Midea Real Estate: The Manufacturing Mindset in a Bricks-and-Mortar World

I. Introduction: The "Other" Midea

If you walked through the glass-and-steel forest of Shenzhen Bay in the autumn of 2023, you could feel the shudder of a civilization-scale deleveraging. Evergrande's once-sparkling lobby in Shenzhen had become a pilgrimage site for journalists cataloguing the ruin—$300 billion in liabilities, unfinished towers rusting across three hundred cities, and a founder who once owned the largest private yacht in Asia now under "residential surveillance." Country Garden, which had sold more apartments in 2020 than any developer in human history, was cycling through restructuring advisors. Sunac, Shimao, Kaisa, Logan—each name used to rhyme with wealth. Each, by early 2024, rhymed with default.

And yet, buried in the middle of that rubble, tucked into a corner of the Hong Kong Stock Exchange under the ticker 3990.HK, a developer kept completing buildings. On time. With working elevators. With occupancy certificates. The company was Midea Real Estate Holding Limited—and if you stopped a Chinese homebuyer in Foshan or Zhuhai and asked them to name a developer they still trusted, this was the name they murmured. Not Vanke. Not Poly. Midea.

The thesis of this episode is deceptively simple. Midea Real Estate survived the most violent property bust in modern economic history because it was never, in spirit, a property company. It was a manufacturer that happened to make apartments. Its DNA was traceable to a rice-cooker and air-conditioner empire built in the rural outskirts of Foshan by a man named He Xiangjian, one of China's reform-era legends. When the Chinese state drew its three red lines across the industry in 2020, Midea Real Estate crossed none of them. When peers were paying 12% on dollar bonds in distress, Midea was tapping domestic credit at 4%. When the music stopped, Midea still had a chair, a drink, and a reputation.

Then, in June 2024, management did something that even the sell-side analysts who loved them did not see coming. They announced that the entire property development business—the thing the company had been built on, the engine that had produced tens of billions of renminbi in annual contracted sales—would be carved out and handed back to the controlling shareholder. The listed vehicle would shrink, return cash to minority shareholders, and re-emerge as a light-asset property services and technology firm. For a sector where every CEO still believed the next land auction would bring the cycle back, it was heresy. For Midea's management, it was arithmetic.

This is the story of how a family office real estate side-project grew into a Top 20 Chinese developer, how it avoided the asteroid that killed most of its peers, and why—having survived—it chose to walk away from the very business that had made it famous. It is also the story of a question every investor in Chinese property is now being forced to answer. If the "golden era" is truly over, what does the after-picture look like? Midea Real Estate has decided to draw that picture first.

From a family office housing project in the mid-1990s to the 2018 Hong Kong listing, from the Three Red Lines crackdown to the 2024 restructuring bombshell—this is how a company built on rice cookers ended up rewriting the rules of real estate.

II. Origins: The Appliance Halo

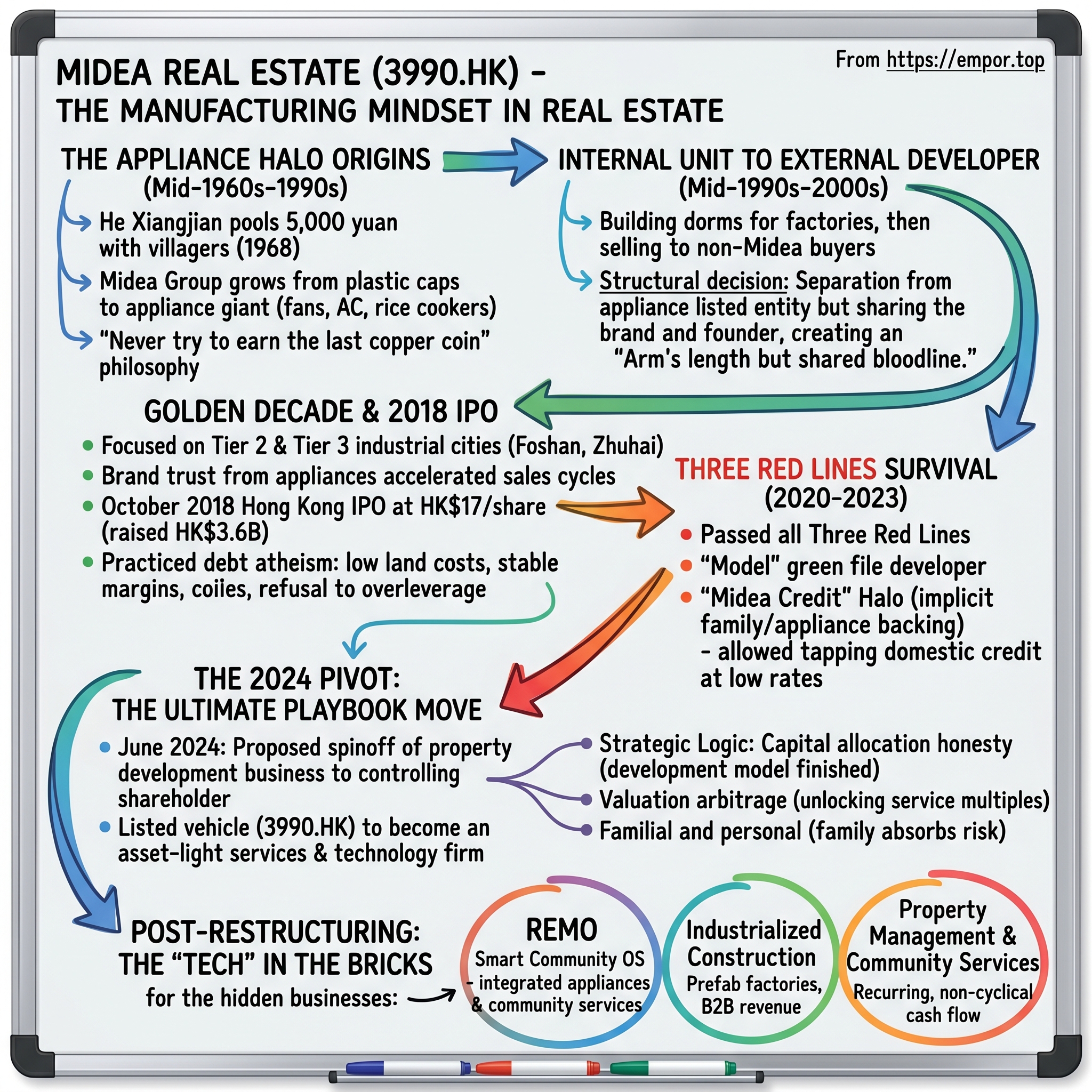

The village of Beijiao sits in the southern curl of the Pearl River Delta, about thirty kilometers from the center of Foshan in Guangdong Province. In the late 1960s, it was a cluster of fishponds, mulberry fields, and dirt paths. If you had visited then and told the locals that this unremarkable town would one day host the headquarters of the world's largest home appliance manufacturer, with roughly a million people directly or indirectly depending on its factories, they would have thought you were delirious.

He Xiangjian would have been one of them. A junior high school graduate with a bookkeeper's handwriting and an unusual appetite for risk, He founded what became Midea Group in 1968 by pooling 5,000 yuan with twenty-three villagers to make plastic bottle caps. The company moved into fans in the 1980s, air conditioners in the 1990s, and then everything else—rice cookers, microwaves, washing machines, kitchen ranges. By the time Midea listed its appliance arm on the Shenzhen Stock Exchange in 2013, He Xiangjian had become one of China's richest men. He was famously soft-spoken, almost allergic to press attention, and disdained the flamboyance that characterized many of his peers. When Forbes asked him in an interview how he had built Midea, he replied with a phrase that would become family scripture: "Never try to earn the last copper coin."

That philosophy is the invisible genetic code of Midea Real Estate. To understand the property company, you have to first understand that its founder's father ran the appliance business as a cost-control monastery. Midea Group's operating culture was obsessive about bill of materials, supplier consolidation, factory throughput, and post-sale warranty cost. These are manufacturing habits. They are not the habits of Chinese real estate developers in the 1990s and 2000s, who were essentially leveraged land speculators in hard hats.

The real estate arm began quietly, the way most family office projects do. As Midea Group's factories expanded through Beijiao in the mid-1990s, the workforce ballooned. Housing dormitories, married-worker apartments, school complexes, and staff canteens had to be built. Outsourcing this to local developers was expensive, slow, and produced shoddy work. So the He family set up an internal construction and property unit to handle it. By the early 2000s, the unit had a side business selling commercial apartments to non-Midea buyers in the surrounding towns, riding the early wave of Chinese home ownership reform.

The critical structural decision came when the He family separated Midea Real Estate from the appliance group entirely. Rather than parking it as a subsidiary of the listed appliance company—where it would be subject to the manufacturing board's capital discipline and the appliance investors' low tolerance for property risk—they housed it under a separate family holding vehicle. The appliance business and the real estate business shared a brand, shared a supply chain for cooling and white goods, and shared a founder, but they did not share a balance sheet. This "arm's length but shared bloodline" arrangement is the single most important structural fact about the company. It meant that when the property sector melted down, the appliance cash flows were not contaminated. It also meant that when Midea Real Estate needed to borrow, Chinese lenders looked across the street at the appliance empire and concluded, correctly, that this was a family that could not afford to let a Midea-branded entity default.

That shared bloodline gave Midea Real Estate something no other developer had. It had a halo before it had a product.

III. The Golden Decade and the IPO Inflection

By 2010, the Midea real estate unit had graduated from building dormitories for forklift operators into selling condominium towers to rising middle-class families. The China that emerged from the 2008 global financial crisis was, for developers, something close to paradise. The government's four-trillion-yuan stimulus had flooded the system with construction credit, local governments were addicted to land sale revenues, and the urban population was adding the equivalent of a Belgium every year. Anyone with a trowel and a bank relationship could become a billionaire.

Midea's expansion strategy in this period diverged in one quiet but important way from its competitors. The big national developers—Vanke, Country Garden, Sunac—were fighting each other for "trophy land" in Beijing, Shanghai, and Shenzhen, bidding premiums of 80% or more over starting prices for parcels where the math only worked if property prices kept rising at double-digit rates forever. Midea's land team, trained by the appliance side, refused to play that auction. Instead, they focused on second- and third-tier cities in the Yangtze and Pearl River Delta industrial belts, cities like Foshan, Zhongshan, Zhuhai, Wuxi, and Hefei. Two things distinguished these markets. First, land was cheaper, and the bidding was less insane. Second—and this is the understated strategic genius of it—these were cities where the Midea brand already had something approaching total consumer awareness. When a family in Jiangmen or Zhaoqing saw a Midea-branded residential development going up, they did not see a faceless developer. They saw the company that made their refrigerator, their air conditioner, and their grandmother's rice cooker.

That brand trust translated directly into sell-through speed. Midea projects routinely sold out their opening phases in days, sometimes hours. Fast sell-through is the most valuable unit of time in Chinese real estate, because the entire business model runs on a cycle: buy land, get construction loan, pre-sell units, use deposit cash to fund build-out, hand over keys, release mortgage proceeds. The shorter the cycle, the higher the return on capital. Midea's cycle was faster than most peers, and its marketing budget per unit sold was lower, because the brand did half the work.

Which brings us to October 11, 2018. Midea Real Estate Holding Limited listed on the Hong Kong Stock Exchange at HK$17 per share, raising roughly HK$3.6 billion. The timing, with the benefit of hindsight, was magnificent. The Chinese property cycle had already shown its first cracks—Beijing had begun deploying its "houses are for living in, not for speculating" framework under Xi Jinping—and the Hong Kong IPO window for developers was closing fast. Midea squeezed through the door at a valuation below its book value, which the market saw as conservative but which management treated as permanent ammunition. The listing converted Midea Real Estate from a private family vehicle into a transparent, institutional-grade, ratings-eligible developer. It also created a public currency for future acquisitions and, critically, a public accountability standard that would later force discipline when the sector went mad.

From 2018 through 2020, Midea's contracted sales roughly doubled, moving the company firmly into the Top 20 national developer rankings. But read the annual reports from those years side by side with Evergrande's or Sunac's, and a pattern jumps out. Midea's land bank turnover was faster. Its average land cost as a percentage of selling price was lower. Its gross margin, while not spectacular, was stable in the 25%-30% band. And its net debt-to-equity ratio refused to climb past roughly 80% even as competitors routinely operated above 150%. In a sector where leverage was a religion, Midea was practicing atheism.

The market rewarded this discipline with a shrug. Through 2019 and 2020, Midea's stock traded at a price-to-book ratio below one, sometimes well below one. Investors who saw real estate as a single monolithic sector lumped Midea in with the speculators. It would take a full-scale industry collapse for the market to learn the difference.

IV. Survival: The "Midea Credit" Halo

On the afternoon of August 20, 2020, officials from the People's Bank of China and the Ministry of Housing and Urban-Rural Development gathered representatives from the country's largest developers in a conference room and quietly introduced a new regulatory framework. It would come to be known as the Three Red Lines. The rules were simple in statement and devastating in application. Liabilities-to-assets ratio excluding advance receipts must stay below 70%. Net debt-to-equity must stay below 100%. Cash-to-short-term debt must be at least 100%. Cross any one line, and your ability to add new interest-bearing debt would be capped. Cross all three, and you were frozen out entirely, unable to roll a single bond.

What followed was a slow-motion industry extinction event. Evergrande, which had crossed all three lines by a wide margin, defaulted on offshore bonds in late 2021 and began its death spiral. Country Garden, which had stayed nominally inside the lines through accounting creativity, discovered in 2022 and 2023 that without the ability to aggressively lever, its extraordinary 2020 sales volume had been a mirage. Sunac defaulted. Shimao defaulted. Fantasia defaulted on a bond it had solemnly told the market the day before it would not default on. By the middle of 2023, somewhere between 40 and 50 of the top 100 Chinese developers had missed a payment on offshore or onshore debt.

Midea Real Estate crossed zero of the three lines. It was one of a handful of private developers designated by the regulators as a "model" or "green file" developer, alongside names like Longfor and a small number of state-backed firms. This was not a happy accident. The conservative balance sheet that the market had mocked in 2019 turned out to be the only balance sheet that mattered in 2022.

But there is a second, subtler story inside the survival narrative, and it is the story of the "Midea Credit" halo. In 2022 and 2023, even developers who were technically in compliance with the Three Red Lines often could not borrow, because the capital markets had closed reflexively around anything that smelled of Chinese property. Offshore dollar bonds from distressed Chinese developers traded at yields above 20%, implying near-certain default. Onshore issuance was gated by quotas. Bank credit officers, terrified of making the next headline default, slow-walked every application.

Midea Real Estate, by contrast, was able to tap onshore credit at rates that hovered in the mid-single digits, and at times issued domestic medium-term notes priced below the industry average for even state-owned developers. Why? Because when a Chinese bank looked at a Midea Real Estate credit application, they were not really looking at Midea Real Estate. They were looking at the implicit backing of the He family, the visible liquidity of Midea Group, and the near-certainty that the family would rather inject capital from the appliance empire than allow a Midea-branded default to scar the family name for a generation. This was not disclosed as an explicit credit enhancement. There was no formal guarantee. There did not need to be. In Chinese credit culture, the family's face—mianzi—was worth more than most written covenants.

The halo compounded. Homebuyers, who in 2022 and 2023 were cancelling purchase contracts on distressed developers in what Chinese media dubbed the "mortgage strike," continued to buy Midea units. In a market paralyzed by fear that a developer would take a buyer's down payment and then fail to complete the building, Midea's delivery record became, quietly, the most valuable marketing asset in the sector. The company leaned into it. It published project completion timelines, invited buyers onto construction sites, and made "handover on schedule" a marketing tagline. When trust was the rarest commodity in Chinese property, Midea used its balance sheet to buy it wholesale.

Through 2023, the company continued to complete tens of thousands of residential units, honor mortgage linkage commitments, and pay coupons on every outstanding note. Contracted sales declined, because the whole market had declined—but the decline was softer than peers, and the quality of remaining sales was higher. The thing that was supposed to destroy them had, perversely, turned them into the most credible brand in an industry that had lost credibility as a category.

And that credibility is exactly what made the 2024 announcement so stunning.

V. The 2024 Pivot: The Ultimate Playbook Move

On the evening of June 23, 2024, after the Hong Kong market had closed, Midea Real Estate Holding Limited filed a circular with the exchange that was so unusual it took analysts twenty-four hours to understand what they were reading. The company was proposing to spin off its property development business in a scheme of arrangement. The listed entity, 3990.HK, would retain the asset-light businesses—property management services, the industrialized construction unit, and the smart home integration operations. The heavy-asset property development business, including the remaining land bank and the work-in-progress residential projects, would be transferred to a private company controlled by the He family. Minority shareholders would receive a cash distribution as consideration.

In the language of Hong Kong takeover practice, this was effectively a partial privatization. The family was using its own capital to buy the development business out of the listed vehicle, and leaving minority shareholders with two things: a cash payment, and a residual equity interest in a much smaller, asset-light company that would continue to trade on the exchange. The announcement was approved by independent shareholders at the required supermajority in the ensuing months, and the restructuring proceeded through the back half of 2024 and into 2025.

Reading the circular carefully, the strategic logic emerges in three layers. The first layer is capital allocation honesty. Management had concluded, and said so in plain language, that the Chinese property development model as it had existed since the 1998 housing reform was finished. Not paused, not cyclical, finished. Demographics had turned, urbanization had matured, household balance sheets had become saturated with property, and the regulatory regime had made explicit what had always been implicit—the Chinese state would no longer tolerate real estate as a vehicle for leveraged wealth creation. In that world, a company that insisted on remaining primarily a property developer was asking its shareholders to accept a structurally declining business. Midea's management refused to ask that.

The second layer is the valuation arbitrage. The public market, by 2024, had decided that it would never again pay a growth multiple for a Chinese property developer. The implied earnings multiple for the sector was somewhere between three and six times—a kind of market signal that said, "we do not believe your future cash flows." But within the same company, the property services business, the industrialized construction business, and the smart home integration business were growing double digits, required almost no incremental capital, and, if separated, could plausibly trade at the higher multiples that the market was willing to pay for capital-light service and technology businesses. By separating the two, management could unlock a valuation that the conglomerate structure was suppressing.

The third layer was familial and personal. He Jianfeng, the chairman, owned somewhere between 70% and 80% of the company through holding vehicles. Taking the heavy-asset development business private did not impoverish the family; it simply moved the risk from minority shareholders onto the family balance sheet. If the property cycle recovered, the family would capture the upside privately. If it did not, the family would absorb the wind-down privately. Either way, the listed vehicle that carried the Midea name was freed from the specific balance sheet and news-cycle risk of the development business. It is hard to overstate how unusual this is in Chinese corporate governance. The normal pattern, when a controlling family restructures, is to extract value into the family and leave risk with the minority. Midea did the opposite.

The 2024 pivot, in other words, was not a retreat. It was a reallocation. The family took the cyclical part back into the private domain, where it belonged, and left the compounding part on the exchange, where it could be valued properly. Whether the market fully processes that distinction remains an open question. But as a declaration of strategic intent, it was among the cleanest we have seen in Chinese capital markets in a decade.

Which raises the obvious question: what, exactly, is the compounding part?

VI. Hidden Businesses: The "Tech" in the Bricks

Walk through a finished Midea residential community in 2025, and the first thing you notice is that it does not look like a typical Chinese residential compound. The lobby scanner recognizes your face and routes the elevator to your floor before you have tapped a button. The apartment, when you step in, is pre-provisioned with a suite of Midea appliances integrated into a single control panel and a mobile app. The air conditioner adjusts to your circadian pattern. The refrigerator tracks staple inventory and flags an automatic reorder. The lighting, the blinds, the doorbell camera, the water heater—all live on a common protocol, all piped into the Midea cloud. The community itself is managed by a Midea property services subsidiary that handles everything from garbage collection to package delivery through a single app. This is not a pitch deck. This is the actual product.

The brand Midea uses for this smart-home integration layer is REMO. It is, in effect, a consumer-facing smart community operating system, and it is one of the most strategically interesting assets inside the post-restructuring entity. REMO works because Midea Real Estate uniquely sits at the intersection of two hard-to-reach populations. It has construction-stage access to physical residential space, meaning it can wire in sensors and infrastructure at build time, rather than retrofitting, which is always cheaper. And through the Midea Group sister relationship, it has access to the entire catalog of Midea appliances, HVAC systems, and IoT devices, which it can bundle at cost into the community offer. A third-party smart home integrator cannot replicate that stack. A third-party developer can buy the appliances, but cannot replicate the brand trust and technical integration that comes with the Midea umbrella. This is a cornered resource in the Hamilton Helmer sense, and we will come back to it.

The second hidden business is industrialized construction, sometimes translated as "prefab" or "prefabricated construction." If REMO is the tech layer, industrialized construction is the factory layer. Traditional Chinese residential construction, even at scale, is astonishingly artisanal. Concrete is mixed on site, rebar is bent on site, walls are poured on site, finishes are installed on site by migrant labor crews whose quality varies by crew. Industrialized construction replaces that with factory-produced modules—pre-cast wall panels, pre-installed bathroom pods, pre-wired electrical spines—that are trucked to the construction site and assembled like a car on a line. The cost savings and quality gains compound across thousands of units.

Midea's industrialized construction arm is, not coincidentally, a direct cultural import from the appliance side. The engineers who run it speak the language of takt time, yield rates, and first-pass-quality, not the language of land bids and launch events. They have extended the service outside the Midea group, selling prefab modules and design services to other developers and, increasingly, to local-government-sponsored "affordable housing" programs that the Chinese state has pushed hard since 2023 as a replacement for speculative development. This is a B2B revenue stream that does not depend on Midea's own land pipeline, which is precisely the kind of revenue the post-restructuring entity needs.

The third business is the property management and community services layer. Chinese property management, historically, was a low-quality, low-margin, lightly regulated afterthought. But the same demographic forces that are squeezing development are expanding property management. Every apartment ever sold in China is a permanent, recurring customer for someone, and that someone is increasingly a branded property management company. Midea's subsidiary manages millions of square meters under management, across in-house developments and a growing book of third-party mandates, and generates high-single-digit to low-double-digit margins on a recurring, non-cyclical revenue base. In the post-2024 structure, it is the most stable cash flow engine the company has.

Tie the three together, and you get a picture that looks very little like a developer. You get a property services operator, a smart-home platform, and an industrial prefab factory sharing a brand, a customer base, and a cross-sell motion. Non-development revenue has been rising as a share of the group's EBITDA mix for years, and after the 2024 spinoff, it becomes effectively the entire business. That is the arithmetic management was doing.

It is also why the management team deserves its own section.

VII. Management and Incentives

He Jianfeng, who serves as chairman of Midea Real Estate, is the second son of founder He Xiangjian, and in the Chinese business family lexicon, he is the "design-minded" successor. His older brother He Jianfeng's elder sibling, and other family members, took on different roles across the broader Midea ecosystem, but He Jianfeng's specific mandate was real estate. He was, in a sense, given a portion of the family's reinvested wealth and told to build something of his own. He has a reputation inside the organization for being cerebral, slightly reclusive, and almost obsessive about balance sheet conservatism. In a sector where chairmen were, for two decades, larger-than-life figures who bought football clubs, movie studios, and personal jets, He Jianfeng kept a profile so low that many Chinese retail investors would not recognize his face.

That temperament is not a coincidence. It is the governance reflection of the founding patriarch's "never try to earn the last coin" philosophy. He Jianfeng controls his stake through a holding structure centered on Midea Development Holding, and those holdings add up to an effective controlling interest that sits comfortably above the two-thirds supermajority threshold used in Hong Kong corporate law. In practical terms, he is aligned with long-term survival rather than quarterly optics because he essentially owns the company. He does not need to juice earnings to satisfy a board, because he is the board. And he does not need to protect a dividend yield for income-oriented minority holders, because the minority is numerically small relative to his position. That ownership concentration cuts both ways—it can be an accountability concern in governance, which we will flag—but through the 2020-2024 crisis it was unambiguously an asset, because it allowed the chairman to make long-horizon decisions that short-horizon shareholders would never have approved.

The operational counterpart to He Jianfeng has historically been a professional management team anchored by Hao Hengle, the company's president. Hao's background is instructive. He spent years inside the Midea Group manufacturing ecosystem before migrating into the real estate arm, which means he brought the factory discipline directly into the development business. He ran land acquisition with the kind of unit-economics rigor that, inside Midea Group, you would apply to a new product line. If the land cost implied a project return below a certain threshold, the deal was killed, no matter how prestigious the parcel. That discipline was, in the end, more valuable to Midea Real Estate than any single piece of land it bought.

Beneath the chairman-president layer, Midea applied a compensation philosophy that Chinese real estate was not used to: the "co-investment" scheme. Under this model, project-level managers were required, or strongly incentivized, to put their own capital alongside the company's into specific development projects. If the project met its margin and cash-flow targets, the managers earned a disproportionate share of the upside. If it missed, their own capital took the first loss. This is a manufacturing-style variable compensation logic imported into real estate. It meant that the people running a given Foshan tower had direct personal skin in the game on whether it was completed on time, at cost, and sold through at the targeted price. Compare this with the fixed-salary-plus-hierarchical-bonus structure at many of the defaulted peers, where project managers were essentially rewarded for launching projects rather than finishing them.

The broader cultural distinction is what Chinese management writers call the shift from "guanxi" to "meritocracy." Old-school Chinese developers—and many of the larger defaulted firms were built on this—ran on relationship networks. The land bureau director's cousin, the bank branch manager's classmate, the local Party secretary's nephew. These relationships were the true skill set, and the cost structure, of development. Midea imported from the appliance side a culture that tolerated guanxi where it was unavoidable but refused to depend on it. Hiring was dominated by the mid-career recruits from engineering and operations, not relationship bankers. Performance reviews were numerical. Promotions were tied to project-level outcomes. This is not a revolutionary management system in a global context—most industrial companies run this way—but in the Chinese property context of the 2010s, it was genuinely unusual, and it explains a lot of why Midea's projects delivered when peers' did not.

All of that governance and culture sets up the strategic question that any investor must answer: does Midea have a durable advantage, or did it just happen to be less leveraged than the rest of a dying sector?

VIII. Power and Forces Analysis

Hamilton Helmer's 7 Powers framework asks a simple question: what differential benefit does this company enjoy over competitors, and what barrier keeps competitors from replicating it? Applied to Midea Real Estate, three powers show up clearly.

The first is Brand. In consumer-facing product categories, brand is often discounted as a soft moat, but in Chinese residential property in the 2020s, brand is, effectively, the moat. When a Chinese family commits two or three generations of savings to a pre-sold apartment, they are underwriting two things: the quality of the unit, and the probability that it will ever be built. The default rate among Chinese developers turned the second question from abstract to existential. A Midea-branded project carries an implicit promise—not contractual, but deeply cultural—that the He family will not allow a branded default. Buyers pay a premium for that promise. Banks underwrite mortgages against it. Local governments grant permits faster because they trust the completion probability. The Sunac brand, the Evergrande brand—those carry negative value today. The Midea brand carries positive value. That gap is the moat.

The second is Cost Power, specifically on the funding side. Because of the family halo and the green-file designation, Midea has access to domestic credit at rates that are, depending on the tenor, somewhere between 300 and 800 basis points inside what many private peers can access. In a business where interest expense is one of the three largest cost items and where a hundred basis points of borrowing cost can wipe out a project's net margin, a structural funding advantage is not a nice-to-have. It is the game. And this is a cost power that does not depend on any operational scale; it depends on the family's reputational collateral, which is, by construction, unreplicable by a non-Midea firm.

The third is Cornered Resource, and this is where the sister-company relationship with Midea Group becomes genuinely unique. No other Chinese developer has preferred pricing, bundled product integration, and co-development access to the catalog of one of the world's largest appliance and HVAC manufacturers. A competitor who wanted to replicate Midea Real Estate's REMO smart community offer would have to negotiate procurement contracts with Midea Group, Haier, or Gree as a third party, without the family relationship and without the ability to cross-subsidize. It is technically possible, but it is not economical. The sister-company access is a cornered resource in the exact sense Helmer defines.

Two of the remaining powers—Scale Economies and Network Economies—are less compelling here. Chinese property is a fundamentally local business at the project level, and scale benefits largely evaporate above a certain size. Counter-Positioning is arguable, with the 2024 restructuring as potentially a counter-positioning move against peers who are structurally unable to exit the development model. Process Power—the manufacturing-style operational discipline in industrialized construction—is real but imitable over time. Switching Costs exist mildly for property management customers but are not dominant.

Turning to Porter's Five Forces, the picture is mixed and changing. Barriers to entry into Chinese property development are, and will remain, very high—both because of capital intensity and because the regulatory licensing regime is complex. That does not help incumbents who are already inside but cannot serve customers; it is a backward-looking moat. The threat of substitutes, depressingly for the sector, is real in the form of used housing, rental substitutes, and simply not forming a household. Bargaining power of buyers has increased dramatically in the 2022-2025 period, because the Chinese homebuyer is now picking from a menu of developers, many of whom may not complete construction, and the buyer demands both discounts and completion guarantees. That pressure disproportionately benefits Midea, whose completion credibility is high. Bargaining power of suppliers—construction contractors, cement producers, labor—has weakened as industry activity has shrunk. Industry rivalry is paradoxically lower than it was, because so many competitors have been effectively removed from the playing field by default, but the remaining pie is also smaller.

The competitive landscape Midea faces today is essentially three groups. There are the state-owned developers—Poly, China Overseas Land, China Resources Land—who have the deepest access to state-backed credit and the highest completion credibility among all private-and-state peers. There are the surviving disciplined privates—Longfor being the closest analogue to Midea—who run similar conservative balance sheets. And there is the long tail of distressed and restructuring names whose brands are impaired and whose balance sheets are in triage. Midea positions between the first and second groups, with a brand strength from the family relationship that outstrips most state-owned peers and a balance sheet that matches the best privates. In a smaller post-crisis sector, that is a competitively enviable spot.

Before we arrive at the investor case, it is worth flagging the second-layer diligence items. The Midea family's influence across Midea Group, Midea Real Estate, and other family holdings creates related-party transaction risk that Hong Kong's independent director and shareholder approval regime has so far handled transparently. The 2024 restructuring itself was passed with appropriate disclosure and minority approval, which is meaningfully better than what has happened at several Chinese developer restructurings. The remaining listed entity's disclosures around the legacy development wind-down and the private absorption of those assets should remain a focus for anyone underwriting the name. Audit, regulatory, and ESG signals have been clean relative to peers, but in Chinese property, the whole sector has operated under elevated scrutiny, and any developer with legacy projects remains exposed to local government policy changes, mortgage-release timing, and completion certification risk. These are not headline red flags, but they are material in context.

IX. The Playbook: Lessons for Founders and Investors

Three lessons emerge from the Midea Real Estate story that travel well beyond Chinese property.

The first is Borrow Your Moat. Midea Real Estate did not build its brand. It inherited it from a sister company that had spent fifty years earning consumer trust selling rice cookers and air conditioners. Most founders spend the first decade of a new venture trying to manufacture trust from scratch, and most fail. Midea's growth path was fundamentally different because it started with an implicit trust dividend—a brand that already meant something to Chinese households—and invested that dividend into categories where trust mattered most. For founders inside large family holdings or corporate incubators, the takeaway is that brand transfer is not automatic, but it is available if managed deliberately. For investors, the takeaway is that spotting a company with a borrowed moat early, and pricing the durability of that moat, is a source of alpha that the market tends to mispriced because balance-sheet screens cannot see it.

The second is Manufacturing the Un-Manufacturable. Chinese real estate, like American real estate in the 2000s, was often treated by its practitioners as a financial asset with a building attached. Midea treated it as a product with a balance sheet attached. That reversal—product first, financing second—meant that when financing disappeared, the product still worked. There is a broader lesson here for any capital-intensive sector: the more your competitors treat the business as a trade, the more you win by treating it as a thing to be made well. The industrialized construction business, the smart home integration, the co-investment incentive structure—all of it flows from treating housing as manufactured product. Investors should watch for companies in cyclical industries that import manufacturing culture from adjacent sectors. That cultural import is almost always undervalued.

The third is Knowing When to Pivot. The hardest decision in business is to voluntarily exit a business that has been good to you before the market forces you out. Midea's 2024 restructuring is exactly that decision. The company could have muddled along in development for another five to ten years, harvesting cash flow from the wind-down and pretending the model would revive. Most boards, most chairmen, and most investor bases would have demanded exactly that muddle-through. Midea's concentrated ownership structure and founding-family governance allowed it to take the harder path—exit the declining core, reposition the rump as a service and tech business, and accept the near-term valuation disruption. For investors, the signal is that corporate structures which enable that kind of long-horizon exit are rare, valuable, and worth a governance premium. For founders, the lesson is that the time to pivot is when you still have the balance sheet strength to do it by choice.

These three lessons—borrowed moat, manufactured product, courageous pivot—are not unique to Midea. But to find all three in one company, inside one of the most punishing sector downturns of the twenty-first century, is unusual. Which finally brings us to the investor case, bull and bear.

X. Conclusion and the Bear and Bull Case

The bear case for Midea Real Estate after the 2024 restructuring is straightforward. The development business, which generated the majority of historic revenue and a substantial share of historic cash flow, is being carved out. What remains is a collection of faster-growing but smaller businesses—property management, industrialized construction, smart home integration—whose combined scale does not yet match the development engine. The question is whether these businesses, growing at their current rates and at their current margins, can compound into a valuation that justifies the post-restructuring equity base. A bear would argue that the Chinese property services sector is more competitive than it looks, with dozens of developer-affiliated property management spinoffs chasing the same third-party mandates. Industrialized construction, while structurally important, depends heavily on government-sponsored affordable housing flows that can be redirected by policy. REMO, for all its strategic elegance, is still a small contributor to EBITDA, and the broader Chinese consumer is in a state of cautious spending that slows smart home upgrade cycles. The bear also notes that the generalized stigma around Chinese property-linked names may persist in global investor portfolios for years, independent of what the company actually does, and that multiple re-rating therefore cannot be assumed. Finally, the bear flags that the family's concentrated ownership, while governance-positive in crisis, can become a discount in peacetime, because minority shareholders have limited ability to force further corporate actions.

The bull case runs the opposite direction. A Chinese population of 1.4 billion still lives somewhere, still needs their buildings maintained, their appliances upgraded, and their communities managed. The flow business that Midea now focuses on is essentially the annuity side of the property industry—the part that does not depend on new housing starts, land prices, or speculative cycles. Property management revenue is structurally recurring, grows with inflation and gross floor area, and, in a market where most developer brands are impaired, naturally consolidates toward the surviving credible brands. Industrialized construction is increasingly favored by Chinese central policy, because it improves construction quality and reduces labor market pressure, and Midea is one of the most advanced operators in the segment. REMO is a technology asset that can scale across in-house and third-party communities, and it benefits directly from the rising installed base of Midea Group appliances. Meanwhile, the family has demonstrated, through the 2024 restructuring, that it will make decisions in minority-aligned fashion, which reduces the governance discount over time. And the Midea brand, having survived an industry extinction event, has never been more differentiated. On a long enough horizon, a credible Chinese brand in an incredible Chinese sector is a rare and valuable thing.

Between the bear and the bull, the investor should concentrate attention on a very short list of KPIs. Three matter most. The first is gross floor area under property management, tracked alongside the proportion of that floor area sourced from third-party developers rather than Midea's own legacy pipeline; the mix shift toward third-party tells you whether the property services business can scale beyond the development heritage. The second is non-development revenue growth, as a composite of property services, industrialized construction, and smart home integration; this is the headline line that tells you whether the new strategy is compounding. The third, more qualitative, is the completion and cash return performance of the private development business that the family absorbed; because the family's balance sheet is the same balance sheet that provides the implicit halo, the durability of the halo depends on whether the private wind-down happens cleanly. Track those three, and you will understand the trajectory of this company better than any quarterly sell-side note will tell you.

Is Midea the Vanke of the next generation? The question itself is imprecise, because the next generation of Chinese property will not look like a Vanke—will not look like any developer we have seen. It will look like a managed services and platform industry attached to a much smaller new-build engine. In that world, the companies that win will be the ones that carried the most trust, the least leverage, and the clearest sense of what business they were actually in, across the transition. Midea Real Estate is, on each of those three dimensions, extremely well positioned. Whether that positioning translates into shareholder returns depends, as always, on price, execution, and macro. The positioning itself is the story. The execution is the decade ahead.

XI. Outro and Reading List

For listeners who want to go deeper, three threads reward the effort.

The first is the founder literature. He Xiangjian's management philosophy, summarized in Chinese-language volumes often grouped under the title "The Midea Way," is the intellectual substrate for everything the real estate arm does. Reading the Midea Group's own governance reforms of the 2010s—the professional manager transition, the introduction of partner-equity schemes, the decision to list in Shenzhen—provides the cultural backdrop for how the real estate unit was structured.

The second is the HKEX disclosure trail around the 2024 restructuring. The scheme of arrangement circular, the independent financial adviser opinion, and the board letter together constitute one of the cleaner case studies in Hong Kong corporate law on how to execute a partial privatization of a cyclical heavy-asset business with minority protection intact. Students of Chinese corporate governance should read those filings closely.

The third is the broader Chinese property policy literature from 2020 forward—the Three Red Lines framework, the 2022 policy easing, the 2023 affordable housing push, and the 2024 urban redevelopment program. Midea's strategic moves only make sense inside the framework of the state's view of what the property sector should become. Understanding that framework is, in the end, the real work of investing in any Chinese listed company.

The Midea Real Estate story is still being written. The 2024 pivot was Chapter One of the next phase, not the conclusion. What comes next—how the non-development businesses compound, how the brand migrates from homebuilder trust to service provider trust, and whether the family's private absorption of the legacy development book resolves cleanly—will define whether this becomes a textbook case study or a cautionary tale. Either way, it is the most interesting company in its sector. And sometimes, in the middle of a collapse, that is where the most interesting stories live.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube