China Merchants Bank: The Private Champion of Chinese Finance

I. Introduction & Episode Setup

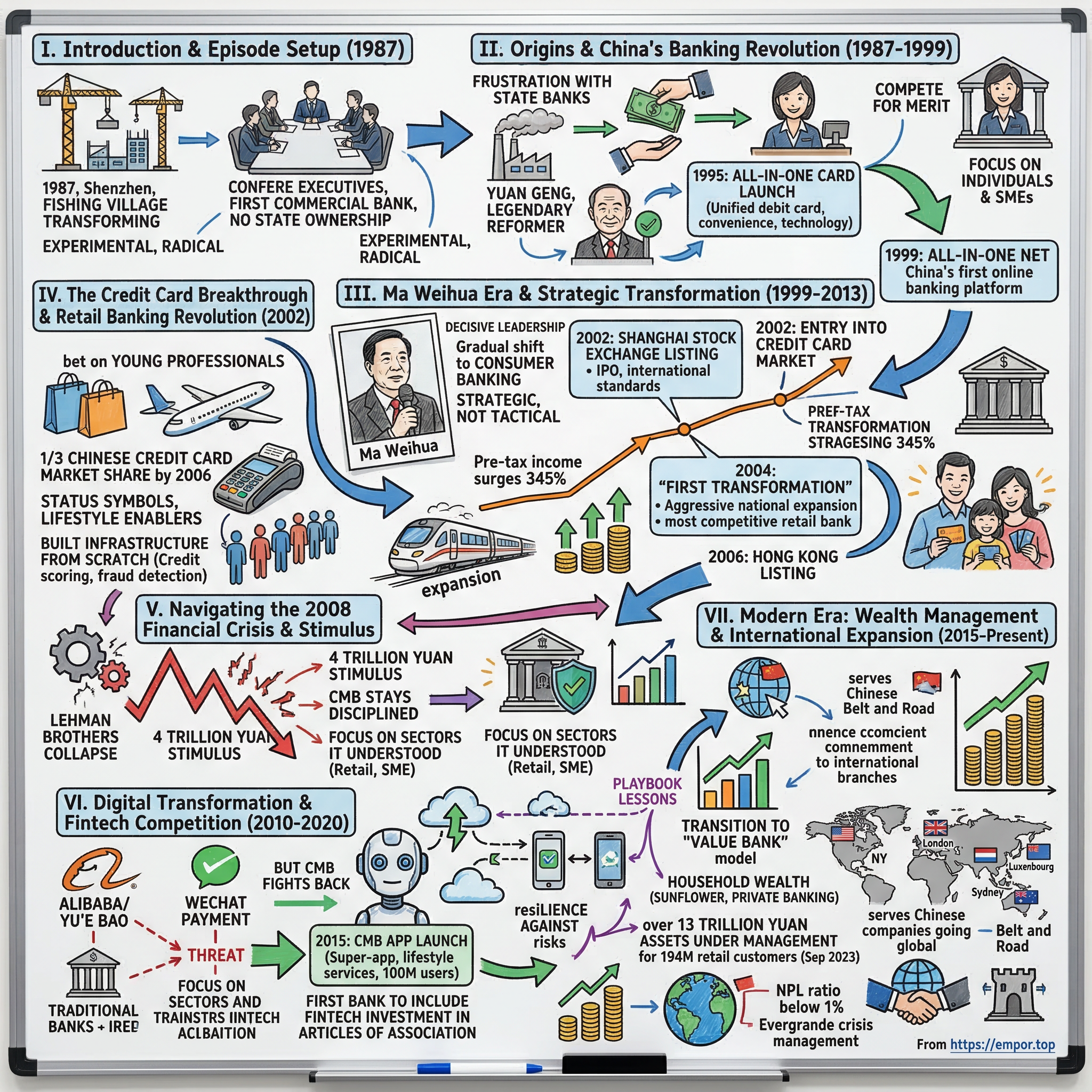

The year is 1987. Shenzhen is still a fishing village transforming into China's first Special Economic Zone. Construction cranes pierce the skyline like bamboo shoots after rain. In a modest office building near the port, a group of shipping executives from China Merchants Group gather around a conference table, their maritime company's 115-year history weighing on their shoulders. They're about to do something that hasn't been done in the People's Republic: create a commercial bank with no direct state ownership. No government guarantees. No political safety net. Just pure corporate ownership in a country where banking meant state control.

This was the birth of China Merchants Bank—an experiment so radical that even its founders weren't sure it would survive. The central question that drives this story isn't just how CMB survived—it's how this experimental non-state bank became China's retail banking innovator, pioneering everything from the country's first unified debit card to its most sophisticated wealth management platform, all while competing against state-owned giants with unlimited government backing. The story we're about to explore spans nearly four decades of Chinese economic transformation. It's a tale of how a bank with no political backing, no guaranteed deposits, and no state-directed lending quotas somehow became the innovation engine of Chinese finance. Along the way, we'll witness the creation of China's first unified debit card, the building of a credit card empire from nothing, and a digital transformation that would make Silicon Valley banks envious.

What makes CMB's journey particularly fascinating is that it is the first share-holding commercial bank wholly owned by corporate legal entities in China—a structure that forced it to compete on merit rather than political connections. Today, China Merchants Bank was ranked 26th in Forbes Global 2000 as of 2023, but the path to this position was anything but guaranteed.

II. Origins & China's Banking Revolution (1987–1999)

Picture Shenzhen in 1987: dust clouds from construction sites, the constant hammering of pile drivers, makeshift markets sprouting between half-finished buildings. This wasn't Beijing or Shanghai—this was the frontier, China's Special Economic Zone where Deng Xiaoping's famous words "to get rich is glorious" weren't just rhetoric but daily practice. Here, in a modest office building owned by China Merchants Group—a shipping conglomerate with roots stretching back to 1872—a radical experiment was about to begin. China Merchants Group's heritage stretched back to 1872, when it was founded as the China Merchants Steam Navigation Company by Viceroy Li Hongzhang—a shipping enterprise created to break the foreign monopoly on Chinese coastal trade. By the 1980s, under the leadership of Yuan Geng, who became the first CEO of the PRC-owned company on January 31, 1979, and founded the Shekou Industrial Zone in Shenzhen, the group had transformed itself into a conglomerate spanning shipping, real estate, and industrial development.

The decision to create a bank wasn't driven by financial theory or strategic planning. It was born from frustration. China Merchants Group's executives found themselves constantly stymied by the state banking system. Need a loan for port expansion? Wait months for approval from Beijing. Want to finance a joint venture? Navigate layers of bureaucracy at state banks who didn't understand commercial imperatives. The Big Four state banks—Industrial and Commercial Bank of China, China Construction Bank, Agricultural Bank of China, and Bank of China—operated more like government departments than financial institutions. They allocated credit based on political directives, not commercial merit. Yuan Geng, the legendary reformer who had already transformed Shekou Industrial Zone into China's first export-oriented industrial park, saw an opportunity. Yuan Geng, born Ouyang Rushan (1917-2016), was a Chinese guerrilla fighter, war hero, spy, policy visionary, and serial entrepreneur on behalf of the Chinese state who went on to create Shekou Industrial Zone, China International Marine Containers, CSG Holding, China Merchants Bank, and Ping An Insurance. At age 70, when most men would be considering retirement, Yuan was just getting started on his most audacious project.

On April 8, 1987, China Merchants Bank officially opened its doors—the first share-holding commercial bank wholly owned by corporate legal entities in China. The initial capital was modest: just 100 million yuan. The first branch had thirty employees. But what CMB lacked in resources, it made up for in hunger. Every employee knew they were part of an experiment that could fail. There were no guaranteed bailouts, no directive from Beijing ordering state enterprises to deposit funds with them. They had to compete for every customer, every deposit, every loan.

The early years were brutal. State-owned enterprises were instructed—sometimes explicitly, often implicitly—to bank with the Big Four. Government departments wouldn't even consider opening accounts with this upstart private bank. CMB's loan officers would visit potential clients only to be told, "Why should we trust you? You're not a real bank."

But adversity bred innovation. Unable to compete for the large corporate accounts that sustained the state banks, CMB's early leadership made a fateful decision: they would focus on the individuals and small businesses that the Big Four ignored. In the late 1980s, getting a personal bank account at a state bank meant waiting in line for hours, filling out forms in triplicate, and often being turned away because your deposit was too small to matter. CMB saw opportunity where others saw hassle. The breakthrough came in 1995 with the launch of the All-in-One Card—a revolutionary product that would reshape Chinese banking. The All-in-One Card was launched as early as 1995, and was the first bank card managed based on customer numbers, with CMB issuing 5,988 All-in-One Cards with an average deposit of over RMB9,800, making it one of the most popular bank cards in China. Before this, Chinese consumers juggled multiple passbooks for different types of accounts—one for savings, another for fixed deposits, yet another for foreign currency. Each transaction meant queueing at different counters, dealing with different clerks, navigating different systems.

CMB's All-in-One Card integrated everything into a single magnetic stripe card—a concept so foreign to Chinese banking that regulators initially didn't know how to classify it. There wasn't much difference between a deposit book and a magnetic strip card. In this background, CMB was rather bold to replace deposit books with magnetic strip cards. The card allowed instant transfers between accounts, ATM access, and even primitive point-of-sale transactions. For the first time, Chinese consumers experienced what Western bank customers had taken for granted for decades: convenience.

But the real genius wasn't just the technology—it was the execution. CMB trained its staff obsessively on customer service, something unheard of in Chinese banking. Tellers were taught to smile, to remember regular customers' names, to process transactions quickly. Branch managers were given performance targets based not just on deposits but on customer satisfaction scores. This cultural revolution within Chinese banking proved as important as any technological innovation.

By 1999, CMB took another leap with All-in-One Net, China's first online banking platform. All-in-One Net is China's first online banking platform. Those who did pass the "internet survival experiment" in 1999 did so via CMB's "All-in-one Card" service. While the Big Four banks were still debating whether the internet was a fad, CMB was already processing transactions online, allowing customers to check balances and transfer funds from their homes—revolutionary in a country where banking had always meant physical presence and paper documentation.

These innovations weren't just products; they were declarations of intent. CMB was positioning itself as the bank for China's emerging middle class—the entrepreneurs, professionals, and private business owners who valued their time and wanted banking that worked around their schedules, not the other way around. By the end of the 1990s, this experimental bank from Shenzhen had proven it could survive. The question now was whether it could thrive. The answer would come from an unlikely source: a shipping executive turned banker who would transform CMB from a regional upstart into a national powerhouse.

III. Ma Weihua Era & Strategic Transformation (1999–2013)

The boardroom at CMB headquarters in December 1998 was tense. Directors faced a stark choice: continue as a competent regional bank with decent returns, or gamble everything on aggressive national expansion and retail banking—a sector the Big Four dominated through sheer scale. Into this pivotal moment walked Ma Weihua, a 49-year-old economist with no banking experience but a reputation for transforming struggling state enterprises. His appointment as president in March 1999 raised eyebrows across Chinese finance. Why hire an outsider when the bank needed someone who understood its unique culture? Ma Weihua's answer became clear within weeks. This four part case series describes the transformation of CMB under Ma Weihua's leadership beginning in 1999. After having worked in the People's Bank of China (PBOC) for 10 years, Ma Weihua became the second president of China Merchants Bank (CMB). His first crisis came almost immediately: Almost as soon as he took office, he had to deal with a run on CMB's Shenyang branch. Fortunately, Ma had handled a similar situation in his former post, when there was a crisis of confidence in Hainan Development Bank. This time Ma swiftly dispatched additional funds to Shenyang and ordered that the branch be kept open around the clock, as a show of confidence. It worked, defusing the crisis.

This early test revealed Ma's leadership style: decisive, theatrical when necessary, and unafraid of bold gestures. But his real transformation of CMB would be strategic, not tactical. For the new CEO, the next challenge was greater: figuring out a means to differentiate CMB from the much larger state rivals that dominated corporate lending. His solution? CMB gradually shifted its focus to consumer banking.

The numbers from this era tell a remarkable story. Headquartered in Shenzhen, the forefront of China's reform and opening-up, CMB had only RMB100 million in capital, one branch and just thirty employees at the beginning. By 2007, under Ma's leadership, CMB was the most profitable bank in China, but new challenges still lay ahead. This transformation didn't happen overnight—it was the result of calculated risks and relentless innovation.

Ma's masterstroke came in 2002 when CMB decided to enter the credit card market—a segment that barely existed in China. Cash was still king, and the concept of consumer credit was alien to most Chinese. The Big Four banks saw credit cards as a Western curiosity, not a serious business opportunity. Ma saw differently. But first came a critical milestone: CMB listed on the Shanghai Stock Exchange in 2002. The IPO raised much-needed capital for expansion, but more importantly, it forced CMB to adopt international accounting standards and governance practices. This wasn't just about money—it was about credibility. Being a public company meant transparency, quarterly earnings calls, and accountability to shareholders beyond just China Merchants Group.

The online banking revolution that Ma championed also gained momentum. The online banking business prospered right after as CMB became the first commercial bank in China with financial services provided online. He was the first to establish online banking, which became China's leading paying bank for electronic business. In an era when most Chinese banks still required customers to visit branches for every transaction, CMB was processing payments over dial-up internet connections.

But the real revolution came in 2004 when Ma made his boldest strategic call. In 2004, Ma officially demanded the 'first transformation' – this involved vast expansion in retail business with an emphasis on service upgrades. At a time in which most banks were focusing on the profitable to-B side, CMB made a conscious decision to take on most of the retail business. The results were staggering: From 2004 to 2008, the pre-tax income of CMB surged over 345%.

This wasn't just a shift in focus—it was a complete reimagination of what a Chinese bank could be. With the knowledge of advanced modes and products of foreign banks, Ma took the lead in proposing the issue of CMB transformation in 2004. In his opinion, CMB should develop its SME business and try to create the most competitive retail bank in China. While the Big Four chased mega-loans to state enterprises, CMB built relationships with individual consumers and small businesses, sectors that would drive China's economic growth for the next two decades. The Hong Kong listing came in September 2006, raising HK$20.69 billion at between HK$7.30 and HK$8.55 per share. CMB's IPO in Hong Kong fetched about $2.4 billion. This dual-listing structure gave CMB access to both domestic and international capital markets, positioning it perfectly for the credit card revolution that was about to unfold.

Ma's leadership style was distinctive. Shanghai Securities News described Ma – who ran CMB for 14 years – as the "heart and soul" of the bank. He combined the strategic thinking of an economist with the showmanship of a startup founder. Guided by Ma, CMB created a uniform electronic platform and established a social image of the most technology-advanced bank. When Bloomberg's mayor welcomed CMB's New York branch opening in 2008, he called it "a breeze in the winter of Wall Street"—high praise during the depths of the financial crisis.

By the end of Ma's tenure in 2013, the transformation was complete. On May 31, 2013, Ma Weihua left the office of president of China Merchants Bank. In his letter of farewell to all the staff members, he quoted Mandela's words: "The most difficult thing to change is not the world, but to change yourself." But Ma had done both—he had changed himself from a government official to a banker, and in doing so, had changed Chinese banking forever. Under his leadership, CMB had grown from a regional player into China's sixth-largest bank, but more importantly, it had become the innovation engine of Chinese finance.

IV. The Credit Card Breakthrough & Retail Banking Revolution (2002–2010)

The conference room at CMB's Shenzhen headquarters in early 2002 was divided. On one side sat the conservatives, arguing that credit cards were a Western luxury inappropriate for China's cash-based society. On the other, the innovators pushed for what seemed like financial suicide: betting the bank's future on a product most Chinese had never heard of. The debate wasn't academic—it would determine whether CMB remained a competent mid-tier bank or became something unprecedented in Chinese finance. The turning point came when CMB decided to issue China's first dual-currency credit card compliant with international standards. CMB issued the first dual-currency credit card compliant with international standard and 36 million such cards have been issued to date. This issuance is even included in the MBA case studies of Harvard University. This wasn't just another product launch—it was a calculated bet that Chinese consumers were ready for credit.

The strategy was brilliant in its simplicity. While state banks focused on corporate lending with its guaranteed returns, CMB targeted young professionals in China's booming coastal cities—people with rising incomes, international aspirations, and no patience for traditional banking. These were the consumers buying their first cars, taking their first overseas vacations, booking flights online. They needed credit, and CMB was ready to provide it.

By April 2006, CMB had issued a total of over 5 million credit cards, capturing one-third of the Chinese credit card market. By successfully entering the emerging credit card industry, the bank confirmed its retail banking strategy in 2004, followed by its great success in occupying 1/3 credit card market share. This wasn't incremental growth—it was market domination. In a country where credit cards barely existed five years earlier, CMB had built a business that would make American Express envious.

The numbers tell only part of the story. Behind the statistics was a revolution in how Chinese consumers thought about money. CMB's credit cards weren't just payment tools—they were status symbols, lifestyle enablers, keys to a modern, globalized life. The bank's marketing didn't sell interest rates or credit limits; it sold dreams. Young couples could buy furniture for their first apartment without waiting years to save. Entrepreneurs could smooth cash flow in their startups. Students could study abroad without their parents liquidating assets.

But perhaps the most impressive achievement was building the infrastructure from scratch. In 2002, China lacked the basic systems American banks took for granted: credit bureaus, fraud detection systems, merchant networks. CMB had to create it all. They built relationships with merchants one by one, convincing skeptical shopkeepers that accepting credit cards would boost sales. They developed proprietary risk models using whatever data they could gather, since China had no FICO scores or credit histories. They trained thousands of staff in credit assessment, fraud prevention, customer service—skills that didn't exist in Chinese banking.

The technology backbone was equally revolutionary. While the Big Four banks still processed transactions on mainframes from the 1980s, CMB built modern, scalable systems that could handle millions of transactions. They pioneered real-time fraud detection, instant credit approvals, mobile banking integration—capabilities that wouldn't become standard in Western banks for another decade. By the end of 2010, CMB had captured the rewards of its retail banking revolution. At the end of 2008, its retail sector accounted for near 20% of income. But more impressively, the bank had built a fee-income business that would prove crucial during the next crisis. Credit cards, wealth management products, and transaction fees provided stable revenue streams independent of interest rate cycles. This diversification would prove prescient when the 2008 financial crisis struck, testing every assumption about Chinese banking.

V. Navigating the 2008 Financial Crisis & Stimulus

October 2008. Lehman Brothers had collapsed a month earlier. Wall Street was in chaos. European banks were being nationalized. And in CMB's headquarters, Ma Weihua faced a conference call that would define his legacy. China Merchants Bank opened its New York branch on October 8, 2008, just as Lehman Brothers was in throes of collapsing and the global economic crisis began escalating. The timing couldn't have been worse—or perhaps, in retrospect, better.

The global financial crisis of 2008 seemed to catch China, and the rest of the world, off guard. To offset the sharp decline in global demand and the resulting slowdown in China's growth, the Chinese government announced in November 2008 a two-year, 4 trillion yuan ($629 billion) stimulus program designed to improve overall economic growth, invest in the nation's infrastructure, and stimulate domestic consumer demand. A statement on the government's website said the State Council of the People's Republic of China had approved a plan to invest 4 trillion yuan in infrastructure and social welfare by the end of 2010.

For Chinese banks, this stimulus was both opportunity and trap. The Big Four state banks, following government directives, opened the lending floodgates. Credit grew at unprecedented rates—In 2009, some $1.46 trillion (Y 9.95 trillion) in lending was granted, with another $1.09 trillion (Y 7.5 trillion) in credit to be issued in 2010. Much of this lending went to local government financing vehicles (LGFVs) and state-owned enterprises, often for projects with questionable economic returns.

CMB faced a strategic crossroads. Join the lending party and risk a mountain of bad loans, or stay disciplined and potentially miss the biggest credit boom in Chinese history? Ma Weihua chose a middle path that would prove inspired. CMB did increase lending—it had to, given political pressure—but it focused on sectors and borrowers it understood: retail customers, small and medium enterprises, and carefully selected infrastructure projects with clear revenue streams.

The bank's retail focus proved its salvation. While other banks chased mega-projects—a new airport here, a ghost city there—CMB stuck to its knitting. Mortgages to middle-class families. Working capital loans to profitable SMEs. Credit cards to young professionals. Boring? Perhaps. But also profitable and, crucially, recoverable.

The results were remarkable. NPLs ratio started to increase following a continuous decline between 2005 and 2012. But the NPL rate was quite low, particularly for a developing economy at the end of 2010. CMB's disciplined approach during the stimulus years meant its asset quality remained stronger than peers who had gorged on infrastructure lending.

The crisis also validated Ma Weihua's retail strategy in ways no one anticipated. While corporate loans to overleveraged state enterprises and local governments would eventually sour, CMB's mortgages to middle-class families and credit cards to young professionals continued performing. The bank's fee income from wealth management and transaction services provided ballast when net interest margins compressed. By 2013, when Ma stepped down, CMB had emerged from the crisis stronger than before—a testament to the power of strategic discipline over opportunistic growth.

VI. Digital Transformation & Fintech Competition (2010–2020)

The year 2013 marked a watershed moment in Chinese finance, though few recognized it at the time. In June, Alibaba launched Yu'e Bao, a money market fund accessible through Alipay that offered returns far exceeding bank deposits. Within a year, it became the world's largest money market fund. WeChat Payment followed in August 2013, turning China's most popular messaging app into a financial platform. Suddenly, CMB wasn't competing with other banks—it was fighting tech giants with billions of users and no legacy infrastructure.

The initial response from traditional banks was denial, then panic. The Big Four dismissed mobile payments as a niche product for young people buying bubble tea. But at CMB, the new leadership under President Tian Huiyu recognized an existential threat. Hit by the 2008 financial crisis, central bank interest rate cuts, as well as cutthroat competition, China Merchants Bank's momentum halted. And it was forced to change yet again, by cost reduction to gradually recovery in growth.

The bank's response was radical: instead of fighting the tech giants, collaborate with them. In 2016, CMB began partnering with Tencent and Alibaba, integrating their payment systems, sharing data (within regulatory limits), and co-developing financial products. This wasn't capitulation—it was strategic jujitsu, using the tech giants' strength to amplify CMB's own capabilities.

But partnership was only part of the strategy. CMB also embarked on its own digital transformation, investing billions in technology infrastructure. China Merchants Bank is the first commercial bank in China to include the ratio of fintech investment in its Articles of association. In recent years, it has set the ambitious goal of becoming the "strongest bank in fintech" with continuous strengthening of information technology infrastructure.

The centerpiece of this transformation was the CMB App, launched in 2015 and continuously upgraded. Unlike the clunky mobile banking apps of competitors, CMB's offering was designed like a consumer technology product. It featured lifestyle services beyond banking—movie tickets, restaurant reservations, shopping discounts. The app became a super-app before banks understood what super-apps were. By 2020, it had over 100 million users, with many checking it daily—engagement rates that rivaled social media platforms.

CMB also pioneered the use of artificial intelligence in Chinese banking. The bank developed intelligent risk control engines that could assess credit risk in real-time, approve loans in seconds, and detect fraud patterns invisible to human analysts. Customer service chatbots handled millions of queries, freeing human staff for complex problems. Robo-advisors provided wealth management advice to mass-affluent customers who couldn't afford human advisors.

The technology investments extended to the back office. CMB rebuilt its core banking systems, moving from mainframes to cloud infrastructure. This wasn't just modernization—it was a fundamental reimagining of how a bank operates. Processes that once took days now happened in real-time. Products that once required months to launch could be deployed in weeks.

By 2020, the results were undeniable. CMB had successfully navigated the fintech disruption that destroyed traditional banks in other markets. Its retail customer base exceeded 150 million. Digital channels accounted for over 90% of transactions. Most remarkably, the bank maintained its premium positioning even as fintech companies commoditized basic banking services.

VII. Modern Era: Wealth Management & International Expansion (2015–Present)

As China's economy matured and its middle class expanded, CMB recognized another strategic inflection point. The country's household wealth was exploding—from $7 trillion in 2010 to over $70 trillion by 2020—creating unprecedented demand for sophisticated financial services. CMB's pivot to wealth management wasn't just about following the money; it was about anticipating where Chinese society was heading.

The transformation began with segmentation. CMB created distinct service tiers: Sunflower for mass affluent (1-5 million yuan in assets), Golden Sunflower for high net worth (over 5 million yuan), and Private Banking for ultra-high net worth individuals (over 10 million yuan). Each tier received tailored products, dedicated relationship managers, and exclusive privileges. This wasn't the mass-market retail banking that built CMB—it was personalized, advisory-driven wealth management.

As of September 2023, China Merchants Bank has over 13 trillion yuan in total assets under management for 194 million retail customers. Six months after officially transitioning to the "Value Bank" model, it has more than one trillion yuan in public funds under management becoming the first bank to achieve this milestone.

International expansion accelerated during this period. After establishing its New York branch in 2008 and London branch in 2016, CMB continued building its global network. The strategy wasn't to compete with global banks on their turf but to serve Chinese companies going global and international firms entering China. CMB's Luxembourg branch, opened in 2018, became a hub for European operations. The Sydney branch followed in 2019, tapping into Australia's significant Chinese diaspora and bilateral trade.

But expansion brought new challenges. Property sector exposure emerged as a critical risk as China's real estate bubble showed signs of strain. The Evergrande crisis in 2021 sent shockwaves through the banking system. China Merchants Bank has been continuously adjusting its strategies to stay resilience against risks, maintaining asset quality and keeping the non-performing loan(NPL) ratio below 1%. The bank also actively works to clear risks related to real estate. In the third quarter this year, its property NPL balance and ratio both edged down quarterly for the first time in 10 months.

Regulatory pressures intensified as Beijing pursued "common prosperity" policies aimed at reducing inequality. Wealth management products faced stricter scrutiny. Lending to property developers was curtailed. Capital requirements tightened. CMB had to navigate between commercial imperatives and political directives—a balance that became increasingly precarious.

The COVID-19 pandemic tested CMB's digital infrastructure like never before. With branches closed and customers confined to homes, digital channels became the only channels. The investments in technology paid off spectacularly. While competitors struggled with system crashes and service disruptions, CMB's platforms handled the surge seamlessly. The pandemic accelerated digital adoption by years, validating the bank's technology-first strategy.

Current leadership under President Wang Liang faces a complex landscape. China's economy is slowing, property developers are defaulting, demographic headwinds are building, and geopolitical tensions threaten international expansion. Yet CMB's position remains strong. The bank's retail franchise generates stable returns. Its wealth management platform captures the growing affluent market. Its technology infrastructure rivals any global bank.

VIII. Key Inflection Points Analysis

Looking back at CMB's journey, five critical moments stand out as inflection points that fundamentally altered the bank's trajectory. Each represents not just a business decision but a bet on China's future that required courage, vision, and perfect execution.

The All-in-One Card Launch (1995) seems obvious in retrospect but was revolutionary at the time. Before this, Chinese banking meant multiple passbooks, endless queues, and bureaucratic friction. The All-in-One Card didn't just consolidate accounts—it introduced the concept of customer convenience to Chinese banking. It created network effects before anyone in Chinese finance understood what network effects were. Every new cardholder made the network more valuable, creating a virtuous cycle that competitors couldn't replicate without years of investment.

The Retail Banking Pivot (2004) was Ma Weihua's masterstroke. When every other bank was chasing corporate mega-loans with their guaranteed returns and political prestige, CMB bet on individuals. This wasn't just contrarian—it was heretical. But Ma understood something his peers didn't: China's economic future belonged to its emerging middle class, not its state-owned enterprises. The retail pivot positioned CMB perfectly for two decades of consumption-driven growth.

Credit Card Market Entry & Dominance (2002-2008) created a business from nothing. In 2002, credit cards were exotic financial instruments most Chinese had never seen. By 2008, CMB controlled a third of the market. This wasn't luck—it was systematic execution. CMB built credit scoring models without credit history, fraud detection systems without fraud patterns, and merchant networks without existing infrastructure. They essentially created Chinese consumer credit culture.

The 2013 Digital Transformation Decision came at the perfect moment. Alibaba and Tencent were just beginning to threaten traditional banking. Most banks were still in denial. CMB's decision to invest massively in technology—not just systems but culture, talent, and partnerships—positioned it to surf the fintech wave rather than be drowned by it. This transformation touched everything: products, processes, people. It turned a traditional bank into a technology company that happens to have a banking license.

The 2016 Fintech Partnership Strategy marked the evolution from competition to "coopetition." Rather than fight the tech giants in a war it couldn't win, CMB chose collaboration. This required swallowing corporate pride and accepting that banks were no longer the sole gatekeepers of finance. But it also gave CMB access to billions of users, cutting-edge technology, and innovation capabilities no bank could build alone.

Each inflection point shares common characteristics: they anticipated market shifts years in advance, required significant investment before returns were clear, and fundamentally changed how CMB operated. Most importantly, each built on the previous ones, creating cumulative advantages that competitors couldn't replicate simply by copying individual initiatives.

IX. Playbook: Business & Investing Lessons

CMB's journey offers profound lessons for both business operators and investors, particularly about competing in regulated markets, building sustainable moats, and managing the tension between innovation and tradition.

First-mover advantages in regulated markets prove especially powerful. Unlike technology markets where fast followers can quickly catch up, banking regulations create massive barriers to replication. CMB's early licenses, approved products, and established processes became competitive moats. Regulators, naturally conservative, trusted CMB with innovations they wouldn't permit newcomers. Each successful innovation made the next approval easier, creating a regulatory flywheel effect.

Building moats through customer experience sounds simple but proves devastatingly effective. CMB didn't have the Big Four's government backing, political connections, or unlimited capital. So it competed on the one dimension state-owned enterprises struggled with: customer service. This wasn't just about smiling tellers—it was about fundamentally reimagining banking from the customer's perspective. Every process, product, and policy was evaluated through the lens of customer experience. Over time, this created a brand premium that translated into pricing power and customer loyalty.

The power of retail deposit franchises becomes clear during crises. Corporate deposits are fickle, flowing to whoever offers the highest rates or best connections. Retail deposits are sticky, especially when combined with comprehensive services. CMB's millions of retail customers provide stable, low-cost funding that enables profitable lending. This deposit franchise—built over decades—cannot be replicated quickly regardless of capital investment.

Technology as competitive advantage in traditional industries requires more than just spending money. CMB succeeded because it treated technology as core to strategy, not just operations. Technology wasn't just about efficiency—it was about creating entirely new products, reaching previously unreachable customers, and building data advantages that compound over time. The bank's technology transformation succeeded because it changed culture, not just systems.

Managing state vs. private ownership dynamics remains CMB's most delicate balance. As China's only major bank without direct state ownership, CMB must navigate between commercial imperatives and political realities. This requires sophisticated stakeholder management, careful communication, and strategic alignment with national priorities while maintaining operational independence. The bank's success proves that this balance, while difficult, is possible.

Capital efficiency and ROE optimization strategies distinguish great banks from good ones. CMB consistently generates returns on equity above 15%, exceptional for a bank operating with Basel III capital requirements. This comes from disciplined capital allocation, focus on fee-generating businesses that don't consume capital, and rigorous risk management that minimizes write-offs. The bank proves that in banking, how you deploy capital matters more than how much capital you have.

Network effects in financial services create winner-take-all dynamics in specific niches. CMB's credit card business, wealth management platform, and digital ecosystem all exhibit network effects where value increases exponentially with scale. Understanding and deliberately building these network effects—through product design, partnership strategies, and platform approaches—creates competitive advantages that strengthen over time.

X. Analysis & Bear vs. Bull Case

As we evaluate CMB today, the investment case presents a fascinating study in contrasts. The bull case rests on structural advantages and secular trends, while the bear case reflects cyclical challenges and systemic risks.

The Bull Case starts with CMB's unassailable retail franchise. With nearly 200 million retail customers generating over half of revenues, the bank has built China's premier retail banking platform. This isn't just about numbers—it's about quality. CMB's customers are younger, wealthier, and more digitally engaged than any competitor's. They're the entrepreneurs, professionals, and innovators driving China's economic transformation.

The wealth management opportunity alone could double CMB's business. China's household wealth continues growing despite economic headwinds, and regulatory changes are pushing savings from property into financial assets. CMB's private banking and wealth management platforms are perfectly positioned to capture this shift. The bank already manages over 13 trillion yuan in customer assets—a number that could triple as China's wealth management industry matures.

Technology leadership among traditional banks provides sustainable competitive advantage. While fintech companies grabbed headlines, CMB quietly built capabilities that rival any digital bank: real-time risk assessment, AI-driven customer service, cloud-based infrastructure. These aren't just efficiency improvements—they're fundamental capabilities that enable new products and services impossible for banks running on legacy systems.

Superior asset quality versus state-owned peers reflects disciplined underwriting and risk management. In 2022, the non-performing loan ratio at China Merchants Bank was 0.96 percent, among the lowest ratio since 2014. This isn't luck—it's the result of systematic credit culture, sophisticated risk models, and willingness to walk away from bad deals regardless of political pressure.

The Bear Case begins with property sector exposure. Despite prudent management, CMB cannot fully insulate itself from China's property crisis. Real estate-related loans, including mortgages, developer loans, and loans secured by property, represent significant exposure. A severe property downturn could trigger waves of defaults that overwhelm even conservative underwriting.

Regulatory uncertainty clouds the outlook. Common prosperity policies could cap fees, force lending to unprofitable sectors, or require costly social programs. The regulatory pendulum in China swings dramatically, and banks often bear the cost of policy shifts. CMB's premium positioning makes it particularly vulnerable to populist measures targeting wealth inequality.

Fintech competition continues intensifying. While CMB successfully navigated the first fintech wave, new threats emerge constantly. Digital banks backed by tech giants operate with lower costs and fewer regulatory constraints. Cryptocurrency and central bank digital currencies could disrupt traditional banking infrastructure. CMB must continue investing billions in technology just to maintain competitive parity.

Margin compression from rate liberalization presents ongoing challenges. As China liberalizes interest rates and increases banking competition, net interest margins face structural pressure. CMB's superior margins make it particularly vulnerable to compression. Fee income growth must accelerate to offset declining spread income—a challenge as regulators scrutinize wealth management fees.

Geopolitical risks affecting international expansion cannot be ignored. Rising tensions between China and the West threaten CMB's global ambitions. Sanctions, regulatory restrictions, or forced divestments could derail international growth plans. Even without explicit actions, the poisoned atmosphere makes winning international business increasingly difficult.

XI. Epilogue & "If We Were CEOs"

If we were running CMB today, our strategic priorities would focus on navigating the treacherous transition from China's old economy to its new one while maintaining the bank's innovation edge.

First, we would accelerate the pivot from traditional lending to capital-light businesses. Wealth management, transaction banking, and advisory services generate high returns without consuming regulatory capital. We'd set an aggressive target: 70% of revenues from non-interest income within five years. This isn't abandoning banking—it's evolving beyond banking.

Second, international expansion needs rethinking. Rather than competing globally, we'd focus on specific corridors where CMB has unique advantages: serving Chinese companies expanding abroad and facilitating Belt and Road transactions. We'd build partnerships rather than branches, leveraging technology to serve customers without physical presence.

Third, technology investment must evolve from digitizing existing processes to reimagining banking entirely. We'd create autonomous AI agents that manage entire customer relationships, blockchain-based systems that eliminate settlement risk, and embedded finance platforms that make banking invisible. The goal isn't to be a better bank—it's to transcend banking.

Fourth, managing the property cycle aftermath requires surgical precision. We'd create specialized workout units, partner with asset management companies, and potentially spin off non-performing assets into separate vehicles. The goal is to clean up the balance sheet quickly while preserving capital and maintaining market confidence.

Finally, we'd embrace regulatory alignment while maintaining commercial discipline. This means proactively supporting government priorities—rural finance, green lending, small business support—but through innovative models that remain profitable. Technology enables serving previously unprofitable segments at acceptable returns.

The next decade will test CMB like never before. China's economy faces structural headwinds: demographics, debt, and deglobalization. The financial system must navigate between supporting growth and managing risks. Technology continues disrupting traditional business models.

Yet CMB's history suggests it will not just survive but thrive. Every crisis has made it stronger. Every challenge has sparked innovation. Every threat has become an opportunity. The experimental bank from Shenzhen has proven that in Chinese finance, as in life, it's not the strongest or largest that survive—it's the most adaptable.

Conclusion

China Merchants Bank's journey from a modest experiment in Shenzhen to one of Asia's most valuable banks represents more than a corporate success story—it's a lens through which to understand China's entire economic transformation. The bank that began with 30 employees and 100 million yuan in capital now serves nearly 200 million customers and manages over 13 trillion yuan in assets.

What makes CMB's story remarkable isn't just its growth but its method. In a system designed to favor state-owned enterprises, a bank with no government backing became the innovation engine of Chinese finance. While competitors relied on political connections and directed lending, CMB competed on merit, service, and innovation. Each challenge—from the Asian Financial Crisis to the fintech disruption—forced adaptation that ultimately strengthened the bank.

The lessons extend beyond banking. CMB proves that in regulated markets, first movers can build insurmountable advantages. That customer experience creates more durable moats than capital or connections. That technology transformation requires cultural change, not just system upgrades. That navigating between commercial and political imperatives, while difficult, remains possible.

As China enters a new era of slower growth, technological disruption, and geopolitical tension, CMB faces its greatest test. Property bubbles threaten asset quality. Regulatory shifts challenge business models. International expansion faces headwinds. Yet the bank's track record suggests it will adapt, evolve, and ultimately thrive.

The story of China Merchants Bank is far from over. The next chapters will be written in code and algorithms, in wealth management products and global partnerships, in navigating between China's past and its future. But if history is any guide, the bank that began as an experiment in market-oriented finance will continue pioneering the future of Chinese banking.

For investors, operators, and students of business, CMB offers a masterclass in building enduring competitive advantages in dynamic markets. The bank's journey reminds us that in business, as in evolution, survival belongs not to the strongest or largest, but to those most responsive to change. In that regard, China Merchants Bank has proven itself supremely fit for whatever future awaits.

XII. Recent News

The financial landscape for CMB in 2024 presents a complex picture of resilience amid challenging conditions. In 2024, CMB's operating income was 337.537 billion yuan, a year-on-year decrease of 0.47%, while net profit attributable to shareholders was RMB148.391 billion, representing a year-on-year increase of 1.22%. This modest profit growth against declining revenue reflects the bank's operational efficiency and cost management capabilities during a period of significant industry headwinds.

Asset quality metrics demonstrate CMB's disciplined risk management approach. As of 31 December 2024, the Group's non-performing loan ratio was 0.95%, unchanged from the end of the previous year. This stability is remarkable given the broader challenges facing Chinese banks, particularly regarding property sector exposure. The provision coverage ratio was 411.98%, down 25.72 percentage points from the end of the previous year, and the loan provision ratio was 3.92%, down 0.22 percentage points from the end of the previous year.

The third quarter 2024 results provided additional context to CMB's performance trajectory. Key financial highlights include a 5.68% increase in total assets to RMB 11,654.763 billion and a 7.08% growth in equity attributable to shareholders. However, the bank saw a slight decrease in net profit and net operating income year-on-year, with a 0.62% decline in net profit attributable to shareholders. The bank also achieved a significant increase in net cash generated from operating activities, marking a 435.40% rise, driven by higher customer deposits and reduced loan increments.

The property sector remains a critical watch point for all Chinese banks. By the end of 2024, China's commercial bank loans to property developers accounted for about 6.2% of total loans, while residential mortgage loans accounted for about 17.3%. For context, Banks are faced with an elevated non-performing loans (NPLs) ratio in the property sector, with a median NPL ratio of 2.79 per cent among the top 18 banks. The average property-related bad loan ratio across China's "big four" state-owned banks was 5.2 per cent.

CMB's relatively lower NPL ratio compared to peers reflects its more conservative underwriting and better exposure to tier-one cities where property values have proven more resilient. The bank's asset quality remained stable, with a non-performing loan ratio of 0.94% in Q3 2024, significantly better than the industry average of 1.56%.

Looking forward, CMB faces both opportunities and challenges. We expect Chinese bank residential mortgage loan portfolio to resume low single digit growth in 2025, recovering from a decline of 1.3% in 2024 and 1.6% in 2023. The government's various measures to support the housing market, including cutting interest rates, also help homebuyers confidence as well as developers. This potential recovery in mortgage lending could benefit CMB's retail franchise, though margin pressures persist.

The regulatory environment continues evolving with measures to support the property market while preventing systemic risks. China's minister of housing and urban-rural development Ni Hong announced that the country will expand its "whitelist" of real estate projects and increase bank lending to 4 trillion yuan by year-end. China approved a total of 2.23 trillion yuan in loans to "whitelisted" developers. CMB's participation in these programs will be selective, maintaining its focus on asset quality over growth.

International expansion faces new complexities as geopolitical tensions influence cross-border banking relationships. While CMB maintains its branches in New York, London, Luxembourg, and Sydney, the focus has shifted from aggressive expansion to consolidating existing operations and serving the Belt and Road corridor where political risks are more manageable.

Digital innovation remains a bright spot. The bank's continued investment in artificial intelligence, cloud infrastructure, and mobile banking positions it well for the next phase of financial services evolution. With over 100 million mobile app users and digital channels handling over 90% of transactions, CMB has successfully transformed from a traditional bank to a technology-enabled financial services platform.

XIII. Links & Resources

For those seeking deeper insights into CMB's journey and Chinese banking evolution, several resources prove invaluable:

Primary Sources: - China Merchants Bank Investor Relations (english.cmbchina.com/CmbIR) - Annual Reports and Quarterly Earnings (2002-2024) - Hong Kong Stock Exchange Filings (3968.HK) - Shanghai Stock Exchange Disclosures (600036.SS)

Academic Case Studies: - Harvard Business School: "China Merchants Bank" (Case Series 309-047) - INSEAD: "China Merchants Bank: Ma Weihua's First Transformation" - Stanford GSB: "Digital Banking in China: The CMB Story"

Books on Chinese Banking Reform: - "Red Capitalism" by Walter and Howie - "China's Great Wall of Debt" by Dinny McMahon - "The Chinese Banking Industry" by Yuanyuan Peng - "Banking Reform in China" by Violaine Cousin

Regulatory Documents: - People's Bank of China Policy Papers - China Banking and Insurance Regulatory Commission Guidelines - National Financial Regulatory Administration Reports

Industry Analysis: - McKinsey: "China Banking Annual Reports" - S&P Global: "China Banks Outlook Series" - UBS: "Chinese Financial Sector Analysis" - Morgan Stanley: "Asia Pacific Banks Research"

Historical Context: - "Deng Xiaoping and the Transformation of China" by Ezra Vogel - "The Shenzhen Experiment" by Juan Du - "China Merchants Group: 150 Years of History"

These resources provide the foundation for understanding not just CMB's specific journey but the broader transformation of Chinese finance from a state-controlled system to a increasingly market-oriented one, albeit with Chinese characteristics. The bank's story cannot be separated from China's economic miracle, and these materials help illuminate both the micro and macro narratives that shaped modern Chinese banking.

The transformation narrative took another dramatic turn in 2024 when CMB announced its evolution from "retail bank" to "value bank." Chairman Miao Jianmin described this strategic shift with initiatives designed to strengthen management, accelerate innovation, and improve both wealth management and fintech risk management. This wasn't merely rebranding—it represented a fundamental reimagining of the bank's role in China's evolving financial ecosystem.

The numbers validate this strategic pivot. The number of retail customers surpassed 200 million and the total assets under management (AUM) from retail customers approached RMB15 trillion. The number of customers holding retail wealth management products exceeded 58 million, and the number of retail clients covered by the "CMB TREE Asset Allocation Service System" exceeded 10 million. These weren't just account openings—they represented deep, multi-product relationships generating sustainable fee income.

Technology investment intensified as competition from fintech giants evolved from disruption to collaboration. Focusing on the goal of online, data-based, intelligent, platform-based and ecological operation, CMB continued to develop a digital and intelligent foundation based on "cloud + AI + middle platform". With "AI + Finance" as the key focus, CMB promoted innovation in products, services, businesses, models, and management by technological innovation, accelerating the transition from an "Online CMB" to a "Digital & Intelligent CMB".

The bank's digital infrastructure proved particularly valuable in serving corporate clients. As CMB's adoption of cloud native technologies, the Kubernetes container platform is now supporting 100k+ applications in CMB. CMB built its new generation load balancer platform with BFE, achieving traffic balancing and failure resilience between multiple private clouds and Kubernetes clusters. With BFE's multi-tenancy model and RESTful APIs, it is easy to integrate BFE into cloud management platform(CMP) of CMB and achieve self-serviced, automated application publish.

International recognition followed domestic success. In 2024, CMB ranked 10th in terms of Tier 1 capital on the list of "Top 1,000 World Banks" released by The Banker (UK), and 10th on the list of "Top 500 Banking Brands" released by Brand Finance. CMB's MSCI ESG rating was "AAA", securing a leading position among global peers. CMB was awarded "Best Digital Bank" in China by Euromoney.

The latest financial results demonstrate remarkable resilience despite economic headwinds. Net operating income was RMB337.5 billion, ranking 6th in the industry, and net profit attributable to the Bank's shareholders was RMB148.4 billion, ranking 5th in the industry. As at the end of 2024, CMB's total assets exceeded RMB12 trillion, ranking 7th in domestic banking industry. The return on average assets (ROAA) and the return on average equity (ROAE) were 1.28% and 14.49% respectively, both ranking 1st among large- and medium-sized listed banks in domestic market.

Wealth management emerges as the crown jewel of CMB's transformation. The bank's partnership with international asset managers demonstrates its sophisticated approach. Since its founding in 1987, China Merchants Bank (CMB) has quickly emerged as one of the top 20 world banks by Tier 1 capital. Believing innovation will help attract fund flows and improve efficiency, CMB decided to expand its focus on fintech and distribute asset management products via its online platform to provide an end-to-end digital client experience. As CMB began to implement digitization with international asset managers, it was clear from experience with domestic partners that the speed, efficiency and customization of Application Programing Interface (API) trading, compared to traditional trading transmission, was essential to enhancing CMB's capabilities.

The broader Chinese wealth management market provides tailwinds for CMB's strategy. By the end of last year, the number of investors holding wealth management products in the banking market rose 9.88 percent year-on-year to 125 million. The balance of wealth management products stood at 29.95 trillion yuan ($4.17 trillion) at the end of 2024 -- up 11.75 percent compared with the value at the beginning of last year. 30,800 wealth management products were launched by a combination of 179 banking institutions and 31 wealth management companies in China's banking system last year, raising a total of 67.31 trillion yuan.

CMB's focus on the "five major articles" reflects alignment with national priorities while maintaining commercial discipline. CMB accelerated the campaign to build distinctive financial services centering the "five major articles", namely technology finance, green finance, inclusive finance, retirement finance and digital finance, realizing rapid loan growth in corresponding fields. This strategic alignment positions CMB to benefit from policy support while maintaining its independence.

The subsidiary ecosystem amplifies CMB's competitive advantages. Its subsidiaries, such as CMB Wealth Management, China Merchants Fund, CMB Financial Leasing and Merchants Union Consumer Finance, ranked among the top in their respective sectors, with their market influence steadily rising. CMB Group's flywheel effect was further amplified. Each subsidiary reinforces the parent bank's capabilities while expanding the addressable market.

Looking forward, CMB faces a complex operating environment requiring continued adaptation. Property sector challenges persist, though the bank maintains industry-leading asset quality. Regulatory evolution continues as Beijing balances financial innovation with systemic stability. International expansion faces geopolitical headwinds requiring careful navigation.

Yet CMB's track record suggests continued resilience. The bank that began as an experiment in market-oriented finance has proven its ability to adapt, innovate, and thrive through multiple economic cycles. As China's financial system continues evolving, CMB remains positioned as both beneficiary and catalyst of change.

The transformation from regional upstart to national champion to global player represents more than corporate success—it demonstrates the power of strategic focus, operational excellence, and cultural differentiation in building enduring competitive advantages. CMB's journey proves that in banking, as in life, success comes not from following the crowd but from charting your own course.

For investors evaluating CMB today, the calculus involves balancing structural advantages against cyclical challenges. The retail franchise generates predictable returns. The wealth management platform captures secular growth. The technology infrastructure enables continued innovation. Against these strengths stand property exposure, margin pressure, and regulatory uncertainty.

The ultimate question isn't whether CMB will survive current challenges—its track record suggests it will. The question is whether it can maintain its innovation edge as the Chinese banking system matures and competition intensifies. History suggests betting against CMB's ability to adapt would be unwise.

As we conclude this exploration of China Merchants Bank's remarkable journey, several themes emerge with crystal clarity. First, competitive advantages in regulated markets prove remarkably durable when built on customer relationships rather than regulatory privilege. Second, technology transformation succeeds when it changes culture, not just systems. Third, navigating between commercial and political imperatives, while challenging, creates unique opportunities for those who master the balance.

CMB's story continues unfolding, with new chapters being written in artificial intelligence, green finance, and cross-border connectivity. The bank that started with 30 employees in a Shenzhen office building now shapes the future of Chinese finance. Its journey from experiment to exemplar offers timeless lessons about innovation, adaptation, and the courage to be different in industries that reward conformity.

For those seeking to understand China's economic transformation, CMB provides an illuminating case study. For investors evaluating opportunities in Chinese finance, it offers a masterclass in building sustainable competitive advantages. For business leaders navigating disruption, it demonstrates the power of strategic focus and operational excellence.

The story of China Merchants Bank ultimately transcends banking. It's a story about vision triumphing over resources, innovation defeating inertia, and merit succeeding despite systemic disadvantages. In an industry where size traditionally determines success, CMB proved that strategy, execution, and culture matter more. That lesson, perhaps more than any financial metric, explains why this experimental bank from Shenzhen became the champion of Chinese finance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube