Solid State System (3S): The HBM Moonshot and the Pivot to AI

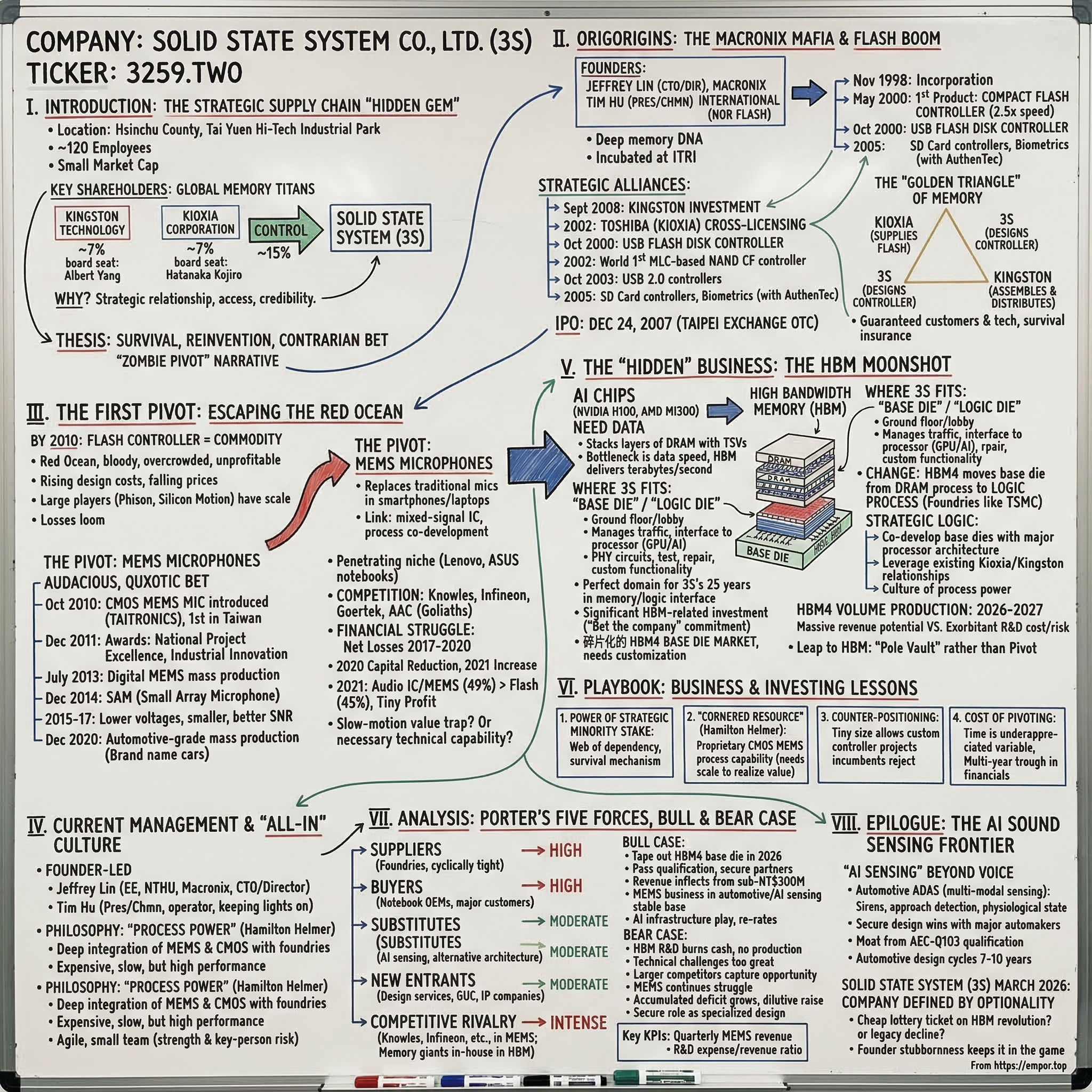

I. Introduction: The Strategic Supply Chain "Hidden Gem"

Somewhere in the sprawl of Hsinchu County's Tai Yuen Hi-Tech Industrial Park, tucked into the fifth floor of a nondescript office building, sits a company with roughly 120 employees, a market capitalization smaller than a mid-tier Manhattan apartment building, and a shareholder register that reads like a who's who of global memory. Kingston Technology—the world's largest independent memory products maker, privately held by the legendary John Tu and David Sun—owns a meaningful stake. Kioxia Corporation, the former Toshiba Memory and one of the planet's top NAND flash manufacturers, holds another chunk and has a representative on the board. Together, these two memory titans control nearly fifteen percent of Solid State System Co., Ltd., a Taiwanese IC design house trading under ticker 3259 on the Taipei Exchange's OTC board. The obvious question: why?

The answer is a story about survival, reinvention, and the kind of contrarian bet that either looks visionary or catastrophic in hindsight. Solid State System—known in industry circles simply as "3S"—is what happens when a company dominates one technology wave, watches it commoditize into oblivion, spends a decade fighting giants in a new market, and then attempts yet another pivot into the hottest corner of the semiconductor universe. Think of it as a "zombie pivot" narrative: a company that by all conventional metrics should have faded into irrelevance but keeps finding new reasons to exist, powered by deep technical DNA and strategic relationships that money alone cannot buy.

The thesis is straightforward. In the mid-2000s, if you plugged a USB 2.0 flash drive into your computer, there was a meaningful probability that a 3S chip was the "brain" orchestrating data flow between your PC and the NAND flash memory inside that thumb drive. The company was a genuine leader in an era when flash storage was exploding. But flash controllers became a commodity, margins collapsed, and 3S made the difficult decision to pivot into MEMS microphones—tiny silicon devices that convert sound waves into electrical signals. That pivot consumed the better part of a decade and left the stock price in ruins. Now, as of early 2026, the company appears to be swinging for the fences once more, this time in the direction of High Bandwidth Memory, the critical component that feeds data to the AI accelerators powering everything from ChatGPT to autonomous vehicles.

Whether 3S can pull off this transformation is genuinely uncertain. The company is loss-making, revenue has declined sharply from its peak, and the competitive landscape is ferocious. But the strategic cap table—Kingston, Kioxia, and connections throughout Taiwan's semiconductor ecosystem—gives 3S access and credibility that most micro-cap IC designers can only dream of. This is a story about what happens when deep technical founders refuse to give up, when strategic investors see something the market does not, and when a company bets everything on being in the right place at exactly the right time.

To understand where 3S is going, we need to start where it began: in the late 1990s, when two engineers walked out of one of Taiwan's most important memory companies with a plan to ride the flash storage revolution.

II. Origins: The Macronix Mafia and the Flash Boom

In November 1998, Jeffrey Lin cleaned out his desk at Macronix International, Taiwan's dominant player in NOR flash memory, and set out to build something of his own. Lin had spent years as a manager at Macronix, absorbing the intricacies of non-volatile memory architecture—how to store data reliably on silicon even when the power goes off. Joining him was Tim Hu, a Division Chief at Macronix with a master's degree in electrical engineering from the University of Missouri. Between them, they possessed an unusually deep understanding of flash memory at the circuit level, the kind of knowledge that comes from years of debugging silicon in the lab rather than reading about it in textbooks.

The company they founded, Solid State System, was admitted to the new-venture incubation center at ITRI—Taiwan's Industrial Technology Research Institute, the legendary institution that had birthed TSMC, UMC, and much of the island's semiconductor ecosystem. Being incubated at ITRI was more than just cheap office space. It meant access to equipment, process engineers, and a network of fellow startups and established companies that formed the connective tissue of Hsinchu's tech corridor. For two Macronix alumni with expertise in flash memory, the timing could not have been better.

By May 2000—barely eighteen months after incorporation—3S had its first product in mass production: a compact flash controller IC that the company claimed delivered write speeds two and a half times faster than anything else on the market. Five months later, they followed with a USB flash disk controller. These were the chips that made thumb drives work. A USB flash drive is essentially three things: a USB connector, a NAND flash memory chip that stores the data, and a controller chip that manages the communication between the two, handling error correction, wear leveling, and the translation between the USB protocol and the raw flash interface. That controller was where 3S lived.

The early 2000s were a golden age for flash storage. USB drives were replacing floppy disks. Digital cameras needed compact flash and SD cards. MP3 players were eating the portable CD market. Every one of these products needed a flash controller, and 3S was one of the companies designing them. In March 2002, they achieved what they called a world first: a four-level cell MLC-based NAND compact flash controller, pushing the boundaries of how much data could be crammed into each memory cell. By October 2003, they had USB 2.0 controllers in mass production, riding the wave as USB 2.0 became the standard interface for consumer storage.

The product portfolio expanded rapidly. SD card controllers arrived in 2005, complete with proprietary intellectual property. That same year, 3S even ventured into biometrics, developing a USB 2.0 controller for linear fingerprint sensors in cooperation with AuthenTec, the American biometrics firm that Apple would later acquire to build Touch ID. Each new product demonstrated the same core competency: taking raw NAND flash from the major memory manufacturers and making it usable through elegant controller design.

Then came the deal that would define 3S's strategic position for the next two decades. In September 2008, the company executed a private placement to bring in strategic alliance partners. The most consequential of these was Kingston Technology. To understand why Kingston invested, you need to understand the economics of the flash storage supply chain. Kingston does not manufacture NAND flash—it buys wafers from the big memory fabs (Samsung, Kioxia, Micron, SK Hynix) and turns them into finished products like USB drives and SSDs. But a flash wafer without a controller is like an engine without a transmission. Kingston needed a reliable, technically excellent controller partner who would prioritize Kingston's needs and give them early access to designs optimized for the latest NAND technology. A small, dependent IC design house was actually preferable to a large one that might deprioritize Kingston in favor of bigger customers.

Kingston's investment was substantial—by 2021, the company held over five million shares, representing roughly seven percent of 3S. More importantly, Kingston secured a board seat, with Albert Yang, Director of Kingston's Flash Engineering Division, serving as a director. This was not a passive financial investment. It was a supply chain lock-in, a way for Kingston to ensure that the controller brains going into its products would always be available, always optimized, and always aligned with Kingston's roadmap.

The Kioxia relationship was even older and arguably more technically significant. As early as 2002, 3S had signed a cross-licensing agreement with Toshiba for flash memory controller development. This was extraordinary for a tiny startup. It meant that 3S could develop controllers in synchronization with each new generation of Toshiba's NAND flash—getting early access to specifications, silicon samples, and process details that competitors would not see for months or years. When Toshiba spun off its memory business as Toshiba Memory (later renamed Kioxia), the relationship continued seamlessly. By 2021, Kioxia held nearly seven percent of 3S and had its own board representative, Hatanaka Kojiro from the Memory Division's NAND System Engineering Department.

This arrangement—a small IC design house flanked by a downstream giant (Kingston) and an upstream giant (Kioxia)—created what industry observers sometimes call the "Golden Triangle" of memory. 3S designed the controller. Kioxia supplied the flash. Kingston assembled and distributed the finished product. Each player needed the other two, and the cross-shareholdings and board seats ensured alignment. For 3S, this meant something invaluable: survival insurance. When flash controllers became commoditized and dozens of small Taiwanese IC houses went under, 3S had guaranteed customers, guaranteed technology access, and strategic investors who would not dump their shares at the first sign of trouble.

The company went public on December 24, 2007, listing on the Taipei Exchange's OTC market. The IPO came at the tail end of the flash controller boom—right before the market dynamics that had made 3S successful began shifting dramatically beneath its feet.

III. The First Pivot: Escaping the Red Ocean

By 2010, the flash controller business had become what competitive strategists call a "Red Ocean"—bloody, overcrowded, and unprofitable. The problem was structural. As NAND flash technology advanced—from 43 nanometer to 34 nanometer to 24 nanometer process nodes—the controller design grew more complex. More aggressive error correction was needed, wear-leveling algorithms had to become more sophisticated, and the interface speeds kept climbing. But the customers—the Kingstons and generic flash drive assemblers of the world—were engaged in brutal price wars of their own. The value of a flash controller was being squeezed from both sides: rising design costs and falling selling prices.

Larger players like Phison and Silicon Motion had the scale to survive. They could spread their R&D costs across massive volumes and move upmarket into SSD controllers where margins were better. For a company of 3S's size, however, the math was becoming impossible. Revenue was decent—the company would report over NT$600 million in annual sales through this period—but profitability was elusive. The flash controller was becoming a commodity, and 3S needed a new act.

The pivot Jeffrey Lin chose was audacious and, in retrospect, somewhat quixotic: MEMS microphones. MEMS—Micro-Electro-Mechanical Systems—are tiny mechanical structures etched into silicon using semiconductor fabrication techniques. A MEMS microphone works by using a microscopic diaphragm that vibrates in response to sound waves; those vibrations are converted into electrical signals by a nearby sensing element. In 2010, MEMS microphones were beginning to replace traditional electret condenser microphones in smartphones, tablets, and laptops. The market was growing fast, driven by the smartphone revolution and the increasing number of microphones in each device (modern phones typically have three or four for noise cancellation and beamforming).

At first glance, the connection between flash controllers and MEMS microphones seems tenuous. But Lin saw a thread linking the two: both required deep understanding of mixed-signal IC design and the ability to co-develop manufacturing processes with foundry partners. The MEMS microphone itself—the tiny mechanical diaphragm—needed to be paired with an ASIC (Application-Specific Integrated Circuit) that amplified and digitized the signal. 3S's expertise in designing ASICs that interfaced with finicky physical components (in the flash case, NAND memory cells with their complex error behaviors; in the MEMS case, a vibrating silicon membrane) was genuinely transferable.

In October 2010, 3S introduced its CMOS MEMS microphone at the TAITRONICS trade show, becoming the first IC design house in Taiwan to offer a MEMS microphone solution. The approach was distinctive: rather than the two-separate-die solution used by most competitors, 3S aimed to integrate the MEMS sensor and the readout ASIC as tightly as possible, eventually developing single-chip and compact two-chip configurations. The government took notice. By March 2011, the technology had won a National Project Excellence Award. By December 2011, it had earned both an Industrial Innovation Achievement award from the Ministry of Economic Affairs and a Taiwan Excellence Award.

Awards, however, do not pay the bills. The MEMS microphone market was dominated by formidable incumbents. Knowles Corporation, the American company that had essentially invented the silicon MEMS microphone, held commanding market share in smartphones. Infineon Technologies had deep automotive expertise. Chinese players like Goertek and AAC Technologies were leveraging their massive manufacturing scale to drive prices down. For 3S, penetrating this market meant going up against companies with ten to a hundred times its resources.

The company pressed forward methodically. In June 2012, digital CMOS MEMS microphone prototypes were verified. By July 2013, digital MEMS microphones entered mass production. In July 2014, 3S launched what it called the SAM—Small Array Microphone—a single-chip solution that combined multiple microphone elements for improved performance in voice capture and noise rejection. The SAM won another Taiwan Excellence Award in December 2014. Each year brought incremental improvements: lower operating voltages (1.2V in 2015), smaller form factors (mini CSP packages in 2016 and 2017), better signal-to-noise ratios, and higher acoustic overload points.

The product found traction in specific niches. Lenovo and ASUS reportedly designed 3S MEMS microphones into some of their notebook computers, where the growing importance of video conferencing created demand for better built-in audio. The automotive segment opened up too—by December 2020, 3S had automotive-grade analog MEMS microphones in mass production, with design wins at what the company's annual report described as "brand name car manufacturers."

But the financial story told a different tale. The MEMS pivot was consuming R&D resources while the flash controller business shrank. The company reported net losses in 2017 (NT$78 million), 2018 (NT$20 million), 2019 (NT$120 million), and 2020 (NT$78 million). In 2020, 3S executed a capital reduction—shrinking its share capital from NT$808 million to NT$647 million—essentially acknowledging accumulated losses by reducing the par value of shares. The following year brought a capital increase back to roughly NT$730 million, raising fresh funds for continued R&D.

By 2021, revenue had shifted decisively. Audio ICs and MEMS products accounted for forty-nine percent of revenue, overtaking flash controllers at forty-five percent. The company managed to eke out a tiny profit of NT$1.158 million—its first profitable year in recent memory—but this was rounding error on a base of NT$692 million in revenue. The stock price, which had been in a prolonged decline, offered little comfort to shareholders who had been through the desert of the MEMS transition.

This is the classic innovator's dilemma in miniature. 3S had genuine technical differentiation—its integrated CMOS MEMS approach produced smaller, potentially cheaper microphone modules than the two-chip solutions used by most competitors. But technical differentiation means nothing without scale, and scale requires either massive capital investment or a breakthrough design win with a major customer. 3S had neither. It was fighting Goliaths with a slingshot, and a decade into the fight, the scoreboard showed it. For investors who had held through the flash controller era, the MEMS pivot looked less like a strategic masterstroke and more like a slow-motion value trap. What those investors could not have known was that the company's deepest expertise—understanding the interface between memory and logic at the silicon level—was about to become extraordinarily relevant.

IV. Current Management and the "All-In" Culture

To understand how a company survives two decades of near-continuous financial distress without collapsing, you have to understand the people running it. Solid State System is not a company managed by professional hired guns cycling through on three-year contracts. It is a founder-led enterprise where the original architects remain at the helm, driven by the conviction that the big breakthrough is still ahead.

Jeffrey Lin, the co-founder, is an electrical engineering graduate of National Tsing Hua University—Taiwan's equivalent of MIT or Caltech, located just minutes from 3S's offices in the Hsinchu ecosystem. His years at Macronix gave him something that cannot be taught in a classroom: an intuitive feel for the boundary between memory and logic, the place where data storage meets data processing. In the semiconductor world, this boundary is where the most interesting—and most difficult—engineering problems live. Flash controllers sit at this boundary. MEMS readout ASICs sit at this boundary. And as we will explore, HBM logic dies sit at this boundary too.

Lin served as Chairman through most of the company's history, combining strategic oversight with deep technical involvement as CTO. He is the kind of founder who reviews layout designs and argues with process engineers, not the kind who plays golf while the VP of Engineering handles the details. As of the tenth board term beginning in May 2024, Lin transitioned from Chairman to a Director and CTO role, suggesting a partial evolution in governance while maintaining his technical leadership. He remained a significant shareholder throughout—holding over 2.5 million shares as of 2021, representing roughly three and a half percent of the company. For a micro-cap company, founder ownership at this level signals genuine skin in the game.

Tim Hu, the other co-founder, served as President (General Manager) since July 2006, running day-to-day operations through the lean years. His Macronix background as a Division Chief, combined with an earlier stint as R&D Chief at Atronics International, gave him both management experience and technical credibility. Hu's role was that of the operator—keeping the lights on, managing customer relationships, and making the quarterly numbers work (or at least explaining to investors why they did not) while Lin focused on the next technology bet. In a notable governance evolution, Hu assumed the Chairmanship for the tenth board term in May 2024, and by December 2025, became both Chairman and President.

The management philosophy at 3S can best be described as "Process Power"—a term from Hamilton Helmer's 7 Powers framework that describes competitive advantage derived from deeply embedded organizational processes that competitors cannot easily replicate. In 3S's case, this manifests as a culture of co-developing manufacturing processes with foundry partners rather than simply sending designs over the wall and hoping for the best. When 3S designs a MEMS microphone, the team does not just draw up a circuit and hand it to a foundry. They work hand-in-hand with the fabrication partner to optimize the MEMS process—the etching of the diaphragm, the cavity formation, the release steps—alongside the CMOS circuitry. This kind of deep process integration is expensive, slow, and difficult to manage, but it produces devices with performance characteristics that a purely fabless competitor cannot match.

This process-centric approach also explains the company's ability to attract and retain strategic investors who are themselves process-obsessed. Kingston does not invest in dozens of random IC design houses. Kioxia does not grant cross-licensing agreements and board seats to companies it does not deeply trust. These relationships endure because 3S's engineering culture speaks the same language as its partners—a language of process corners, yield optimization, and reliability qualification that can only be learned through years of collaboration.

The team is lean by any standard—roughly 120 employees as of recent reports. In a world where the major IC design houses employ thousands of engineers, 3S's headcount means that every person has to wear multiple hats and that institutional knowledge is concentrated rather than distributed. This is both a strength and a vulnerability. The strength is agility: a small team with deep domain expertise can pivot quickly and take on custom projects that larger companies would reject as insufficiently profitable. The vulnerability is obvious: key-person risk is extreme, and any significant departure could be devastating.

What keeps this team together through years of losses and a depressed stock price? The answer appears to be a combination of founder conviction, strategic investor patience, and the genuine belief that the technologies they are developing will eventually find their market. In the semiconductor industry, timing is everything—a product can be technically excellent and commercially irrelevant if it arrives five years too early or two years too late. 3S has been early before. The question is whether they are early again or simply wrong.

V. The "Hidden" Business: The HBM Moonshot

The segment data tells one story: as of 2024, approximately seventy-nine percent of 3S's revenue comes from audio and MEMS products, with roughly twenty percent from legacy flash controllers. But the financial statements are backward-looking. The forward-looking story—the one that explains why anyone would pay attention to a loss-making, sub-fifty-million-dollar IC design house—centers on High Bandwidth Memory.

To understand why HBM matters, and why a tiny Taiwanese company might have a role to play, requires a brief detour into how modern AI chips work. When Nvidia's H100 or AMD's MI300 processes an AI workload, the bottleneck is rarely the compute itself. It is the speed at which data can be fed to the compute engines. Traditional DRAM, connected via standard interfaces, simply cannot deliver data fast enough. HBM solves this by stacking multiple layers of DRAM vertically—like a high-rise building made of memory—and connecting them through thousands of tiny wires called through-silicon vias, or TSVs. The result is a memory system that can deliver bandwidth measured in terabytes per second, orders of magnitude faster than conventional approaches.

Here is where it gets interesting for 3S. At the bottom of every HBM stack sits what the industry calls a "base die" or "logic die." Think of it as the ground floor and lobby of our memory high-rise. This die does not store data. Instead, it manages the traffic—handling the interface between the memory stack above it and the processor (GPU or AI accelerator) beside it. It contains the PHY (physical interface) circuits, the test and repair logic, and increasingly, custom functionality that the processor manufacturer wants integrated directly into the memory subsystem.

In earlier generations of HBM (HBM2 and HBM3), this base die was manufactured using DRAM process technology by the memory makers themselves—SK Hynix, Samsung, and Micron. But starting with HBM4, a fundamental shift is underway. The base die is moving from DRAM process to logic process, meaning it will be manufactured at foundries like TSMC using the same kind of fabrication technology used for processors and ASICs. This is a massive change. It means the base die is no longer just a simple interface—it becomes a sophisticated logic chip that can incorporate custom features, advanced error correction, security functions, and even computational elements.

This transition opens the door for IC design companies that specialize in the boundary between memory and logic. And this is precisely the domain where 3S has spent twenty-five years. The company's core competency has always been designing controllers that sit between a processor and memory—first NAND flash controllers that managed the interface between USB hosts and flash storage, now potentially HBM base dies that manage the interface between AI accelerators and stacked DRAM.

Industry reports suggest that 3S has been investing significantly in HBM-related development, with capital deployment figures that are extraordinary relative to the company's size. For a company with a market capitalization of roughly forty million dollars, any investment in the hundreds of millions of New Taiwan dollars range represents a genuine "bet the company" commitment. To put this in perspective, that level of R&D investment for a company this size is analogous to a family putting their entire net worth into a single real estate development. If it works, the returns could be transformative. If it does not, the cash burn could be existential.

The strategic logic for why 3S might succeed where larger companies have not tried centers on three factors. First, the HBM4 base die market is inherently fragmented. As AI accelerator designs diversify—with companies like Nvidia, AMD, Google, Amazon, Microsoft, and dozens of startups all developing custom silicon—the demand for customized base dies is growing. The memory giants want design partners who can co-develop base dies tailored to specific processor architectures, and they may prefer working with a small, nimble, deeply technical partner rather than a large design house that has its own competing priorities. Second, 3S's existing relationships with Kioxia (a potential future HBM producer) and Kingston (a potential channel for memory modules) provide a distribution pathway that most startups would spend years building. Third, the engineering culture—the "Process Power" described earlier—means that 3S knows how to co-develop silicon with manufacturing partners in a way that is directly relevant to the base die challenge.

The parallels to the company's original flash controller business are striking. In both cases, 3S is designing the interface chip that sits between a processor and a memory array. In both cases, the value comes from deep understanding of both the memory characteristics and the system requirements. And in both cases, the strategic investors who surround 3S are the same players who need these interface chips to build their own products.

Whether this bet pays off depends on execution and timing. The HBM4 generation is expected to enter volume production in the 2026-2027 timeframe. If 3S can successfully tape out a competitive base die design and secure qualification with one or more memory manufacturers, the revenue potential dwarfs anything in the company's history. But the "if" is enormous. Taping out a complex logic die, achieving first-pass silicon success, qualifying it for production at a major foundry, and then getting it designed into HBM stacks that ship in volume is a multi-year, multi-hundred-million-dollar endeavor. For a company that has struggled to turn a profit on MEMS microphones, the leap to HBM is less a pivot and more a pole vault.

The market, for now, is skeptical. At roughly NT$16.65 per share as of March 2026, the stock trades well below its historical levels, and the price-to-book ratio suggests that investors are assigning minimal value to the HBM optionality. This is either an opportunity or a warning, depending on one's assessment of the probability that 3S can actually deliver.

VI. Playbook: Business and Investing Lessons

The Solid State System story, whatever its ultimate outcome, offers a masterclass in how a micro-cap IC design house can survive in an industry that ruthlessly consolidates around scale. Several lessons stand out.

The first is the power of the strategic minority stake. When Kingston invested in 2008 and Kioxia established its cross-licensing relationship even earlier, they created a web of mutual dependency that protected 3S during years when the company's standalone financials would have made it a prime candidate for dissolution. Most small IC design houses that competed with 3S in the mid-2000s flash controller market no longer exist. They were acquired, merged, or simply shut down as the market consolidated around Phison, Silicon Motion, and a handful of other survivors. 3S survived not because it was the largest or most profitable, but because its strategic investors had a vested interest in its continued existence. Kingston needed an independent controller designer that would prioritize Kingston's requirements. Kioxia needed a partner to develop controllers optimized for Kioxia's NAND flash. For both, a small, dependent 3S was preferable to a large, independent alternative that might become a competitor or deprioritize their needs.

This model—using strategic minority stakes from supply chain partners as a survival mechanism—is replicable and underappreciated. It works because the strategic investors gain something money cannot buy (dedicated engineering attention and supply priority) while the investee gains something scale cannot provide (guaranteed demand and technology access). The arrangement is stable precisely because both sides need each other, and the minority stake ensures alignment without the governance complications of a majority acquisition.

The second lesson involves what Hamilton Helmer would call a "Cornered Resource." In 3S's case, the resource is their proprietary CMOS MEMS process capability. Most MEMS microphone competitors use a two-chip solution: one die for the MEMS sensor (made using specialized MEMS fabrication) and a separate die for the readout ASIC (made using standard CMOS fabrication). The two dies are then packaged together. 3S's approach of deeply integrating the MEMS and CMOS elements—co-developing the manufacturing process to enable tighter coupling—produces devices that are physically smaller and potentially cheaper at scale. The key phrase is "at scale." This Cornered Resource only generates economic value if the company can achieve sufficient volume to amortize the process development costs. So far, that scale has proven elusive, making the Cornered Resource more of a theoretical advantage than a realized one.

The third lesson is about counter-positioning. In Helmer's framework, counter-positioning occurs when an entrant adopts a new, superior business model that the incumbent cannot copy without damaging their existing business. For 3S, the counter-positioning is subtle. By being tiny, 3S can take on custom controller projects—both in flash and potentially in HBM—that the major players simply will not touch. Marvell, Phison, and Silicon Motion focus on high-volume standard products because that is where their scale advantages pay off. A custom controller for a niche application with volumes of a few hundred thousand units per year is not worth their attention. For 3S, with its lean cost structure and small team, that same project can be highly profitable and strategically important, particularly if it deepens a relationship with a major customer.

The fourth and perhaps most sobering lesson is about the cost of pivoting. 3S's stock price decline over the decade following the MEMS pivot is a cautionary tale for investors in any company undergoing a strategic transformation. The technical pivot may be correct—MEMS microphones are indeed a growing market, and 3S's technology is genuinely differentiated—but the financial manifestation of that pivot takes far longer than almost anyone expects. R&D spending ramps up immediately. Revenue from the new product line builds slowly. The legacy business declines on its own timeline, regardless of the new strategy. The result is a multi-year trough during which the income statement looks progressively worse even as the underlying technology and market position are improving. Investors who bought into the MEMS story in 2012 or 2013 have endured more than a decade of losses and capital erosion. Whether they are ultimately rewarded depends on events that have not yet occurred.

The broader investing lesson is that time is the most underappreciated variable in technology pivots. A company can be right about the technology, right about the market, and right about its competitive positioning, and still destroy shareholder value if the timeline extends beyond what the balance sheet can support. 3S has managed to extend its runway through capital reductions, capital increases, and the patience of strategic investors. But the margin for error is thin.

VII. Analysis: Porter's Five Forces, Bull Case, and Bear Case

To assess 3S's competitive position rigorously, it helps to apply the classic frameworks of industry analysis alongside the narrative we have built.

Starting with Porter's Five Forces as applied to 3S's two primary markets—MEMS microphones and the emerging HBM opportunity—the picture is nuanced. The bargaining power of suppliers is high and represents a genuine constraint. As a fabless IC design house, 3S depends entirely on foundry partners for manufacturing. In Taiwan, this means TSMC, UMC, and potentially specialty MEMS foundries. Foundry capacity has been cyclically tight, and smaller customers like 3S often find themselves deprioritized when capacity is scarce. A single foundry allocation decision can make or break a product launch. In the HBM base die space, this supplier power dynamic would intensify, as the base die would need to be manufactured on advanced logic nodes where capacity allocation is even more competitive.

The bargaining power of buyers varies by segment. In MEMS microphones, the major customers—notebook OEMs, smartphone brands, and automotive tier-one suppliers—are enormous relative to 3S and have significant leverage on pricing. They can switch between microphone suppliers with modest redesign effort, which limits 3S's pricing power. In the flash controller segment, the buyer concentration is even more extreme: Kingston alone likely represents a substantial portion of controller revenue. The strategic relationship mitigates the adversarial dynamic, but it also means that 3S's financial health is tied to a handful of key customers.

The threat of substitutes is evolving in interesting ways. In the microphone market, the long-term shift from traditional audio capture to "AI sensing"—where microphones detect not just voice but environmental sounds, machinery health, and even biometric signals—could expand the addressable market significantly. A MEMS microphone that can detect a failing bearing in a factory machine or monitor a patient's breathing patterns is a very different product, sold to very different customers, than a microphone that captures voice for a laptop. If this transition accelerates, 3S's early work in high-performance MEMS could prove prescient. In the HBM space, the relevant substitution threat is architectural: if future AI accelerators move to alternative memory architectures (processing-in-memory, for example), the HBM base die market could shrink before 3S even enters it.

The threat of new entrants is moderate. Designing analog and mixed-signal ICs—whether for MEMS readout or memory interfaces—requires specialized expertise that takes years to develop. The barrier is not capital so much as accumulated knowledge and relationships. However, in the HBM base die space, the new entrants are not startups—they are well-funded design service companies like GUC (Global Unichip Corp, a TSMC subsidiary) and established IP companies that could pivot engineering teams to this opportunity quickly.

Competitive rivalry is intense in both segments. In MEMS microphones, Knowles, Infineon, STMicroelectronics, Goertek, and AAC Technologies all have advantages of scale, brand recognition, and established supply chain positions. In HBM, the competitive landscape includes the memory giants' in-house design teams (SK Hynix, Samsung, Micron all have substantial logic design capabilities), large design service firms, and other niche players attempting similar pivots.

Now, the bull case. It goes something like this: 3S successfully tapes out an HBM4-generation base die in 2026, leveraging its twenty-five years of memory controller expertise and its strategic relationships with Kioxia and other memory players. The die passes qualification, enters production, and 3S becomes one of a small number of companies capable of designing customized HBM logic dies for the rapidly diversifying AI accelerator market. Kingston and Kioxia help with distribution and customer introductions. Revenue inflects dramatically, moving from the current sub-NT$300 million range to multiples of that as HBM volumes ramp. Meanwhile, the MEMS microphone business finds its niche in automotive and AI sensing, providing a stable base while HBM scales. The stock, currently priced for irrelevance, re-rates as a genuine AI infrastructure play. In this scenario, the strategic cap table—the same Kingston and Kioxia stakes that have sustained the company through lean years—become the distribution engine for a transformed business.

The bear case is equally compelling. The HBM R&D investment burns through 3S's limited cash reserves without reaching production readiness. The technical challenges of designing a competitive logic die—one that meets the performance, power, and reliability requirements of the memory manufacturers—prove too great for a team of 120 people. Larger, better-funded competitors capture the opportunity. Meanwhile, the MEMS microphone business continues to struggle against scale players, generating insufficient cash flow to fund the HBM bet. Revenue continues its decline from the NT$692 million peak in 2021. The accumulated deficit grows. Eventually, the company faces another capital reduction or a dilutive capital raise that further erodes existing shareholders. The strategic investors, patient as they have been, eventually conclude that their interests are better served by other partners. In this scenario, 3S remains what it has been for most of the past decade: a technically impressive but commercially marginal player in a market that demands scale.

Between these extremes, the most likely outcome may be a middle path where 3S secures a role as a design partner for specific HBM applications but does not achieve the scale to become a major standalone player. In this scenario, the company might be acquired by one of its strategic investors or by a larger IC design house looking to bolt on HBM design capability.

For investors tracking this story, two key performance indicators matter most. The first is the quarterly revenue trajectory in the audio and MEMS segment. Any meaningful design win—particularly in automotive, where volumes are large and customer switching costs are high—would show up as a step-function increase in this segment's revenue. Watch for quarter-over-quarter acceleration, not just year-over-year comparisons, since the base effects from revenue decline can make percentage growth rates misleading. The second KPI is R&D expense as a percentage of revenue. An increase in this ratio, while normally a negative signal, would in 3S's case indicate continued investment in the HBM program. A decline, by contrast, might signal that the company is pulling back from its most ambitious bet, which would be either prudent capital allocation or a surrender flag depending on the reason. These two metrics—MEMS revenue momentum and R&D intensity—together tell you whether the company is successfully executing on its dual-track strategy or retreating to its shrinking legacy business.

VIII. Epilogue: The AI Sound Sensing Frontier

The semiconductor industry has a saying: every technology eventually finds its application if the engineers are stubborn enough. Solid State System's engineers have been remarkably stubborn.

At trade shows in recent years, including appearances at Computex, 3S has been showcasing an evolution of its MEMS microphone technology that goes well beyond traditional voice capture. The concept is "AI sensing"—using MEMS microphones not merely to record speech but to detect, classify, and interpret environmental and biological sounds. A MEMS microphone with sufficient sensitivity and an accompanying AI inference chip can distinguish between a normal heartbeat and an arrhythmia, between a healthy machine bearing and one about to fail, between a car approaching from the left and a bicycle from the right. This is not science fiction. The sensor hardware already exists; the question is whether the AI algorithms and the system integration are mature enough for commercial deployment.

For 3S, the automotive segment represents the most tangible near-term opportunity in AI sensing. Advanced driver-assistance systems, or ADAS, increasingly rely on multi-modal sensing—combining cameras, radar, lidar, and, increasingly, acoustic sensors to build a comprehensive picture of the driving environment. An array of MEMS microphones on a vehicle can detect emergency sirens before they are visible, identify the direction of approaching vehicles at intersections, and even monitor the driver's physiological state through acoustic analysis. 3S's automotive-grade MEMS microphones, which entered mass production in late 2020 and have secured design wins with major automakers, position the company at the edge of this emerging market.

The company's annual report has referenced promotion efforts toward "brand name car manufacturers" and growing adoption of 3S microphones in automotive applications. While specific customer names and volumes are not publicly disclosed, the automotive qualification process—which requires meeting stringent AEC-Q103 reliability standards and passing extensive validation—creates a meaningful moat once achieved. Automotive design cycles are long, but once a supplier is qualified and designed in, they tend to remain for the life of the vehicle program, which can span seven to ten years.

Looking at the broader picture, Solid State System in March 2026 is a company defined by optionality. The legacy flash controller business, while declining, still generates revenue and maintains the Kingston and Kioxia relationships that are the company's strategic bedrock. The MEMS microphone business has achieved technical credibility and automotive qualification but has not yet reached the scale needed for profitability. And the HBM opportunity—if it materializes—could redefine the company entirely.

The stock, trading at roughly NT$16.65 with a market capitalization around forty million dollars, reflects deep skepticism about all three prongs of this strategy. For those who view 3S as a legacy semiconductor company in structural decline, the price may still be too high. For those who see it as an "option value" play—a cheap lottery ticket on the HBM revolution, backed by strategic relationships with some of the biggest names in memory—the current valuation assigns nearly zero probability to the most transformative outcome.

What is beyond dispute is that Jeffrey Lin, Tim Hu, and their small team have kept this company alive and technically relevant for over twenty-seven years, through multiple technology cycles, competitive upheavals, and near-death financial experiences. Whether the next chapter is triumph or capitulation, the story of Solid State System is a testament to the peculiar resilience of founder-led companies in Taiwan's semiconductor ecosystem—where deep technical conviction, strategic relationships, and sheer stubbornness can keep a company in the game long after the market has written it off.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube