Fernandes is making a joke at somebody's expense. The composition is unplanned, but the symbolism is not. The founder is still in the room. He is still animating the energy of the organization. But the document—the operating reality of AirAsia X—is being held by someone else.

Benyamin is, in almost every respect, the mirror opposite of the man who created AirAsia. Fernandes is a showman, a brand-builder, a man who once personally drove Formula 1 cars around tracks to promote sponsorships. Benyamin is a finance professional. He speaks in measured sentences, presents investor decks that emphasize capital structure and unit economics, and has become fluent in the dense vocabulary of aviation KPIs: RASK, CASK, stage length, ancillary per passenger. His background—corporate finance at CIMB, investment banking at Maybank, mergers and acquisitions work across Southeast Asia—is exactly what a company emerging from a near-death restructuring needs, and essentially nothing like what the company's founders brought to the table in 2001.

That said, describing the current governance purely through Benyamin would miss most of what is actually happening. Tony Fernandes and Kamarudin Meranun remain structurally central to AirAsia X through two vehicles. The first is Tune Group Sdn Bhd, the private holding company founded by the two of them, which has historically owned roughly 10% of AirAsia X and retains significant influence through board representation. The second is Capital A Berhad, the former parent of AirAsia that will, once the ongoing aviation reorganization completes, hold a controlling stake in the combined "One AirAsia" entity—reportedly in the range of 31% or higher depending on final terms. Between these two pools of ownership, Fernandes and Kamarudin collectively influence well over 40% of the combined entity's voting economics, even without formal executive roles.

The arrangement that has settled into place is something closer to a specialist-operator model than a traditional founder-led company. Fernandes and Kamarudin operate as strategic architects. They approve major capital allocation. They manage the political relationships with ASEAN governments and with Airbus in Toulouse. They are the public face of the brand. Benyamin and his team run the airline—the hundreds of daily operating decisions about routing, pricing, maintenance scheduling, crew deployment, ancillary product design. When Fernandes gives a speech about "making ASEAN travel seamless," it sounds, by design, like a Steve Jobs keynote. When Benyamin gives a speech about load factor discipline on the Osaka route, it sounds, by design, like an industrial executive.

The financial incentives matter here in ways that are subtle but important. Under the 2021 restructuring, management stock options and executive share schemes were heavily recalibrated. A senior AirAsia X executive who held options struck at RM 0.40 during 2019 found those options essentially worthless through the pandemic, then reset against the company's new capital structure. The practical effect is that the entire current management team is holding equity whose value depends almost entirely on the next five years of operating performance. There is, in the phrase the founders have used publicly, "no nostalgic value" left in the old incentive structure. It is turnaround-or-die economics, and the board has carefully designed it that way.

One quieter feature of the governance worth noting: the board composition shifted meaningfully through the restructuring. Independent directors with deep aviation-finance backgrounds replaced several earlier appointees whose presence reflected the company's brand-first early years. Datuk Kamarudin's role evolved into something closer to a non-executive chairman of the broader AirAsia platform. And a new layer of specialists—people with MRO backgrounds, airline-industry CFOs, logistics operators—joined to support the operational rebuild.

The philosophy animating the current governance, articulated by Benyamin in multiple earnings calls, is what might be called "rigorous asset management." Every aircraft is a capital asset whose economic productivity must be measured weekly. Every route is a portfolio position that must clear a minimum return threshold or be cut. Every ancillary product is a margin contribution that must be A/B tested. This is not how AirAsia X was run in 2014. It may well be how it has to be run in 2026 if the freshly enlarged "One AirAsia" platform is to generate the kind of free cash flow that justifies the M&A gambit now underway. And it is the kind of governance that tends, in aviation, to quietly compound over long periods—if the operators can avoid becoming complacent, which is the one failure mode founders like Fernandes are specifically designed to prevent.

V. The "One AirAsia" M&A: Consolidation as Survival

At 9:47 AM on an unremarkable Thursday in March 2024, AirAsia X filed a disclosure on Bursa Malaysia that, in the dry language of Malaysian capital markets regulation, announced what industry watchers had been whispering about for nearly a year. AirAsia X Berhad proposed to acquire the entire aviation business of Capital A Berhad—the short-haul operations across Malaysia, Indonesia, the Philippines, Thailand, and Cambodia—for a consideration of approximately RM 6.8 billion, settled primarily through the issuance of new AirAsia X shares. By the time the detailed circular was published to shareholders, the transaction had acquired a name that management clearly loved: "One AirAsia."

To understand why this deal happened at all, one has to appreciate the bizarre corporate geometry that had emerged through the pandemic years. Capital A, the rebranded parent of the original AirAsia short-haul operations, was itself under PN17 status and had been for some time. Its short-haul airlines were profitable again in 2023, but the parent entity was burdened by legacy liabilities, an awkward collection of non-aviation digital businesses, and a structure that confused investors. AirAsia X, having completed its own restructuring earlier, was the clean entity. The long-haul subsidiary had, through the miracle of sequencing, ended up healthier than the short-haul parent.

The transaction effectively flipped the pyramid. Capital A would contribute its aviation assets—AirAsia Berhad (the Malaysian operation), AirAsia Aviation Group (the broader ASEAN network), associated operating subsidiaries, and certain shared services—into the listed AirAsia X vehicle. In exchange, Capital A would receive a very large stake in the enlarged AirAsia X, while AirAsia X would receive the operational heart of Southeast Asia's largest low-cost network. Once complete, AirAsia X would be delisted and relisted (or simply renamed) as the consolidated "AirAsia Group" holding, and Capital A would be freed to resolve its own PN17 status focused on its non-aviation businesses.

The question that immediately occupied analysts: did they overpay? The honest answer, on enterprise-value-to-EBITDA multiples, is that the consideration looks reasonable against global low-cost carrier benchmarks. Ryanair has, in normal operating years, traded in the mid-single digits on EV/EBITDA. Cebu Pacific in the Philippines has traded in a similar range. IndiGo in India has historically commanded a premium closer to the high single digits given its growth profile. The approximately RM 6.8 billion consideration, measured against the combined short-haul EBITDA run-rate Capital A's aviation businesses were generating by late 2023, prices the acquisition in a range consistent with or modestly below those peers. The structure also matters: paying primarily in newly-issued AirAsia X shares rather than cash means the company is not draining its balance sheet to fund the purchase, at the cost of diluting existing shareholders.

The strategic logic, however, is where the deal becomes genuinely interesting. Before the transaction, AirAsia X was a long-haul specialist. A useful one, arguably a unique one, but fundamentally a single-product aviation company whose fate was tied to wide-body economics and a narrow band of four-to-seven-hour Asian routes. The "feeder effect"—the idea that short-haul AirAsia passengers naturally connected onto long-haul AirAsia X services—was real but was a commercial arrangement between legally separate companies, subject to pricing disputes, revenue-allocation negotiations, and occasional public tension between the two boards.

After the transaction, that feeder effect becomes an internal operating reality. Network planners at the combined entity can optimize schedules holistically—setting an AirAsia short-haul arrival in KLIA at 11:30 AM specifically because it connects to an AirAsia X departure to Tokyo at 12:45 PM, with all revenue recognized in one P&L and crew rotations scheduled across both fleets. Aircraft utilization can be managed as one asset pool. Procurement—jet fuel, engine maintenance, ground handling contracts—can be renegotiated with significantly more leverage. The cost synergies management has publicly flagged are not exotic. They are the standard playbook of any serious airline merger, and the logic is well-understood.

What makes this transaction different from the typical airline merger is that the cultural and brand foundations were already aligned. This is not America West acquiring US Airways. This is not Northwest merging with Delta. Both entities have shared the AirAsia brand for nearly two decades, share significant overlapping ownership, operate out of the same hubs, and use the same distribution platforms. The integration risk that historically destroys airline mergers—the culture clash, the pilot seniority wars, the incompatible IT systems—is drastically lower here.

Capital deployment strategy under the new structure is where things get strategically bold. Management has signaled that the enlarged AirAsia Group will use its publicly-traded shares as a currency for aircraft financing and fleet expansion in ways the two separate entities could not. The combined fleet is expected to cross 250 aircraft within the next several years. Aircraft orders that have been placed over the past decade—for A321neos, A321XLRs, and A330neos—can be allocated flexibly across the combined network. Ownership of the shared commercial platform, AirAsia MOVE, consolidates under the listed entity. The hub-and-spoke network effect that management has long described as the AirAsia flywheel—short-haul feeds long-haul, long-haul funnels back into short-haul—becomes, for the first time, financeable as a single story rather than two separate ones.

The risk, of course, is that M&A integration can quietly consume three years of management attention. Many analysts covering Asian aviation have noted that if Benyamin and his team spend 2026 and 2027 in boardrooms arguing over SAP migration plans instead of in operations centers chasing RASK improvements, the promised synergies will arrive late if they arrive at all. But the deal's structural advantages—shared brand, shared ownership, shared operating culture—give this integration a better-than-average chance of actually delivering. In aviation M&A, "better than average" is already a compliment.

VI. The "Hidden" Businesses: Beyond the Seat

Somewhere in the belly of an AirAsia X Airbus A330 flying from Kuala Lumpur to Incheon on a random Tuesday afternoon is a pallet of cosmetics headed to a fulfillment center in Seoul, a container of semiconductor components destined for Pyeongtaek, and a box of live tropical fish for a specialty importer in Gangnam. None of this cargo appears on the airline's passenger manifest. None of it is visible to the 377 human passengers upstairs. But the economics of those cargo shipments, quietly invoiced through a subsidiary called Teleport, are increasingly central to how AirAsia X will generate cash flow in the next decade.

Teleport was set up in 2018, and for its first two years it was barely noticed outside a small group of logistics executives in the Kuala Lumpur expatriate community. The original premise was straightforward: AirAsia X's wide-body aircraft had substantial belly-hold capacity, and competitor cargo carriers like DHL, FedEx, and Cathay Cargo were charging premium rates to move goods across ASEAN. If Teleport could capture even a portion of those flows, the incremental margin would be almost pure profit, because the aircraft was flying anyway and the cargo was a rider rather than a purpose.

The pandemic, improbably, made Teleport important. With passenger operations grounded, cargo demand—particularly for medical supplies, pharmaceuticals, and cross-border e-commerce—surged globally. Teleport became one of the only parts of the AirAsia X ecosystem that continued earning revenue through 2020 and 2021. More significantly, the logistics team used the forced pause to build out dedicated capabilities: customs brokerage across ASEAN, last-mile delivery partnerships in Indonesia and the Philippines, and—critically—a direct integration with the booming Chinese cross-border e-commerce platforms. By 2024, Teleport was moving goods for Shopee, Lazada, and a long tail of mid-tier platforms looking for reliable intra-Asian airfreight at prices dramatically below the legacy integrators.

The strategic opportunity Teleport is chasing is enormous and specific. Southeast Asian e-commerce is expected to exceed roughly $200 billion in gross merchandise value annually by the late 2020s, per widely-cited industry estimates. A meaningful fraction of that value flows cross-border—Chinese sellers shipping to Indonesian buyers, Vietnamese manufacturers shipping to Malaysian distributors, Thai producers shipping to Filipino consumers. The logistics for those flows are fragmented, expensive, and slow. Teleport's pitch is that it can be the ASEAN-native alternative to DHL: same-day customs, next-day delivery, prices that look like a regional postal service rather than a global integrator. Whether Teleport actually captures the share it is projecting is an open question, but the addressable market is unambiguously massive.

Alongside Teleport sits AirAsia MOVE—the digital platform and superapp rebranded from AirAsia.com. To understand why MOVE matters to AirAsia X's unit economics, consider the economics of passenger acquisition at a legacy carrier. A flag carrier like Singapore Airlines or Malaysia Airlines acquires a large share of its passengers through global distribution systems like Amadeus and Sabre, paying meaningful per-booking fees, and through third-party online travel agencies like Booking.com and Agoda, paying commissions of 15% or more. Those acquisition costs are embedded in the overall ticket economics and are one of the largest non-fuel variable expenses for a legacy airline.

MOVE's premise is that AirAsia's customer base—over 600 million cumulative passengers flown since inception, a vast loyalty database, and deep penetration in Southeast Asian demographics—can be monetized directly through an owned-and-operated booking channel. When a customer books an AirAsia flight through the MOVE app, the third-party commissions are avoided. When that customer also books hotels, activities, or rides through MOVE, additional margin is captured. The data exhaust from the platform—where people are flying, when, how often, at what price sensitivity—becomes an input to revenue management systems that can dynamically reprice fares in ways less sophisticated competitors cannot match. The platform also competes for non-AirAsia bookings against regional OTAs, which opens an optionality few Asian airlines have seriously pursued.

Then there is ADE—AirAsia Engineering, often written "Asia Digital Engineering" in filings—the group's maintenance, repair, and overhaul business. This one is the sleeper. ADE runs a large MRO facility at Sepang adjacent to KLIA, offering airframe checks, engine line maintenance, and component services. It services AirAsia's own aircraft, which are the anchor customer, but it also increasingly takes work from third-party airlines in the region. The comparison management has used privately is Lufthansa Technik—the MRO subsidiary of Lufthansa that has become one of the world's largest independent MRO operators and generates margins significantly higher than the parent airline's passenger business.

Whether ADE becomes Lufthansa Technik of Southeast Asia depends on the next several years of commercial wins. The facility has the scale. The regulatory approvals are in place. The labor cost advantage versus competing MRO bases in Europe or Hong Kong is substantial. What is needed is a growing book of third-party business, and that is a grinding, relationship-based sale that takes years to compound. If management executes, ADE could quietly become a meaningful component of group earnings. If they do not, it remains a useful captive cost center.

The synergy story across all three businesses is worth quantifying carefully, because it is the real answer to the question "why does the One AirAsia consolidation matter strategically, beyond scale?" A short-haul AirAsia flight lands in KLIA with both passengers and e-commerce cargo. The passengers connect to an AirAsia X long-haul flight, generating a premium connecting fare versus the standalone segment. The cargo connects to the same wide-body's belly, generating incremental freight revenue. The aircraft that just landed gets serviced by ADE between rotations, generating MRO revenue recognized within the same consolidated entity. The customer rebooks their return trip through MOVE, avoiding OTA commissions. This is not a fantasy hub-and-spoke—it is an operating reality that already exists at smaller scale. The consolidation makes the entire chain visible and optimizable on one P&L for the first time.

VII. Framework Analysis: 7 Powers & Porter's 5 Forces

Strip away the narrative drama of restructurings, the branding, and the founder charisma, and ask a harder question: what, if anything, protects AirAsia X from commoditization in a brutally cyclical industry? Hamilton Helmer's 7 Powers framework offers the most rigorous vocabulary for answering this, and its application to AirAsia X reveals three powers that are genuinely durable, two that are partial, and two that are essentially absent.

Start with scale economies, which in aviation translate into cost per available seat kilometer—CASK—the unit-cost metric that determines whether an airline can sustainably price below competitors. AirAsia X's wide-body CASK has, for years, been the lowest in Asia and arguably the lowest for any long-haul operator globally. The drivers are not mysterious: the 377-seat configuration of the A330, the single-fleet simplicity, the labor cost advantage of Malaysian crew bases, and the high aircraft utilization that comes from operating to fleet hubs where turnaround times can be compressed. On a per-seat-kilometer basis, full-service competitors like Singapore Airlines and Qantas operate at meaningfully higher unit costs. Even other LCCs—Scoot, Jetstar International—operate at costs significantly above AirAsia X on comparable routes. This is a real, measurable, and durable power. It is also the foundation on which everything else rests.

Cornered resources represent the second meaningful power. The AirAsia brand across Southeast Asia is a cornered resource by almost any reasonable definition—earned through two decades of advertising, sustained by millions of cumulative passengers, and essentially impossible to replicate without a similar decade-plus commitment. Landing slots at secondary Asian airports represent another. Slots at airports like Don Mueang in Bangkok, Clark in the Philippines, or Soekarno-Hatta's budget terminal in Jakarta, accumulated through early-mover positioning, are extraordinarily difficult to replicate. A new entrant attempting to launch low-cost operations in ASEAN today would find the attractive slot portfolio already owned.

Network economies—the third clearly present power—flow directly from the One AirAsia consolidation. The more short-haul destinations AirAsia serves, the more valuable each long-haul destination becomes, because connections multiply combinatorially. A traveler in Medan can reach Seoul with one intra-AirAsia connection at Kuala Lumpur. A traveler in Manila can reach Tokyo through an Incheon layover. As the combined network grows past 200 destinations, the marginal passenger becomes cheaper to acquire because the itinerary options expand. This is the classic hub airline flywheel, compressed into a low-cost economics model, and it is structurally difficult to disrupt.

The partial powers deserve their own treatment. Switching costs for passengers are essentially zero in consumer aviation—no leisure traveler feels "locked in" to AirAsia in the way a Windows user feels locked in to Microsoft. But the AirAsia MOVE loyalty ecosystem is attempting to build modest switching costs through points, frequent-flyer benefits, and integrated travel products. It is partial. Process power—the organizational muscle memory that allows an operator to execute at cost levels competitors cannot match—probably exists at AirAsia X as well, built painfully over twenty years, but is never cited as a differentiator because nobody wants to advertise that their ability to turn a plane in thirty-five minutes is a company secret.

Branding as a power is interesting because AirAsia is one of the most recognized consumer brands in Southeast Asia, but premium pricing—the classic manifestation of brand power—is not really available in the LCC segment. AirAsia charges what the market pays. Its brand drives share, not price. Counter-positioning as a power was genuinely present in the 2003–2013 era when AirAsia operated outside the economic frame of full-service carriers. Today, with LCCs normalized and even legacy carriers running their own budget subsidiaries, the counter-positioning edge has significantly eroded.

Turning to Porter's Five Forces, the picture is similarly mixed but generally favorable on balance. The threat of new entrants in long-haul low-cost is, empirically, low. Capital intensity is enormous—a wide-body Airbus A330neo carries a list price of roughly $300 million, though lease economics moderate this considerably. Regulatory barriers are meaningful: Malaysia's Air Operator Certificate regime, bilateral air services agreements that gate international routes, and slot-pair allocation at congested airports all combine to create a regulatory moat. And the graveyard itself is a barrier. Every prospective LHLC entrant must confront the history that precedes them.

The bargaining power of buyers—airline passengers—is structurally high. Price sensitivity in leisure travel approaches elastic, consumers freely comparison-shop across Skyscanner and Google Flights, and switching carriers is costless. But this force is meaningfully moderated by the MOVE ecosystem, the brand's emotional recognition in ASEAN, and the network effect of the hub-and-spoke model.

The bargaining power of suppliers in aviation is always a nuanced picture. Aircraft manufacturers—Airbus and Boeing—are effectively a global duopoly, and their pricing power on list prices is substantial. But major fleet customers like AirAsia X, with orders in the hundreds, negotiate delivered prices that bear little relation to list. Jet fuel suppliers are commodity producers with zero pricing power, though fuel prices themselves are the greatest single operational risk. Labor has moderate power through organized pilot associations and cabin crew unions, though Malaysian labor markets remain less adversarial than European or American equivalents.

The threat of substitutes is real but bounded. For intra-ASEAN short-haul routes under three hours, high-speed rail—where it exists—and ferry networks compete. For long-haul routes, there is no real substitute; Kuala Lumpur to Seoul is a fourteen-hour bus ride through impossible geography.

The intensity of rivalry is the most competitive of the five forces. Malaysia Airlines, the flag carrier, operates a full-service long-haul network to overlapping destinations. Singapore Airlines' Scoot subsidiary targets the exact same mid-haul Asian market with a modern wide-body fleet. Thai AirAsia X, operated by a separate corporate group, competes on some routes. Chinese carriers—particularly the big three and aggressive regional players like Juneyao—have expanded aggressively into ASEAN. IndiGo from India is increasingly pushing into Southeast Asia. This is not a protected market. Every incremental percentage point of load factor has to be fought for.

What makes AirAsia X's competitive position durable is not the absence of rivalry. It is the specific combination of lowest-in-class CASK, brand, and network effect operating in a market where most rivals are either full-service carriers structurally unable to match the cost base, or LCCs that lack the scale and brand to match the network. The power stack is real, but it requires continuous reinvestment to preserve.

VIII. Playbook: Business & Investing Lessons

The most useful lessons from AirAsia X are the ones that generalize beyond aviation, because the temptation to treat the company as a narrow case study in airline management misses what is actually interesting about the story. Four lessons, in particular, stand out.

The first is the lesson of asset-light flexibility in capital-intensive industries. The conventional management wisdom in aviation, for most of the post-deregulation era, was that fleet ownership versus leasing was a capital structure question with minimal strategic significance. What the pandemic exposed—and what AirAsia X's restructuring demonstrated—is that the asset structure fundamentally determines survivability in a tail-risk scenario. Airlines with heavy owned fleets carried sunk costs they could not shed. Airlines with aggressive operating lease books could, in extremis, return aircraft and shrink their cost base in ways owned-fleet operators could not. The restructuring outcome at AirAsia X was possible only because most of the pre-pandemic fleet was on leases that could be renegotiated or surrendered through the court process. The lesson generalizes: in industries with severe demand cyclicality, the value of optionality in asset structure is routinely underpriced until a crisis reveals it.

The second lesson is the durability of brand equity even through technical insolvency. AirAsia as a consumer brand survived a multi-billion-ringgit debt restructuring with essentially no damage to customer perception. The first post-pandemic passenger booking a flight to Seoul did not know or care that the operating entity's balance sheet had been reconstituted. This is almost the opposite of how brand equity behaves in certain other industries—consider how dramatically Lehman or Arthur Andersen disappeared after their respective corporate failures. Consumer brands appear to be more resilient to balance-sheet events than institutional or B2B brands, and in cyclical industries this creates an option value for brand owners that tends to be systematically underappreciated during normal operating periods.

The third lesson concerns M&A as a structural cleanup tool. The "One AirAsia" consolidation is not primarily a scale play or a synergy play, though it has elements of both. It is fundamentally a corporate simplification play—collapsing two listed PN17-legacy entities into one coherent vehicle in a way that makes the equity investable again for mainstream institutional investors. This use of M&A, where the strategic logic is legibility rather than growth, is relatively underappreciated in business school case studies. It is also extremely common in markets with complex cross-holdings, which describes most of Asia-Pacific, Latin America, and European conglomerates.

The fourth and most provocative lesson is the LHLC paradox—why AirAsia X succeeded where Norwegian failed, where Oasis failed, where Skytrain failed. The thesis here is somewhat counterintuitive. Norwegian's long-haul failure is typically attributed to operational execution—the Dreamliner reliability issues, the aggressive expansion, the fuel hedging losses. All of that happened. But the deeper cause was strategic overreach: Norwegian attempted to operate long-haul low-cost to destinations where it had no short-haul feeder network, no recognized brand, and no consumer flywheel. New York to Paris. Bangkok to Los Angeles. London to Austin. Each route was treated as an independent commercial proposition competing against established legacy carriers with loyalty programs, distribution, and premium cabins.

AirAsia X succeeded, paradoxically, through concentration rather than diversification. Its long-haul network is narrow—a concentrated fan of routes from Kuala Lumpur and secondary Asian hubs—and its feeder is massive. The LHLC business only works when it is embedded in a short-haul ecosystem that can provide incremental passengers, share brand marketing, and absorb cyclical shocks. Freddie Laker had no feeder. Norwegian's short-haul business was European; its long-haul was transatlantic; the networks barely intersected. AirAsia X's feeder and long-haul networks are the same brand serving the same customers across the same geography. The model only scales when the networks are genuinely coupled.

The investment implication, for those thinking about similar opportunities in other industries, is that hybrid business models with embedded distribution advantages are systematically undervalued by investors who model them as the sum of their parts. AirAsia X as a standalone long-haul airline would be worth considerably less than AirAsia X as the long-haul component of an integrated low-cost ecosystem. The One AirAsia consolidation makes this integration explicit on a single balance sheet for the first time. What happens to the equity valuation when the market fully internalizes that shift is the central question every analyst covering the name is wrestling with.

IX. Analysis & Bear vs. Bull Case

No honest analysis of AirAsia X reaches a conclusion that does not preserve substantial ambiguity. The bear case is serious. The bull case is also serious. Both rely on specific assumptions about factors largely outside management's control, and the honest investor's job is to weigh them rather than resolve them.

The bear case starts with fuel. Jet fuel is typically the single largest operating cost for any airline, and for a low-cost carrier operating wide-bodies on long sectors, it can approach 40% of total operating expense when prices spike. AirAsia X hedges a portion of its fuel exposure, but the structural long position is enormous. A sustained $30 per barrel increase in crude oil could compress operating margins by a measurable percentage of revenue. The 2022 fuel crisis, triggered by the Russia-Ukraine conflict, caused meaningful earnings pain across the global airline industry; a repeat under a more fragile balance sheet would be painful. The company's ability to absorb fuel spikes depends heavily on whether demand remains resilient enough to pass costs through to passengers, and in the budget segment, that demand elasticity works against the operator.

Key-man risk is the second serious bear concern. Tony Fernandes and Kamarudin Meranun have built AirAsia over more than two decades, and their involvement—through Tune Group, through Capital A, through the informal political capital they command with ASEAN governments—is structurally embedded in the entire platform. Neither founder is young. Succession planning, while publicly discussed, has not been tested. A sudden departure of either founder through health or retirement would trigger material uncertainty about the direction of strategic decisions and the management of the key external relationships that have been essential to the network's development.

Geopolitical sensitivity on China and India routes is the third bear concern, and one that has grown in importance. A significant portion of AirAsia X's post-pandemic growth has been in North Asian and South Asian routes. Routes to major Chinese cities generate substantial load factors during normal periods, but they are also subject to bilateral aviation agreement dynamics, potential pandemic-related restrictions, and occasional diplomatic frictions that can compress demand abruptly. Routes to India are similarly vulnerable to regulatory changes in Indian aviation policy, tax regime shifts affecting outbound leisure travel, and competitive pressure from rapidly expanding Indian carriers.

Balance sheet fragility, while dramatically improved from the 2021 trough, remains a concern. The restructuring extinguished legacy liabilities, but the combined One AirAsia entity will take on its own capital structure commitments to fund fleet renewal, aircraft acquisition, and integration. The Malaysian ringgit's volatility against the U.S. dollar—the currency of most aircraft lease payments and a significant portion of fuel—creates translation exposure that has historically been painful during ringgit weakness.

Integration risk from the One AirAsia consolidation is the fifth bear concern and the most timely. Airline mergers have a historically poor track record. IT system integration is genuinely difficult. Union dynamics, even in less adversarial labor environments, introduce friction. The period between announcement and completion is a distraction from operational execution. Management's stated confidence that this integration is "different" because of the shared brand and ownership is plausible but not yet tested in execution.

Turning to the bull case, the counterargument is fundamentally structural. The consolidated AirAsia Group, post-integration, is arguably the only entity in Southeast Asia that has a genuine lowest-cost-producer position across both short-haul and long-haul segments, a continent-wide consumer brand, a digital distribution platform that bypasses the expensive global OTAs, and a fleet plan that has been stress-tested through the worst aviation crisis in seventy years. If ASEAN air travel grows at its widely-projected mid-to-high single digit annual rate through the late 2020s, the combined entity captures a disproportionate share of that growth on unit economics competitors cannot match.

The bull thesis also depends on a particular view of demand resilience. Asian middle-class growth, urbanization, rising outbound leisure travel, and the structural shift in travel preferences toward experience-based consumption all point to sustained demand tailwinds for budget aviation. The corridor of markets AirAsia X serves—four-to-seven-hour flights from Kuala Lumpur to the demographic centers of East and South Asia—represents several billion potential customers at various stages of discretionary income growth. The comparison sometimes used internally is Ryanair in European aviation—a business that, over several decades of operation, compounded free cash flow through relentless cost discipline and gradual share gains. If AirAsia Group becomes the "Ryanair of Asia" even in a diluted form, the eventual cash flow profile is substantial.

The fleet plan targets are material to the bull case. Management has publicly committed to aggressive aircraft deliveries over the next several years, with orders in the hundreds of A321neo-family and A330neo aircraft pending with Airbus. If these deliveries occur on time and are absorbed into profitable routes, the operating leverage is significant. If they are delayed, or if weaker-than-expected demand turns them into excess capacity, the same fleet plan becomes a balance sheet weight.

Dividend potential is an explicit part of the bull story. Management has signaled that once the integration stabilizes and the post-restructuring net debt position is reasonable, returning capital to shareholders becomes a priority. For a stock that essentially offered no dividend yield through most of the 2020s, the future income profile is a potential re-rating catalyst, though the exact timing is heavily dependent on fuel prices, integration costs, and fleet capex.

Applying the 7 Powers and Porter's Five Forces frameworks summarized earlier, the bull case is effectively the argument that scale economies, network economies, and cornered resources combine to produce a durable cost and distribution advantage that persists through a cycle. The bear case is the argument that the competitive intensity of aviation, combined with fuel volatility and execution risk, erodes those advantages faster than management can exploit them. Both views are internally consistent.

Three KPIs matter above all others for tracking whether the thesis—bull, bear, or somewhere in between—is playing out over the next several reporting periods. The first is RASK, revenue per available seat kilometer, which captures whether the network is generating premium yield through the combination of connecting traffic and ancillary revenue, or whether pricing competition is degrading the economics. The second is ancillary revenue per passenger, which captures whether MOVE and the unbundled product strategy are actually deepening monetization beyond the ticket. The third is fleet integration progress—specifically the percentage of combined fleet operations consolidated onto a single operational platform after the One AirAsia closing—which captures whether management is executing the integration on its stated timeline.

X. Epilogue & Final Reflections

There is a particular moment in every Acquired.fm deep dive where the analysis, however rigorous, gives way to something more reflective—an attempt to say what the story actually means. With AirAsia X, that meaning is unusually specific, and it has to do with the nature of survival in capital-intensive, cyclical industries.

The version of AirAsia X that existed in 2019 was a promising, ambitious, slightly over-extended airline executing a distinctive strategy in a market segment most operators had failed to crack. Under any normal macroeconomic scenario, it would have continued growing, continued refining its route network, continued trading as a mid-cap Malaysian aviation equity, and continued operating within the orbit of its short-haul parent. A garden-variety success story.

The version of AirAsia X that exists in 2026 is something different. It is a company that went through corporate death and returned with a clarified purpose and a restructured liability stack. The executives running it have done something very few management teams ever get the chance to do: rebuild an enterprise from its foundations while retaining its brand and customer base. The strategic decisions they are making—the route rationalization, the focus on the Asian mid-haul "fat middle," the aggressive absorption of the short-haul parent, the careful cultivation of Teleport, MOVE, and ADE—all reflect lessons learned expensively.

Whether this produces what management aspires to become—a consolidated Asian aviation group with the unit cost profile of Ryanair, the network density of Southwest, the ancillary monetization of the global LCC pioneers, and the long-haul reach of a genuine international flag carrier—depends on execution over the next several years. The ambition of becoming what Fernandes has sometimes called "the Ryanair of Asia, connecting East and West through Kuala Lumpur" is real. It is also a substantial commitment that will be tested by fuel prices, by competitive dynamics, by geopolitics, and by the quiet grind of integrating two aviation businesses into one.

The broader significance of the story extends beyond Malaysian aviation. In every industry where cyclicality meets capital intensity—shipping, commodities, heavy manufacturing, semiconductors at certain cycles—the companies that survive downturns intact and execute consolidations during recovery periods are often the ones that end up capturing disproportionate long-term value. AirAsia X is a particularly vivid case study because the downturn was so severe, the restructuring was so aggressive, and the post-crisis consolidation was so strategically audacious. Most companies that experience near-death events do not re-emerge as the consolidating vehicle for their former parent. The corporate geometry of that outcome is genuinely rare.

For Tony Fernandes and Kamarudin Meranun, the two former record-industry executives who bought an airline for one ringgit twenty-five years ago, the journey has been a study in founder resilience. They built a business. They watched it nearly die. They rebuilt it. They reorganized it. They are now handing substantially more of the operational work to a specialist management team while retaining the strategic and political influence that only founders tend to accumulate. The transition from founder-led to founder-influenced is a transition most companies manage badly. AirAsia X appears, so far, to be managing it reasonably well.

For Benyamin Ismail and the rest of the current operating team, the job ahead is less about vision and more about execution. The vision has been articulated. The corporate structure has been simplified. The debt has been restructured. The fleet plan is in place. What remains is the long, disciplined, unglamorous work of running a very large airline very efficiently for a very long time. That work does not produce dramatic headlines. It produces compound earnings, if it produces anything at all.

What began in 2001 with a handshake over a one-ringgit purchase of a struggling airline has become, in 2026, a consolidated regional aviation platform operating at scale, with a clean balance sheet, a restructured shareholder base, and a strategic vision that has survived a global pandemic and a corporate near-death experience. Whether it becomes the dominant low-cost consolidator of Asian aviation in the decades ahead or settles into a role as one of several successful regional operators is a question that the next five years of fuel prices, passenger demand, and operational execution will answer.

The phoenix metaphor that opened this episode is easy to overuse, but in this case it is essentially literal. An airline was extinguished. Its legal and financial architecture was rebuilt around the surviving brand and operating know-how. The entity that now flies under the AirAsia X ticker is not quite the same company that entered the pandemic. It is both more and less—more disciplined, more focused, more strategically clear; less extended, less over-optimistic, less burdened by legacy commitments. Whether this particular rebirth results in the emergence of a genuinely category-defining Asian aviation franchise, or simply a better-run version of what was already there, is the central open question.

What is not open to question is that the story of how it got here—from a record-label executive mortgaging his house, to a handshake in a Malaysian boardroom, to a hibernating fleet wrapped in plastic at KLIA, to a 99.9% creditor haircut, to the corporate inversion of a listed holding structure—is one of the more remarkable chapters in modern aviation history. For investors, for operators, for anyone interested in how durable businesses get built in unforgiving industries, AirAsia X is a case study worth studying. For the traveler boarding an A330 at KLIA tomorrow morning with a cheap ticket in hand, it is simply the airline that made long-haul flying affordable. Both descriptions are correct. Both descriptions are part of what makes the story worth telling.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube