Bank of China Limited: The Global Sentinel of Chinese Capital

I. Introduction & Episode Roadmap

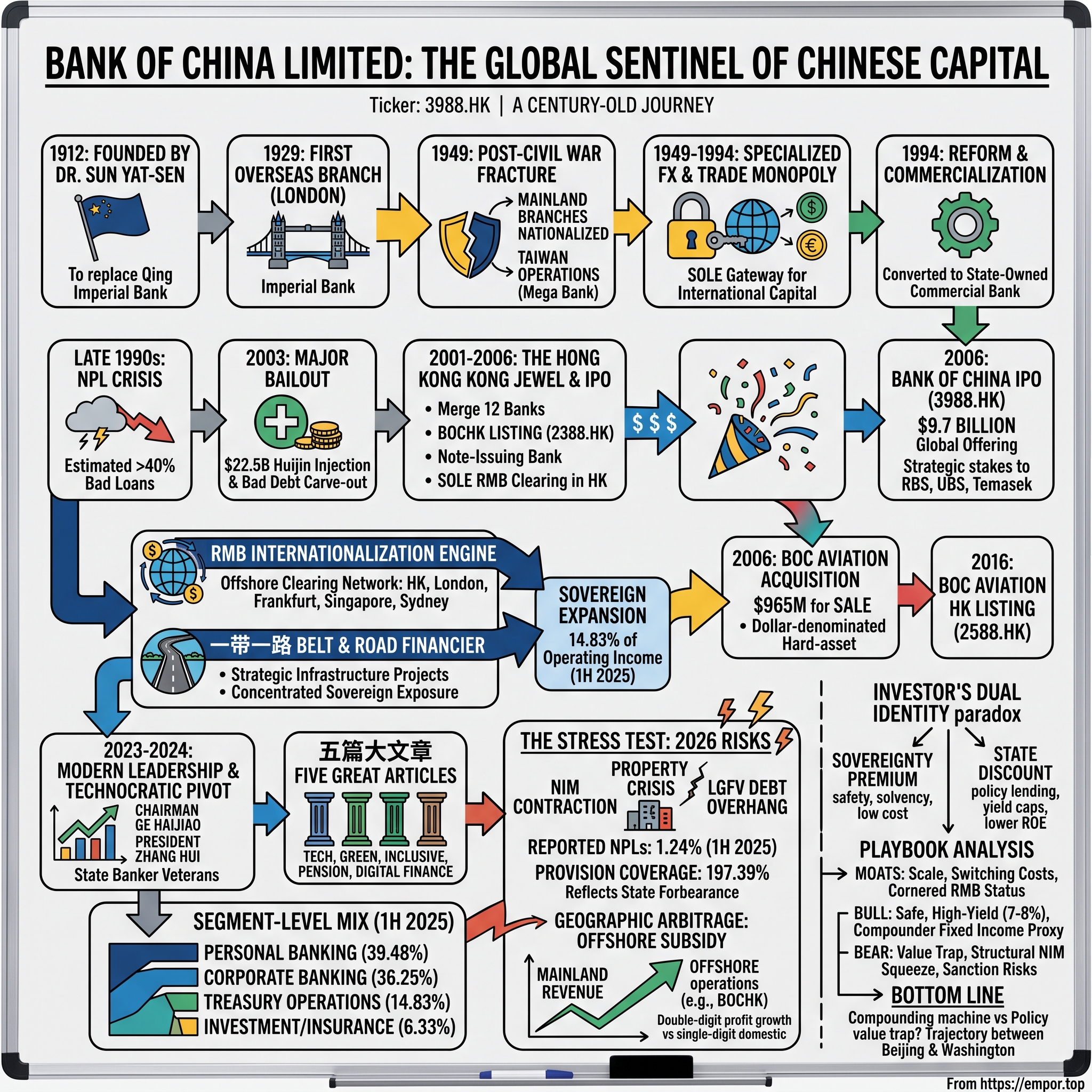

Picture a balance sheet so large it is difficult to hold in the mind. As of the end of 2025, 中国银行股份有限公司 Bank of China Limited carried total assets north of RMB 38 trillion — somewhere in the neighborhood of $5.3 trillion once you translate it into dollars.1 That figure makes it the fourth-largest bank on the planet, and it sits inside a country whose entire financial system is often described, by outsiders, as an opaque monolith. Yet the striking thing about Bank of China is not its size. Its three state-owned siblings in the Chinese "Big Four" — 工商银行 ICBC, 建设银行 China Construction Bank, and 农业银行 Agricultural Bank of China — are each larger by assets. What makes Bank of China a genuinely different animal is what it does, and where it does it.

Here is the paradox at the center of this story. An institution founded in 1912, blessed into existence by 孙中山 Dr. Sun Yat-sen to replace the collapsing Qing dynasty's imperial bank, somehow survived a century of revolution, civil war, famine, Maoist upheaval, and forced nationalization — and emerged as the primary clearing engine for the internationalization of the 人民币 renminbi and the financing backbone of Beijing's 一带一路 Belt and Road Initiative. How does a bank born to serve a fragile new republic become, a hundred years later, the financial nervous system connecting the world's second-largest economy to everyone else's?

The answer lies in a dual identity that runs through everything the bank touches. On one level, Bank of China is a commercially competitive joint-stock bank with genuinely world-class subsidiaries — 中银香港 BOC Hong Kong (2388.HK), a note-issuing bank in one of the planet's great financial centers, and 中银航空租赁 BOC Aviation (2588.HK), one of the largest aircraft lessors in the world, earning hard dollars from airlines on five continents. On another level, it is a core organ of the Chinese state, its senior appointments made by the Communist Party, its lending priorities shaped by macro-stability policy rather than by the pursuit of the highest risk-adjusted return. Investors who buy the Hong Kong-listed shares are buying both of those banks at once, whether they understand it or not.

This is the tension a sophisticated investor has to sit with. The state ownership that guarantees the bank will never be allowed to fail is the same state ownership that caps what equity holders can ever extract from it.

Over the course of this story we will travel from a revolutionary foreign-exchange monopoly, through the near-death experience of China's banking system in the late 1990s and the landmark $9.7 billion Hong Kong IPO of 2006, into a genuinely masterful piece of capital allocation — the acquisition of Singapore's largest aircraft lessor — and onward through the offshore renminbi franchise, an anti-corruption storm that ended with a former chairman under a suspended death sentence, and finally a hard, skeptical stress-test of the investment case as it stands in 2026: collapsing net interest margins, a property-sector debt overhang, and a valuation that the market has priced at a fraction of book value for years. Let us begin where the bank began: in the wreckage of an empire.

II. Century-Old Origins: From Imperial Bank to specialized FX Monopoly (1912–1994)

In February 1912, the Qing dynasty was dead. Two thousand years of imperial rule had ended, and the men trying to build a republic in its place needed something every state needs and few revolutions bother to plan for: a bank. The outgoing dynasty had left behind the 大清银行 Ta-Ching Government Bank, the imperial state bank, and rather than tear it down, the new government did something pragmatic. Dr. Sun Yat-sen approved its transformation into a new institution — the Bank of China — which would serve simultaneously as the central bank of the young Republic of China and as its international exchange bank. From the very first day, then, this was an institution with a foot in two worlds: domestic monetary authority on one side, and the gateway to foreign capital on the other. That dual DNA never left it.

The bank's central-banking role did not last. Warlords, competing governments, and eventually the establishment of a separate central bank stripped it of monetary authority, and Bank of China narrowed into what it did best — foreign exchange and international trade finance. It opened a branch in London in 1929, the first Chinese bank to plant a flag on foreign soil, and built out a network across the treaty ports and financial capitals of Asia and Europe. By the 1930s it was, in practical terms, China's window on the world's money.

Then came the great fracture. The Chinese Civil War split the institution as it split the nation. When the Communists won the mainland in 1949, the bank's leadership and a portion of its operations followed the Nationalists to Taiwan, where those branches were eventually privatized and, decades later, folded into what became Mega International Commercial Bank. The mainland branches were nationalized under the new People's Republic. Two banks, one ancestor, sundered by history — a small illustration of how completely 1949 rewired everything it touched.

What happened next is the part that matters most for understanding the bank today. For three decades, from 1949 until the reforms of 1979, the People's Republic was largely walled off from the Western financial system. In that isolated economy, Bank of China was handed a role that would have made any commercial banker weep with envy: it was the country's sole specialized bank for foreign exchange and international trade settlement. If a Chinese enterprise needed to buy a machine from abroad, sell a commodity overseas, open a letter of credit, or touch foreign currency in any way, it went through Bank of China. There was no competitor because competition did not exist. The bank managed the nation's early foreign-exchange reserves, ran its gold trading, and quietly maintained the only physical Chinese banking presence in London, Hong Kong, and Singapore during years when the mainland had almost no other commercial contact with the outside world.

The consequence of those decades is easy to underrate and impossible to replicate. While future rivals like ICBC and Agricultural Bank grew up as purely domestic lenders — one to industry, one to the countryside — Bank of China spent a generation as the country's only internationally facing financial institution. It became the elite training ground where Chinese technocrats learned how global finance actually worked: how trade was settled, how currencies were hedged, how sovereign reserves were managed. That accumulated institutional knowledge — an "international DNA" no domestic-focused peer could buy or fake — is the single most durable competitive asset in this entire story. Everything the bank monetizes today in offshore renminbi and cross-border trade traces back to a monopoly it held when China had almost nothing else to trade with. The question that would define the next chapter was whether a bank built as a state monopoly window could survive being turned into a commercial enterprise.

III. Commercialization, the HK Jewel, and the Grand 2006 IPO (1994–2006)

By the early 1990s, 邓小平 Deng Xiaoping's reforms had unleashed an economy growing at double digits, and the old model — where the Big Four state banks functioned as little more than cashiers for the government's industrial plans — was buckling. In 1994, under the reforming hand of Premier 朱镕基 Zhu Rongji, China restructured its banking system. Bank of China was formally converted into a state-owned commercial bank, and the policy-lending mandates that had forced it to fund whatever the plan required were hived off to newly created policy banks such as China Development Bank. On paper, Bank of China was now supposed to make loans that got repaid.

The trouble was the loans already on the books. Decades of directed lending to inefficient state-owned enterprises had left the entire Chinese banking system carrying a mountain of bad debt. By the late 1990s, credible estimates put non-performing loans across the big banks at more than 40% of the portfolio — a level that, in any market economy, would mean the banks were not merely troubled but technically insolvent several times over.13 This was the dirty secret beneath China's growth miracle: an economy expanding at a breakneck pace, financed by a banking system that was, by conventional accounting, bankrupt.

Beijing's solution was a bailout of extraordinary scale, executed with a bluntness Western regulators could only marvel at. In 2003, a newly created sovereign vehicle, Central Huijin Investment, injected $22.5 billion of the nation's foreign-exchange reserves directly into Bank of China's capital base.1 Simultaneously, the bad loans were carved out — transferred at face value, not market value, to newly established asset management companies whose entire purpose was to warehouse the toxic debt off the banks' balance sheets. It was a fiction, in a sense: the losses did not vanish, they were simply moved to a different pocket of the state. But it worked, because in a system where the state owns the bank, the borrower, and the bad bank, solvency is ultimately a political decision rather than an accounting one. Remember that mechanism. It is the same one that lets the bank report a pristine loan book today, and we will return to it when we stress-test the numbers.

While the mainland restructuring ground forward, the most valuable asset in the entire group was quietly being assembled a thousand miles south. In 2001, Bank of China merged twelve separate sister banks operating in Hong Kong into a single entity: 中银香港 Bank of China (Hong Kong) Limited. In July 2002, that entity, BOCHK, listed on the Hong Kong Stock Exchange under 2388.HK. This was not a minor subsidiary. BOCHK was designated one of only three note-issuing banks in Hong Kong — the currency in a Hong Konger's wallet is printed by HSBC, Standard Chartered, or Bank of China — and, crucially, the sole clearing bank for renminbi in Hong Kong. That combination handed BOCHK an almost unfair advantage: a vast, sticky, low-cost retail deposit base in a hard-currency financial center, feeding a franchise sheltered from mainland interest-rate policy. It is the crown jewel, and understanding why requires understanding what a clearing monopoly is worth — a subject we will come to shortly.

Then came the main event. On June 1, 2006, Bank of China Limited itself listed on the Hong Kong Stock Exchange under the ticker 3988.HK, raising $9.7 billion in its H-share global offering; when the over-allotment option was exercised days later, the total swelled to roughly $11.2 billion, making it one of the largest IPOs the world had ever seen.45 The retail tranche in Hong Kong was oversubscribed dozens of times over, drawing hundreds of billions of Hong Kong dollars in orders — a frenzy that captured the global appetite, circa 2006, for a piece of the China growth story.5 A Shanghai A-share listing under 601988.SH followed shortly after, giving the bank a dual home in both the offshore and onshore markets.

What made the 2006 float more than a fundraising exercise was who Beijing let in the door. In the run-up to the IPO, Bank of China sold strategic stakes to a roster of blue-chip foreign institutions: the Royal Bank of Scotland led a consortium investing around $3.1 billion, alongside Switzerland's UBS and Singapore's state investor Temasek Holdings.6 The point was not the money — the Huijin injection had already recapitalized the bank. The point was governance. By binding in sophisticated foreign shareholders, Beijing was importing risk controls, board discipline, and international credibility, signaling to global investors that this century-old state bank could be trusted to behave like a modern listed company. Whether that discipline truly took root, or was quietly diluted once the foreign partners sold down their stakes in later years, is one of the open questions a skeptic should keep in the back of their mind. What is beyond dispute is that the freshly raised capital gave the bank firepower — and within months it made a move that, two decades later, still looks like the smartest thing it ever did.

IV. Capital Deployment Masterclass: The BOC Aviation Acquisition (2006)

It is December 2006. Bank of China is sitting on a war chest, its coffers freshly stuffed from the largest IPO of the year, and every investment bank in Asia is pitching the newly rich giant on ways to spend it. This was the era when Chinese financial institutions, flush with cash and national pride, went shopping in the West — and, in hindsight, mostly overpaid at the top of the market. The sovereign wealth fund CIC would soon pour billions into a stake in Morgan Stanley just as the financial crisis detonated; the insurer Ping An would famously lose the bulk of a multi-billion-euro bet on the Belgian-Dutch group Fortis. Buying trophy stakes in Western investment banks was the fashionable trade, and it destroyed staggering amounts of Chinese capital.

Bank of China did something quieter and far smarter. Instead of an equity stake in a leveraged Western financial firm it could not control, it bought a business it could — and one made of steel rather than paper. In December 2006 it acquired 100% of Singapore Aircraft Leasing Enterprise, or SALE, then the largest aircraft lessor in Asia, for $965 million.7 Aircraft leasing is a beautifully simple business to understand: you buy planes, you lease them to airlines on long-term contracts, the airlines send you dollars every month, and at the end of the lease you own an asset with residual value that you can re-lease or sell. It is a hard-asset, cash-generative, dollar-denominated business — precisely the opposite of a minority stake in a bank whose own balance sheet you cannot see.

The discipline showed in the price. The $965 million reflected a book-value multiple of roughly 1.2 to 1.3 times — a sober number in an industry where transaction multiples would later run to 1.5 or 1.8 times book at the cyclical peak.8 Bank of China bought a franchise asset near the bottom of a valuation range, using capital raised at the top of an equity market. That is the textbook definition of good capital allocation, and it stands in sharp relief against the crisis-era trophy purchases of its peers.

Renamed 中银航空租赁 BOC Aviation in 2007, the business did exactly what a well-run lessor is supposed to do: it compounded.8 The fleet grew from dozens of aircraft into the hundreds, spread across a globally diversified roster of airline customers, and the unit generated net profit margins that consistently ran north of 15%. Because its revenues are earned in dollars from airlines all over the world, BOC Aviation became something genuinely valuable to a Chinese parent — a countercyclical, hard-currency earnings stream that keeps generating dollars even when the mainland economy softens and domestic loan yields sag.

In 2016, Bank of China monetized part of what it had built, floating BOC Aviation on the Hong Kong Stock Exchange under 2588.HK while retaining a 70% controlling stake.8 The parent got a public valuation, a liquid currency, and a continued claim on the earnings, all at once. By the middle of this decade the subsidiary carried a market value well above $6 billion — a striking return on a $965 million check written twenty years earlier. The lesson an investor should draw is not merely that the deal made money. It is that Bank of China, alone among the Big Four, demonstrated it could think like an owner of global hard assets rather than a passive allocator of state capital. That instinct — to earn dollars offshore where returns are market-driven — is the same instinct that would make it Beijing's natural choice for a far larger mission.

V. The Twin Engines of Sovereign Expansion: RMB Internationalization & Belt and Road

The autumn of 2008 taught Beijing a lesson it has never forgotten. As Lehman Brothers collapsed and the dollar funding markets that grease global trade seized up, China discovered how dangerously dependent its export machine was on a currency it did not control and a banking system centered in New York and London. Chinese exporters could not get dollar letters of credit; trade financing evaporated overnight. The world's factory had been reminded, brutally, that it was settling almost all of its commerce in someone else's money. Out of that shock came a strategic decision that would reshape global finance over the following fifteen years: China would internationalize the renminbi, building an alternative plumbing for trade and payments that ran, at least partly, on Chinese rails.

And when Beijing looked around for a national champion to build that plumbing, the choice was obvious. Bank of China already had the international branch network, the foreign-exchange expertise, and the offshore presence that no domestic-focused peer possessed. The renminbi internationalization mission was, in effect, custom-built for the bank's century-old DNA.

The mechanism at the heart of it is worth slowing down to explain, because it is where a great deal of quiet profit hides. When two parties in different countries want to settle a transaction in renminbi outside mainland China, the money has to pass through a designated "clearing bank" — an institution anointed to be the official gateway between the offshore renminbi pool and the onshore financial system. Being the clearing bank is like owning the only toll booth on a bridge that an entire economy has to cross. Every transaction touches you; you earn a small, reliable fee on enormous volume; and the position, once granted by the state, is nearly impossible for a competitor to dislodge. BOCHK was appointed the sole clearing bank for offshore renminbi in Hong Kong, the largest offshore renminbi center in the world, handling the lion's share of global offshore renminbi flows.9 Bank of China then went on to win clearing-bank designations in a string of other financial capitals — London, Frankfurt, Paris, Sydney, Singapore — knitting together a network of toll booths across the world's time zones.

Layered on top of the currency mission came the 一带一路 Belt and Road Initiative, unveiled in 2013 as 习近平 Xi Jinping's signature foreign-economic strategy: a vast program of ports, railways, power plants, and pipelines stretching across Central Asia, Southeast Asia, the Middle East, and Africa. Somebody had to finance all that concrete and steel, and Bank of China positioned itself as the primary commercial financier of the effort — arranging syndicated loans, providing cross-border settlement, and following Chinese contractors into markets where Western banks were often unwilling or unable to lend. The independent-minded investor should note the double edge here: Belt and Road lending generates fees and extends China's financial reach, but it also concentrates exposure in some of the least creditworthy sovereigns on earth, a risk that does not show up cleanly in a domestic NPL ratio.

The financial payoff of these twin engines shows up in the bank's treasury and cross-border businesses. In the first half of 2025, Treasury Operations contributed 14.83% of operating income, roughly RMB 48.84 billion, drawn from cross-border trade settlement, syndication fees, and foreign-exchange market-making.9 That is not a rounding error. In a period when the bank's domestic lending margins were being crushed, the fee and trading income thrown off by its international franchise acted as a genuine cushion — a diversification benefit that the purely domestic Big Four banks simply do not enjoy. The offshore engine, in other words, is not just prestige; it is ballast. The people steering that ship, however, answer to a chain of command that looks nothing like a Western bank's — as the events of the last three years made violently clear.

VI. Modern Leadership, State Governance, and the Technocratic Pivot

To understand who really runs Bank of China, you have to abandon the org chart a Western investor instinctively reaches for. Yes, there is a board of directors, an audit committee, and all the trappings of a listed company. But the ultimate locus of power inside the institution is the Communist Party Committee, which answers upward to the Central Financial Commission and to the sector's regulator, the 国家金融监督管理总局 National Financial Regulatory Administration, or NFRA.14 Strategy, senior appointments, and the boundaries of acceptable risk are set through that Party channel, not through a shareholder vote. When people say the bank has "corporate governance with Chinese characteristics," this is what they mean: the fiduciary duty that a Western director owes to shareholders is, here, subordinate to a duty owed to the state's economic objectives.

Nothing dramatized the stakes of that system more than what happened to the man who used to sit at the top. In March 2023, former chairman 刘连舸 Liu Liange was placed under investigation for corruption.[^2] The case moved with the grim inevitability such cases do. In November 2024, a court in Shandong province handed Liu a suspended death sentence — death with a two-year reprieve, a Chinese legal formulation that, if the convict commits no further offense, is typically commuted to life imprisonment.[^2]23 The court found he had accepted bribes of more than RMB 121 million and, across his tenure at Bank of China and earlier at the Export-Import Bank of China, had illegally approved some RMB 3.3 billion in loans, causing substantial losses.[^5] For good measure, the bank's president, 刘金 Liu Jin, abruptly resigned in August 2024, deepening the sense of a leadership ranks in turmoil.

For an investor, the Liu Liange affair is not gossip — it is data. It tells you two things at once. First, that the anti-corruption apparatus reaches the very top of these institutions, which is a genuine governance risk: strategy gets disrupted, decisions freeze, and the market discounts the uncertainty. Second, and more subtly, that the loans Liu waved through were real losses buried inside a bank that reports a pristine NPL ratio — a reminder that the reported credit quality of a state bank rests partly on trust in the honesty of the people approving the loans. When that trust is shown to have been misplaced at the chairman level, a skeptic is entitled to wonder what else is not visible.

Into the breach stepped a new technocratic guard. Chairman 葛海蛟 Ge Haijiao, appointed in April 2023, is a career state banker — a veteran of Agricultural Bank of China who had also served as a vice governor of Hebei province, the kind of resume that blends financial management with Party administration.1 Alongside him, 张辉 Zhang Hui was appointed president in December 2024, arriving from Bank of Communications where he had been a vice president.1 Neither man is a charismatic empire-builder in the Western CEO mold, and that is precisely the point.

Consider how these executives are actually incentivized, because it explains almost everything about how the bank behaves. They hold virtually no stock and receive no meaningful equity awards; their cash compensation is capped by state guidelines at levels that, converted to dollars, often sit below the mid-six figures — a rounding error next to what a division head at a Western bank earns.1 Their real "upside" is not a bonus but political promotion — the chance to ascend to a ministerial post or a provincial governorship. Their "downside" is not a bad year but career annihilation or, as Liu Liange discovered, a courtroom. When you internalize that incentive structure, the bank's conservatism stops being a mystery. Executives paid this way have every reason to preserve capital, avoid scandal, and hit the state's targets — and almost no reason to swing for aggressive growth or fight to maximize the share price.

Those state targets now travel under a memorable banner: the 五篇大文章 "Five Great Articles," Beijing's directive that the big banks steer credit toward technology finance, 绿色金融 green finance, 普惠金融 inclusive finance, pension finance, and digital finance.1 Under Ge and Zhang, management's job is to channel lending into these politically favored channels — often at concessionary rates — while simultaneously preserving capital and protecting the roughly 30% dividend payout that the state, as majority owner, relies upon. That is the needle they are threading. Whether it can be threaded indefinitely, as domestic margins compress, is the question the numbers now force us to confront.

VII. Segment-Level Deep Dive & Financial Architecture

Strip away the geopolitics and the century of history, and a bank is ultimately a machine for turning deposits into assets at a spread. So how is this particular machine actually performing? For the full year 2025, Bank of China reported operating income of RMB 659.87 billion, up 4.28% year on year, and net profit attributable to shareholders of RMB 243.02 billion, up 2.18%.1012 Those are not the numbers of a company in crisis, but nor are they the numbers of a growth business. Low-single-digit profit growth from a bank of this scale, in an economy still expanding faster than that, tells you the story is about defense — protecting earnings against a hostile rate environment — rather than expansion.

The engine has four cylinders, and the interim disclosures for the first half of 2025 let us see how much each contributes. Personal Banking — retail deposits, mortgages, wealth management, consumer credit — was the largest, at 39.48% of operating income, roughly RMB 130.04 billion.9 Corporate Banking, the business of lending to state-owned giants, strategic industries, and trade, came next at 36.25%, or about RMB 119.44 billion.9 Treasury Operations, the cross-border and markets engine discussed earlier, added 14.83%.9 And a cluster of Investment Banking and Insurance activities — driven by the securities arm BOC International and the insurer BOC Life — contributed roughly 6.33%.9 It is a reasonably balanced mix, more diversified than a pure lender, with a meaningful slug of fee income insulated from interest-rate compression.

But the segment breakdown is not where the real insight lives. The most important number in the entire financial architecture is geographic. In the first half of 2025, the Chinese mainland generated 76.23% of operating income, about RMB 251.69 billion; Hong Kong, Macao, and Taiwan contributed 19.14%, roughly RMB 63.19 billion; and other countries and regions added 4.63%, around RMB 15.30 billion.9 On the surface that looks like an ordinary home-heavy revenue split. The magic is in the profitability, not the volume.

Here is the arbitrage that defines Bank of China as an investment. Mainland margins have been ground down by policy — the bank is expected to lend cheaply to favored sectors and to refinance troubled borrowers at concessionary rates. But its offshore commercial operations, led by BOCHK, operate in genuine markets where they can price risk properly and earn a real spread. In 2025 those offshore operations grew profit by double digits even as domestic margins sagged, and overseas operations delivered on the order of a quarter of the group's total profit before tax — a contribution far out of proportion to their share of revenue.910 Read that again, because it is the crux of the bull case: the international assets, roughly a quarter of the group's revenue, subsidize the domestic policy concessions that the state extracts on the other side of the border.

This is the payoff of a century of international DNA, expressed in a single line of the financials. The overseas franchise is not a vanity project or a diplomatic gesture; it is the highest-return part of the bank, and it exists precisely because Bank of China spent decades as China's only window on the world. The independent question, of course, is whether that offshore engine can keep growing fast enough, and stay high-margin enough, to offset a domestic business under structural pressure. To answer that, we have to walk straight into the storm.

VIII. The Stress Test: NIM Contraction, Property Crisis, and Material Risks

Every bank lives and dies by a single, deceptively simple number: the net interest margin, or NIM. It is the difference between what the bank earns on its loans and what it pays on its deposits — the spread that is, quite literally, the core of the business model. And across the Chinese banking system, that spread has been collapsing. To rescue a property sector in freefall and to stimulate a slowing economy, the People's Bank of China has cut interest rates repeatedly, dragging loan yields down faster than banks can cut what they pay depositors. Industry-wide NIMs for China's major banks have fallen toward, and in some cases below, the 1.5% line that regulators themselves have flagged as a threshold of concern; Bank of China's own margin ran around 1.26% in the first half of 2025.913 To put that in human terms: the bank now earns barely more than one yuan of gross spread for every hundred yuan it lends, before it has paid a single employee or absorbed a single bad loan.

Management's defense against this squeeze is twofold, and both levers are visible in the results. On one side, it has aggressively cut deposit rates, using its enormous and sticky deposit franchise to claw back some of the margin lost on the lending side. On the other, it leans harder on the fee and trading income from its international businesses — the treasury and cross-border engine that does not depend on the domestic lending spread at all. Net fee income grew mid-single digits in the first half of 2025 even as margins compressed, which is exactly the offset the strategy is designed to produce.9 Whether that offset is large enough to hold profits flat indefinitely is the open question; the arithmetic gets harder every time the PBOC cuts again.

Then there is the elephant in the room: property. The multi-year Chinese real-estate crisis — the serial defaults of developers like Evergrande and Country Garden, the unfinished apartment towers, the collapse in land sales — has hammered the sector to which Chinese banks are most exposed. Layered underneath it sits the debt of Local Government Financing Vehicles, or LGFVs — the off-balance-sheet borrowing entities that provincial and municipal governments used for years to fund infrastructure, and which now stagger under obligations they cannot easily repay. Both of these are precisely the kind of exposure that should show up as bad loans on a bank's books.

Yet here is where the skeptic's antennae should twitch. As of mid-2025, Bank of China reported an NPL ratio of just 1.24% and a provision coverage ratio of 197.39% — numbers that suggest a loan book in robust health, comfortably reserved against losses.9 Can that possibly be the whole truth, in an economy going through the property downturn this one is? The honest analytical answer is: probably not entirely. Recall the mechanism from the bailout era. In a system where the state owns the bank and often the borrower too, a loan that would be written off in New York can instead be quietly "rolled over" — extended, refinanced, restructured — so that it never technically goes into default. State-directed refinancing of LGFV debt does exactly this at scale, and off-balance-sheet exposures blur the picture further. The reported NPL ratio is therefore best understood not as a lie but as an understatement — a number that reflects the state's willingness to prevent defaults as much as the underlying economic health of the borrowers. The tell is the heavy provisioning: the bank sets aside nearly two yuan of reserves for every yuan of admitted bad loans, which is prudent — but that provisioning is also part of what holds the bank's return on equity down to around 8.94%.10 Capital that sits in the provision jar cannot earn a return for shareholders.

Finally, there is the geopolitical tail. Operating in dozens of countries and sitting at the center of the global renminbi clearing network makes Bank of China uniquely exposed to a risk its purely domestic peers barely face: Western secondary sanctions, anti-money-laundering enforcement, and the broader machinery of a potential US–China financial decoupling. A bank whose competitive edge is its global plumbing is, by the same token, the most vulnerable if that plumbing is cut. It is a low-probability, high-severity risk — the kind that does not appear in any quarterly metric until the day it suddenly dominates everything. Having walked through the machinery and its stresses, we can now extract the durable lessons.

IX. Playbook: Business & Investing Lessons

Step back from the specifics, and Bank of China offers three lessons that generalize well beyond one Chinese bank.

The first is the double-edged nature of what we might call the sovereignty premium and discount. State ownership hands the bank something no private institution can buy: an absolute solvency and liquidity floor. Depositors and creditors of Bank of China face something very close to zero default risk, because behind the bank stands the full balance sheet of the Chinese state, which has both the means and the overwhelming political motive to prevent a systemic bank from failing. That is the premium, and it is enormous — it is why the bank can fund itself so cheaply and why its bonds are treated as quasi-sovereign. But the very same ownership imposes a permanent discount on the equity. When the controlling shareholder's objective is national economic stability and the 共同富裕 common prosperity agenda rather than the share price, equity holders must accept that value maximization is not, and will never be, the point. You cannot have the safety without the subordination; they are two faces of one coin.

The second lesson is a masterclass in conglomerate regulatory arbitrage. By holding roughly two-thirds of the Hong Kong-regulated BOCHK and 70% of Singapore-based BOC Aviation, Bank of China effectively runs high-margin, market-priced international businesses inside a group whose core is subject to mainland policy caps. Profits earned under Hong Kong and Singapore rules, in hard currency, flow up to a parent whose domestic earnings are being deliberately suppressed. It is a legal, structural way of sheltering a meaningful slice of the group's economics from the very policy machine that owns it. Investors should look for this pattern wherever a state-constrained parent controls market-facing subsidiaries in freer jurisdictions — it is often where the real value hides.

The third lesson is methodological: how to analyze state-directed financials at all. Reflexively applying Western yardsticks — is ROE expanding, is NIM widening — to a bank like this misses the forest for the trees, because the bank is not trying to maximize those metrics. The more revealing question is whether the bank can accomplish its actual mandate — funding national champions, absorbing policy costs, and refinancing troubled borrowers — without triggering the kind of balance-sheet crisis that would force another bailout. Measured against that mandate, the relevant KPI is capital-allocation efficiency relative to state targets, not return maximization. This does not mean an investor should be complacent about the metrics; it means understanding what the metrics are actually being managed toward. With that framing, we can weigh the two sides of the case.

X. Analysis & Bull vs. Bear Case

Let us war-game the competitive position first, because the moats here are real even if the returns are capped. Through the lens of Hamilton Helmer's 7 Powers and Porter's Five Forces, three durable advantages stand out. The first is scale economies: a retail deposit base measured in the tens of trillions of renminbi gives Bank of China one of the lowest funding costs achievable anywhere, and low-cost funding is the closest thing to a permanent edge a bank can have. The second is switching costs: corporate and sovereign clients whose payroll, trade finance, and cross-border settlement are wired into the bank's domestic and international clearing platforms do not casually move; the operational friction of leaving is enormous. The third, and most distinctive, is a genuine cornered resource: the state-granted status as the primary clearing house for offshore renminbi, a monopoly position no competitor can win by being better, only by the state choosing to reassign it.

On the Five Forces, the picture is a bank insulated on most fronts but squeezed on one. Rivalry among the Big Four is real but muted by their shared state ownership and coordinated policy roles — they compete for clients but not to the death. The threat of new entrants into systemically important state banking is essentially nil. Supplier power — depositors — is low, which is precisely why the bank can cut deposit rates to defend margin. The genuine pressure comes not from a competitor at all but from the bank's own owner, whose policy demands compress the domestic spread. In Porter's frame, the most dangerous force facing Bank of China is the buyer of last resort dictating the price of its core product.

The bull case is best understood as a compounding-yield machine rather than a growth story. The Hong Kong shares have traded for years at a deep discount to book value — a price-to-book ratio in the vicinity of 0.35 to 0.4 — which means the market is valuing the bank's equity at roughly a third of its stated net worth.11 Against that depressed price sits a dividend payout the bank has held at around 30% of earnings, underwritten by the Ministry of Finance as majority owner, which at these prices has translated into a dividend yield that has frequently run in the 7% to 8% range on the Hong Kong listing.111 The bull argument, then, is not that the shares will re-rate — they may never re-rate — but that they function as a premium, low-volatility, high-yield fixed-income proxy backed by the sovereign balance sheet. In a world hungry for safe yield, a near-sovereign 7%-plus payout with a solvency floor beneath it is a genuine proposition.

The bear case is that this is a policy-driven value trap — a stock that looks perpetually cheap because it perpetually deserves to be. The structural margin decay is not a cyclical dip but a secular condition: as long as Beijing needs the big banks to subsidize property bailouts, local-government refinancing, and inclusive-finance lending, the domestic spread will stay compressed and returns on equity will stay in the single digits. Stack on top of that the governance overhang — the Liu Liange saga and the abrupt executive turnover that recur across China's state banks — and you have an institution whose strategy can be disrupted from above at any moment and whose reported credit quality rests on state forbearance rather than transparent accounting. The bear does not argue the bank will fail; the bank will not be allowed to fail. The bear argues that a stock which is safe but structurally incapable of growing its per-share value, and whose cheapness is a permanent feature rather than a temporary anomaly, can disappoint patient capital for a very long time even as it pays its dividend.

An activist would find little room to operate here, and that itself is the point: there is no path to unlocking value by breaking up the conglomerate, replacing management, or forcing a buyback, because the controlling shareholder is the state and the state's objectives are not financial. The complexity of the structure, the political compensation of the executives, the opacity of the true loan book — all the things an activist would normally attack — are load-bearing features of the system, not fixable inefficiencies.

Which leaves the disciplined investor watching a small number of things. Three KPIs matter more than all the others: first, whether the net interest margin stabilizes — the single clearest signal of whether the domestic squeeze is bottoming; second, the provision coverage ratio and the pattern of NPL migration in property and LGFV exposures, which is where hidden impairment would first betray itself; and third, the share of profit contributed by overseas operations, the health of the global arbitrage that makes this bank different from its peers. Watch those three, and you are watching the real story rather than the headline.

XI. Epilogue & Outro

The remarkable thing about Bank of China is not that it is old, though a century and change is a long life for any financial institution. It is that it accomplished something most state enterprises never manage: it commercialized without ever ceasing to be an organ of the state. It learned to run a world-class aircraft lessor, to operate a note-issuing bank in a global financial center, to clear the currency of the world's second-largest economy across a dozen time zones — and it did all of that while remaining, at its core, an instrument of national policy answerable to the Party.

That is the paradox we opened with, now fully drawn. Bank of China is simultaneously one of the most internationally sophisticated financial institutions on earth and one of the most tightly controlled; simultaneously a source of premium hard-currency earnings and a subsidizer of domestic policy losses; simultaneously as safe as the Chinese state itself and as constrained as the Chinese state requires. For the investor, it remains what it has quietly been for a hundred years — the indispensable financial bridge between mainland China and the global capital markets. Whether that bridge is a compounding yield machine or a policy-driven value trap depends less on the bank's execution than on forces far above it: the trajectory of Chinese interest rates, the depth of the property overhang, and the state of relations between the two powers whose money flows across its network. It is a stable, high-yield, state-backed giant navigating a world that is, all around it, coming apart into rival blocs. The next chapter of its century will be written not in its branches but in the space between Beijing and Washington.

References

-

Bank of China 2024 Annual Report — Bank of China Limited, 2025-03-26 ↩↩↩↩↩↩↩

-

Ex-Bank of China Chairman Sentenced to Death With Reprieve — Bloomberg, 2024-11-26 ↩

-

Former Bank of China Chairman Sentenced to Death with 2-year Reprieve — China Daily, 2024-11-26 ↩

-

Bank of China Was Successfully Listed in Hong Kong and Opened a New Chapter in Its One-Hundred-Year History — Bank of China ↩

-

Bank of China prices world's sixth largest IPO close to top — FinanceAsia, 2006 ↩↩

-

Bank of China and Temasek Holdings Sign Strategic Investment Agreement — Temasek, 2005 ↩

-

Bank of China Acquires Singapore Aircraft Leasing Enterprise — Bank of China, 2006 ↩

-

Bank of China Limited 2025 Interim Report — Bank of China Limited, 2025-08 ↩↩↩↩↩↩↩↩↩↩↩

-

Bank of China reports rising revenue, profit in 2025 — Bank of China / Xinhua, 2026-03-30 ↩↩↩

-

Bank of China Limited (3988.HK) Corporate Profile & Stock Quote — Reuters ↩↩

-

Bank of China posts 2.18% rise in 2025 profit — MarketScreener, 2026-03-30 ↩

-

Listed banks in China: 2024 review and outlook — Ernst & Young, 2025-05 ↩↩

-

National Financial Regulatory Administration Official Portal — NFRA ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube