SG Micro: The Analog Architect of the East

I. Introduction: The "Bridge" Between Two Worlds

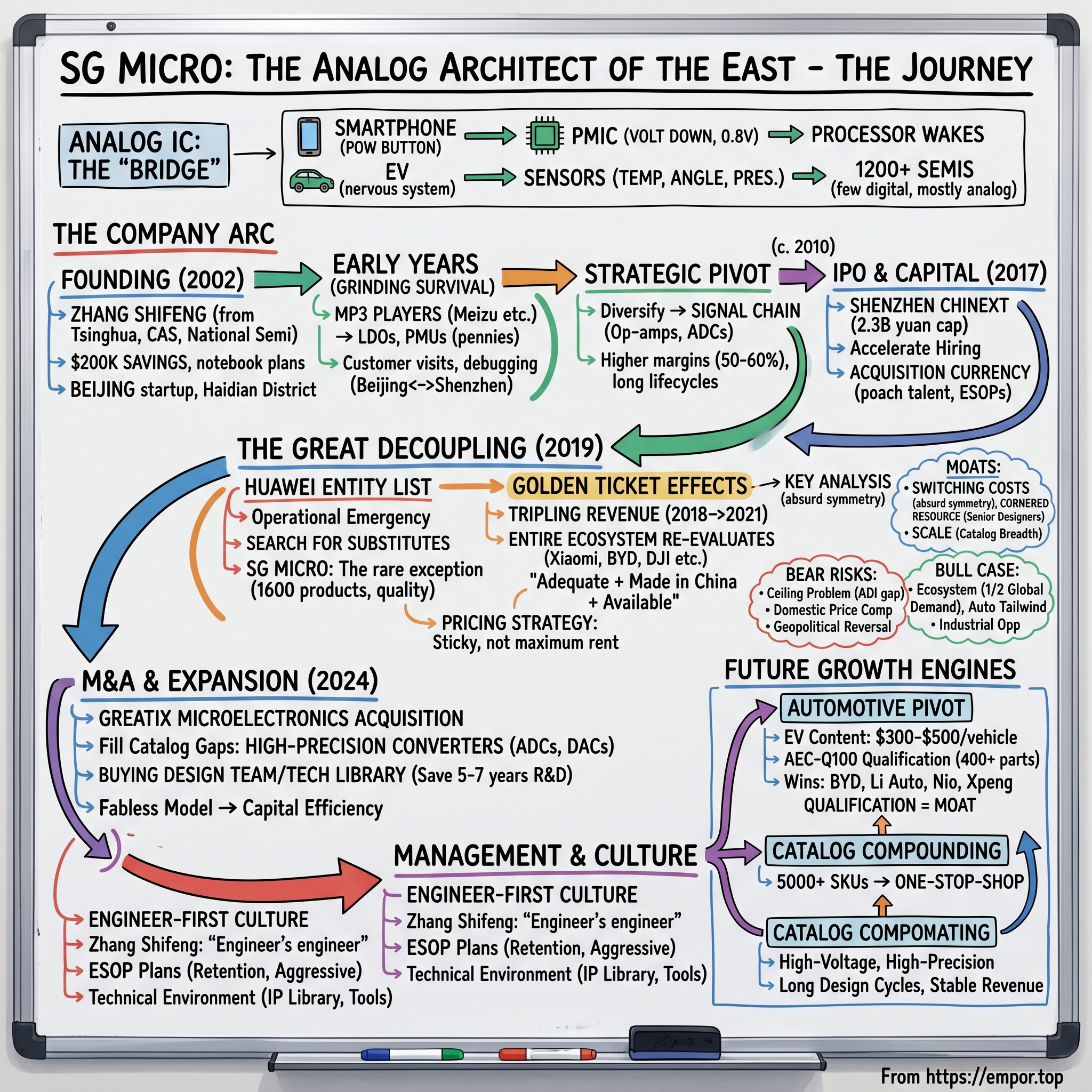

Picture the inside of a Xiaomi smartphone at the exact moment you press the power button. A cascade of events unfolds in microseconds. Lithium ions begin flowing from the battery, but they do not flow directly into the processor. They pass through a thin sliver of silicon—a power management IC no larger than a grain of rice—that steps the voltage down from 4.2 volts to the precise 0.8 volts the application processor needs to wake up. That tiny chip, invisible to every reviewer who obsesses over the Snapdragon inside, is what the industry calls an analog integrated circuit. Without it, the phone is a brick.

Now imagine a BYD Han EV rolling off the production line in Xi'an. It contains roughly 1,200 semiconductors. Of those, fewer than a dozen are the glamorous digital brains that get covered in the trade press—the Nvidia Orin for autonomous driving, the MediaTek infotainment chip. The rest, the overwhelming majority, are humble analog workhorses. They translate the temperature of the battery pack, the angle of the steering wheel, the pressure on the brake pedal, the sound of your voice, the current flowing through the 800-volt inverter. They are the nervous system of the car.

That is the business SG Micro Corp—圣邦微电子 in Mandarin, ticker 300661 on the Shenzhen ChiNext—has spent a quarter century building. And as of April 2026, the company commands a market capitalization of roughly 45 billion yuan, employs more than 1,700 people, and ships more than 5,000 distinct analog part numbers to over 20,000 customers across Asia. The story of how a scrappy 2002 Beijing startup became the "Texas Instruments of China" is not a story about a single breakthrough chip or a moonshot fabrication facility. It is a story about patience, about artisanal engineering, and about one of the most consequential geopolitical accidents in the history of the semiconductor industry.

The thesis of this episode is simple but counterintuitive. Most investors tracking Chinese semiconductors are watching the wrong stocks. They watch SMIC for the fab race, they watch Will Semi for CMOS image sensors, they watch Cambricon for AI accelerators. Meanwhile, the most durable cash-flow machine in the entire Chinese chip ecosystem has been quietly compounding in plain sight, selling parts that cost less than a cup of coffee, designed by engineers whose skill cannot be automated, and protected by moats that Moore's Law does not erode. SG Micro is the most successful "import substitution" case study in modern Chinese industrial policy—not because it was subsidized into existence, but because when the US-China decoupling hit in 2019, it was the only domestic analog company with a catalog broad enough and a design team deep enough to actually absorb the orders that Texas Instruments, Maxim, and Analog Devices could no longer fulfill.

From a tiny Haidian district startup in 2002 with a handful of returnees from National Semiconductor, to a company shipping chips into every major EV, drone, and smartphone brand in China today, the SG Micro arc is the analog chapter of the larger Chinese technology self-sufficiency story. But unlike so many politically driven industries, this one actually works. And the reason it works is because analog is, as its founder Zhang Shifeng likes to say, less a science than a craft.

II. Analog vs. Digital: The "Black Art" of Engineering

To understand why SG Micro matters, you have to understand why analog semiconductors are such a strange, stubborn, beautiful industry. And the best way in is to contrast them with their louder digital cousins.

Digital chips live in a binary world. A transistor is either on or off, a one or a zero. Because of this, digital design has been ruthlessly automated over five decades. An engineer at Nvidia designing the next Blackwell GPU does not hand-draw transistors. They write code in a hardware description language like Verilog, and electronic design automation software from Synopsys and Cadence translates that code into a physical layout of twenty-five billion transistors. Moore's Law—the biannual doubling of transistor density—has been the relentless tailwind. Every two years, the node shrinks, the chip gets faster, and the previous generation becomes economically obsolete.

Analog is the opposite universe. The physical world is not binary. Temperature, pressure, light intensity, sound waves, battery voltage—these are continuous, messy, unpredictable signals. Designing a chip that can faithfully convert a microvolt-level signal from a medical heart rate sensor into a clean digital number, without adding noise, without drifting over temperature, without drawing too much battery power, requires a kind of artistry that no software has yet replicated. There is a reason the industry has a running joke that you can tell an analog engineer from across the room—they are the ones with gray hair. It takes, on average, ten to fifteen years before an analog designer produces reliably excellent work. You cannot speedrun this profession.

This artisanal quality has profound business implications. Analog chips do not follow Moore's Law. A power management chip designed in 2008 on a 180-nanometer process can still be the best-in-class part in 2026, because the physics of stepping down a battery voltage has not changed. Consequently, analog product lifecycles are measured in decades, not quarters. Texas Instruments still sells op-amps designed in the 1970s. Gross margins in the industry regularly exceed 60 percent at the blue chip level, because once a design is qualified into a product—a car, a medical device, an industrial robot—the customer will keep buying that exact part number for the entire production life of their end product. Switching out a one-dollar analog chip would require redesigning and re-certifying the entire circuit board, which can cost hundreds of thousands of dollars and months of engineering time. The economic asymmetry is absurd.

This is the moat SG Micro has been building, chip by chip, for a quarter century. And the competitive set they benchmark themselves against is not other Chinese companies. It is the Western gold standard: Texas Instruments of Dallas, with its $17 billion in annual revenue and 80,000-plus product catalog, and Analog Devices of Wilmington, Massachusetts, with its dominance in the highest-margin signal chain and RF segments. These two companies together command roughly 30 percent of the global analog market, which in 2025 was worth about $85 billion. They are also, not coincidentally, two of the most durable compounders in the history of public equities. Texas Instruments has generated free cash flow every year for more than three decades.

When Zhang Shifeng sat in his small Beijing office in the early 2000s and sketched out SG Micro's business plan, he did not dream of beating Nvidia. He dreamed of cloning the TI playbook onto Chinese soil. The key insight: if you can build a broad catalog of reliable, cheap, well-supported analog parts, and you can embed yourself with thousands of small and medium-sized design customers, you end up with a business that looks less like a semiconductor company and more like an industrial utility. Slow to build. Nearly impossible to disrupt. That was the prize he was chasing, and he knew it would take decades to claim it.

III. The Founding & The Silicon Valley DNA

Zhang Shifeng's story begins, like so many in the modern Chinese technology industry, in the hallways of a Silicon Valley company in the 1990s. Born in 1962, Zhang earned his bachelor's degree in electronics from Tsinghua University in 1983, followed by a master's from the Chinese Academy of Sciences. Like thousands of talented engineers of his generation, he made his way west, landing at the University of Minnesota for his doctorate and eventually settling at National Semiconductor in Santa Clara—the storied analog house that would later be acquired by Texas Instruments in 2011 for $6.5 billion.

At National, Zhang cut his teeth designing power management chips for a customer base that included the entire first wave of PC and mobile computing. Colleagues from those years describe him as relentlessly technical, almost monk-like in his devotion to circuit design. He was not a sales guy, not a self-promoter. He was an engineer's engineer. And by the late 1990s, he had absorbed the TI/National playbook from the inside: the catalog strategy, the customer support discipline, the importance of maintaining a vast array of low-volume but high-margin SKUs that added up, over time, to an unassailable moat.

In 2002, at the age of forty, Zhang made the decision that every Chinese returnee of his generation faced. He boarded a flight back to Beijing, carrying roughly $200,000 in personal savings and a business plan scribbled across several notebooks. The China he returned to was barely recognizable as a semiconductor market. Domestic analog chip consumption was dominated almost 100 percent by imports. The only local design houses were tiny workshops making low-grade parts for calculator and toy manufacturers. When he registered SG Micro Corp in Haidian District, just down the road from the old Tsinghua campus, the entire Chinese analog design industry probably employed fewer than a thousand people.

The first five years were a grinding exercise in survival. SG Micro's earliest customers were MP3 player manufacturers in Shenzhen—companies like Meizu and a host of forgotten brands that flourished briefly before the iPhone killed the category. The chips SG Micro sold were simple linear regulators and power management units, priced at pennies each, competing head-to-head with TI, Maxim, and Richtek on price. Margins were thin, volumes were lumpy, and Zhang spent much of his time on the road, personally visiting customers in the Pearl River Delta to solve design-in problems. A former employee from that era recalled that Zhang would fly from Beijing to Shenzhen on a Monday morning, spend two days at a customer's design bench debugging a circuit, and fly home Tuesday night—never expensing a hotel, always returning to work Wednesday morning.

By 2010, SG Micro had around 200 employees and was doing roughly 150 million yuan in annual revenue. Not a venture capital darling. Not a media story. Just a slowly compounding engineering shop, reinvesting everything into product development. The strategic decision that would define the next decade came around this time: rather than chasing the highest-volume, lowest-margin consumer commodity business, Zhang pushed the company to diversify into signal chain products—op-amps, ADCs, voltage references, interface chips. These were harder to design, smaller in volume, but carried gross margins of 50 to 60 percent and, crucially, dramatically longer product lifecycles.

The inflection point came on June 6, 2017, when SG Micro listed on the Shenzhen Stock Exchange's ChiNext board. The IPO was modest by the standards of today's Chinese chip listings—it raised roughly 260 million yuan at an offering price of 28.67 yuan per share, giving the company a post-money market capitalization of around 2.3 billion yuan. But for Zhang Shifeng and the core team, the listing was transformational for two reasons. First, it provided the capital to dramatically accelerate hiring of analog engineers, the scarcest resource in the industry. Second, and more subtly, it gave the company an acquisition currency. From 2017 onward, SG Micro's stock price became a weapon it could wield to poach top engineering talent from domestic rivals and even from TI and ADI's China offices, through employee stock ownership plans that vested over five and seven years.

But the real test of Zhang's vision was still two years away, across the Pacific, in a trade dispute that nobody had yet seen coming. When it hit, SG Micro would be one of a handful of Chinese companies standing in exactly the right place, at exactly the right time, with exactly the right catalog.

IV. The "Great Decoupling" & The Golden Ticket

On May 15, 2019, the US Commerce Department added Huawei Technologies and 68 of its affiliates to the Entity List, prohibiting American companies from supplying them with technology without a license. The immediate focus of the press coverage was on Google's Android operating system and on the advanced logic chips that TSMC manufactured for HiSilicon. But deep inside Huawei's procurement department, alarm bells were ringing for a far less glamorous reason. Tens of thousands of analog chips from TI, Maxim, Analog Devices, and ON Semiconductor flowed into every Huawei base station, every router, every smartphone. Losing them was not a theoretical risk. It was an operational emergency.

Huawei's procurement teams fanned out across the Chinese semiconductor landscape looking for substitutes. Most of what they found was disappointing. Many domestic analog startups had one or two promising parts but no production-tested catalog. Quality was inconsistent. Supply reliability was shaky. SG Micro was the rare exception. By 2019, the company had already built out a catalog of roughly 1,600 products across power management and signal chain, had been qualified into consumer electronics customers for years, and had developed the quality management systems necessary to handle enterprise-grade demand. When Huawei knocked, SG Micro was ready.

What followed over the next three years was, in retrospect, the single greatest commercial tailwind in the history of Chinese analog semiconductors. Revenue at SG Micro grew from 788 million yuan in 2018 to 1.78 billion yuan in 2020, then to 2.24 billion yuan in 2021—a tripling in three years. Net profit margins expanded from the mid-teens into the high twenties, because the incremental volume came largely from high-margin signal chain parts that had been developed years earlier but had struggled to win share against entrenched Western competitors.

But the deeper story was not just Huawei. The entire Chinese electronics ecosystem was simultaneously re-evaluating its supplier list. Xiaomi, Oppo, and Vivo realized that even though they were not on any US entity list, they faced the same structural risk if relations deteriorated further. BYD and Geely, pushing aggressively into the EV market, concluded that designing next-generation vehicles around US-supplied analog chips was a strategic mistake. DJI, facing its own tightening US restrictions, rebuilt drone power systems around domestic alternatives. Even white-goods giants like Midea and Gree quietly began qualifying Chinese analog chips as second sources for their inverter controllers and motor drivers.

For SG Micro, this was the moment the entire strategy of patient catalog-building paid off. The company had spent fifteen years developing chips that were adequate substitutes for TI's most popular parts. In the pre-2019 world, "adequate" was not enough—Chinese customers would happily pay a small premium for the brand safety of TI or Maxim, because there was no cost to doing so. In the post-2019 world, "adequate" plus "made in China" plus "reliably available" suddenly became the most valuable combination in the market. SG Micro's chips went from being a defensive backup option to being the preferred primary supplier for tens of thousands of design wins.

The customer relationships that developed during this window were the most durable assets the company built. Engineers at Xiaomi's handset division, at DJI's flight controller team, at BYD's electronics division, no longer treated SG Micro as a cheap alternative. They began treating the company as a strategic partner, bringing SG Micro's designers into early-stage product development meetings, sharing multi-year roadmaps, and jointly developing custom variants of stock parts. In the analog business, this kind of intimacy is priceless. Once an SG Micro engineer has sat in a Xiaomi conference room for six months iterating on a power management chip for a specific phone model, the probability that the next phone model will use SG Micro again approaches unity.

The company also used this period to make a crucial strategic move on pricing. Rather than exploiting the supply shortage to maximize per-unit margins, Zhang Shifeng's team held prices relatively steady and prioritized long-term volume commitments. The logic was classic TI playbook: the goal of analog pricing is not to extract maximum rent in any given quarter, but to be sticky enough that customers never re-evaluate. By 2022, when the global chip shortage began to ease and Western suppliers returned to the Chinese market looking to reclaim share, they discovered that the ground had shifted permanently beneath their feet. SG Micro had embedded itself so deeply in Chinese customers' bills of materials that recovering design-in positions became economically irrational for many of the lost sockets.

The story, however, was not a simple upward march. By 2023, as the post-pandemic consumer electronics cycle turned and a flood of domestic analog competitors rushed into the market, SG Micro entered a more painful chapter—one that would test whether its moat was as real as the bull case implied. Revenue actually declined in 2022 on a reported basis before recovering. Net profit margins compressed sharply as the company pushed to maintain volumes and fend off price-cutting rivals. This was not the story of easy victory. It was the story of an industry in adolescence, with all the volatility that implies.

V. M&A and Capital Deployment: Buying the Future

If the 2019 trade war was SG Micro's demand-side windfall, then the 2024 acquisition of Greatix Microelectronics—钰泰半导体 in Mandarin—was its most important supply-side chess move. The deal was announced in early 2024 and closed in stages throughout the year. SG Micro acquired an additional 14.5 percent of Greatix, bringing its total stake to a controlling position above 70 percent, at a total valuation that implied Greatix was worth roughly 3 billion yuan. For a company that SG Micro had first invested in back in 2020, this was a multi-year, staged buyout rather than a single headline-grabbing event.

To understand why the Greatix deal mattered, you have to understand the structural gap in SG Micro's catalog. For all of SG Micro's strengths in general-purpose power management and mid-range signal chain products, the company had historically under-invested in high-precision converters—the segment where Analog Devices earns its highest margins and where Chinese industrial and automotive customers were increasingly demanding domestic alternatives. Greatix, founded by a team of former ADI engineers, had spent nearly a decade developing exactly these parts: high-precision analog-to-digital converters, digital-to-analog converters, and a growing portfolio of sensor interface chips aimed at industrial test and measurement, medical imaging, and EV battery management systems.

The valuation, on any static multiple basis, looked aggressive. At the deal price, Greatix was trading at an implied price-to-earnings ratio of more than 40 times, and SG Micro was paying in a mix of cash and the premium currency of its own equity. Skeptics argued that Zhang was overpaying for a company whose revenue base was still under 500 million yuan. The bull response—and the case Zhang made to his own board and to investors at the annual shareholder meeting in May 2024—was that the Greatix acquisition was not about buying a revenue stream. It was about buying a design team and a technology library that would have taken SG Micro five to seven years to build organically. In a market where analog engineering talent was the single scarcest resource, paying a 40x P/E to skip five years of R&D cycle time was a bargain, not a premium.

The pattern here echoes what Texas Instruments did in its own formative decades. TI's current dominance is not the product of a single acquisition, but of a steady stream of small, tuck-in deals over forty years—Unitrode, Burr-Brown, Silicon Systems, National Semiconductor—each of which filled a specific catalog gap and added a few hundred design engineers to the TI bench. SG Micro, with the Greatix deal and a handful of smaller 2022 and 2023 investments in domestic analog startups, has begun running the same playbook on Chinese soil. The fragmentation of the Chinese analog industry, with more than 100 small design houses each focused on narrow niches, is a structural opportunity for a consolidator with a broad catalog, strong balance sheet, and premium stock currency.

Capital efficiency has become one of SG Micro's most underappreciated strengths. The company operates a fabless model, outsourcing all its manufacturing to third-party foundries in China, Taiwan, and Singapore. This means the capital intensity of the business is dramatically lower than a vertically integrated peer like TI, which runs its own fabs. SG Micro's property, plant, and equipment balance at year-end 2025 was under 1 billion yuan, against annual revenue of more than 3 billion yuan. Return on invested capital in the best years of the cycle has exceeded 25 percent. When the business generates high returns on capital and reinvests into R&D and acquisitions rather than factories, the compounding math becomes extremely favorable—assuming, of course, that the underlying product demand holds.

One second-layer diligence note worth flagging here: the Greatix transaction structure, with its staged purchase and minority interest accounting, introduces some complexity into SG Micro's consolidated financials that investors should read carefully. Non-controlling interest disclosures, goodwill amortization judgments, and the treatment of fair value step-ups at consolidation are all worth scrutinizing in the 2024 and 2025 annual reports. This is not a red flag, but it is a reminder that as SG Micro moves from a pure organic grower into an acquisitive consolidator, the accounting complexity rises meaningfully. The auditors—currently Ernst & Young Hua Ming—have issued clean opinions, but the comparison across historical financial periods has become less apples-to-apples than it was pre-2024.

With the catalog expanded, the capital deployed, and the integration underway, the question the market began asking in 2025 was simple: could SG Micro's culture—built around a small, tightly-knit founding team—absorb the organizational complexity of a $4 billion-revenue, multi-site, multi-product business? The answer to that question lives in the company's approach to people.

VI. Management & The "Engineer-First" Culture

Zhang Shifeng is not a Jack Ma. He does not deliver keynote speeches at Davos, he does not maintain a polished public persona, and he does not sit for glossy magazine covers. On the rare occasions when he addresses industry conferences—most recently at the China Semiconductor Industry Association annual meeting in November 2025—he speaks quietly, almost diffidently, for perhaps fifteen minutes. His slides are dense with circuit diagrams and process node roadmaps. His jokes are engineer jokes. The people in the room who understand analog design laugh. Everyone else checks their phones.

This is not a personality defect. It is a conscious cultural signal. Zhang has spent two decades explicitly building SG Micro as an engineer-first company, and he has been remarkably consistent about it. In every annual report, in every investor presentation, he foregrounds the design team. The company's headcount breakdown tells the same story: as of the most recent filings, more than 75 percent of SG Micro's employees were R&D personnel, and within that group, the ratio of senior analog design engineers to junior staff was among the highest in any Chinese semiconductor company.

The management team around Zhang reflects this technical orientation. The core leadership group—including Deputy General Manager and Chief Technology Officer Shuang Yanwei, and CFO Lin Jingrong—has been stable for more than a decade. There is no celebrity president brought in from a Western multinational. There is no former banker running strategy. The people making decisions about which product categories to enter, which engineers to hire, and which customers to prioritize are the same people who have been designing chips together since the company was 50 people in a walk-up office.

This cultural consistency matters enormously in analog semiconductors, where, as we discussed, the learning curve for a senior designer is ten to fifteen years. SG Micro has lost remarkably few senior engineers to competitors over the past decade. In a Chinese technology industry where job hopping for 30 percent salary bumps has been endemic—particularly during the 2020-2022 boom when every venture-backed analog startup was trying to poach TI and SG Micro alumni—the retention story stands out. The reason, as multiple former employees have explained to industry researchers, is a combination of three factors.

First, the employee stock ownership plans are aggressive. SG Micro has run multiple rounds of ESOP over the past decade, covering progressively wider segments of the employee base. The 2022 plan, for example, allocated shares to more than 400 employees at discounted strike prices, with vesting tied to both individual and company performance metrics. For a senior engineer, an ESOP grant at SG Micro has historically been worth several million yuan over a four-to-seven-year vesting period—life-changing money in the Chinese context, and dramatically more than even the most generous Shenzhen startup could offer without public-market valuation backing.

Second, the technical environment is genuinely competitive with what Western companies offer. SG Micro has built up an internal IP library, a set of simulation tools, and a process technology ecosystem that allows a senior designer to work on challenging problems without being starved for resources. For a returnee from Silicon Valley, or a poaching target from TI China or ADI China, this matters. Nobody wants to leave a world-class tool environment to go work in a startup with bootleg software and no test equipment. SG Micro, after twenty-plus years of reinvestment, has closed most of that infrastructure gap.

Third, and most subtly, the culture has a distinctly un-Chinese-startup feel. There is no 996 work culture mandated from the top. Meetings are engineering-led, not management-led. Decisions are made through consensus among the senior technical team, not by fiat from the founder. For engineers who have spent time in the American analog industry, the SG Micro environment feels more like the old National Semiconductor or the pre-acquisition Linear Technology than like the typical Shenzhen chip startup.

On the shareholding side, Zhang Shifeng remained the largest shareholder of SG Micro as of the most recent filings, directly holding roughly 15 percent of outstanding shares. Concentrated founder ownership is a feature, not a bug. It aligns the long-term incentive structure with the long-tail product philosophy. Zhang is not going to sell out at any price; he is building a forty-year institution, and his net worth compounds with the company's slow, broad growth across thousands of SKUs. For long-term fundamental investors, this kind of ownership structure is historically among the best predictors of durable value creation.

All of which sets up the most important business question: what is the growth engine that justifies the valuation the market has been assigning to SG Micro, and where will the next decade of compounding come from?

VII. The "Hidden" Growth Engines

Walk the floors of the China International Import Expo in Shanghai, or the automotive electronics conference in Munich, or the industrial automation trade show in Nuremberg, and you will see the second act of the SG Micro story unfolding in real time. The company's revenue mix in 2016 was approximately 70 percent power management and 30 percent signal chain, weighted overwhelmingly toward consumer electronics end markets. The mix as of the 2025 annual report tells a very different story.

Power management integrated circuits—PMICs in industry shorthand—still contribute the majority of revenue, somewhere in the range of 55 to 60 percent. This is the cash cow. These are the chips that regulate battery voltages, manage charging protocols, drive LED backlights, and power the thousands of small circuits inside every consumer and industrial device. Growth in this segment is steady rather than spectacular, closely correlated with the broader Chinese electronics production cycle and with SG Micro's ability to introduce incremental new parts and win sockets from Western incumbents.

The more interesting story is in signal chain. This is the portfolio of operational amplifiers, analog-to-digital and digital-to-analog converters, comparators, voltage references, and interface chips that are used to capture and process real-world signals. Signal chain revenue has been growing at north of 30 percent annually for several years, and gross margins in this segment are meaningfully higher than in general-purpose power management—reflecting both the technical difficulty of the parts and the longer qualification cycles required to win designs. The Greatix acquisition, in particular, has accelerated SG Micro's push into high-precision signal chain products aimed at industrial and automotive customers.

And then there is the automotive pivot, which is the single most important multi-year growth story at the company. The arithmetic here is extraordinary. A traditional internal combustion engine car contained roughly 200 semiconductors. A modern Chinese EV contains anywhere from 1,000 to 1,500. Of those, the analog content—everything from battery management chips to motor driver ICs to touchscreen interfaces to LiDAR signal conditioners—can represent $300 to $500 of silicon value per vehicle. China produced roughly 30 million vehicles in 2025, and new energy vehicles accounted for more than 40 percent of the mix. The total addressable market for analog content in Chinese vehicles alone is north of $10 billion and growing.

SG Micro began its serious push into automotive around 2019, investing in the AEC-Q100 qualification process—the industry standard for automotive-grade silicon, which requires chips to operate reliably at temperatures from -40°C to +150°C, survive vibration and humidity testing, and meet automotive safety standards like ISO 26262. As of the latest filings, SG Micro had more than 400 AEC-Q100 qualified part numbers in production, up from fewer than 50 just three years earlier. Automotive revenue, while still a minority of the total, grew dramatically through 2024 and 2025 and had become one of management's primary focus areas. Key design wins at BYD, Li Auto, Nio, Xpeng, and increasingly at European and Japanese automakers sourcing from Chinese EV supply chains, have created a revenue base that will likely compound for a decade as those vehicle models reach steady-state production volumes.

Industrial automation represents a third leg of the growth story. Chinese industrial customers—makers of robotics, factory automation equipment, medical imaging devices, and smart grid components—have historically been the most conservative buyers of analog chips, preferring the proven reliability of TI and ADI parts. The 2019-2022 supply disruptions cracked that conservatism open, and SG Micro has been systematically building a catalog of high-voltage, high-precision parts aimed at these applications. Growth here is slower than in automotive because design cycles in industrial markets can run five to seven years, but the long tail of stable revenue from qualified industrial designs is exactly the kind of business Zhang Shifeng has been trying to build since day one.

One qualitative overlay worth mentioning: the automotive qualification process is itself a kind of moat. Once a Chinese EV maker has designed an SG Micro battery management chip into a specific vehicle platform, the cost and time required to switch to a Western alternative—re-qualifying the part, re-certifying the safety case, re-running reliability tests—is prohibitive. This is the analog industry's equivalent of a pharmaceutical drug being locked into a patient's treatment regimen. It creates a multi-year, and in some cases decade-long, annuity of recurring revenue.

The KPIs worth tracking as this story unfolds are narrower than the diversity of segments might suggest. First and most important: the company's total SKU count and the rate at which new products are released into revenue each year. A slowing product release cadence is the leading indicator of a broken moat in this business. Second: the share of revenue from automotive and industrial end markets, because that ratio measures the company's success in migrating from cyclical consumer electronics into stickier, higher-margin verticals. Everything else—quarterly revenue growth, segment gross margin, individual customer concentration—matters far less than those two leading indicators.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Sit down with a long-term fundamental investor and ask them what they are really buying when they buy an analog semiconductor company, and the answer eventually comes down to moats. Analog is an industry of moats. The question is always which moats are real, how deep they are, and how long they can hold.

Starting with switching costs, which is Power Number One in Hamilton Helmer's 7 Powers framework. This is the most important moat in analog, and SG Micro has been building it systematically for two decades. An SG Micro chip embedded in a BYD Han EV is not a fungible component. To swap it out for a Texas Instruments equivalent, BYD would have to re-spin the printed circuit board, re-run thermal and EMI testing, re-qualify the automotive safety case, and re-certify the vehicle in each regulatory market. The fully loaded cost of swapping a $2 chip can easily run into hundreds of thousands of dollars and six to nine months of engineering time. No procurement department does this lightly, and once a chip is designed in, it typically stays in for the life of the product—which in automotive means seven to ten years of steady revenue.

Second: cornered resource. In the analog world, the cornered resource is not a patent or a factory. It is senior design engineers. SG Micro employed more than 1,300 R&D engineers as of year-end 2025, with a meaningful share having 10-plus years of experience. That kind of talent concentration cannot be replicated quickly, because the only way to create a senior analog designer is to have them spend a decade under the mentorship of another senior analog designer. The ESOP structure and the cultural stability of the company have created a talent flywheel that competitors find difficult to match.

Third: scale economies, but in a counterintuitive sense. In analog, scale does not come from building giant factories—the industry is largely fabless or uses older process nodes where capacity is abundant. Scale comes from catalog breadth. When an OEM designer sits down to design a new product, the decision to go with SG Micro over a smaller competitor often comes down to whether SG Micro has the adjacent parts needed for the full board—the power management chip, the op-amp, the interface chip, the voltage reference. A one-stop-shop is enormously valuable, and SG Micro's 5,000-plus SKU catalog gives it this advantage against every domestic rival, though it is still well below TI's 80,000-plus.

Fourth, and more speculative: branding. SG Micro is increasingly becoming a trusted name inside the Chinese electronics engineering community. Young Chinese electrical engineers graduating today grew up in a world where SG Micro was a viable, often preferred, supplier. That generational shift in mindshare is a slow but powerful moat-builder.

Turning to Porter's 5 Forces, the picture mostly reinforces the bullish structural view. The threat of new entrants is low, because the minimum viable catalog for an analog company to win enterprise customers requires hundreds of qualified parts and a deep bench of senior designers—both of which take years to build. The threat of substitutes is also low, because analog chips have no functional substitute; you cannot replace a power management IC with a digital signal processor. Buyer power is moderate: individual chips are cheap, but customers buy thousands of them across hundreds of designs, which gives them some leverage, offset by the high switching costs described above. Supplier power—primarily the fabs that manufacture SG Micro's chips—has been manageable, although the 2021-2022 foundry capacity crunch was a reminder that this is not a risk-free dependency.

The most intense force in Porter's framework, and the one most worth watching, is internal rivalry. SG Micro's primary competitors fall into two camps. The first is the Western incumbents—TI, ADI, Maxim (now part of ADI), Infineon, STMicro. These companies still dominate at the very high end of performance and in many industrial and automotive segments where long-standing design wins persist. The second is the rapidly expanding roster of Chinese analog startups: 3PEAK Incorporated, Silergy Corp, Will Semiconductor, Maxscend, Gigadevice, and dozens of smaller private players. Some of these, particularly 3PEAK and Silergy, have overlapping catalogs with SG Micro and have been aggressive on pricing. Intra-Chinese price competition has been the single biggest margin pressure on SG Micro over the past three years, and will likely remain the biggest watch-point for the next three.

The strategic implication is nuanced. SG Micro's moat against Western incumbents has been strengthening, thanks to the geopolitical tailwind and to sustained R&D investment. But the moat against other Chinese domestic rivals has been weakening at the low end of the catalog, where the barriers to design and manufacture are lower. The company's competitive future depends on whether it can continue to migrate its revenue mix upmarket—into automotive, industrial, and high-precision signal chain—faster than domestic rivals catch up.

IX. The Bear vs. Bull Case

Put two seasoned fundamental investors in a room and ask them to make the bear case on SG Micro, and here is what emerges.

The ceiling problem is real. For all of SG Micro's progress, the company remains in the mid-tier of global analog performance. The very highest-margin, highest-technology segments—RF, high-speed data converters for communications infrastructure, ultra-precision instrumentation—remain dominated by Analog Devices, which has spent fifty years and billions of dollars building an IP library that no Chinese company, SG Micro included, has come close to matching. If SG Micro's growth story is predicated on eventually taking share in these premium segments, the bears argue it is betting against fifty years of compounding technical advantage that cannot be shortcut with capital or trade policy.

The second bear thesis is domestic price competition. The flood of Chinese analog startups funded during the 2019-2022 venture boom is now reaching commercial maturity, and many are willing to accept breakeven or loss-making operations for years to win design sockets. This is the same dynamic that destroyed margins in Chinese solar panels, Chinese lithium battery chemistry, and Chinese LED chips. SG Micro's gross margins have already compressed from their pandemic-era peak, and the bear case extrapolates that pressure forward, arguing that the company's current profit margins are not sustainable through a full competitive cycle.

The third bear thesis is geopolitical reversal. The current tailwind from US-China decoupling assumes that trade relations continue to deteriorate, or at least remain fragmented. A meaningful détente—a scenario that looked unlikely in 2024 but has been discussed intermittently in 2025 and 2026 as new administrations took office on both sides—could bring Western analog suppliers back aggressively, particularly if they are willing to price-cut to recover share. SG Micro's recent revenue and margin uplift has been meaningfully boosted by the trade tension; a partial reversal of that dynamic is a real risk.

Fourth, and more accounting-oriented: the Greatix acquisition and the staged minority investments in other domestic analog companies have introduced consolidation complexity, non-controlling interest volatility, and goodwill balances that will need to be tested for impairment in any downturn. None of this is intrinsically alarming, but it does mean that reported earnings are less clean than they were in the pre-acquisition era.

Now the bull case.

The ecosystem argument is powerful. China represents roughly half of global semiconductor consumption, and nearly half of global analog chip demand. If SG Micro captures even 20 percent of the domestic analog market over the next decade—a share that TI has held globally for years and that would still leave plenty of room for competitors—the company would be generating 20 to 30 billion yuan in annual revenue at significantly higher margins than today. That is a top-ten global analog company by revenue, and it requires no heroic assumptions about international expansion or about winning in the highest-end technology segments.

The automotive tailwind has not peaked. Chinese EV production is projected to continue compounding at double-digit annual rates through 2030, and the analog content per vehicle is still rising as vehicles add more sensors, more safety features, and more sophisticated power electronics. SG Micro's qualified automotive portfolio is now large enough to capture meaningful share as new vehicle platforms ramp into volume production over the next three to five years. The automotive revenue ramp is arguably the single most underappreciated line item in the company's forward story.

The industrial and medical opportunity has barely begun. In these markets, design cycles are long and conservative, but once qualified, parts can generate revenue for 15 to 20 years. SG Micro is in the early innings of building that long-tail industrial franchise, and the compounding effects of stacking qualified designs year after year are enormous. This is the purest expression of the TI playbook, and it is the quietest but most durable piece of the bull thesis.

On valuation versus reality, the market has oscillated in how it treats SG Micro. During the peak enthusiasm of 2021 and early 2022, the stock traded at triple-digit price-to-earnings multiples—pricing in a decade of uninterrupted high growth and margin expansion. Through the 2023-2024 cyclical downturn and the post-Greatix integration phase, multiples compressed meaningfully, and the stock traded more like a value play on long-term Chinese industrial demand. Current levels in April 2026 reflect something in between—a market that believes in the long-term franchise but is pricing in real execution risk around margins and competition. For long-term fundamental investors, the key question is not whether SG Micro is fundamentally cheap or expensive on any given day, but whether the underlying thesis of a multi-decade compounder in Chinese analog semiconductors is intact. Based on the KPIs that matter—SKU growth, automotive qualification pace, engineering headcount retention—that thesis continues to hold.

One myth worth correcting. The popular narrative that SG Micro is "just" a beneficiary of Chinese import substitution policy oversimplifies the story. The company was building its catalog and its engineering bench for seventeen years before the 2019 trade war began. The policy tailwind accelerated a story that was already in motion. If you believe the bull case, you have to believe the engineering bench and the catalog breadth are the real moats, and the trade policy was merely the trigger that unlocked the value. If you believe only in the trade policy, you are betting on a tailwind that may not last.

X. Epilogue & Final Reflections

Step back from the quarterly print, the product roadmaps, and the earnings debates, and the deeper lesson of SG Micro is a lesson about the nature of industrial compounding.

Zhang Shifeng did not build a single hit product. He built a catalog. Every year, for more than two decades, his team added a few hundred new parts to a list. Most were unglamorous. Most generated modest revenue on their own. But the list, taken as a whole, became something no competitor could casually replicate. Fifteen hundred SKUs. Three thousand. Five thousand. Each new part made the next customer design-in easier. Each customer design-in added a tiny, durable stream of revenue that could run for a decade or more. The math compounds.

This is the lesson for founders operating in slow, unglamorous, deeply technical industries. You do not need one moonshot. You need a thousand competent base hits, strung together over twenty years, with the patience to let the catalog compound into an asset that cannot be built in a weekend sprint. It is the opposite of the Silicon Valley mythology of the breakthrough product, and it is, for the right business, the more durable strategy.

Zhang has also, intentionally or not, proven a second point that is increasingly relevant as the global semiconductor industry fragments along geopolitical lines. The highest-value segments of the chip industry are not always the most glamorous ones. The world's attention is focused on who will own the next generation of AI accelerators, 3-nanometer logic, and high-bandwidth memory. But the nervous system of every device, every vehicle, every factory, runs on analog chips. The country, or company, that dominates analog ends up with a kind of infrastructural influence that the digital headline-grabbers often do not. China's strategic industrial planners understand this, which is why SG Micro and a handful of peers have received steady, if quiet, policy support over the past decade.

Looking out to 2030, the question is whether SG Micro will be a global player or a national champion. The answer will depend on a few things. Does the automotive ramp continue, and does the company succeed in exporting its automotive parts to European, Japanese, and Korean automakers who are increasingly willing to source from Chinese analog suppliers? Does the industrial and medical qualification effort produce a self-sustaining second-act revenue stream? Does the Greatix acquisition integration succeed in pushing SG Micro up the precision converter value stack? And perhaps most importantly, does Zhang Shifeng's engineer-first culture survive the transition from a 1,700-person company to a 5,000-person company, without losing the patience and craft discipline that built the franchise in the first place?

None of those questions can be answered today. But the structural setup is as favorable as any investor could reasonably hope for in a Chinese technology company in 2026. A $90 billion global market growing at mid-single digits, a domestic market growing faster, a trade policy environment that remains favorable to local suppliers, a founder-led company with aligned ownership, a deep and stable engineering bench, a broad catalog with accelerating SKU velocity, and a balance sheet with the flexibility to keep consolidating a fragmented domestic industry. Not every year will be easy. The 2022-2023 slowdown was a reminder that cyclicality has not been repealed, and domestic price competition will continue to compress margins at the low end of the catalog. But the long-tail franchise built around the patient accumulation of thousands of small, sticky, engineering-intensive products is as close to an industrial compounder as the Chinese semiconductor industry has yet produced.

The story that began in that small Haidian office in 2002, with a forty-year-old returnee sketching business plans in a notebook, has become something that would have seemed improbable even a decade ago: a credible, scaled, domestically dominant analog semiconductor franchise, built in the shadow of Texas Instruments, quietly taking its place as one of the most important nodes in the Chinese technology supply chain. The next chapter is still being written. But the foundation—chip by chip, engineer by engineer, design win by design win—has already been laid.

Analog, as Zhang has always insisted, is art. And this particular piece of art has been twenty-four years in the making, with at least another two decades of brush strokes still to come.

XI. Top Long-Form Links & References

- SG Micro Annual Reports (2017-2025) – the definitive source for tracking SKU count growth from roughly 600 products at IPO to more than 5,000 today, along with evolving segment breakdowns and automotive qualification milestones.

- "The Analog Art" – industry analyses exploring why analog engineers represent one of the most scarce and durable resources in the global semiconductor labor market.

- SEMI China Reports on import substitution trends across the Chinese semiconductor industry from 2019 onward, providing context on the broader policy and supply-chain environment that shaped SG Micro's rise.

- Analysis of the Greatix Microelectronics acquisition – staged deal documentation comparable in structure and valuation multiples to historical tuck-in deals made by Texas Instruments and Analog Devices during their own consolidation phases.

- Zhang Shifeng's keynote addresses at the China Semiconductor Industry Association annual meetings, providing the clearest available window into management's technical philosophy and long-term catalog strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube