Legend Holdings: The Architect of Chinese Enterprise

I. The "Incubator" Hook: More than just Lenovo

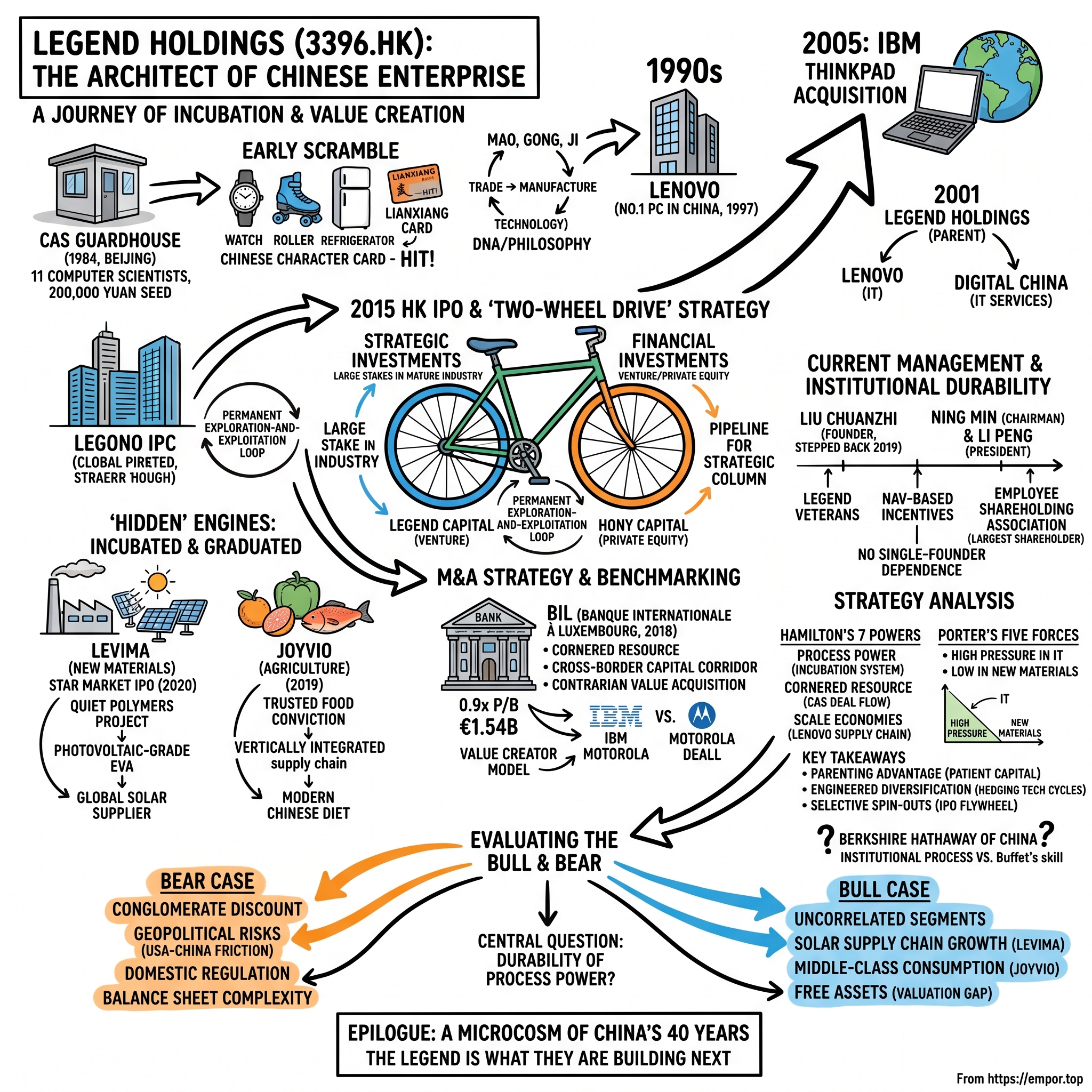

Picture a cramped guardhouse on the leafy campus of the Chinese Academy of Sciences in the Zhongguancun district of Beijing, autumn of 1984. The room is perhaps twenty square meters. The heating is uneven, the wiring suspect, and the furniture consists of government-issue desks that have seen better decades. Inside, eleven computer scientists, led by a 40-year-old engineer named Liu Chuanzhi, are trying to figure out how to turn 200,000 yuan—roughly $25,000 at the time—into something that resembles a business. None of them have ever run a company. China has barely begun experimenting with the idea that citizens might run companies at all. Deng Xiaoping's reforms are six years old and still largely theoretical for most people. The eleven scientists are betting their careers, their reputations, and the patience of the Communist Party's most prestigious research institute on whether they can build a computer company out of a guardhouse.

Fast-forward 42 years. That guardhouse experiment is now Legend Holdings Corporation, a Hong Kong–listed conglomerate whose most famous child—Lenovo—is the world's largest PC maker by shipments, whose portfolio includes a systemic European bank headquartered in Luxembourg, whose new-materials subsidiary is a supplier to the global solar industry, and whose agriculture arm owns a chunk of the Chilean salmon supply chain. The market capitalization of Legend Holdings hovers in the range where an ordinary investor can buy the whole enterprise for less than the value of the Lenovo stake alone—a fact that reveals more about conglomerate discounts and investor skepticism than about the underlying assets.

Here is the investment riddle that Legend Holdings presents. Most people outside China know Lenovo as "the company that bought IBM's ThinkPad division in 2005." Very few realize that Lenovo is just one of several "Strategic Investments" sitting inside a much larger holding company, and fewer still can name the other businesses in the stable. Legend Holdings is, in the most literal sense, an iceberg. Lenovo is the tip everyone sees. Below the waterline sits a portfolio that includes a private-equity franchise (Hony Capital) with tens of billions of dollars under management, a venture-capital franchise (Legend Capital) that has backed over 500 Chinese technology startups, a European bank (BIL) that was acquired in a €1.54 billion cross-border deal, a new-materials company (Levima) that IPO'd on the Shanghai STAR Market, and an agriculture business (Joyvio) that stretches from blueberry farms in Yunnan to salmon farms in the Aysén Region of southern Chile.

The thesis of this episode is that Legend Holdings is not a conglomerate in the tired 1970s-General-Electric sense. It is a purpose-built ecosystem—state-adjacent in its origins, entrepreneurial in its execution, and disciplined enough in its capital allocation that it has, for four decades, repeatedly taken small bets on Chinese technology themes and grown them into standalone public companies. It is, in the words of its own management, a "value creator" that operates on two wheels: strategic investments in mature-industry platforms, and financial investments that scan the horizon for the next wave. The question Western investors have to answer is whether that model is worth more than the sum of its discounted parts—or whether the conglomerate discount is, in fact, correctly priced because the parts are opaque, politically exposed, and structurally second-tier.

To answer that question, the story has to start in that Beijing guardhouse. It has to wind through the extraordinary shift in 2001 when Legend formally separated the operating company from the holding company, through the 2015 Hong Kong listing that announced the "two-wheel" model to the world, through the 2018 European banking acquisition that startled observers, and through the quieter growth of Levima and Joyvio—the two assets that almost nobody talks about but that increasingly drive the narrative. Along the way, we will test Legend against Hamilton Helmer's 7 Powers framework, apply Porter's lens, weigh the bull and bear, and ask the uncomfortable question at the end: is this the Berkshire Hathaway of China, or something stranger?

The legend, in other words, isn't what they built. It's what they're still building.

II. Context: The CAS Origins & The Lenovo Bedrock

Liu Chuanzhi did not want to start a company. In 1984 he was a 40-year-old researcher at the Chinese Academy of Sciences, a Communist Party member of conventional ambition, and—by his own later admission—somewhat resigned to the idea that the rest of his career would be spent writing papers that nobody outside the Institute of Computing Technology would ever read. He had watched with frustration as Chinese computing research, however impressive on paper, failed to translate into products that ordinary Chinese workplaces could use. The Academy had shelves full of prototypes. The country had virtually no computer industry.

The turning point came when Zeng Maochao, the director of the Institute, made a proposition that would have been unthinkable even three years earlier: the Academy would give Liu 200,000 yuan of seed capital, loan him a building (the now-legendary guardhouse), and let him try to build a company that could commercialize the Institute's research. The Academy would retain a majority ownership stake, but Liu and his team would run it. In the vocabulary of later decades, Legend was China's first major technology spin-out from a state research institute. In the vocabulary of 1984, it was a bizarre experiment with no obvious precedent.

The first two years nearly killed it. The eleven founders tried to sell electronic watches, roller skates, and refrigerators—anything that could generate cash. They lost money on most of it. At one point, Liu was defrauded of nearly the entire seed capital by a Shenzhen middleman. The company survived only because it pivoted to distributing foreign computers—reselling IBM, AST, and Hewlett-Packard machines to Chinese state enterprises—and because, critically, one of the Institute's engineers had invented a Chinese-character card that plugged into imported PCs and made them usable for Mandarin-speaking office workers. The "Lianxiang" card—"Lianxiang" meaning "associative thinking," the same word that later became the Mandarin name of Lenovo itself—was the company's first genuine product, and it became a runaway hit inside the peculiar, word-processor-starved Chinese office market of the late 1980s.

Out of this scramble came a philosophy that Liu would articulate for the rest of his career: "Mao, gong, ji"—trade, then manufacture, then technology. The idea was that a developing-country firm could not start with pure R&D. It needed cash from trading, which would fund manufacturing, which would eventually fund proprietary technology. It was a sequence, not a rejection of innovation. And it would define Legend's DNA in ways that still shape the holding company's capital allocation today: earn first, spend second, and never confuse ambition with solvency.

Through the 1990s, Legend did exactly that. It manufactured its own desktops, rode the explosion of Chinese office computing, and by 1997 had overtaken IBM to become the number-one PC brand in China. It listed its IT business in Hong Kong in 1994. It acquired IBM's ThinkPad division in 2005 for $1.75 billion in a deal that was widely viewed at the time as the most symbolically important Chinese overseas acquisition ever completed—a scrappy Beijing upstart buying the crown jewel of American business computing. That deal vaulted Lenovo into the global top three PC makers and, a decade later, made it the world's largest.

But the more consequential decision for our story happened in 2001. Legend's leadership reorganized the business into two tracks. The operating IT company—by then publicly known as Lenovo—kept the Hong Kong listing and continued to pursue PC dominance. A separate entity, Legend Holdings, became the parent: the owner of Lenovo, yes, but also the vehicle that would deploy Lenovo's cash flow into new industries. A third business, Digital China, was spun off to handle IT distribution and services. It was a deliberate architectural choice. The founders had watched other Chinese technology companies fall into a trap where the single operating business dominated all resource allocation, leaving no oxygen for new ventures. By creating a holding company one level above, Liu ensured that future bets would be made from a position of patient capital rather than from the operating budget of a PC manufacturer fighting margin wars with Dell and HP.

This is the decision that most observers miss. Legend Holdings was not created to diversify. It was created to institutionalize diversification—to build an organization whose explicit purpose was to originate and grow new Chinese champions, funded by the old one. Everything that follows in this story flows from that 2001 design choice.

III. Inflection Point 1: The 2015 HK IPO & The "Two-Wheel" Strategy

By the mid-2010s, Legend Holdings had a problem that many companies would envy. It was sitting on a portfolio that had quietly grown into something enormous. Lenovo was now a global top-three PC maker and had just closed its acquisition of Motorola Mobility from Google in 2014. Hony Capital, the private-equity arm founded by John Zhao in 2003, had raised multiple billion-dollar funds and orchestrated landmark buyouts. Legend Capital, the earlier-stage venture arm founded by Chen Hao in 2001, had backed a generation of Chinese tech founders. New businesses—in agriculture, in new materials, in financial services—were moving from experimental to industrial scale. And yet, to the outside world, Legend Holdings was invisible. The market knew Lenovo. It did not know the parent.

On June 29, 2015, Legend Holdings listed on the Hong Kong Stock Exchange, raising approximately HK$15.2 billion (about US$2 billion at the time) in what was, at that moment, one of the ten largest IPOs of the year in Hong Kong. The offer priced at HK$42.98 per share, valuing the company at around HK$100 billion. For a firm whose entire existence had been spent incubating other firms—several of which were already publicly listed themselves—the IPO was an almost philosophical act. It was saying: the incubator itself is the asset. The machinery that turns state research into global companies is, finally, for sale.

The prospectus introduced the world to a phrase that Legend had been using internally for years: the "two-wheel drive" strategy. Imagine a bicycle. One wheel is Strategic Investments—large, controlling or near-controlling stakes in operating businesses such as Lenovo, Levima, Joyvio, and the financial-services franchise that would eventually include BIL. The other wheel is Financial Investments—the venture and private-equity arms, Legend Capital and Hony Capital, which make minority bets across the Chinese economy with a mandate to earn returns, not to build empires.

The synergy is not obvious until you see it in action. Legend Capital, writing early-stage checks into hundreds of startups a year, functions as a radar: it sees which technology themes are gaining commercial traction, which founders are operationally serious, which categories are attracting the best talent. When a portfolio company starts to cross from "interesting" to "strategically important," the Legend parent can step in, take a larger stake, and absorb the business into the Strategic column. It is a pipeline. Not every bet graduates—most do not—but the few that do become the next Lenovo. The holding company is, in effect, running a permanent exploration-and-exploitation loop, with the financial wheel exploring and the strategic wheel exploiting.

At IPO, the segment breakdown told the story of where the company had been. IT—Lenovo—was the cash cow. It contributed the vast majority of consolidated revenue and provided the free cash flow that funded everything else. Financial Services, still a relatively small segment, was positioned for stable-yield expansion, a theme that would culminate in the BIL acquisition three years later. New Materials, at the time anchored by the early-stage Levima business, was presented as a long-duration growth bet tied to China's industrial upgrading story. Agriculture and Food, branded under the Joyvio banner, was the most speculative-looking of the strategic segments—but also the one most clearly tied to a demographic trend that was impossible to miss: a rising Chinese middle class that wanted higher-quality, safer, traceable food.

Investors who bought the IPO expecting a pure Lenovo proxy were confused. Investors who understood the two-wheel model saw something rarer: a Chinese public company whose explicit commitment was to reallocate capital across industries over multi-decade horizons, with a track record of actually doing it. The post-IPO performance has been volatile—Hong Kong's market has not been kind to holding-company structures in general—but the strategic logic laid down in 2015 has largely played out. Each of the "long-term bet" segments has since hit at least one milestone (a portfolio IPO, a major acquisition, a supply-chain breakthrough) that validates the case that Legend is something more than a Lenovo shell with extra pockets.

What the 2015 IPO also revealed, perhaps unintentionally, was the scale of the incubation machine sitting inside the parent. Hony Capital, at the time, managed roughly US$10 billion across multiple funds. Legend Capital had backed or was backing companies that, taken together, were worth tens of billions. These were not hobby businesses. These were full-franchise asset managers that, in any other listed structure, would themselves be the main event. For Legend Holdings, they were one of two wheels.

That architectural reality—two wheels, each of them substantial—is what sets the stage for the next fifteen minutes of our story, because the two wheels have been spinning at different speeds, and the hidden engines under the hood are more important than most investors realize.

IV. The "Hidden" Engines: Levima and Joyvio

If you walked into a chemical-industry trade show in 2010 and asked an executive about Levima, you would have gotten a blank stare. Levima did not exist as an independent operating name in the mass consciousness. It was a quiet polymers project inside the Legend Holdings New Materials portfolio, built around the acquisition of petrochemical assets in Shandong Province. A decade later, Levima was one of China's leading producers of EVA—ethylene-vinyl acetate—a specialty resin that, depending on the grade, is used to make everything from shoe soles to hot-melt adhesives. But one specific grade—photovoltaic-grade EVA—turned out to be something else entirely: the encapsulant film that sits between the glass and the silicon cells inside every solar panel manufactured on Earth.

Here is the technical aside worth a moment. When you look at a rooftop solar panel, the blue silicon you see is the active ingredient, but the silicon is extraordinarily fragile and sensitive to moisture. Between the glass cover and the silicon cells, and again between the silicon and the back sheet, manufacturers sandwich a transparent polymer film that encapsulates and protects the cells for the 25-plus-year operational life of the panel. For decades, the dominant chemistry for this encapsulant has been EVA. And photovoltaic-grade EVA is not an easy product to make: the resin has to hit specific optical clarity and curing properties, the production lines require years of engineering optimization, and most global chemical majors have not bothered to build domestic Chinese capacity at scale. Levima did, exactly as China was becoming the manufacturing hub for roughly 80% of the world's solar panels.

Levima listed on the Shanghai Stock Exchange's STAR Market in September 2020. The IPO raised the company's profile dramatically and, more importantly, gave Legend Holdings a publicly-traded, independently-governed subsidiary in a segment that nobody had previously associated with the parent. In the years since, Levima has expanded capacity, invested in next-generation polymer chemistries including biodegradable plastics, and positioned itself as one of the clean material suppliers riding the green-energy transition. The segment's operating performance has been cyclical, because chemicals always are, and margin pressure from EVA overcapacity has been a recurring headache. But the strategic positioning—a domestic Chinese producer of a critical input to the world's fastest-growing power-generation technology—is the kind of thing that Legend Holdings' prospectus in 2015 would have called "incubating a long-term bet in a hard-tech category." That's what actually happened.

The second hidden engine, Joyvio Group, is stranger and in some ways more interesting. Joyvio began as Liu Chuanzhi's personal conviction that Chinese consumers, as they grew richer, would want food they could trust. China in the late 2000s was living through a series of food-safety scandals—adulterated milk, contaminated cooking oil, mystery meat—and the commercial opportunity, not just the moral one, was to build a vertically integrated food business that could credibly guarantee provenance. Joyvio started in high-end fruit, particularly blueberries and kiwifruit, which were new to the Chinese palate and commanded premium prices. Over time, it expanded into seafood, into animal protein, into ready-to-eat foods, and into what management calls the "modern Chinese diet."

The headline acquisition in this segment was the 2019 deal in which Joyvio took control of Australis Seafoods, one of the major Atlantic salmon producers in Chile. The transaction was the largest Chinese acquisition ever completed in the Latin American aquaculture industry, and it gave Joyvio—and, by extension, Legend Holdings—direct ownership of the supply chain for a protein category that Chinese consumers were discovering at an extraordinary rate. Salmon consumption in China grew several-fold over the 2010s. Owning the farm, rather than just importing the product, meant margin capture from hatchery to dinner plate. It also meant exposure to the operational risks of industrial aquaculture—sea-lice outbreaks, algal blooms, regulatory disputes with Chilean authorities—and Joyvio has absorbed its share of those risks in the years since.

Joyvio's financial profile is volatile in the way that vertically integrated food companies always are. One bad harvest can compress a year's operating margin. But the thesis is not a single-year thesis. The thesis is that China's middle class, several hundred million people strong, is going to spend the next decade trading up on food quality, and whoever controls the supply chain for premium protein and premium fruit will be an attractive business even if the journey is lumpy. Joyvio's role inside Legend Holdings is exactly this: patient capital for a long-duration consumption bet, sheltered from the quarterly-earnings pressures that would force a standalone food company to optimize for near-term EPS.

Together, Levima and Joyvio demonstrate something important about how the two-wheel model actually works. These are not subsidiaries that Legend Holdings bought off the shelf. They were incubated. They were assembled over years, through a combination of platform acquisitions, greenfield investments, and portfolio rollups. They depended on patient parent funding during years when their numbers would have looked ugly to a public-market investor. And they graduated—in Levima's case literally, through a STAR Market listing—into businesses that are now substantial in their own right. This is the "enterprise incubation" process that Legend's management has been talking about since 2001, and it is the pattern investors should look for when evaluating future bets.

V. M&A Strategy: The BIL Acquisition & Benchmarking

In the summer of 2018, Legend Holdings did something unusual even by its own eclectic standards: it bought a systemic bank in Luxembourg. Banque Internationale à Luxembourg—BIL—was founded in 1856, making it one of the oldest commercial banks in continental Europe. It sits at the heart of Luxembourg's financial ecosystem, serves private-banking, corporate, and retail customers, and operates across the Benelux region and beyond. Precision Capital, BIL's previous majority owner, sold a 89.936% stake to Legend Holdings in a deal that closed in September 2018 at a reported enterprise value of approximately €1.54 billion. It was, at the time, the single largest overseas acquisition Legend had ever executed outside of the Lenovo-IBM and Lenovo-Motorola transactions.

The question observers asked in 2018 was the obvious one: what on earth does a Chinese holding company want with a Luxembourgish bank? The deeper question—the one that mattered for long-term investors—was whether the valuation made sense.

Start with the price. Legend paid, on reported metrics, approximately 0.9 times price-to-book for BIL. European banks at the time were trading in a depressed band; the post-2008 regulatory environment and the prolonged negative-rate experiment by the European Central Bank had compressed European bank valuations to multi-year lows. A 0.9x P/B for a profitable, well-capitalized universal bank in a AAA-rated sovereign jurisdiction was, by the standards of 2018 European banking M&A, a disciplined entry price. For comparison, contemporaneous M&A in Southeast Asian and South Asian banking was happening at 1.2 to 1.5 times book, because those markets were growth-oriented and the acquirers were willing to pay for expansion. Legend was not paying for growth. It was paying for stability, for a regulatory license, and for access to a European financial infrastructure.

Now the strategic rationale. BIL is, in Hamilton Helmer's language, a Cornered Resource. You cannot simply start a systemic bank in Luxembourg. The licenses, the regulatory relationships, the correspondent-banking network, the client book accumulated over more than 150 years—these are assets that cannot be replicated at any price, and certainly not by a Chinese holding company writing a check. By acquiring BIL, Legend gave its portfolio companies a cross-border capital corridor. Chinese manufacturers needing euro-denominated financing for European expansion, Chinese investors seeking private-banking services in Europe, Legend portfolio companies raising capital from European institutions—all of these flows now had an in-house provider with genuine European regulatory standing. That is not a synergy in the old General Electric cross-selling sense. It is a platform capability that is very difficult to rent.

The execution risk was, and remains, non-trivial. Cross-border ownership of European systemic banks attracts scrutiny from the ECB, from the Luxembourg regulator CSSF, and from political observers in multiple jurisdictions. Legend has had to invest heavily in governance, compliance, and local talent retention to operate BIL as a stable, independent financial institution rather than a captive Chinese vehicle. The bank has continued to operate under European management, with Legend exercising ownership through governance structures rather than through day-to-day intervention. That restraint is, in itself, a strategic choice: Legend understands that BIL's value is its standalone European credibility, and that credibility erodes fast if the new shareholder starts to look like a parent rather than an investor.

The broader lesson from the BIL deal is about the kind of M&A Legend Holdings does. It does not chase trophy assets. It does not pay up for growth stories that depend on continued multiple expansion. It pays disciplined, often contrarian, prices for platform assets that deliver structural capabilities to the rest of the portfolio. The earlier Lenovo-IBM deal fit the same pattern: IBM's PC division was a money-losing, out-of-favor asset when Legend bought it in 2005, and the purchase price of $1.75 billion reflected that. Within a decade, the combined entity was the world's largest PC maker. The Motorola Mobility deal in 2014, paid for by Lenovo directly, was similarly contrarian: Google had written down Motorola's valuation significantly before selling it on. These are not growth-at-any-price transactions. They are value acquisitions made at cyclical lows in the target industries.

This pattern—contrarian entry, platform capability, long-duration payoff—is the thread running through Legend's external M&A history. It is also, not coincidentally, the thread running through the great holding-company operators in Western history. Berkshire bought newspapers at cyclical lows. It bought Burlington Northern Santa Fe when railroads were deeply out of favor. The Legend management team, whether consciously or not, has absorbed a very similar discipline. Whether they can sustain that discipline over the next decade, amid geopolitical volatility and domestic Chinese regulatory shifts, is the open question. But the track record through 2026 is consistent.

With an institutional M&A muscle now validated across three major transactions, the next natural question is about the people running the shop—and here, too, Legend is deep into a generational transition that is reshaping how the holding company operates.

VI. Current Management & Incentive Structures

For thirty-plus years, Legend Holdings was inseparable from Liu Chuanzhi. He was not merely the founder. He was the moral architecture of the place, the figure whose aphorisms about management—"set strategy, build team, lead team" became standard issue across Chinese business schools. Liu stepped back from the Legend Holdings chairmanship in December 2019, at the age of 75, handing the role to a longtime lieutenant. The formal transition had been telegraphed for years, but the emotional weight of the moment was not small. Liu had, in a very real sense, personally embodied the holding company's continuity with its 1984 origins. His departure forced the question that every founder-led firm eventually faces: what does the institution look like without its founder?

The post-founder era at Legend Holdings is defined by Ning Min as Chairman and Li Peng as President. Both are, in the local idiom, "Legend veterans"—executives who spent their entire careers, two decades or more, inside the Legend system, rotating through roles at Lenovo, at the investment arms, and at portfolio companies before arriving at the parent. That career pattern is not incidental. It reflects a deliberate institutional choice: Legend promotes from within, and it promotes from a talent pool whose mental models have been shaped by the holding-company culture rather than by external capital-markets norms.

Ning Min's background runs through Legend's investment side. His career at the firm included senior roles in financial management and strategic investment, and his fingerprints are visible on many of the transactions that built the current portfolio shape. His chairmanship has been characterized by a more institutional, more quantitatively-driven style of communication than Liu's visionary rhetorical mode. Where Liu talked about "the Legend spirit" and "the long river of history," Ning talks about net asset value, capital deployment discipline, and portfolio-level risk management. It is a shift from founder charisma to fund-manager precision, and for public-market investors it is a shift that makes the company easier to underwrite.

Li Peng, as President, handles day-to-day operations across the strategic-investment portfolio. His remit includes the oversight of the Lenovo relationship (while Lenovo operates with its own independent CEO, Yuanqing Yang), the monitoring of Levima, Joyvio, BIL, and the other strategic holdings, and the allocation of parent-level resources among them. The division of labor between Chairman and President at Legend Holdings has converged, in practice, toward a model familiar to anyone who has studied Western holding companies: the Chairman is the steward of long-term capital allocation and board-level oversight, and the President runs the operational architecture.

The shareholding structure is where the institutional story gets interesting. The largest single shareholder remains the Legend Holdings Employee Shareholding Association—a vehicle that collectively represents the ownership interests of longtime employees who received shares over decades of service. This is unusual. Most large Chinese companies are dominated either by state entities or by founder-family holdings. Legend has both—CAS Holdings, the investment arm of the Chinese Academy of Sciences, remains a very substantial shareholder—but the employee association is the single largest bloc. In practical terms, that means decision-making is anchored in a coalition whose incentives are aligned with long-term enterprise value rather than with short-term stock-price optics.

The executive compensation model has evolved in a direction consistent with this shareholding base. Legend's senior executives are compensated, in significant part, against long-term net-asset-value metrics. The holding company explicitly discourages incentive structures that tie leadership pay to year-on-year stock price. Instead, the framework rewards multi-year NAV growth across the portfolio, which maps to the actual economic activity of a holding company more faithfully than share-price targets would. Critics can argue that NAV measurement has its own discretion problems—how do you value Levima between quarterly marks? how do you handle BIL's fair value in a stressed European banking environment?—but the philosophical alignment is in the right place: if you run a holding company, you should be paid on NAV, and the Legend management team is.

There is also a cultural dimension worth naming. Chinese technology and finance companies have become synonymous, in Western media, with the dominant-founder model. Jack Ma at Alibaba, Pony Ma at Tencent, Lei Jun at Xiaomi—the founder's presence is so central that the institution and the individual become, at times, indistinguishable. Legend has been trying, for a decade, to inoculate itself against that pattern. The 2001 separation into holding and operating companies was a structural inoculation. The long internal apprenticeships of Ning Min and Li Peng were a talent-pipeline inoculation. The NAV-based compensation is a financial inoculation. None of these, individually, guarantee that the institution outlives its founder's cultural DNA. But collectively, they represent a serious and decades-long commitment to building a firm that does not depend on any single person—even Liu Chuanzhi.

That orientation toward institutional durability sets up the question that investors need to ask next: when you strip away the personalities and look at the raw strategic powers of Legend Holdings, what exactly does this enterprise hold that is hard to replicate?

VII. Strategy Analysis: Hamilton's 7 Powers

Hamilton Helmer's 7 Powers framework asks a simple but brutal question of any business: what is the specific source of durable competitive advantage that generates differential returns above the cost of capital, and that cannot be arbitraged away by rivals? Most companies, when examined honestly, have one or two of the seven powers. Great companies have one deep power that defines them. Legend Holdings is unusual because its most durable power is not a product advantage but a process advantage—and that makes it easy to undervalue.

The primary power is Process Power. Legend has built, over four decades, a repeatable enterprise-incubation system that takes a technology spin-off from a research lab, survives it through the cash-flow-negative early years, installs professional management, and graduates it into a standalone public company. The sequence looks simple when you write it down. It is extraordinarily hard to execute. Most sovereign-linked technology transfer programs around the world fail at the management-installation step. Most venture capital firms fail at the patient-capital step because their ten-year fund lifecycles force premature exits. Legend's holding-company structure, with permanent capital and an internal bench of operators who have grown up inside the system, solves both problems simultaneously. Levima's journey from Shandong petrochemical platform to STAR-Market-listed materials leader is not a unique case—it is an instance of a pattern. Lenovo was the pattern. Joyvio is the pattern. Legend has done this so many times that the process itself is the product.

The second power is Cornered Resource: privileged access to the Chinese Academy of Sciences network. Legend is not just a spin-out of CAS. It retains, to this day, structural relationships with the Academy that function as an upstream deal-flow pipeline. When CAS scientists commercialize research, Legend is a natural first-look counterparty. No other holding company in China has anything comparable. You cannot replicate this by writing a check, because it runs on institutional memory, personal relationships, and governance norms that have been maintained over four decades. For a country where deep-tech commercialization is becoming the decisive competitive battle, that upstream pipeline is a meaningful structural advantage.

The third power is Scale Economies, which Legend expresses somewhat unusually through Lenovo. Lenovo's global supply chain—its procurement relationships with component suppliers, its logistics network, its manufacturing footprint across China, Mexico, India, and Brazil—constitutes a chassis that smaller Legend portfolio companies can, in principle, plug into for sourcing and distribution. This is not a synergy that shows up in every portfolio company, because not every portfolio company sells hardware. But where relevant—and it is sometimes relevant for Levima's specialty-chemicals logistics, for Joyvio's cold-chain ambitions—it creates a real cost advantage that a standalone startup would not have.

Several of the other Helmer powers are thin or mixed for Legend. Network Economies are not present at the parent level, though Lenovo has modest network effects in its enterprise software and services offerings. Switching Costs exist within specific portfolio companies (BIL's private-banking relationships are sticky) but not across the holding structure. Branding is interesting: the Lenovo brand is globally strong, but the Legend Holdings brand is essentially invisible to end consumers. Counter-Positioning applies in pieces—Hony Capital's willingness to take control positions in underpriced state-linked assets is a form of counter-positioning against traditional Western private equity—but it is not the headline power.

Now apply Porter's Five Forces to the consolidated enterprise. The Threat of New Entrants for the holding-company model itself is low, because the Process Power described above takes decades to build; there simply are not new entrants trying to do what Legend does at Legend's scale. The Bargaining Power of Suppliers is the area of highest ongoing pressure, particularly in the IT segment, where Lenovo negotiates against Intel, AMD, Qualcomm, Microsoft, and a Taiwanese/Korean display and memory supply chain that sets its own terms. Margin compression in PCs is a recurring headache that no amount of scale fully solves. The Bargaining Power of Buyers is moderate: Lenovo's enterprise customers are large and sophisticated and do shop competitively, but the customer base is diversified enough that no single buyer dominates. The Threat of Substitutes is genuinely low in the New Materials business, where EVA and its adjacent chemistries have few practical alternatives for solar encapsulation, and moderate in the IT business, where tablets, phones, and cloud services substitute for traditional PCs at the margin. Competitive Rivalry in the IT segment is intense and consolidated; in New Materials, it is cyclical; in Financial Services, it is regulated.

What this combined analysis reveals is that Legend Holdings' strongest strategic moats sit in the less-visible parts of the portfolio. Process Power operates at the holding-company level and is invisible to most investors because it does not show up as a line item on the income statement. Cornered Resource around CAS is similarly invisible. Scale Economies through Lenovo are visible but are exposed to the most competitive environment. This mismatch—durable advantages that are hidden, cyclical exposures that are loud—is part of why the stock has carried a persistent conglomerate discount.

A sophisticated investor looking at Legend should therefore focus less on the quarterly Lenovo numbers (already priced by the Lenovo-specific market) and more on the signs of process-power validation: are new portfolio companies reaching scale? is the incubation flywheel still turning? is the CAS deal pipeline still active? Those are the signals that will determine whether the holding company compounds over the next decade, and they are signals that require patience to observe.

VIII. The Playbook: Business & Investing Lessons

Stripped down to its essentials, Legend Holdings offers three distinct lessons that transfer well beyond the specifics of Chinese capitalism. They are lessons about how to build, how to deploy capital, and how to manage the relationship between a parent and its children.

The first lesson is the Parenting Advantage. Legend's core argument for its own existence is that a holding company can provide something that a conventional venture capital fund cannot: truly patient capital. A VC fund raised in 2014 with a ten-year life needs exits by 2024, or at most 2026 if extensions are granted. That timeline forces premature decisions. The fund cannot, in good conscience, hold a portfolio company through a full industry cycle if the cycle is twelve years and the fund is ten. A holding company with permanent capital faces no such constraint. Levima was allowed to grind through multiple years of middling margins while the EVA thesis matured. Joyvio has been allowed to absorb aquaculture operational shocks without the pressure to exit Australis. This patience is not a soft, culturally-Chinese thing. It is a structural capital-markets advantage that comes from having a holding company above the operating company, and it is transferable to any jurisdiction that will tolerate the governance arrangement.

The second lesson is Diversification as Explicit Risk Management. Conventional corporate finance teaches that investors can diversify their own portfolios and therefore do not need diversified companies. Conglomerate discounts exist because the market believes the investor can do a better job than the conglomerate's capital allocators. Legend's response is subtle. It argues that the diversification inside Legend Holdings is not generic—it is specifically engineered to hedge the tech-cycle exposure of its largest asset, Lenovo, with stable-yield assets like BIL and long-duration-growth assets like Levima. A pure Lenovo shareholder rides the full volatility of the PC cycle. A Legend Holdings shareholder rides the cycle but also owns a European bank whose earnings cycle is driven by interest rates and a materials business whose cycle is driven by solar demand. These are largely uncorrelated. The diversification is a risk-management choice, not an empire-building choice, and that distinction is what separates Legend from the discredited 1970s conglomerate model.

The third lesson is the Spin-Out Flywheel. When Legend incubates a business to sufficient scale, it does not insist on keeping the subsidiary tucked inside the parent balance sheet. It lists the subsidiary. Lenovo is publicly traded. Levima is publicly traded. Other portfolio companies have gone through their own IPO paths. This choice has real costs: the parent gives up some optionality, management of the subsidiary has to answer to a second set of public investors, and consolidated accounting becomes more complex. But the benefits are significant. An independently-listed subsidiary has its own cost of capital, its own market-based compensation mechanisms for talent, and its own discipline from public-market scrutiny. Legend, as the controlling shareholder, captures the economic upside while offloading some of the governance burden. It is a deliberately non-imperial model of conglomerate building, and it is different from the historical American norm where holding companies preferred to keep subsidiaries tightly wrapped inside consolidated reporting.

There is a fourth, more subtle lesson worth noting: cultural durability through institutionalization. Liu Chuanzhi did something that very few Asian founders have done successfully. He built a personality-driven company in the founding decade, then spent two decades systematically transferring authority to institutional structures—compensation schemes, ownership associations, internal talent pipelines, and, ultimately, to a Chairman and President who were trained inside the system rather than parachuted in. The failure mode of Asian founder-led companies, broadly, has been a rough transition when the founder departs, either because the successors are family members chosen for loyalty rather than capability or because the personality cult leaves no institutional DNA behind. Legend's post-Liu trajectory has, so far, avoided that failure mode. The fact that the enterprise does not need Liu Chuanzhi to function is, perhaps paradoxically, his most impressive achievement.

These lessons—parent patience, engineered diversification, selective spin-out, and institutional durability—form a coherent playbook. It is not a playbook that every market or every culture will support. You need a capital-markets regime that tolerates holding-company structures, a legal system that respects minority-shareholder rights in partially-owned listed subsidiaries, and a pool of operational talent willing to spend careers inside a system rather than hopping between startups. China in the Legend Holdings era has provided those conditions. Whether it continues to do so, amid regulatory shifts and geopolitical friction, is a central question for the bull-versus-bear analysis that follows.

IX. Bull vs. Bear Case

Every complex holding company eventually boils down, for public investors, to the same fundamental tension. On one side, the bear argues that the parts are worth more than the whole because the market applies a conglomerate discount. On the other side, the bull argues that the discount is an opportunity because the qualitative features of the holding structure are under-priced. Legend Holdings sits squarely in the middle of that argument, and both sides have legitimate points.

Start with the bear case. The most obvious bearish observation is the conglomerate discount itself. At various points in its post-IPO history, Legend Holdings has traded at a market capitalization that is 40 to 50 percent below a simple sum-of-the-parts valuation using the market caps of its listed subsidiaries and reasonable estimates for its private holdings. A shareholder could, in theory, construct a portfolio of direct Lenovo shares, direct Levima shares, a private-equity fund allocation, and a separate European-bank exposure for less capital than the implied Legend Holdings stake would cost on a look-through basis—and receive identical economic exposure without paying the holding-company overhead. This is the capital-markets translation of "why would I pay for a middleman?" For many institutional allocators, the answer is that they would not.

The bear case extends into geopolitics. Lenovo's role as a PC supplier to both Chinese and Western enterprise markets makes it peculiarly exposed to U.S.-China trade friction, export controls on semiconductors, and data-sovereignty disputes. A significant escalation of any of these vectors would pressure Lenovo's margins and volumes in ways that the holding company cannot fully offset. BIL, sitting in Luxembourg under Chinese ownership, is also politically sensitive; European regulatory attitudes toward Chinese ownership of systemic financial institutions have hardened since 2020, and a hypothetical forced divestment, while unlikely in the near term, is a tail risk that cannot be dismissed entirely. Domestic Chinese regulation is another overhang: shifts in policy toward state-linked holding companies, CAS-affiliated entities, or overseas investment approvals could reshape the operating environment faster than public disclosure can keep up.

There is also a more specific financial concern. Integrating BIL produced a noticeable increase in Legend's consolidated balance-sheet complexity and debt-to-equity profile. A holding company that owns a bank is effectively a holding company with a very large set of regulatory capital considerations sitting inside one segment, and the optics of its leverage ratios depend heavily on whether you look at the group level or the operating-segment level. Investors who want clean balance sheets find Legend harder to underwrite post-2018 than pre-2018, and that analytical friction has weighed on valuation.

Now the bull case. The bullish translation of the conglomerate discount is that the Lenovo stake alone, at most points in time, has a market value that approaches or exceeds Legend Holdings' entire market capitalization. If that math holds, a Legend shareholder is effectively buying the Lenovo exposure at close to market price and receiving Levima, Joyvio, BIL, Hony Capital, Legend Capital, and the incubation platform for free. That is a cartoonishly generous framing, because it ignores the holding-company overhead and the illiquidity of the non-Lenovo assets, but the directional point is real. The market has repeatedly priced Legend Holdings as if the non-Lenovo portfolio has a value close to zero, and that is a hard position to defend if you take even a modest view on Levima's value in the solar-supply-chain context or on Hony Capital's value as a standalone private-equity franchise.

The bullish case also rests on the cyclical and structural positioning of the non-IT segments. Levima sits inside the solar-supply-chain growth story, which, despite its well-documented cycles, has an end-demand arc that is measured in decades rather than quarters. Joyvio sits inside the Chinese middle-class food-quality story, which similarly has a multi-decade demand arc. BIL provides a stable-yield, rate-sensitive banking profile that acts as a volatility-dampener against Lenovo's cycle. Taken together, these segments turn Legend Holdings into a diversified exposure to themes that are, on their own, attractive to long-duration investors—particularly those who want Chinese exposure without being concentrated in a single company or sector.

Apply Porter's framework to the consolidated enterprise and the picture brightens slightly. The Threat of Entrants is low at the holding-company level, as we have already discussed. The Bargaining Power of Buyers is moderate across segments but diversified enough that no single buyer disciplines the group. The Threat of Substitutes is low in materials, moderate in IT, and not very meaningful in banking or aquaculture. Competitive Rivalry is segment-specific. In aggregate, the five-forces snapshot is not the snapshot of a company that should trade at a 50% discount to NAV—unless that discount is really about governance perception and geopolitical positioning, in which case the discount is a political-risk premium rather than an operational-risk premium.

Through Hamilton Helmer's lens, the bull and bear cases crystallize around the durability of Process Power. If Legend's incubation machine is still working—if the next Levima, the next Joyvio, the next BIL-style platform acquisition is being assembled right now inside the parent—then the sum-of-the-parts value understates the compounding potential and the conglomerate discount is an opportunity. If the incubation machine is slowing, if the CAS pipeline is drying up, if the post-Liu management is more conservative than entrepreneurial, then the discount is fair, or potentially insufficient. That is the central empirical question for Legend investors over the next five to ten years.

What to watch, specifically: one, the growth trajectory of the New Materials segment, because Levima is the single best barometer of whether the holding company can still graduate bets. Two, the debt-to-equity ratio and the integration metrics from the BIL acquisition, because leverage and regulatory friction inside a systemic bank are the kind of issues that can surprise a holding-company balance sheet. Three, the pace of new strategic-investment additions, because a holding company that stops originating new platforms is no longer a holding company in the active sense. These are the three KPIs most worth monitoring. Everything else is downstream.

Comparative positioning matters too. Globally, the closest analogues are Japan's Softbank Group, Hong Kong's CK Hutchison, India's Tata Sons (private but philosophically similar), and, at the ideological extreme, Berkshire Hathaway. Legend sits in a distinctive niche between these: more operationally intrusive than Berkshire, more diversified than Softbank, less family-controlled than Tata, more state-linked than CK Hutchison. The comparable that investors most often reach for is Berkshire, because the NAV-compounding language is familiar. The reality is that Legend's model is closer to an early-stage Tata Sons, if Tata Sons had come from a state research institute rather than a Parsi business family. That is a distinctive profile, and it deserves its own framing rather than a forced analogy.

X. Epilogue

It is worth, at the end of this story, pulling back to the altitude from which the entire trajectory becomes visible. Legend Holdings is, among other things, a microcosm of China's last forty years. It began in 1984, the same year that Deng Xiaoping's market reforms were formally extending from agriculture into urban enterprise. Its first product, the Lianxiang Chinese-character card, was a literal translation technology—a piece of hardware designed to let foreign computing power communicate with Chinese users. The whole company, at birth, was an act of translation between the state-planned scientific establishment and the emerging private economy.

Over the decades that followed, Legend's evolution mirrored the broader national arc. In the late 1980s and 1990s, it was a manufacturer, mastering the operational disciplines of building physical products at scale. In the 2000s, it became a global acquirer, with Lenovo's IBM deal announcing China's arrival as a credible owner of Western intellectual property. In the 2010s, via the 2015 IPO and the subsequent platform acquisitions, it became a capital allocator, operating across materials, food, and financial services. The shift from making things to owning things, from manufacturing to allocating, is the same shift that the Chinese economy itself has been making—and Legend's balance sheet reads, in many ways, like a scaled-up version of the same transition.

That framing is what makes the Berkshire Hathaway comparison so tempting and, in the end, only partially satisfying. Berkshire is, at its core, an insurance-float arbitrage operating under an exceptional investor. Its moat is Warren Buffett's personal capital-allocation record, extended through a distinctive corporate culture. Legend Holdings is something genuinely different. Its moat is an institutional process: a four-decade-old incubation system linked to a state research network, operating under a generation of professional managers who have spent their careers inside the firm. The individuals matter, but the process is the asset. It is a model that the United States, with its deep preference for individual-founder stories, does not replicate often. It is a model that exists in certain Japanese trading houses, in certain Korean chaebols, and in a few large Indian family businesses—but Legend's version of it, rooted in a state-affiliated research origin, is distinctive.

For the long-term fundamental investor, the central question is not whether Legend deserves a re-rating today. It is whether the incubation process can keep producing new platforms over the next decade. If it can, the conglomerate discount will narrow as each new platform emerges and validates the machine. If it cannot, the holding company will gradually devolve into a static portfolio of mature assets, which the market will continue to value at a discount for perfectly rational reasons. The bet, in other words, is a bet on institutional continuity.

And that brings us back to the guardhouse in 1984. Eleven scientists. Twenty thousand dollars. A few prototype computers. At the time, no one had any reason to believe that the experiment would produce the world's largest PC company, a European systemic bank, a solar-supply-chain specialty chemicals producer, and a Chilean salmon farming operation. The pattern of surprise has, so far, worked in favor of the people who bet early. Whether it continues to work depends on whether the process that produced those surprises is still running, forty-two years in.

The legend, as the roadmap promised, is not what they built. It is what they are building next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube