Zhuzhou CRRC Times Electric: The Heart and Brain of China's High-Speed Rail and the Rise of Its Silicon Empire

I. Introduction & Episode Roadmap

Picture the cab of a CR400 "Fuxing" bullet train slicing across the North China Plain at 350 kilometres per hour. The driver's hands rest lightly on the controls; the real work is happening in steel cabinets bolted beneath the floor, where electricity pulled from a 25,000-volt overhead wire is being chopped, inverted, and metered into the traction motors thousands of times per second. The brain doing that metering — the converters, the inverters, the silicon switches at the centre of it all — was very likely designed and built in a single industrial city in central China's Hunan province: Zhuzhou.

Here is the puzzle this story turns on. Over the last two decades, most Western industrial champions in power electronics either got disintermediated by software or quietly outsourced their fabrication to Asia and became designers of things other people built. 中车时代电气 CRRC Times Electric (3898.HK / 688187.SH) went the opposite direction. It doubled down on heavy hardware physics. It bought a struggling, almost forgotten UK semiconductor pioneer for the price of a nice London flat in the middle of the 2008 financial crisis, transferred the know-how home, and used it to build what is today, by installation volume, the second-largest automotive power-module supplier in China — behind only 比亚迪 BYD.1

How does a state-owned enterprise in a train-manufacturing town evolve from a components workshop into a company that controls well over half of China's domestic rail traction market and then leverages that captive cash machine into a multi-billion-renminbi merchant semiconductor business? And — the question a sceptical investor should keep asking throughout — is the second act real, durable engineering advantage, or is it a state-directed capacity build that the market is right to discount?

Here is the roadmap. We start with the Soviet-era research institute that seeded the whole thing. We dig into the physics and unit economics of train traction — the boring, beautiful cash cow. We tell the story of the 2008 Dynex deal, arguably one of the most efficient technology acquisitions in modern Chinese corporate history, and then the 2015 SMD deal, which is the cautionary footnote to it. We follow the 2021 STAR Market listing that raised the war chest for the fabs. Then we size the silicon empire as it stands in 2026, examine how an SOE motivates managers who own no stock, and finish by stress-testing the bull case against related-party dependence, the conglomerate discount, and a maturing domestic rail network. Let's begin where everything in Zhuzhou begins — with a railway institute.

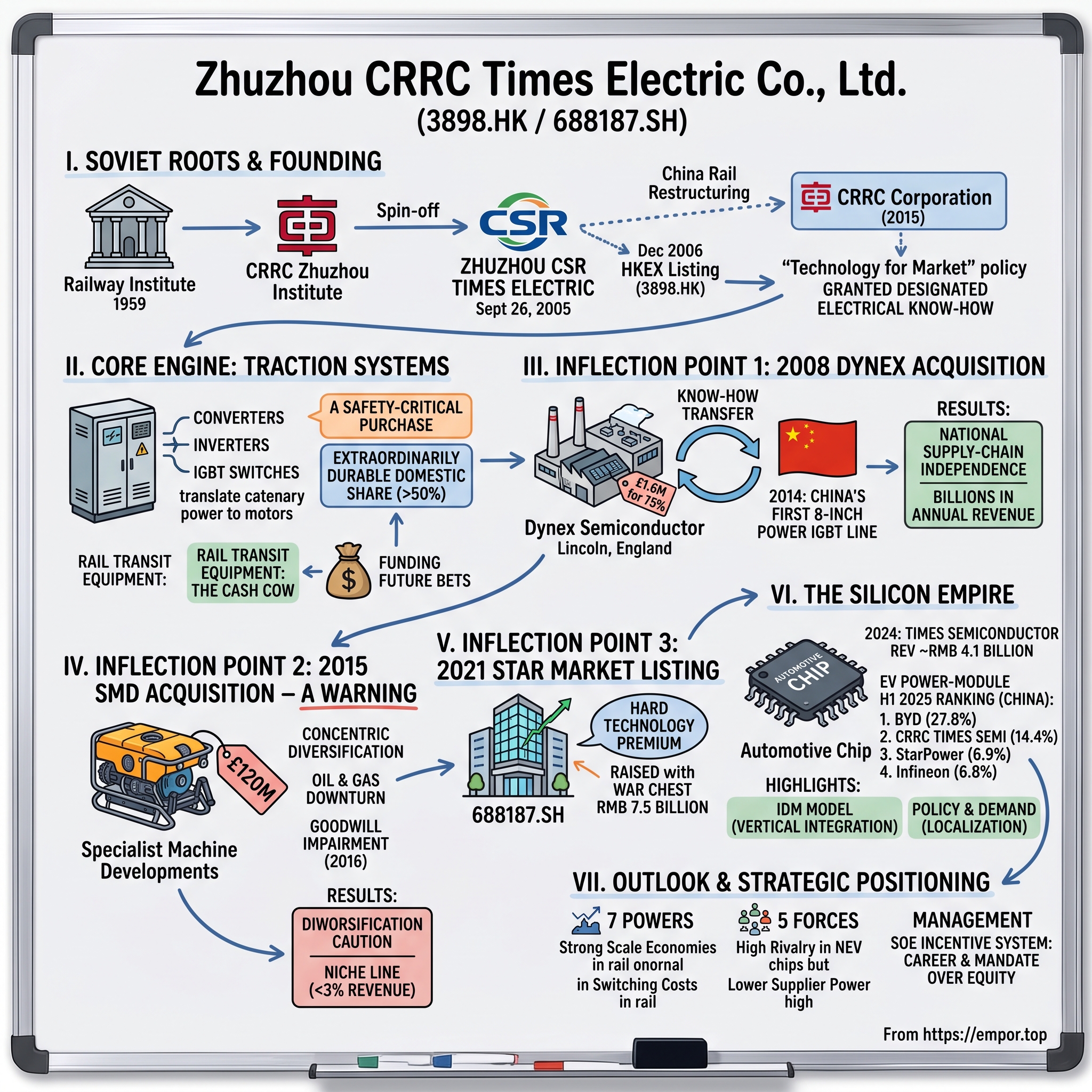

II. From Soviet Rails to National Champion: The Founding Story

In 1959, when much of China was reeling from famine and political upheaval, the Ministry of Railways did something that would echo for the next seven decades: it planted a research institute in Zhuzhou dedicated to a single, almost futuristic idea for the time — the electrification of China's railways. The 株洲电力机车研究所 Zhuzhou Electric Locomotive Research Institute, eventually known as 株洲所 CRRC Zhuzhou Institute, was the kind of place where engineers in padded jackets pored over Soviet schematics under bare bulbs, trying to understand how to make a locomotive run on electricity drawn from a wire rather than coal shovelled into a firebox.2

That distinction matters more than it sounds. A diesel or steam locomotive is fundamentally a mechanical machine. An electric locomotive is fundamentally a power-electronics machine — it is a giant, mobile substation on wheels. The institute that mastered the electrical "guts" of trains was, without quite knowing it, positioning itself at the exact spot where the future value of the industry would concentrate. The steel shell of a railcar is a commodity. The traction system that turns voltage into motion is not.

For decades the institute did unglamorous, vital work inside a planned economy. The pivot to a recognisable modern company came with the great restructuring of Chinese rail. In the late 1990s and early 2000s, Beijing split its sprawling locomotive industry into two competing giants — CSR (China South Locomotive & Rolling Stock) and CNR (China North Locomotive & Rolling Stock) — deliberately pitting north against south to force efficiency. The high-tech electrical brains of CSR's locomotives were carved out and incorporated as Zhuzhou CSR Times Electric on September 26, 2005, which then listed on the Hong Kong Stock Exchange in December 2006 under the ticker 3898.HK.3 The "Electric" in the name was the whole point: this was the company that held the converters, the control systems, the signalling — not the bogies and carriages.

Then came the move that defined the modern competitive landscape. In 2015, the Chinese state reversed its own logic and ordered CSR and CNR to merge back together into a single colossus, 中国中车 CRRC Corporation — the largest rolling-stock manufacturer on earth.4 The north-south rivalry that had driven a decade of improvement was switched off in favour of consolidated scale and a unified front for exports. Inside that merged empire, Times Electric became the technology crown jewel: the supplier of the one component category that is genuinely hard to replicate.

To understand why Times Electric ended up holding such valuable cards, you have to understand the industrial policy that built the high-speed network. China ran what it openly called a "technology for market" bargain. Global titans — 阿尔斯通 Alstom, 西门子 Siemens, Bombardier, Japan's Kawasaki — were told they could sell into the largest railway build-out in human history, but only if they transferred core technology to designated domestic partners and manufactured locally.5 The foreign firms, dazzled by the order book, largely agreed, calculating they could stay ahead on the next generation. They mostly could not. And among the designated recipients of the critical electrical know-how — the traction and control systems — was Times Electric. The foreigners handed over the blueprints to the heart and brain of the train, kept the lower-value assembly, and within a decade found themselves competing against a vertically integrated Chinese champion in third markets.

For an investor, the founding story carries one durable lesson: this company did not earn its position by inventing the category. It inherited a privileged seat — a state-anointed monopoly on the highest-value part of a strategic industry — and the real question for the rest of this story is whether it has turned that inherited advantage into something it can defend on open ground, outside the protected rail network. To judge that, we first have to understand exactly what the core machine does and why it prints cash.

III. The Core Engine: The Physics and Economics of Traction Systems

Strip away the marketing and a high-speed train is a deceptively simple energy problem. Up on the catenary wire hangs alternating current at roughly 25,000 volts — wildly too much voltage, in the wrong form, to feed directly into a motor. The job of the traction system is to take that raw firehose of electricity and tame it: step it down, convert it from alternating to direct current and back again, and precisely control the frequency and voltage delivered to the wheels so the train accelerates smoothly from a standstill to 350 km/h and brakes without throwing passengers from their seats.

Think of it as a translator and a throttle rolled into one. The converter turns the incoming AC into a stable pool of DC — the equivalent of filling a reservoir. The inverter then draws from that reservoir and synthesises a brand-new AC waveform, at exactly the frequency the motor needs at that instant, by switching the current on and off thousands of times a second. The components doing that switching are power semiconductors — the silicon valves we will spend most of this story on. Get the switching even slightly wrong and you either melt the electronics or jerk the train. The whole assembly is what the company calls its traction propulsion system, and it is, almost literally, the heart (the converter/inverter) and the brain (the control electronics) of the train.

Sitting alongside it is the nervous system: signalling. Times Electric supplies communications-based train control, the systems that keep trains a safe distance apart and let metro lines run trains every ninety seconds without collisions. This is software and communications wrapped around the same safety-critical discipline.

Now the economics, which are the genuinely attractive part. Rail Transit Equipment remained the company's cornerstone in 2024, generating roughly RMB 14.6 billion of its RMB 24.9 billion in total revenue — close to 59% of the business.6 Within urban metros, the company has held a dominant domestic share of its core traction-systems market — above 50% — for well over a decade, an extraordinarily durable position.7

Why is that share so sticky? Because nobody buys train brakes on price. A metro operator running a line under a major city is making a safety-critical purchase where the cost of failure is measured in human lives and front-page disasters, not in basis points of margin. Winning a traction tender requires years of demonstrated fault-free operation in the field — a track record a new entrant simply cannot fake or buy. The certification barrier is the moat, and it compounds: every additional fleet-year of flawless running makes the incumbent harder to dislodge. The result is a business with high switching costs, predictable multi-year order visibility, and the kind of stable operating margins that let management treat the rail division as a reliable cash engine — one that can quietly fund capital-hungry bets elsewhere.

And that is precisely what management did. The genius — or the gamble, depending on your view — of Times Electric is that it took the dependable cash thrown off by a protected railway monopoly and pointed it at one of the most competitive, capital-intensive industries on the planet: semiconductors. The story of how that began is a story about a tiny, almost invisible acquisition in a Lincolnshire town in the autumn of 2008.

IV. Inflection Point 1: The 2008 Dynex Masterstroke

By the mid-2000s, China could build the physical train — the steel, the bogies, the assembly. But there was a humiliating dependency hiding inside every locomotive. The high-power switches that do the actual work of converting energy — the IGBTs, or insulated-gate bipolar transistors — were imported, essentially 100%, from a handful of foreign monopolies: Germany's 英飞凌 Infineon, Japan's Mitsubishi and Fuji. An IGBT is best understood as an extraordinarily fast, extraordinarily tough electronic switch that can handle thousands of volts and switch tens of thousands of times a second without wearing out. It is the single most critical component in the traction chain, and China made none of its own at the required voltage class. For a government that viewed the railway as strategic infrastructure, depending entirely on Germany and Japan for the one irreplaceable part was an unacceptable vulnerability.

The solution arrived from an unlikely place: Lincoln, England. There sat Dynex Semiconductor, a power-device maker with a real fabrication line and decades of high-voltage know-how, but a tiny market capitalisation and a parent, the TSX-listed Dynex Power Inc., that was struggling to fund itself. Dynex was the kind of overlooked specialist that does world-class work in a niche too small for the giants to bother crushing.

In October 2008 — with the global financial system in freefall and asset prices collapsing — CRRC's predecessor stepped in and acquired a 75% stake in Dynex. The price was almost comically small for what it bought: on the order of £1.6 million in fresh equity.8 For roughly the cost of a few flats in Kensington, a Chinese state enterprise had just bought a controlling interest in a fully operational Western high-voltage semiconductor business, with its fab, its patents, and — most importantly — its people.

What happened next is the part worth studying, because it is the opposite of the asset-stripping playbook foreigners often expected from Chinese acquirers. CRRC kept the Lincoln R&D centre open and running. It embedded its own Zhuzhou engineers inside Dynex for extended stretches, where they absorbed the fabrication blueprints, the process recipes, the hard-won tacit knowledge that never appears in a patent filing. Dynex management, in turn, played a central role in helping stand up manufacturing back in China.9 Then, in 2014, using exactly this transferred expertise, the company commissioned China's first 8-inch high-power IGBT chip production line in Zhuzhou — a milestone that, at a stroke, gave the national railway a domestic source for its most critical component.10 In 2019 CRRC Times Electric mopped up the rest of Dynex it did not already own, taking it fully private.11

Step back and weigh the capital efficiency, because this is the heart of the section. A total outlay that, even generously counted across the original stake and the later buyout, ran to the low tens of millions of dollars, seeded a business segment that now generates billions of renminbi in annual revenue and — far harder to value — delivered national supply-chain independence in a strategically vital technology. Measured purely as a return on invested capital, Dynex belongs in the conversation with the most lucrative technology acquisitions any company has ever made.

But a sceptic should hold two caveats. First, the deal's success depended on a willing, distressed seller and an open transfer of know-how that would be far harder to replicate in today's climate of tightened export controls and foreign-investment screening — this was a product of its specific historical moment. Second, buying a fab and a patent stack does not automatically confer a durable competitive edge; what mattered was the decade of subsequent investment and execution that turned a Lincolnshire process into a high-volume Chinese one. Dynex was the spark, not the engine. The lesson of capital discipline it seemed to teach, though, was about to be tested by a far less happy acquisition.

V. Inflection Point 2: The 2015 SMD Acquisition – A Capital Allocation Warning

Success is a dangerous teacher. By 2015, flush with cash from the railway boom and intoxicated by the Dynex story, Times Electric went looking for its next overseas home run. It found a British company — and this time it paid up.

The target was Specialist Machine Developments, better known as SMD, a Newcastle-area maker of deep-sea remotely operated vehicles and seabed trenching machines — the robotic submersibles that lay and bury subsea cables and pipelines and crawl the ocean floor for oil-and-gas infrastructure. Times Electric completed the acquisition in April 2015 for around £120 million, roughly RMB 1.1 billion at the time — nearly two orders of magnitude more than it had paid for Dynex.12

The strategic thesis sounded plausible in a PowerPoint. SMD's underwater vehicles are, at their core, electrically powered, motion-controlled machines. Times Electric was a master of traction and power conversion. Surely the company's expertise in driving electric motors and converting power could be transplanted from the railway to the seabed? Concentric diversification — expand into an adjacent field that shares your core competence — is a respectable idea in the strategy textbooks.

Reality was less accommodating. The synergy between locomotive traction and subsea robotics turned out to be abstract to the point of theoretical; the engineering disciplines, customers, and sales channels barely overlapped. Worse, the timing was brutal. The subsea oil-and-gas market, SMD's bread and butter, entered a structural downturn almost immediately as the 2014–2016 oil-price collapse gutted offshore capital spending. A business bought at the top of a cycle was suddenly staring at a market that had fallen off a cliff. By 2016 the company was already taking goodwill impairment charges on the SMD acquisition, a public admission that it had paid more than the business was worth.13

Today, the marine engineering business is a rounding error. It sits inside the Emerging Equipment segment as a niche line — on the order of RMB 0.5 billion of revenue, comfortably under 3% of the group's 2024 total.14 It survives; it does not move the needle.

For investors, SMD is the essential counterweight to the Dynex legend, and the two should always be read together. The same management instinct — buy a distressed Western specialist and absorb its technology — produced one of the great bargains and one of the clearer value-destroyers within seven years of each other. The difference was not the playbook but the fit and the price: Dynex sat dead-centre in the company's core technology and was bought for a pittance in a buyer's market; SMD sat at the speculative edge and was bought near a cyclical peak. The episode is a useful, permanent reminder that this management team is capable of the diversification overreach that the strategy literature politely calls "diworsification," and that its capital-allocation record is good on average precisely because one enormous win offsets the misses. Chastened, the company refocused on what it understood. The next big move would not be an acquisition at all — it would be a trip to the capital markets.

VI. Inflection Point 3: The 2021 STAR Market Catalyst

Why would a profitable, cash-generative company already listed in Hong Kong bother to list a second time at home? The answer is that fabs are voracious, and Hong Kong investors were not paying the right price for the dream.

In September 2021, Times Electric completed a second listing — this time on the Shanghai Stock Exchange's 科创板 STAR Market, China's Nasdaq-style board for "hard technology" companies, under the ticker 688187.SH.15 The STAR Market exists precisely to channel domestic capital into strategic technology, and it rewards semiconductor and deep-tech stories with valuations that Hong Kong's more sceptical, internationally minded investors rarely extend to a state-owned railway supplier. For a company trying to fund a capital-intensive pivot into chips, listing where the chip premium lives was simple financial logic.

The raise was substantial: net proceeds on the order of RMB 7.5 billion.16 That is real money even for a company of this size, and crucially it was equity, not debt — the right instrument for funding multi-year fab construction whose payback lies far in the future.

Where did it go? The proceeds were earmarked for the next leg of the silicon build-out: expanding silicon IGBT wafer capacity and, more strategically, funding silicon carbide. Silicon carbide, or SiC, is the next-generation material that lets power devices run hotter, faster, and more efficiently than ordinary silicon — the enabling technology for the 800-volt electric-vehicle architectures now coming to market. By tapping the STAR Market, Times Electric was explicitly recasting itself: no longer a niche supplier making chips for its own trains, but a merchant foundry intending to sell power semiconductors to the entire EV and renewable-energy industry. Whether that ambition has translated into a genuinely competitive merchant business — rather than a state-funded capacity bet chasing a crowded market — is the question the next section confronts head-on.

VII. The Silicon Empire: Merchants, EV Fabs, & Market Disruption

For years, the power-semiconductor operation was treated as a curiosity bolted onto a railway company — interesting, strategically tidy, financially immaterial. That framing is now obsolete. In 2024, the power semiconductor business, 时代半导体 Times Semiconductor, generated roughly RMB 4.1 billion in revenue, growing in the double digits year on year.17 It is no longer a novelty; it is a genuine growth engine and, for many investors, the entire reason to look at the stock.

The clearest proof point came in the EV power-module battleground in the first half of 2025. China publishes detailed installation rankings for the power-semiconductor modules that sit at the heart of every electric car's drivetrain, and the H1 2025 table told a striking story. CRRC Times Semiconductor ranked second in the entire Chinese market, with a 14.4% share on roughly 903,000 module sets installed. Ahead of it sat only BYD, the vertically integrated EV giant, at 27.8%. Behind it — and this is the headline — trailed StarPower at 6.9% and the mighty Infineon at 6.8%.18 A company most Western investors have never heard of was shipping more than twice as many automotive power modules in China as the German firm that practically invented the category.

Why is Times Electric winning here, in an open, brutally competitive market with no railway certification moat to hide behind? The honest answer is a mix of genuine structural advantage and Chinese market dynamics, and an investor should separate the two.

The structural advantage is the IDM model — integrated device manufacturer. Unlike a fabless chip-design house that outsources manufacturing to a foundry like TSMC, Times Electric owns and runs its own fabrication lines. It designs the chip, makes the wafer, and packages the module under one roof. In power electronics, where the module's performance depends on tightly co-optimising the silicon, the packaging, and the thermal design, that vertical integration is a real edge: it compresses cost and lets the company tune the whole stack rather than buying a generic chip off a foundry menu. Management's argument is that owning the fab meaningfully lowers module cost versus fabless competitors. That is directionally credible — controlling the wafer does remove a layer of margin and a layer of coordination friction — though the precise cost gap is a company claim, not an audited fact, and it narrows when a fabless rival has scale a captive fab cannot match.

The second, less-advertised driver is policy and demand. Chinese EV makers have strong incentives — supply security, cost, and political tailwinds toward domestic substitution — to design out Infineon and design in a local champion. The H1 2025 rankings showed seven of the top suppliers were Chinese, collectively taking over 65% of the market.19 Times Electric is riding a powerful localisation wave, and a sceptic should ask how much of its share is engineering merit versus a captive domestic market that would prefer not to buy German.

Where the company's moat is least contestable is at the very top of the voltage range. Times Electric dominates ultra-high-voltage IGBTs — the 3,300V to 6,500V class used in bullet trains and in the 国家电网 State Grid's ultra-high-voltage DC transmission lines that wheel power across the breadth of China. This is a small, fiendishly difficult, high-margin niche with essentially no domestic competitor and only a couple of foreign ones — the natural extension of the railway heritage into the grid.

The frontier now is silicon carbide. As Chinese EVs migrate to 800V platforms, SiC becomes the material of choice, and Times Electric is scaling its Zhuzhou SiC lines to compete directly with STMicroelectronics and Infineon on this next-generation battlefield. SiC is where the established Western players are strongest and where the company is least proven; it is the truest test of whether the silicon empire is a durable engineering franchise or a well-funded fast-follower. The answer will not be clear for several years. In the meantime, the more immediate question for any investor in a state-owned enterprise is who is actually running this, and what makes them get out of bed in the morning.

VIII. Management & Incentives: The SOE Playbook

Here is where a Western investor's instincts can lead them badly astray. There is no charismatic founder in this story holding 20% of the equity, no Jensen Huang in a leather jacket whose net worth rises and falls with the stock. This is a state-owned enterprise, and its leadership operates inside a logic that looks alien from a Silicon Valley vantage point.

Consider the top team as it stands in 2026. The chairman is 李东林 Li Donglin, a lifelong railway man who has held the chair since 2018 and was re-elected to the eighth board session in 2026 — an engineer's engineer who came up through the industry rather than parachuting in from finance.20 尚敬 Shang Jing, long the company's general manager, stepped up to vice chairman in 2026. The day-to-day presidency — the general manager role — passed to 徐绍龙 Xu Shaolong, appointed in mid-2024 in a structured, telegraphed succession rather than an abrupt shake-up.21

Now the part that genuinely puzzles outsiders. None of these key executives holds any meaningful direct equity stake in the listed company. Their salaries paid by the listed entity are, by global standards for a business of this scale and technological complexity, strikingly modest — the kind of figures, in the low-to-mid hundreds of thousands of renminbi, that a mid-level engineer at a Western chipmaker would consider underwhelming, with the remainder of their compensation flowing through the parent group.22 There are no nine-figure option packages here. So the obvious question is: if they own no stock and earn modest pay, what on earth motivates them to run a hard-charging semiconductor business well?

The answer is the SOE incentive system, which substitutes career and mandate for equity. These managers are evaluated against national strategic key performance indicators — supply-chain security in critical technologies, R&D breakthroughs, returns on net assets — and their reward is advancement within the vast hierarchy of CRRC and ultimately the 国资委 SASAC, the state body that owns and supervises China's central SOEs. Success means promotion to ever-larger platforms of responsibility and influence; failure means stagnation. It is a tournament for status and power inside the state apparatus, not a lottery ticket on a share price.

For an investor, this cuts both ways, and honesty requires holding both halves. On the positive side, the incentive to chase national-priority technology breakthroughs aligns management's interests reasonably well with the long-term, patient, capital-intensive bet on semiconductors — there is no pressure to strip-mine the business for a quarterly share-price pop, and the disciplined refocusing after the SMD misadventure suggests a team that learns. The structured 2024 general-manager handover and the steady execution of the STAR Market expansion are points in the management's credibility column.

On the negative side, the same system means minority public shareholders are simply not the constituency management primarily answers to. When national strategic objectives and minority-shareholder returns diverge — over, say, pricing to related parties, or the willingness to chase low-margin volume to support domestic substitution — there is little reason to expect the public float to win the argument. The absence of equity alignment is not a scandal; it is a structural feature investors must price. And nowhere does that tension surface more sharply than in the company's web of transactions with its own parent.

IX. Activist/Skeptical Investor Stress Test

Let's now put on the short-seller's hat, because a serious investor should be able to argue the bear case better than the bulls. Three things should worry you.

Start with the related-party question, the single most uncomfortable fact in the financials. In 2024, Times Electric derived a large slice of its revenue — on the order of 37%, well over RMB 9 billion — from selling to other entities inside the CRRC Group, principally the parent's locomotive-assembly businesses that buy its traction systems.23 An activist would frame this bluntly: how much of this "business" is a genuine arm's-length market, and how much is simply CRRC moving money from one of its pockets to another, with the listed company functioning as an internal supplier whose prices the parent effectively sets? If the parent controls both the customer and the supplier, transfer pricing becomes a lever — and the lever can be pulled in whichever direction suits the group rather than the minority holders of 3898.HK and 688187.SH. The risk is not theoretical; it is structural to any partially listed SOE subsidiary.

The company's defence is procedural. These sales are governed by formal "mutual supply framework agreements," renewed in multi-year cycles (the current cycle covering 2026–2028) and subject to price caps, independent non-executive director oversight, and shareholder approval of the caps.24 That governance is real and is more than many SOEs offer. But a sceptic will note that a price cap negotiated between a parent and the subsidiary it controls is not the same as a price discovered in open competition, and independent directors on an SOE board operate within obvious limits. The honest verdict: the framework reduces the most egregious abuse, but it cannot eliminate the underlying conflict, and the dependence on captive intra-group demand is a genuine quality-of-earnings discount that the rail segment's lovely margins should be read against.

The second bear argument is the conglomerate discount, and here the activist actually has a constructive demand. Inside one listed wrapper sit two utterly different businesses. One is a mature, slow-growing, monopoly-like rail-equipment cash cow — the kind of asset that, on its own, the market values at a single-digit-to-low-teens earnings multiple. The other is a fast-growing, world-relevant EV-and-grid power-semiconductor business — the kind of asset that, listed independently, might command a multiple several times higher. Bolted together, the whole trades closer to the boring multiple than the exciting one. The high-growth jewel is, in effect, trapped inside a low-multiple SOE shell, and its value is partly masked.

The obvious activist move is to demand a spin-off: carve 时代半导体 Times Semiconductor out as a standalone listed entity and let the market re-rate it on its own merits. It is a clean value-unlock thesis. And it is almost certainly going nowhere — which is itself the point. Power semiconductors are strategically inseparable from the railway supply chain the state is determined to keep sovereign; Beijing is highly unlikely to relinquish control of, or fully decouple, the chip business from the integrated whole. The very thing that makes the semiconductor business strategically protected — its national-security salience — is the thing that keeps it locked inside the lower-multiple structure. An investor cannot wish that contradiction away; they can only decide what discount it warrants.

The third worry is simpler: a business this entangled with the state and this dependent on policy-driven domestic substitution is, by construction, exposed to political and geopolitical winds it does not control — which brings us to how the competitive position actually stacks up, and then to the concrete risks.

X. Strategic Positioning: Powers & Forces

Run the company through Hamilton Helmer's 7 Powers and a clear, asymmetric picture emerges — strong moats in rail, thinner ones in chips.

Scale economies are the most dominant power, and they operate in both halves of the business. Train manufacturing and semiconductor fabrication are both ferociously capital-intensive, with enormous fixed costs that must be spread across volume. As the largest domestic player by a wide margin, Times Electric spreads those costs across a volume no domestic rival can match, yielding a structural unit-cost advantage. In rail it is close to absolute; in semiconductors it is real but contested by larger global players.

Switching costs are the second genuine power, and they are highest exactly where the company is strongest — rail. Once a traction or signalling system is designed into a fleet and certified through years of safe operation, ripping it out to save a few percent is unthinkable; the incumbent is locked in for the life of the asset and often the next procurement cycle too. In automotive semiconductors switching costs exist but are far lower — an EV maker can and does dual-source modules.

Cornered resource is moderate and rooted in the Dynex inheritance: the accumulated high-voltage process know-how and the physical fabs, especially at the ultra-high-voltage end where genuine alternatives are scarce. It is a real but narrowing edge, because process knowledge diffuses and competitors invest.

Counter-positioning — the power that comes from a business model incumbents cannot copy without harming themselves — is essentially absent. The IDM model is the oldest model in semiconductors, not a disruptive reinvention. Times Electric wins on scale, integration, and policy tailwinds, not on a structurally novel approach that pins its rivals. Investors should not mistake it for a disruptor; it is a heavyweight incumbent on its home turf.

Now Porter's Five Forces, segment by segment, because the two businesses live in opposite worlds. Competitive rivalry is low in rail — a domestic monopoly-to-duopoly with the parent's blessing — and high in NEV semiconductors, where it slugs it out with BYD, StarPower, Silan, and the global incumbents in a market with brutal price competition. Supplier power over Times Electric is low, by design: vertical integration as an IDM means it makes its own most critical inputs rather than depending on a merchant chip supplier — the entire strategic point of the Dynex deal. Buyer power is high in both segments but for different reasons: in rail the buyer is effectively the state and the parent; in autos the buyers are large, sophisticated OEMs running aggressive cost-down programmes. In both cases buyer power is partly blunted by how critical and hard-to-qualify the components are — but "partly" is the operative word, especially as automakers vertically integrate their own power electronics. The net read: a fortress in rail, a competent and rising challenger in chips, but not an unassailable one. That competitive reality sets up the specific risks worth watching.

XI. Risk Radar & Key KPIs to Track

Three risks are material enough to dwell on; the rest is noise.

Risk one is geopolitical equipment access. Here is the uncomfortable irony at the centre of the silicon story. A company whose founding semiconductor logic was reducing dependence on foreign technology remains, at the manufacturing layer, dependent on foreign technology — specifically the Dutch, Japanese, and American photolithography and wafer-processing equipment needed to build and expand fabs. Every announced capacity expansion, every new SiC line, implicitly assumes continued access to imported tools. A tightening of export controls aimed at China's semiconductor sector could slow or freeze that expansion regardless of how strong demand is. This is the single risk most outside the company's control, and it sits directly on top of its primary growth engine.

Risk two is the EV price war. China's domestic NEV market is in the middle of a savage, multi-year price war, and the pain flows straight down to tier-one component suppliers. Automakers demanding double-digit annual cost reductions will squeeze power-module margins, and the more Times Electric leans into automotive volume to grow, the more it risks diluting the lovely, stable margins of its rail cash cow with thin, hard-fought automotive economics. Growth in the chip business is not automatically accretive to group profitability — a point easily lost when celebrating market-share rankings.

Risk three is railway saturation. China's high-speed network, the greatest infrastructure build-out in history, is maturing. The era of laying vast quantities of new track is giving way to a future built on replacement cycles, signalling upgrades, and the much harder, riskier work of winning export orders abroad against entrenched and politically wary foreign incumbents. The rail cash cow is not shrinking, but its growth is structurally decelerating, which raises the stakes on the emerging-equipment pivot succeeding.

Given all that, an investor tracking this company quarter to quarter should ignore most of the noise and watch three things:

First, Emerging Equipment revenue growth — the single clearest gauge of whether the semiconductor-led second act is genuinely outrunning the maturing rail core, or merely treading water. Second, the gross margin of the semiconductor segment specifically — the real-time test of whether vertical integration is holding the line against the EV price war, or whether share is being bought with margin. Third, utilisation of the new silicon and SiC capacity funded by the 2021 raise — because billions in fab investment only create value if the lines run full; underutilised fabs are where capital-intensive dreams go to destroy returns. Those three numbers, watched over time, will tell the story more honestly than any management presentation.

XII. Epilogue & Outro

The enduring lesson of Zhuzhou CRRC Times Electric is how a state-owned enterprise, of all things, pulled off a technological leapfrog not through a grand organic research programme or a flashy mega-merger, but through a micro-acquisition almost no one noticed at the time — a few million pounds for a struggling fab in Lincoln, executed with patience and an unglamorous commitment to absorbing know-how rather than stripping assets. The Dynex deal is the kind of capital-allocation story business-school cases are built around. The SMD deal is the chastening reminder, filed right next to it, that the same instinct misapplied destroys value.

What sits in front of investors today is an unusual hybrid: a dependable, high-share, utility-like rail-transit business whose certification moat and switching costs throw off steady cash, strapped to a high-beta, genuinely globally relevant power-semiconductor venture with a real engineering edge at the high-voltage end and a fiercely contested, policy-aided position in automotive. The bull case is that the cash cow funds a chip champion the market is undervaluing inside an SOE wrapper. The bear case is that related-party dependence, the conglomerate discount, equipment-import vulnerability, and the EV margin war are all real, all structural, and all reasons the discount exists for a reason.

In the end, CRRC Times Electric is perhaps the clearest single illustration of the modern Chinese state-capitalism model functioning at its most effective: strategic in intent, patient with capital, vertically integrated by design, and relentlessly focused on technological sovereignty — with the corollary, never to be forgotten, that the public minority shareholder is a passenger on that train, not the one holding the throttle.

References

-

Rankings of electrification component suppliers in China (H1 2025) — Gasgoo, 2025 ↩

-

Case Studies in PRC Foreign Tech Transfers: CRRC Acquisition of Dynex Semiconductor — Pointe Bello ↩

-

Brief History of Zhuzhou CRRC Times Electric Co. — MatrixBCG ↩

-

2024 Annual Results Announcement — Zhuzhou CRRC Times Electric (HKEXnews), 2025-03-28 ↩

-

Zhuzhou CRRC Times Electric Reports Strong 2024 Financial Performance — TipRanks ↩

-

Dynex Semiconductor / CRRC acquisition case study — Pointe Bello ↩

-

Ten Year Anniversary CRRC – Dynex — Paul Taylor (LinkedIn) ↩

-

Zhuzhou CRRC Times Electric to Acquire Dynex Power for 160% Premium — EE Power ↩

-

Annual Report 2016 — Zhuzhou CSR Times Electric (HKEXnews) ↩

-

2024 Annual Results Announcement — Zhuzhou CRRC Times Electric (HKEXnews), 2025-03-28 ↩

-

Zhuzhou CRRC Times Electric Co., Ltd. (688187.SH) — Shanghai Stock Exchange ↩

-

Brief History of Zhuzhou CRRC Times Electric Co. — MatrixBCG ↩

-

2024 Annual Results Announcement — Zhuzhou CRRC Times Electric (HKEXnews), 2025-03-28 ↩

-

Rankings of electrification component suppliers in China (H1 2025) — Gasgoo, 2025 ↩

-

Rankings of electrification component suppliers in China (H1 2025) — Gasgoo, 2025 ↩

-

Zhuzhou CRRC Times Electric Proposes Li Donglin, Shang Jing, Xu Shaolong as Exec Director Candidates of Eighth Board Session — TradingView/Reuters, 2026 ↩

-

Zhuzhou CRRC Times Electric Announces Leadership Shuffle — Nasdaq ↩

-

2024 Annual Results Announcement (directors' and senior management remuneration) — Zhuzhou CRRC Times Electric (HKEXnews), 2025-03-28 ↩

-

2024 Annual Results Announcement (related-party transactions) — Zhuzhou CRRC Times Electric (HKEXnews), 2025-03-28 ↩

-

Circular on continuing connected transactions / mutual supply framework agreements — Zhuzhou CRRC Times Electric, 2024-06-12 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube