Unimicron Technology: The Invisible Spine of Advanced Semiconductor Packaging

I. Introduction & Episode Roadmap

Picture the inside of an NVIDIA server rack. Everyone talks about the GPU — the H100, the Blackwell B200 — as the beating heart of artificial intelligence. But a bare silicon die cannot talk to a motherboard any more than a human brain can talk to the outside world without a spinal cord. The connections coming off a modern processor are tens of thousands of impossibly fine electrical pathways, packed at a density far finer than any circuit board could ever resolve. Something has to bridge the gap between the microscopic world of the chip and the merely tiny world of the printed circuit board. That something is the IC substrate — a miniature, ultra-high-precision circuit board that sits directly beneath the die, fanning its thousands of connections out to a scale the rest of the system can handle. It is, quite literally, the spine.

The highest-performance version of this spine is built on a material called 味之素 Ajinomoto Build-up Film — ABF — and it is the physical gating item for advanced computing. You cannot deploy an NVIDIA Blackwell, an AMD Instinct MI300, or Apple's custom M-series silicon without high-end ABF substrates underneath them. No substrate, no server. It is that binary. And Unimicron sits at the center of that chokepoint as the world's leading maker of these carriers, a position it has held near the top of the ABF industry alongside Japan's Ibiden and Shinko.23

Why does a coaster-sized rectangle of resin cost more than the silicon it carries? Because the tolerances are unforgiving and the failure modes are merciless. The lines etched into a high-end substrate are measured in single-digit microns — thinner than a red blood cell — and there can be twenty or more layers of them, each perfectly aligned with the one below. A modern AI accelerator package might route tens of thousands of connections through this structure, and if any one of them fails, the entire multi-thousand-dollar chip on top is scrap. The substrate is thus not a passive tray; it is an active, precision-engineered component whose defect rate directly determines whether the most valuable silicon on Earth works or does not. That is why substrate capacity, not chip design, has repeatedly been the true limiting factor in shipping advanced processors — and why a company that most people cannot name sits astride one of the most important chokepoints in modern technology.

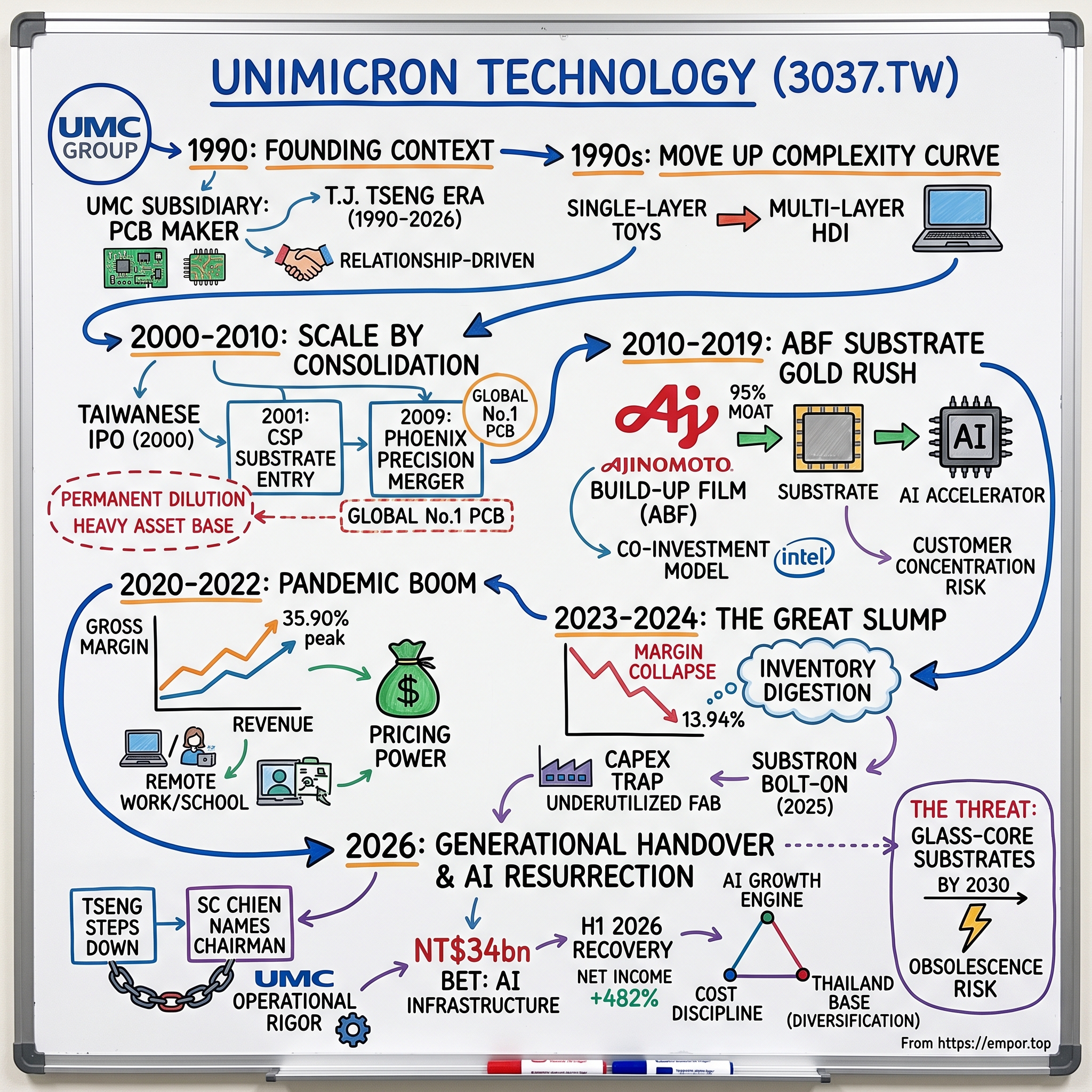

The company arrives at 2026 at a genuine inflection point, and it is worth naming all four pillars of it up front, because the rest of this story is the excavation of each. First, a change of dynasty. In February 2026, the board named a successor to 曾子章 T.J. Tseng, the relationship-driven patriarch who had run Unimicron for decades. His replacement as chairman is 簡山傑 SC Chien, a semiconductor lifer who had been Co-President of 聯華電子股份有限公司 United Microelectronics Corp. (聯電 UMC) — the very foundry group that spawned Unimicron in the first place.2 Chien joined UMC in 1989 and spent more than three decades inside one of the most operationally disciplined manufacturing cultures in Taiwan.3 His mandate reads like a corrective: bring "UMC-style" cost discipline and return-on-capital rigor to a company that had spent years expanding first and counting later.

Second, a financial resurrection. In the first quarter of 2026 — reported on April 28 — Unimicron posted net sales of NT$37.45 billion, up 24.45% year-over-year, with gross margin recovering to roughly 18% and earnings per share of NT$3.28, a thirteen-quarter high.1 Total net income came in at about NT$5.38 billion, up roughly 482% from a deeply depressed base a year earlier (net income attributable to the parent was NT$5.04 billion, up about 452%).1 Those are the numbers of a company climbing out of a hole.

Third, the physics of the AI opportunity — the yield mathematics that make advanced substrates so hard, and therefore so profitable for whoever masters them. And fourth, the threat that could unmake the whole thesis: the industry's flirtation with glass-core substrates, a next-generation technology that could, over time, render tens of billions of dollars of organic-substrate assets obsolete.

Here is the roadmap. We begin in the shadow of Taiwan's foundry miracle, where Unimicron was born as a corporate afterthought. We trace its decade of consolidation, when it rolled up half the Taiwanese board industry and paid for it with shareholder dilution. We follow it into the ABF gold rush and the strange co-investment dance with its largest customers. We live through the pandemic boom that made substrates the scarcest thing in electronics, and the crash that followed. And then we arrive at 2026 — the handover, the AI comeback, and the war-game over what comes next. To understand any of it, we have to go back to the moment a foundry decided it needed to own the boards its chips would sit on.

II. The UMC Group & Founding Context (1990–2000)

In the late 1980s, Taiwan was in the middle of pulling off one of the great industrial magic tricks of the twentieth century. The island had almost no natural resources, a modest domestic market, and a geopolitical status so precarious that most of the world would not formally acknowledge it existed. And yet, out of the 工業技術研究院 Industrial Technology Research Institute (ITRI) — a state-backed research lab in Hsinchu — came the blueprint for an entirely new kind of company: the pure-play foundry, a factory that made other people's chips and never competed with its own customers by designing its own. That model would eventually crown TSMC as one of the most valuable companies on the planet. But TSMC was not the only child of ITRI. Its older sibling was UMC, Taiwan's first true semiconductor company, and it was UMC's ambition that gave the world Unimicron.

To understand Unimicron you have to understand the peculiar corporate ecology of the UMC group in that era. UMC was Taiwan's semiconductor pioneer — spun out of ITRI in 1980, years before TSMC — and it was run with an empire-builder's ambition. Where TSMC would eventually choose the monastic focus of doing one thing, foundry, better than anyone, UMC's culture in the 1980s and 1990s was more expansive, spinning off and investing in a constellation of affiliated companies across the electronics value chain. This was the archipelago into which Unimicron was born: not as a standalone startup with a visionary founder chasing a market, but as a deliberate piece of a larger industrial strategy, a subsidiary created to serve a need the parent had identified.

UMC's leadership understood something early that the pure logic-chip narrative tended to obscure: a transistor is only as useful as the packaging that connects it to the rest of the machine. Silicon lives in a clean, microscopic realm; the everyday world of motherboards and power supplies is comparatively coarse. Between the two sits the humble printed circuit board and, later, the far more demanding IC substrate. If you were building a vertically integrated electronics empire, you did not want to be at the mercy of outside board suppliers for the physical scaffolding of your chips.

So in January 1990, UMC reorganized an existing electronics operation — a predecessor entity — into a new company to handle printed circuit boards for the group. That company was Unimicron.6 Its first job was decidedly unglamorous: make the boards that the UMC ecosystem needed, at volume, at cost. This was not a moonshot. It was infrastructure. And the man handed the keys was T.J. Tseng, who would spend the next thirty-six years turning a captive board shop into a global substrate power.

The patriarch and his method

Tseng belonged to a generation of Taiwanese industrialists whose competitive edge was as much social as technical. His management style was relationship-driven to its core — he cultivated customers personally, over years, in the way a Japanese keiretsu executive might, and he was famously willing to make big, early, capacity bets on the strength of a trusted relationship rather than a spreadsheet. In a commodity business where the winner is often simply whoever has qualified capacity ready when the customer needs it, this instinct for aggressive pre-building was, for a long time, an asset. It is also, as we will see, the exact instinct that SC Chien was hired to rein in. The seeds of the 2026 leadership philosophy were planted in the founding culture of 1990.

From toys to computers

The strategic pivot of the first decade was a move up the complexity curve. In the early 1990s, the bottom of the PCB market — the single-layer boards inside toys, remote controls, and cheap appliances — was a race to the floor, a place where Taiwanese and later mainland Chinese fabs competed almost entirely on price. Unimicron's ambition was to climb out of it toward High-Density Interconnect boards, or HDI: multi-layered, finely patterned boards that could handle the denser, faster chips going into personal computers. HDI required more process control, tighter tolerances, and cleaner manufacturing — which meant fewer competitors and better margins. Over the 1990s, Unimicron built a reputation as a reliable, high-volume board supplier for the PC era, riding the same personal-computing wave that was making Taiwan the workshop of the digital world.

There is a deeper strategic lesson in this early climb, and it is worth pausing on because it recurs throughout the company's history. Unimicron's competitive method has never been to invent a category. It has been to identify where the industry is heading, then get there at scale a little before its rivals and with better process control once it arrives. That is a fundamentally different kind of company from a technology pioneer. It is a manufacturing company, and manufacturing companies win on cost, yield, capacity timing, and capital access — not on patents or brand. It means Unimicron's fortunes are tied less to any single breakthrough than to its ability to keep climbing the complexity ladder faster than the commoditization wave rising beneath it. When it climbs fast enough, it earns high-end margins; when the wave catches up, its products become commodities and its margins compress. Hold that mental model, because it explains every boom and every bust in the pages that follow.

By the end of the decade, Unimicron had done something quietly important: it had established that a UMC-affiliated board maker could scale. What it had not yet done was become a giant. That transformation would not come from making better boards. It would come from buying its rivals. And the vehicle for that — a Taiwanese initial public offering in January 2000 and a decade of aggressive mergers — is where the Unimicron story shifts from steady climber to industry consolidator.24

III. Scale by Consolidation: The Great Taiwanese PCB Consolidator (2000–2010)

If the 1990s were about learning to make boards, the 2000s were about learning to swallow other companies whole. And here the story acquires a distinctly Taiwanese flavor: this was not the hostile, activist-driven M&A of Wall Street, but the patient, group-orchestrated consolidation of an industrial family. UMC sat at the head of the table, and it decided that its scattered board and packaging affiliates were worth more welded together than apart.

The first big move came in 2001. UMC engineered a consolidation of several of its board and substrate affiliates, with Unimicron as the designated survivor. The deal had begun life as an even larger four-company combination, but one partner dropped out during negotiations, and what actually closed around October 2001 folded a set of affiliated entities — including operations that brought chip-scale package (CSP) substrate technology and capacity — into Unimicron.7 This is the moment that matters analytically, because it was Unimicron's first real step off the printed circuit board and onto the IC substrate: the carrier that sits under an actual packaged chip. The company had crossed the border from making boards for systems to making substrates for semiconductors. It also gained meaningful manufacturing scale, including a growing footprint in mainland China, where the Suzhou operations would become a high-volume hub for the group.

But the transaction that truly defined the decade — and cast the longest shadow over Unimicron's financials — came in 2009.

The Phoenix Precision gamble

The 2008 global financial crisis had brutalized the semiconductor supply chain, and among the wounded was 全懋精密科技股份有限公司 Phoenix Precision Technology Corp., a serious Taiwanese IC-substrate maker. In December 2009, Unimicron absorbed Phoenix Precision through a share-swap merger, and in doing so became the largest PCB company by capital on the entire Taiwan stock market.7 On paper, it was a triumph. Unimicron had consolidated its domestic competition and vaulted itself into the front rank of high-end IC substrates. Indeed, in 2009 and 2010, Unimicron briefly ranked as the world's number-one PCB producer.6

Why did Unimicron want Phoenix Precision badly enough to do the deal at the bottom of a crisis? Because the crisis was the opportunity. Phoenix was a genuine IC-substrate specialist — precisely the high-end capability Unimicron had been building toward since the 2001 CSP move — and the 2008 collapse had left substrate makers everywhere cash-starved and cheap. Buying a wounded specialist in a downturn is, in theory, textbook counter-cyclical capital allocation: acquire capability when it is on sale, integrate it while demand is slack, and emerge from the recession with a stronger hand. The instinct was sound. The execution, and the currency used to pay for it, are where the story gets more complicated.

And here is where an independent analyst has to be honest about what a share-swap merger actually does. When you pay for a company by printing your own shares rather than spending cash, you are handing the acquired company's owners a slice of your future earnings forever. If the assets you buy are high-yielding, that is a fine trade. If they are not, you have permanently diluted your existing shareholders to acquire capital overhead. The Phoenix Precision deal brought Unimicron scale and technology, but it also brought legacy fabs, older process lines, and a heavier capital base that had to be sweated for years before it earned its keep. In the decade that followed, Unimicron's return on equity and asset turnover were persistently unremarkable — the tell-tale fingerprint of a company carrying more assets than its earnings could comfortably justify. The consolidation made Unimicron big. It did not, for a long time, make it efficient. That distinction — bigness versus efficiency — is the exact fault line the 2026 management change would try to correct, which is why the Phoenix deal is not ancient history but the opening chapter of a governance argument that is still live today.

Reading the strategy

Step back and the logic of the decade is clear enough. Taiwan's board industry in 2000 was fragmented, and a fragmented industry in a capital-intensive, cyclical business is a value-destroying industry — everyone over-invests in the good times and bleeds in the bad. UMC's consolidation thesis was that scale would bring pricing stability, purchasing power, and the balance-sheet heft to fund the next technology transition. That thesis was half right. Unimicron did get the scale, and it did get a seat at the high-end substrate table just as the industry's center of gravity was about to shift toward a new material born, improbably, in a Japanese food laboratory. But it paid for that seat with a diluted share count and a stubborn drag on capital returns — a bill that would come due, over and over, every time the cycle turned. The next act is about the material that made the high end worth fighting for.

IV. The ABF Substrate Gold Rush & The Co-Investment Era (2010–2019)

Every so often a company stumbles into a monopoly by accident, in a business it never meant to enter. That is the story of how a Japanese seasoning giant came to control the single most critical material in high-performance computing.

味之素 Ajinomoto is best known for inventing monosodium glutamate — MSG, the umami seasoning that sits in kitchens across Asia. In the course of its amino-acid chemistry, Ajinomoto's researchers developed an insulating film derived from that same chemical heritage, and in 1999 they commercialized it as Ajinomoto Build-up Film. It turned out that this film had near-magical properties as a dielectric layer for high-frequency semiconductor packages: low electrical loss, fine patterning, and the ability to be stacked in many build-up layers. Today, ABF sits underneath virtually every high-performance CPU, GPU, and server chip in the world, and Ajinomoto holds something on the order of 95% of that market — a monopoly so complete that the entire advanced-computing industry depends on a single company's specialty film.10 It is one of the strangest supply-chain facts in technology: the AI boom runs on a byproduct of the seasoning business.

Why has no one dislodged Ajinomoto in more than two decades? The answer reveals something about how deep moats can run in materials science. ABF is not a simple polymer; it is a precisely tuned formulation whose electrical, mechanical, and thermal behavior must remain stable across brutal manufacturing conditions and years of field use. The substrate makers who buy it have qualified their entire production processes around its exact properties, and requalifying an alternative film would ripple through every downstream customer's own qualification. That creates a self-reinforcing lock-in: Ajinomoto's dominance makes it the default, being the default deepens the ecosystem's dependence, and the dependence raises the cost of ever switching. It is a cornered resource in the truest sense — and, as we will see, the one genuine vulnerability sitting underneath Unimicron's otherwise formidable position.

BT versus ABF, in plain terms

To see why this mattered so much to Unimicron, you need the one technical distinction at the heart of the substrate business. There are two great families of organic substrate material. The first is BT — bismaleimide-triazine resin — a rigid, cost-effective material used in the thin, low-power packages inside smartphones, memory modules, and RF components. The second is ABF, which is used for the big, hot, high-layer-count packages that sit under CPUs and GPUs. The simplest way to think about it: BT is for chips that sip power in your pocket; ABF is for chips that guzzle power in a data center.15 As computing shifted toward ever-more-powerful processors, ABF became the high-margin frontier, and the makers who could produce it at high yield — Unimicron, Ibiden, Shinko, AT&S, Nan Ya PCB — became a small, defensible club.

The co-investment dance

There is a peculiar economic feature of high-end substrate manufacturing that shaped Unimicron's relationships with its biggest customers: it is savagely capital-intensive, and the learning curve is brutal. When a substrate maker begins producing a new, high-layer-count design, yields can start dismally low — a large fraction of early production simply fails, warped or cracked or mis-registered — and it can take many months of process refinement to climb toward profitability. That combination — enormous upfront capital plus a slow, uncertain yield ramp — creates a coordination problem. The chipmaker desperately needs guaranteed capacity years before its product launches; the substrate maker cannot justify building a dedicated fab on a handshake.

The solution the industry evolved was co-investment: chipmakers pre-funding or otherwise underwriting a substrate maker's advanced capacity in exchange for dedicated, priority access. Unimicron's most visible example was a new plant at Yangmei, built specifically to produce ABF substrates for Intel, with production slated to begin in early 2022.11 The arrangement solved the coordination problem, but it introduced a different vulnerability that is fundamental to Unimicron's business model: customer concentration. When you build a dedicated line for one giant customer, your fortunes are welded to that customer's roadmap. If the customer's product slips — and in the semiconductor industry, products slip all the time — your expensive new line sits underutilized, its depreciation grinding away at your income statement regardless of whether a single unit ships. The co-investment model transfers demand risk only partway; the capacity, and the fixed costs that come with it, still live on Unimicron's balance sheet.

There is a subtler point here about who really bears risk in these arrangements, and it is worth drawing out because it recurs in 2026. Co-investment and prepayment sound like the customer taking on risk — the chipmaker fronting cash to guarantee supply. But look closely and the substrate maker is still the one holding the durable asset and its depreciation. The customer's prepayment is a claim on future product; the fab, once built, is Unimicron's problem for a decade regardless of what the customer does. So the model shifts near-term demand risk onto the customer while leaving long-term asset risk with Unimicron. In a rising market, that is a wonderful deal — you get funded to build capacity you would have wanted anyway. In a falling market, the prepayments run out, the take-or-pay commitments get renegotiated or quietly lapse, and you are left holding fabs. This asymmetry is the hidden engine beneath Unimicron's violent earnings swings.

That structural exposure — concentrated customers, dedicated capacity, punishing fixed costs — is the reason Unimicron's earnings swing so violently with the cycle. It is a company whose costs are largely fixed and whose revenues are entirely cyclical. For most of the 2010s, that tension was manageable. Then came a pandemic, and the tension snapped in Unimicron's favor so hard that for about two years it looked like the company had escaped the cycle altogether. It had not.

V. The Pandemic Boom, The Chip Shortage, & The CapEx Trap (2020–2022)

In the spring of 2020, as the world locked its doors, something happened that no substrate planner had modeled: overnight, a few billion people needed a second screen. Remote work, remote school, remote everything drove an unprecedented surge in demand for laptops, PCs, monitors, and the data-center capacity to serve them all. And every one of those machines needed chips, and every one of those chips needed a substrate.

For Unimicron, the timing was extraordinary. The demand surge collided with an industry that had spent the prior decade being disciplined about ABF capacity — no one had built ahead of a pandemic no one saw coming. The result was that IC substrates, and ABF substrates in particular, became the physical bottleneck of the entire semiconductor supply chain. Lead times stretched to extraordinary lengths, and the power dynamic between substrate maker and chipmaker inverted completely. Where Unimicron had once courted Intel and Apple, now the chip giants were the supplicants, flying executives to Taoyuan to plead for capacity allocations. Management publicly warned that tight supply would persist for years.12

The economics of scarcity

When a commodity supplier suddenly holds the scarce resource, the economics become spectacular, and Unimicron's financials tell the story with unusual clarity. Consolidated gross margin — the purest measure of pricing power in a manufacturing business — vaulted to a historic peak of 35.90% in 2022.22 For a company whose margins had spent the 2010s stuck in the mid-teens, this was a transformation so complete it looked like a different business. Revenue swelled to roughly NT$140 billion, and net profit reached a scale the company had never approached before. For a brief, heady window, the market began to wonder whether Unimicron had graduated from cyclical board-maker to structural bottleneck baron.

It is worth translating what a margin like that actually means for the business, because the abstraction hides the drama. Gross margin is the share of every dollar of sales left after the direct cost of making the product. When it more than doubles from the mid-teens to the mid-thirties, it means Unimicron was selling substrates for far more than it cost to make them — not because the substrates were suddenly cheaper to produce, but because customers, desperate and unable to source elsewhere, simply paid whatever was asked. That is the signature of genuine, if temporary, pricing power. And pricing power that flows from scarcity rather than from a durable moat is the most dangerous kind, because it evaporates the instant the scarcity does. Management, and the market, had to decide in 2021 and 2022 whether the pricing power was structural or borrowed. The company's capital spending revealed which way it bet.

But there is a trap buried inside a boom like this, and it is a trap that this industry falls into with almost clockwork regularity. When your customers are begging for capacity and offering long-term agreements and cash prepayments to fund it, the temptation to build — aggressively, enormously — is nearly irresistible. Unimicron did exactly that, pouring capital into new plants, including advanced fabs whose depreciation would begin the moment they were switched on. Capital expenditure peaked at roughly NT$32 billion in 2022. The company was, in effect, betting billions that the pandemic demand curve was the new normal.

The Subtron consolidation

Amid the boom, Unimicron also moved to tidy up its corporate family. In February 2022, it announced a share-swap merger to fully absorb its long-time affiliate 旭德科技股份有限公司 Subtron Technology Co., Ltd., offering 0.219 Unimicron shares for each Subtron share — a premium of roughly 26%.8 Subtron's value was specialization: it was heavily weighted toward System-in-Package substrates, which made up the bulk of its business, along with expertise in RF and Mini-LED substrates — niches where Subtron had, in Tseng's own framing, "walked its own path" into products Unimicron did not itself make.8 The merger, which was later restructured and took effect on January 1, 2025, was a targeted bolt-on: it deepened Unimicron's position in specialty packaging and diversified it modestly away from pure PC-and-server exposure. As acquisitions go, it was small, strategic, and far less dilutive than the Phoenix Precision epic of 2009 — arguably a sign of a company learning, slowly, to be more surgical with its share count.

But surgical bolt-ons could not change the fundamental physics of what Unimicron had just done. It had built enormous capacity into the teeth of a demand spike, and advanced substrate fabs take two to three years to build and qualify. Which meant that Unimicron's biggest pandemic-era capacity was scheduled to come online at precisely the moment the pandemic demand evaporated. The bill for the boom was about to arrive, and it was enormous.

VI. The Great Slump: 2023–2024 Inventory Digestion

The hangover began in late 2022, and it was one of the worst the PC industry had ever recorded. As economies reopened and the pull-forward of pandemic buying exhausted itself, personal-computer demand did not merely soften — it collapsed. Global PC shipments posted a record year-over-year decline in the fourth quarter of 2022, the steepest drop the industry had seen in decades.13 Every laptop that did not get built was a substrate that did not get ordered. And sitting in warehouses up and down the supply chain was a mountain of inventory that customers had frantically over-ordered during the shortage, terrified of being caught short. Now they stopped buying entirely and worked down what they had. The industry calls this "inventory digestion," which is a polite term for a period in which your customers buy almost nothing while they eat through their own stockpiles. For ABF substrates, that digestion stretched deep into 2024.14

The math of a margin collapse

Watch what happened to the single most revealing number in this business. Consolidated gross margin, which had peaked at 35.90% in 2022, fell to 19.52% in 2023, then collapsed to 14.14% in 2024, and slipped again to 13.94% in 2025.225 In two years, Unimicron gave back essentially the entire margin gift of the pandemic and returned to the mid-teens grind of the pre-boom era. This is the whole cyclical thesis of the company written in a single line: the margins are borrowed from the cycle, not owned by the company.

But the crash was worse than a demand story alone would suggest, because of the trap laid in the prior chapter. Remember all those fabs Unimicron built at the peak — the ones whose depreciation begins the instant they power on? They came online into the teeth of the downturn. So Unimicron was now carrying the fixed costs of pandemic-scale capacity while running that capacity at low utilization. Massive depreciation charges from newly built plants landed on the income statement precisely when there was too little revenue to absorb them. This is what operating leverage looks like in reverse: in the boom, every incremental sale drops almost entirely to profit; in the bust, the fixed costs stay fixed while the revenue falls away, and operating income gets crushed from both sides. It is the defining hazard of any business that must pour billions of concrete and equipment years ahead of the demand it hopes to serve.

The cruelty of the timing deserves emphasis, because it is the heart of the cyclical curse. A substrate fab is not a light switch. From the decision to build to the point of qualified, high-yield volume production runs two to three years — the planning, the construction, the equipment installation, the agonizing yield ramp. That lag means the industry is structurally incapable of matching supply to demand in real time. Capacity decisions made at the euphoric peak of 2021 and 2022 could only bear fruit in 2023 and 2024 — which is to say, capacity conceived in a shortage was born into a glut. Every major substrate maker faced the same trap simultaneously, which is precisely why downturns in this industry are so brutal: everyone over-builds at the same time and everyone's new capacity floods the market at the same time. It is a coordination failure baked into the physics of the manufacturing lead time, and no amount of individual corporate cleverness fully escapes it.

The survival playbook

Faced with this, management reached for the standard downturn toolkit, but with a strategic twist that would prove decisive. It delayed non-essential capital spending. It began scrutinizing underperforming affiliates, including flexible-PCB maker 同泰電子科技股份有限公司 Tongtai Technologies Co., Ltd., whose weak returns made it an obvious candidate for restructuring. And — critically — it began redirecting whatever capacity and capital it could toward the one corner of the technology economy that was not merely surviving the downturn but exploding through it: artificial intelligence. By mid-2025, Unimicron was publicly reorienting its ABF business toward CoWoS-class advanced-packaging clients — the substrates that sit beneath AI accelerators — even as its legacy PC-substrate demand languished.16

This pivot is the hinge of the entire modern Unimicron story. The company that had been nearly drowned by the collapse of PC demand discovered that the very same advanced-substrate capabilities it had built for CPUs were exactly what the AI wave required — only in larger sizes, higher layer counts, and at yields that only a handful of firms on Earth could achieve. The slump had been a near-death experience. What came next would test whether Unimicron could convert survival into a genuine second act — and it would arrive alongside the most significant leadership change in the company's history.

VII. 2026: The Generational Handover & The AI Resurrection

For thirty-six years, Unimicron had been, in a meaningful sense, one man's company. T.J. Tseng had built it from a captive board shop into a global substrate power through the force of relationships, instinct, and an appetite for capacity bets. So when the news came in February 2026 that Tseng was stepping down as chairman upon reaching retirement age, it was not merely a personnel change. It was the end of an era — and, in the eyes of many investors, the beginning of an overdue reckoning with how the company allocated capital.9

The mechanism of the change was itself revealing. Unimicron remained tied to the UMC group, and it was a representative change by UMC, acting as a corporate director, that formally triggered the succession.9 On February 24, 2026, the board named its new chairman: SC Chien.2

Who is SC Chien?

If you wanted to design a leader to be the anti-Tseng, you might well arrive at Chien. He was not a board man; he was a chip man. He had joined UMC in 1989 and spent more than three decades inside the foundry, rising to Co-President with responsibility for the core of the business — manufacturing operations and technology R&D.3 UMC's culture is the opposite of relationship-first improvisation; it is a culture of yield obsession, cost accounting, and disciplined return on invested capital, forged in the brutal economics of the foundry business where a fraction of a percentage point of yield separates winners from casualties. Chien's entire career was spent learning to extract maximum output from expensive assets. That is precisely the skill Unimicron's balance sheet had been crying out for.

There is a neat historical symmetry in the appointment that is easy to miss. Unimicron was born, in 1990, as a piece of the UMC empire. Thirty-six years later, when the founder-era leadership reached its end, it was UMC — still a corporate director of the company — that reached back in and installed one of its own most senior operators at the top. In one sense this is simply parent-company governance asserting itself. In another, it is a statement of philosophy: the group appears to have decided that Unimicron's next phase should be defined less by the dealmaking and relationship-cultivation that built it and more by the operational rigor that defines UMC itself. Whether that transplant takes — whether a foundry operator's instincts translate cleanly to the different rhythms of the substrate business — is one of the genuine open questions of the 2026 story. Cultures do not always graft.

The market read the appointment as a signal that the era of expansion-first was over and an era of efficiency-first had begun. And Chien wasted little time demonstrating it. In March 2026, he moved to consolidate control over the troubled Tongtai subsidiary, becoming its chairman directly — a hands-on move to grip an underperforming affiliate rather than let it drift.20 This is exactly the kind of decisive intervention a return-on-capital-minded operator makes: you do not delegate the fixing of your worst assets; you own it personally.

"UMC-style" management, in practice

The clearest early evidence of the new philosophy is in how the company chose to spend money in 2026 — and how much. Rather than pulling back capital entirely, the board actually raised 2026 capital expenditure, in a third successive increase, to NT$34 billion (up from an earlier plan of NT$25.4 billion).4 But — and this is the crucial distinction from the pandemic-era spending spree — the money was pointed with precision. The spending was concentrated on high-end ABF substrate expansion for AI, on advanced AI system boards, and on building a new production base in Thailand.4 This is not spray-and-pray capacity expansion; it is targeted deployment into the only demand pool with structural growth. Whether it stays disciplined as the cycle heats up is the open question — aggressive capital allocation after promises of discipline is exactly the pattern skeptical investors watch for — but the stated intent marks a genuine break from the past.

The Thailand base folded into that 2026 plan deserves a note of its own, because it addresses a risk that has nothing to do with substrates and everything to do with maps. Virtually all of Unimicron's advanced capacity sits in Taiwan, an island whose geopolitical status injects a permanent discount into every hardware company domiciled there — the market's shorthand for the small-but-nonzero chance that the Taiwan Strait becomes a flashpoint. Unimicron's largest customers, the American chip giants, have grown increasingly vocal about wanting supply-chain options outside the first island chain. A Thai production base does not move the company's center of gravity, and it will not for years. But it is the first concrete step toward giving customers a non-Taiwan source of supply, and in an era where "where is it made" has become a boardroom question rather than a purchasing footnote, that optionality has strategic value beyond the units it will ship. It is, in miniature, the same pattern reshaping the whole semiconductor supply chain: diversification bought at the price of efficiency, because concentration has stopped feeling safe.

The physics of AI packaging — and why it is a moat

To understand why Unimicron's advanced-substrate capability is so valuable, you have to sit with one piece of manufacturing physics, because it is the entire competitive story. Advanced packaging — TSMC's CoWoS, Intel's EMIB, and their kin — works by placing multiple silicon dies (a GPU, stacks of high-bandwidth memory) side by side on a single large substrate, so they can communicate at enormous speed over very short distances. To do that, the substrate has to be big — growing from roughly 50 or 70 millimeters on a side toward 100 millimeters and beyond — and it has to carry many build-up layers, twenty or more, to route the staggering number of connections.

Here is the killer: substrate yield falls off a cliff as area and layer count rise. Think of it like printing a newspaper where a single smudged letter anywhere ruins the whole page. Double the page size and add more pages, and the odds that something goes wrong somewhere climb relentlessly. A substrate design that yields, say, 90% at ten layers might yield well under half that at twenty layers on a much larger panel. Every additional layer and every additional square millimeter multiplies the ways the part can warp, crack, or mis-register. The dominant enemy is warpage: when you bond rigid silicon onto an organic substrate and heat the whole assembly, the two materials expand at different rates — a mismatch in what engineers call the coefficient of thermal expansion — and the sandwich bends. Control that bending across a large, thick, many-layered part, at volume, at a yield you can make money on, and you have something very few companies on Earth can replicate.

That is the moat, and it is not written down anywhere. It lives in the accumulated, hard-won process knowledge of managing material stresses — the "unwritten recipe," refined over decades of failures. A new entrant with a checkbook can buy the equipment; it cannot buy the years of yield-learning that separate a profitable line from a scrap heap. This is why the AI-substrate club is so small, and why Unimicron's decades in the trade convert, in this specific moment, into pricing power.

There is a useful way to see the economics of yield in this business. Imagine two suppliers making the identical high-layer AI substrate. One achieves 60% yield; the other, having climbed the learning curve longer, achieves 75%. On paper the gap sounds modest. But because so much of the cost — the ABF film, the labor, the machine time, the energy — is sunk into every panel whether it passes or fails, the higher-yield supplier's cost per good unit can be dramatically lower, and its effective capacity from the same physical plant meaningfully larger. In a market where good units are scarce and command premium prices, that yield edge translates directly into both fatter margins and more sellable output. This is why "we have capacity" and "we have profitable, high-yield capacity" are entirely different statements — and why the incumbents' experience advantage is so hard for a well-funded newcomer to erase quickly. The learning curve is the moat, and the moat compounds with every generation of harder parts.

The payoff — and the caveat

The first-quarter 2026 results are the evidence that the AI pivot is translating into operating leverage. Gross margin back to around 18%, revenue up more than 24%, earnings at a multi-year high, net income up several-fold off the depressed base.1 After the trauma of 2023–2024, this is a genuine and rapid recovery, and it validates the thesis that high-value AI substrates carry very different economics from commodity PC boards.

The independent caveat is equally important: an 18% gross margin, impressive as the rate of improvement is, remains only half of the 35.90% the company earned at the 2022 peak. This is a recovery, not a return to the golden age — and it is being driven, at least in part, by the same industry-wide capacity tightness that once inflated and then destroyed the company's margins. The question the next two chapters must answer is whether this recovery rests on a durable structural moat or on another cyclical updraft that will, in time, reverse. To answer it, we have to war-game the competitive position directly.

VIII. Strategic Moats & The 7 Powers Analysis

Strip away the AI excitement and the leadership drama, and the investor's real question is coldly structural: does Unimicron possess durable competitive advantages, or is it a fixed-cost commodity producer that happens to be enjoying a good cycle? Hamilton Helmer's 7 Powers framework is a useful scalpel here, and Unimicron scores unusually well on several of its powers — with one glaring vulnerability.

Scale economies — strong. A modern high-end ABF substrate fab costs billions to build and qualify, and that capital intensity is itself a barrier: only a handful of firms can afford to play. But the deeper scale advantage is the one described in the last section — the yield learning curve. Cumulative production volume generates process knowledge that lowers cost and raises yield, and a competitor starting from behind faces not just a capital gap but an experience gap that money alone cannot close quickly. Unimicron's standing near the top of the global ABF hierarchy, in a club of roughly five makers, reflects this dynamic.23

Switching costs — high. Substrates are not off-the-shelf parts; they are co-designed with the chipmaker years in advance of a product launch, and qualifying a new substrate source for a high-end part can take twelve to eighteen months of joint engineering. Once a design is qualified and ramping in volume, switching to a rival supplier means re-qualifying, re-testing, and risking a yield stumble on a product already in market — an expensive and dangerous proposition. That inertia protects incumbent share on any given design and gives Unimicron a stickiness that pure price competition would not.

Process power — very strong. This is Unimicron's deepest power, and it is essentially the warpage-and-CTE mastery described earlier. The engineering IP required to bond thin silicon onto large organic substrates without cracking or bending is proprietary, tacit, and jealously guarded. It cannot be reverse-engineered from a finished part, and it does not walk out the door easily. In a business defined by yield, whoever holds the recipe holds the margin.

Cornered resource — not Unimicron's, but its supplier's. This is the framework's warning label. The one genuinely cornered resource in the ABF value chain is not held by Unimicron at all — it is held by Ajinomoto, which controls roughly 95% of the build-up film.10 For Unimicron, this is not a power; it is a dependency and a vulnerability. Every high-end substrate it makes rests on a material it does not control and cannot substitute, sourced from a single company. It is the sort of concentration risk that never matters until, one day, it suddenly does.

Porter's Five Forces, briefly

Layer Porter's framework on top and the picture sharpens. Supplier power is extreme on the ABF dimension, for the reason just given — Ajinomoto's near-monopoly is the single most uncomfortable fact in the supply chain. Buyer power is high but balanced: Unimicron's customers are a concentrated set of giants — NVIDIA, AMD, Intel, Apple, TSMC and the major OSATs — any one of which is large enough to hurt, yet the scarcity of qualified high-end capacity forces even these behemoths to sign long-term agreements and, increasingly, to underwrite capacity through prepayments. In 2026, Intel publicly floated exactly this kind of substrate-prepayment mechanism for its EMIB packaging, with multiple Taiwanese and Japanese suppliers reportedly sought for commitments — a live illustration of buyers being compelled to fund the capacity they depend on.21 Rivalry is real but disciplined, confined to that small club of ABF makers; the very capital intensity that keeps new entrants out also keeps the incumbents rational, since no one benefits from a price war in a business where everyone's costs are mostly fixed and everyone remembers 2023. And the threat of substitutes — the one force pointed straight at Unimicron's heart — comes from a different material entirely: glass. That threat is serious enough to warrant its own place in the bear case, which is where we turn next.

Myth versus reality

Before the bear and bull cases, it is worth puncturing two comfortable narratives that circulate about this company. The first myth is that Unimicron is a "pure AI play" — a clean bet on artificial-intelligence infrastructure. The reality is more mixed: a large share of its business remains conventional PCBs and lower-end substrates tied to PCs, handsets, and general electronics, which is exactly why its blended gross margin sits near the mid-teens rather than at AI-substrate economics. The AI exposure is the growth engine and the margin story, but it does not yet define the whole company, and the legacy base is both a drag on returns and a source of the cyclicality that periodically swamps the AI narrative. The second myth is that Unimicron's leadership in ABF is permanent and uncontested. The reality is that it leads a close pack — Ibiden, Shinko, AT&S, Nan Ya PCB are all real, well-capitalized rivals — and that its "world's largest" laurels date to a specific historical peak around 2009 and 2010, not to an unbroken reign.623 Leadership in this industry is a rolling contest re-run with every technology node, not a title held for life.

IX. Analysis & Bear vs. Bull Case (Investor Stress Test)

Every cyclical capital-intensive company invites two coherent and opposite stories. The discipline of investing here is holding both in your head at once, and then watching the specific evidence that would tip the balance one way or the other.

The bull case

The bull case is elegant in its simplicity: Unimicron is a structural tollbooth on high-performance computing. If AI infrastructure spending is a multi-year build-out rather than a one-year spike, then demand for large, high-layer-count ABF substrates grows structurally, and the small club of firms that can make them at profitable yield captures durable pricing power. On this reading, the process-power and scale moats described above are not cyclical accidents but genuine, widening advantages, and the yield mathematics of ever-larger AI packages actively raises the barrier to entry over time — the harder the part is to make, the fewer companies can make it.

The management-and-capital leg of the bull case is the SC Chien thesis: that UMC-style discipline will finally break Unimicron's decades-long habit of dilutive, margin-diluting expansion, lift return on invested capital, and prune the low-margin legacy PCB and underperforming-affiliate drag that has weighed on returns since the Phoenix Precision era. And the geopolitical leg is the new Thailand base, which begins — modestly — to address the "everything in Taiwan" concentration risk that hangs over every Taiwanese hardware name, offering customers a measure of supply-chain diversification away from the Strait.4

It is worth being concrete about why the AI substrate is a fundamentally better business than the PC substrate that preceded it, because this is the crux of the structural-versus-cyclical debate. A PC-CPU substrate is, relatively speaking, a mature, standardized part made in enormous volumes, where competition grinds margins toward the cost of production over time — the classic commoditization wave catching up with the climber. An AI-accelerator substrate is larger, more complex, produced in a design cycle that changes fast, and gated by yields that only a few firms can achieve. As long as the AI chip roadmap keeps demanding bigger packages and more layers, the complexity frontier keeps moving, and the climbers who stay ahead of it keep earning frontier margins. The bull's deepest claim is not merely that AI demand is large; it is that AI demand keeps the complexity rising fast enough that commoditization never catches up. If that is true, Unimicron has finally found a product where its structural manufacturing method — climb the ladder faster than the wave — pays off durably rather than fleetingly.

The bear case — the activist's stress test

Now the other side, and it is not weak.

The glass substrate disruption. This is the existential item. In September 2023, Intel publicly announced industry-leading glass-core substrates for advanced packaging, promising dramatically higher interconnect density and far better dimensional stability than organic substrates, with complete glass solutions targeted for the latter part of the 2020s.17 Glass does not warp the way organic material does — it is, in principle, a superior platform for exactly the large, high-density AI packages that are Unimicron's growth engine. The industry consensus is that glass-core substrates arrive in volume before 2030.18 Unimicron is not standing still: it is building its own through-glass-via pilot line, with sample validation reached in early 2026 and batch equipment installation targeted around late 2026, though management guides that its glass line only stabilizes in the second half of 2026 and that mass production is unlikely before roughly 2028.19 But here is the bear's sharpest point: a technology transition of this magnitude demands enormous new capital, and it threatens to strand the multi-billion-dollar organic-ABF asset base Unimicron is right now spending NT$34 billion to expand. The company could win the organic race and still lose the war if the finish line moves to glass. Every dollar poured into organic capacity in 2026 is a dollar exposed to obsolescence risk if glass arrives faster than expected.

Cyclicality, again. The second bear argument is that we have seen this movie. A capacity boom into a demand spike is exactly what produced the 2023–2024 catastrophe. The NT$34 billion of 2026 capex, however well-targeted, is being deployed into an AI infrastructure wave whose durability is unproven. If AI capital spending plateaus — if the hyperscalers digest their build-out the way PC buyers digested theirs in 2023 — Unimicron's fixed costs will once again outrun its revenues, and the reverse-operating-leverage machine will grind in the wrong direction. The company's entire history is a warning that its margins are borrowed from the cycle.

The capital-allocation record. The third argument is about trust, and it is the one an activist would press hardest. Unimicron's history of share-swap dilution — Phoenix Precision above all — dragged down asset turnover and shareholder returns for the better part of a decade. Management is promising discipline under new leadership, but it is simultaneously raising capex three times in a single year. Promises of restraint accompanied by aggressive spending are precisely the combination that warrants skepticism rather than applause. The correct posture is to withhold judgment until the discipline shows up in the numbers — in returns on capital, not in press-release language. SC Chien's credibility will be earned or lost on whether ROIC actually improves through the next full cycle, not on his UMC pedigree.

The balance-sheet undertow. One more item belongs in the skeptic's file, and it is quieter than glass but no less real: how the spending has been funded. Through the downturn years, Unimicron's capital expenditure ran well ahead of the cash its operations generated, and the gap was bridged with borrowing — the company took on meaningful new debt while its earnings were depressed and, at points, trimmed the cash returned to shareholders to conserve capital. That is a defensible way to ride out a trough if the recovery arrives on schedule and the new fabs fill up. But it means the company enters its 2026 expansion with a heavier balance sheet than it carried into the last one, and with less margin for error if AI demand disappoints or if a glass transition forces yet another wave of spending on top. Financing an up-cycle build-out with debt raised during a down-cycle is not reckless, but it does compress the room to be wrong. For an investor, the interplay of capex, operating cash flow, and leverage is the same story told three ways, and it all points back to the single discipline question hanging over the new regime.

The KPIs that actually matter

For a company this complex, most metrics are noise. Three are signal, and a long-term investor should track these and largely ignore the rest.

First, high-end substrate utilization and yield — the single most direct driver of gross margin. Because Unimicron's cost base is so fixed, the margin line is essentially a real-time readout of how full and how efficient the advanced fabs are running. When management discusses utilization and yield on earnings calls, that is the number that matters.

Second, AI-related revenue mix. The whole modern thesis rests on the transition from commodity PC-and-consumer substrates to high-value AI substrates. Watching AI-related revenue climb as a share of the total — the market has floated 60% as a symbolic threshold — is the cleanest gauge of whether the pivot is real or rhetorical.

Third, capital expenditure against operating cash flow. This is the discipline test made quantitative. In recent years, capex has run well ahead of operating cash flow — the company spent more building than its operations generated, funding the gap with debt and dilution. Whether SC Chien narrows that gap, and whether capex is eventually funded from within rather than from the balance sheet, is the truest measure of whether "UMC-style management" is real. Watch the free-cash-flow line; it does not lie.

Hold those three numbers, and you can follow this story for years without needing anyone to interpret it for you.

X. Epilogue & Outro

There is a certain justice in the fact that the most advanced computers ever built rest, physically, on a material invented by a seasoning company and a manufacturing craft refined over decades of managing something as mundane as the tendency of hot materials to bend. Unimicron's whole history is the story of taking the least glamorous object in electronics — the circuit board — and, through consolidation, joint investment, and sheer accumulated engineering grit, transforming it into an indispensable, fiendishly difficult piece of semiconductor technology. The company that started as UMC's captive board shop in 1990 became, for a moment, the largest PCB maker in the world, and is today one of the small handful of firms that can put a spine beneath an AI accelerator.

The 2026 handover is the hinge of the whole narrative. T.J. Tseng's relationship-driven, capacity-first instincts built the company and, at times, over-built it; SC Chien's yield-and-returns discipline is the market's bet that the next chapter can be more efficient than the last. It is a genuine test of corporate governance — whether a founder-shaped culture can be re-engineered without losing what made it work.

There is a broader lesson in Unimicron for anyone trying to understand where value accrues in the AI age. The popular imagination fixes on the designers and the foundries — the companies whose logos appear on the chips. But every technology wave creates chokepoints in unglamorous places, and those chokepoints often earn extraordinary economics precisely because no one is looking at them until they become the thing standing between demand and supply. The substrate is such a chokepoint. It is invisible, it is physical, it is fiendishly hard to make well, and for a stretch of the early 2020s it was the single most binding constraint on the world's most valuable industry. Companies that occupy these positions are rarely household names, and their economics are rarely smooth — they boom and bust with the capital cycle of the thing they serve. But they are structurally important in a way that a casual reading of the technology press would never reveal. Understanding them is a large part of understanding how the physical world of computing actually gets built.

What makes Unimicron worth watching is not that its outcome is knowable. It is that the two forces pulling on it are so clear and so opposed. On one side, a widening process-and-scale moat, a structural AI demand wave, and new management promising the discipline the company has always lacked. On the other, a savage cyclical history, a total dependency on a single supplier's film, a capital-allocation record that demands proof rather than faith, and a glass-shaped technology transition that could, before the decade is out, move the finish line entirely. The invisible spine of advanced computing is, itself, remarkably exposed. Which of those forces prevails is the question the numbers — utilization, AI mix, and free cash flow — will answer, one quarter at a time.

References

-

欣興首季稅後純益逾50億元、年增逾4倍,EPS 3.28元 (Unimicron Q1 2026 results) — China Times, 2026-04-29 ↩↩↩

-

欣興電子董事會改選 由簡山傑接任董事長 (Unimicron board names SC Chien chairman) — CNA / 中央社, 2026-02-24 ↩↩

-

聯電共同總經理簡山傑轉任欣興董事長 (SC Chien, UMC Co-President, background) — Economic Daily / 經濟日報, 2026-02-24 ↩↩

-

欣興三度追加資本支出至340億元 布局高階ABF與泰國基地 (Unimicron raises 2026 capex to NT$34bn) — cnyes / 鉅亨網, 2026 ↩↩↩

-

欣興2025年營收1312億元、毛利率13.94% (Unimicron FY2025 results) — cnyes / 鉅亨網, 2026-02-24 ↩

-

Unimicron — Wikipedia (founding 1990, UMC subsidiary, global No. 1 PCB 2009–2010) ↩↩↩

-

欣興電子 公司沿革與併購 (Unimicron corporate history: 2001 merger, 2009 Phoenix Precision share-swap) — MoneyDJ 理財網 ↩↩

-

Unimicron to merge with Subtron Technology in share swap — Taipei Times, 2022-02-23 ↩↩

-

Unimicron chairman Tzyy-jang Tseng to step down upon retirement — Digitimes, 2026-02-15 ↩↩

-

The Ajinomoto Group's Unexpected Role in Semiconductor Manufacturing: ABF — Ajinomoto Group ↩↩

-

Unimicron new plant set to produce ABF substrates for Intel in early 2022 — Digitimes, 2020-07-28 ↩

-

Chip Supplier to Apple, Intel Sees Strong Demand Lasting Years — Bloomberg, 2022-02-23 ↩

-

Global PC Shipments See Record YoY Decline in Q4 2022 — Counterpoint Research, 2023-01-19 ↩

-

Inventory adjustment for ABF substrates extends to 2024; long-term AI optimism — Digitimes, 2023-07-31 ↩

-

ABF Substrate Demand Likely to Recover in H2 2023, BT Substrate Demand to Remain Weak — Counterpoint Research, 2023-07-05 ↩

-

Tariff tensions delay ABF substrate recovery as Unimicron shifts focus to CoWoS clients — Digitimes, 2025-05-06 ↩

-

Intel Unveils Industry-Leading Glass Substrates for Advanced Packaging — Intel Newsroom, 2023-09-18 ↩

-

Intel announces glass core substrate, expected before 2030 — DataCenterDynamics, 2023-09-19 ↩

-

玻璃載板量產遞延 欣興產線估明年H2回穩 (Unimicron glass substrate line to stabilize H2 2026) — Commercial Times / 工商時報, 2025-04-28 ↩

-

同泰董事長異動 由簡山傑接任 (SC Chien becomes chairman of Tongtai) — cnyes / 鉅亨網, 2026-03 ↩

-

Intel Says EMIB Customers Back Substrate Prepayments; Taiwan and Japan Suppliers Seek Commitments — TrendForce, 2026-05-20 ↩

-

欣興電子 投資分析:毛利率 2022 35.90%/2023 19.52%/2024 14.14% (Unimicron gross margin history) — Vocus 方格子 ↩↩

-

ABF substrate crunch reshapes market: Unimicron leads and rivals close in — Digitimes, 2026-01-30 ↩↩↩

-

Unimicron Technology Corp (3037.TW) Company Profile — Reuters ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube