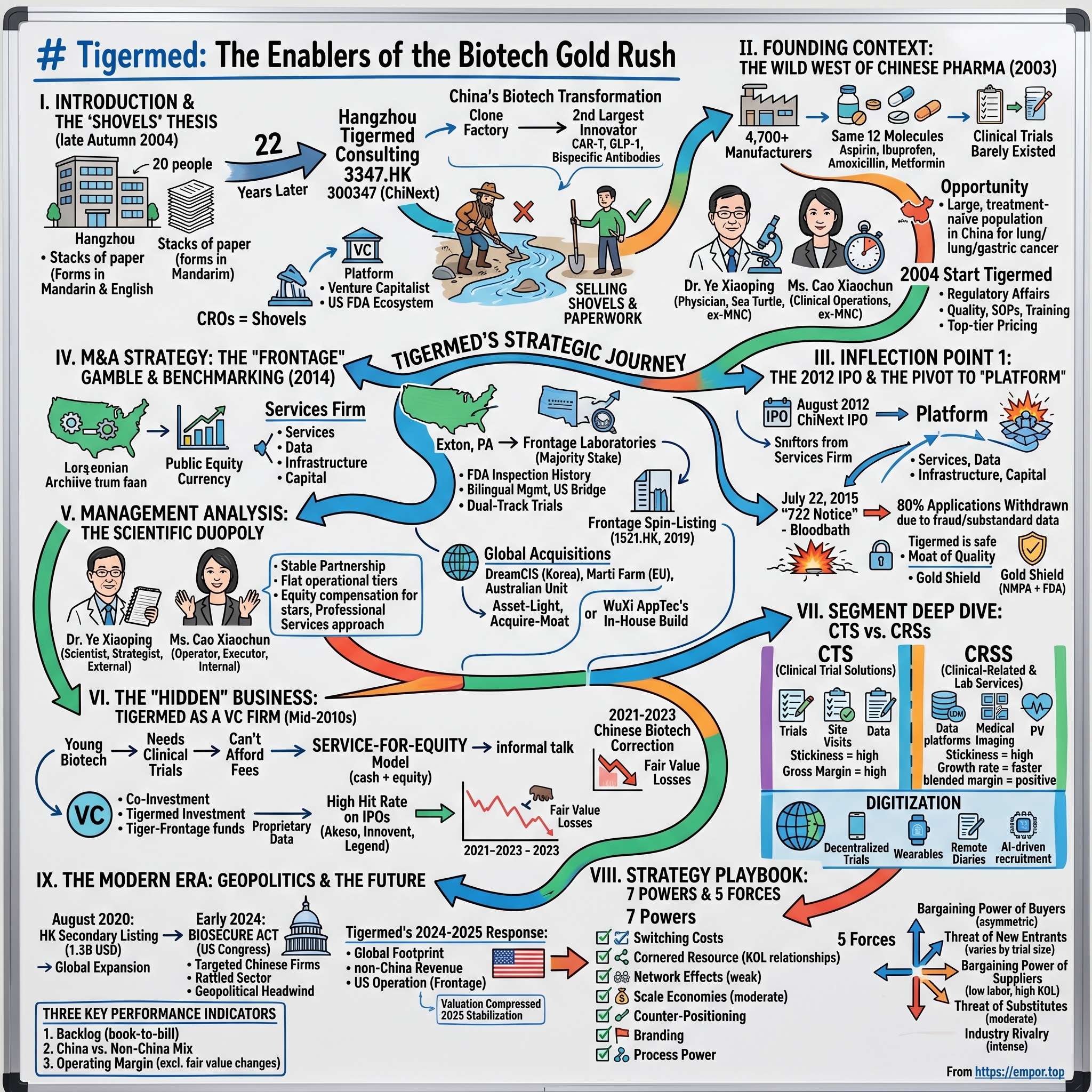

Tigermed: The Enablers of the Biotech Gold Rush

I. Introduction & The "Shovels" Thesis

Picture Hangzhou in the late autumn of 2004. The West Lake is draped in its famous mist, the tea hills of Longjing are turning gold, and somewhere in a modest office building on the outskirts of the city, twenty people are hunched over stacks of paper. Most of them are in their late twenties and early thirties. A handful hold Western pharmacology PhDs. Others are former regulators, medical doctors, biostatisticians. They are filling out forms in Mandarin and English, cross-referencing dossiers that will eventually be submitted to the State Food and Drug Administration—back then still an opaque, cash-strapped agency housed in a gray Beijing compound. Their business cards, when translated, read "clinical research consulting." Almost no one in the country knows what that phrase really means.

Twenty-two years later, that little team has become Hangzhou Tigermed Consulting—3347 on the Hong Kong Stock Exchange and 300347 on ChiNext. Tigermed sits at the center of what is arguably the most important industrial transformation in global pharma over the last two decades. Between 2004 and 2026, China went from being a clone factory—a country that produced cheap copies of Lipitor and aspirin at scale but never invented a significant drug—to being the world's second-largest originator of biotech innovation, the home of CAR-T programs, GLP-1 contenders, bispecific antibodies, and more INDs filed each year than any single European nation.

Here is the thesis of today's episode, stolen shamelessly from the 1849 California gold miners: when there is a gold rush, you do not want to be the prospector standing knee-deep in a river with a sieve. You want to be the person selling shovels, tents, denim jeans, and regulatory paperwork. In China's biotech boom, the shovels are the contract research organizations—the CROs. And the largest, most consequential, most strategically interesting of them all is Tigermed.

This is not just a story about a services firm that grew big. It is a story about how a services firm became a platform, how a platform became a venture capitalist, how a Chinese company quietly stitched itself into the US FDA ecosystem before anyone was watching, and how the same company then had to navigate the greatest geopolitical headwind in modern pharma—the Biosecure Act era, Washington's decoupling push, and the funding winter that decimated the biotech counterparties it had spent two decades building up.

Over the next three hours we trace the arc from that twenty-person Hangzhou office to a multi-continent platform managing trials across North America, Europe, Southeast Asia, and Latin America. We will spend time with the founders, Dr. Ye Xiaoping and Ms. Cao Xiaochun, whose partnership is one of the quiet masterclasses in Chinese corporate governance. We will dissect the 2014 Frontage acquisition that was widely considered a flyer and turned out to be the bridge that made the whole business global. We will examine the hidden venture capital arm that has made Tigermed one of the most prolific biotech investors on the planet. And we will end, as always, with the playbook—the Hamilton Helmer powers, the Porter forces, the bull and bear cases, and the key performance indicators long-term investors will want to keep their eyes on.

Let's start where every good Acquired episode starts: in the dust of a frontier, before the gold rush began.

II. Founding Context: The Wild West of Chinese Pharma

To understand why Tigermed exists, you have to first understand what Chinese pharma looked like before it did. In 2003, the year before Tigermed was founded, China had roughly 4,700 registered pharmaceutical manufacturers. To put that number in perspective, the entire United States had perhaps 200 at the time. Most Chinese manufacturers made the same twelve molecules: aspirin, ibuprofen, amoxicillin, metformin, and a handful of anti-tuberculosis drugs that the government had been subsidizing since Mao's Barefoot Doctor era. Margins were paper-thin. The joke inside the industry was that a bottle of Chinese-made amoxicillin cost less than the paper label wrapped around it.

Clinical trials barely existed in any meaningful scientific sense. The SFDA, the predecessor to today's National Medical Products Administration, had been spun out of the Ministry of Health in 1998 and was, in the early 2000s, both under-resourced and, in some corners, deeply corrupt. In 2007 the agency's head, Zheng Xiaoyu, would be executed by the Chinese state for accepting bribes to approve substandard drugs—a fact that tells you everything you need to know about the integrity crisis the sector was in. Trials that did happen were often run by individual hospitals with no unified protocol. Patient records might be handwritten. The concept of electronic data capture was nearly unknown outside of the three or four academic medical centers in Beijing and Shanghai that had Western collaboration agreements.

Against this chaotic backdrop, two characters began to see the same opportunity from very different angles. Dr. Ye Xiaoping had trained as a physician in China, gone abroad for graduate work, and spent years inside multinational pharmaceutical companies learning how Western clinical trials actually worked—the documentation discipline, the good clinical practice guidelines, the dance with the FDA. He was, in the Chinese term of the era, a haigui, a "sea turtle"—one of the returning overseas Chinese who was quietly reshaping the country's technical professions. Ms. Cao Xiaochun came from the operational side. She had run clinical operations at a multinational's China office and had built a reputation as someone who could actually get a trial completed on time in a country where "on time" was a concept many hospitals did not recognize.

They saw the same thing Western Big Pharma was starting to see: China had an enormous, treatment-naïve patient population for many diseases that were rare or expensive to recruit for in the West. Lung cancer, gastric cancer, hepatitis B—these were conditions where a Phase III trial could be recruited in China in half the time and at a third of the cost of the equivalent US trial. But no one knew how to bridge the gap between Western protocols and Chinese hospital practice. No one had the bilingual regulatory specialists. No one had relationships with both the FDA and the SFDA. No one was translating protocols, training investigators, standardizing informed consent documents in a Chinese cultural context.

So in 2004 Dr. Ye and Ms. Cao left their comfortable multinational jobs, gathered roughly twenty colleagues, pooled some personal savings, and opened Tigermed. The name itself was aspirational—a tiger in the field of medicine, hungry and aggressive. Their first year revenue was trivial. Their second year was better but still small. The business they were scrambling to win was regulatory affairs work—the dark art of turning a Western pharmaceutical company's IND dossier into a SFDA-ready submission. It was unglamorous work. It was the kind of work that, in a Western CRO, would sit in a back office and be paid modestly. In China, because the regulatory code was shifting every quarter and the agency was underfunded and arbitrary, it was high-value specialist labor.

Those lean years—2004 through roughly 2010—shaped the culture that defined everything that came later. The founders obsessed over quality, because they had seen enough sloppy Chinese trials to know that one audit failure could kill a young company. They invested heavily in SOPs—standard operating procedures that were written, in the early days, in bilingual format so they could be read by both a local investigator and an FDA inspector. They built training programs when no one else in China was willing to spend money on training. And they made an early decision that, in hindsight, was the single most important strategic call of the company's first decade: Tigermed would price its services near the top of the Chinese market, not the bottom. If cheap CROs wanted to race each other to zero, fine. Tigermed would sell the expensive shovels.

This obsession with the upper tier of the market meant a slower initial growth curve but a very different kind of customer base. By the early 2010s Tigermed was already working with Pfizer, Roche, Eli Lilly, and a handful of Chinese innovators who were themselves trying to play at international standards. The company had also, quietly, begun building what would become its most underrated asset: relationships with Key Opinion Leaders at the major Chinese academic hospitals. In China more than anywhere else, clinical research runs on guanxi—the web of personal and professional relationships that determines whether a top oncologist at Fudan Cancer Hospital will actually refer patients to your trial. Tigermed spent a decade building that network one dinner, one conference, one co-authored paper at a time.

By 2012, with revenue in the low hundreds of millions of renminbi and growing at better than 40 percent a year, Tigermed had outgrown the private-company model. It was time to tap the public markets, and the timing, it turned out, could not have been better.

III. Inflection Point 1: The 2012 IPO & The Pivot to "Platform"

August 2012 was an interesting moment to list a Chinese company. The Shanghai Composite was still licking its wounds from the 2011 selloff. The US was worried about its own fiscal cliff. Xi Jinping was a few months from taking over from Hu Jintao. And on ChiNext, Shenzhen's Nasdaq-inspired growth board, a small Hangzhou consulting firm walked in with an unusual pitch: we are the first pure-play clinical CRO to ever list on mainland China.

Tigermed priced its ChiNext IPO on August 17, 2012. The offering was modest by any later standard—Tigermed was a small-cap, the float was small, and the capital raised was meant primarily to fund organic expansion of the domestic clinical operations business. But the listing did something more important than raise cash. It gave the company a public equity currency, at a time when the Chinese M&A market for specialist services was almost entirely private. That currency would become the weapon of choice for the next decade of deal-making.

More importantly, the IPO triggered an internal strategic re-evaluation that in retrospect looks like the company's single most important pivot. Up to that point, Tigermed had been a services firm—a very good services firm, but a services firm nonetheless. You hired Tigermed to execute a trial. You paid Tigermed. You got your data. Transaction complete. The founders realized, as they watched WuXi AppTec grow into a monster on the manufacturing side and as they watched global CROs like Quintiles (later IQVIA) move up-market, that pure services was a ceiling. Services businesses scale linearly with headcount. To break out, you needed to be a platform—a thing that biotech companies came to not just for one trial, but for a bundle of services, data, infrastructure, and, eventually, capital.

The platform pivot was slow and not always clean. The company started acquiring adjacencies—small site management organizations, a pharmacovigilance specialist, a medical imaging group. Each acquisition was bolt-on, not transformational. What was transformational was the growing conviction, visible in the 2013 and 2014 annual reports, that Tigermed wanted to be the one-stop-shop for any Chinese biotech's journey from molecule to market.

Then came 2015. And 2015, for the entire Chinese pharmaceutical industry, was a before-and-after moment.

On July 22, 2015, the China Food and Drug Administration—the direct predecessor to today's NMPA—issued what became known as the "722 Notice." The directive was blunt: every pharmaceutical company that had a new drug application pending would be required to "self-inspect" the underlying clinical trial data and decide whether it was fit for purpose. If the data was not fit for purpose, the company was "invited" to withdraw the application before the regulator did it for them, with criminal referrals as a live threat.

What followed was a bloodbath. Of the 1,622 drug applications that were subject to the 722 Notice, roughly 80 percent were withdrawn within the following year. Entire pipelines disappeared. Mid-tier Chinese generic houses that had submitted dozens of applications simultaneously found themselves with nothing in the regulatory queue. Small CROs that had cut corners to win business on price were discovered to have fabricated patient records, forged signatures, recycled lab values. Several were raided. Several were shut down. A few executives went to prison.

For Tigermed, 722 was the moment the long investment in quality paid for itself. Because the company had built its reputation on "we do trials the way the FDA would do them," almost none of the applications on which Tigermed was the lead CRO were withdrawn. When the dust settled in 2016 and 2017, the company emerged with a competitive position that was incalculably better than it had been before the storm. Big pharma clients, watching the carnage from Basel and New York, concluded that Tigermed was the only Chinese CRO they could trust. Chinese innovators, many of whom had been using cheaper providers, migrated en masse. Industry consolidation, in other words, worked in Tigermed's favor not because Tigermed acquired its competitors but because its competitors collapsed and their clients came knocking.

The 722 episode is also when Tigermed's founders began to talk internally about something they called the "Gold Shield." Their argument—which they eventually made in investor presentations and interviews—was that a Chinese CRO that could credibly claim dual-standard quality (Chinese NMPA and US FDA) had a moat that no local-only competitor could cross. Building that moat, however, was going to require something the company did not yet have. To be credible at FDA standard, you needed an actual American operation. You needed American scientists, American inspectors in your history, American audit trails. That calculation led, directly, to the most important deal Tigermed ever did.

IV. M&A Strategy: The "Frontage" Gamble & Benchmarking

In late 2013 and early 2014, Dr. Ye and Ms. Cao started flying to Exton, Pennsylvania. Exton is a suburb about forty miles west of Philadelphia, home to the kind of office park anonymous enough that the average American has never heard of it. Inside one of those office parks sat Frontage Laboratories, a bioanalytical services firm founded in 2001 by a group of ethnic-Chinese US-based scientists, several of whom had done their training at major American pharma companies. Frontage was modestly sized—single-digit-millions of revenue growing to perhaps forty or fifty million by the early 2010s—but it had two things that mattered more than its income statement. First, it had an FDA inspection history. The FDA had walked through Frontage's doors, looked at its instruments, audited its records, and certified the operation. Second, its management team was bilingual and bicultural. They could talk to an American regulator in the morning and a Hangzhou client in the afternoon without missing a beat.

Tigermed completed its majority stake in Frontage Labs in 2014 for a price that was reported around the 50 million US dollar range, though the exact consideration was not fully disclosed. At the time, the deal was considered, charitably, a flyer. Global CROs like Parexel and Covance were trading at 15 to 20 times EBITDA. Frontage was barely profitable and had no meaningful growth engine. Why would a Chinese clinical CRO, which had no US operating experience, pay what looked like a premium for a sub-scale American lab?

The bears were loud. Analysts at several Chinese brokerages wrote that Tigermed was wasting shareholder capital on a vanity transaction. A few US-based observers, on the rare occasions they paid attention to a Chinese CRO's deal activity, were politely skeptical.

Here is what the bears missed. Tigermed was not buying Frontage's revenue. Tigermed was buying a bridge. In one transaction, Tigermed got an FDA-inspected bioanalytical platform in Pennsylvania that it could offer to Chinese biotech clients who needed to run dual-track trials—that is, to generate data simultaneously acceptable to the Chinese NMPA and the American FDA. Chinese innovators who wanted to eventually file with the FDA suddenly had a one-stop option: use Tigermed for the trial and Frontage for the bioanalytics, and your chain of custody is clean from Beijing to Washington. That was a capability no other Chinese CRO could match. It was also a capability that, in 2015 and 2016, became the single most demanded feature in Chinese biotech services procurement.

By 2019, Frontage had grown enough to justify its own Hong Kong IPO as a separate listed entity, 1521.HK. Tigermed retained a majority stake and consolidated Frontage's numbers, which meant Tigermed shareholders got two bites: they owned the operating asset and they owned a public-market security whose movement they could mark to market. The Frontage spin-listing was a kind of magic trick. It validated the 2014 deal at a multiple that made the original 50 million look like a rounding error. More importantly, it opened Tigermed's eyes to the possibility that its other adjacencies—clinical operations subsidiaries, data management arms, regional site managers—could each, potentially, be vehicle-ized and monetized in capital markets at multiples higher than the consolidating parent.

The Frontage playbook became the template. Over the next several years Tigermed would make a series of international bolt-on acquisitions that followed a recognizable pattern. DreamCIS, a Korean clinical CRO, brought Seoul and Busan capabilities and a pipeline of Korean oncology trials. Marti Farm, a Central and Eastern European specialist, brought regulatory expertise in a region where Russian-speaking investigators were starting to see reduced access to Western trials. An Australian unit brought FIH (First-in-Human) capability in Sydney and Melbourne, where local regulatory timelines were among the fastest in the developed world. Each acquisition was small—usually sub-100 million US dollars in headline value—and each one added a specific regulatory geography to the Tigermed platform.

This was a deliberate contrast with the other great Chinese services story of the era. WuXi AppTec, run by Dr. Ge Li, had chosen to build most of its capacity in-house. WuXi's capital-expenditure-heavy model meant it had to pour money into facilities, equipment, and headcount on a continuous basis. The result was a larger, more vertically integrated beast, but also a beast with geopolitical vulnerabilities (as the 2024 Biosecure Act saga would later show) and with capital intensity that sometimes pressed returns on invested capital. Tigermed, by choosing the asset-light M&A path, kept its balance sheet flexible and its return on capital attractive. Every acquisition came with a team of specialists already in place, already licensed, already audited. Tigermed paid for the ticket; it did not have to build the theater.

This asset-light, acquire-the-regulatory-moat strategy is what made the 2020s platform possible. By the time Tigermed went to Hong Kong for its secondary listing, the company had already assembled a global footprint that looked less like a CRO and more like a constellation of specialist firms stitched together by a common quality management system.

V. Management Analysis: The Scientific Duopoly

Walk into the Tigermed headquarters on a weekday morning and, if you are lucky, you might see the two of them in conversation. Dr. Ye Xiaoping tends to be the one with the notebook—always a physical notebook, never a laptop—scribbling in a mix of Chinese characters and English technical terms. Ms. Cao Xiaochun tends to be the one gesturing with her hands, explaining an operational fix to an engineer or a project manager. They are, by most accounts of the people who have worked closely with them, a classic complementary partnership: one scientist, one operator; one strategist, one executor; one external-facing, one internal.

Dr. Ye's biography is, in many ways, the archetypal Chinese pharma sea turtle story. Trained as a physician in China, moved abroad for advanced training, worked inside multinational pharma for long enough to learn both the science and the politics, returned to China with a head full of comparisons between what was and what could be. He is thoughtful in interviews, careful with words, quick to credit collaborators, slow to self-promote. He rarely gives press conferences and almost never appears on television. If you want to understand his thinking, you read the annual letter—dense, technical, sometimes awkwardly written, full of specific examples.

Ms. Cao is the other half. She came up through clinical operations and is, in the words of one former Tigermed executive, "the kind of leader who knows every CRA by first name." CRA stands for clinical research associate—the foot soldiers of the CRO world, the people who actually drive to hospital sites, audit case report forms, and chase down missing data points. The fact that the president of a multibillion-dollar public company is rumored to remember the names of her CRAs tells you something about both her management style and the culture she has cultivated. Chinese services firms tend to be hierarchical and top-heavy. Tigermed, by its own description, is deliberately flat in the operational tiers.

The dynamic between the two founders has been remarkably stable over more than two decades, and that stability is itself a corporate asset. In a country where joint founders of high-growth firms frequently end up in court or in news headlines over equity disputes, the Ye-Cao partnership has been drama-free. They have complementary equity positions, they have aligned incentive structures, and—crucially—they have a clearly delineated division of labor. Dr. Ye handles the capital markets, the major client relationships, and the board. Ms. Cao handles operations, talent, and the day-to-day. When they disagree, which they do, they disagree behind closed doors.

Founder shareholding—sum of the two principals and the related-party entities they influence—has hovered in the 20 to 25 percent combined range for much of the public company's life. For a services firm in China, where insider concentration often falls precipitously after IPO, that is a meaningful level of skin in the game. The two have sold shares periodically, typically in measured tranches disclosed in advance, and have used the proceeds partly to fund the family-office-scale biotech investments that sit outside the listed company.

The deeper insight into Tigermed's management philosophy lies in how the company compensates talent below the C-suite. CROs are the ultimate human-capital business. You cannot manufacture a clinical trial; you can only staff one. And the single biggest operational risk in any CRO is losing your most experienced project leaders—the people who have shepherded ten or twenty or thirty trials and who know exactly how to handle a protocol amendment or a site audit. Tigermed addressed this problem early and aggressively. The company's restricted share incentive schemes, which have been refreshed multiple times since the 2012 IPO, push equity well below the senior management layer. Project leaders, key scientists, star biostatisticians—all of them have been part of the equity plans. This is the McKinsey partnership model applied to a Chinese services firm: your most valuable non-partner professionals have a real economic stake in the outcome.

The philosophical distinction is worth emphasizing because it is the thing most Western investors miss when they look at Chinese services companies. Tigermed is not a factory. It does not compete on the cost of its throughput. It competes on the credibility of its protocols, the relationships of its principal investigators, and the speed with which its project managers can solve problems. It is run like a professional services firm—like a law firm, a consulting firm, or a banking division—not like a contract manufacturer. The internal vocabulary, the promotion tracks, the way senior staff are rewarded, all of it is closer to Kirkland & Ellis than it is to Foxconn.

That cultural design choice has consequences up and down the income statement. Tigermed's gross margins are higher than those of a typical Chinese industrial services firm, because the work is intellectually dense and the pricing sticks. Its SG&A as a percentage of revenue runs higher than a pure manufacturer's, because a professional services firm has to carry business development, client service, and partner-track leadership. And its return on invested capital is attractive because the physical capex base is relatively light; most of the assets are between people's ears. The trade-off is that in bad years, when revenue slows, costs do not come down as fast as a factory's would. A CRO downturn is a long, grinding event, not a cyclical whoosh.

With that management canvas in mind, we turn to the second business inside the business—the one that hides in plain sight inside Tigermed's balance sheet and that has quietly generated some of its most dramatic returns.

VI. The "Hidden" Business: Tigermed as a VC Firm

If you read only Tigermed's income statement you would conclude this is a CRO. If you read only its balance sheet you would conclude that, buried among the long-term investments and the equity securities at fair value through profit and loss, there is a venture capital firm of unusual quality hiding in a closet.

The story of how it got there begins, like most good stories in Chinese pharma, with a lunch. In the mid-2010s, as the Chinese biotech ecosystem began to explode, Tigermed's leadership started noticing a pattern. Promising young Chinese founders—often themselves returning sea turtles—would come to Tigermed looking for clinical trial services but could not afford the full price tag. The founders would ask, informally over tea or dumplings, whether Tigermed would consider taking equity in the start-up in lieu of a portion of cash fees. At first the answer was a tentative yes on a case-by-case basis. Then it became a formal program. Then it became a fund.

The "service for equity" model was simple and, in hindsight, genius. A Chinese biotech with, say, $10 million in cash and a need for $3 million of Phase I trial work could pay Tigermed $2 million in cash and issue Tigermed equity valued at $1 million of the services received. The biotech kept more runway. Tigermed locked up the client for the entire trial, and usually for the Phase II and Phase III trials that would follow, because by the time a company has a CRO running its Phase I, switching for Phase II is operationally painful. And Tigermed took a slug of equity in a company it knew better than anyone—because Tigermed was literally running the biology inside that company.

From service-for-equity, the logic extended naturally to co-investment. Tigermed began participating as a limited partner in biotech venture funds, often alongside marquee names like Sequoia China, Qiming, Lilly Asia Ventures, and Hillhouse. It also set up its own vehicles—Tigermed Investment, Ningbo Tigermed, and later the Tiger-Frontage fund platform, which leveraged the combined capability of Tigermed and Frontage to source US-China dual-track deals. By the late 2010s the portfolio ran into the hundreds of companies, many of which were early-stage and privately held.

The critical insight is that this was not a portfolio of random bets. It was a portfolio of companies whose biology Tigermed was being paid to evaluate. When a biotech came to Tigermed for a Phase I, Tigermed's scientists saw the preclinical data, ran the early human trials, analyzed the pharmacokinetics, watched the first biomarker signals. If the drug was working, Tigermed knew before the general market did. If the drug was failing, Tigermed also knew before the general market did. In informational terms, the venture arm was receiving a stream of proprietary data that no outside VC could hope to replicate.

The result was a hit rate that, in the good years, would make a Sand Hill Road partner blush. Several of the companies in which Tigermed took early positions—Akeso, Innovent, Legend Biotech, Hutchmed, and others across the Chinese biotech cohort—went on to successful Hong Kong or Nasdaq listings. Tigermed booked fair value gains in the hundreds of millions of renminbi in multiple reporting periods between 2019 and 2021. In 2020 and 2021 specifically, the profit contribution from fair-value-through-P&L portfolio marks in some periods rivaled the profit contribution from the core CRO business.

And then the music stopped.

The Chinese biotech correction that began in mid-2021 and deepened through 2022 and 2023 was brutal. The Hang Seng Biotech Index fell by more than 70 percent peak-to-trough. IPOs that had priced at frothy valuations traded below their offer prices for months on end. New listings dried up. Primary capital became scarce. Tigermed's portfolio, which had been a tailwind, became a headwind. Fair value losses began to appear in quarterly reports. Management was forced, in analyst calls, to distinguish between the "underlying operating earnings" of the CRO business and the "fair value adjustments" of the investment portfolio.

For investors, the biotech correction was a useful reminder of what the investment arm actually was. In bull markets, it was an accelerator. In bear markets, it was a drag. Management's growing emphasis, from 2022 onward, on reporting adjusted earnings that stripped out fair value changes was not spin; it was the right way to think about the underlying business. The CRO is the compounder. The portfolio is the option.

The symbiosis between the two, however, remained structurally intact. Even in a downturn, a biotech that had taken Tigermed equity was almost certainly still using Tigermed to run its trials. Service revenue from portfolio companies has continued to grow, and the pipeline of late-stage trials from those companies represented embedded future revenue that would show up in Tigermed's order book for years. In that sense, the investment arm was never really a separate business. It was the customer acquisition engine for the core business, dressed up as a venture fund.

With the venture dynamics understood, we can now look under the hood of the operating business and see why its own internal shape matters.

VII. Segment Deep Dive: CTS vs. CRSS

Tigermed reports its business in two main segments, and understanding the difference between them is critical to understanding what the company is actually worth over the next decade. The first is Clinical Trial Solutions, or CTS. This is the stuff you think of when you hear "CRO"—Phase I through Phase IV trial management, the bit where Tigermed runs the actual studies, handles the site visits, manages the investigators, coordinates with the regulators, and delivers the locked data set. The second is Clinical-Related and Laboratory Services, or CRSS. This is everything around the trial—the site management organization work, the data management platforms, the medical imaging reads, the pharmacovigilance, the patient recruitment services, the specialty laboratories.

To understand why the split matters, think of CTS as the headline act and CRSS as the concession stand. The headline act sells the ticket. The concession stand makes the margin.

CTS is a beautiful business in its own right. Once a Phase III trial is under way with a given CRO, switching mid-stream is nearly unthinkable. The protocol has been filed, the investigators have been trained, the electronic data capture system is set up, the statistical analysis plan is locked. To swap CROs would mean months of lost time, regulatory notifications, retraining, and a very real risk that the trial data set would be questioned by the FDA or NMPA for consistency issues. The result is that CTS revenue, once won, tends to be sticky for the life of the program, which can be five to eight years for a large oncology trial. Gross margins on CTS run in the range you would expect for a high-end services firm—not commodity-level, but not software-like either.

CRSS is the more interesting story. The SMO—site management organization—business is one of the great unsung growth engines in Chinese pharma services. An SMO is, essentially, a pool of certified clinical research coordinators who embed inside hospitals to help investigators run trials. In the US and Europe, most SMO work is done in-house by the hospitals themselves. In China, because the hospitals are under-resourced and the trial volume has been growing faster than hospital staffing, SMOs have become an essential middle layer. Tigermed's SMO business is one of the largest in the country. Once an SMO is embedded at a given hospital for a given therapeutic area, the relationship becomes deeply sticky.

Data management and medical imaging have similar stickiness dynamics. Once a pharma client uses Tigermed's data management platform—the software and process that takes raw case report forms and turns them into regulator-ready data sets—the cost of switching platforms between trials is high enough that most clients simply keep using the same system across subsequent programs. Medical imaging, where Tigermed reads radiology scans for oncology endpoints, has similar characteristics. Once a reader roster is trained on a given protocol, changing readers means risking endpoint inconsistency.

For investors, the CTS versus CRSS distinction matters because it drives two different growth rates and two different margin profiles. CTS grows with the absolute number of trials being run in China and, increasingly, with the number of global multi-regional trials that include Chinese sites. CRSS grows with the depth of service each client is buying and with the shift in industry norms toward more complex, data-heavy trials. Over the long term, the CRSS side of the business has been growing faster than CTS, which has been a positive for blended margins and for revenue visibility. The more a client buys from the CRSS side, the harder it is for the client to leave.

Digitization is the connective tissue that runs through both segments. Tigermed has been investing, since the late 2010s, in what the industry calls decentralized clinical trials—trials where at least some of the data collection happens at the patient's home rather than at a hospital site. Wearable devices that measure heart rate, glucose, or gait. Remote electronic diaries. Video-based symptom assessments. Direct-to-patient drug shipment logistics. The COVID-19 pandemic, for all its horrors, accelerated the adoption of these techniques across the industry, and Tigermed invested meaningfully in building out its decentralized capability during the 2020–2022 window. AI-driven patient recruitment, where natural language processing is used to match electronic health record data to trial inclusion criteria, is another frontier. Tigermed does not disclose specific AI-related revenue, but executives have spoken about the technology as a potential source of competitive advantage in matching patients to specialized trials.

The digitization theme is particularly interesting because it gets at one of the subtle long-term risks for the industry. If AI and decentralized techniques make trials faster and cheaper, that is broadly good for biotech clients but could compress services revenue per trial. The CRO that adapts best—that prices for outcomes rather than hours, that owns proprietary platforms, that captures the value of efficiency gains rather than passing them all through—will be the winner. Tigermed's bet, so far, has been that it can be that CRO in China and in a growing share of the emerging markets.

Understanding the segment mix sets up the strategic playbook—the classic Acquired frameworks through which we can weigh the durable advantages the company has built.

VIII. The Strategy Playbook: 7 Powers & 5 Forces

Time for the playbook section. Hamilton Helmer's Seven Powers framework is the lens we use on this show to stress-test whether a company has a durable business or a rented one. Porter's Five Forces is the complement—the map of where the competitive pressure comes from. Let us run Tigermed through both.

Start with Switching Costs, which is unambiguously the primary power here. We have already talked about how hard it is to change CROs mid-trial, but the point deserves a little more color. Imagine you are a mid-cap biotech with a Phase III oncology asset. You have enrolled 800 patients across 60 sites in 8 countries. Each site has been trained on your protocol. Each investigator has been credentialed. Each country's regulator has been notified of your chosen CRO. The database has been built in a specific electronic data capture system. The statistical analysis plan has been signed off. Your CMO has built a six-year relationship with the project leader at the CRO. Now imagine your CFO says, "We can save 8 percent on the remaining services budget by switching to a cheaper CRO." The CMO laughs out loud. You do not switch. You would rather cut your own arm off. That is switching cost, in Helmer's sense, and it is the single most important economic characteristic of the CRO industry.

Cornered Resource is the second power, and it manifests in the relationships Tigermed has with Key Opinion Leaders—the principal investigators at China's top academic hospitals. In oncology, for example, the ability to run a trial at Fudan University Shanghai Cancer Center, Sun Yat-sen University Cancer Center, or Peking Union Medical College Hospital is practically a precondition for a Chinese trial to be credible. Those relationships have been cultivated, by Tigermed's clinical operations team, over two decades. They are not transferable. A new entrant cannot buy them. This is a power that compounds with time.

Network Effects is the third power and, in the Tigermed case, it is subtler but real. More trials means more patient data, which means better predictive models for recruitment, which means faster recruitment per site, which means happier biotech clients, which means more trials. The data network effect is weak in any single year but strong over a decade. The site network effect is stronger: more Tigermed trials at a given hospital means the hospital's investigators get more experience with Tigermed's SOPs, which means Tigermed's subsequent trials at that hospital start faster and run cleaner.

The remaining four Helmer powers—Scale Economies, Counter-Positioning, Branding, and Process Power—are present to varying degrees but are not the primary drivers. Scale helps on fixed-cost absorption for the data management platforms and on negotiating power with hospital networks. Branding helps with multinational client wins, where the Tigermed name on the contract carries weight with a risk-averse Basel procurement team. Process power is, arguably, the internal reason for the quality moat—two decades of SOP refinement is hard to replicate. But the fundamental engine is switching costs plus cornered KOL relationships, amplified by a real but slow-building network effect.

Now Porter's Five Forces. Bargaining power of buyers is asymmetric in a fascinating way. For small biotechs, Tigermed has the leverage: a credible CRO brand is itself part of the venture story those biotechs sell to their VCs, and the cost of going with a second-tier provider is a lower-probability trial success. For Big Pharma, the leverage flips: Pfizer, Roche, or Merck can play Tigermed off against ICON, IQVIA, PPD, and Parexel, and the negotiating dynamics look more like a procurement auction. The blended buyer power is therefore moderate, with the small-biotech share of revenue being the high-margin tail.

Threat of new entrants varies by trial size. At the small, Phase I, domestic-only end of the spectrum, entry barriers are low and Tigermed faces real competition from mid-tier Chinese CROs. At the large, multi-national, FDA-ready end, the barriers are nearly insurmountable for a new Chinese entrant. You need the regulatory geography footprint, the KOL relationships, the SOP library, and the multi-year audit history. Building that from zero would take a decade and hundreds of millions of dollars in investment. This asymmetry is why Tigermed's long-term margin defense is better than a naïve look at industry headcount would suggest.

Bargaining power of suppliers is low in the traditional sense—Tigermed's main input is labor, and labor is abundant if sometimes expensive. The nontraditional supplier is the hospital investigator, and there the power sits with the principal investigators themselves. But because Tigermed has cultivated relationships over time and because many investigators have worked repeatedly with Tigermed project managers, the practical supplier leverage is muted.

Threat of substitutes comes from in-house clinical teams at big pharma companies and from alternative R&D strategies like computational biology, in-silico trials, and AI-driven preclinical screening that could, theoretically, reduce the volume of human trials needed. In practice, most substitutes either expand the market (preclinical AI means more candidates reaching human trials) or shift the mix (in-house teams still use CROs for specific geographies). The substitution threat is real on a twenty-year horizon but not on a five-year one.

Industry rivalry is the force that deserves the most attention. Tigermed competes against two categories of rival. Domestically, it competes with a growing list of Chinese peers—WuXi AppTec's clinical arm, Pharmaron's clinical services unit, ClinChoice, and others. Globally, it competes against IQVIA, ICON, Syneos, PPD (now part of Thermo Fisher), Parexel, and a few specialist firms. The domestic rivalry is intense on price, especially at the lower end of the complexity curve. The global rivalry is intense on capability. Tigermed's positioning—premium Chinese provider with a global footprint—is a specific, defensible niche, but it requires the company to keep investing in geographic expansion and in capability depth to hold.

Holding all that in mind, we can zoom out to the strategic question that dominates Tigermed's current era: what happens when the geopolitical ground shifts?

IX. The Modern Era: Geopolitics & The Future

August 2020 was a strange month to list a company on the Hong Kong Stock Exchange. The pandemic was still raging. US-China tensions had escalated through the Trump administration's final year. The Hong Kong National Security Law had just been imposed. And yet, on August 7, 2020, Tigermed priced a secondary listing on the HKEX, trading under the 3347 ticker. The offering raised roughly 1.3 billion US dollars, making it one of the largest healthcare listings in Hong Kong that year.

The timing, in retrospect, looks prescient. The proceeds funded the global expansion push that allowed Tigermed to build out non-China capability before the geopolitical winds got truly harsh. Between 2020 and 2023, the company deepened its presence in Australia, Southeast Asia, South Korea, India, the EU, and select Latin American markets. The stated rationale was customer-driven: multinational clients wanted trials that could run simultaneously across regions. The unstated rationale was risk management: if the US-China relationship continued to deteriorate, a CRO that could credibly run trials entirely outside of China would be worth more than one that was purely domestic.

That risk management became urgent in early 2024, when a bipartisan group in the US Congress introduced the Biosecure Act. The draft legislation, aimed at restricting US federal contracts and funding from flowing to a specific list of Chinese biotechnology companies, named a handful of firms explicitly—most notably WuXi AppTec, WuXi Biologics, BGI, MGI, and Complete Genomics. Tigermed was not on the initial list. But the act's existence, and its subsequent passage through the House in 2024 before stalling in the Senate, rattled the entire Chinese services sector. Biotech clients that were heavily dependent on US federal grant dollars began to ask their Chinese providers uncomfortable questions. Some began to explore moving trials to non-Chinese geographies as insurance. The headline risk, even for firms not on the named list, was meaningful.

Tigermed's public response through 2024 and into 2025 was measured. Management emphasized the global footprint that had been built. They noted that a meaningful and growing share of revenue came from non-China activities. They pointed to the acquisitions in Europe, Korea, and Southeast Asia as evidence that the platform was no longer a pure China play. They also, quietly, accelerated hiring in the US operation centered around the Frontage subsidiary, with an eye toward having local capability in the jurisdictions where the geopolitical headwind was strongest.

The 2025 year, based on the company's most recent disclosures, was a year of stabilization rather than growth. The biotech funding winter that had started in 2022 continued to suppress new program starts. Chinese domestic biotechs, Tigermed's highest-growth cohort for most of the 2010s, were spending cautiously. Multinational pharma clients remained, but the procurement cycles lengthened and price negotiations hardened. Tigermed's revenue grew in the low single digits. Margins compressed modestly due to operating deleverage. Investment portfolio fair value changes, which had been a tailwind in the boom, remained a drag or a wash.

The valuation picture tells its own story. In the peak biotech cycle of 2021, Tigermed traded at multiples that reflected a full-throated "Chinese biotech growth story" narrative. By 2024 and into 2026, the multiple had compressed meaningfully, closer to the levels at which global CROs like ICON and IQVIA trade, but with the additional discount that the market applies to Chinese-listed companies during periods of high geopolitical tension. The question every fundamental investor has been asking is whether the market is pricing Tigermed correctly as a global platform or still as a China-exposure vehicle with all the associated risks.

The answer depends in part on how one thinks about three structural pieces. First, the long-term growth of biotech R&D spending globally, which is still secular and still supportive of CRO demand in aggregate. Second, the share of that global R&D that continues to be directed toward China, which depends on both the US regulatory posture and the Chinese domestic funding environment. Third, Tigermed's ability to continue expanding its non-China revenue mix, which depends on execution more than on external winds. The bull case requires all three to hold. The bear case requires any two of them to slip.

Before concluding, it is worth flagging the second-layer diligence items that have appeared in Tigermed's filings and in sell-side commentary over the last several quarters. Management has disclosed ongoing fair value adjustments on equity investments, which remain material quarter-to-quarter and can whipsaw reported earnings. Related-party transactions, common across the Chinese services sector, deserve attention; Tigermed's disclosures on co-investment funds and on transactions with portfolio companies are extensive, but the sheer volume requires careful reading. Share-based compensation, which reflects the incentive design discussed earlier, runs at a level higher than a pure manufacturer's and should be factored into any free cash flow conversion analysis. There have been no known auditor changes, no going-concern flags, and no restatements of consequence in the recent reporting history. The overhang that the market has been most focused on is the Biosecure-adjacent regulatory uncertainty and the separate question of whether STAR-market or HKEX rule changes could affect the listing structure.

With those contours in mind, we can assemble the two-sided case that any long-term investor must hold simultaneously.

X. Conclusion & Final Reflections

Every company worth studying has a bull case and a bear case, and the discipline of holding both is what separates the analyst from the fan.

The bear case for Tigermed is unambiguous and worth taking seriously. The regulatory environment in China remains a moving target, and a future NMPA policy shift could once again reorder the domestic landscape in ways that are hard to predict. The biotech funding winter that began in 2022 may persist longer than optimists hope, depressing new program starts and compressing pricing across the services sector. The geopolitical overhang, even if the Biosecure Act never becomes law in its maximalist form, creates an ambient cost-of-doing-business headwind: biotech clients may reserve a portion of their spend for non-China providers even when Chinese providers are cheaper or better. The investment portfolio, once an accelerant, has become a drag in the bear market and could remain so for years. And inside the operating business, competitive pressure from rising Chinese peers—some of whom are growing fast on the back of their own M&A strategies—could erode Tigermed's pricing power over time.

The bull case begins with demographics and ends with innovation. China's population is aging rapidly. The cohort over age 65 is growing at a pace that will double the country's chronic disease burden within two decades. Drug demand, which has historically been price-constrained by the national insurance system, is being partially released by the rapid expansion of private insurance and by the government's willingness to reimburse for innovative therapies under the Negotiated Drug List mechanism. Chinese biotechs are shifting meaningfully from me-too strategies to first-in-class molecules, with 2024 and 2025 seeing a wave of licensing deals in which Chinese assets were acquired by Western pharma at substantial premiums. Each of those licensing deals implies downstream clinical development that has to happen somewhere, and much of it will happen in China and in the emerging-markets footprint that Tigermed has been building.

Applied through the Helmer and Porter frameworks we worked through earlier, the durable edges are the switching costs on in-flight trials, the KOL relationships at Chinese academic hospitals, and the slow-building network effects in data and recruitment. The vulnerabilities are the concentrations in exactly those same assets: a shock to Chinese hospital-based trial activity would be painful, and a geopolitical decoupling that forced multinational clients to wall off China from their global programs would compress the addressable market.

Comparing against the global set is instructive. IQVIA, the industry gorilla, brings a data-plus-services model, a massive US footprint, and a long track record of margin expansion. ICON is the pure-play scale operator, focused relentlessly on execution. PPD, now inside Thermo Fisher, is the integrated play. In that peer set Tigermed is the China-centric growth platform with a global optionality kicker and a venture portfolio lurking on the balance sheet. Whether that profile deserves a discount or a premium depends entirely on what one believes about the China story over the next decade.

For the long-term investor who wants to hold Tigermed and actually monitor it rather than pray, three key performance indicators matter more than any others. The first is the backlog—the contracted but not-yet-recognized revenue that sits at the end of each reporting period. Backlog growth, and particularly its book-to-bill ratio relative to revenue, is the leading indicator of the next two to three years of top-line. The second is the mix of China versus non-China revenue. A company that successfully decouples from a single-geography growth story by building real non-China revenue is worth more than one that remains a single-geography bet, and that mix shift is the cleanest way to track whether the platform strategy is actually working. The third is operating margin excluding fair value changes from the investment portfolio. This is the cleanest measure of the underlying services business and the one that tells you whether the company is holding pricing and controlling costs through the cycle.

The final reflection, in the style Ben and David would want, is about the larger historical arc. Chinese industrial history in the post-Deng era has produced a small number of companies that were not just big beneficiaries of a boom but that were infrastructurally necessary for the boom to happen at all. Tencent made social communication possible. Alibaba made e-commerce possible. TSMC, across the Strait, made the chip economy possible. In pharmaceuticals, Tigermed is arguably that kind of firm. The company did not invent a drug. It did not cure a disease. It did something less glamorous and, in the long view, more consequential: it built the plumbing, the vocabulary, the audit trails, and the trust that allowed a generation of Chinese scientists to test their ideas in humans at international standards of rigor.

When the history of Chinese biotech is written a generation from now, the first-in-class drugs will get the headlines. The founders who built them will be the heroes. And underneath all of it, in the footnotes and the methodology sections of the scientific papers, will be the CROs that made the trials happen. Tigermed will be the name that comes up most often.

The architects of the infrastructure rarely get statues. They get something more valuable: the long, compounding reward of having built the thing that everyone else has to use.

Top References for Further Reading

- Tigermed Annual Reports (2020–2025), particularly the management discussion and analysis sections and the related-party transaction disclosures.

- NMPA policy archives, especially the July 22, 2015 self-inspection notice and subsequent clinical trial reform guidance.

- Academic literature on China's transition from a fragmented generics industry to an innovation-driven pharmaceutical ecosystem.

- Frontage Holdings prospectus and subsequent annual reports for detail on the US-China bridge strategy.

- Hong Kong Stock Exchange secondary listing documents from August 2020.

- Industry reports benchmarking the global CRO sector, including peer disclosures from IQVIA, ICON, and the former PPD.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube