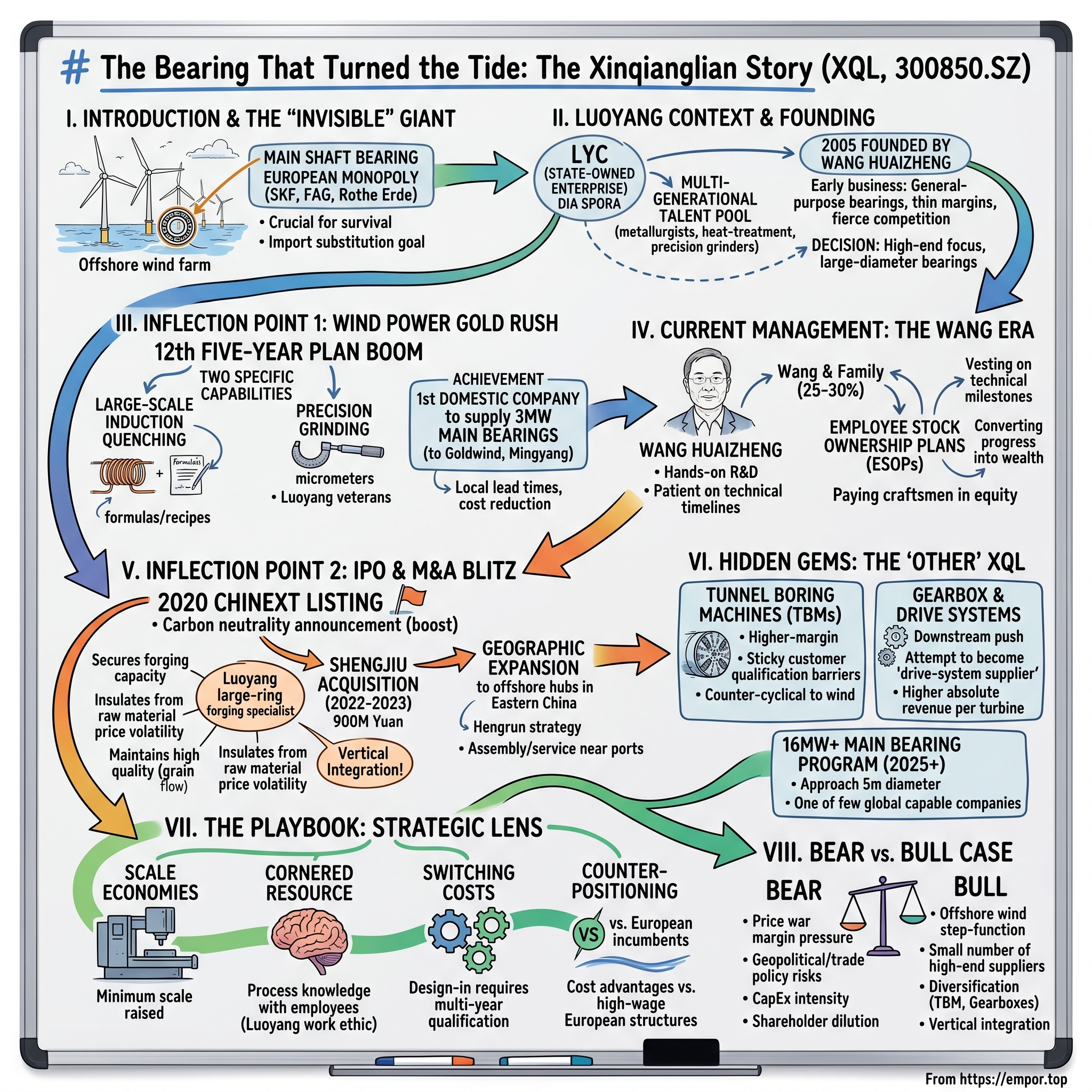

The Bearing That Turned the Tide: The Xinqianglian Story

I. Introduction & The "Invisible" Giant

Stand on a breakwater along the Pingtan Strait in Fujian on a gray October morning and watch the wind farm in the distance. The turbines look almost stationary from shore—deceptively slow, almost meditative. But each of those 180-meter-tall machines is rotating a rotor the weight of two fully loaded 737s against ocean-gale forces that peak above 50 meters per second during typhoon season. And the single component that allows the whole thing to survive—the part that cannot, under any circumstance, fail—is a ring of hardened steel, roughly three and a half meters across, buried inside the nacelle at the top of the tower.

That ring is called a slewing bearing. More specifically, a main shaft bearing. It carries the entire dynamic load of the rotor and blades, transferring it into the drivetrain. If it fails, the turbine doesn't just stop. It has to be disassembled by specialized crane vessels that charge north of a million dollars per deployment. For twenty years, every one of those rings going into a Chinese offshore turbine came from a short list of European suppliers: SKF of Sweden, Schaeffler-owned FAG of Germany, or Thyssenkrupp Rothe Erde, whose name became shorthand for "the bearing the Germans build and nobody else can."

Today, a startling share of the main bearings spinning above the East China Sea were forged, heat-treated, and ground in the dusty industrial parks of Luoyang, a second-tier city in Henan province best known for its Tang dynasty tombs and its peonies. The company stamping its name onto them is Luoyang Xinqianglian Slewing Bearing Company—listed on the ChiNext board in Shenzhen under the ticker 300850. It goes by XQL for short.

This is the story of how a private workshop founded in 2005, operating in the shadow of one of China's largest state-owned bearing enterprises, cracked a hundred-year European monopoly on the most technically demanding rolling element in heavy industry. It is also, in a more subtle sense, a story about Chinese industrial policy—about the "little giants" program, about import substitution as a deliberate act of national strategy, and about what happens when vertical integration meets a once-in-a-generation demand cycle in offshore wind.

The arc runs from a provincial forge to a 2020 IPO that priced into the teeth of China's carbon neutrality announcement, through a 900 million yuan acquisition of the forging supplier that made the whole thing work, and into a present moment where XQL is quietly shipping 16-megawatt main bearings while Western incumbents re-run feasibility studies.

Put another way: the turbines turn because the bearing turns. And for a growing share of the world's largest turbines, the bearing that turns was made in Luoyang. This is how that happened.

II. The Luoyang Context & Founding

To understand XQL, start with Luoyang. The city sits on the south bank of the Yellow River in the wheat belt of Henan province, and it has been a locus of Chinese manufacturing since the First Five-Year Plan in the early 1950s, when Soviet engineers helped designate it as one of Mao's key heavy-industry bases. Among the mills and tractor plants built in that era was one called Luoyang Bearing Corporation, or LYC. For forty years, LYC was the bearing industry in China. It made railway bearings for the Ministry of Railways, mining bearings for the coal bureaus, aerospace bearings for the state defense sector. Every engineer in the city either worked at LYC or had a brother-in-law who did.

This created an unusual labor market. By the early 2000s, Luoyang had something few industrial clusters anywhere in the world had managed to accumulate: a multi-generational talent pool of heat-treatment specialists, precision grinders, metallurgists, and forging engineers, all trained inside a single vertically integrated state enterprise. The city was called the "Bearing Capital of China" in the trade press, and it was not hyperbole. When LYC began shedding workers in the late 1990s under state-owned enterprise reform, those workers didn't leave the city. They spilled into the hundred-plus small bearing workshops that ringed the LYC campus in the industrial districts of Jianxi and Luolong.

Xinqianglian was born out of that diaspora. The company was founded in 2005 by a group of engineers and businesspeople, with Wang Huaizheng emerging as the central figure. The early business was ordinary: general-purpose slewing bearings for cranes, excavators, and industrial machinery. The customers were local OEMs in construction equipment. The margins were thin. The competition was ferocious. In that first decade there were, by industry estimates, more than two hundred firms in the Chinese slewing bearing market, and most of them were doing some version of the same thing.

The founding insight—and this is where the story begins to diverge from the two hundred other workshops—was a refusal to compete on price in the commodity segment. Management looked at the market and concluded, correctly, that the low end was a pit without a bottom. A hundred competitors could each shave a percentage point off and nobody would win. The high end, meanwhile, was empty of domestic players. Large-diameter bearings—anything over two meters across, with demanding concentricity and surface-hardness specifications—were being imported from Europe at prices that Chinese end-users grudgingly paid because there was no alternative.

The pivot was philosophical before it was technical. A small, cash-constrained workshop in Henan deciding, in roughly 2008 and 2009, that it was going to take on SKF and FAG in the most demanding product category available—that required a particular kind of ambition. But it also required a reading of where Chinese industrial demand was heading. Management saw three curves forming: the coming boom in tunnel boring machines as subway construction accelerated in dozens of Chinese cities, the early signals of the wind power installation wave under the Twelfth Five-Year Plan, and the slow but inevitable substitution of domestic content into imported-heavy capital goods. Each of those curves demanded exactly the kind of large-diameter, precision-ground, induction-quenched bearing that nobody in China was yet making at scale.

The company raised its ceiling, invested in larger grinding machines than the books said it could afford, and went looking for its first customer in wind. That search would define everything that followed.

III. Inflection Point 1: The Wind Power Gold Rush

There is a moment in every industrial company's history when the market hands it a gift, and the only question is whether management has done the preparatory work to receive it. For XQL, that moment arrived somewhere between 2011 and 2013, as China's installed wind capacity began to compound at rates that made Western analysts recheck their spreadsheets. The Twelfth Five-Year Plan called for wind to scale from roughly 45 gigawatts to 100 gigawatts by 2015. Beijing overshot the target. By the middle of the decade, China was adding more wind capacity annually than the next three countries combined.

Every one of those turbines contained, in rough terms, three categories of bearings. The pitch bearings controlled the angle of each blade. The yaw bearing controlled the rotation of the entire nacelle on top of the tower. And the main bearing—sometimes a single massive unit, sometimes split into a two-bearing arrangement—carried the rotor shaft. Pitch and yaw were difficult but manageable; by 2012 there were a handful of Chinese firms producing them with acceptable quality. The main bearing was something else entirely. It operated under combined axial, radial, and moment loads, at rotation speeds of maybe 15 to 20 revolutions per minute, for a required design life of 20 years in salt-laden offshore conditions. Nobody in China was making them. Every Goldwind, Envision, Mingyang, and Sany turbine installed through the mid-2010s had a European main bearing at its heart.

To the turbine OEMs, this was an open wound. Main bearings were among the highest-value components in the nacelle, they carried long lead times because European suppliers had limited capacity, and they had to be paid for in euros during a period when the renminbi was not particularly cooperative. Every Chinese turbine manufacturer was quietly asking the same question: would someone please localize this?

XQL's answer was a bet-the-company investment in two specific capabilities. The first was large-scale induction quenching. This is worth pausing on because it sits at the heart of the entire thesis. Imagine trying to surface-harden a steel ring nearly three meters across without warping it. Traditional oven quenching heats the whole part to more than 800 degrees Celsius and then plunges it into oil or water. A three-meter ring treated that way will deform—measurably, catastrophically, unacceptably. Induction quenching instead uses an electromagnetic coil that traces around the raceway, heating only the surface layer to transformation temperature and immediately quenching it with a water spray trailing behind. The result is a hardened surface zone, precisely controlled, over a ductile core. It is the difference between a bearing that survives 20 years in the North Sea and one that cracks in the third year.

The engineering challenge isn't the physics. It's the tooling, the process control, and the institutional knowledge. Induction quench lines for bearings this size are custom-built. The inductor geometry, the coupling distance, the traverse speed, the power profile, the quench timing—all of these are recipes, and the recipes are different for every bearing diameter, every steel grade, every raceway profile. XQL spent years accumulating those recipes, breaking rings, adjusting parameters, and building internal know-how that is not, in any meaningful sense, written down in a textbook.

The second capability was precision grinding at diameters that most machine tools could not accommodate. A 3-megawatt main bearing requires raceway roundness and surface finish specifications measured in micrometers. The grinders themselves were imported, initially from German and Japanese suppliers; the operators were Luoyang veterans; the fixtures were built in-house.

The breakthrough came when XQL became the first domestic company to pass the multi-year certification required to supply main bearings to a Chinese turbine OEM at the 3-megawatt class. It was not a headline event. It was a quiet design-in, followed by field performance data, followed by a slow ramp in supply. But for the economics of Chinese wind, it was transformational. The cost of a main bearing fell sharply, and more importantly, it became sourceable on domestic lead times.

For Goldwind and Mingyang—who would go on to become the world's two largest wind turbine makers by volume—having a reliable domestic main bearing supplier changed the calculus of every subsequent turbine generation. The OEMs could design more aggressively. They could commit to offshore projects with shorter delivery windows. And they could put sustained pricing pressure on their remaining European bearing suppliers, knowing they now had a credible alternative.

That alternative, in Luoyang, was preparing for a much bigger stage.

IV. Current Management: The Wang Era

Wang Huaizheng does not fit the mold of the Chinese tech-era founder. He does not publish think pieces on industrial policy. He does not appear on business magazine covers. His public biography is, by the standards of a chairman of a listed company, almost sparse. What emerges from filings and industry accounts is the portrait of a technical craftsman leader: someone whose authority inside the company derives from having spent decades on shop floors, in heat-treatment bays, and at the grinding lines, and whose decisions are legible mostly to other engineers.

This is not a neutral observation. A lot of Chinese industrial companies that attempted to move up the value chain in the 2010s were led by charismatic dealmakers with MBA polish. Many of them failed. The companies that succeeded in cracking high-end industrial imports tended to be led by people who could argue with a process engineer about induction frequency and who understood, from direct experience, why a particular heat-treatment schedule mattered. Wang is in that second camp. He is reportedly hands-on with R&D prioritization, directly involved in customer qualification reviews, and notoriously patient with timelines on technical programs that take years to come to fruition.

The ownership structure mirrors the management style. Wang and his family, together with concert-party entities including Luoyang Xinqianglian Investment, hold a combined stake that has historically sat in the 25 to 30 percent range of the listed company. This is meaningful for two reasons. It is tight enough to signal management conviction and alignment, but not so concentrated that minority shareholders carry outsized governance risk. And the holding is structured through entities whose economic interests are tied to long-run performance rather than short-term trading.

The more interesting mechanism, though, is the employee stock ownership plans that XQL rolled out in the post-IPO period. In 2021 and again in 2022, the company structured ESOPs that tied vesting to engineering and operational milestones rather than pure stock price targets. This matters more than it sounds. An industrial company trying to hold onto its senior metallurgists and process engineers faces a specific threat: a competitor, often state-owned, can simply poach them with a salary package. An ESOP that vests on turbine certification milestones or new-product industrialization targets does two things. It converts technical progress into personal wealth for the people actually doing the work. And it creates a disincentive to leave mid-program, because the value crystallizes at the back end.

One person close to the situation described the ESOPs as "paying the craftsmen in equity for the craft," which is almost too clean a phrase, but it captures the strategic logic. In an industry where the moat is held in human hands, the chairman chose to put the equity in those hands too.

The cultural backdrop is what local industry observers call the Luoyang work ethic. This is a city where the default shift pattern in heavy industry is still 7-on, 1-off, where the cafeteria opens before 6 a.m., and where foremen and engineers eat at the same tables. The bearing industry here is not glamorous. The margins are respectable but not spectacular. The work is dusty, hot in summer, cold in winter, and unglamorous in any weather. What XQL has done—and this is not guaranteed when a Henan industrial firm goes public—is preserve the operational discipline of a private workshop while acquiring the balance-sheet capacity of a ChiNext-listed enterprise. The engineers still show up early. The grinding lines still run three shifts. The only thing that has changed is the scale.

The question of whether that culture survives further expansion—particularly into overseas markets where the labor norms and customer expectations are different—is one of the real open questions about the next decade. For now, the Luoyang approach has held.

V. Inflection Point 2: The IPO and the M&A Blitz

XQL priced its ChiNext listing in 2020, in what in retrospect looks like one of the most fortuitously timed industrial IPOs in recent Chinese market memory. The pricing landed just ahead of President Xi Jinping's September 2020 announcement that China would target carbon neutrality by 2060, a statement that rewired capital flows into renewable energy names for the next eighteen months. Wind and solar supply chain stocks rerated. Investors who had treated bearings as a dull components business suddenly looked at XQL and saw a picks-and-shovels play on the single largest energy transition in human history.

The company used the ChiNext listing for what it was: a chance to pull forward several years of capex and to secure strategic supply-chain assets that had been running ahead of its ability to finance them. The two most consequential moves were the Shengjiu acquisition and a parallel series of capacity expansions into the offshore wind hubs of eastern China.

The Shengjiu transaction, announced and finalized across 2022 and 2023, was the one that forced every analyst covering the name to open a new model. XQL acquired Luoyang Shengjiu, a large-ring forging specialist, at a headline valuation in the vicinity of 900 million yuan. To the casual observer, this was a straightforward vertical integration—bearing maker buys its forging supplier—but the strategic logic was deeper than that.

Forging the blanks for large-diameter bearings is itself a specialist capability. The rings start as steel billets that are heated, upset, punched, and rolled on ring-rolling mills capable of producing forgings of extraordinary size. The quality of the forging—specifically the grain flow, the cleanliness, the absence of internal inclusions—directly determines the fatigue life of the finished bearing. A bearing maker that does not control its forging supplier is exposed to two things: raw-material price volatility, particularly in specialty steels, and capacity rationing during industry-wide demand surges.

XQL had been buying forgings from Shengjiu for years. In the 2021 to 2022 period, with offshore wind demand accelerating and steel prices whipsawing, the cost and timing volatility became a headline drag on margins. The acquisition converted a supplier relationship into an internal transfer-pricing arrangement, and it did something else that mattered more over the long run: it secured forging capacity for the 10-megawatt-plus class main bearings that were about to become the central product category in offshore wind.

Was 900 million yuan a fair price? The industry comps are imperfect—specialty forging companies don't trade in liquid markets—but on any reasonable multiple of normalized earnings the deal was in the range of acceptable, and on a strategic-optionality basis it was almost certainly accretive. The hardest test for vertical integration deals is usually the culture knit, and here XQL had a genuine advantage: Shengjiu was already embedded in the Luoyang industrial ecosystem, its workforce was drawn from the same multi-generational bearing talent pool, and its management was familiar to XQL's leadership from years of supplier audits and joint process development.

The second leg of the post-IPO capital deployment was geographic. Chinese offshore wind is concentrated along the eastern seaboard, from the Bohai Bay down through Jiangsu, Zhejiang, Fujian, and into Guangdong. Turbine OEMs have historically asked their major component suppliers to locate final assembly or service capacity close to port logistics, because a 16-megawatt main bearing is not something you want to truck from Henan to a shipyard. XQL's push into Jiangsu and Zhejiang—sometimes described in company materials as part of the broader "Hengrun strategy"—was about putting large-ring final assembly and service within a day's drive of the major offshore installation ports. The company committed significant capex to facilities that were sized not for the current market but for the 2028-2030 offshore wind pipeline.

There is a pattern here that's worth naming. XQL's capital allocation through this period was not pretty. The share count diluted. The capex-to-sales ratio ran well above industry averages. Working capital swelled. By any short-term financial metric, management was reinvesting more aggressively than a steady-state industrial company would. But the reinvestment was directed almost entirely at two things: vertical integration on the supply side and geographic/product positioning on the demand side. In a cycle where offshore wind was about to take a step-function up in turbine size, those were precisely the two places to be spending.

That step-function was coming faster than most Western analysts realized.

VI. Hidden Gems: The Other XQL

Spend enough time with XQL's disclosures and a picture emerges that the headline narrative misses. Wind bearings are the engine—by 2024 they accounted for well above 80 percent of revenue, and in some segments considerably more—but there are two other businesses inside the company that quietly shape the investment case.

The first is tunnel boring machines. If you have ridden the Beijing, Shanghai, Shenzhen, Chengdu, or Wuhan subway systems in the past decade, you have passed through tunnels cut by TBMs. These are the spectacularly large machines—some more than 15 meters in diameter—that chew through rock and soil at a few meters per hour, lining the tunnel behind them with precast segments as they go. At the front of every TBM is a cutterhead, and supporting that cutterhead is a main bearing that has to rotate a piece of equipment weighing thousands of tons while absorbing tremendous thrust and moment loads from the tunnel face.

For decades, the main bearings in the world's TBMs came from the same European suppliers that made wind turbine bearings. Rothe Erde. SKF. IMO. The technical overlap with large-diameter wind bearings is substantial, and XQL moved into TBM bearings as a natural extension of its wind capability. What it found was a market that is smaller than wind but considerably stickier and, in many segments, higher-margin. TBM projects are multi-year; the bearings are single-unit, high-value products; and the qualification barriers are genuinely prohibitive for new entrants. A city transit authority in Chengdu or Zhengzhou is not shopping for the cheapest bearing. It is shopping for a bearing whose supplier has a track record and whose failure would not result in a stalled 2-billion-yuan tunneling project.

The TBM business also has a very different cyclicality profile than wind. Chinese subway construction is running at elevated rates through the late 2020s as second- and third-tier cities extend their networks, and export demand from Southeast Asia, the Middle East, and increasingly Europe is adding incremental volume. Where wind has experienced periodic capacity gluts and tariff-driven price pressure, TBM bearings have been a steady, quietly profitable drag-anchor.

The second adjacent business is industrial gearboxes and drive systems. This is the more strategically ambitious move. Historically, XQL made the bearing that went inside the gearbox. The gearbox itself was made by someone else—ZF, Winergy, or a Chinese peer. By pushing downstream into gearbox components and in some cases complete drive assemblies, XQL is attempting to move up the value stack from "bearing maker" to "drive-system supplier." This is the path that Schaeffler walked in Europe over decades, and it is the path that positions a component maker for much higher absolute revenue per turbine.

The risk is real. Moving from components into sub-assemblies puts XQL into more direct competition with some of its own customers, and it requires a set of system-integration capabilities that are different from bearing manufacturing. Management has been measured about the pace, focusing on specific gearbox applications where the bearing already dominated the cost structure. Whether this expands into a full drive-system offering over the next three to five years is one of the more interesting open questions about the business.

The third and most forward-looking piece is the 16-megawatt-plus main bearing program. In 2025 and into 2026, the global offshore wind market crossed into a new product regime. The largest turbines being installed off the coasts of Guangdong, Jiangsu, and increasingly also Vietnam, the UK, and Germany are rated at 16 to 20 megawatts. These are machines with rotor diameters north of 250 meters and main bearings whose outer diameters approach five meters. The number of companies in the world that can produce a main bearing at that scale, with the required precision and fatigue life, can be counted on one hand. XQL is on that hand. It is one of perhaps three or four companies globally—alongside Rothe Erde and, depending on the specific configuration, SKF—with commercial-volume capability at the top of the range.

That is a structurally different competitive position than the one XQL occupied a decade ago, when it was trying to prove it could make a 3-megawatt bearing at all. The frontier has moved, and XQL moved with it.

VII. The Playbook: Seven Powers and Five Forces

If you run XQL through Hamilton Helmer's Seven Powers framework—the strategic lens that has quietly become the dominant analytical vocabulary among thoughtful industrial investors—three of the seven powers show up as genuinely durable, and a fourth is on the boundary.

Scale economies come first. A grinding machine capable of finishing a five-meter-diameter bearing raceway to the required surface finish costs tens of millions of yuan and takes more than a year to commission. An induction quench line for bearings at that scale is similarly capital-intensive. The minimum efficient scale in high-end wind main bearings is not a question of running three shifts versus two; it is a question of whether your capex base supports 16-megawatt production at all. XQL's post-IPO capex binge was, in effect, a deliberate push to raise the minimum scale of competition high enough that regional competitors could not follow. It has worked. The number of Chinese firms capable of bidding credibly into the 10-megawatt-plus main bearing segment is small and shrinking.

Cornered resource shows up in the process knowledge, and this is the least obvious of the moats. There is a temptation to look at a bearing and think, "it's a ring of steel, how hard can it be?" The answer is that the specific induction-quench recipes, the forging schedules, the grinding sequences, and the final inspection protocols that produce a main bearing with a 20-year offshore design life are not documented in public literature. They are held in the heads and hands of a specific cohort of senior engineers in Luoyang. XQL has, through its ESOPs and its cultural approach, invested unusually heavily in keeping those people inside the company. The cornered resource here is not a patent or a license; it is a labor pool with a particular multi-decade specialization and incentives to stay.

Switching costs are the third, and they are structural rather than contractual. When Mingyang designs a next-generation offshore turbine, it spends two to three years qualifying the main bearing supplier. That qualification involves load-case analysis, finite element modeling, full-scale rig testing, and eventually field demonstration. Once a bearing is designed in, swapping to a different supplier requires redoing meaningful portions of that qualification. The result is that XQL's incumbency with the major Chinese turbine OEMs is considerably stickier than a typical components supplier relationship. It is also why the company's main bearing business tends to lock in multi-year visibility on a platform-by-platform basis.

The fourth power—counter-positioning—is present in a limited but interesting form. The European incumbents, SKF and Schaeffler and Rothe Erde, have cost structures built around high-wage European manufacturing, legacy pension obligations, and dividend-paying public parent companies. They cannot easily respond to XQL's pricing in the volume segment of the wind market without cannibalizing their own economics. They have responded instead by emphasizing highest-end offshore and niche applications. This is a classic counter-positioning dynamic, and it has created room for XQL to operate without triggering a full competitive response.

Run the same company through Porter's five forces and the picture is equally informative. Threat of new entrants is extraordinarily low, both because of the capex barrier and because of what one supply chain director called "the trust barrier"—the multi-year field data required before any new supplier is accepted onto a turbine platform. Threat of substitutes is low in any meaningful engineering sense; alternative drivetrain architectures, including direct-drive designs, still require bearings, just configured differently. Supplier power is the barrier XQL addressed by acquiring Shengjiu, converting an external dependency into an internal capability.

Bargaining power of buyers is the most real of the five pressures. The Chinese wind OEM market is highly concentrated—Goldwind, Envision, Mingyang, and a small handful of others account for the overwhelming majority of domestic turbine production—and that concentration gives buyers significant leverage on pricing. This is precisely why XQL's push into TBM bearings and drive systems matters strategically. It diversifies revenue into segments with different customer concentration profiles and more favorable pricing dynamics.

Industry rivalry, finally, is intense in the commoditized pitch and yaw bearing segments and considerably less intense in large-diameter main bearings. This bifurcation is not an accident. It is the result of the capex and knowledge barriers discussed above, and it is the single most important structural feature of the market XQL has built itself into.

VIII. Bear vs. Bull Case

The bear case on XQL is not hard to articulate, and a sober investor has to take it seriously.

Start with the Chinese wind market itself. Installed capacity targets have been met and exceeded. The country is not going to continue adding onshore wind at the pace of the early 2020s. Turbine manufacturer pricing has been under sustained pressure—the so-called "price war" among Chinese wind OEMs through 2023 and 2024 drove turbine ASPs down by margins that would have been unthinkable a decade ago, and those pressures propagated upstream into component suppliers. Bearing manufacturers, including XQL, have had to absorb some of that squeeze. Gross margins in pitch and yaw bearings have been under pressure for several years.

Overseas expansion into European and American markets—the natural next growth vector—runs directly into the buzz saw of geopolitical and trade policy. The European Union has been increasingly vocal about Chinese clean energy component imports, and anti-dumping or anti-subsidy investigations remain a persistent overhang. The United States is effectively closed to XQL in any direct sense for Chinese-manufactured renewable components. Exports to Southeast Asia and the Middle East have been a growth area, but those markets are smaller and carry their own execution risks.

Then there is the pure CapEx intensity of the business. XQL is not a software company and will never have software-like margins. Every incremental growth dollar requires substantial upfront investment in machinery, facilities, and working capital. In a downturn, those assets are not easily repurposed. The company is structurally more cyclical than a diversified industrial.

Finally, there is the issue of shareholder dilution. The post-IPO period has seen a measurable increase in share count, partly through ESOPs and partly through strategic issuances tied to acquisitions and capex programs. Minority shareholders have been partially funding the growth, and while the capital has been deployed into strategically sensible projects, the per-share economics have been less attractive than the absolute growth numbers suggest.

The bull case, by contrast, rests almost entirely on the offshore wind step-function. The global offshore wind pipeline through 2030 calls for installations at a scale that was considered fanciful ten years ago. The average turbine size continues to creep up. The number of bearing suppliers qualified to produce at the very top of the size range is small. Every 16-megawatt turbine installed at sea consumes bearing content that is several multiples of what a 3-megawatt onshore turbine consumed a decade ago, and the pricing power in those top-end bearings is meaningfully better than in the commodity range.

On top of that, the TBM business is a steadier secondary growth vector that smooths the wind cyclicality. The drive-system expansion, if it plays out, opens a pathway to higher absolute revenue per turbine over time. And the vertical integration with Shengjiu provides both a margin cushion and a strategic capacity moat that is difficult for any non-integrated competitor to replicate.

The competitive landscape is useful context for both cases. SKF, the Swedish global leader, remains formidable in precision bearings across many applications, but it has been conservative in its capacity expansion at the very largest wind sizes. Schaeffler, with its FAG brand, is integrated into automotive and industrial markets and is not optimized specifically for offshore wind. Thyssenkrupp Rothe Erde is perhaps the purest competitor in large-diameter slewing bearings, and it has invested in capacity, but it operates with a European cost structure. Among Chinese peers, ZWZ and LYC are the legacy giants with enormous product breadth but less focused wind execution. The space XQL occupies—specialized, focused, and vertically integrated in large-diameter wind bearings—is defensibly narrow.

The KPIs worth tracking, if an investor wants to stay close to the ongoing performance of the business, come down to three. The most important is gross margin on main bearings, reported separately where disclosure allows, because it is the single best indicator of the mix shift between commodity and specialty product. The second is R&D as a percentage of sales, because the business runs on process knowledge and technical advancement, and a sustained commitment of research spend is the closest signal to long-run competitive durability. The third is capital expenditure intensity—specifically the ratio of capex to depreciation—because in a business where the next product generation requires new tooling, a sustained elevation of capex signals that management continues to push the frontier.

There is a fourth signal that is harder to track but worth watching: qualification announcements with global turbine OEMs beyond the Chinese domestic players. If XQL makes inroads into the supply chains of Vestas or Siemens Gamesa in a meaningful way, the bull case expands considerably. If it does not, the story remains a China-focused renewable industrialist with excellent domestic positioning. Both are interesting businesses; they are different businesses.

One piece of accounting discipline worth flagging for the diligent reader: XQL's inventory and receivables have grown at a pace that reflects both the project nature of its end markets and the extended working capital cycles of wind OEM customers under pricing pressure. This is visible in the cash conversion dynamics and merits ongoing monitoring. It is not an aggressive accounting signal; it is an industry-wide feature of wind supply chains in the current cycle.

IX. Conclusion & Final Reflections

There is a term in Chinese industrial policy, zhuan jing te xin—often translated as "specialized, refined, differentiated, and novel," and typically shortened to the "little giants" designation. Beijing has used the program to identify medium-sized enterprises that dominate narrow but strategically important technology niches, the kind of firms that in Germany would be called Mittelstand hidden champions. XQL is a textbook little giant. It is not a household name. It will never sell a consumer product. Its entire existence is oriented toward solving one hard industrial problem exceptionally well, and using that solution to earn a defensible position in a market that touches the lives of hundreds of millions of people without their ever knowing it.

Zoom out and the arc of the story becomes clearer. Luoyang in 1955 was a Soviet-planned bearing city. Luoyang in 1995 was a state-owned monolith shedding workers. Luoyang in 2005 was a hundred small workshops competing at the bottom of a commodity market. Luoyang in 2015 was the home of the first domestic 3-megawatt main bearings. Luoyang in 2025 was shipping 16-megawatt main bearings into the largest offshore wind projects in the world. That sixty-year compounding of institutional knowledge—passed through a state enterprise to a diaspora of workshops to a listed, vertically integrated specialist—is the real underlying asset.

The capital allocation record through XQL's listed life is defensible but not flawless. The Shengjiu integration looks, with three years of hindsight, like a genuinely strategic move that secured the company's position at the top end of the wind bearing market at a reasonable price. The capex-heavy expansion into eastern China offshore hubs was the right call ahead of the 16-megawatt cycle. The ESOPs tied to engineering milestones were an unusually thoughtful way to keep technical talent aligned through a period of rapid growth. Set against those, the share count dilution and the working capital expansion are real, and they are the ongoing tension in the story.

What remains to be seen, from this vantage point in 2026, is whether XQL can take the same playbook—technical obsession, vertical integration, patient capital deployment—and extend it into two harder arenas. The first is overseas markets, where the company's ability to win business in European and Southeast Asian wind projects will determine whether it is a Chinese champion or a global one. The second is the move up the stack into drive systems and gearbox components, which if executed converts XQL from a bearing specialist into a platform supplier with materially higher revenue per turbine.

Both of those transitions are bet-the-company-adjacent decisions, and both are currently in motion. The outcome is genuinely uncertain. What is not uncertain is that the engineers in Luoyang have, across two decades, accumulated a set of capabilities that almost nobody in the world can match at the top end of wind bearings. The question is no longer whether they can make the bearing. The question is what they build with it.

Stand back on that breakwater in Fujian and watch the turbines turn. The blades slice the sea air. The generator spins. And at the heart of each machine, a ring of Luoyang steel rotates through another hour of its 20-year life, bearing the weight of a sliver of the energy transition. That ring, and the firm that makes it, is one of the less visible but more consequential industrial stories of this decade. It is the bearing that turned the tide.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube