Anker: The Google Engineer's Global Consumer Empire

I. Introduction: The "Amazon Native" Giant

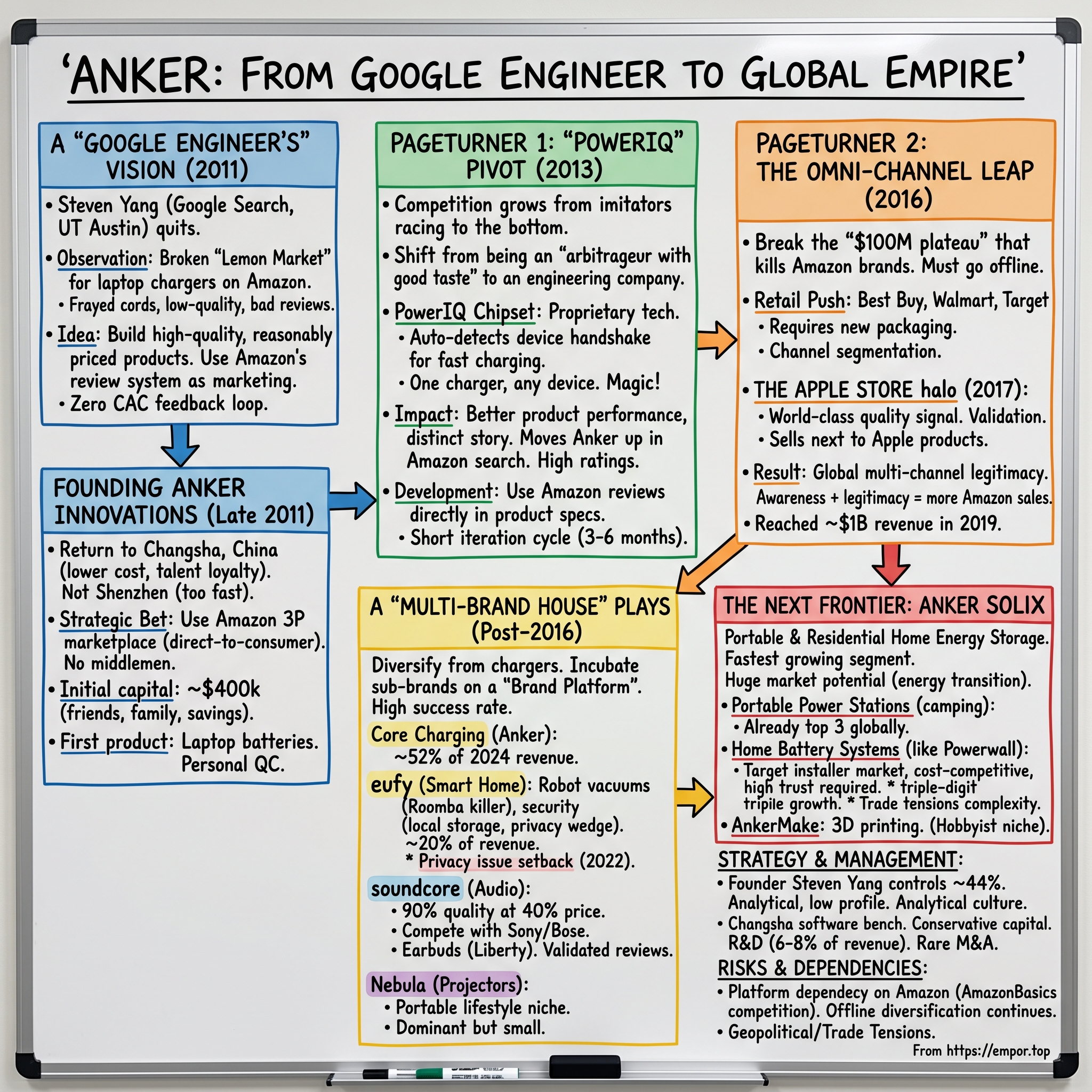

In the late summer of 2011, inside a Mountain View campus building where engineers got unlimited kombucha and stock options vested over four years, a Chinese-born Google engineer named Steven Yang was quietly spending his lunch breaks clicking through the "Computer Accessories" category on Amazon.com. He wasn't shopping. He was studying.

Yang had an obsession that bordered on the clinical. Every few days, someone in his family, his engineering team, or his friend group would complain about the same thing: the original Apple laptop charger had frayed at the cord, the replacement was $80, and the third-party alternatives on Amazon were a graveyard of one-star reviews. Batteries that died in three months. Chargers that smelled like burning plastic. Cables that worked for a week, then didn't. The entire category was a lemon market—broken trust, broken products, broken promises.

Yang ran a simple query in his head, the kind of mental model Google had drilled into him. If the incumbents were overpriced, and the challengers were junk, what happened if someone built a product that was actually good, priced it 40% below Apple, and used Amazon's review system as the marketing channel? The CAC would be near zero. The feedback loop would be instant. And China, thirty minutes by plane from Shenzhen, had a battery and lithium cell supply chain that was the best on Earth.

That question, asked over a Google cafeteria burrito, launched what has become one of the most successful consumer electronics stories of the past fifteen years. Fifteen years later, in April 2026, Anker Innovations trades on the Shenzhen Stock Exchange with a market cap that has vaulted past $10 billion equivalent at peak, annual revenue of approximately 24.7 billion RMB for 2024 (roughly $3.4 billion), a portfolio of six distinct consumer brands, operations in more than 146 countries, and a quiet, founder-led culture operating out of Changsha—a city most Silicon Valley founders could not locate on a map.

Here is the thesis, the one that makes Anker unique among the tens of thousands of Chinese consumer hardware companies that sprouted up in the 2010s. Anker is the first—and so far, really the only—"Amazon Native" brand to successfully cross the chasm into a global, multi-category technology leader. Most brands born on Amazon die on Amazon. They peak at $100 million in revenue, get gutted by private-label clones, and end up acquired by aggregators like Thrasio at 2-3x EBITDA in a fire sale. Anker didn't. Anker did something different, and understanding what that something is will take a while.

The roadmap for today: the origin story of how a Google search engineer built a charging empire from a 200-square-foot office in Shenzhen; the crucial pivot from arbitrage to real engineering via a chipset called PowerIQ; the leap from being purely an Amazon brand to being sold inside the Apple Store itself; the multi-brand house Anker has quietly constructed under the umbrella names Eufy, Soundcore, Nebula, AnkerMake, and now the fastest-growing piece, Anker SOLIX; and the emerging bet that will define the next decade—the energy transition, and whether a Chinese charging company can really take on Tesla Powerwall in American suburban garages. Buckle up.

II. Founding Context: The Google Escapee

Steven Yang—Chinese name Yang Meng—was not supposed to become the Jeff Bezos of chargers. Born in 1982 in Hunan province, he was the classic Chinese academic prodigy, the kid who won provincial math olympiads and landed at Peking University's computer science department, a program whose acceptance rate makes Stanford look like community college. From Peking, he continued to the University of Texas at Austin for a master's in computer science, where he specialized in search algorithms. In 2006, Google hired him to Mountain View, where he worked on the Search Infrastructure team—the team responsible for crawling, indexing, and serving the actual trillion-page corpus that makes "Google it" a verb.

This is important context, because it tells you how Anker's DNA was formed. Most Chinese consumer hardware companies were founded by people who came up through contract manufacturing—the OEM/ODM world of Foxconn and Flextronics. They thought in bill-of-materials terms, in cost-per-unit terms, in factory utilization terms. Yang thought in data terms. He thought in product-market-fit terms. He thought, crucially, in software terms, even though what he was going to build was profoundly hardware.

By 2011, Yang was in his late twenties, comfortable, stock options maturing, but restless. The mobile revolution was in full swing. The iPhone 4 had launched the year before. Android was exploding. Smartphones were getting faster, brighter, more powerful. And yet—and here is the insight that kept nagging Yang—the batteries were getting worse. Or more precisely, battery technology was improving linearly while power consumption was exploding exponentially. Every iPhone user in 2011 knew the feeling: your phone was dead by 3 pm. The accessories to fix that problem—portable chargers, USB wall chargers, replacement laptop batteries—were either Apple-branded and priced accordingly, or they were genuine garbage.

Yang called this "the battery gap," and he became convinced it represented a multi-decade opportunity. He quit Google in late 2011 and moved back to China. Not to Shenzhen, the obvious choice, but to Changsha, Hunan—his hometown. This was a strange decision. Changsha is a lovely city famous for spicy food, but it is not a hardware hub. His reasoning was twofold. First, talent in Changsha was dramatically cheaper than in Shenzhen, and crucially, loyalty was higher—people didn't jump companies every six months for a 15% raise. Second, Yang wanted to build a culture more like Google Mountain View than like a Shenzhen factory, and he wanted distance from the gritty, transactional, "fast money" ethos of the Huaqiangbei electronics district.

The other founding insight—the one that still defines Anker today—was a read on Amazon that almost no one else had in 2011. Amazon in 2011 was not the retail colossus it is today. It was still primarily a bookstore that happened to sell electronics. But Yang saw what was coming. The marketplace was opening up to third-party sellers. Fulfillment by Amazon had just launched in meaningful volume. And critically, the review system was becoming the most trusted signal in consumer electronics. Yang understood that if you could produce a product whose Amazon reviews averaged 4.5 stars instead of 3.2, you would win, full stop. The customer acquisition cost was not a Google AdWords number—it was zero.

He also made a deliberate strategic call that sounds obvious today but was radical then: Anker would sell direct through Amazon's 3P marketplace, not wholesale through traditional distributors. No middlemen. No retailers. Full margin capture. Full data capture. Full control of the customer relationship. In 2011, this was heresy in Chinese hardware. Everyone wanted to be inside Best Buy. Yang wanted to be inside Amazon. It turned out he was five years early to what would become the playbook for an entire generation of DTC brands.

The early days were lean. The initial seed capital was roughly $400,000, raised from friends, family, and Yang's own Google savings. The first product was laptop battery replacements—ThinkPad, Dell, HP—sourced from Shenzhen suppliers but with Yang personally QC'ing every batch. The brand name "Anker" was chosen as something Western-sounding, pronounceable in any language, and evocative of reliability. It worked. By the end of 2012, Anker was doing meaningful millions in revenue. By 2013, it was profitable. By 2014, it was the #1 mobile power brand on Amazon.com. And that's when the real story begins.

III. Inflection Point 1: The "PowerIQ" Pivot

Here's the dirty secret of the early Anker years that no founder PR deck will ever feature: in the first twenty-four months, Anker was essentially an arbitrageur with good taste. Yang and his small Changsha team were sourcing components and finished goods from the same Shenzhen supply chain as everyone else. Their advantage wasn't engineering—it was curation, quality control, and branding. They picked the best suppliers, they rejected bad batches, they over-invested in packaging, and they treated customer service like a religion. If your Anker charger broke, you got a replacement overnight, no questions asked.

This works, until it doesn't. By 2013, the imitators were coming. Every reasonably savvy Shenzhen trader had noticed what Anker was doing on Amazon, and a flood of lookalike brands—RavPower, Aukey, Jackery, iClever, Poweradd—started racing to the bottom on price. If Anker's only advantage was sourcing, Anker was going to get commoditized by 2015. Yang understood this, and he made the bet that arguably defines the company's entire trajectory: Anker would stop being a sourcing company and start being an engineering company.

The first real proprietary technology was called PowerIQ. To understand why this mattered, you need to understand a genuinely annoying technical problem that existed in 2013. Different devices—iPhones, Android phones, iPads, Bluetooth speakers—used different "handshake" protocols to tell a charger how much current to deliver. An iPhone wanted one signal pattern. A Samsung Galaxy wanted another. Plug an iPhone into a generic Android charger and you'd get slow charging, or worse, no charging. Plug an Android into an Apple charger and the same thing happened. This was not a conspiracy—it was genuine protocol fragmentation stemming from the fact that USB charging specs had evolved chaotically.

PowerIQ was Anker's solution. It was a small integrated chipset baked into their chargers that auto-detected what device was plugged in and spoke its specific handshake language. One charger, any device, full-speed charging. Today this sounds trivial. In 2013, it was magic. It was also the first time Anker had genuinely invested in silicon-level R&D—hiring actual chip designers, not just mechanical and product engineers.

The business impact was immediate. PowerIQ allowed Anker to sell a premium multi-port charger—say, a 40-watt, 5-port desktop charger at $35—that genuinely outperformed Apple's own accessory, which forced single-port, single-speed charging at a higher price. On Amazon, where reviewers are ruthlessly empirical, this showed up in star ratings. PowerIQ products averaged 4.7 stars. Generic competitors averaged 3.9. In the rank-ordered Amazon search, that gap is the difference between appearing on page one and appearing on page five. It is the difference between a $100 million business and a zero.

PowerIQ also did something subtler, something that mattered more in the long run. It gave Anker a reason to talk about itself as a technology company. "Powered by PowerIQ" became a phrase. Marketing copy could reference proprietary engineering, not just "great quality." Reviews started citing the technology by name. Anker began to pull away from RavPower and Aukey not because their chargers were dramatically better in absolute terms, but because Anker now had a story, and a story with a trademark inside it.

This shift coincided with another bet that looks obvious in retrospect but was non-obvious at the time: Anker used the Amazon review system itself as a product development engine. Most hardware companies in 2013 did user research the traditional way—focus groups, surveys, dealer feedback. Yang's team did something different. They read every single Amazon review. Not the aggregates. Every individual review. Then they categorized complaints and feature requests in a database, and fed that database directly into the next product's engineering spec. The next generation of a product literally addressed the top ten complaints from the previous generation. If customers said the LED indicator was too bright at night, the next version had a dimmable LED. If customers said the cable was too stiff, the next version had a softer cable.

This was, in effect, "building in public"—a phrase that would not be coined for another decade—applied to hardware. Anker's product iteration cycle shrunk to roughly three to six months, versus eighteen to twenty-four months for traditional accessory makers like Belkin and Logitech. It was a genuine structural advantage, and it compounded.

By 2015, Anker wasn't just a brand anymore. It was the brand. The category leader in portable charging globally. But being the best brand on Amazon still leaves a ceiling, and Yang knew it. To break out, he was going to have to do something Amazon-native brands almost never successfully do: go offline.

IV. Inflection Point 2: The Omni-Channel Leap

There's a graveyard in the DTC and Amazon-brand world, and it has a name: the $100 million plateau. Pour one out for Pax Labs, or Casper, or any of the dozens of brands that figured out how to scale from zero to nine figures on a digital channel, then hit a wall. The wall was always the same. Digital ads get more expensive as you scale. Amazon takes more of the margin as you grow. Private-label clones erode the category. The only way through the wall is to become a real, honest-to-god brand that exists in physical retail, in consumer consciousness, in the cultural air. Very few Amazon brands make it through. Most die.

Anker started the omni-channel push around 2016, and the strategic chess moves that Steven Yang and his team executed between 2016 and 2019 are worth studying carefully, because they are a masterclass. The first move was Best Buy. Getting onto Best Buy shelves required Anker to rebuild its packaging—Amazon packaging is optimized for cardboard-box warehouses, retail packaging is optimized for a fluorescent-lit aisle with five seconds of customer attention. Anker overhauled its packaging language, hired a design team that had worked at Apple's packaging group, and invested in what retail buyers call "shelf drama"—the ability of a product box to command attention on a crowded shelf.

The second move was Walmart and Target—mass retail. This was harder, because mass retail compresses margin brutally, and because the Anker brand had been positioned as a "premium discount" on Amazon. Yang's team navigated this by releasing sub-lines—slightly different SKUs with different features—for different retail channels. The Anker product at Walmart was not quite the same as the Anker product at Best Buy, which was not quite the same as the Anker product on Amazon. This is channel segmentation 101, but Anker did it with unusual discipline.

The third move—and this is the one that genuinely changed everything—was getting into the Apple Store. Not the online Apple Store, which is somewhat easier. The physical, retail, Tim-Cook-certified Apple Store. The marble-floored cathedral of consumer electronics branding. The place where the only accessories on the shelves are either Apple-branded or genuinely world-class.

Getting into the Apple Store is a process that can take years. Apple's accessory buyers are famously demanding. They want proof that a product will not embarrass the Apple brand—which means industrial design must be immaculate, packaging must be flawless, warranty policies must be better than Apple's own, and the product itself must genuinely work. Anker made its Apple Store debut in 2017 with PowerCore portable chargers. By 2019, Anker products occupied meaningful shelf space in Apple Stores globally—often literally next to Apple's own charging accessories, sometimes priced 30% below the Apple equivalent.

The halo effect of this was enormous, and Yang had explicitly engineered it. Every time a customer walked into an Apple Store, saw an Anker charger on the shelf at a lower price than the equivalent Apple product, and bought it, Anker earned two things: revenue, and a validation signal that could not be bought with marketing dollars. "Sold in Apple Stores" became part of Anker's own marketing copy on Amazon. The cross-channel flywheel was complete—Amazon drove awareness, retail drove legitimacy, and legitimacy drove more Amazon conversion.

By 2019, Anker was doing roughly $1 billion in annual revenue, with offline retail accounting for somewhere between 30% and 40% of the mix depending on the quarter. The Amazon-native brand had done what almost no Amazon-native brand had ever done. It had gone fully multi-channel, without losing its online dominance, and without destroying its brand equity. This was the moment Anker graduated from being "a cool Amazon story" to being a real, multi-billion-dollar consumer electronics company. And with that legitimacy came the confidence to do the next thing—which was to stop being just a charging company.

V. Hidden Businesses: The Multi-Brand House

If you only know Anker as "the charger company," you are dramatically underestimating what has been built. The charging business—the core Anker-branded portable chargers, wall chargers, cables, and power banks—remains the anchor, generating approximately 52% of 2024 revenue. But the truly interesting story is in the other 48%, which consists of a constellation of sub-brands that Anker has spawned, incubated, and scaled over the past eight years. Collectively, these brands represent Anker's answer to a question every successful consumer brand eventually faces: where does growth come from once the core category matures?

Start with Eufy, which is the hidden growth engine that most American consumers don't realize is Anker. Eufy was launched in 2016 as Anker's "smart home" sub-brand, with an initial focus on robot vacuums. The strategic logic was pure Yang-think: the Roomba market was overpriced (iRobot's flagship cost $800+), the off-brand Chinese vacuums were unreliable, and the software layer—app control, mapping, AI navigation—was a software problem, which played directly to Anker's Google-engineering DNA. Eufy's first robot vacuum, RoboVac 11, launched in 2016 at around $200. It immediately became Amazon's #1 robot vacuum. Within eighteen months, Eufy had meaningful share in a category where everyone had assumed iRobot's moat was permanent.

From robot vacuums, Eufy expanded into home security—doorbell cameras, indoor cameras, outdoor cameras, smart locks. This category was dominated by Ring (owned by Amazon) and Nest (owned by Google). Eufy's positioning was sharp: local storage, no monthly subscription fees, AI processing done on-device rather than in the cloud. For a certain kind of privacy-conscious American consumer—the kind who was increasingly suspicious of Ring sharing footage with police departments, the kind who didn't want to pay $8 a month to access their own video—Eufy became the sophisticated choice. By 2024, Eufy was generating a meaningful slice of Anker's revenue, with smart home products representing roughly 20% of the total mix.

Eufy did stumble, importantly. In late 2022, security researchers demonstrated that Eufy cameras, despite marketing claiming local-only processing, were actually uploading thumbnail images to AWS servers, and that video streams could be accessed via URL without authentication in certain circumstances. The company initially denied the problem, then walked it back, then pushed firmware patches. For a brand whose entire wedge was "trust us on privacy," this was genuinely damaging, and it forced a reorganization of Eufy's security engineering team. The episode is worth knowing because it illustrates both a vulnerability—Anker's software layer is not always as mature as its hardware—and a recovery—the brand did not collapse, sales eventually re-accelerated, and Eufy remains a category leader in 2026.

Then there's Soundcore, the audio brand launched in 2015. The Soundcore strategic playbook is different from Eufy's and arguably cleaner. In audio, the incumbents are Bose, Sony, and Beats/Apple—all premium-priced, all heavily branded, all generating massive margins on what are, materially, commoditized speaker components. Soundcore's insight was that if you built a genuinely good Bluetooth speaker using the best components from the Shenzhen supply chain, you could deliver roughly 90% of the audio quality of a comparable Sony or Bose product for roughly 40% of the price. And you could do it at Anker-level gross margins because the component costs were similar; the incumbents were just pricing at a massive brand premium.

Soundcore now covers Bluetooth speakers, earbuds, headphones, and home audio. The Soundcore Liberty earbuds—directly competing with Apple AirPods and Sony WF-series—have become genuinely competitive products in their own right, winning reviews at publications like The Verge and Wirecutter. Soundcore's audio engineering team, initially hired from Chinese audio companies, now includes former engineers from Bose and Sony. The brand is less of a pure discount play and more of a legitimate audio challenger.

Nebula, Anker's projector brand, is smaller—what Yang's team internally calls a "lifestyle bet." The insight here is that traditional projectors are expensive, stationary, and tied to home theaters. Nebula's product line is portable, battery-powered, and designed for casual outdoor use—camping, backyard movie nights, dorm rooms. It's a category Anker essentially invented at scale, and while revenue is modest (probably under 5% of total), the brand is dominant in its niche.

The genuinely impressive thing about all this is not that Anker has multiple brands—lots of companies have multiple brands. The impressive thing is the incubation model. Anker has, over the past decade, developed something internally called the "brand platform"—a shared infrastructure layer of supply chain relationships, industrial design resources, software engineering, customer service operations, marketing templates, and retail relationships, that any new brand can plug into. Launching a new brand at Anker is, by the founder's own description, closer to launching a new product line at Procter & Gamble than it is to starting a new company. This is why, of the handful of sub-brands Anker has launched, most have become profitable within eighteen months—a success rate that is, frankly, staggering in consumer electronics where most new product launches fail.

The deeper point, and the one that should interest long-term investors, is that Anker has effectively built a platform company wearing the clothes of a product company. The platform is the incubator, the supply chain, the software infrastructure, and the brand-building machinery. Each sub-brand is an application running on that platform. And the next two applications Anker is launching could be the biggest yet.

VI. The Next Frontier: Anker SOLIX and AnkerMake

Of everything happening at Anker Innovations in 2026, the single most important business to understand is Anker SOLIX, the home and portable energy storage brand. It is, by a significant margin, the fastest-growing segment of the company and, more importantly, the segment with the largest potential ceiling. SOLIX is where Anker bets that the decades-old playbook—good engineering, good software, Amazon-native distribution, omni-channel expansion—can be repeated in a category that is roughly 20x larger than consumer charging.

The logic is almost embarrassingly simple. A portable power bank for your phone stores maybe 30 watt-hours of energy. A portable power station—the kind you take camping or use for emergency backup—stores 500 to 2,000 watt-hours, or about 50x more. A full home battery backup system, like Tesla Powerwall, stores 13,500 watt-hours, or 450x more. Each step up in capacity represents not just a bigger battery, but a dramatically bigger market. The home energy storage market globally is projected to grow from roughly $15 billion in 2024 to over $60 billion by 2030, driven by the residential solar boom, electrification, grid instability, and climate-driven extreme weather events.

Anker launched into portable power stations in 2020 under the Anker PowerHouse brand, which was rebranded to Anker SOLIX in 2023. The initial products were "jackery killers"—gas-generator-replacement portable stations for camping and RV use, priced 10-20% below competitor products from Jackery, Goal Zero, and Bluetti. Anker's engineering advantages—thermal management, battery management systems, inverter efficiency—translated directly. By 2023, Anker SOLIX was among the top three portable power station brands globally.

The step up from portable to residential is harder. Tesla Powerwall, the category-defining product, benefits from enormous brand equity, deep integration with solar installers, and Tesla's vertical control of the battery supply chain. Competing here is not a marketing problem; it is an installation and trust problem. When you spend $10,000 on a whole-home battery system, you need an electrician to install it, you need a permit from your city, you need your utility to bless the interconnection, and you need to trust that the battery will work in a blackout three years from now.

Anker SOLIX entered the residential market in 2023-2024 with the F3800, a modular home energy storage system targeting the U.S. and European markets, and has been expanding rapidly through both direct sales and installer partnerships. In 2024, SOLIX accounted for a meaningful slice of Anker's revenue growth and was identified in the annual report as the segment with the highest growth rate—the segment was on a revenue run-rate expanding at triple-digit percentage year-over-year from a smaller base. The strategic question for investors is whether Anker can establish itself as a credible #2 or #3 in residential energy storage globally, given that Tesla, Enphase, Sonnen, and LG have the incumbent positions.

There are reasons to be optimistic and reasons to be cautious. On the optimistic side, the U.S. residential solar market is fragmented at the installer level—there are thousands of solar installers, most of whom do not have exclusive battery partnerships, and who would welcome a cost-competitive alternative to Tesla. Anker has spent two years building installer relationships, training programs, and fulfillment infrastructure. On the cautious side, residential energy storage is a long-cycle, high-trust purchase, and brand equity in this category accrues slowly. Anker is also navigating the added complexity of U.S.-China trade tensions, which have resulted in tariffs on Chinese-manufactured lithium batteries and which Anker is addressing in part through Southeast Asian manufacturing expansion.

The other frontier business is AnkerMake, the 3D printing brand launched in 2022. The strategic fit is actually quite elegant. Consumer 3D printing as a category has been dominated by either expensive professional brands (Formlabs, Ultimaker) or cheap but unreliable hobbyist brands (Creality). AnkerMake's wedge is the Anker playbook—take the best components from the Chinese 3D printing supply chain, add superior industrial design, add genuinely good software (the AnkerMake app does AI-driven print failure detection, which is novel), and sell at a price between the cheap and expensive ends of the market. The AnkerMake M5 launched in 2022 at around $700 and was well-received critically.

AnkerMake is still a small business relative to the rest of Anker. The strategic question is whether consumer 3D printing is actually a mass-market category or a hobbyist niche. The answer is probably "mostly hobbyist, with slow expansion." Which is fine—not every Anker bet needs to be SOLIX-scale. The portfolio approach means small wins are acceptable as long as the big wins are big enough.

Zooming out: what Anker is attempting across SOLIX and AnkerMake, and what it has already executed across Eufy and Soundcore, is to prove that the "Anker playbook"—engineering-led, Amazon-native, omni-channel, software-enhanced, globally distributed—is replicable across essentially any consumer hardware category. If that thesis holds, then Anker is not a charger company. It is a platform for building consumer hardware brands, in the same way that Procter & Gamble is a platform for building consumer packaged goods brands. And that framing, if it proves correct, implies a dramatically larger long-term opportunity than the current financials suggest.

VII. Management and Capital Deployment

At the center of Anker Innovations sits Steven Yang Meng, and understanding Yang's style, incentive structure, and management philosophy is essential to understanding how the company makes decisions. Yang is, by most accounts from those who have met him, the kind of founder you'd expect given his résumé: soft-spoken, intensely analytical, allergic to hype, and genuinely obsessed with engineering details. Where many Chinese founders adopt a flashy public persona, Yang has kept a notably low profile—he rarely does Western media, rarely tweets, rarely headlines conferences. The closest Anker has to a celebrity CEO moment is when Yang appeared briefly on Chinese business programs around the 2020 IPO.

Yang's ownership structure is the single most important data point for a long-term investor. As of the most recent disclosures, Yang holds roughly 44% of Anker Innovations through direct and indirect stakes, which gives him absolute control over board composition, strategic direction, and capital allocation. For better and for worse, Anker is Steven Yang's company. The structural bull case here is that founder-led companies with high insider ownership consistently outperform professionally-managed alternatives in consumer electronics, where long-term thinking and willingness to cannibalize existing products are critical. The structural bear case is key-person risk: if something happened to Yang, the succession picture is less clear than investors might want.

The president, Zhao Dongping, has been at Anker since the early years and serves as the operational complement to Yang's product vision. Where Yang is the chief product officer in all but title, Zhao is the chief operator—responsible for supply chain, manufacturing partnerships, logistics, and the day-to-day running of an organization that now exceeds 6,000 employees globally. The Yang-Zhao duo has been remarkably stable for a Chinese tech company—no public disputes, no coup attempts, no sudden departures—which in itself is noteworthy.

The Changsha headquarters deserves a paragraph of its own, because it is genuinely unusual. Changsha, again, is not Shenzhen. It is not Beijing. It is not a tier-one Chinese tech hub. And yet Anker has built, over the past decade, a recruitment engine that brings top-tier software engineering talent to Changsha. The pitch combines Google-style work culture (flat hierarchies, casual dress, abundant food), substantial equity upside, meaningfully lower cost of living than Beijing or Shanghai, and the psychological appeal of not commuting two hours a day. The result is that Anker has a software engineering bench that is, person-for-person, stronger than most Chinese hardware companies—which shows up directly in product quality for the sub-brands.

The capital allocation philosophy at Anker is, by Chinese tech standards, conservative and disciplined. Three features stand out.

First, R&D intensity. Anker consistently spends roughly 6-8% of revenue on R&D—significantly higher than traditional accessory makers like Belkin or Logitech, which sit closer to 3-4%, and comparable to genuinely technology-led consumer electronics companies. This R&D investment is what funds the proprietary silicon work (PowerIQ and its successors), the software platforms across sub-brands, and the new category incubations. Yang has been explicit that Anker will not cut R&D to hit a margin target—a commitment that is easy to make and hard to keep in public markets, but which Anker has actually honored.

Second, M&A is rare and surgical. Unlike Chinese tech conglomerates that acquire aggressively (Tencent, Alibaba, ByteDance), Anker has made very few acquisitions. The preference is aggressively internal—new categories are incubated in-house rather than bought, because Yang believes (probably correctly) that the Anker platform advantages don't transfer to acquired companies, and that integrating acquisitions destroys more value than it creates. When Anker has acquired, it has been small, targeted technology tuck-ins—acoustic IP for Soundcore, battery chemistry know-how for SOLIX—not big strategic moves.

Third, capital return to shareholders has been thoughtful. Since its 2020 Shenzhen IPO, Anker has paid dividends consistently and has executed modest buybacks, particularly during the 2022-2023 period when the stock traded lower. The dividend policy is not aggressive—payout ratios typically in the 20-40% range—but it reflects Yang's apparent belief that the best use of capital is reinvestment into R&D and new category expansion, with incremental returns to shareholders once reinvestment opportunities are covered.

The question investors should ask about management is whether the internal incubation model continues to scale. It has worked brilliantly through Eufy, Soundcore, Nebula, AnkerMake, and SOLIX. But each new sub-brand stretches the platform further, and at some point organizational complexity becomes the bottleneck, not the asset. Yang has said publicly that Anker is essentially a "house of brands" and wants each brand to develop its own distinct identity. In practice, this means giving sub-brand leaders real operational autonomy while keeping centralized control over supply chain, engineering infrastructure, and capital. Whether that balance holds as the company scales beyond $5 billion in revenue is one of the most important governance questions facing the business.

VIII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

If you strip away the narrative and just ask the strategic question—why should Anker earn above-market returns on capital over the long term—you end up running two frameworks that are worth doing explicitly. Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

On Hamilton's 7 Powers, Anker clearly has three of the seven, arguably four.

Brand. The Anker name, over fifteen years, has become genuinely synonymous with "reliable consumer electronics" in a sea of generic Amazon junk. This brand equity took a decade to build and compounds every year. A new entrant cannot replicate it with marketing spend—it was earned through millions of positive Amazon reviews, through Apple Store placement, through category-leading warranty policies, through not shipping defective products for fifteen years. Brand is a real power here, and it extends (though more weakly) to the sub-brands Eufy, Soundcore, Nebula. Anker's brand allows pricing power of 15-25% above commodity alternatives, which directly supports the roughly 40% gross margins the company has maintained despite operating in categories popularly described as "commodity."

Cornered Resource. Anker's cornered resource is the combination of deep Shenzhen supply chain integration plus Google-caliber software engineering talent in Changsha. Neither of these alone is unique. Plenty of Chinese companies have Shenzhen supply chain relationships; plenty of companies have good software engineers. The combination, operating at scale, is rare. It is the reason Anker can launch a product in three to six months when incumbents like Belkin need eighteen to twenty-four. This cornered resource is culturally embedded—it would be very difficult for a competitor to replicate even with unlimited capital.

Scale Economies. This one is subtle but real. Anker's scale economies are not in manufacturing—Anker mostly uses contract manufacturers, so unit costs are roughly similar to competitors at similar volumes. The scale economies are in distribution and R&D, which are amortized across the multi-brand platform. Amazon advertising spend, for example, can be optimized across a portfolio of Anker, Eufy, and Soundcore listings in ways a single-brand competitor cannot replicate. Retail relationships established for the Anker brand can be leveraged to get Soundcore onto shelves faster. This is platform-level scale, and it compounds as the portfolio grows.

Process Power is the fourth, possibly. The internal incubation process—the way Anker launches new sub-brands and new categories—has produced a remarkable track record. Whether this is genuinely a replicable organizational process or just a consequence of Yang's judgment is an empirical question. If it is truly process power, it becomes one of Anker's most durable advantages. If it is founder power, it is more fragile.

On Porter's 5 Forces:

Threat of New Entrants. Moderate. The charging category in particular has seen continuous entrant pressure from both Chinese upstarts and retailer private labels. The threat is partially offset by Anker's brand and PowerIQ-style technical differentiation, but it is not zero.

Bargaining Power of Buyers. Moderate to high on Amazon, where consumers can comparison-shop frictionlessly. Lower in offline retail, where brand visibility and shelf position matter more. Anker's omni-channel strategy is partly a buyer-power mitigation play.

Bargaining Power of Suppliers. Low. The Shenzhen component supply chain is deep and competitive, and Anker is a large enough buyer to negotiate favorable terms.

Threat of Substitutes. Varies dramatically by category. Low for core charging (a phone charger is a phone charger). Moderate for audio (Soundcore competes against Bose, Sony, and also against the AirPods-as-default substitution from Apple). High for smart home (Eufy competes against Ring, Nest, and dozens of others).

Competitive Rivalry. High in every category Anker operates in. Charging is brutal. Audio is brutal. Smart home is brutal. Residential energy storage is increasingly brutal as more entrants arrive. The intensity of rivalry means that Anker must constantly innovate on product and cost to maintain share.

There's a sixth "force" worth discussing explicitly, because it is arguably the most important factor in Anker's long-term fortunes: platform dependency on Amazon. Anker was built on Amazon, and while it has aggressively diversified off Amazon since 2016, Amazon still represents a meaningful plurality of global sales. Amazon's private-label program, AmazonBasics, directly competes with Anker in multiple categories—AmazonBasics charging cables, AmazonBasics batteries, AmazonBasics speakers. Amazon has every incentive to promote its own private labels over third-party brands, and this tension has been a persistent theme throughout Anker's history. Anker's defense has been a combination of premium positioning (AmazonBasics competes on price, Anker competes on quality), continuous innovation (AmazonBasics copies slowly), and offline channel diversification (AmazonBasics does not exist outside Amazon). This defense has held for fifteen years, but it is not a permanent solution, and investors should monitor the relationship carefully.

IX. The Bull and Bear Case

Time to lay out the bull and bear case explicitly, because any long-term investor needs both.

The Bull Case. Anker becomes what might be called "the Procter & Gamble of the 21st-century electronic home." In this scenario, the Anker platform continues to successfully spawn new sub-brands across every category where consumer hardware is undergoing a transition—energy storage (SOLIX), smart home (Eufy), audio (Soundcore), 3D printing (AnkerMake), and future categories that don't exist yet. Each sub-brand builds to multi-hundred-million-dollar revenue. SOLIX, in particular, rides the residential energy storage mega-trend to become a $5+ billion business within a decade, representing the single largest category at Anker. The consolidated business scales to $15-20 billion in revenue by 2035, with blended gross margins around 40-45% (aided by software-attached products in smart home and energy), and operating margins in the mid-teens. R&D continues at 6-8% of revenue, which feeds the innovation flywheel. Founder control and disciplined capital allocation compound returns over a multi-decade horizon. The comp is less "Belkin, but bigger" and more "what if Philips had actually innovated for the past thirty years."

Supporting the bull case are several underappreciated data points. The multi-brand platform has produced a track record of successful launches that few consumer companies can match. The energy storage market is enormous and genuinely under-penetrated at the residential level—the total addressable market for home batteries is probably 100x the current installed base. Anker's supply chain and engineering combination gives it a durable cost-plus-quality advantage over Western competitors. And the company's 44% insider ownership aligns management incentives with long-term shareholders in a way that professionally-managed alternatives rarely achieve.

The Bear Case. Now the other side, and this needs to be taken seriously.

First, geopolitical risk. Anker is a Chinese company manufacturing mostly in China, selling mostly to Western consumers. The U.S.-China trade relationship has been on a multi-year deterioration trajectory, and the risk of tariffs, import restrictions, or outright bans on Chinese consumer electronics is real and material. The Huawei and TikTok experiences loom over every Chinese company operating in the U.S. market. Anker has been expanding manufacturing in Vietnam, Indonesia, and elsewhere to reduce China exposure, but this transition is incomplete and expensive. A meaningful escalation in trade tensions could directly compress margins or disrupt revenue.

Second, Amazon private-label encroachment. AmazonBasics has become more aggressive over time, and Amazon has increasing technical capability to identify top-selling third-party products and clone them at private label. The historical defense—premium positioning and continuous innovation—works only as long as Amazon does not decide to move AmazonBasics upmarket, which it occasionally shows signs of doing. A serious AmazonBasics push into the core Anker charging categories could meaningfully compress Anker's dominant position there.

Third, the commodity trap. In categories where Anker cannot continue to differentiate on technology or brand—and charging may eventually reach this state as USB-C and wireless charging standardize the entire category—Anker becomes a high-scale commodity producer. Margins would compress toward industry averages. R&D intensity would become hard to justify. The multi-brand platform might start to look less like a platform and more like a conglomerate discount.

Fourth, sub-brand execution risk. The platform has worked so far, but not every sub-brand has been a hit. Eufy had the privacy fiasco. Nebula remains a niche business. AnkerMake is unproven. If SOLIX, the bet with the largest capital outlay and the largest ambition, underwhelms—perhaps because Tesla, Enphase, and LG simply hold the residential market—it would materially change the growth narrative.

Fifth, and this is the one few investors talk about: the transition from founder to post-founder leadership. Yang is still in his early forties and shows no sign of stepping back, but consumer electronics companies that survive their founder's eventual departure are the exception, not the rule. Anker has not been stress-tested on this dimension yet.

In the middle of these two cases is the middle case, which is probably the base case. Anker continues to grow revenue at 15-20% per year, margins hold roughly flat, the multi-brand platform produces a mix of hits and misses, SOLIX becomes a solid-but-not-transformational business, and the company trades at something like 20-25x earnings, reflecting a high-quality consumer electronics platform but not a Procter & Gamble-style re-rating. This base case is honestly fine, and probably reflects most investor consensus in 2026.

The single most important KPI to track over the coming years is the Anker SOLIX revenue run-rate. Within SOLIX, the breakdown between portable power stations (the mature, steady-state business) and residential home energy storage (the bet) is what matters. If residential home storage revenue starts compounding at triple-digit rates for multiple consecutive years, the bull case is coming true. If it stalls below $500 million in global revenue, the base case prevails. Second most important: gross margin at the consolidated level. If Anker can hold gross margins around 40% as the mix shifts toward energy (which has different margin characteristics than charging), the cornered-resource thesis is validated. Third, offline retail share of total revenue. If offline continues to scale toward 50% of revenue, the Amazon-dependency bear case is increasingly dead; if it plateaus in the low 30s, the Amazon tail risk remains.

X. Conclusion and Lessons for Founders

There's a line from Hemingway, quoted to death in startup decks: "Gradually, then suddenly." It is almost always misapplied. In Anker's case, it fits precisely. For the first six years of the company's life, from 2011 to 2017, almost nothing that happened would have generated a Silicon Valley headline. The company was selling laptop batteries on Amazon, then phone chargers on Amazon, then portable power banks on Amazon. It was growing fast but from a small base. It was profitable, which in Chinese tech in the mid-2010s was almost suspicious—real tech companies were supposed to burn cash. It was not raising venture capital. It was not doing press. It was, by every superficial measure, a boring small business run by a former Google engineer who had moved back to a tier-two Chinese city to sell charging accessories.

Then, suddenly, it was everywhere. Apple Stores. Best Buy. Walmart. A $1 billion revenue run-rate in 2019. A Shenzhen IPO in August 2020 at what turned into a premium valuation. Eufy doing half a billion. Soundcore doing half a billion. SOLIX scaling faster than any previous Anker sub-brand. A market cap that at various points has exceeded the market cap of Belkin, Logitech, and iRobot combined.

What the Anker story teaches, if you squint, is that consumer hardware success in the twenty-first century can be engineered from the "bottom" of the market. You do not need to start premium and descend. You do not need to launch on the cover of Wired. You can start on Amazon page three, build a 4.7-star product, iterate every quarter based on reviews, reinvest profits into R&D, slowly migrate into premium channels, and eventually stand on the shelf of an Apple Store while competing against Bose. The entire process takes roughly a decade, requires extreme operational discipline, and rewards founders who can hold a long-term vision while executing in quarterly product cycles.

The other lesson, and this is probably the one that matters most for anyone thinking about building a consumer technology business today, is about the compounding value of an engineering-led culture in a category perceived as commoditized. Everyone in 2011 would have told Steven Yang that portable batteries were a commodity business—that the winning move was to find the cheapest Chinese factory and slap a brand on top. Yang refused that framing. He invested in real silicon engineering. He invested in software that could have been a feature but became a brand. He built a team in Changsha that treated consumer chargers with the same rigor that his Google colleagues treated distributed search. The results compounded for fifteen years, and the compounding is not over.

The story ahead of Anker is genuinely uncertain. The energy storage bet could transform the company into something ten times its current size, or it could disappoint and leave Anker as a very good but not transformational consumer electronics platform. The geopolitical environment could deteriorate meaningfully, forcing painful supply chain restructuring. Amazon could escalate its private label aggression and compress the core charging business. Steven Yang could decide to step back, and succession could be messier than it looks today. None of these scenarios are priced into the stock at 2026 levels, and reasonable people can disagree on the probability of each.

What is not uncertain is that what Steven Yang built, from a cafeteria lunch at Google in 2011 to a multi-billion-dollar consumer empire listed in Shenzhen by 2026, is one of the most instructive case studies in modern consumer electronics. It is a story about patience, about operational discipline, about refusing the commodity framing, about using new distribution platforms as leverage rather than as constraints, and about the compounding power of small weekly improvements to a product over fifteen consecutive years. It is a story that hundreds of founders will try to replicate in the next decade, in categories ranging from kitchen appliances to EV accessories to pet technology. Most of them will fail. The ones who succeed will, whether they acknowledge it or not, have read the Anker playbook carefully.

For long-term fundamental investors, Anker Innovations is neither a no-brainer nor a trap. It is, as the best companies usually are, a genuine test of one's framework. The bulls and the bears can both draw respectable lines on a graph and point to real evidence. What matters—what really matters—is watching the KPIs. Watch SOLIX's residential revenue. Watch consolidated gross margin. Watch offline as a share of total. Watch R&D as a share of revenue. And watch Steven Yang, who, if the past fifteen years are any guide, is probably at this moment reading a one-star Amazon review of an Anker product and asking his engineering team why.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube