EEKA Fashion: The House of Shenzhen Luxury

I. Introduction: The "Hermès of China" Ambition

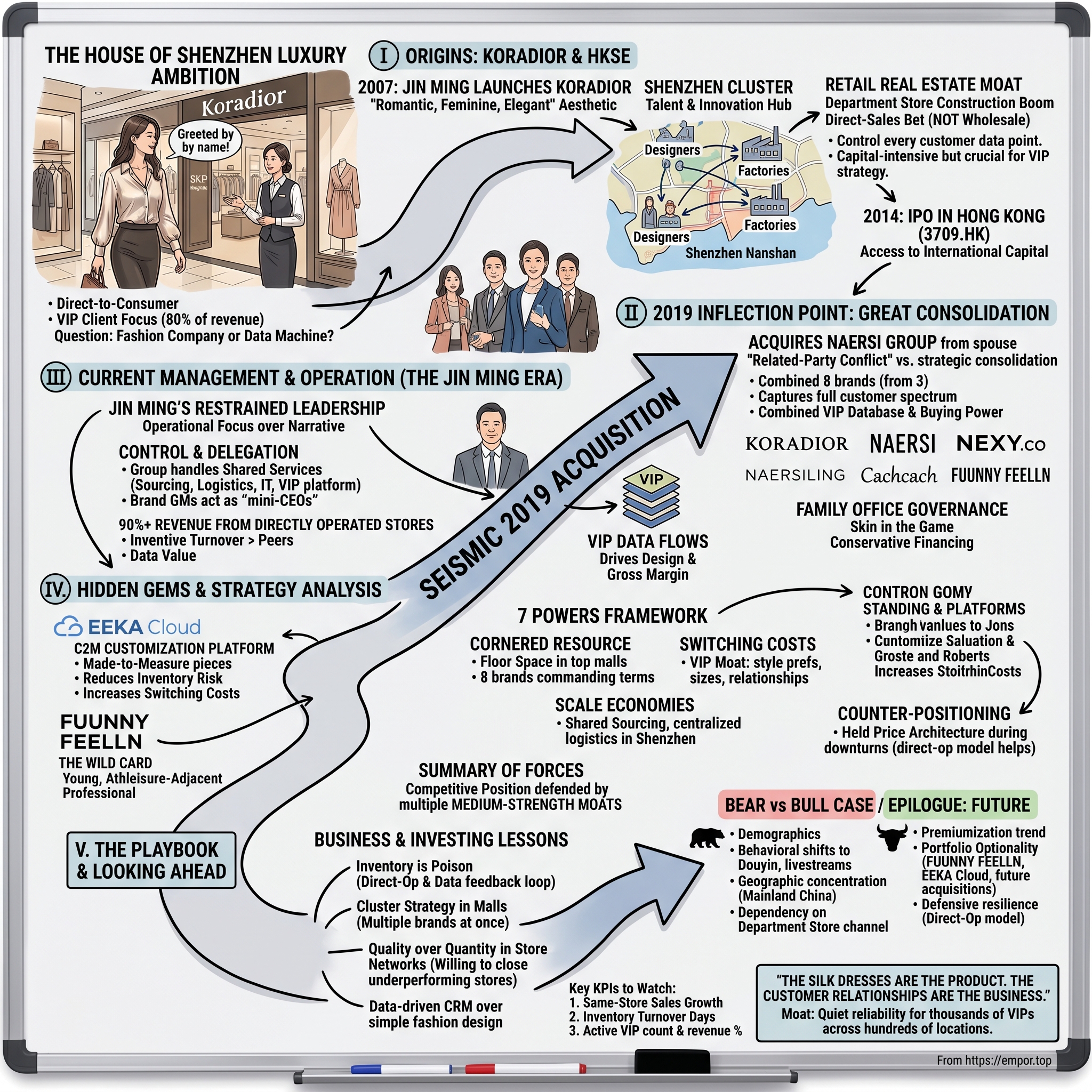

Walk into the SKP mall in Beijing on any Saturday afternoon. The air smells faintly of leather and expensive perfume. A woman in her mid-forties, dressed in a cream silk blouse with embroidered cuffs, glides past the Chanel boutique toward something less familiar to Western eyes. The logo reads Koradior. She is greeted by name. Her usual tailor is waiting in the back. Her measurements have been on file for seven years. This is not Paris. This is not Milan. This is the quiet, almost invisible empire that a company called EEKA Fashion Holdings has built across the top floors of China's most exclusive department stores.

For most global investors, the word "Shenzhen" conjures images of drone factories, semiconductor foundries, and the shimmering glass towers of Tencent. Few associate it with haute couture. Yet for the better part of two decades, the Nanshan district of Shenzhen has quietly operated as the fashion design capital of East Asia, responsible for a disproportionate share of the mid-to-high-end womenswear brands that Chinese consumers actually wear. EEKA Fashion Holdings Limited, ticker 3709 on the Hong Kong Stock Exchange, sits at the dead center of that ecosystem.

The thesis of this episode is straightforward, though the execution was anything but. EEKA began life as a single-brand enterprise, built around a romantic, feminine aesthetic called Koradior. Through a combination of patience, deep relationships with department store operators, and one audacious family-style acquisition in 2019, it transformed into a multi-brand portfolio operator commanding roughly eight distinct labels, all targeting slightly different slices of what the company internally refers to as "the Chinese middle-class lady." The strategy sounds almost boringly simple. The execution required the kind of governance maneuvers that would give a Delaware-trained corporate lawyer a migraine.

What makes EEKA worth two hours of careful attention is not the clothes themselves, elegant as they are. It is the question hiding underneath the brand portfolio. Is this a fashion company, or is it something closer to a direct-to-consumer data machine that happens to sell silk dresses? The answer, as we will see, shapes everything from how investors should value the business to how competitors like JNBY and the remnants of Esprit have historically fared against it.

The roadmap runs from Jin Ming's founding of Koradior in the early 2000s, through the 2014 IPO in Hong Kong, to the seismic 2019 acquisition that nearly doubled the company overnight, and finally into the post-pandemic repositioning that has defined the last three years. Along the way, we will look at the incentive structures that make brand heads behave like founders, the C2M customization platform that nobody outside China talks about, and the VIP clientele that generate roughly four out of every five yuan that hits the company's register.

II. The Origins: From Koradior to the HKSE

Jin Ming did not set out to build a luxury conglomerate. In the early 2000s, he was a young entrepreneur in Guangdong watching the first generation of Chinese white-collar professionals form into something the country had never really seen before: a cohort of economically independent women with disposable income and nobody selling to them properly. The mass-market brands of the era were cheap and cheerful. The international luxury houses were priced for a tiny elite and styled for Western body frames and Western social occasions. In between sat a chasm.

Koradior, launched in 2007, was his answer to that chasm. The brand's design language was deliberate and almost stubbornly consistent: romantic, feminine, elegant. Floral prints. Lace detailing. Silhouettes that flattered without screaming. The positioning was not avant-garde. It was not meant to be. Jin understood something that many first-time fashion founders miss, which is that the customer for a premium everyday brand does not want to be a runway experiment. She wants to look like the most put-together version of herself at a cousin's wedding, a business lunch, or a gallery opening in Chengdu.

The early moat was not the designs, though the designs mattered. The moat was retail real estate. In the late 2000s and early 2010s, mainland China was in the middle of a department store construction boom that is hard to overstate. Wang Fu Jing, Intime, Parkson, and later SKP were rolling out anchor locations in provincial capitals at a pace that required them to fill floors faster than established brands could supply product. Jin and his team made a bet that is obvious in hindsight and was merely shrewd at the time. They went to those department store operators and offered to commit to long-term floor space, operated directly rather than through franchisees, at a time when most Chinese fashion companies were still licensing their names out to distributors.

That single operational choice, direct-sales over wholesale, became the genetic code of everything EEKA would later do. It is worth pausing on, because it runs against the grain of how most apparel companies scale. A wholesale model gets you cash upfront. A franchise model pushes inventory risk onto partners. Direct operation, by contrast, means you eat every unsold skirt, you train every sales associate, and you sign every lease. It is slow, capital-intensive, and operationally punishing. It also means you control every single data point that touches the customer. For a company that would eventually build its competitive edge on VIP loyalty data, this was not a retail strategy. It was the entire strategy.

By 2013, Koradior was generating meaningful revenue across more than five hundred points of sale, primarily in Tier-1 and Tier-2 cities. The decision to list in Hong Kong in 2014 rather than pursue an A-share listing on the mainland reflected a mix of pragmatism and ambition. A-share listings at that time were subject to long queues, political reviews, and price controls that made timing uncertain. Hong Kong offered faster access to international capital, a valuation benchmark against regional peers like Ports Design and Glorious Sun, and, crucially, visibility to the global luxury investor community that was beginning to take Chinese consumption seriously. The IPO in March 2014 was a modest affair by global standards, but it capitalized the business for what would become its defining act five years later.

The Shenzhen connection mattered more than most outside observers appreciate. The Nanshan fashion cluster, organized loosely under the Shenzhen Fashion Association, functioned as an informal talent exchange. Patternmakers, fabric sourcing agents, and merchandising directors rotated between Koradior, NAERSI, Ellassay, Marisfrolg, and a dozen other brands in ways that would be unthinkable in Paris. It compressed learning curves and lowered the cost of building new brand concepts from scratch. When the time came to absorb another portfolio of brands, EEKA would find that the integration challenge was not cultural or geographic. It was familial.

III. The 2019 Inflection Point: The Great Consolidation

In the summer of 2019, investors reading the Hong Kong Exchange filings for 3709 came across a document with the bland bureaucratic title of "Major Transaction and Connected Transaction." The substance inside was anything but bland. EEKA Fashion Holdings announced that it would acquire the entirety of Global Mallow, a company that housed the NAERSI group of brands, for a consideration that would nearly double the group's revenue base. The detail that jumped off the page to anyone who followed the Shenzhen fashion world was the identity of the seller. The controlling shareholder of Global Mallow was Jin Ming's wife.

This is the moment in the EEKA story that separates casual observers from serious students of the business. On its surface, the transaction looked like the textbook definition of a related-party conflict. A controlling shareholder purchasing his spouse's company, inside a listed vehicle, using a mix of cash and newly issued shares. The independent directors had to bless it. The minority shareholders had to vote on it. The fairness opinions had to be commissioned. Every connected-transaction rule the HKEX had written since the Asian financial crisis was stress-tested in the deal circular, which ran to hundreds of pages and became required reading for any analyst covering the Chinese apparel sector.

Yet when you read the logic underneath the governance theater, the transaction was not a conflict. It was a consolidation that the market had been pricing as though it would never happen. Koradior had reached a natural ceiling. A single brand, no matter how well-managed, can only occupy so many department store floors before it starts cannibalizing itself. The NAERSI group, built over roughly two decades by the same extended family, targeted a demographic that Koradior had never served well. NAERSI spoke to the executive woman, the forty-five-year-old finance director who needed three suits, four dresses, and two overcoats per season, and who was willing to pay a serious premium for cut, fabric, and fit. NEXY.CO, sitting inside the same group, extended the professional chic aesthetic into a slightly younger, slightly more playful register. NAERSILING pushed further upmarket. Cachcach targeted a different age bracket again.

The strategic logic was to move from a three-brand house to an eight-brand portfolio in one stroke, capturing the entire spectrum of the premium womenswear customer from her late twenties to her early sixties. Piece by piece, it would have taken another decade to build organically, assuming it could have been done at all. In Chinese fashion, the relationships between brand founders, their longtime design teams, and the department store buyers who allocate floor space are sticky in a way that makes lift-outs almost impossible. The only way to get NAERSI was to buy the family that built it.

On price, the consensus at the time was mixed. The deal valued Global Mallow at a multiple that looked rich compared to where Ellassay was trading, but cheaper than private-market comparables in the broader Chinese luxury space. The critical debate was whether EEKA was paying for a stable cash-flow portfolio or paying for overlapping brands with slowing growth. The counter-argument, which has largely been vindicated by subsequent performance, was that the real prize was neither the individual brand names nor their current profitability. The real prize was the combined VIP database and the buying power across suppliers, landlords, and media partners. Eight brands in a negotiation with an SKP mall or a Joy City developer command pricing terms that three brands cannot.

The capital deployment deserves a closer look because it defined the post-deal balance sheet. EEKA structured the consideration as a combination of cash and new shares issued to the vendor. The cash component drew down the war chest built up since the IPO without forcing the company into the debt markets. The share component accomplished two things simultaneously. It aligned the vendor, and by extension the controlling family, to the post-deal value creation. It also avoided the dilution shock that a fully cash-funded deal of that size would have required, which would have meant either a large equity raise or a leveraged balance sheet going into what turned out to be the most turbulent period in Chinese retail in a generation. The 2019 deal was not timed to the pandemic. It was timed before the pandemic. That it survived what came next is itself a validation of the conservative financing.

For investors, the takeaway from the 2019 transaction is less about the price tag and more about the pattern. EEKA operates as a family office dressed up as a listed company. Governance shareholders should watch connected-party transactions carefully. Business analysts should recognize that the family structure is what enabled the deal to happen at all.

IV. Current Management: The Jin Ming Era

Jin Ming's public persona is notably restrained for a controlling shareholder of a consumer brand. He does not appear on magazine covers. His social media presence is minimal. He rarely speaks to press in English, and his Chinese-language interviews tend to focus on operational details rather than grand vision. This is a tell. Founders who dwell on narrative are usually selling something. Founders who dwell on inventory turnover are usually building something.

His transition from Koradior brand founder to EEKA group portfolio manager was not inevitable. Many founders of single-brand fashion businesses fail at the portfolio transition because the skills are different. Running a brand requires taste, conviction, and the willingness to bet on a specific aesthetic. Running a portfolio of brands requires capital allocation discipline, the humility to let brand-level creative directors disagree with you, and the organizational sophistication to build shared services without strangling individual brand identities. Jin made the leap primarily by refusing to dilute his control over capital allocation while aggressively delegating creative authority down to the brand level.

Shareholding structure tells you most of what you need to know about alignment. Jin Ming retained a significant majority stake after the 2019 acquisition, a position that has not materially changed in the years since. This is not a founder who has been gradually cashing out. For a Hong Kong-listed consumer company of this size, ownership concentration at that level keeps the interests of the controlling shareholder and the minority shareholders pointed in broadly the same direction. When the company pays a dividend, he receives the majority of it. When the company reinvests in inventory systems or new brand launches, he bears the majority of the opportunity cost. Skin in the game, as Nassim Taleb would put it, is not a slogan here. It is the capital structure.

The more interesting design choice is at the brand level. Each of the eight brands operates with a dedicated general manager who functions, in practical terms, as a mini-CEO. The GM controls the brand's design direction, merchandising calendar, store network strategy, and marketing budget. The group center handles the functions where scale compounds, namely sourcing, logistics, IT, and the shared VIP platform. Compensation for brand GMs is heavily weighted toward performance of the brand they run rather than the group as a whole. The intent, which several former executives have described in industry interviews, is to recreate the psychological conditions of founder-ownership inside a salaried management structure.

This philosophy extends directly into the operating model. More than nine out of every ten yuan of revenue comes from directly operated stores. That is an extraordinary figure in the context of Chinese fashion, where wholesale and franchise models dominate for structural reasons. Direct operation means EEKA books the full retail revenue rather than the wholesale margin, but it also means the company bears full inventory risk, full lease obligations, and full staffing costs. The trade-off makes sense only if the operational sophistication is there to manage it, and only if the data value of direct customer contact is worth the overhead.

Both conditions appear to hold. EEKA has consistently delivered inventory turnover metrics that run ahead of most Hong Kong-listed fashion peers, which is how you know the operational discipline is real. The VIP data that flows from direct operation, which we will come back to in the Hamilton's 7 Powers section, is what allows the company to design next season's collection with an unusually high confidence in what will actually sell. For investors trying to understand why EEKA's gross margins hold up during downturns when competitors are discounting, the answer traces back to this single architectural choice made more than fifteen years ago.

The governance lesson is worth naming explicitly. Family-controlled Chinese consumer companies often carry a governance discount in the eyes of foreign institutional investors, and sometimes that discount is deserved. In EEKA's case, the family structure is what enabled the 2019 consolidation to happen at all, and the brand-level incentive design shows a serious attempt to professionalize without centralizing. Neither feature is visible on a standard screening tool. Both are visible in the operating metrics.

V. Hidden Gems and the Segments

The portfolio view of EEKA is where the business gets genuinely interesting. A casual reading of the company's filings suggests eight brands organized by price point. A closer reading reveals something more like a generational map of Chinese professional women, layered with a quiet second business in digital customization that most investors still do not price.

Koradior and NAERSI are the cash cows. Koradior, the original brand, continues to target the romantically inclined mid-premium customer who skews toward events and occasion wear. NAERSI, acquired in 2019, sits slightly higher on the price ladder and targets the executive woman whose wardrobe is more tailored and more formal. Both brands operate at scale across hundreds of points of sale, both command gross margins that run well above the sector average, and both have the kind of sticky VIP bases that allow them to withstand sector-wide discounting without giving up price integrity. In an investor presentation framework, these are the pillars that fund everything else.

The growth engines are NEXY.CO and NAERSILING. NEXY.CO occupies a specific slot that is harder to fill than it looks: professional wear for the woman who wants to signal taste rather than wealth, which in the current Chinese market is a growing rather than shrinking demographic. The brand's silhouettes lean more architectural than Koradior's, and the price point sits at an interesting premium level that captures the customer graduating up from fast fashion but not yet ready for imported luxury. NAERSILING pushes further into the high-end professional segment, with a more restrained aesthetic and small-batch production that tilts the unit economics toward very high margins on modest volumes. Both brands have expanded their store network in recent years as Koradior and NAERSI have held relatively flat.

Then there is EEKA Cloud, which is the part of the business that most Western investors miss entirely. Over the last several years, the group has invested materially in a customer-to-manufacturer platform, commonly shortened to C2M, that allows high-end customers to receive bespoke adjustments or even made-to-measure pieces through the store network and connected digital channels. The technology stack is not dramatic. The business model implication is. Customization accomplishes two things at once. It reduces inventory risk, because garments produced to order do not sit on shelves. It increases switching costs, because a customer whose measurements and style preferences sit inside EEKA's systems is meaningfully harder to poach. For a company that has always competed on data rather than on design alone, C2M is less a new initiative than a logical extension of the founding philosophy.

FUUNNY FEELLN is the wild card. Positioned as the newer, younger brand aimed at the athleisure-adjacent professional customer, it represents the group's bet on what the next decade of Chinese premium womenswear will look like. The challenge is specific. Athleisure globally has been a graveyard for established premium brands that tried to muscle in late. Lululemon built its moat through a decade of community-led marketing and product iteration before the major fashion houses noticed. FUUNNY FEELLN does not have a decade. It has a few years, a well-capitalized parent, and the distribution advantage of sitting inside a group with established department store relationships. Whether it becomes the next Koradior or a cautionary footnote is one of the genuine open questions in the EEKA story, and one investors should watch carefully over the next several reporting cycles.

The brand portfolio lesson for investors is that EEKA is closer to a small-cap luxury holding company than to a traditional apparel business. The capital allocation question facing Jin and his team is not which design to ship next season. It is which brands to feed, which to hold flat, which to gently de-emphasize, and whether to add a ninth. That kind of portfolio discipline is rare in Chinese consumer companies, which historically have preferred to launch new brands organically rather than trim underperformers. EEKA's willingness to close underperforming stores rather than paper over weakness is one of the quieter signals that the discipline is real.

VI. Strategy Analysis: Hamilton's 7 Powers

To understand why EEKA has defended its position through three consecutive years of Chinese retail turbulence, it helps to run the business through Hamilton Helmer's 7 Powers framework. Not all seven apply, but the ones that do apply with force.

The first and most underappreciated is Cornered Resource. In the Chinese premium womenswear market, the cornered resource is not talent or intellectual property. It is floor space. The top-performing floors in the top ten department stores in China, the SKP Beijing and Xi'an locations, the Shin Kong Place properties, the high-end Joy City positions, are effectively capped in supply. Once a brand holds a floor position, displacing it requires both the department store's willingness to break a long-standing relationship and the challenger brand's ability to guarantee revenue per square meter at least equal to what the incumbent delivers. EEKA holds prime positions across most major premium malls in the country, accumulated over nearly two decades, and controls roughly eight brands that can occupy different sections of the same mall. Competitors trying to enter those malls at the premium tier face a structural constraint, not a pricing negotiation.

The second is Switching Costs, specifically the VIP moat. EEKA's CRM and loyalty infrastructure is built around a base of active VIP customers numbering in the low millions, with VIP sales contributing the dominant share of total revenue. The exact contribution moves year to year, but the direction is consistent: the top of the pyramid drives the majority of the business. Once a customer has been in the system for several years, her style preferences, size profile, purchase cadence, and sales associate relationships all live inside EEKA. A competitor brand does not just need to win her on design. It needs to replace a service relationship that has been forming for a long time. This is the single most valuable asset the company owns, and it does not appear on the balance sheet.

The third is Scale Economies. Running eight brands off a shared sourcing function, a centralized logistics hub in Shenzhen, and a shared IT and customization platform generates unit cost advantages that single-brand competitors cannot match. The scale advantage is not of the Amazon or Walmart variety, where the absolute size of the enterprise bends the supplier market. It is more a regional premium-category scale, where the group is large enough to negotiate favorable fabric lots, favorable freight contracts, and favorable landlord terms without being so large that it loses the craft quality that the end customer pays for.

The fourth is Counter-Positioning, which in EEKA's case is a story best told in contrast. Esprit's long decline in Asia, the structural problems at Belle International before its privatization, and the broader fast-fashion hangover all created a vacuum at the premium end of the Chinese women's market. Where competitors raced down-market with discounts in the hope of moving volume, EEKA held its price architecture and accepted lower store footfall in exchange for protecting the brand equity. This is easy to say in hindsight and hard to do in the middle of a downturn, because the short-term revenue cost is real. The counter-positioning works only because the direct-operation model and the VIP base allow the company to ride out the demand gap without triggering a fire sale.

Brand Power itself, in the classic luxury sense, is a complicated case for EEKA. The group's brands carry genuine equity inside China, but they do not yet carry the kind of global recognition that allows Hermès or Chanel to price independently of local competitive dynamics. This is a real limit on how much margin expansion is available from pricing alone, and it is one of the reasons the bull case on EEKA rests more on the scale and switching-cost powers than on pure brand pricing power.

Process Power and Network Economies are less central. Cornered Resource in distribution is a physical asset advantage that does not compound through network effects. The process advantage in inventory management is meaningful but replicable in theory, assuming a competitor could rebuild the data infrastructure from scratch, which would take years.

Running the same business through Porter's Five Forces produces a complementary read. Supplier power is moderate to low, given that China's textile supply base is enormously fragmented and EEKA's eight-brand volume gives it real leverage. Buyer power is low at the individual customer level but moderate at the department store landlord level, where the largest mall operators can extract rent terms that the smaller brands cannot negotiate. Threat of new entrants at the premium Chinese womenswear tier is structurally limited by the floor-space constraint we have already discussed. Threat of substitutes is real and rising, particularly from international luxury brands trading down into accessible price points and from domestic designer labels trading up. Rivalry is intense, with JNBY, Ellassay, Ports Design, and Marisfrolg all competing for overlapping demographics, but the market is large enough that the rivalry has not yet produced the kind of destructive price war seen in Chinese e-commerce or consumer electronics.

The synthesis for investors is that EEKA's competitive position is genuinely defended, but defended by multiple medium-strength moats rather than a single unassailable one. That profile tends to look boring in good years and impressive in bad years.

VII. The Playbook: Business and Investing Lessons

If you were running a classroom case study on how to build a scaled premium apparel business in China, EEKA would give you at least three lessons that generalize beyond the specific company.

The first lesson is that inventory is poison. In fashion, every unsold unit at the end of a season is a triple cost: the working capital tied up in producing it, the markdown taken to clear it, and the brand damage of putting premium goods on a discount rack. EEKA's direct-operation model, combined with the data feedback loop from the VIP base, allows the company to order more conservatively than competitors who must push inventory to wholesalers at the start of each season. The result shows up in inventory turnover metrics that consistently run ahead of the Hong Kong-listed apparel peer group. Investors looking at any fashion company, Chinese or otherwise, should treat inventory days as a leading indicator of management quality, not as a lagging financial metric.

The second lesson is the cluster strategy, borrowed loosely from the LVMH playbook. When EEKA enters a new premium mall, it often opens multiple of its brands at once rather than leading with a single label. This accomplishes several things simultaneously. It increases total floor space commanded by the group, which strengthens the negotiating position with the mall operator. It captures a wider customer demographic inside a single location, which improves same-customer conversion across brands. And it creates an intra-group cross-selling opportunity, where a VIP customer of Koradior can be introduced to NAERSILING by the same sales team. Single-brand competitors cannot replicate this without the portfolio depth, which is itself a function of the 2019 consolidation.

The third lesson is quality over quantity in store networks. Over the last several reporting cycles, EEKA has been willing to close underperforming stores rather than subsidize them indefinitely. This is harder than it sounds. Closing a store incurs lease break costs, severance, and the optical hit of shrinking a publicly disclosed store count that investors have historically treated as a growth metric. Management's willingness to trade short-term optics for long-term brand integrity is one of the quieter signals that the family-office governance structure, for all its complexity, is oriented around long-term value rather than quarterly financial cosmetics.

There is a second-layer observation worth naming here. The Chinese retail property market has been under meaningful stress since 2022, with several large mall operators facing liquidity challenges. For a retailer like EEKA, this environment creates both a risk and an opportunity. The risk is that landlord insolvency could disrupt specific store locations and trigger unplanned relocations. The opportunity is that well-capitalized retailers can negotiate materially better lease terms on new openings, because landlords are desperate for credit-worthy anchor tenants. The group's ability to close weak locations while selectively adding strong ones in premium malls is a direct beneficiary of this dynamic.

The broader takeaway for long-term fundamental investors is that EEKA's playbook is closer to a disciplined capital allocation exercise than to a fashion design bet. The company is not trying to win by having the hottest designer. It is trying to win by owning the best real estate, running the tightest inventory, and compounding the most valuable customer relationships. Over a twenty-year horizon, that is historically a more reliable formula than chasing trends.

VIII. Bear vs Bull Case

Every serious investment thesis has to survive contact with the best available counter-argument. EEKA's bear case is not hypothetical. It is the operating environment the company has been navigating for roughly four years.

The bear case starts with Chinese demographics. The country has entered a period of declining working-age population, and the premium womenswear customer is a specific subset of that shrinking pool. Even if EEKA holds share, the underlying market may grow more slowly than it did during the 2010s. Layered on top is a behavioral shift that cuts deeper. Chinese consumers under thirty-five now spend a disproportionate share of their discretionary time and money on Douyin, the domestic TikTok equivalent, and on live-streamed commerce that favors different brand aesthetics and price points than the traditional department store floor. EEKA's customer acquisition model was built for a world where the premium mall was where status-conscious women went to shop. That world has not disappeared, but it has gotten smaller at the margin, and the replacement channels are not where EEKA is strongest.

A second bear argument is geographic concentration. Virtually all of the company's revenue comes from mainland China. There is no meaningful hedge against domestic consumption weakness, and the international expansion thesis that many Chinese consumer brands have attempted has a mixed track record at best. A third concern is the dependency on the department store channel itself. If premium mall footfall continues to decline structurally, EEKA's cornered-resource advantage loses value, because the resource itself becomes less valuable. And finally, the family-controlled governance structure means that minority shareholders are always operating with less direct influence over capital allocation decisions than they would be in a more dispersed ownership structure.

The bull case reads as the mirror image, and it rests heavily on a single macro idea: premiumization. The observation is that Chinese consumers, particularly in the middle-to-upper-middle income bracket, have been gradually shifting from buying many things to buying fewer, better things. This shift is consistent with what happened in Japan during the 1990s and in South Korea during the 2000s, both of which saw the emergence of scaled premium domestic brands that captured the trading-up behavior. If that pattern holds in China, EEKA is structurally positioned as one of the clearest beneficiaries, because it operates exactly in the price and quality band that premiumizing consumers are moving into.

The second bull argument is the optionality embedded in the portfolio. FUUNNY FEELLN could become a meaningful new engine if the athleisure-adjacent positioning finds a loyal customer base. EEKA Cloud's customization platform could evolve from a loyalty tool into a genuine differentiator. The 2019 consolidation playbook is not necessarily a one-time event; a future acquisition of a distressed European or domestic premium brand would extend the portfolio further at potentially attractive cyclical valuations, should management choose to pursue it.

A third bull argument is defensive in nature. The combination of direct operation, high VIP contribution, and disciplined inventory management produces a business model that is unusually resilient during retail downturns. While other apparel companies are forced into deep discounting to clear inventory, EEKA's ability to hold price architecture means that when the macro environment eventually improves, the company comes out the other side with brand equity intact rather than damaged. This is the subtle but powerful advantage of having built the direct-operation muscle through twenty years of operational investment.

Running the competitive landscape against the 7 Powers framework once more, the bull case has Cornered Resource, Switching Costs, and Scale Economies doing the work. The bear case has a potential weakening of the Cornered Resource if department store relevance declines faster than EEKA can pivot channel mix. The outcome depends heavily on the pace of that channel shift, the speed at which EEKA can build omnichannel capabilities, and the staying power of the VIP relationships.

For long-term fundamental investors, the key performance indicators to watch fall into a tight set. The first is same-store sales growth, which is the single cleanest measure of whether the underlying brand equity is holding, softening, or strengthening. The second is inventory turnover days at the group level, which signals whether the operational discipline that has defined the company is being maintained or slipping. The third, more qualitative but arguably just as important, is the percentage of revenue contributed by VIP members and the growth in the active VIP count, which collectively tell you whether the customer relationship engine is compounding or decaying. These three metrics, tracked across reporting cycles, will tell the EEKA story more accurately than any headline revenue number.

IX. Epilogue: The Future of EEKA

The last three years have been, by any honest measure, the toughest operating environment EEKA has faced in its public life. The 2022 lockdown-induced retail collapse in mainland China, followed by the halting and uneven recovery through 2023 and into 2024, put pressure on every assumption underlying the premium womenswear model. Mall footfall in Tier-1 cities dropped sharply during the acute lockdown phases. VIP in-person service, which is central to how the direct-operation model actually works, became difficult or impossible for extended periods. Competitors across the sector reported double-digit revenue declines, inventory write-downs, and store network contractions.

EEKA navigated that period with a mix of caution and opportunism. The company closed underperforming locations more aggressively than in prior cycles, taking the short-term hit rather than subsidizing weak stores through the downturn. It leaned further into the VIP channel, using digital tools to maintain customer relationships when physical stores were restricted. It held back on major new brand launches that would have required significant upfront investment, preferring to preserve the balance sheet flexibility that has defined the company since the 2019 deal financing. When the recovery began to take hold through 2024 and into 2025, EEKA was one of the better-positioned operators in the category, with inventory levels healthier than most peers and brand equity largely intact.

The final word on EEKA is that it is not quite the company its ticker symbol suggests. On the surface, 3709.HK is a Hong Kong-listed Chinese fashion company. Underneath, it is a data-driven CRM business with eight brand storefronts and a customization platform. Every strategic choice that has differentiated the company over the past two decades, from the original decision to prioritize direct operation over wholesale to the 2019 portfolio consolidation to the ongoing investment in EEKA Cloud, makes more sense through the CRM lens than through the fashion lens. The silk dresses are the product. The customer relationships are the business.

For mid-cap operators looking at EEKA's trajectory and wondering what lessons translate, the most important one is probably the patience of the consolidation strategy. The 2019 deal was not executed at an opportunistic moment in the market cycle. It was executed when the family structure, the operational readiness, and the strategic logic all aligned. Lesser companies often pursue M&A because the banker is in the room or because a quarterly growth target needs to be hit. EEKA pursued M&A because two businesses that had grown up alongside each other could create more value combined than apart, and because the family that controlled both was willing to structure the transaction in a way that the market could ultimately accept. That alignment is rare, and when it occurs, the results tend to compound for years afterward.

Looking forward, the questions that will define the next chapter are straightforward to state and hard to answer. Will FUUNNY FEELLN scale into a meaningful growth engine, or will it remain a small experiment inside a larger portfolio? Will EEKA Cloud evolve from a loyalty feature into a genuine competitive differentiator that the rest of the industry has to respond to? Will the company pursue another major acquisition, potentially of an overseas brand that the current operating environment has made available at attractive terms? And perhaps most importantly, will the generational transition inside the controlling family, whenever it comes, preserve the capital allocation discipline that has defined the business to this point?

None of these questions have clean answers today. What they share is that they are all questions about execution rather than strategy. The strategy, built painstakingly over two decades, is in place. Whether EEKA Fashion Holdings continues to compound value for the next twenty years depends less on whether the thesis is right and more on whether the next generation of operators, inside the family and beyond it, can continue to run the playbook with the same discipline that built it.

The woman in the cream silk blouse at SKP will be back next Saturday. Her tailor will still be waiting. That quiet reliability, across thousands of customers and hundreds of locations, is the closest thing Chinese premium womenswear has to a moat. And for as long as it holds, EEKA will remain one of the most interesting small-cap case studies in Asian consumer markets.

Top Links and References

-

EEKA Fashion 2019 Circular on the Global Mallow and NAERSI acquisition, filed with the Hong Kong Stock Exchange and available through the HKEX disclosure portal. The definitive primary source on the consolidation economics, governance structure, and fairness opinion framework.

-

Industry coverage of the Shenzhen Nanshan fashion cluster, variously referred to as "The Shenzhen Fashion Miracle" in Chinese business media. Useful context on the talent ecosystem that enabled EEKA and its peer group to scale faster than comparable Western premium brands.

-

HKEX Filing 3709 archive, covering annual reports, interim reports, and connected-transaction disclosures since the 2014 IPO. Essential for historical shareholding analysis, dividend payout tracking, and store network evolution.

-

Brand-level profiles of Koradior, NAERSI, NEXY.CO, NAERSILING, Cachcach, and FUUNNY FEELLN, available through both company materials and independent fashion industry publications, including the distinct design philosophies that differentiate each label within the portfolio.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube