The Smart Bomb: The Story of Daiichi Sankyo

I. Introduction & Episode Roadmap

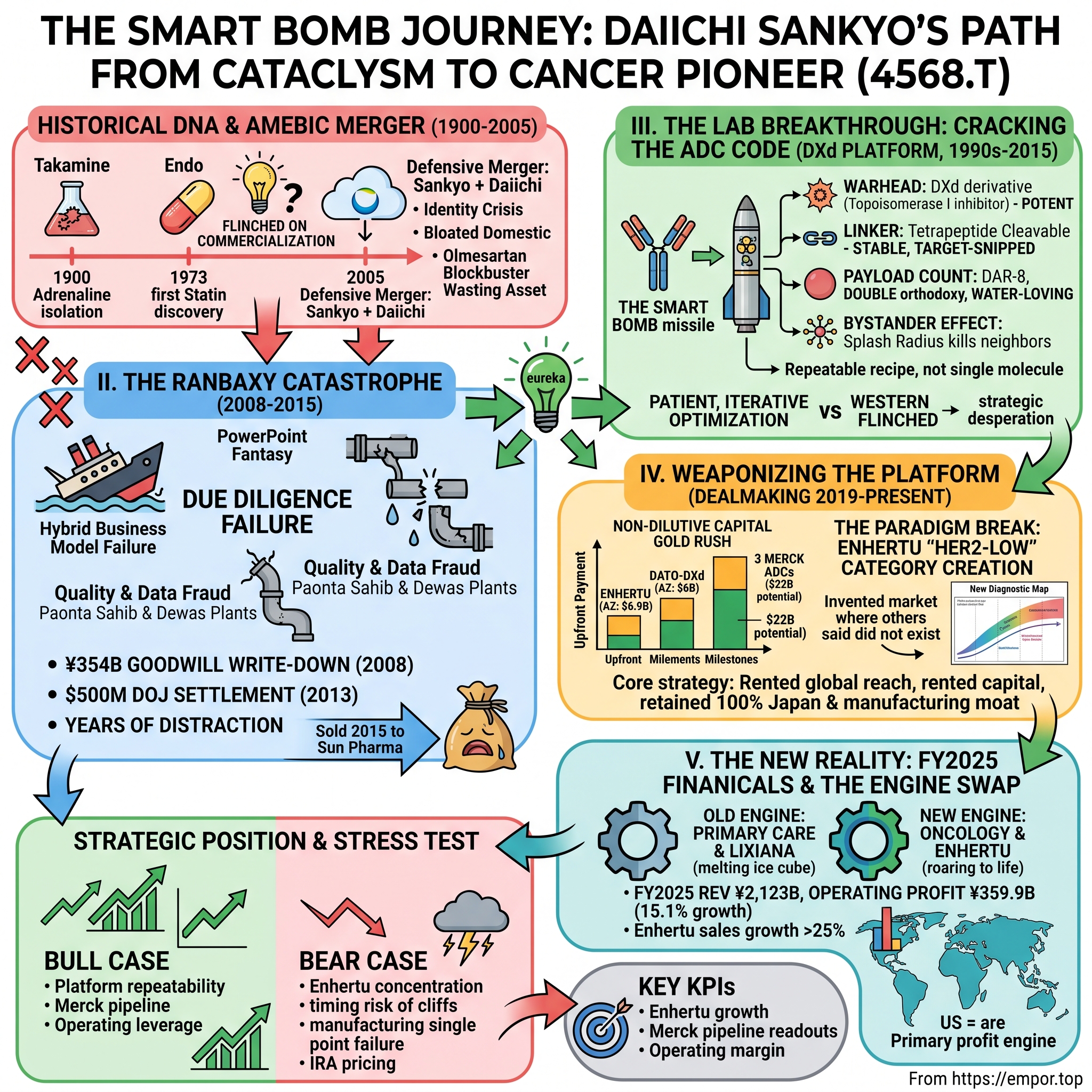

Let's start with the thing that makes this company genuinely unusual. Most pharmaceutical franchises are built on a single molecule. A biotech discovers one compound, bets the company on it, and lives or dies by a Phase III readout. Daiichi Sankyo built something different: a platform. Its DXd chemistry is a repeatable recipe for attaching a potent cancer-killing payload to an antibody that acts like a homing beacon. Change the antibody, and you can aim the same warhead at a different tumor. That repeatability is why a mid-sized Japanese firm, long dismissed as a sleepy domestic player, suddenly found itself holding intellectual property that the biggest names in oncology were willing to pay billions to share.

The financial validation is stark. Daiichi Sankyo's AstraZeneca alliance for Enhertu was structured for up to $6.9 billion, with $1.35 billion paid upfront.2 A second AstraZeneca deal for a different ADC was worth up to $6 billion.3 Then in October 2023, Merck agreed to a collaboration for three more DXd candidates carrying a total potential value of up to $22 billion, including a $4 billion upfront cheque.4 Crucially, Daiichi Sankyo did not sell these assets outright. It kept 100% of Japan, retained global manufacturing, and used the partners' cash to fund its own transformation into a global commercial oncology company. That is the strategic heart of this episode: a company that surrendered half the upside on paper to keep control of the machine that produces the upside.

But we should be skeptical of clean redemption arcs, and this article will keep testing the narrative rather than celebrating it. The same platform that generates the bull case also concentrates the risk. Enhertu is now the entire growth story; the legacy franchise underneath it is quietly shrinking. A single clinical disappointment — and there has already been an ambiguous one, in lung cancer — can erase billions in expected value overnight. And the company's insistence on manufacturing everything itself, celebrated as a moat, is also a single point of failure.

Before we start, it's worth naming the myth this story invites, because we'll spend the article testing it rather than swallowing it. The tidy version — the one management would happily narrate — goes: a proud Japanese science house stumbled once in India, learned humility, rediscovered its research soul, and ascended to global oncology leadership on the strength of pure chemistry. That arc is real in its broad strokes. But it flattens the messier truths underneath: that the ADC breakthrough was underway before the Ranbaxy lesson was fully absorbed, not because of it; that "leadership" was purchased in part by handing half the economics to Western partners; that the company's crown jewel is dangerously concentrated; and that the redemption has been road-tested only in a bull market for its lead drug. Keep both versions in your head as we go.

Here is the road we'll travel. First, the deep DNA: a company descended from the chemist who first isolated adrenaline and the lab that discovered the world's first statin, stitched together by a defensive 2005 merger. Then the Ranbaxy catastrophe, the most expensive lesson in corporate focus you will find anywhere. Then the laboratory breakthrough — how an in-house Japanese team cracked a chemistry problem that had defeated global pharma for two decades. Then the dealmaking that turned that chemistry into cash. Then the financials, the management, the competitive war-game through Helmer and Porter, the bull-and-bear stress test, and finally the transferable lessons. It begins more than a century ago, in a laboratory where a Japanese chemist was about to isolate the first hormone ever obtained in pure form.

II. Historical DNA: Adrenaline, Statins, and Defensive Merger (1900–2005)

Picture a laboratory in New York at the turn of the twentieth century. A Japanese-born chemist named 高峰譲吉 Jokichi Takamine — already famous for a digestive enzyme he'd extracted from mold and licensed to what would become a great American pharmaceutical fortune — is boiling down the secretions of animal adrenal glands. In 1900, he succeeds in crystallizing the active compound: adrenaline, the first hormone ever isolated in pure form.5 It is one of the foundational achievements of modern biochemistry, and the man who did it would lend his prestige to a fledgling Japanese drug house. 三共 Sankyo had begun in 1899 as Sankyo Shoten, a trading concern built to sell Takamine's enzyme; when it incorporated as Sankyo Co., Ltd. in 1913, Takamine became its first president.5

That origin matters because it set a cultural template that echoes through the company to this day: Daiichi Sankyo's ancestors were, at their best, discovery houses — organizations that prized the isolation of a novel molecule over the grind of commercial scale. The other parent, 第一製薬 Daiichi Pharmaceutical, traces to a venture founded in 1915 (renamed Daiichi Pharmaceutical in 1918) and made its name in synthetic anti-infectives.6 Two Japanese chemistry cultures, a century deep, both proud of the flask and the assay.

The statin that got away

The most revealing episode in this pre-history is one the company would probably rather forget. In July 1973, a Sankyo biochemist named 遠藤章 Akira Endo, having screened thousands of fungal broths in search of a compound that could block cholesterol synthesis, isolated compactin (mevastatin) — the world's first statin.7 It was a Nobel-caliber discovery. Statins would go on to become the best-selling class of drugs in history, extending tens of millions of lives.

And Sankyo largely let it slip. Spooked by ambiguous toxicity signals in early animal work, the company hesitated. Merck, working from Endo's published science, pressed ahead and won the race to market with lovastatin. Sankyo eventually commercialized its own statin, pravastatin, but the pioneer had ceded the frontier to a bolder Western rival. Hold that pattern in mind, because it recurs: a Japanese lab produces world-changing chemistry, then flinches at the moment of commercial commitment. The company that would later bet everything on ADCs was, in its DNA, the company that once let the statin get away.

The defensive merger of 2005

By the early 2000s, both Sankyo and Daiichi Pharmaceutical faced the same slow suffocation. Their cash cows were primary-care drugs — the olmesartan blood-pressure franchise chief among them — sold heavily into a Japanese market that the government was methodically squeezing through mandatory price cuts. Patent cliffs loomed. Pipelines looked thin. Neither company had the scale to fund a globally competitive R&D engine alone.

So in 2005 they combined. Daiichi Pharmaceutical and Sankyo integrated under a joint holding company, with the share exchange completed in late September 2005, creating 第一三共 Daiichi Sankyo — listed on the 東京証券取引所 Tokyo Stock Exchange as 4568.T, today a constituent of 日本取引所グループ JPX.8 It was, in the honest telling, a defensive merger: two mid-tier Japanese firms lashing themselves together against the tide, hoping combined scale would buy time.

The crown jewel of that combined primary-care engine was the olmesartan franchise — a blood-pressure medicine sold as Olmetec and, in the United States, Benicar. It was a genuine blockbuster, and for a while it masked the underlying problem. But blockbusters in the primary-care world are wasting assets on a timer: the moment patent protection lapses, generic competitors flood in and the revenue collapses almost overnight. Daiichi Sankyo could see its own cliffs coming down the calendar, and it had no obvious next act.

What the merger actually produced, in the short run, was an identity crisis. Daiichi Sankyo emerged as a large, cash-generative but strategically cornered company: a bloated domestic sales machine selling maturing primary-care drugs into a shrinking, price-controlled home market, with a research pipeline that did not yet contain an obvious global winner. There is a bitter irony worth marking here. The company's ancestors had twice produced world-changing science — adrenaline and the first statin — and both times the commercial glory had migrated elsewhere. Now their heir sat on maturing me-too franchises with the clock running. Management knew it needed a bold move to escape the trap. The move it chose would very nearly destroy the company.

III. The Ranbaxy Disaster: The Pitfalls of "Hybrid" M&A (2008–2015)

Every corporate catastrophe begins as a PowerPoint slide that looks brilliant. For Daiichi Sankyo's then-CEO 庄田隆 Takashi Shoda, the slide was labeled the "hybrid business model." The logic ran like this: innovative patented drugs are enormously profitable but cliff-exposed; generics are low-margin but durable and fast-growing in emerging markets. Marry the two under one roof, and you would smooth the earnings, hedge the patent cliffs, and plant a flag in India and the developing world all at once. On paper, it was elegant. In practice, it rested on a fantasy — that a high-margin innovator and a high-volume generics operator could share a quality culture, a management style, and a balance sheet without one poisoning the other.

The deal

In June 2008, Daiichi Sankyo agreed to acquire a controlling stake in Ranbaxy Laboratories, India's largest generics maker, for roughly $4.6 billion — ultimately taking its holding to 63.92% by late 2008.1 The price implied a rich premium to where generics peers traded, a valuation that only made sense if you believed the hybrid thesis and Ranbaxy's growth trajectory. What Daiichi Sankyo appears not to have adequately priced was what was rotting inside Ranbaxy's factories.

The fall

The unraveling was almost immediate. In September 2008 — the same year the deal was struck — the FDA issued an import alert covering Ranbaxy's Paonta Sahib and Dewas plants, blocking some thirty drugs from the U.S. market over manufacturing-quality and data-integrity failures.9 It emerged, through the work of a whistleblowing former Ranbaxy executive, that the company had systematically falsified data and violated good-manufacturing practices. This was not a solvable teething problem; it was fraud baked into the operating model of the asset Daiichi Sankyo had just bought.

The due-diligence failure here is the lesson that stings. Daiichi Sankyo had leaned heavily on the assurances of Ranbaxy's controlling family, the Singh brothers, rather than commissioning the kind of exhaustive, independent forensic audit that the red flags warranted. It bought a black box and trusted the previous owner's description of what was inside.

And the box had been rattling for years before Daiichi Sankyo arrived. A former Ranbaxy executive, Dinesh Thakur, had internally documented the systematic fabrication of test data and eventually turned whistleblower to U.S. authorities — the thread that ultimately unraveled the whole affair.9 This is the part that should haunt any acquirer: the information existed. The problem was not that the fraud was undetectable; it was that Daiichi Sankyo did not dig hard enough to detect it, because the deal thesis was too seductive to interrogate. Confirmation bias is expensive. In this case it cost billions.

What made the situation nearly unfixable was the collision of cultures. Daiichi Sankyo was a company whose entire identity, stretching back to Takamine's flask, was built on scientific rigor and quality. Ranbaxy's operating model, at least at the implicated plants, had normalized cutting corners on precisely those quality systems. You cannot patch that gap with a management memo; quality culture is built or corroded over decades. The Japanese parent found itself the majority owner of a subsidiary whose core practices contradicted its founding values — and no amount of oversight from Tokyo could rewire a factory floor in Himachal Pradesh fast enough to satisfy the FDA.

The damage

The financial reckoning came fast. For the quarter ended December 2008, Daiichi Sankyo booked a consolidated goodwill write-down of ¥354.0 billion and a non-consolidated valuation loss of ¥359.5 billion on its Ranbaxy investment — on the order of $3.5 billion — plunging the company to a full-year net loss.10 Then came years of drag: management attention consumed by an unfixable subsidiary, and, in May 2013, a guilty plea by Ranbaxy to U.S. felony charges and a $500 million settlement with the Department of Justice — $150 million in criminal fines and forfeiture plus $350 million to resolve civil False Claims Act allegations, one of the largest such penalties ever levied on a generics maker.11

The exit and the strange partial rescue

By 2014, Daiichi Sankyo surrendered. In April it agreed to sell its entire Ranbaxy stake to Sun Pharmaceutical Industries in an all-stock deal, receiving roughly 9% of the enlarged Sun Pharma.12 Here the story takes an ironic turn: Sun's shares performed well, and when Daiichi Sankyo liquidated the position in April 2015, it raised about $3.2 billion.13 The equity appreciation softened the raw cash loss considerably — but it does not redeem the episode. Measured properly, against the $4.6 billion deployed, the years of distraction, the reputational damage, and the opportunity cost of capital that could have funded research, Ranbaxy remains a textbook case of overpayment and cultural mismatch.

There was one final act of retribution. In 2016, an arbitration tribunal seated in Singapore ordered the Singh brothers to pay Daiichi Sankyo about $525 million, finding they had concealed material information about the FDA and DOJ investigations during the 2008 sale.14 It was vindication of a sort — a legal confirmation that Daiichi Sankyo had been deceived. But collecting from the Singhs would prove its own multi-year saga, and no arbitral award could return the half-decade the company had lost.

The deepest cost of Ranbaxy was not the write-down. It was the years. While Daiichi Sankyo's executives were mired in Indian courtrooms and FDA consent decrees, a small team of its own chemists, largely ignored, was quietly solving a problem that would matter far more than any generics portfolio. The company was about to be saved not by strategy, but by science.

IV. The Lab Breakthrough: Cracking the ADC Code with DXd (1990s–2015)

To understand why Daiichi Sankyo's laboratory work is a genuine competitive asset and not just a marketing story, you have to understand the problem the whole industry had failed to solve. Start with an analogy.

The guided missile that kept missing

Chemotherapy is carpet bombing. You flood the body with a poison that kills fast-dividing cells, hoping to kill more cancer than patient. The dream, for decades, was a guided missile instead: a drug that would deliver the poison only to tumor cells and spare healthy tissue. That is precisely what an antibody-drug conjugate is meant to be. You take a monoclonal antibody — a protein exquisitely designed to latch onto a specific marker on the surface of cancer cells — and you chemically bolt a toxic payload onto it via a connector called a linker. The antibody is the guidance system; the payload is the warhead; the linker is the bolt that holds them together until the missile reaches its target.

Simple in concept, brutally hard in practice. The first-generation ADCs, such as Pfizer's Mylotarg, and the more refined second generation, such as Roche's Kadcyla, ran into a physics problem. If the linker was too flimsy, the warhead fell off in the bloodstream, poisoning healthy tissue — the guidance system failed and the bomb went off over the wrong city. If you tried to load more warheads onto each antibody to increase potency, the whole molecule turned greasy, clumped together, got cleared by the body too fast, or became intolerably toxic. Industry orthodoxy hardened into a rule of thumb: you could not safely attach more than three or four payload molecules to an antibody — a metric called the drug-to-antibody ratio, or DAR — before the thing fell apart.

The rebellion in the lab

While the company's leadership was consumed by Ranbaxy, a team of Daiichi Sankyo chemists set about attacking every one of those failure points at once. The result, refined over years, was the DXd platform. It is worth walking through what they actually changed, because the details are the moat.

First, the warhead. They took exatecan, a potent inhibitor of an enzyme called topoisomerase I that cancer cells need to copy their DNA, and engineered a derivative they named DXd. Company literature describes each conjugate as an antibody attached to topoisomerase I inhibitor payloads — specifically an exatecan derivative — via cleavable linkers.15 The payload was designed to be far more potent than the older-generation chemotherapies, so that even a small delivered dose could do lethal damage inside the tumor.

Second, the linker. They built a tetrapeptide-based connector — a short chain of four amino acids — engineered to stay locked shut in the bloodstream but to be snipped open by enzymes called cathepsins that are highly concentrated inside cancer cells.15 In practical terms: the bolt holds firm while the missile is in transit and releases the warhead only after the antibody has been swallowed by the target cell. Independent literature on the lead molecule reports the linker's design gave it remarkable stability in circulation while permitting efficient release at the target.16

Third, and most audacious, the payload count. Because the team engineered the linker to be highly water-loving rather than greasy, they broke the orthodox DAR ceiling. On the flagship molecule they loaded eight payload molecules onto a single antibody — a DAR of 8 — with none of the aggregation or instability that dogma said was inevitable.16 Roughly double the standard potency, delivered with high plasma stability. (This is a place to be precise rather than promotional: DAR-8 is the signature of the flagship, trastuzumab deruxtecan; other DXd drugs in the portfolio use different ratios tuned to their targets. The platform is a set of design principles, not one fixed number.)

The bystander effect

The final piece was almost a happy accident of the chemistry, and it turned out to be clinically decisive. Once the DXd warhead is released inside a target cell and does its work, it is membrane-permeable — it can slip out and drift into neighboring tumor cells and kill them too, even if those neighbors don't carry the surface marker the antibody was aiming at.16 Oncologists call this the bystander effect, and it addresses one of cancer's cruelest tricks: tumors are heterogeneous, a patchwork in which only some cells display the target. A missile that also takes out the cells next door is far harder for a tumor to evade.

Why an outsider cracked it

There is a genuine puzzle worth sitting with: why did Daiichi Sankyo, and not one of the far larger, far better-funded Western ADC pioneers, solve this? Pfizer, Roche, and others had decades of head start and billions more to spend. Part of the answer is cultural, and it loops back to the company's DNA. Solving the DXd problem was not a matter of a single brilliant insight; it was the patient, iterative optimization of every component at once — payload potency, linker chemistry, hydrophilicity, conjugation site — the kind of methodical, incremental engineering at which Japanese research organizations have historically excelled. It was, in a sense, the same meticulous chemistry culture that had isolated adrenaline and compactin, finally applied to a problem where meticulousness was the decisive variable.

Part of the answer is also strategic desperation. A company flush with blockbusters has less reason to bet on an unproven modality; a company staring at patent cliffs and the smoking ruin of its diversification strategy has every reason to swing for a fence. The ADC program was, in effect, Daiichi Sankyo's counter-bet against its own near-death experience — and it had the freedom to pursue it precisely because it was not yet a global oncology player defending an existing franchise.

But we should resist over-romanticizing. The DXd platform's superiority is demonstrated in specific molecules against specific comparators; it is not a metaphysical guarantee that every future DXd drug will win. The honest read is that Daiichi Sankyo assembled a genuinely differentiated toolkit and has so far deployed it with an unusually high hit rate. Whether that hit rate reflects a durable, structural edge or a run of well-executed programs is one of the central questions an investor in this company must continually re-ask.

Put the pieces together and you have a machine: a stable delivery system, a potent warhead, double the payload, and a splash radius. The question by the late 2010s was no longer whether the chemistry worked. It was how a company still nursing its Ranbaxy wounds could possibly afford to fund global clinical trials and build a worldwide oncology sales force from scratch. The answer would rewrite the economics of the entire company.

V. Enhertu & The Non-Dilutive Capital Gold Rush (2019–Present)

The molecule at the center of everything is DS-8201, later christened Enhertu — generic name trastuzumab deruxtecan, or T-DXd. It aims the DXd warhead at HER2, a growth-signaling protein famous as the target of Roche's Herceptin. And in its early trials, it did something that made oncologists sit up in their chairs.

The clinical shockwave

Patients with HER2-positive metastatic breast cancer who had already failed multiple therapies — including Roche's own ADC, Kadcyla — were showing dramatic responses to Enhertu. That alone would have made it a valuable drug, because it meant Enhertu could work after the previous best-in-class ADC had stopped working, a strong hint that the DXd chemistry was operating in a different league from the second-generation designs.

But the truly paradigm-breaking result came in a group the field had written off. Roughly half of breast cancer patients have tumors with low levels of HER2 — too little to qualify as HER2-positive, so historically they were lumped into the "HER2-negative" bucket and denied HER2-targeted therapy entirely. The clinical dogma was blunt: no HER2, no HER2 drug. Thanks to the bystander effect — the warhead's ability to spread to neighboring cells regardless of whether they carry the target — Enhertu worked in these "HER2-low" patients too. In August 2022, the FDA approved Enhertu for HER2-low metastatic breast cancer on the strength of the DESTINY-Breast04 trial, in which median progression-free survival roughly doubled (about 10.1 versus 5.4 months in the hormone-receptor-positive group) and overall survival improved to about 23.4 versus 16.8 months against chemotherapy.17 Overnight, a category that did not exist as a treatable disease became a multi-billion-dollar market — one that Daiichi Sankyo had defined and now led.

The strategic implication is subtle but enormous. Most drugs fight for share within an existing market. Enhertu created its market by redrawing the diagnostic map. When you invent the category, you don't just win the competition — for a while, there is no competition, because rivals are still running trials against a patient definition you authored. That is the rarest kind of commercial advantage in pharma, and it is precisely what a licensing partner pays a premium to stand next to.

The 2019 AstraZeneca alliance: the template

Here was the strategic fork. Daiichi Sankyo had a potential mega-blockbuster but lacked a global oncology sales force and the balance sheet to run dozens of simultaneous international trials. The conventional options were unappealing: sell the drug outright and forfeit the upside, or raise enormous amounts of equity or debt and dilute or leverage the company. Daiichi Sankyo chose a third path.

In March 2019, it signed a global co-development and co-commercialization alliance with AstraZeneca for Enhertu, structured for up to $6.9 billion — including $1.35 billion upfront (half on signing, half a year later), up to $3.8 billion in regulatory and other milestones, and up to $1.75 billion in sales milestones.2 The genius was in the structure. The two companies would split development costs and profits 50/50 everywhere in the world except Japan, where Daiichi Sankyo kept 100% of the economics. And Daiichi Sankyo retained sole responsibility for manufacturing and supply.2 In other words, it brought in a deep-pocketed partner to fund and sell alongside it, took a large slug of non-dilutive cash, kept its home market entirely, and kept its hands on the one thing hardest to replicate — the factory.

Doubling and tripling down

AstraZeneca liked what it saw enough to come back. In July 2020, the two signed a second alliance, this time for datopotamab deruxtecan (Dato-DXd), a DXd ADC aimed at a different target called TROP2, for up to $6 billion including a $1 billion upfront — the same 50/50-ex-Japan architecture.3 The platform was proving it could be re-aimed.

Then, in October 2023, came the deal that announced Daiichi Sankyo's arrival as a platform power. It signed a collaboration with Merck & Co. — MSD outside North America — covering three clinical-stage DXd ADCs at once: patritumab deruxtecan (HER3-DXd), ifinatamab deruxtecan (I-DXd, targeting B7-H3), and raludotatug deruxtecan (R-DXd, targeting CDH6). The terms were staggering: a $4 billion upfront payment, $1.5 billion in continuation payments over 24 months, and up to $16.5 billion in sales-based milestones — a total potential value of up to $22 billion.4 As with AstraZeneca, Daiichi Sankyo kept exclusive rights in Japan and retained manufacturing.18

Read the three deals in sequence and you can watch Daiichi Sankyo's negotiating leverage compound. In 2019, an unproven single molecule commanded a $1.35 billion upfront. By 2023, with the platform de-risked by Enhertu's real-world success, three earlier-stage molecules together commanded a $4 billion upfront — a far richer per-asset, earlier-stage price. That escalation is not luck; it is the market repricing Daiichi Sankyo's chemistry as validated. The company essentially used the proof-of-concept it earned with AstraZeneca as collateral to extract better terms from Merck. This is what it means to weaponize a platform: each success raises the price of the next partnership.

It is worth pausing on why a partnership beat the alternatives so decisively for a company in Daiichi Sankyo's position. Selling a drug outright would have meant forfeiting the long tail of economics and, worse, ceding control of the very manufacturing and platform know-how that constitute the moat. Going it alone would have meant either crushing dilution — issuing enormous equity to fund a dozen simultaneous global Phase III programs and a from-scratch worldwide oncology salesforce — or a debt load that would have terrified a company only a few years removed from a multi-billion-dollar write-down. The partnership route threaded the needle: it imported both capital and an established Western commercial machine, while leaving Daiichi Sankyo's ownership of the platform, the factories, and its home market untouched. For a mid-sized company trying to punch at global weight, it was arguably the only viable path — which is itself a reminder that the strategy was born as much of constraint as of genius.

What the dealmaking really accomplished

Step back and add up what these alliances did, because the significance is easy to miss under the big headline numbers. Between the AstraZeneca and Merck deals, Daiichi Sankyo pulled in on the order of $6.35 billion in raw upfront cash, plus ongoing cost-sharing that offloaded a huge share of the world's most expensive clinical trials onto partners' income statements. That cash and cost relief is what funded the buildout of Daiichi Sankyo's own global oncology commercial infrastructure and the scaling of its biologics manufacturing.

The analytical point is this: Daiichi Sankyo did not sell its future to survive. It used partners' money to finance its transformation from a regional primary-care company into a company that books oncology sales directly around the world — while retaining Japan outright and controlling the supply chain everywhere. It traded away half the economics on each molecule to keep control of the platform that produces the molecules. Whether that was the right trade depends entirely on how many more winners the platform yields — and on whether keeping all the manufacturing in-house proves a moat or a liability. To judge that, we need to look at what the machine actually earns today.

VI. Segment Economics & Sizing the Core Business (FY2025 Financials)

Numbers in a pharmaceutical company can mislead if you read them the way you'd read a retailer's. So let's read Daiichi Sankyo's fiscal 2025 results — the year ended March 31, 2026 — as a story about a company in the middle of an engine swap, with one motor roaring to life while the old one gently winds down.

The top line, and what's driving it

For fiscal 2025, Daiichi Sankyo reported consolidated revenue of ¥2,123.0 billion, up 12.6% year on year, and core operating profit — the company's preferred measure of underlying profitability — of ¥359.9 billion, up 15.1%.19 To give the figures a familiar frame, at prevailing exchange rates that revenue is on the order of $14 billion and change — placing Daiichi Sankyo among the larger pharmaceutical companies in the world, though still a fraction of the size of the Western majors it now partners with and competes against. Double-digit growth in both lines is not what you would expect from the sleepy domestic drugmaker of fifteen years ago, and it is not what most of Big Pharma delivered in the same period. The growth is almost entirely an oncology story.

The engine is Enhertu. Global product sales of the drug reached ¥698.4 billion in fiscal 2025, up 26.3%, and the company also collected an ¥86.0 billion sales-milestone payment after combined global alliance sales crossed the $5 billion mark.19 Put plainly: a drug that generated essentially nothing in 2019 now accounts for roughly a third of the entire company's revenue. That is the fastest transformation of a large drugmaker's revenue base you will find in recent memory, and it is the single most important fact about the business.

One number deserves a footnote of caution, because "core" is doing work in "core operating profit." That ¥359.9 billion figure strips out certain one-off items. On a fully reported basis, operating profit for fiscal 2025 actually fell about 31%, to roughly ¥229.1 billion, weighed down by temporary charges.19 The gap is not a scandal — heavy R&D reinvestment and one-time items are exactly what you'd expect from a company in the middle of a global buildout — but an investor should notice that the headline growth story lives in the adjusted numbers, and that the reported bottom line is lumpier. Management's job over the next few years is to close that gap by converting today's investment into tomorrow's structural margin.

Management has put hard targets on that ambition. Alongside the fiscal 2025 results in May 2026, Daiichi Sankyo laid out a five-year plan running to fiscal 2030, aiming for revenue above ¥3.0 trillion, operating profit above ¥600 billion, and earnings per share above ¥260.19 These are stretch goals, not guidance, and they encode the entire thesis: revenue up roughly 40%-plus from here, but operating profit up far more — the mathematical signature of a mix shift toward high-margin oncology. Whether those targets are met is, in effect, the scoreboard for everything else in this article.

Where the money is actually made

Averages hide the economics, so look at the geography. Of Enhertu's ¥698.4 billion in fiscal 2025 product sales, the United States accounted for roughly ¥386.3 billion, Europe about ¥174.8 billion, the ASCA region (Asia, South and Central America) ¥99.7 billion, and Japan just ¥37.7 billion.20 The lesson is unmistakable. The profit engine is the United States, where oncology drugs command premium prices and where the addressable patient population is vast. Japan — Daiichi Sankyo's home, where it keeps 100% of the economics — contributes a comparatively thin slice, precisely because the government's pricing regime caps what any drug can earn there. The company's crown jewel makes most of its money abroad, which is both an opportunity and, as we'll see, a regulatory exposure.

The legacy cash cows, quietly aging

Beneath the oncology rocket sits the old business that pays the bills during the transition. The most important legacy asset is Lixiana (edoxaban), an oral anticoagulant that is highly cash-generative in Japan and Europe — European sales alone reached about ¥193.0 billion in fiscal 2025, with roughly ¥141.8 billion more booked in Japan.20 Lixiana is a genuine blockbuster, but it is a melting ice cube: it faces patent expiries across major geographies over the coming years. Around it sits the broader primary-care and domestic Japan business, stable but structurally declining under Japan's National Health Insurance regime of near-annual price cuts. The strategic clock is therefore real. The oncology engine has to keep accelerating fast enough to outrun the decline of Lixiana and the primary-care book — a race the company is currently winning, but only because Enhertu is growing at an extraordinary clip.

The optionality, honestly sized

Two other pieces deserve mention precisely because they should not be over-weighted. The first is the mRNA vaccine platform, marketed as ダイチロナ DAICHIRONA — Japan's first domestically developed mRNA COVID-19 vaccine, approved in updated form in November 2023.21 It matters symbolically, as proof of a homegrown mRNA capability and a nod to national health security, but it is financially immaterial to the company's value today. The second is the crop of earlier-stage ADCs and novel modalities — assets aimed at targets like MUC1, and a DLL3-directed T-cell engager co-developed with Merck. These represent real optionality if the platform keeps producing, but they carry minimal economic weight now and should be valued as lottery tickets, not earnings. With the money mapped, the question becomes who is steering it — and whether they've earned the benefit of the doubt.

VII. Current Strategy, Management Credibility & Governance

The most important test of a management team is not what it says when a drug is winning. It is what it says when a drug disappoints — and whether the story it tells across years actually holds together. Daiichi Sankyo offers a live opportunity to run that test, because the company changed leaders at the exact moment its strategy reached maximum stakes.

The changing of the guard

On April 1, 2025, 奥澤宏幸 Hiroyuki Okuzawa became Representative Director, President and CEO, succeeding 真鍋淳 Sunao Manabe, who moved up to Representative Director and Executive Chairperson.22 This was not a rupture but a relay: Manabe, a veterinarian by training who had steered the oncology pivot, stayed on to anchor continuity while Okuzawa took operational command. The succession was announced months in advance, in January 2025 — a measured, telegraphed handover rather than the abrupt exits that marked the Ranbaxy era, when leadership turned over under the cloud of the write-down.22

The other name that matters is Ken Keller, who runs Daiichi Sankyo, Inc. — the U.S. commercial subsidiary — and serves as Global Head of the Oncology Business.23 His importance is easy to underrate. A Japanese company selling premium oncology drugs into the American market must bridge two very different corporate cultures: the consensus-driven, 稟議 ringi-style deliberation of Tokyo and the aggressive, fast-moving commercialization of U.S. biotech. Keller is that bridge, and having a credible Western operator atop the profit engine is part of why global investors take the company's commercial ambitions seriously rather than dismissing them as a Japanese exporter's overreach.

Incentives and alignment

An honest governance assessment has to flag where Daiichi Sankyo diverges from Western norms. Consistent with Japanese corporate practice, executive equity ownership is modest by U.S. pharma standards, and compensation is tied to core operating profit and progress against the multi-year business plan rather than to share-price performance.19 For a Western activist, that is a double-edged sword: it insulates management from short-term market swings and lets it invest through cycles, but it also weakens the direct wealth link between executives and outside shareholders that Anglo-American governance prizes. Neither framing is automatically correct; it is a genuine structural feature investors should weigh.

Capital allocation — the redemption, tested

The strongest evidence for management credibility is the sharp, sustained reversal in how the company allocates capital. The Ranbaxy era was value-destructive diversification: buying a business it did not understand in a category it could not run. The current framework is the opposite — reinvesting the AstraZeneca and Merck upfronts directly into global oncology trials and biologics manufacturing capacity. Its shareholder-return policy, reaffirmed in the FY2026–FY2030 business plan unveiled in May 2026, pairs progressive dividends with a target for adjusted dividend-on-equity above 10% annually and flexible buybacks; notably, the fiscal 2025 payout ratio actually ran high, near 55%, so this is a company returning meaningful cash while it invests, not hoarding it.19 The company has, in effect, spent a decade doing the opposite of what destroyed it. That is a real behavioral signal, not just rhetoric — though it is worth noting the discipline has only truly been tested in good times, with Enhertu carrying everything.

The credibility test: how they handle a miss

Which brings us to the live stress test. Datopotamab deruxtecan — the TROP2 drug from the second AstraZeneca deal — delivered an ambiguous result in its pivotal lung cancer trial, TROPION-Lung01. The trial met one co-primary endpoint, progression-free survival, but the improvement was statistically significant yet clinically modest (a hazard ratio around 0.75), and the overall-survival co-primary endpoint did not reach statistical significance in the full population; there were also interstitial lung disease safety signals, including some fatal events.24 Interstitial lung disease — inflammation and scarring of lung tissue — is a known hazard of this drug class and precisely the kind of signal that can constrain a label.

How management handled it is the point. Rather than burying the ambiguity or blaming trial design, the leadership acknowledged the modest magnitude, leaned into the nonsquamous subgroup where the drug performed better, and recalibrated its regulatory strategy accordingly. This is the behavior investors should want: transparent framing of a disappointing readout and a concrete plan, rather than spin. It is a modest but genuine data point in favor of the current team's credibility — and a reminder that even a validated platform produces drugs that only partly work.

There is, though, a fair skeptic's rejoinder, and it belongs in any honest credibility assessment. It is easy to be transparent and disciplined when your lead asset is compounding at north of 25% a year and partners are wiring you billions. The real test of a management team's candor and capital discipline comes in adversity — when a pivotal Enhertu expansion trial disappoints, or when the Lixiana cliff bites and the growth math tightens. The current team has not yet been through that fire. The Ranbaxy generation's failures are a matter of record; the Okuzawa–Manabe team's resilience is, for now, largely an inference from good-weather behavior. Investors should watch how management communicates the next genuine setback at least as closely as they admire how it handled the last modest one. With the human and governance picture drawn, we can war-game the competitive position itself.

VIII. Strategic Position: Helmer's 7 Powers and Porter's 5 Forces

Strip away the drama and ask the cold strategist's question: what, exactly, protects Daiichi Sankyo's economics from competition, and for how long? Two frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — help us pressure-test the moat rather than admire it.

Helmer's 7 Powers

Cornered resource — the primary power. The DXd platform is the closest thing Daiichi Sankyo has to a genuine cornered resource: a body of patented chemistry — the specific exatecan-derivative payload, the hydrophilic tetrapeptide cleavable linker, and the conjugation method that achieves high, stable payload loading — that has repeatedly produced superior efficacy across multiple targets where rivals stumbled.1516 The evidence for this power is not a single drug but the hit rate: HER2, TROP2, HER3, B7-H3, CDH6 — the same recipe re-aimed and working again and again. That repeatability is what convinced AstraZeneca and Merck to pay platform prices. The obvious question a skeptic asks is durability: patents expire, and rival ADC chemistries are advancing fast. The cornered resource is real today; it is not permanent.

Process power — the secondary, and underrated, power. Making an ADC is not like pressing a pill. Consider what the manufacturing actually involves: you must grow a monoclonal antibody in living cells, separately synthesize a payload potent enough that a stray milligram is a workplace hazard, chemically bolt an average of eight of those payloads onto each antibody with enough consistency that the whole batch behaves identically in a patient, and do all of it under sterile conditions, at commercial scale, with regulators auditing every step. A batch that comes out with the wrong average payload count, or with aggregation, or with a trace contaminant, is not a discount product — it is unusable. This is a multi-step manufacturing art that is not fully captured in any patent or manual; it lives in the accumulated tacit knowledge of the people and facilities that have done it thousands of times. Daiichi Sankyo deliberately kept this in-house rather than outsourcing to contract manufacturers. That non-codified process knowledge is genuinely hard for competitors to replicate quickly, and it is why the company could credibly promise AstraZeneca and Merck that it alone would handle global supply. The flip side, examined in the bear case, is that this same choice concentrates operational risk in facilities Daiichi Sankyo cannot easily substitute.

Scale economies. By partnering rather than going it alone, Daiichi Sankyo effectively rented global scale — in trial enrollment and commercial reach — spreading the fixed costs of development across far larger international sales bases than it could have supported itself. This is a borrowed scale advantage more than an owned one, which is an important nuance.

The powers it doesn't have. Helmer's discipline is as much about what's absent as what's present. Daiichi Sankyo has no meaningful network economies — a doctor prescribing Enhertu creates no direct value for the next prescriber. It has limited switching costs in the durable sense; oncology prescribing follows the data, and a superior competitor drug can displace an incumbent as quickly as Enhertu displaced Kadcyla. And its branding power, while growing, is of a specific clinical kind: oncologists have come to associate the DXd family with efficacy, which lowers the friction of adopting the next DXd drug and shapes trial-design expectations. That reputational tailwind is real but conditional — it survives exactly as long as the clinical readouts keep validating it, and an ambiguous result like TROPION-Lung01 chips at it. In short, the moat rests overwhelmingly on the cornered resource and the process power, not on the softer, stickier powers that protect consumer franchises. That makes the platform's continued scientific productivity not one factor among many, but the load-bearing wall of the entire investment case.

Porter's Five Forces

Threat of new entrants: low. Building a competitive ADC franchise demands specialized chemistry, oncology commercial infrastructure, and fiendishly complex supply chains — a capital and know-how barrier that keeps the field small.

Bargaining power of buyers: high in Japan, moderate-to-high in the U.S. In Japan, the single-payer NHI system dictates near-annual price cuts. In the U.S., Medicare gained the power to negotiate certain drug prices under the Inflation Reduction Act, putting high-priced oncology blockbusters squarely in the future crosshairs. Since the U.S. is Daiichi Sankyo's profit engine, this is the force that matters most.

Bargaining power of suppliers: low. The upstream chemical reagents and biological inputs are relatively commoditized; suppliers hold little leverage.

Threat of substitutes: moderate. ADCs are the leading solid-tumor modality of the moment, but bispecific antibodies, cell therapies like CAR-T, and radiopharmaceuticals are all advancing and could claim share over time.

Competitive rivalry: very high. Daiichi Sankyo is fighting the heavyweights — Roche (Kadcyla and beyond), Gilead (Trodelvy in TROP2), Pfizer (which bought its way into ADC leadership via Seagen), and AbbVie among them. The ADC field has become one of oncology's most crowded battlegrounds precisely because Daiichi Sankyo proved the category could work.

The composite picture: a strong, evidence-backed platform power and a rare process power, wrapped inside an industry where buyers (governments) and rivals both press hard. The moat is real but bounded — which is exactly why the bull and bear cases are both credible.

IX. Stress Test: Bull Case, Bear Case, and Risk Radar

The bull case: why this company wins from here

The optimist's argument rests on the word we keep returning to: platform. A single-molecule drugmaker is a binary bet on one trial. Daiichi Sankyo has converted drug discovery into something closer to a repeatable industrial process, and the bull case is that the process keeps producing. Enhertu itself is still expanding — into earlier lines of therapy, into ever-lower HER2 expression thresholds, and across a widening set of HER2-expressing solid tumors from gastric to lung to colorectal, with tumor-agnostic ambitions. Each new indication is incremental revenue on an already-built commercial base.

The mechanics of that expansion matter, because they explain why the bull case is more than hope. Every time Enhertu wins approval in an earlier line of therapy or a lower HER2-expression threshold, it enlarges the eligible patient pool without a proportionate increase in the fixed cost of the commercial machine already selling it — the definition of operating leverage. A drug that started in heavily pretreated, late-line patients moving toward first-line and adjuvant settings is a drug moving toward far larger populations of earlier, healthier patients who stay on therapy longer. The same salesforce, the same brand, more patients: that is how a franchise compounds.

Layered on top is the Merck pipeline optionality. If even one or two of the three Merck-partnered ADCs approach a fraction of Enhertu's success, Daiichi Sankyo collects high-margin milestones and profit share — with Merck footing much of the development bill. This is optionality with someone else's money at risk, which is the most attractive kind. And the mix shift itself is a margin story: as high-margin oncology revenue outgrows the low-margin primary-care legacy, corporate operating margins have structural room to expand from the mid-teens toward materially higher levels — the arithmetic embedded in that fiscal-2030 target of operating profit growing far faster than revenue. Win, and Daiichi Sankyo is a durable global oncology platform compounding on validated chemistry, no longer dependent on any single molecule.

The bear case: what breaks the story

The pessimist starts with concentration. This is now, to a first approximation, a one-drug growth company. The entire equity story leans on Enhertu, and the TROPION-Lung01 experience is the cautionary tale: the platform does not guarantee every molecule works, and a serious clinical miss on a major Merck-partnered asset — or a setback in one of Enhertu's expansion trials — could vaporize billions in expected value and cap the growth narrative.

The second pillar of the bear case is timing. The Lixiana cliff is coming, and the primary-care base is eroding under Japanese price cuts. If oncology growth decelerates even modestly while the legacy melts, the transition stalls and the whole "engine swap" thesis wobbles.

Third is the manufacturing paradox. The in-house supply chain that Helmer's framework counts as a process power is, from the bear's seat, a single point of failure. A contamination event, a facility shutdown, or a supply disruption at a plant that Daiichi Sankyo alone operates would instantly choke global Enhertu supply and inflict severe financial and reputational damage — with no second source to fall back on.

Fourth is the IRA sword of Damocles. A high-price, high-margin oncology blockbuster earning most of its money in the United States is the archetypal target for future Medicare price negotiation. The very concentration of profit in the U.S. that makes the bull case also makes the drug a policy bullseye.

An activist skeptic would add sharper points: that Japanese governance and modest executive equity ownership blunt shareholder accountability; that the celebrated non-dilutive structure means Daiichi Sankyo has permanently given away half the economics of its best assets outside Japan; and that the redemption narrative has never been tested in a genuine downturn, because Enhertu has masked everything.

The competitive war-game

The bear case sharpens when you look at who is coming. Daiichi Sankyo proved ADCs work, and proof invites imitation. Gilead's Trodelvy is a direct TROP2 competitor to Dato-DXd, meaning Daiichi Sankyo's second ADC franchise is fighting an entrenched rival rather than inventing a category the way Enhertu did — a materially harder commercial task, and a reason the TROPION-Lung01 ambiguity stings more than it otherwise might. Pfizer bought its way to the front of the ADC pack by acquiring Seagen, the field's original pioneer, for a total enterprise value of roughly $43 billion in a deal announced in March 2023, signaling that the largest balance sheets in pharma now treat ADCs as a must-win battleground.25 Roche, humbled in HER2 by Enhertu's defeat of its own Kadcyla, is reinvesting across oncology. And a wave of Chinese biotechs has begun out-licensing next-generation ADCs to Western partners at aggressive prices, threatening to commoditize the very "platform premium" that Daiichi Sankyo has enjoyed.

The competitive lesson is double-edged. Daiichi Sankyo's first-mover advantage in the DXd era is real and has bought it years of lead and a validated brand among oncologists. But first movers in pharma do not enjoy permanent moats; they enjoy a head start that patents and know-how can defend only for a finite window. The company's ability to keep re-earning its edge — through the Merck-partnered pipeline and Enhertu's own relentless label expansion — is what separates a durable platform from a spectacular but fading first act.

The risk radar

The material, mechanism-specific risks are therefore four, and each has a concrete transmission channel worth naming. Clinical and pipeline risk is the most acute: because value is concentrated in Enhertu and the Merck-partnered assets, a single high-profile Phase III failure — or a safety signal serious enough to constrain a label, as interstitial lung disease has threatened to do — translates directly into billions of erased expected value and a re-rating of the whole platform premium. Regulatory pricing risk operates through the payers: Japan's NHI cuts prices almost every year by administrative fiat, and the U.S. Inflation Reduction Act now lets Medicare negotiate prices on selected high-spend drugs, so the very success that makes Enhertu a blockbuster also paints it as a future negotiation target in the market where it earns the most. Manufacturing and supply-chain risk flows from the in-house single-source model: with no contract-manufacturer backstop, a contamination event or facility shutdown converts instantly into a global supply interruption for a life-saving cancer drug. And patent-cliff timing risk is a matter of the calendar: Lixiana's exclusivity is finite, and if oncology growth cools before the cliff arrives, the transition math turns hostile.

Macro risks that don't map to a real mechanism here — generic inflation-and-rates hand-wringing — matter far less than these four. One genuine second-layer item does deserve a note: the company's transformation has been financed in part by partner cash rather than by its own retained operating cash flow, so an investor should keep an eye on how self-funding the oncology engine becomes as milestone-and-upfront income (which is inherently lumpy) gives way to recurring product economics. The quality of earnings, not just the quantity, is the thing to watch as the mix matures.

The 1–3 KPIs that actually matter

For an investor tracking this company, the noise-to-signal ratio is best managed by watching a very short list:

- Enhertu global product sales growth, especially in the U.S. and Europe — the single clearest read on whether the engine is still accelerating.

- Merck-partnered ADC clinical readouts, patritumab deruxtecan (HER3-DXd) foremost — the test of whether the platform is truly repeatable or whether Enhertu was singular.

- Core operating margin expansion — the proof, or disproof, that the shift from low-margin primary care to high-margin oncology is translating into structurally better profitability, and the metric against which the fiscal-2030 ambition will ultimately be judged.

Note what is deliberately not on this list. Total revenue growth is too coarse — it blends the rising oncology engine with the fading legacy book and obscures both. Reported net profit is too noisy, distorted by the milestone lumpiness and one-off items already discussed. The three metrics above isolate the actual load-bearing questions: is the engine still accelerating, is the platform repeatable beyond its first hit, and is the growth translating into durable profit. Everything else is detail. Which points to the broader lessons this story holds for anyone thinking about businesses, not just biotech.

X. Business & Investing Lessons

The power of platforms. The deepest lesson of Daiichi Sankyo is the difference between owning a drug and owning a method. A single-molecule biotech is a coin flip dressed up as a company; a validated chemical platform turns discovery into something closer to portfolio manufacturing, where each new target is a fresh draw from the same well-understood process. That structural lowering of R&D risk is what the market ultimately rewarded — and it is why the most valuable question about any research-driven company is whether it has a repeatable engine or just a lucky hit. Daiichi Sankyo's own history warns against complacency here: a platform's edge is real but time-boxed by patents and rivals, and must be re-earned.

The fallacy of the hybrid model. Ranbaxy is the negative image of the platform lesson. The attempt to be both a low-cost, high-volume generics operator and a high-risk, high-margin innovator did not double the company's strengths; it fractured its focus and imported a quality culture incompatible with everything Daiichi Sankyo stood for. Capabilities, cultures, and quality systems do not blend on command. The company only found its footing when it divested the hybrid dream and committed fully to proprietary science. Diversification that dilutes focus is not a hedge — it is a second way to lose.

Due diligence is a test of discipline, not intelligence. There is a fourth lesson buried in the Ranbaxy wreckage that generalizes far beyond pharma. The information that would have killed the deal was, in retrospect, findable — a whistleblower had already documented the problems, and the regulatory warning signs were flashing. Daiichi Sankyo's failure was not a failure of access; it was a failure of will. When a strategy feels too important to abandon, the organization stops asking whether it should. The most dangerous acquisitions are not the ones where the buyer knows too little, but the ones where the buyer wants the deal too much to look hard. The discipline to run the audit that might blow up your own thesis is the rarest and most valuable trait in corporate M&A — and its absence is the common thread through most of history's great deal disasters.

Weaponizing non-dilutive capital. The final lesson is the most sophisticated, and the most double-edged. Facing the need to fund global trials and a worldwide sales force, Daiichi Sankyo refused both the dilution of a big equity raise and the outright sale of its crown jewels. Instead it monetized partnership upfronts from AstraZeneca and Merck to finance its own transformation — surrendering roughly half the long-run economics outside Japan in exchange for the cash, the shared risk, and, above all, continued control of the platform and the factory. Whether that was brilliant or merely expensive depends on how many more winners the DXd engine yields. But the underlying move is a template worth studying: when you own something rare, the goal is not to maximize the next cheque. It is to fund your independence while keeping your hands on the thing that made you rare in the first place.

Daiichi Sankyo began as a discovery house that once let the statin get away, nearly destroyed itself chasing a hybrid it could not run, and was rescued by a small team solving a chemistry problem the giants had abandoned. The company that emerged is neither the cautionary tale of 2009 nor the invincible platform of the press releases. It is something more interesting: a business that learned, at enormous cost, the difference between what it could do and what it should — and whose future now rides on proving that its greatest breakthrough was a method, not a moment.

References

-

Daiichi Sankyo Acquires Generic Drug Maker Ranbaxy Laboratories for $4.6 Billion — Jones Day, 2008 ↩

-

Daiichi Sankyo and AstraZeneca Announce Global Development and Commercialization Collaboration for HER2 Targeting ADC Trastuzumab Deruxtecan (DS-8201) — Daiichi Sankyo, 2019-03-29 ↩↩↩

-

Daiichi Sankyo and AstraZeneca Enter New Global Development and Commercialization Collaboration for Daiichi Sankyo's ADC DS-1062 — Daiichi Sankyo, 2020-07-27 ↩↩

-

Daiichi Sankyo and Merck Announce Global Development and Commercialization Collaboration for Three Daiichi Sankyo DXd ADCs — Merck, 2023-10-19 ↩↩

-

Researcher Dr. Jokichi Takamine's Success in the Crystallization of Adrenaline — Daiichi Sankyo, Our Stories ↩↩

-

History of Daiichi Pharmaceutical Co., Ltd. — Daiichi Sankyo ↩

-

Akira Endo: Father of Statins — PMC (US National Library of Medicine) ↩

-

Daiichi Pharmaceutical / Sankyo Integration Form F-4 — SEC EDGAR, 2005 ↩

-

Ranbaxy-Daiichi affair: How & why the deal went south — Business Standard, 2016-08-11 ↩↩

-

Daiichi Sankyo Records Valuation Loss / Goodwill Write-down on Investment in Ranbaxy Laboratories — Daiichi Sankyo, 2009-01-05 ↩

-

Generic Drug Manufacturer Ranbaxy Pleads Guilty and Agrees to Pay $500 Million to Resolve False Claims Allegations, cGMP Violations and False Statements to the FDA — HHS Office of Inspector General / U.S. DOJ, 2013-05-13 ↩

-

Daiichi Sankyo to sell Ranbaxy to Sun Pharmaceutical — Reuters, 2014-04-07 ↩

-

Daiichi Sankyo sells its entire stake in India's Sun Pharma for $3.25bn — Pharmaceutical Technology, 2015-04-21 ↩

-

Ranbaxy Owners Deliberately Buried Information From Daiichi Sankyo, Singapore Tribunal Ordered — BioSpace, 2016 ↩

-

DS3790 Enters Clinical Development as First DXd ADC in Hematology (DXd platform description) — Daiichi Sankyo, Inc., 2026-02-04 ↩↩↩

-

The clinical development of antibody-drug conjugates for non-small cell lung cancer therapy (trastuzumab deruxtecan DAR 8 and bystander effect) — Frontiers in Immunology, 2023 ↩↩↩↩

-

FDA Approves Enhertu for Unresectable or Metastatic HER2-Low Breast Cancer (DESTINY-Breast04) — Breastcancer.org, 2022-08-04 ↩

-

Daiichi Sankyo and Merck DXd ADC Collaboration press release (PDF) — Daiichi Sankyo, 2023-10-20 ↩

-

FY2025 Financial Results and 5-Year Business Plan Presentation — Daiichi Sankyo, 2026-05-11 ↩↩↩↩↩↩

-

Reference Data for FY2025 (Year Ended March 31, 2026) — Daiichi Sankyo, 2026-05-11 ↩↩

-

DAICHIRONA for Intramuscular Injection Approved in Japan as Omicron XBB.1.5-adapted Monovalent mRNA Vaccine (PDF) — Daiichi Sankyo, 2023-11-28 ↩

-

Daiichi Sankyo Appoints Hiroyuki Okuzawa as Chief Executive Officer (PDF) — Daiichi Sankyo, 2025-01-31 ↩↩

-

Datopotamab Deruxtecan Met Dual Primary Endpoint of Progression-Free Survival in TROPION-Lung01 Phase 3 Trial — Daiichi Sankyo, Inc., 2023-07-03 ↩

-

Pfizer to Acquire Seagen for $43 Billion (Form 8-K exhibit) — Pfizer Inc. / SEC EDGAR, 2023-03-13 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube