Otsuka Holdings: The "Dual-Track" Giant of Global Healthcare

I. Introduction & Episode Roadmap

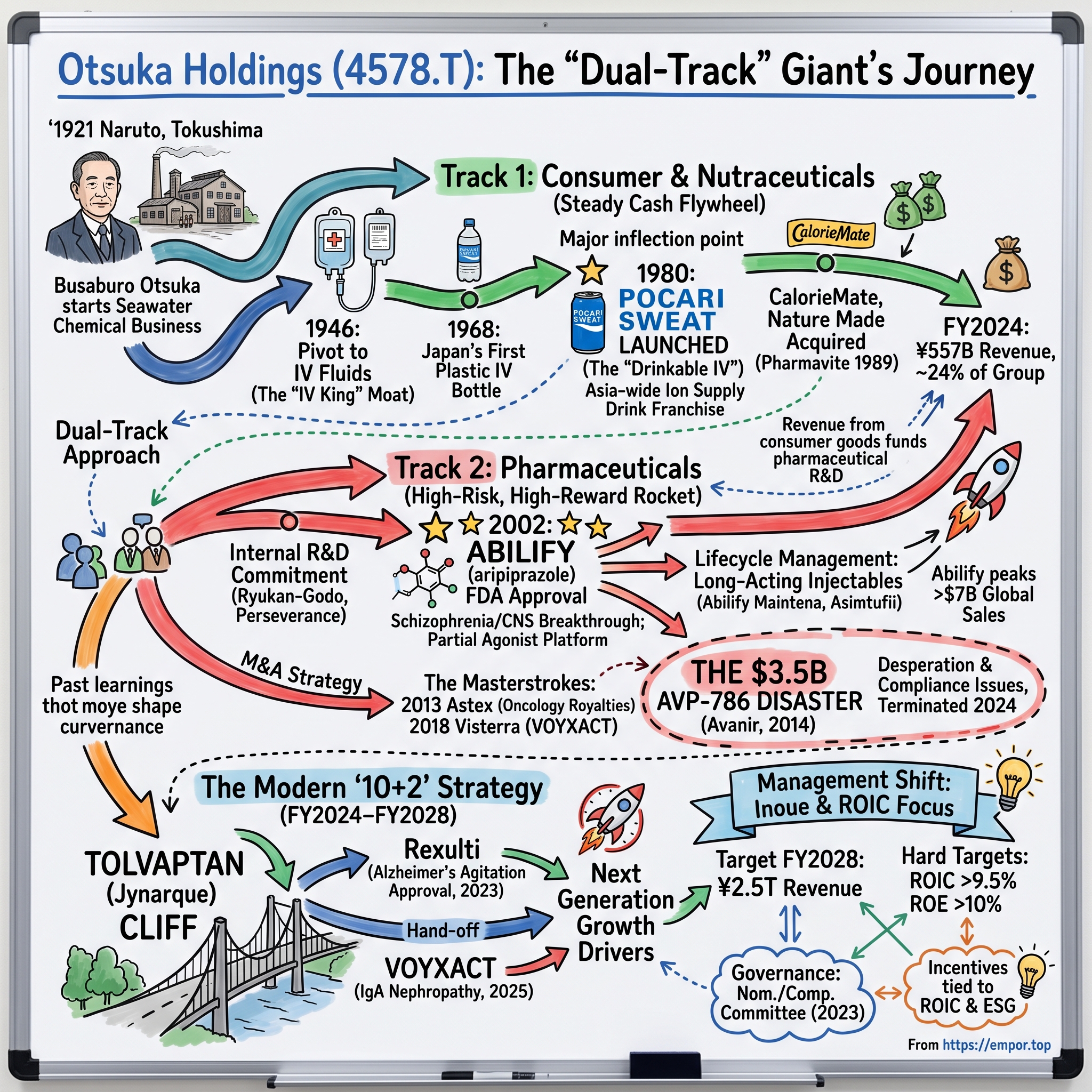

Stand on the seawall at Naruto, in Tokushima prefecture (徳島県鳴門市) on the eastern edge of Shikoku, and you can watch the tide rip through the strait between the island and Awaji in whirlpools the size of city blocks. In 1921, this was one of the more inconvenient corners of Japan to build a business — far from Tokyo, far from Osaka, far from anything except the sea. Yet it was here, boiling seawater to extract industrial chemicals, that a man named Busaburo Otsuka (大塚 武三郎) started a company that would, more than a century later, sell psychiatric drugs in Manhattan and sports drinks in Jakarta and generate revenue of ¥2.33 trillion in a single fiscal year.1

That is the first thing to understand about 大塚ホールディングス Otsuka Holdings Co., Ltd. (4578.T), listed on the 東京証券取引所 Tokyo Stock Exchange and today carrying a market value of roughly ¥6 trillion: it does not fit any of the boxes investors like to sort healthcare companies into.12 It is not a sleepy Japanese generics house grinding out low-margin infusions. It is not a pure-play biotech living and dying on a single molecule. And it is not a consumer-goods company dressed up in a lab coat. It is all three at once — a genuinely unusual "dual-track" operator that runs a high-risk, high-reward innovative-drug engine alongside a stable, cash-gushing consumer nutrition business, and uses the second to pay for the first.

The paradox is the whole story. In the pharmaceutical world, the recurring nightmare is the "patent cliff" — the day a blockbuster loses exclusivity and 80% of its revenue evaporates into generic competition within a year. Most drug companies answer that terror by getting bigger, merging their way out of the problem, or borrowing against the future. Otsuka answered it differently: it built a second business selling Pocari Sweat (ポカリスエット), CalorieMate (カロリーメイト), and vitamins, whose steady, non-cyclical cash flow could bankroll the decade-long, mostly-failing science of inventing new medicines. Whether that dual-track structure is a durable competitive advantage or simply an unusually elegant way of subsidizing risk is one of the questions this story will keep testing.

There is a useful way to hold the whole company in your head. Think of Otsuka as two engines bolted to one chassis. The first engine — consumer nutrition — is a flywheel: heavy, slow, hard to start, but once spinning it stores energy and keeps turning through storms. The second engine — pharmaceutical innovation — is a rocket: capable of extraordinary thrust, but temperamental, expensive to fuel, and prone to blowing up on the launch pad. Most healthcare companies choose one or the other, because the temperaments required to run them are opposites. Consumer businesses reward patience, brand-building, and pennies of margin defended over decades. Drug businesses reward scientific conviction, tolerance for serial failure, and the willingness to spend a billion dollars on a molecule that may never reach a patient. Otsuka's central bet, sustained for a century, is that one company can house both temperaments at once — and that each makes the other stronger. The consumer flywheel steadies the group when a trial fails; the rocket gives it the growth a beverage company could never achieve alone.

Four themes run through what follows. The first is the "drinkable IV" — how mastering sterile hospital infusion fluids led, by a strange act of translation, to one of Asia's most iconic beverage franchises. The second is the dopamine stabilizer — Otsuka's lonely, decades-long journey to invent Abilify (aripiprazole), which became one of the best-selling psychiatric drugs in history. The third is the capital-allocation dichotomy — a company capable of both the Astex masterstroke and the $3.5 billion Avanir disaster, sometimes within the same few years. And the fourth is the modern transformation — the attempt by current chief executive Makoto Inoue (井上 眞) to drag a proud, founder-influenced Japanese group toward the harder discipline of return on invested capital.4

The scale of what that founding produced is worth sitting with for a moment. A company that began by extracting chemicals from seawater in one of Japan's quieter prefectures now operates a pharmaceutical business selling across the United States, Europe, and Asia; a consumer-nutrition franchise with iconic brands; and a research pipeline spanning psychiatry, nephrology, oncology royalties, and rare metabolic disease. Its FY2024 revenue of ¥2.33 trillion grew more than 15% year on year, and its net profit nearly tripled, powered by the pharmaceutical engine.1 Those are not the numbers of a sleepy legacy firm coasting on old products. They are the numbers of a company in the middle of one of the more consequential transitions in its history — swapping out aging blockbusters for a new generation of drugs while a new management team tries to rewire how it thinks about capital. Whether that transition succeeds is the live question that makes the company interesting right now, rather than merely storied.

A note on posture before we begin. Otsuka's own materials tell a triumphant story, and much of it is genuinely earned. But this is not an investor-relations document. Where management says it will win, the useful question is always: what evidence supports that, and what would prove it wrong? Keep that lens handy, because Otsuka is a company that has been spectacularly right and expensively wrong, and both instincts are still very much alive inside it. To see how they got here, start at the water's edge.

II. The Salt, the Sea, and the Sterile Bag: Origins of Otsuka (1921–1970s)

Busaburo Otsuka was not chasing a grand vision when he founded Otsuka Seiyaku Kogyobu (大塚製薬工業部) in 1921. He was chasing magnesium carbonate. The Naruto coast had two things in abundance — seawater and the salt-making tradition that came with it — and the byproducts of salt production could be refined into inorganic chemical raw materials that Japan's growing industrial base needed.2 It was an unglamorous, commodity business: extract, purify, sell by the ton. For its first quarter-century the company was a regional chemical supplier, and there was little in that to suggest what came next.

To understand why that beginning mattered, place it in the Japan of the 1920s and 1930s — a country industrializing at breakneck speed, importing many of the chemical inputs its factories needed, and eager for domestic substitutes. A regional producer of inorganic chemicals extracted from a local, renewable resource was a sensible, if modest, enterprise. It taught the young company two things it would never unlearn: how to run a purification-and-refining process at industrial scale, and how to build a business in a place the rest of corporate Japan overlooked. Tokushima was, and remains, one of the country's less populous prefectures, and Otsuka's persistence in headquartering and manufacturing there — rather than decamping to Tokyo — became part of its identity. This was a company comfortable being provincial, patient, and self-reliant, traits that would later look like competitive advantages when the industry rewarded exactly those qualities.

What came next was catastrophe and reinvention. Japan emerged from the Second World War physically shattered and medically desperate; basic clinical supplies were scarce, and the country's hospitals lacked something as fundamental as reliable intravenous fluids — the sterile saline and nutrient solutions that keep a dehydrated or post-surgical patient alive. In 1946, the second-generation leader Masahito Otsuka (大塚 正士) made the decision that turned a chemicals firm into a healthcare company: he pivoted the war-battered business toward clinical nutrition, manufacturing intravenous injection and infusion solutions.2 It was a bet on the most basic medical need imaginable, and it was rooted in a physical-chemistry competence the company already had — making things sterile, pure, and consistent at scale.

Here is where the economics get interesting, because IV fluid is a deceptively hard business. The product is mostly water. Its value per kilogram is low, it is heavy to ship, and it must be manufactured and delivered under absolute sterility, because a contaminated infusion bag can kill. That combination — low value, high weight, zero tolerance for error — means the whole game is logistics and regional density. Whoever can manufacture sterile fluid cheaply and deliver it reliably to every hospital in a region wins, and no distant competitor can easily undercut them, because the freight cost of shipping water across the country erases any manufacturing edge. Otsuka understood this instinctively. It built out regional distribution, tied itself into Japan's hospital system, and became the undisputed "IV King" of the country — a position it has never surrendered.

It is worth pausing on how counterintuitive this advantage is, because it inverts the usual logic of pharmaceutical value. In most of medicine, value concentrates in the molecule — the patent-protected compound that took a decade and a fortune to discover, and that can be manufactured almost anywhere once the recipe is known. IV fluid is the opposite. There is no secret chemistry in saline; the "product" is a manufacturing-and-distribution system so reliable that a hospital will stake a patient's life on it and never think twice. The value lives in the physical network, not the formula. That distinction shaped Otsuka's DNA in a way that still matters today: the company learned, from its earliest profitable business, that owning the hard-to-replicate delivery system can be worth more than owning the idea. It is a lesson most drug companies never learn, and it explains why Otsuka has always been as much an operations company as a science company.

The moat was reinforced by industrial design, and this is a detail that reveals the company's engineering character. In 1968, Otsuka introduced Japan's first plastic polyethylene bottle for IV solutions, replacing the heavy, breakable glass vials that had been standard.[^3] It sounds trivial. It was not. Glass shattered, it was heavy to transport, and cleaning and reusing it introduced contamination risk. A lightweight, single-use plastic container was safer, cheaper to ship, and easier to handle at the bedside. Then in 1995 the company went further, developing a multi-chamber bag system that stored incompatible components — amino acids in one chamber, glucose in another — separately, so a nurse could break the internal seal and mix them at the moment of infusion rather than in advance.[^3] Each innovation deepened Otsuka's grip on the clinical-nutrition market by making its products the safe, obvious default.

The multi-chamber bag deserves a moment more, because it is a perfect miniature of how Otsuka thinks. The clinical problem it solved was mundane and dangerous at once: certain nutrients a patient needs — amino acids and concentrated glucose, for instance — react badly if stored together for long periods, yet mixing them by hand at the bedside introduced exactly the contamination risk that kills vulnerable patients. Otsuka's answer was not a new drug but a better container: two sealed chambers, one frangible internal seal, and a nurse's single firm squeeze to combine them sterile at the moment of use. It removed a step, removed a risk, and removed a reason to ever switch suppliers. This is the pattern to watch throughout Otsuka's history — the company repeatedly wins not by out-discovering rivals but by engineering the friction out of a clinical routine, so that its product becomes the path of least resistance for the people at the bedside.

Out of this era came a corporate culture that still shapes how Otsuka talks about itself. Three phrases recur in its literature: Ryukan-godo (流汗悟道, roughly "by sweat we recognize the way") — the belief that real R&D comes from hard, persistent, often manual effort rather than flashes of genius; Jissho (実証, "actualization") — the demand that ideas be proven in reality; and Sozosei (創造性, "creativity").2 It is easy to dismiss corporate philosophy as decoration, but these particular slogans map onto real behavior: a willingness to grind on a single scientific problem for a decade, and a taste for products that are physically hard to make. Both traits were about to produce something no infusion company had any business inventing — a beverage.

III. The "Drinkable IV Fluid": How Pocari Sweat Built the Nutraceutical Empire

The origin of Pocari Sweat reads like corporate folklore, and like most folklore it is worth telling because it captures a real strategic instinct. In the late 1970s, an Otsuka researcher named Rokuro Harima fell seriously ill while traveling in Mexico and became badly dehydrated. Recovering in a hospital, he reportedly watched — or heard of — a doctor rehydrating himself by drinking the contents of a medical IV bag, using the sterile electrolyte solution the way an exhausted person might reach for water. The question that came out of that scene was deceptively simple: if the body's fluid loss through sweat is essentially the same problem an IV drip solves, why can't we make a drinkable IV solution that actually tastes good, for everyday replenishment?3

For most beverage companies that question would have been unanswerable. For Otsuka it was almost a home game, because the company had spent thirty years studying exactly how to balance electrolytes and ions in solutions the human body would accept. The team set out to replicate the electrolyte and ion balance of human plasma in a drink — sodium, potassium, magnesium, calcium, in the proportions the bloodstream actually uses. The science was tractable. The taste was a nightmare. Faithfully reproducing plasma chemistry produced a liquid that was bitter and faintly metallic, because the magnesium and potassium the body needs taste terrible. The breakthrough, after a reported thousand-plus failed iterations, was almost humble: blending the formula with citrus juice to mask the bitterness, trading a little physiological purity for something a person would actually choose to drink twice.3

When Pocari Sweat launched in 1980, Otsuka made a marketing decision that looks obvious in hindsight and was contrarian at the time: it deliberately refused to position the drink as medicine.3 It could have sold it through pharmacies as an oral rehydration therapy. Instead it framed it as an everyday "ion supply" beverage — something you drink after sport, after a bath, on a hot commute, not because you are sick but because you sweat. That reframing converted a narrow clinical product into a mass-market habit, and it built a category ("ion supply drinks") that Otsuka then dominated across East and Southeast Asia. The pale-blue can became a generational icon in markets from Japan to Indonesia.

The expansion strategy that followed is a study in patience. Rather than storming Western supermarkets — where "sweat" on a label was a marketing headache and Coca-Cola and PepsiCo owned the shelves — Otsuka concentrated on East and Southeast Asia, markets where hot, humid climates made the functional case for an electrolyte drink obvious and where Western beverage giants were less entrenched. It built local manufacturing, invested in decades of "science of hydration" education, and let the brand become part of daily life in places like Indonesia, where Pocari Sweat became a genuine cultural staple rather than an imported curiosity. This was distribution-and-density thinking imported straight from the IV business: win a region deeply before spreading thin, and make the product a habit rather than an impulse. The payoff was a consumer franchise with the kind of local entrenchment that is very hard for a latecomer to dislodge.

The consumer portfolio widened from there, and each addition rhymed with the original logic of selling function backed by science. CalorieMate, launched as a compact, balanced "block" of calories and nutrients, targeted the same everyday-functional niche as Pocari Sweat but for eating rather than drinking. SOYJOY carried a soy-based nutrition story; EQUELLE extended into women's health around soy-derived compounds for menopausal symptoms. And in 1989 Otsuka bought the American vitamin maker Pharmavite, owner of the Nature Made brand — a move that gave it a major position in the enormous US dietary-supplements market and turned the nutraceutical arm from a Japanese story into a genuinely international one. What unites this grab-bag of products is not a category — drinks, snacks, vitamins, women's health span very different shelves — but a posture: health-adjacent consumer goods sold on functional benefit and clinical credibility, riding the same "we understand what the body needs" authority the company earned making IV fluid.

Today that instinct underpins an entire business segment. Otsuka's Nutraceutical division — Pocari Sweat, the calorie-block snack CalorieMate, the soy-based SOYJOY (ソイジョイ), the women's-health line EQUELLE, and Nature Made vitamins from the US firm Pharmavite it acquired in 1989 — generated ¥557.0 billion of revenue in FY2024, roughly 24% of the group, and ¥64.1 billion of business profit.1 Those figures matter less as trophies than for what they enable. Consumer nutrition is non-cyclical: people buy sports drinks and vitamins in good times and bad, with no patent cliff and no FDA panel able to erase the franchise overnight. That reliability is the financial ballast of the whole enterprise.

There is a subtler benefit to the nutraceutical engine that pure financial figures understate: it keeps Otsuka in daily contact with hundreds of millions of ordinary consumers, and that relationship has strategic value beyond the cash it throws off. A company that sells a beloved beverage across Asia has brand permission, distribution relationships, and consumer trust that a pure drug company lacks entirely. It also has a natural bridge between "wellness" and "medicine" — the exact territory where health-conscious consumers, aging populations, and preventive care increasingly overlap. Whether Otsuka fully exploits that bridge is debatable; skeptics would argue the two halves of the company operate more as separate silos than as a genuinely integrated whole. But the optionality is real, and it is the kind of asset that does not appear on a segment income statement.

Here is the analytical point, and it is the crux of the entire Otsuka thesis. A pure-play biotech lives in permanent existential jeopardy: one failed Phase III trial or one patent expiry can gut it. Otsuka bolted a stable consumer cash machine onto its risky drug-discovery engine, so that the years-long, mostly-failing work of inventing medicines is bankrolled by people buying blue cans on hot afternoons. Whether that makes Otsuka a more durable compounder or simply a diversified conglomerate trading at a "conglomerate discount" is a genuine debate — diversification can dampen risk and dampen returns at the same time. But the mechanism is real, and it is what let a company from Naruto go hunting for one of the hardest prizes in medicine: a better drug for schizophrenia.

IV. The DSS Breakthrough: Discovering Abilify and Redefining Psychiatry (1980s–2015)

To appreciate what Otsuka's chemists were attempting, you have to understand the trap that psychiatry had been stuck in for decades. Schizophrenia's most visible symptoms — hallucinations, delusions, the so-called "positive" symptoms — were understood to involve too much dopamine signaling in certain brain circuits. The obvious fix was to block dopamine, and first-generation antipsychotics did exactly that, acting as brute-force dopamine D2 receptor antagonists. They worked, after a fashion. But shutting dopamine down across the brain caused devastating collateral damage: tremors and involuntary movements, the potentially permanent motor disorder tardive dyskinesia, and a worsening of the "negative" symptoms — the apathy, flatness, and withdrawal that leave patients unable to function. You could quiet the hallucinations and leave a person hollowed out. It was a terrible trade.

Otsuka's researchers, led by the chemist Yasuo Oshiro, chased a subtler idea: the Dopamine System Stabilizer, or DSS, hypothesis. The analogy that makes it click is a thermostat. A conventional antipsychotic is like ripping the heating system out of a house — it stops the overheating but leaves you freezing. What if, instead, you installed a thermostat that dialed dopamine down where it was pathologically high and up where it was too low? In pharmacology, the tool for that is a "partial agonist" — a molecule that binds the same receptor as dopamine but only partially activates it, so it behaves as a brake when dopamine is abundant and as a mild accelerator when dopamine is scarce. It is a genuinely different philosophy of treatment: stabilize the system rather than suppress it.

The molecule that embodied the idea, OPC-14597 — aripiprazole — was synthesized in 1987. It bound the D2 receptor with high affinity but only partial intrinsic activity, exactly the thermostat behavior the theory predicted. What followed was the long, grinding, mostly-invisible slog that the Ryukan-godo ethic romanticizes and that the income statement punishes: years of preclinical and clinical development on a mechanism many outsiders doubted. Otsuka was a mid-sized Japanese firm proposing to overturn the reigning model of antipsychotic action. Conviction, not consensus, carried it.

There is a deeper point buried in the DSS story about how a company can build a scientific franchise, not just a product. Aripiprazole was not a one-off; it became a platform. Once Otsuka had proven that a dopamine partial agonist could work in the clinic and be tolerated by patients, it had accumulated something rivals could not easily buy: deep, hard-won expertise in the chemistry and biology of a whole receptor-modulation strategy. That know-how seeded a family of related compounds and gave the company a durable home in central-nervous-system medicine — one of the hardest, highest-failure areas of drug development, and precisely for that reason one of the least crowded. Many large pharmaceutical companies actively retreated from psychiatry in the 2000s and 2010s, deterred by the difficulty of measuring symptoms, the placebo effect, and the regulatory risk. Otsuka leaned in. Being willing to work where others quit is itself a kind of moat, and it is one Otsuka chose deliberately.

It helps to translate the partial-agonist idea into something concrete, because it explains why the drug mattered clinically and not just commercially. Imagine a dimmer switch versus an on-off switch. Older antipsychotics were an off switch for dopamine — flick it and the room goes dark everywhere, including the rooms you needed lit. Aripiprazole behaved more like a dimmer that also sensed the ambient light: in the overlit rooms it dialed brightness down toward a comfortable middle, and in the too-dark rooms it nudged brightness up toward that same middle. The practical result was a drug that could calm the overactive dopamine driving hallucinations while causing fewer of the movement disorders and less of the emotional flattening that made older drugs so hard for patients to tolerate. Tolerability, in psychiatry, is not a luxury — it is the whole game, because a patient who cannot stand the side effects stops taking the drug and relapses. A medicine people will actually keep taking is worth far more than a marginally more potent one they abandon.

Conviction, though, does not sell drugs in America, and Otsuka lacked a large US sales force. So it made the move that defined the commercial side of the story: it partnered with Bristol Myers Squibb to co-promote the drug in Western markets, trading a share of the economics for BMS's enormous distribution muscle. Approved by the FDA in 2002 as Abilify, aripiprazole became a phenomenon, eventually peaking at over $7 billion in annual global sales and ranking among the best-selling pharmaceuticals in the world. For a company still best known at home for IV bags and sports drinks, it was a staggering validation — proof that Otsuka could invent, not just manufacture.

The Bristol Myers Squibb partnership deserves scrutiny as a business arrangement, not just a distribution convenience, because it embodies a trade-off Otsuka would make again and again. By co-promoting with BMS, Otsuka reached a scale in the US it could never have achieved alone, and it did so without the enormous fixed cost of building a nationwide sales force from scratch. The price was a shared economics — a partner's cut of one of the most valuable drugs of its era. For a mid-sized firm inventing above its weight class, that was a shrewd bargain: better a large share of a market you can actually reach than the whole of one you cannot. The pattern — invent the science, borrow the distribution — recurs across Otsuka's history, from BMS to Lundbeck to Novartis, and it reflects an honest institutional self-awareness about where the company's edge does and does not lie. Its edge is discovery and clinical development. Its historical weakness has been global commercial muscle, and it has consistently rented what it lacked.

But every blockbuster contains its own doomsday clock, and Abilify's was set for 2015, when oral aripiprazole would lose US exclusivity and generics would flood in. Otsuka's response is a case study in lifecycle management done well. Partnering with Denmark's Lundbeck, it developed long-acting injectable versions — Abilify Maintena, dosed once a month — that reformulated the same molecule into a product generics could not easily copy and that solved a real clinical problem: patients who stop taking daily pills relapse, and a monthly injection keeps them protected.[^12] In 2023 it pushed further with Abilify Asimtufii, a once-every-two-months formulation. The franchise built around aripiprazole still generated ¥237.9 billion in FY2024 — remarkable staying power for a molecule first synthesized in the 1980s.1 Yet Abilify also taught Otsuka a dangerous lesson: that the answer to a patent cliff is to go shopping. That lesson would soon cost it billions.

V. The M&A Playbook: Masterstrokes (Astex, Visterra) vs. The $3.5B Avanir Disaster

Every acquisitive company has a highlight reel and a blooper reel, and the honest way to judge management is to watch both. Otsuka's M&A record over the past fifteen years is unusually instructive precisely because it contains such vivid examples of each — brilliant, cheap, high-returning deals sitting a few years apart from an expensive, value-destroying one. Run them side by side and a pattern emerges about when Otsuka buys well and when it buys badly.

Start with the masterstrokes. In 2013, Otsuka acquired the British firm Astex Pharmaceuticals for roughly $886 million, buying a fragment-based drug-discovery engine and, crucially, a set of partnerships.7 Astex's platform fed into oncology programs that Novartis would commercialize, and the deal ultimately gave Otsuka a high-margin royalty stream tied to blockbusters like the breast-cancer drug Kisqali and the radioligand therapy Pluvicto. Royalties are the most beautiful revenue in pharma: no sales force, no manufacturing, no marketing spend — money that arrives because someone else sells your chemistry. Judged on cash returned versus price paid, Astex was a home run.

Then, in 2018, Otsuka paid about $430 million for the US biotech Visterra, acquiring an antibody-engineering platform and an early-stage molecule then known as sibeprenlimab.8 At the time it was a speculative bet on a program years from market. Seven years later that bet paid off spectacularly. After the FDA granted the molecule priority review in mid-2025 — a signal the agency saw it addressing a serious unmet need — the regulator granted accelerated approval in November 2025 to sibeprenlimab, now branded VOYXACT, for reducing proteinuria in adults with IgA nephropathy, a serious kidney disease with few good options.[^14]10 A $430 million purchase became a potential blockbuster and, as we will see, the designated successor to one of Otsuka's biggest current drugs. A more recent bet, the 2024 acquisition of the US biotech Jnana Therapeutics for $800 million upfront and up to $1.1 billion in total, brought in an oral therapy for the rare metabolic disorder PKU (phenylketonuria), which Otsuka advanced into a global Phase III trial in December 2025.9[^13] Its verdict is still unwritten — promising optionality, not a proven win.

What makes Astex and Visterra genuinely instructive is not just that they worked, but how they were structured. Both were relatively small checks — under a billion dollars each — written for platforms and early-stage assets years from generating revenue. Neither required Otsuka to overpay for a marketed, de-risked product at the peak of its visibility. Instead, the company bought scientific capability and optionality cheaply, then supplied the patience and the development capital to let the value mature over five, seven, ten years. That is textbook value-oriented dealmaking: pay for potential the market has not yet priced, and accept that some bets will fail while the winners pay for everything. The Astex royalty stream, in particular, is the kind of asset investors dream about — recurring, high-margin, and effectively free of the commercial risk that torments the rest of the drug business, because Novartis bears the cost of selling.

And then there is Avanir. In December 2014, Otsuka agreed to buy the California CNS company Avanir Pharmaceuticals for about $3.5 billion, a price that valued it at a steep premium.6 The logic was transparent and, in hindsight, revealing: with oral Abilify's cliff looming in 2015, Otsuka wanted more central-nervous-system assets, fast. Avanir offered Nuedexta, an approved treatment for a neurological condition called pseudobulbar affect, and a pipeline drug, AVP-786, being developed for agitation associated with Alzheimer's dementia — a huge unmet need. The premium was a bet on that pipeline.

Notice the structural contrast with Astex and Visterra, because it is the whole lesson. Those were small, early, cheap bets on capability. Avanir was a large, late, expensive bet on a specific pipeline outcome — and it was made at a moment of maximum strategic pressure, with a nearly $3.5 billion price tag that only made sense if AVP-786 hit. Otsuka paid a premium for a marketed product it partly wanted as cover and a pipeline asset it desperately needed to work. When a company pays top dollar for a single binary outcome under a deadline, it has effectively surrendered its margin of safety. That is not hindsight bias; it is the recognizable signature of an acquisition driven by need rather than opportunity.

The bet failed on two fronts, and the failure is worth dwelling on because it is the most honest thing in Otsuka's recent history. Scientifically, AVP-786 repeatedly missed its primary endpoints in Phase III trials, and in May 2024 Otsuka terminated the program outright — nearly a decade of development written off.[^12] Reputationally, the damage came sooner and dirtier: in 2019, Avanir paid more than $116 million to resolve US Department of Justice criminal and civil allegations that it had paid kickbacks to doctors and aggressively marketed Nuedexta off-label to elderly, often demented patients in nursing homes.[^7] Otsuka absorbed a compliance scandal along with the science that ultimately didn't work, and eventually dissolved the subsidiary, integrating its remnants in 2023. The lesson is not simply "Otsuka overpaid." It is why it overpaid: it bought Avanir from a position of anxiety, hunting for a CNS replacement as its own cliff approached. Desperation is the enemy of price discipline, and the contrast with the cheap, patient, unhurried bets on Astex and Visterra could hardly be sharper.

VI. The "Global 10 Plus 2" Era: Present Strategy & Portfolio Engine

Walk into an Otsuka investor presentation today and you will meet a piece of jargon that doubles as the company's entire growth strategy: the "Global 10+2." Behind the label sits the segment that actually drives the enterprise. In FY2024 the Pharmaceutical business recorded ¥1,629.0 billion of revenue — about 70% of the group — and ¥390.6 billion of business profit, an outsized 86% of consolidated business profit.1 In other words, nutrition provides the ballast, but drugs provide the horsepower. The margin gap tells the story: pharmaceuticals throw off far more profit per yen of sales than consumer products do, which is why the group's fate ultimately rides on its pipeline.

That 70/86 split — 70% of revenue but 86% of profit from pharmaceuticals — is the single most important number for understanding how to value Otsuka, and it cuts against the cozy "dual-track" framing in an important way. Yes, nutrition provides stability. But the group is, in economic terms, overwhelmingly a drug company with a large, steady consumer side business attached. When investors debate Otsuka's fair value, they are really debating the durability and pipeline of the pharmaceutical engine; the nutraceutical arm sets a floor and smooths the ride, but it does not drive the multiple. This matters because it clarifies where the risk actually lives. A bad year for Pocari Sweat would dent the group modestly. A failed pipeline transition in nephrology or neuroscience would hit the part of the business that generates the vast majority of profit. The consumer flywheel is insurance, not the growth story — and an investor who buys Otsuka mainly for its sports-drink stability is misreading the income statement.

The "10" refers to ten priority products Otsuka is pushing globally, and two of them anchor the current cash flows. Rexulti (brexpiprazole) is the company's leading central-nervous-system asset, generating ¥256.0 billion in FY2024.1 It is chemically a cousin of aripiprazole, but its strategic significance jumped in May 2023, when it won a genuinely historic FDA approval: the first-ever treatment cleared in the US for agitation associated with Alzheimer's dementia — the very indication AVP-786 had been chasing and failing to reach. That approval opened a large, previously untreated market with, at the time, no directly competing approved drug. It also illustrates a recurring Otsuka pattern: succeeding in a high-barrier neuroscience indication that most of the industry finds too hard and too risky.

The second anchor is tolvaptan, sold as Samsca and, in its kidney indication, as JYNARQUE, which generated ¥240.0 billion in FY2024.1 It is the nephrology crown jewel — the first and, for years, only drug approved to slow the decline of kidney function in autosomal dominant polycystic kidney disease (ADPKD), a genetic condition in which cysts progressively destroy the kidneys. For patients, slowing that march toward dialysis is transformative. For Otsuka, tolvaptan proved the company could build a franchise in nephrology, not just psychiatry — a second therapeutic home.

Rexulti's Alzheimer's-agitation approval rewards a closer look, because it is both a genuine achievement and a cautionary tale about how much of its promise is proven. Agitation in Alzheimer's dementia — the restlessness, aggression, and distress that torment patients and exhaust caregivers — is a large and heartbreaking unmet need, and being first to a US approval there is a real competitive coup. But "first with no direct competitor" is a claim about the label, not yet about the market. The commercial value depends on how widely physicians actually prescribe an antipsychotic to elderly dementia patients — a population where the entire drug class carries serious safety warnings — and on how payers reimburse it. The upside is real; so is the uncertainty about how large the real-world market becomes. A neutral observer holds both thoughts at once rather than accepting the bull framing that a first-mover label automatically equals a multi-billion-dollar franchise.

The "+2" are the royalty assets: Kisqali and Pluvicto, the Novartis-partnered oncology blockbusters inherited through the Astex deal, which funnel high-margin recurring royalties to Otsuka without the company lifting a commercial finger. And the "Next 8" is the pipeline meant to replace today's earners as their own cliffs approach. The headline name there is VOYXACT (sibeprenlimab), the anti-APRIL antibody for IgA nephropathy. Its role in the strategy is explicit and, frankly, load-bearing: tolvaptan faces its own loss of exclusivity, and Otsuka is counting on VOYXACT — freshly approved in late 2025 — to take the nephrology baton and carry the growth story forward.10

That hand-off is exactly where a skeptical investor should focus, because the entire "Global 10+2" narrative depends on newer drugs ramping faster than older ones fade. Otsuka has done this before — aripiprazole to Rexulti, injectables extending the franchise — but "we did it last time" is not proof of "we will do it again." Accelerated approvals can be narrower than full ones; a novel antibody has to win formulary access, physician habit, and payer reimbursement; and the market for an Alzheimer's-agitation drug is only as big as real-world prescribing turns out to be. The portfolio is genuinely strong. The execution risk in the transitions is genuinely real. Both things are true, which is precisely why the people running the company — and how they are paid — suddenly matter more than ever.

VII. The Modern Guardians: Inoue, Governance, and Capital Allocation

For most of its history, Otsuka was run the way many great Japanese companies were run — with a long-term, stewardship mindset, deep respect for the founding family's philosophy, and a balance sheet that erred heavily toward caution. That last trait had a cost that Japanese investors know well: the "cash-hoarding discount," the market's habit of valuing a company below the sum of its parts when it sits on idle cash and deploys capital without visible return discipline. The modern chapter of Otsuka's story is, at bottom, an attempt to shed that discount — and it is being written by two very different figures at the top.

The chief executive, Makoto Inoue, is an unusual choice to run a company whose profits come overwhelmingly from drugs, because he came up through the nutraceutical and consumer side of the house rather than the pharmaceutical labs.4 That background cuts two ways. Critics might worry that a consumer executive lacks the deep scientific instinct to allocate an R&D budget measured in the trillions of yen. But there is a case that it is exactly the right résumé for this moment: Inoue understands the defensive, cash-generative engine intimately, and the central strategic task now is not inventing the next molecule but allocating capital across a complex, dual-track group with discipline. Alongside him sits Ichiro Otsuka (大塚 一郎) as chairman — a grandson of the founder, embodying the family stewardship and the philosophical DNA that still runs through the organization.4 The pairing is deliberate: a professional operator on capital efficiency, a family guardian on continuity and culture.

The centerpiece of the new discipline is the 4th Medium-Term Management Plan, covering FY2024 through FY2028, and its numbers are worth reading not as promises but as a public scorecard investors can hold management to. The plan targets ¥2.5 trillion of revenue by FY2028 — a record — and, more tellingly, sets an explicit capital-efficiency goal of ROIC of 9.5% or more and ROE of 10% or more.45 Putting a hard return-on-invested-capital target in a medium-term plan is precisely the kind of behavior the old Otsuka avoided; it converts a vague commitment to "efficiency" into a measurable bar. The plan also frames a multi-year capital-allocation envelope of roughly ¥3.2 trillion, weighted heavily toward R&D (on the order of ¥1.5 trillion) and capital expenditure (around ¥500 billion), with the balance earmarked for M&A and shareholder returns.5

Numbers on a slide are cheap; incentives are what actually move behavior, and here Otsuka has made concrete changes. In April 2023 it established an independent Nomination and Compensation Committee — a governance upgrade that matters because it moves decisions about who runs the company and how they are paid away from purely internal hands.11 Executive compensation was restructured to pair base salary with short-term bonuses and restricted stock units tied to ROIC targets and to international ESG indices such as those from FTSE Russell.13 In plain terms, management now gets paid more when invested capital earns its keep — the exact metric a skeptic of Japanese cash-hoarding would demand.

There is a broader context that makes Otsuka's pivot more than a company-specific story. Over the past decade, Japan's corporate-governance reforms — the Stewardship Code, the Corporate Governance Code, and sustained pressure from the Tokyo Stock Exchange itself on companies trading below book value — have pushed a generation of Japanese blue chips to justify their balance sheets and lift returns on capital. Otsuka is, in part, responding to that wider current. The useful question for an investor is whether the company is a leader or a laggard in that shift, and the honest answer is somewhere in between: setting an explicit ROIC target and tying pay to it puts Otsuka ahead of the most reluctant reformers, but the group still carries the complexity — multiple segments, a consumer arm, an art museum — that an activist would flag as a candidate for simplification. Complexity is not automatically value-destroying; the dual-track model is the entire thesis. But complexity does demand a higher standard of disclosure and discipline to earn the market's trust, and that standard is exactly what the new plan promises to meet.

Management credibility, in the end, is assessed through behavior over time, not slogans. Otsuka's record is genuinely mixed and should be read as such. On the positive side of the ledger: decades of patient, high-returning science; disciplined, cheap bets like Astex and Visterra that paid off years later; and a franchise-extension track record — from oral Abilify to long-acting injectables to Rexulti — that shows real skill at defending revenue against patent cliffs. On the negative side: the Avanir acquisition, an expensive, anxious deal that ended in a terminated program and a compliance scandal, and a legacy reputation for conservative capital deployment that the market long penalized. A management team that can point to both a masterstroke and a disaster is, paradoxically, easier to evaluate than one with an unblemished record, because you can see the conditions under which it makes each kind of decision. Otsuka does well when it buys capability cheaply and patiently, and badly when it buys outcomes expensively under deadline pressure.

The honest verdict is that the intent is credible and the proof is incomplete. Otsuka has said the right things and, unusually, wired them into pay and governance — which is more than rhetoric. But a five-year plan launched in 2024 is only partway run, and the real test is behavioral: will management hold the ROIC line when the next patent cliff tempts it toward another anxious, Avanir-style acquisition? The structure now exists to punish that mistake. Whether it will is the open question — and it feeds directly into the broader lessons this company offers.

VIII. Playbook: Business & Investing Lessons

Strip away the specifics and Otsuka's century of history yields a handful of transferable lessons, some inspiring and at least one cautionary. They are worth stating plainly, because they are the reusable parts of the story — the patterns an investor can carry to other companies.

Lesson 1: The power of adjacent translation. The single most creative act in Otsuka's history was not a molecule but a reframing: taking the low-margin, unglamorous competence of making sterile IV fluid and translating it into the high-margin consumer category of "ion supply" sports drinks. The deep skill — balancing electrolytes the human body will accept — was the same. The market was entirely different. Great companies often grow less by inventing new capabilities than by carrying an existing capability across a boundary nobody thought to cross. The trick is recognizing that the capability, not the industry, is the asset.

Lesson 2: The symbiotic balance of cash-flow profiles. Pure-play biotechs are fragile by construction — hostage to a single trial readout or a single patent expiry. Otsuka's dual-track model pairs steady consumer FMCG cash flow with high-risk pharmaceutical R&D, so that the reliable business funds the volatile one. This is genuinely durable, but it carries a subtle cost worth naming: diversification that reduces risk can also cap upside and invite a conglomerate discount. The model is a shock absorber, not a growth accelerator, and investors should value it as such.

Lesson 3: The danger of strategic desperation in M&A. The Avanir debacle was not bad luck; it was a predictable consequence of buying under pressure. When a blockbuster's cliff approaches, the temptation to overpay for a replacement becomes almost irresistible, and the premium paid in that state of anxiety is rarely recovered. The tell is emotional as much as financial: watch what a company acquires in the two or three years before a major loss of exclusivity, and watch the price. Discipline is easy to promise in calm years and hard to keep in frightened ones.

There is a fifth lesson that sits underneath the other four, about the relationship between culture and strategy. Otsuka's slogans — recognizing the way through sweat, proving ideas in reality, valuing creativity — are not marketing garnish; they describe a genuine tolerance for the long, unglamorous grind that both the IV business and the aripiprazole program required. A company that genuinely believes breakthroughs come from persistence rather than flashes of brilliance is temperamentally suited to work that takes a decade to pay off and fails most of the time. That same culture, though, has a shadow side worth naming: a company that prizes conviction and stamina can become stubborn, slow to admit a bet has gone wrong, and reluctant to cut losses — the very traits that let AVP-786 run for years before termination. Culture is a double-edged asset. The persistence that discovered Abilify is a cousin of the persistence that sank billions into Avanir's pipeline before finally walking away.

Lesson 4: Capitalizing on clinical serendipity — and rigor. Rexulti's expansion into Alzheimer's-related agitation succeeded where AVP-786 failed, in the same broad indication, a few years apart. The lesson is not that Otsuka got lucky but that pursuing high-barrier, under-served clinical needs — rather than piling into crowded oncology categories — occasionally produces a first-mover franchise with no direct competitor. High-barrier problems are high-barrier for a reason: most attempts fail. But the ones that succeed are extraordinarily defensible, and Otsuka has shown a repeated appetite for that kind of asymmetric bet. Those bets, and the risks around them, are what the bull and bear cases ultimately argue about.

IX. Analysis, Stress Test, and Bear vs. Bull Cases

Put Otsuka on the analyst's operating table and start with Hamilton Helmer's 7 Powers, because the company exhibits at least three of them clearly. The first is scale economies, and the sharpest example is the IV moat. Otsuka controls more than half of Japan's clinical-infusion market, and the advantage is structural rather than clever: because IV fluid is heavy, low-value, and must be sterile, a foreign competitor simply cannot ship water into Japan cheaply enough to beat a domestic incumbent with dense regional manufacturing and distribution. The physics of the product is the moat. It is not glamorous, but it is close to unassailable, and it throws off dependable domestic cash.

The second power is switching costs, and it lives in the psychiatric franchise. A patient stabilized on Rexulti or Abilify Maintena is a patient whose doctor is extremely reluctant to change anything, because the downside of switching — relapse into psychosis or severe agitation — is catastrophic and sometimes irreversible. That clinical inertia keeps patients on the same regimen for years and makes demand unusually sticky. The third power is brand: Pocari Sweat and CalorieMate carry generational equity across East and Southeast Asia, the kind of trust that lets Otsuka charge a premium for what is, chemically, salty water and a nutrient bar. Run the same portfolio through Porter's five forces and the picture holds up on most axes — high barriers to entry in both sterile manufacturing and novel drug discovery, meaningful supplier and buyer dynamics mediated by regulators — with the notable exception of the threat of substitutes, where generics and government price-setters press hardest.

It is worth stress-testing the durability of each of those three powers, because a moat that is real today is not automatically permanent. The IV scale advantage is the sturdiest — the physics of shipping sterile water does not change — but it is also the least valuable, anchored to a low-growth, price-regulated domestic market that Japan's health system squeezes every year. The switching costs in psychiatry are powerful but not eternal: they protect the installed base of stabilized patients, yet they do nothing to guarantee that new patients start on Otsuka's drug rather than a generic aripiprazole or a rival's newer molecule. And the consumer brand power, while genuine, is concentrated in Asian markets where local competitors and shifting consumer tastes are a constant pressure, and where the "sweat" branding that became an asset in one region remains a liability in others. None of these powers is eroding quickly. But each has a ceiling, and stacking three capped advantages is precisely why the group's growth ultimately depends on the pharmaceutical pipeline rather than on the moats it already has.

Which brings us to the risk radar, and two risks dominate. The first is the National Health Insurance (NHI) price squeeze: Japan reprices drugs downward on a regular cadence, systematically eroding domestic pharmaceutical margins regardless of how good the product is. It is a slow, structural headwind that no amount of R&D brilliance fully offsets. The second, and more acute, is the tolvaptan loss of exclusivity. JYNARQUE's looming cliff places enormous weight on VOYXACT and on repinatrabit (JNT-517) to ramp cleanly, and any stumble in those launches would leave a visible hole in the nephrology franchise before the replacements are ready to fill it.

The bull case writes itself from the strengths: Rexulti's Alzheimer's-agitation indication keeps expanding into a large market with little direct competition; VOYXACT establishes itself as a standard of care in IgA nephropathy; the Novartis royalty streams from Kisqali and Pluvicto keep swelling with no incremental cost; and the new ROIC discipline drives a re-rating as the market finally gives Otsuka credit for capital efficiency it long lacked. In this version, the dual-track model compounds durably and the conglomerate discount narrows.

A word on the royalty engine, since it features heavily in the bull case and deserves neither uncritical enthusiasm nor dismissal. The Kisqali and Pluvicto streams are genuinely high-quality — recurring, high-margin, and commercially de-risked because Novartis does the selling. But royalties are also a function of someone else's success and someone else's product life cycle, over which Otsuka has no control. If Novartis's oncology franchises face their own competitive or patent pressures down the line, those streams thin, and there is nothing Otsuka can do about it. The royalties are a wonderful asset precisely because they are passive; they are a vulnerable asset for exactly the same reason. Counting on them to "keep swelling" indefinitely is the kind of extrapolation that flatters a bull case and should be held loosely.

The bear case is the mirror image, and it is not far-fetched. Tolvaptan's revenue declines faster than VOYXACT and repinatrabit can ramp, opening an earnings air-pocket. The Jnana PKU asset — still unproven — fails in Phase III, turning a $1.1 billion bet into another write-down. And most damaging of all, management slips back into legacy, low-ROIC capital deployment the moment the next cliff induces the next bout of anxiety, proving that the governance reforms were signaling rather than discipline. An activist would press exactly these points: why should a diversified healthcare-and-beverage conglomerate not be worth more in pieces; is the R&D budget earning its cost of capital; and will the compensation committee actually claw back rewards if ROIC misses? Those are fair questions, and the honest answer is that the evidence is still being written — which points to what an investor should actually watch.

X. Epilogue & Surprises

Two footnotes to the main story reveal something about Otsuka's peculiar character. The first concerns the name itself. When Pocari Sweat expanded toward Western markets, the word "sweat" was, to put it gently, a marketing liability — few American consumers reach for a beverage that advertises perspiration. The obvious move was to rename it. Otsuka refused. Rather than sand down the brand for Western tastes, it doubled down on the science of hydration and built a dominant position across Asia on the strength of function and electrolyte education, letting the name stand as a badge of authenticity rather than a bug to be fixed. It is a small act of stubbornness that says a great deal about a company willing to be misunderstood in one market to remain itself in another.

The refusal is more strategically revealing than it first appears. A conventional consumer-goods company optimizes relentlessly for the largest addressable market, and by that logic Otsuka should have localized the name to crack the West. But Otsuka is not, at heart, a conventional consumer-goods company; it is a company that trusts function and science over marketing polish, and that trust runs so deep it was willing to forgo the world's richest beverage market rather than dilute a brand it believed in. Whether that was wisdom or obstinacy is genuinely arguable — a more marketing-driven firm might have built a global juggernaut. But it is entirely consistent with the character on display everywhere else in this story: a company that would rather be authentically itself in the markets that accept it than be a watered-down version of itself everywhere.

The second is stranger still. In Naruto, a short drive from where Busaburo Otsuka once boiled seawater, the family built the Otsuka Museum of Art — one of the most unusual and expensive art museums in the world. It contains no original masterpieces. Instead it displays more than a thousand exact-scale reproductions of Western masterworks — including a full recreation of the Sistine Chapel ceiling — rendered on ceramic boards using the group's specialized chemical-tile technology. The reproductions are designed to survive for millennia, impervious to fading. There is something almost perfectly Otsuka about it: a company born from industrial chemistry, using that same chemistry to make permanent copies of art it could never own, in the provincial town where it all began. Grit, translation, and a refusal to do things the conventional way — the museum is the corporate philosophy rendered in tile.

XI. Outro

A century after a chemicals workshop opened on the shore at Naruto, Otsuka Holdings stands as one of the more genuinely distinctive companies in global healthcare — a ¥6 trillion enterprise that answers the industry's deepest fear, the patent cliff, not with scale for its own sake but with a stubbornly diversified structure that lets sports drinks pay for neuroscience. The strengths are real and, in places, close to unassailable: the physics-based IV moat, the sticky psychiatric franchise, the generational consumer brands, and a drug-discovery engine that has produced two of the best-selling psychiatric medicines in history. The vulnerabilities are equally real: a looming nephrology cliff, an unproven pipeline that must ramp on schedule, chronic domestic price pressure, and a management team whose newfound capital discipline is credible in structure but not yet proven in a crisis.

For a long-term investor, the whole case narrows to a small number of things worth actually tracking. Watch, first, the nephrology hand-off — whether VOYXACT's revenue ramp outpaces tolvaptan's decline, because that single transition validates or breaks the "Global 10+2" growth story. Watch, second, group ROIC against the 9.5% FY2028 target, because that number is the honest scoreboard for whether the governance reforms are discipline or decoration. And watch, third, the next major acquisition, whenever it comes — its price and its timing will reveal, more than any slide, whether Otsuka has truly learned the lesson Avanir taught it. The company from the whirlpools has been both brilliant and foolish with capital. Which instinct governs the next decade is the question that will decide whether the dual-track giant compounds or merely endures.

References

-

Otsuka Holdings Reports Strong FY2024 Financial Performance (FY2024 consolidated revenue ¥2,329.9bn; segment revenue and business profit) — TipRanks, 2025 ↩↩↩↩↩↩↩

-

Otsuka Holdings Corporate History & Milestones — Otsuka Holdings Co., Ltd. ↩↩↩

-

Pocari Sweat Brand Development and Science of Hydration — Otsuka Pharmaceutical Co., Ltd. ↩↩↩

-

Otsuka Holdings 4th Medium-Term Management Plan (FY2024–FY2028) — Otsuka Holdings Co., Ltd. ↩↩↩↩

-

The 4th Medium-Term Management Plan, June 7, 2024 (capital allocation, ROIC and revenue targets) — Otsuka Holdings Co., Ltd., 2024-06-07 ↩↩

-

Otsuka to Buy Avanir for $3.5 Billion to Expand in U.S. CNS Drugs — Bloomberg, 2014-12-02 ↩

-

Otsuka to Buy Cancer Drug Maker Astex for $886 Million — Reuters, 2013-09-05 ↩

-

Japan's Otsuka Pharmaceutical to Buy Visterra for $430 Million — Reuters, 2018-07-11 ↩

-

Otsuka to Buy US Drugmaker Jnana Therapeutics for Up to $1.1 Billion — Reuters, 2024-08-01 ↩

-

Otsuka Receives FDA Accelerated Approval for VOYXACT® (sibeprenlimab-szsi) for the Reduction of Proteinuria in Adults with Primary IgA Nephropathy — Otsuka Pharmaceutical Co., Ltd., 2025-11-26 ↩↩

-

Otsuka Holdings Corporate Governance Guidelines & Committee Structure — Otsuka Holdings Co., Ltd. ↩

-

Otsuka Holdings (4578.T) — Market Capitalization — CompaniesMarketCap ↩

-

Otsuka Holdings Grants Restricted Stock to Directors Tied to Medium-Term Performance Targets — TipRanks, 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube