CATL: The Emperor of Energy

I. Introduction: The TSMC of the 21st Century

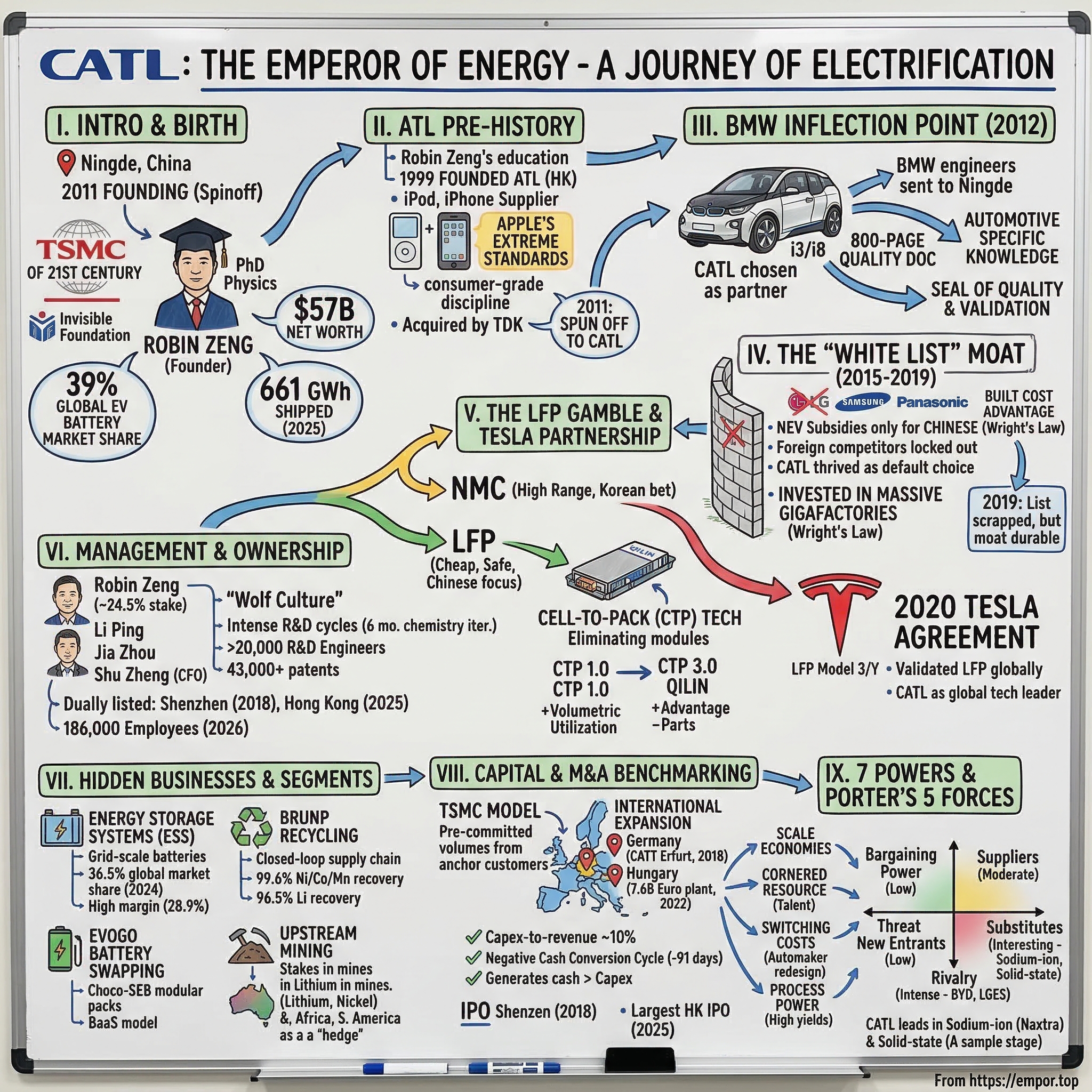

If you own an electric vehicle, there is a 37% chance the heart of your car was built by one company. Not in Detroit, not in Stuttgart, not in Nagoya. In Ningde — a humid coastal city in Fujian Province, China, that most people outside the country have never heard of. The company is Contemporary Amperex Technology Co., Limited, or CATL, and its rise to global dominance is one of the most extraordinary industrial stories of the 21st century.

Consider the sheer improbability. In 2011, CATL did not exist. It was a spinoff — a carve-out from a mid-sized consumer electronics battery maker that most auto executives had never heard of. Fourteen years later, it commands roughly 39% of the global EV battery market, more than double its nearest competitor. It shipped 661 gigawatt-hours of batteries in 2025 alone, enough to power approximately 10 million electric vehicles. Its market capitalization on the Shenzhen Stock Exchange hovers around 1.77 trillion yuan, and its Hong Kong secondary listing in May 2025 was the largest IPO anywhere in the world that year. Its founder, Robin Zeng, is worth approximately $57 billion.

The comparisons to TSMC are not accidental. Just as Taiwan Semiconductor Manufacturing Company became the indispensable chokepoint in global chipmaking — the company that everyone from Apple to Nvidia depends on, the company that entire geopolitical strategies revolve around — CATL occupies a similar position in the electrification of transportation. Tesla depends on it. BMW depends on it. Volkswagen, Hyundai, Stellantis, Mercedes-Benz — they all depend on it. When the world decided to stop burning gasoline, it inadvertently created a new kind of monopoly, and that monopoly sits in a city of three million people on the coast of the Taiwan Strait.

But the TSMC analogy runs deeper than market share. Like TSMC, CATL is not a brand that consumers interact with directly. Nobody walks into a dealership and says "I want the CATL battery." And yet, like TSMC's silicon, CATL's cells are the invisible foundation upon which an entire industry is being rebuilt. The transition from the Oil Age to the Electron Age runs through Ningde. This is the story of how that happened — and what it means for the companies, countries, and investors trying to navigate the most important industrial transformation since the internal combustion engine.

The thesis is simple but profound: CATL did not win because it was Chinese, though China helped. It did not win because it was cheap, though its costs are extraordinary. CATL won because a physicist from a farming village understood something that the legacy auto industry did not — that batteries are not commodities to be sourced from the lowest bidder, but precision-engineered systems that reward relentless iteration, vertical integration, and scale. CATL built the Great Wall of Batteries, and everyone else is still trying to figure out how to climb over it.

II. Pre-History: The ATL Foundation

The story of CATL begins not in a laboratory or a boardroom, but on a farm. Robin Zeng — Zeng Yuqun in Mandarin — was born in March 1968 in a village outside Ningde. His family were farmers, and in the China of the late 1960s, that was very nearly a destiny. But Zeng was academically gifted, and through a combination of talent and determination that would define his career, he tested into Shanghai Jiaotong University, one of China's elite institutions, where he studied marine engineering.

After graduating, Zeng did what was expected: he took a position at a state-owned shipbuilding company in Fujian Province. It was a safe, respectable job in the socialist system. He lasted about three months. The bureaucracy and the pace drove him crazy. "I didn't want to see my life at sixty while I was still in my twenties," he later said. He quit and joined an electronic parts factory, where he spent the next decade learning the rhythms of manufacturing — quality control, yield rates, the unglamorous discipline of making the same thing a million times without variation. It was the education of a future industrialist, even if nobody knew it yet.

In 1999, Zeng co-founded Amperex Technology Limited — ATL — in Hong Kong with two former colleagues. Their business was lithium polymer batteries for consumer electronics: laptops, MP3 players, the kind of devices that were about to explode in the early 2000s. The timing was impeccable. ATL acquired technology licenses from Bell Labs and began manufacturing batteries at a time when portable electronics were becoming ubiquitous. By 2003, ATL had caught the attention of the most important consumer electronics company on the planet: Apple. ATL became the battery supplier for the original iPod, and eventually for iPhones and other Apple products. This was the relationship that taught CATL everything it needed to know about building batteries at scale.

Working for Apple is an education in a very specific kind of excellence. Apple's quality standards are legendarily demanding. Defect rates that any other customer would accept are cause for rejection. Supply chain discipline is absolute. If you can make batteries for Apple — at Apple's volumes, at Apple's defect tolerance, at Apple's price points — you can make batteries for anyone. This "consumer grade" discipline became embedded in ATL's DNA, and it would later give CATL an enormous advantage over legacy automotive battery suppliers who had grown up in a much more forgiving environment. Traditional auto suppliers measured defect rates in parts per million. Apple measured them in parts per billion.

In 2005, Japan's TDK Corporation acquired ATL, providing capital and global distribution. Zeng continued as a senior manager, but by the late 2000s, he was increasingly interested in a market that TDK had little appetite for: automotive batteries. The global auto industry was beginning to talk seriously about electrification, and Zeng saw the opportunity with the clarity of someone who had spent his career understanding battery chemistry at the cellular level.

Here is where the founding myth of CATL takes shape. TDK, as a Japanese conglomerate, was wary of the automotive battery business. The investment cycles were long, the customers were demanding, and the technology risk was substantial. More importantly, TDK was watching the Chinese government's early signals about requiring domestic ownership of critical EV supply chain assets. A Japanese-owned company making EV batteries in China would face regulatory headwinds.

In 2011, Zeng and his lieutenant Huang Shilin led a group of Chinese investors to acquire an 85% stake in ATL's automotive battery operations, spinning them off into a new entity: Contemporary Amperex Technology Co., Limited. TDK retained a 15% stake, which it would sell by 2015. The carve-out was clean, the assets were modest, and the company was unknown.

But there was something in the water — or more precisely, in the culture. CATL's founding team brought with them a decade of consumer electronics manufacturing discipline. They understood yield rates, rapid iteration, and the relentless pursuit of cost reduction at scale. Legacy auto battery suppliers like Panasonic and Samsung SDI came from the same consumer electronics world, but they had spent years adapting to the automotive industry's slower cadences. CATL arrived without those bad habits. It was building car batteries with the speed and precision of a smartphone battery factory, and that difference would prove decisive.

Meanwhile, Zeng was accumulating academic credentials that would shape his technical vision. He had earned a master's degree in electronics and information engineering from South China University of Technology in 2001, and in 2006, he completed a PhD in physics at the Chinese Academy of Sciences. This was not a ceremonial degree. Zeng remained deeply involved in battery chemistry, and his academic work informed CATL's research agenda in ways that set it apart from competitors led by business executives rather than scientists. He was, and remains, a physicist who runs a company, not a businessman who employs physicists.

III. The BMW Inflection Point

In 2012, one year after CATL was founded, something happened that should have been impossible. BMW — Bayerische Motoren Werke, one of the most quality-obsessed automakers on earth, a company that will reject a supplier over a surface finish measured in microns — chose CATL as its primary battery cell partner for the Brilliance BMW joint venture in China. The company was twelve months old. It had no track record in automotive. It was competing against Panasonic, which had been making batteries for Toyota's Prius since the 1990s, and Samsung SDI, which had the backing of South Korea's largest conglomerate.

How did a one-year-old startup win a contract with BMW? The answer reveals something fundamental about CATL's strategy and Robin Zeng's understanding of what automotive customers actually need.

BMW was developing the i3 and i8, its first serious electric vehicles, and it needed a battery partner in China that could deliver cells meeting German automotive standards. The obvious choices — LG Chem, Samsung SDI, Panasonic — were all viable, but they were also Japanese and Korean companies operating in a Chinese market that was beginning to signal strong preferences for domestic suppliers. BMW needed a Chinese partner, and CATL was the only Chinese company with even a plausible claim to consumer-electronics-grade battery manufacturing discipline, thanks to its ATL heritage.

But winning the contract was only the beginning. What followed was one of the most consequential technology transfers in modern industrial history. BMW sent engineers from Munich to Ningde — not for a week, not for a month, but for extended rotations that lasted years. They brought with them an approximately 800-page document detailing German automotive quality standards for battery cells. Every specification, every test protocol, every failure mode analysis, every environmental tolerance — it was all in there. CATL engineers were expected to internalize it, implement it, and prove compliance through rigorous testing.

This was not a partnership of equals. BMW was the teacher, and CATL was the student. But CATL was a very fast student. The ATL veterans on staff had already internalized the discipline of building to extreme quality standards — they had done it for Apple. What BMW added was automotive-specific knowledge: thermal management under crash conditions, vibration tolerance over hundreds of thousands of miles, degradation curves over decade-long lifespans. These were dimensions that consumer electronics batteries never had to worry about.

The BMW relationship did something even more valuable than technology transfer: it gave CATL a seal of quality that money could not buy. When other automakers — Volkswagen, Daimler, Hyundai — began looking for battery suppliers in China, CATL could point to the BMW partnership and say, effectively, "If we are good enough for BMW, we are good enough for you." This is a dynamic that repeats throughout industrial history. Boeing's early customers served the same function for the 707 that BMW served for CATL: they were not just customers, they were validators. CATL used the BMW contract to skip the "untrusted startup" phase entirely. By 2014, it was being treated as a credible alternative to Panasonic and LG by virtually every major automaker, a status that would have taken a decade to achieve through organic reputation-building.

BMW continued to deepen the relationship. In 2018, BMW committed to purchasing four billion euros worth of battery cells from CATL. In 2022, the two companies signed a framework agreement for CATL to supply cylindrical cells for BMW's NEUE KLASSE platform, the architecture that would underpin BMW's next generation of electric vehicles starting in 2025. CATL dedicated production capacity of up to 20 gigawatt-hours at two plants — one in China and one in Europe — specifically for BMW.

The lesson is worth dwelling on. CATL did not win by being the cheapest or the most innovative. It won by being teachable. Robin Zeng understood that the fastest path to credibility was to find the most demanding customer in the market and submit completely to their standards. The humility of the student became the authority of the graduate. By the time other Chinese battery makers tried to follow the same path, CATL was already two or three product generations ahead, and it had relationships with every major automaker that competitors could not replicate.

IV. The "White List" and the Regulatory Moat

In March 2015, China's Ministry of Industry and Information Technology issued a document with the bureaucratic title "Standard Conditions for the Automobile Power Storage Battery Industry." Behind the bland language was one of the most consequential industrial policies of the decade. The document created a catalogue — quickly nicknamed the "white list" — of recommended EV battery suppliers. The mechanism was elegant in its simplicity: automakers operating in China were eligible for New Energy Vehicle subsidies only when they installed batteries from companies on the list. And the list included exactly zero foreign companies.

To understand the impact, you have to understand the scale of China's EV ambitions. By 2015, China was already the world's largest automobile market, and the government had committed tens of billions of dollars in subsidies to accelerate EV adoption. These subsidies were not marginal — they could represent 30-40% of an EV's sticker price for consumers. No automaker could afford to ignore them. And if you wanted the subsidies, you needed a Chinese battery.

The effect on foreign competitors was devastating. LG Chem had opened a battery factory in Nanjing in 2015 with capacity to supply more than 100,000 electric vehicles annually. The plant never made it onto the white list. By 2017, LG sold the factory to Geely. Samsung SDI suspended the second phase of its Xi'an production base. Both companies had invested hundreds of millions of dollars in Chinese manufacturing capacity that was effectively rendered worthless by a regulatory decision.

Meanwhile, CATL thrived. As one of the most prominent companies on the white list — and the only one with BMW's stamp of approval — it became the default choice for virtually every automaker in China. Volkswagen needed batteries for its Chinese EV program? CATL. Hyundai wanted to sell electric vehicles in Shanghai? CATL. Toyota, historically committed to its own battery partnerships, found itself directed toward CATL if it wanted to participate in the subsidy system. The white list didn't just protect CATL from competition; it funneled the entire Chinese market — the largest EV market on earth — directly to its door.

But here is where the story becomes more than just a tale of regulatory capture. What CATL did with its protected window was far more important than the protection itself. Between 2015 and 2019, CATL invested aggressively in manufacturing capacity, building what can only be described as the mother of all gigafactories. While competitors were locked out, CATL was driving costs down the learning curve at a pace that no one could match. Every doubling of cumulative production volume brought predictable cost reductions — this is Wright's Law, the manufacturing equivalent of Moore's Law, and CATL was riding it harder than anyone.

By 2016, the white list included 57 companies, all Chinese. But within that group, CATL was pulling away from domestic competitors too. Its consumer-electronics DNA, its BMW quality certification, and its increasingly massive scale gave it advantages that smaller Chinese players like CALB, EVE Energy, and Gotion High-Tech could not match. The white list created a protected domestic market, but CATL dominated that market through genuine operational superiority.

On June 21, 2019, China's MIIT scrapped the white list, officially opening the Chinese market to foreign battery manufacturers. LG Energy Solution, Samsung SDI, and Panasonic could now compete freely. But the window had served its purpose. By 2019, CATL's cost structure was so far ahead that reopening the market barely mattered. The company had used four years of protection to build a cost advantage that would have taken a decade to achieve in an open market. When LG and Samsung returned, they found themselves competing against a company that had already achieved economies of scale they could not match without years of investment and customer acquisition.

This is the playbook that critics of Chinese industrial policy point to — and that admirers study with envy. The white list was protectionism, plain and simple. But it was protectionism in service of building genuine competitive advantage, not in service of propping up an uncompetitive industry. CATL emerged from the white list era not as a hothouse flower that would wilt in open competition, but as a hardened competitor with the lowest costs, the largest installed base, and the deepest customer relationships in the industry. The regulatory moat had become an economic moat, and that transformation is what made the white list era so consequential.

For investors, the key question about the white list era is not whether it was fair — it obviously was not — but whether its effects are durable. The answer appears to be yes. CATL's scale advantages compound over time. Every new gigawatt-hour of installed capacity drives procurement costs lower, manufacturing yields higher, and the fixed cost of R&D gets spread across a larger revenue base. Competitors who were locked out for four years lost more than four years of market position — they lost four years of learning-curve progress that they may never recover.

V. The LFP Gamble and the Tesla Partnership

In the battery industry, chemistry is destiny. And the chemistry wars of the 2010s reveal as much about corporate strategy and industrial philosophy as they do about electrochemistry.

There are two dominant lithium-ion battery chemistries for electric vehicles. The first is NMC — nickel-manganese-cobalt — which offers higher energy density, meaning more range per kilogram of battery. The second is LFP — lithium iron phosphate — which is cheaper, safer, and longer-lasting, but stores less energy per unit of weight. For most of the 2010s, the Western and Korean battery industries placed their bets on NMC. The logic was straightforward: consumers wanted range, range required energy density, and NMC delivered more energy density. LG Chem, Samsung SDI, and Panasonic all focused their R&D on pushing NMC energy density higher.

CATL made a different bet. While it continued to develop NMC cells — and remains one of the world's leading NMC producers — it also invested heavily in LFP. Robin Zeng's insight was characteristically contrarian: the energy density gap between LFP and NMC was a real problem, but it was an engineering problem, not a physics problem. If you could not pack as much energy into each cell, you could instead pack the cells more efficiently into the battery pack. This is the idea behind Cell-to-Pack, or CTP, technology — one of the most important innovations in battery engineering in the past decade.

To understand CTP, imagine a traditional battery pack as a bookshelf. Each book is a cell. Traditionally, the books are organized into smaller groups — modules — which are then placed on the shelf. The modules add structural support and wiring, but they also take up space. CTP eliminates the modules entirely, placing the cells directly into the pack, like putting books directly on the shelf without dividers. The result is dramatically higher volumetric utilization — more energy in the same physical space.

CATL announced CTP 1.0 at the Frankfurt Motor Show in September 2019. It boosted volumetric utilization to roughly 55%, reduced parts count by 40%, and improved production efficiency by 50%. The first application was in the BAIC EU5. But it was CTP 3.0, unveiled in June 2022 under the brand name "Qilin," that changed the game. Qilin achieved 72% volumetric utilization — the highest in the world — with an energy density of 255 Wh/kg for NMC cells and 160 Wh/kg for LFP cells. The breakthrough was a large-surface cell cooling design that increased heat transfer area by four times, enabling hot start in five minutes and fast charging in ten minutes. CATL claimed, with some justification, that Qilin delivered 13% more power than Tesla's much-hyped 4680 cell in the same pack volume.

The Qilin announcement was a statement of technical supremacy. But it was the Tesla partnership that proved CATL's LFP strategy was not just technically sound, but commercially transformative.

The relationship began with preliminary discussions in 2019, confirmed by a formal supply agreement in February 2020. CATL would supply LFP batteries to Tesla for the Model 3 and Model Y assembled at Gigafactory Shanghai, initially for a two-year term from July 2020 through June 2022. The agreement was later extended through December 2025.

For Tesla, the CATL partnership was a strategic pivot. Tesla had been exclusively supplied by Panasonic since the original Roadster. Panasonic's NCA (nickel-cobalt-aluminum) cells powered the Model S, Model X, and the initial Model 3. But Elon Musk had a problem: the $35,000 Model 3 — the car that was supposed to make Tesla a mass-market company — was economically marginal with NCA batteries. The raw materials alone — nickel, cobalt, aluminum — were too expensive for a true mass-market vehicle. LFP, which uses iron and phosphate instead of nickel and cobalt, was dramatically cheaper, and CATL's CTP engineering had closed enough of the energy density gap to make it viable for standard-range vehicles.

The Tesla deal was a watershed for three reasons. First, it validated LFP for Western consumers and automakers who had dismissed it as inferior Chinese technology. If Tesla — the aspirational, Silicon Valley-engineered EV brand — was using LFP, then LFP was not a compromise; it was a choice. Second, it established CATL as a global technology leader, not just a "subsidized Chinese player." The narrative shifted from "CATL is big because China protects it" to "CATL is big because it builds better batteries." Third, it accelerated the global adoption of LFP. By 2024, LFP accounted for roughly 45% of global EV battery installations, up from less than 20% in 2019. CATL's bet on the cheaper, safer chemistry had paid off enormously, and its early investment in CTP gave it a structural advantage in LFP packs that competitors are still struggling to match.

For investors watching the battery space, the LFP story illustrates a critical principle: in manufacturing businesses, the winning strategy is often not the one that maximizes the performance of each individual component, but the one that optimizes the system. CATL won not by making the best cell, but by making the best pack — and by understanding that cost, safety, and longevity would ultimately matter more than raw energy density for the mass market.

VI. Current Management and Ownership Structure

Robin Zeng's office in Ningde reportedly features a piece of calligraphy that reads, in classical Chinese, "Fortune favors the bold." This is notable because the traditional calligraphy that Chinese executives display — the equivalent of a motivational poster in a Western office — typically reads something like "Hard work pays off" or "Perseverance leads to success." Zeng's choice is more revealing than he perhaps intends. He is not a grinder. He is a gambler. A calculated one, certainly — a physicist who thinks in probabilities rather than certainties — but a gambler nonetheless. He bet on automotive batteries when TDK would not. He bet on LFP when the world was buying NMC. He bet on scale when competitors were hedging. And he bet on himself, maintaining a roughly 24.5% ownership stake in CATL that has made him one of the thirty wealthiest people on earth, with a fortune of approximately $57 billion.

Zeng's leadership style is often described by employees and observers as intense. The culture at CATL headquarters in Ningde is sometimes characterized as a "wolf culture" — a term borrowed from Huawei that implies high pressure, high performance, and limited tolerance for mediocrity. R&D cycles are punishing. CATL iterates battery chemistry every six months, compared to the 18-24 month cycles typical of Korean and Japanese competitors. The compensation structure is heavily weighted toward patent generation, yield improvements, and technical milestones. This is not a company that rewards seniority or process adherence. It rewards results.

The management team around Zeng reflects the company's evolution from a battery laboratory to a global industrial enterprise. Li Ping serves as Executive Vice Chairman, having been with the company since its founding. Jia Zhou, another Executive Vice Chairman born in 1978, represents the younger generation of leadership. Pan Jian serves as Executive Co-Chairman. The CFO, Shu Zheng, oversees a finance function that has scaled from managing a single Chinese factory to coordinating capital allocation across manufacturing operations on three continents.

What is interesting about the management structure is how it has professionalized without losing its technical core. Many global industrial companies undergo a transition from founder-led to professionally managed, and in the process they lose the technical intensity that made them successful. CATL has not. Zeng remains deeply involved in technical decisions. The R&D organization employs more than 20,000 people across six global research centers, and Zeng personally reviews major technical milestones. The company held over 43,000 patents and patent applications as of the end of 2024 — roughly 25,400 domestic and 17,900 international — a portfolio that rivals those of companies ten times its age.

There is a telling anecdote that captures Zeng's self-image. When NIO founder Li Bin joked publicly that all EV makers "have to make money for Robin Zeng," Zeng's response was disarming: "We're just making bricks." The humility is partly performative — you do not build a $57 billion fortune by being genuinely modest — but it also reflects a genuine industrial philosophy. CATL sees itself as the essential building block of the electrification age, the company that makes the thing that makes the thing work. The "Intel Inside" of EVs, if Intel Inside actually mattered.

One important governance note for investors: CATL's dual listing — Shenzhen since June 2018 and Hong Kong since May 2025 — creates a shareholder base that spans domestic Chinese institutional investors, retail traders on the ChiNext board, and global institutional investors who accessed the stock through the Hong Kong listing. Zeng's 24.5% stake gives him effective control, but the company is subject to Chinese securities regulations that differ materially from Western norms in areas like related-party transactions, disclosure timing, and minority shareholder protections. The total employee count reached approximately 132,000 by the end of 2024 and has reportedly grown to nearly 186,000 by early 2026, driven largely by international expansion. R&D spending exceeded 22 billion yuan in 2025, representing about 5.2% of revenue — a ratio that positions CATL among the most R&D-intensive industrial companies in the world.

VII. Hidden Businesses and Segment Analysis

The casual observer knows CATL as a battery company. The informed investor knows it as at least four companies operating under one roof, and the fastest-growing one is not what you would expect.

Start with Energy Storage Systems, or ESS. This is the business that does not make batteries for cars — it makes batteries for the electrical grid. When a solar farm generates more power than the grid needs at noon, that excess energy has to go somewhere. When a wind farm produces power at three in the morning and nobody is using it, that power needs to be stored. Grid-scale energy storage is one of the most important enabling technologies of the clean energy transition, and CATL is the dominant player.

In 2024, CATL's energy storage battery sales reached 93 gigawatt-hours, up 34% year-over-year, generating 57.3 billion yuan in revenue — roughly 16% of the company's total sales. The gross profit margin on ESS was 28.9%, the highest of any CATL business segment, exceeding even its EV battery margins. CATL held a 36.5% share of the global energy storage battery market in 2024, the top position for four consecutive years. In 2025, ESS system integration shipments grew by more than 160% year-over-year, and the segment's gross margin of 26.8% continued to surpass the power battery business at 23.9%.

The ESS business matters for investors because it represents a second major growth vector that is substantially independent of the automotive cycle. Even if global EV sales growth decelerates — and there are reasonable arguments that it will in some markets — grid storage demand is accelerating as renewable energy penetration increases worldwide. Every solar panel and wind turbine installed creates incremental demand for storage. CATL launched the TENER Stack in 2025, described as the world's first mass-producible ultra-large-capacity energy storage system at 9 megawatt-hours per unit, targeting utility-scale deployments. This is a product with no direct equivalent from any competitor.

Then there is Brunp, CATL's recycling subsidiary and arguably its most underappreciated strategic asset. Brunp was founded in 2005 as a consumer battery recycler, pivoted to power battery recycling in 2011, and was acquired by CATL in 2015. It operates two large industrial parks — in Yichun and Foshan — and has developed proprietary Directional Recycling Technology that achieves recovery rates of 99.6% for nickel, cobalt, and manganese, and 96.5% for lithium. In 2024, Brunp processed over 120,000 tons of waste batteries and produced 17,100 tons of recycled lithium salts.

The strategic significance of Brunp is difficult to overstate. As the first generation of EV batteries reaches end-of-life, the company that can most efficiently recover and reuse the critical minerals — lithium, nickel, cobalt — from those batteries will have an enormous cost advantage. CATL, through Brunp, is building a closed-loop supply chain. It mines lithium, manufactures it into battery cells, sells those cells to automakers, and then — years later — recovers the lithium from the spent batteries and feeds it back into the manufacturing process. No competitor has this loop operating at comparable scale. Brunp has led or participated in drafting more than 80% of China's national standards for lithium battery recycling, effectively writing the rules for the industry.

EVOGO, CATL's battery swapping initiative, represents a more speculative bet. Launched in January 2022 through subsidiary CAES, EVOGO is built around the "Choco-SEB" — Swapping Electric Block — a standardized modular battery pack based on CTP technology. Each swap station holds up to 48 blocks in a footprint of three parking spaces, and a swap takes about one minute per block. The business model is Battery as a Service: consumers buy the vehicle body and rent the battery, reducing the upfront cost of an EV by separating the most expensive component. CATL has partnered with multiple OEMs to launch compatible models, and the service has rolled out in ten cities in China.

Finally, there is the upstream mining business. CATL has taken equity stakes in lithium mines across multiple continents: an 8.5% stake in Australia's Pilbara Minerals acquired through a A$55 million placement; the Jianxiawo lithium mine in Jiangxi Province with capacity of approximately 46,000 metric tons of lithium carbonate equivalent annually; investments in the Democratic Republic of Congo, where a CATL subsidiary signed an agreement for 50% of lithium output from the Manono project; interests in Zimbabwe through the Zulu lithium-tantalum mine; and reported investments in Chile. This upstream integration follows the same industrial logic as the Brunp acquisition: control the inputs, control the costs, reduce dependence on volatile commodity markets. When lithium prices spiked dramatically in 2021-2022, CATL's upstream positions provided a natural hedge that competitors lacked.

Together, these businesses — ESS, Brunp, EVOGO, and mining — represent CATL's evolution from a battery cell manufacturer to a vertically integrated energy company. The EV battery business remains the core, accounting for roughly 70% of revenue. But the ancillary businesses provide diversification, margin enhancement, and strategic optionality that the market may not fully appreciate.

VIII. Capital Deployment and M&A Benchmarking

CATL's approach to capital allocation reveals an industrial philosophy that is closer to TSMC than to the Big Tech companies that dominate American markets. There are no headline-grabbing, bet-the-company acquisitions. No battles for social media platforms or streaming services. Instead, CATL deploys capital with the methodical discipline of a company that understands manufacturing economics at the molecular level.

The pattern is consistent: invest in capacity ahead of demand, but secure customer commitments before breaking ground. This is the "TSMC Model" of capital deployment — building factories with pre-committed volumes from anchor customers who share the construction risk through advance payments and long-term supply agreements. When CATL builds a 20-gigawatt-hour plant dedicated to BMW's NEUE KLASSE, it is not speculating on demand. It has a signed framework agreement. When it expands in Hungary, the 40-gigawatt-hour facility is, according to the company, fully booked by customers before production begins.

The international expansion tells the most interesting capital allocation story. CATL established its European subsidiary, Contemporary Amperex Technology GmbH, in Munich in 2014 — just three years after founding. The German manufacturing operation, Contemporary Amperex Technology Thuringia GmbH (CATT), broke ground in Erfurt in 2018 with an investment of 1.8 billion euros. Cell production began in late 2022, and the facility employs more than 1,700 people, with target capacity sufficient to power between 185,000 and 350,000 electric vehicles annually. This was CATL's beachhead in Europe, placing production close to its largest customers — BMW, Volkswagen, Mercedes-Benz, Stellantis — and insulating against the logistics costs and geopolitical risks of shipping cells from China.

The Hungary plant, announced in August 2022, is larger and more ambitious: 7.6 billion euros, 40 gigawatt-hours of annual capacity, with mass cell production expected to begin in early 2026. This is one of the largest single industrial investments in Hungarian history, and it positions CATL at the geographic center of European auto manufacturing. The Indonesia project — an integrated EV battery facility involving nickel processing — targets the growing Southeast Asian market and is expected to begin production in early 2026 as well.

Benchmarking CATL's capital efficiency against legacy automakers makes the company look extraordinary. In 2025, CATL generated 423.7 billion yuan in revenue and 72.2 billion yuan in net income on capex-to-revenue of roughly 10%. Compare this to the legacy auto industry, where companies like Ford and Volkswagen have invested tens of billions in EV pivots while losing money on every electric vehicle they sell. CATL's capital expenditure is funded substantially through operating cash flows — the company generated 133.2 billion yuan in operating cash flow in 2025 — and customer prepayments that reduce working capital requirements. The negative cash conversion cycle, which stood at approximately minus 91 days in 2025, means that CATL collects payment from customers and earns interest on that cash before it has to pay its own suppliers. This is the financial signature of a company with enormous bargaining power.

The Hong Kong listing in May 2025 deserves attention as a capital allocation event. CATL priced its secondary offering at HK$263 per share, raising HK$35.7 billion initially — about $4.6 billion — which grew to approximately $5.3 billion after exercising the greenshoe option. Shares surged 16% on the first day of trading, closing at HK$306.2. The company disclosed that 90% of the proceeds were earmarked for the Hungary factory, suggesting that the Hong Kong listing was less about raising capital per se — CATL is deeply cash-flow positive — and more about accessing international institutional capital to fund international expansion. The listing attracted sovereign wealth funds, insurance companies, and institutional investors from 15 countries. It was the largest IPO globally in 2025 and the largest in Hong Kong in four years.

The original Shenzhen IPO in June 2018 was a very different affair. CATL offered a 10% stake at 25.14 yuan per share, valuing the company at approximately $8.5 billion. Shares surged the maximum allowed 44% on the first day. Within a few years, CATL would become the most valuable company on China's ChiNext board. The trajectory from an $8.5 billion valuation at listing to roughly $243 billion today — approximately a 28-fold increase in under eight years — places CATL's post-IPO performance among the most impressive of any industrial company listed anywhere in the world during that period.

IX. 7 Powers, Porter's 5 Forces, and Competitive Positioning

To understand CATL's competitive position, it helps to apply two frameworks systematically: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. The results are striking — CATL scores unusually well on both.

Scale Economies. This is CATL's most obvious and most powerful advantage. With 661 gigawatt-hours shipped in 2025 and nearly 40% of the global market, CATL's purchasing power for lithium, nickel, cobalt, manganese, and other raw materials is unmatched. When CATL negotiates a lithium offtake agreement, it is negotiating for volumes that dwarf any single competitor. This purchasing advantage flows directly to the cost line: CATL's cost per kilowatt-hour is estimated to be 15-25% below that of LG Energy Solution and Samsung SDI, and the gap is structural, not temporary. Moreover, CATL's scale allows it to amortize its 22 billion yuan in annual R&D spending across a much larger revenue base than any competitor. R&D as a percentage of revenue is 5.2% — substantial, but manageable at CATL's scale. For a company half its size, matching CATL's absolute R&D spend would require dedicating more than 10% of revenue.

Cornered Resource. CATL's most important cornered resource is not lithium or nickel — those are commodities, even if CATL has upstream positions. The cornered resource is talent. CATL employs over 20,000 R&D engineers and scientists, many of them trained in Chinese universities that have become globally competitive in materials science and electrochemistry. The concentration of this talent in Ningde — a city that has essentially been built around CATL — creates a cluster effect similar to what TSMC created in Hsinchu. Competitors cannot simply hire away CATL's workforce because there is nowhere else in Ningde for those engineers to work. They would have to relocate entire families, and the talent pool is deepening, not shrinking, as CATL's success attracts the best graduates from China's top universities.

Switching Costs. When an automaker designs a vehicle's chassis around a specific battery cell geometry, battery management system architecture, and thermal management interface, switching to a different supplier requires redesigning substantial portions of the vehicle. This process takes three to four years and costs hundreds of millions of dollars. Once CATL's cells are designed into a platform — and they are designed into platforms from BMW, Tesla, Volkswagen, Hyundai, Stellantis, and dozens of others — the automaker is effectively locked in for the life of that platform, which typically spans seven to ten years. This is not quite as sticky as an enterprise software contract, but it is remarkably sticky for a hardware component.

Process Power. This is perhaps the most underrated of CATL's advantages. The company's manufacturing yields — the percentage of cells that pass quality inspection — are reportedly among the highest in the industry, a legacy of the ATL-era discipline of building for Apple. Higher yields mean lower waste, lower cost, and more consistent product. Process power compounds over time: every improvement in yield feeds back into lower costs, which funds more R&D, which improves yields further. Competitors can theoretically replicate CATL's process, but doing so requires thousands of small, incremental improvements accumulated over years of production experience. It cannot be bought, licensed, or shortcut.

Now, Porter's 5 Forces:

Bargaining Power of Buyers. Remarkably low for CATL's scale. Even Tesla — the most powerful buyer in the EV market — is substantially dependent on CATL for its high-volume models. When an automaker needs hundreds of thousands of battery packs per year at competitive prices, the number of suppliers capable of delivering at that scale narrows to perhaps three: CATL, BYD, and LG Energy Solution. And among those three, CATL offers the broadest product range, the lowest costs, and the most flexible chemistries. The result is that CATL can maintain gross margins of roughly 26% even while serving the most cost-conscious customers in the world.

Bargaining Power of Suppliers. Moderate and declining. CATL's upstream mining investments and Brunp's recycling operations are systematically reducing its dependence on external lithium and nickel suppliers. The company's scale also gives it leverage over chemical suppliers, equipment vendors, and component manufacturers that smaller battery makers cannot replicate.

Threat of New Entrants. Low. The capital requirements for a competitive battery manufacturing operation now start at several billion dollars. The technical expertise required — in chemistry, manufacturing, quality control, and thermal management — takes years to develop. And the customer relationships, validated through years of automotive qualification testing, cannot be replicated quickly. New entrants would need to simultaneously solve the capital, technology, and customer acquisition problems, a combination that effectively bars entry except from very large, well-funded companies that are willing to sustain losses for many years.

Threat of Substitutes. This is the most interesting force. The primary substitute threat comes from alternative battery chemistries — specifically sodium-ion and solid-state batteries. Sodium-ion batteries use abundant, cheap sodium instead of lithium, potentially disrupting the cost structure of the industry. Solid-state batteries replace the liquid electrolyte with a solid one, potentially offering dramatically higher energy density and safety. The remarkable thing about CATL's positioning is that it leads in both substitute technologies. In 2021, CATL unveiled its first-generation sodium-ion battery. In April 2025, it launched the "Naxtra" sodium-ion brand and began large-scale production. A next-generation sodium-ion cell announced in September 2025 supports a driving range of more than 500 kilometers with energy density of 175 Wh/kg. On solid-state, CATL has advanced all-solid-state batteries to the 20-amp-hour sample stage, targeting 500 Wh/kg energy density with small-scale production planned for 2027. If either technology disrupts lithium-ion, CATL is positioned to be the disruptor rather than the disrupted.

Industry Rivalry. Intense and increasing. BYD is the most formidable competitor — a vertically integrated Chinese company that manufactures its own batteries and its own vehicles, giving it a cost structure that even CATL envies. BYD held a 17.2% global market share in 2024, nearly half of CATL's, but growing rapidly. LG Energy Solution, at roughly 10-11% share, remains a strong number three with deep relationships with GM, Hyundai, and Tesla. Samsung SDI and Panasonic have both slipped below 4% share and appear to be losing ground. The competitive dynamic is shifting from a multi-polar world to a duopoly: CATL and BYD together accounted for nearly 55% of global EV battery installations in the first eleven months of 2025. Chinese manufacturers collectively control approximately 69% of the global market.

For investors tracking CATL's competitive position over time, two KPIs matter most. First, global market share by gigawatt-hours installed — this is the most direct measure of whether CATL is maintaining or extending its scale advantage. Robin Zeng has stated a goal of reaching 50-60% market share by 2030, and the trajectory from 36.6% in 2023 to 39.2% in 2025 is consistent with that ambition. Second, gross margin per kilowatt-hour — this captures whether CATL is maintaining pricing power even as it scales, or whether competitive pressure is compressing margins. The fact that CATL's gross margin expanded from 19.5% in 2022 to roughly 26.3% in 2025, even as battery cell prices declined sharply industry-wide, suggests extraordinary operating leverage and mix improvement.

X. The Playbook: Lessons for Founders and Investors

CATL's rise offers at least four lessons that transcend the battery industry.

Speed as a Feature. CATL iterates battery chemistry every six months. Its Korean and Japanese competitors take 18 to 24 months. This difference in clock speed is not about working harder — it is about organizational design. CATL's R&D, manufacturing, and testing operations are co-located in Ningde, which means an engineer can design a cell in the morning, have a prototype manufactured in the afternoon, and begin testing by evening. At Korean competitors, the R&D center might be in Seoul, the manufacturing plant in Poland, and the testing facility in Michigan. Every handoff adds weeks. CATL compressed these feedback loops to a degree that competitors have found very difficult to replicate, partly because replication would require them to undo decades of organizational structure. The lesson for founders: speed is not just about effort. It is about proximity, co-location, and eliminating the latency between decision and execution.

Regulatory Arbitrage as a Growth Strategy. The white list era offers a case study in how to use a protected home market to build durable competitive advantages. The key insight is that protection alone is worthless — many companies have enjoyed protected markets and emerged weaker, not stronger, because they used the protection to avoid competition rather than to prepare for it. CATL did the opposite. It used the white list window to invest in capacity, drive down costs, and build customer relationships at a pace that would have been impossible in an open market. By the time protection was lifted, the competitive advantages were self-sustaining. The lesson for investors: when evaluating companies in protected markets, the question is not whether the protection exists, but what the company is doing with it. Are they building or coasting?

Vertical Integration with Purpose. CATL's integration from mining to manufacturing to recycling is not integration for its own sake. Each element of the vertical chain solves a specific strategic problem. Mining reduces dependence on volatile lithium markets. Manufacturing at scale drives unit costs down the learning curve. Recycling through Brunp creates a secondary source of raw materials that hedges against supply disruptions and positions CATL for a future where recycled lithium is cheaper than mined lithium. The lesson for founders: integrate vertically when — and only when — each step of integration solves a problem that the market cannot solve for you at acceptable cost or reliability.

The B2B2C Paradox. CATL is a component supplier that has achieved something very rare: brand awareness among end consumers. This is the "Intel Inside" phenomenon — a component company that is recognized by the people who buy the finished product, even though they never interact with the component directly. When CATL launches a product with a consumer-facing brand name — like the Qilin battery pack or the Naxtra sodium-ion cell — it is building brand equity that gives automakers an additional reason to specify CATL cells. A BMW marketing executive can tell consumers, "This vehicle features CATL's Qilin battery technology," and a growing number of consumers will understand that this is meaningful. This kind of component branding is extraordinarily difficult to build and extraordinarily valuable once established. For investors, it represents an additional layer of switching costs that reinforces CATL's position.

XI. The Bear vs. Bull Case and Conclusion

The Bear Case centers on three risks that are real, material, and worth taking seriously.

First, geopolitics. The United States Inflation Reduction Act, passed in August 2022, effectively excludes Chinese battery manufacturers from the US market by requiring that EV battery components be sourced from the US or countries with which the US has free trade agreements. China is not among them. This means that CATL cannot directly supply batteries for EVs that qualify for the $7,500 US consumer tax credit. CATL has explored licensing its technology to US manufacturers — notably a controversial deal with Ford to build an LFP battery plant in Michigan using CATL technology — but the political environment in Washington makes any Chinese involvement in the US battery supply chain deeply contentious. If the US market, the world's second-largest, remains effectively closed to CATL, it constrains the company's addressable market by roughly 15-20%.

Second, overcapacity. China's battery manufacturing capacity has expanded dramatically, and some analysts estimate that Chinese battery production capacity now exceeds domestic and export demand by a significant margin. This overcapacity puts downward pressure on cell prices, which benefits automakers but compresses margins for battery makers. CATL's scale gives it the best cost position, meaning it will likely be the last company to feel margin pressure, but a prolonged period of oversupply could push smaller competitors into distress selling that drags pricing down for everyone.

Third, technology disruption. While CATL leads in both sodium-ion and solid-state battery development, there is always the risk that a breakthrough from an unexpected direction — a startup, a university lab, a well-funded corporate R&D program — could leapfrog CATL's technology. Toyota has invested heavily in solid-state batteries and claims to be targeting commercialization later this decade. QuantumScape, a US startup backed by Volkswagen, has made progress on solid-state prototypes. If solid-state batteries achieve the promised step-change in energy density and cost, and if CATL is not the company that commercializes them first, the competitive landscape could shift dramatically.

The Bull Case is fundamentally about structural demand and competitive positioning.

The electrification of transportation is not a fad — it is a multi-decade, multi-trillion-dollar transformation driven by government mandates, corporate commitments, and increasingly favorable economics. Every major automaker has committed to an electric future. The European Union has banned the sale of new internal combustion engine vehicles after 2035. China, the world's largest auto market, is approaching 50% EV penetration in new vehicle sales. Even if the pace of adoption varies by region and by year, the direction is unambiguous. As long as the world moves toward electricity, CATL sells the most critical component.

CATL's financial trajectory reflects this structural position. Revenue grew from approximately $4.4 billion in 2018 to $61.4 billion in 2025 — a compound annual growth rate of roughly 46%. Net income rose from $640 million to over $10 billion over the same period, a compound growth rate of approximately 48%. Return on equity stands at roughly 21%, and return on invested capital at about 13% — figures that would be impressive for a high-margin technology company, and are remarkable for an industrial manufacturer. The company's negative cash conversion cycle of minus 91 days means it is effectively funded by its customers and suppliers, a capital efficiency that few industrial companies achieve.

The ESS business provides a second growth engine that is substantially independent of automotive cycles. Grid-scale energy storage demand is growing even faster than EV demand, driven by renewable energy deployment. CATL's leading position in this market — 36.5% global share — gives it a diversified revenue base that reduces cyclical risk.

And then there is the recycling loop. As the first generation of EV batteries reaches end-of-life over the next five to ten years, the ability to recover and reuse critical minerals will become an increasingly important source of competitive advantage. CATL, through Brunp, is further ahead in building this capability than any other company. The closed-loop supply chain — mine, manufacture, recover, remanufacture — is not just environmentally appealing; it is economically compelling, because recycled lithium will increasingly be cheaper than mined lithium.

Ningde, the humid coastal city where Robin Zeng grew up and where CATL is headquartered, is an unlikely candidate for "the new Detroit." Detroit had the Great Lakes, the iron ranges of Minnesota, and the coal fields of Appalachia. Ningde has a deepwater port, proximity to China's electronics manufacturing heartland, and a physicist who did not want to be a farmer. But the parallel is real. Just as Detroit became the center of gravity for an industry that defined the 20th century, Ningde is becoming the center of gravity for the industry that will define the 21st. The cars are different. The fuel is different. But the logic of industrial concentration — talent attracts talent, scale begets scale, and the company that makes the critical component shapes the entire ecosystem — is exactly the same.

The question for investors is not whether CATL is a great company. The evidence for that is overwhelming. The question is whether greatness is adequately priced, and whether the geopolitical, competitive, and technological risks are adequately discounted. That is a question that each investor must answer for themselves, but the framework for answering it starts with two numbers: global market share by gigawatt-hours installed, and gross margin per kilowatt-hour. As long as both are trending in the right direction, the Emperor of Energy reigns.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube