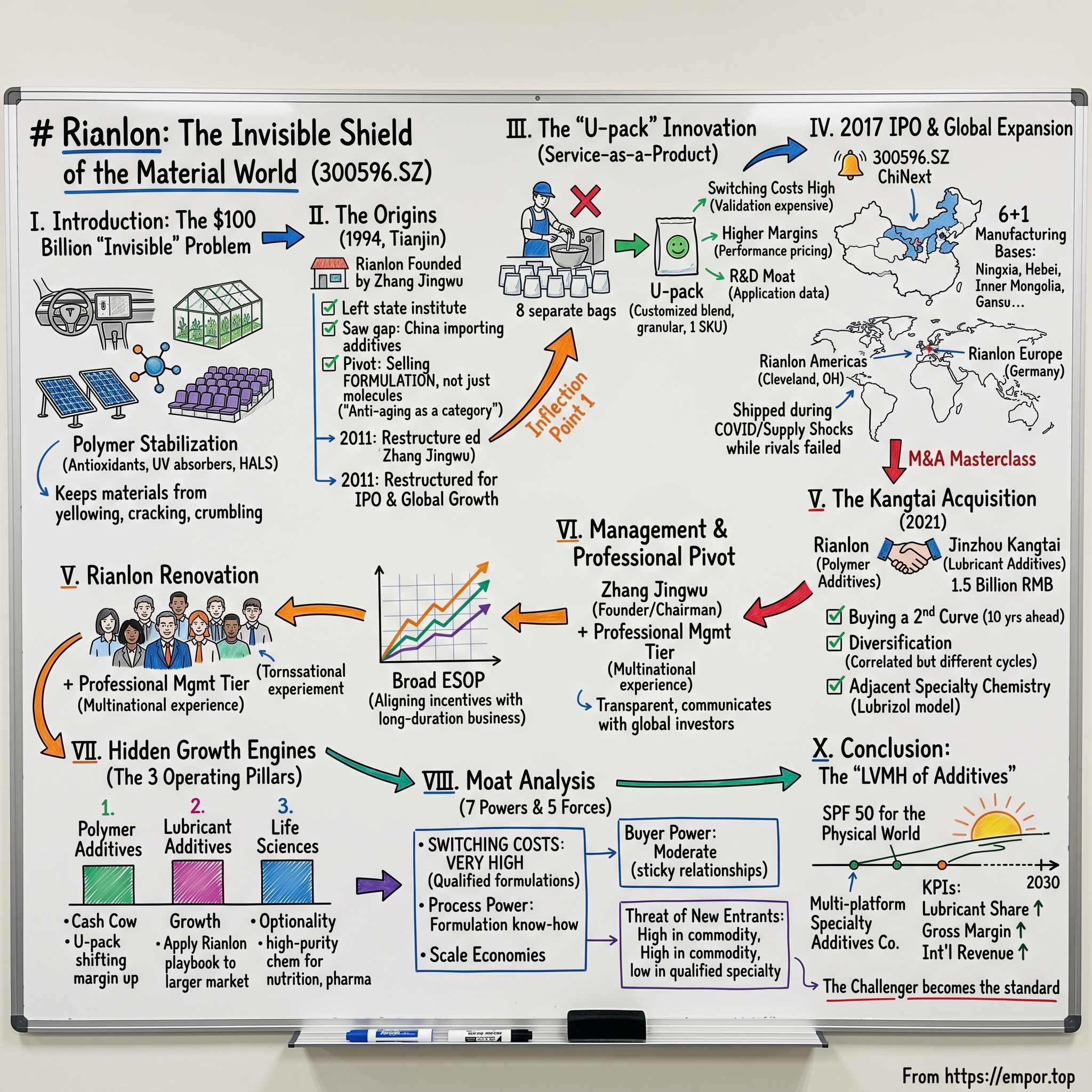

Rianlon: The Invisible Shield of the Material World

I. Introduction: The $100 Billion "Invisible" Problem

Walk into any Tesla showroom on a sunny afternoon and run your hand along the dashboard. It feels solid, silky, engineered. What you are actually touching is a carefully orchestrated chemistry experiment fighting a slow-motion war against physics. Every photon of ultraviolet light striking that surface is trying to rip apart the polymer chains that give the plastic its shape. Every molecule of atmospheric oxygen is hunting for a dangling carbon bond to oxidize. Left unchecked, that dashboard would crack, yellow, and crumble within a year.

It doesn't. And the reason it doesn't is almost never discussed outside of a small tribe of industrial chemists.

Think about the polyethylene sheet covering a greenhouse in Almería, Spain, growing winter tomatoes for European supermarkets. Think about the polypropylene webbing of a stadium seat at the Beijing National Aquatics Center, baking for twelve hours a day in summer. Think about the ethylene-vinyl-acetate film sandwiched between the glass layers of a solar panel in the Mojave Desert, expected to last twenty-five years without delaminating. Think about the nylon rope on a North Sea oil rig. The polyurethane coating on a wind turbine blade. The polymer matrix holding together the carbon fiber in a BMW i4.

All of this is, at a molecular level, dying. And all of it is being kept alive by a category of chemicals most consumers have never heard of: anti-aging additives. Antioxidants. UV absorbers. Hindered amine light stabilizers. In industry shorthand: polymer stabilization.

The global market for these invisible protectors runs into the tens of billions of dollars annually and sits inside a plastics value chain valued north of six hundred billion. For almost the entire post-war era, the business was dominated by German, Swiss, and American chemistry giants. BASF. Ciba-Geigy (later absorbed by BASF). Clariant. SONGWON. The names on the patents reflected the winners of the twentieth century's petrochemical buildout.

Then, quietly, over thirty years, a company from Tianjin started showing up. Not with cheaper me-too products dumped on the market, though that was the stereotype. But with customized "cocktails" of additives delivered as a service. With laboratories in Cleveland and Düsseldorf. With a manufacturing network spread across six Chinese provinces that kept shipping during the worst of the 2020-2022 supply shocks. With a checkbook opened for the kind of adjacent acquisition that would make a Berkshire Hathaway analyst nod approvingly.

The company is Rianlon Corporation, ticker 300596.SZ on the Shenzhen ChiNext. It is not a household name. It will never be a household name. But if you believe that the physical world will continue to exist tomorrow, you are, in a very real sense, betting on Rianlon.

This is the story of how a founder named Zhang Jingwu took a commodity powder business and turned it into a "service-as-a-product" powerhouse. How a seventeen-year-old private enterprise in a state-dominated industry figured out how to charge BASF-like margins without a BASF-sized balance sheet. How a single M&A move in 2021 may have laid the groundwork for a second act bigger than the first. And how the unglamorous business of keeping plastic from turning yellow quietly became one of the more interesting stories in Chinese specialty chemistry.

It is, in Acquired parlance, a "value-add commodity" story with genuine switching costs underneath. Which is a combination you rarely see, because if it were easy, everyone would do it.

Let's begin in Tianjin.

II. The Origins & The "Old" History

In 1994, Tianjin was not Shanghai. It was not Shenzhen. It was a gritty, grey port city on the Bohai Sea, best known for its tramcars, its seafood dumplings, and a chemical industrial zone the central government had spent three decades stuffing with state-owned enterprises making caustic soda, fertilizer, and bulk solvents. Private chemistry, in the modern sense, barely existed. The idea that a handful of researchers could leave a state institute, rent a workshop, and compete with Sinopec on anything was, to put it charitably, optimistic.

Zhang Jingwu was one of those researchers. The son of chemists by training and temperament, he had watched through the 1980s as China's industrialization created enormous demand for plastics without a matching capability for the boring-but-essential additives that make modern plastics actually work. The country was importing nearly every gram of hindered phenolic antioxidant it used. Ciba-Geigy's Irganox 1010, the white powder that kept polypropylene from degrading under heat and light, was effectively a tax on Chinese manufacturing, paid in hard currency to a Swiss company.

Zhang saw the gap. He gathered a small founding team and, in 1994, established what would become Rianlon. The early years were, by any honest telling, unglamorous. The company operated out of a modest facility, made a narrow range of phenolic antioxidants, and sold into domestic plastics converters who would buy on price and walk the moment a rival offered a discount of a few RMB per kilogram. Margins were thin. Competitors multiplied. The list of Chinese antioxidant makers from that decade reads like a war memorial today—most did not survive.

But Zhang spotted something that his peers missed, and it became the founding insight of the entire company. Selling a single white powder, even one as technically difficult as Antioxidant 1010, was a commodity business. You won on cost, and you died on price. The real product customers needed was not a molecule. It was a formulation. A plastic converter making a polypropylene automotive part did not want to buy a phenolic antioxidant. They wanted their part to pass a thousand hours of xenon-arc testing without turning yellow. Those are not the same thing.

This was the pivot from selling "ingredients" to selling "anti-aging as a category." It would take another fifteen years to fully express itself in the product line, but the intellectual seed was planted in the late 1990s.

We're going to move quickly through the 1990s and 2000s, not because nothing happened, but because the pattern of what happened is what matters. The company steadily broadened its product range from antioxidants into light stabilizers. It built its first modern manufacturing plant. It survived the 2008 financial crisis better than most because specialty chemistry demand is less cyclical than bulk petrochemicals. It began hiring chemistry PhDs and building an actual R&D culture, which in 1990s Chinese private industry was genuinely rare.

The moment that bridges the old history to the new came in 2011, when Rianlon restructured itself from a limited-liability company into a joint-stock company. In Chinese corporate law, this is the formal prerequisite for an eventual IPO, and in corporate practice, it is the moment a founder-run private business declares that it intends to become something larger than itself. Zhang and the founding team were effectively announcing: we are going to outgrow Tianjin. We are going to go public. And we are going to go global.

What made that declaration credible, rather than aspirational, was the product innovation that had been quietly brewing in Rianlon's labs. Because by 2011, the company was no longer just making better versions of BASF's molecules. It was starting to make something the incumbents did not make at all.

III. Inflection Point 1: The "U-pack" Innovation

Picture the shop floor of a mid-sized plastics converter in Zhejiang province around 2012. A worker in blue coveralls is standing at a mixing station. Next to him are eight open sacks of white and off-white powders. One is a primary antioxidant. One is a secondary antioxidant. One is a UV absorber. One is a hindered amine light stabilizer. One is an acid scavenger. One is a processing aid. The dosages are different for each. The worker is scooping, weighing, and dumping them into a hopper that feeds the extruder making patio furniture.

Every single step in that process is a chance to screw up. Scoop too much of one. Miss a batch of another entirely. Inhale the dust. Get a lump of unmixed powder in the hopper that creates a weak spot in the product six months later. The worker is doing his best. The plant manager is yelling at him to move faster. The quality engineer back at the brand owner will send back the rejected batch in three weeks and no one will know why.

This was, for decades, how polymer additives were used. Rianlon's observation, in essence, was that the customer did not want eight sacks. The customer wanted one sack. And the contents of that one sack should be Rianlon's problem, not the customer's.

Enter the U-pack.

The U-pack is, at its heart, a simple idea executed with meticulous discipline. Rianlon's R&D team sits with the customer, learns the exact polymer grade, the end application, the temperature profile of the extruder, the expected service life, the regulatory constraints, and the price target. They formulate a customized blend of anti-aging additives, typically in the form of a single free-flowing granular product, sometimes in a wax or polymer carrier, that the customer can dose in one step at the correct loading level. One SKU. One number on the recipe card. One supplier relationship for an entire family of problems.

Why this matters is easy to underestimate. On the surface, it looks like a packaging innovation. In practice, it is a business-model inversion.

Consider what it does to the customer relationship. To make a proper U-pack for a new application, Rianlon has to know things about the customer's process that the customer's own engineers sometimes don't know. The U-pack formulation gets validated inside the customer's product. That validation is expensive, time-consuming, and very difficult to rerun with a second supplier purely on the basis of a lower quote. The moment the customer's product ships with a Rianlon U-pack inside it, switching costs are no longer theoretical.

Consider what it does to margins. A standard phenolic antioxidant is a globally traded commodity with price transparency measured in dollars per kilogram. A customized U-pack, tuned to a specific application, billed for its performance rather than its bill of materials, can command meaningfully higher gross margins. Rianlon has not disclosed a precise per-kilogram breakdown—specialty-chemicals companies almost never do, and reasonable people can have different views on exactly how wide the margin differential is—but the company's segment-level profitability and its qualitative disclosures consistently indicate that customized formulation products carry materially higher unit economics than the base additive sold as a single ingredient.

Consider what it does to the R&D moat. Each U-pack engagement generates proprietary application data. Over a decade, Rianlon built an internal library of formulations, failure modes, and customer-specific solutions that is genuinely difficult for a new entrant to replicate. A competitor can reverse-engineer a molecule. It is much harder to reverse-engineer a decade of "this customer's extruder at this temperature with this resin grade needs this ratio."

This is the heart of what the company later called its "one-stop-shop" strategy, and what I'd argue is more fundamentally a service playbook wrapped in a chemical delivery mechanism. Rianlon began to look less like a specialty chemicals manufacturer and more like a contract formulation partner that happened to also make its own raw materials. The commodity-ingredient pricing war kept raging among its Chinese peers. Rianlon, increasingly, was not in it.

All of which set up the next step in the arc. Because once you have a differentiated product, the next question is whether you can scale it.

IV. Inflection Point 2: The 2017 IPO & Global Capacity War

On February 24, 2017, Rianlon Corporation rang the bell on the ChiNext, Shenzhen's Nasdaq-styled growth board, under the ticker 300596. The listing raised capital that, in absolute terms, was modest by Silicon Valley standards but strategically transformative for a specialty chemistry firm of Rianlon's size. Zhang Jingwu and his team now had public currency, a balance sheet with room to expand, and, just as importantly, a public obligation to execute.

The capital markets framing here matters. ChiNext in 2017 was still searching for a genuine identity. It had its share of bubble-era consumer-internet names and questionable small caps. What it did not have, in abundance, was well-run specialty industrial platforms with real global ambitions. Rianlon's listing positioned it inside a relatively thin cohort of Chinese chemistry companies that institutional investors, foreign and domestic, could actually build a thesis around.

The use of proceeds tells you where Zhang's head was. This was not a war chest for financial engineering. It was gasoline on the capacity fire.

Over the next several years, Rianlon built out what management began describing as its "6+1" manufacturing footprint: six principal production sites across China plus a dedicated base for higher-value intermediates. The geographic logic was deliberate. Zhongwei, in Ningxia's coal-chemistry corridor, gave the company access to low-cost intermediates and utilities. Hengshui in Hebei provided proximity to the Bohai petrochemical cluster and the Tianjin port. Additional sites in Inner Mongolia, Gansu, and elsewhere extended the network in ways that reduced single-point-of-failure risk and tapped local raw-material ecosystems.

For most of 2017-2019, this all looked like standard Chinese industrial capacity expansion. A lot of money spent on sprawling concrete-and-steel production bases that would take years to fully utilize. Skeptics wondered whether Rianlon was overbuilding.

Then 2020 happened, and the "6+1" network turned into what may have been the single most valuable piece of infrastructure the company owned.

During the COVID disruption, the global specialty chemistry supply chain fractured repeatedly. European plants went offline for COVID outbreaks and, later, for energy-cost reasons when natural gas prices exploded after the 2022 Russian invasion of Ukraine. U.S. Gulf Coast facilities got hit by Hurricane Laura in 2020 and the Texas freeze in February 2021. Shanghai's lockdown in the spring of 2022 stranded inventory at the wrong end of the country. Multinational buyers, who a decade earlier had rolled their eyes at the idea of "supply chain security" as a procurement criterion, suddenly found themselves writing it into RFPs in bold type.

Rianlon could ship. When one site was constrained by logistics or regulatory inspection, another could pick up the load. The company's disclosures during this period emphasize high utilization rates across the network and, critically, an ability to maintain deliveries into multinational customers when Western competitors were issuing force majeure letters. For a specialty buyer—say, the procurement team at a European automotive Tier 1—"Rianlon delivered during COVID" is not a marketing line. It is a permanent change in the approved-vendor list.

The second half of the 2017 transformation was what Rianlon did with the other end of the supply chain: sales. It established Rianlon Americas, headquartered near Cleveland, and Rianlon Europe, based in Germany. The decision to plant real offices in Ohio and Germany, rather than run a low-cost export desk from Tianjin, signaled the business-model ambition. These were not shipping agents. They were technical-sales hubs with application chemists, regulatory specialists, and customer-service teams embedded in the time zone and language of the buyer.

The commercial implication is that Rianlon began competing in Europe and North America on the basis of service and responsiveness, not just price. When a coatings formulator in Cologne had a performance issue on a Tuesday morning, a Rianlon technical-service chemist speaking German could be on-site that week. This is the kind of go-to-market that the traditional Chinese-export model simply cannot replicate, and it is where the U-pack strategy and the global footprint started to reinforce each other in a way that was more than the sum of the parts.

By the end of 2020, Rianlon had transformed itself from a domestic Chinese antioxidant maker with an export sideline into something that genuinely resembled a globalized specialty chemistry firm. A smaller BASF, some bulls started saying. And that framing, flattering as it was, brought up the obvious next question: where do you grow from here? Because the polymer additives market, while large, is not infinite.

The answer came in 2021.

V. M&A Masterclass: The Kangtai Acquisition

On August 4, 2021, Rianlon announced that it would acquire a majority stake in Jinzhou Kangtai Lubricant Additives, with the total transaction value, phased across multiple tranches, amounting to roughly 1.5 billion RMB. In the pantheon of Chinese M&A deals announced that year—Tencent, Alibaba, and a parade of EV and semiconductor names were throwing around checks an order of magnitude larger—this was not front-page news.

It should have been.

Because what Zhang Jingwu and his team were doing was, in a very literal sense, buying themselves a second company, a second curve, and a decade of time.

Let's back up and understand Kangtai. Jinzhou Kangtai, based in Liaoning, was founded in 1994—the same year as Rianlon, a coincidence that is almost too neat—and had spent nearly three decades building a specialty lubricant-additive business. Unlike Rianlon's polymer-additive world, which keeps plastics from aging, Kangtai's world is the lubricant world: the chemical packages that go into engine oils, industrial gear oils, hydraulic fluids, transmission fluids, and metalworking fluids. The toolkit is different—detergents, dispersants, anti-wear agents, viscosity modifiers, pour-point depressants—but the strategic structure of the business is strikingly similar. High-spec customized formulations. Sticky customer relationships. Regulatory qualification that creates switching costs. Global buyers. Oligopolistic incumbents.

The global lubricant-additive market is essentially controlled by four players: Lubrizol (owned by Berkshire Hathaway, incidentally), Infineum (the Shell-ExxonMobil joint venture), Chevron Oronite, and Afton Chemical. Outside that "Big Four," the market is fragmented across regional specialty players with specific niches. Kangtai was the leading independent Chinese player, with particular strength in engine-oil additive packages for the domestic market.

Did Rianlon overpay? The honest answer is: maybe a little, probably not egregiously. Public comparables in the space trade at wide bands. Lubrizol's financials aren't independently reported anymore after the Berkshire take-private. Afton is inside NewMarket Corporation and tends to trade on fundamentals that reflect an oligopolist's cash-flow profile. Based on the available disclosures about Kangtai's historical revenue and earnings around the time of the transaction, and cross-referenced against the EV/EBITDA ranges that publicly traded specialty-additive comparables have historically commanded, the acquisition multiple appears to have been in a range that is defensible if you believe in the strategic fit and aggressive if you assume status-quo execution.

Which brings us to the strategic logic, and this is where the deal stops being about a multiple and starts being about a thesis.

First: Kangtai was, in Zhang's own framing to investors, "the Rianlon of ten years ago but for lubricants." Same founding era. Same stage of differentiation. Same challenge of moving upmarket from a commodity base into formulated, customized packages. Rianlon had walked that exact path in polymer additives and had a playbook. Grafting that playbook onto Kangtai's lubricant business was the core of the value-creation argument.

Second: Kangtai's end markets were different from Rianlon's polymer additives in ways that meaningfully diversify the business. Polymer additives sell into plastics converters, which are tied to consumer durables, packaging, construction, and automotive interiors and exteriors. Lubricant additives sell into engine oils and industrial fluids, which are tied to vehicle fleets, manufacturing utilization, and industrial maintenance cycles. The two are correlated with the broader economy, but not identically, and certainly not to the same individual customers.

Third, and this is the subtle one: the capital-allocation discipline is genuinely striking. During the period that Rianlon made this acquisition, Chinese corporate M&A was, to put it generously, a mixed bag. For every sensible deal, you had manufacturing companies buying real estate, chemical companies buying internet startups, and traditional industrial groups paying premiums for blockchain-adjacent ventures they did not understand. Rianlon, sitting on a specialty-chemistry cash engine with a public-market multiple to defend, chose to buy an adjacent specialty chemistry platform. The polite word is "disciplined." The less polite word is "boring." Both are compliments in this context.

The post-acquisition integration has not been flawless—these things never are. Chinese corporate acquisitions frequently struggle with the cultural challenge of stapling a new leadership team onto an existing founder-run business without breaking the thing you just bought. In Kangtai's case, Rianlon's public disclosures indicate that performance has tracked the strategic thesis broadly, with some near-term volatility tied to raw material costs, the cyclicality of industrial lubricant demand, and the ongoing work of integrating Kangtai's product lineup with Rianlon's global sales network.

What the acquisition accomplished, strategically, was simple: Rianlon now had two horses, in two different races, in two different but analogous markets. Polymer additives and lubricant additives. The "multi-platform specialty additives company" framing became internally coherent rather than aspirational.

And the person holding the reins on that transformation is someone we haven't talked about in enough detail yet.

VI. Management & Incentives: The Professional Pivot

Zhang Jingwu is not a character from the Chinese tech-founder mythology. He does not do elaborate annual keynotes. He does not tweet. He does not have a book deal. Interviews with him, when he does them, tend to be in specialty industry trade press and read like conversations with a thoughtful chemical engineer rather than a charismatic CEO.

That understated style is, I suspect, genuinely part of what the company is.

Zhang built Rianlon from a small Tianjin lab over three decades. He retained the chairman's seat through the company's 2017 IPO and has continued to anchor its strategic direction. The founding team, along with early backers, holds a controlling but stable interest in the company—enough to ensure strategic continuity, not so much that the business feels like a private family fiefdom dressed up as a public company. In a country where the founder-dominance of listed companies can sometimes slip into capital-allocation quirks, Rianlon's governance looks more like a Swiss specialty chemistry firm than like a typical Chinese entrepreneurial small-cap.

What's notable, and worth spending a moment on, is how deliberately Zhang has built a professional management tier beneath him. As Rianlon globalized, the company brought in executives with multinational experience, particularly on the international-sales and applications-technology sides. The Americas and Europe operations are run by leaders who understand how multinational procurement teams actually buy specialty chemistry, and who can sit across the table from a BASF-trained counterpart without cultural friction. This sounds trivially obvious until you observe how many Chinese industrial exporters still fail at it.

The deeper signal, though, is in how Rianlon pays its people.

The company has a history, spanning multiple years, of implementing broad-based employee stock ownership plans—ESOPs—that extend well beyond the C-suite into mid-level engineers, application chemists, plant managers, and commercial-team leaders. In specialty chemistry, where institutional knowledge lives in the heads of the people who spent ten years learning how to stabilize a specific kind of polyurethane for a specific kind of customer, the ability to retain that talent is a genuine competitive weapon. Rianlon's ESOP program, viewed alongside its disclosed compensation philosophy, suggests a management team that has thought carefully about how to align incentives with the long-duration nature of the business.

This matters more than it sounds. Specialty chemistry is a field where the unit of value creation is the decade, not the quarter. A U-pack formulation developed in 2020 may deliver its best margin in 2027. A customer qualification started in 2024 may not show up as revenue until 2026. Management teams that are compensated on annual earnings and equity vesting schedules aligned with multi-year product cycles make different decisions than management teams focused on the next twelve months. Rianlon's structure is closer to the former.

The other thing worth mentioning is the "accessibility" factor, which sounds soft but matters a lot in how global capital gets allocated. Rianlon has, over the past several years, developed a reputation among foreign institutional investors as one of the more transparent and communicative Chinese specialty chemistry companies. Management does investor roadshows, engages with analysts, and is willing to discuss the business in the kind of strategic detail that global long-only buyers expect. This is not universally true of Chinese mid-caps. It is the difference, quietly, between being owned by a diversified international shareholder base and being owned primarily by domestic retail speculation.

A Western-style transparency layer. Chinese-speed execution. A founder who remembers mixing antioxidant powders in a small lab in 1994. A professional management team running multi-continent operations. A shareholder base that mixes long-duration institutional capital with founder alignment. This is, in the specialty-industrial world, an uncommon combination.

And it is the platform on which the company's next growth engines are being built.

VII. The "Hidden" Growth Engines: Lubricants & Life Sciences

One of the more interesting discrepancies in how Rianlon is covered versus how the company actually operates is the stickiness of the original label. To most investors, particularly those who last looked at the name around the time of its 2017 IPO, Rianlon is "the Chinese plastic additives company." That framing, already incomplete in 2017, has become meaningfully wrong by 2026.

Let's walk through the three operating pillars of the business as they actually exist today.

The first pillar, polymer additives, remains the majority of revenue. This is the original engine—antioxidants, light stabilizers, and the U-pack formulation business. It grew through the 2010s at rates that, depending on the year and segment, generally fell in a mid-to-high-teens percentage range, with some variability tied to raw material cycles and downstream demand in plastics, coatings, and fibers. This is the business that built the company, built the global footprint, and built the relationships with multinational converters. Anyone who writes this pillar off as "mature" is missing the fact that the U-pack shift from commodity ingredients to formulated solutions continues to expand the margin mix and extend the growth runway. The polymer business is the cash cow, but it's a cash cow that is still walking uphill.

The second pillar, lubricant additives, is the Kangtai-driven second curve. Post-integration, this segment has been scaling into a much larger addressable market than Rianlon's original polymer world. The global lubricant-additive market runs well into the double-digit billions of dollars, and the Chinese domestic market alone, driven by vehicle fleet growth, industrial equipment utilization, and the gradual upgrading of engine-oil specifications toward international standards, represents a structural growth opportunity that the Big Four global incumbents have not fully captured. The strategic thesis for this segment is straightforward: apply the Rianlon playbook—vertical integration, customized formulations, global commercial reach, supply chain reliability—to a market that has historically been served by either imported oligopolist products or lower-tier domestic suppliers. Management's stated ambition is for the lubricant segment to scale to a meaningful share, plausibly above thirty percent, of total revenue over the medium term, with the exact trajectory depending on integration pace and market conditions.

The third pillar is the wildcard, and the one most analysts undervalue: life sciences and specialty intermediates. This is the "small now, potentially big later" piece of the portfolio. Rianlon has been extending its specialty chemistry capabilities into high-purity chemicals for applications in nutrition, pharmaceutical intermediates, and related life-sciences adjacencies. The logic is that the technical infrastructure needed to make a performance antioxidant for a medical-grade polymer is, in many cases, a close cousin of the infrastructure needed to make a high-purity nutraceutical intermediate. The same reaction chemistry. The same purification techniques. Similar regulatory discipline.

Whether this segment becomes a meaningful third leg of the business, or remains a strategic option with optionality value but limited near-term revenue impact, is one of the genuinely open questions about Rianlon. Management has signaled intent. The operational build-out is visible in capital expenditure disclosures. The commercial traction, as of the most recent reporting, is still nascent. Life sciences is the part of the story where I would tell a careful reader: watch the disclosed capacity utilization, watch the product-mix disclosures, and do not underwrite it as a certainty. It is an optionality line in a portfolio that does not need it to make the core thesis work.

What the three-pillar structure buys the company, collectively, is something like the specialty-chemistry version of a diversified industrial platform. Polymer additives provide the current cash. Lubricant additives provide the near-to-medium-term growth. Life sciences provides the longer-dated optionality. The segment margins are different, the customer bases are different, the geographic mixes are different, and the cyclical exposures are different enough to provide real diversification without drifting into the "conglomerate discount" territory that destroys value.

A sharper way to say it: Rianlon looks, increasingly, like a platform designed to allocate capital across a family of specialty-additive businesses rather than a single-product company trying to milk one chemistry. If that reframing catches on in how the market values the company, the implied multiple expansion is not trivial.

But whether the market should value it that way, of course, depends on whether the moat is real.

VIII. The Strategy Framework: 7 Powers & 5 Forces

At this point, any serious Acquired-style analysis has to sit down and run the moat through a couple of frameworks. Let's do the Hamilton Helmer 7 Powers treatment and then the Porter Five Forces view, because they tell complementary stories and neither is complete on its own.

Starting with the 7 Powers:

Switching costs look genuinely high, and this is the single most underappreciated piece of the Rianlon story. When a multinational automotive Tier 1 qualifies a specific U-pack formulation for a specific polymer grade going into a specific interior dashboard component, the validation process has consumed months or years of laboratory testing, accelerated weathering tests, OEM approvals, and regulatory paperwork. Switching that qualified supplier mid-program means re-running the validation, which means accepting program risk, timeline risk, and warranty-exposure risk. The incremental savings from sourcing the same generic antioxidant at a lower price from a competitor do not come close to justifying the switching risk for a qualified specialty formulation. This is the same structural dynamic that has historically protected the specialty-chemistry incumbents—BASF, Clariant, Lubrizol—and it now protects Rianlon on the fraction of its business that is genuinely formulated and qualified.

Scale economies are real but not as decisive as the switching-cost argument. Rianlon's multi-site manufacturing footprint and its vertical integration into certain intermediates do give it unit-cost advantages over smaller Chinese competitors, and those advantages are particularly visible during periods of industry distress, when smaller players get squeezed out of the market by raw material volatility or by underutilized capacity. Scale economies matter here mainly as a survival power rather than as a market-share-taking power.

Cornered resource is where the argument gets interesting. The specific resource Rianlon has cornered is harder to articulate than "we own the lithium deposit." It is closer to "we have a specific combination of proven global supply chain reliability, a multi-site Chinese manufacturing base, a globally distributed technical-service network, and a decade of proprietary application data." None of those individually is a cornered resource in the classical sense. Collectively, they are something approaching one, because the set of global suppliers who can credibly pitch all of the above to a multinational procurement team is small and does not include most of Rianlon's domestic Chinese peers.

Process power is worth mentioning, if subtly. The U-pack formulation business, with its decade-plus accumulation of customer-specific formulation knowledge and application data, represents a process capability that is difficult to replicate rapidly even for a well-capitalized entrant. You can buy the equipment. You cannot buy the learning curve.

Branding and counter-positioning and network economies look less applicable here. The customers are industrial. The network effects are weak. Branding matters at the specification level (the BASF or Lubrizol name on an approved-vendor list does carry weight), but this is the power Rianlon is still building, not the one it has locked in.

Shifting to Porter's Five Forces:

Bargaining power of buyers is moderate. Rianlon's customers include some genuinely large, sophisticated multinational procurement organizations that have experience squeezing specialty suppliers on price. Mitigating factors are the qualified-formulation stickiness already discussed, and the customer-specific nature of the U-pack products, both of which shift the negotiation away from per-kilogram price toward total cost of ownership and reliability.

Bargaining power of suppliers varies by input. Rianlon's vertical integration into certain intermediates reduces its exposure to upstream price volatility, but not entirely, and periods of raw material price spikes have historically compressed margins across the specialty additives industry. This is a structural feature of the business, not a Rianlon-specific weakness.

Threat of new entrants is the force where the Chinese specialty chemistry industry has the most interesting dynamic. On one hand, China has the world's most aggressive capacity-building culture in industrial chemistry, and new entrants appear regularly in adjacent commodity-tier products. On the other hand, the specialty formulation and global-qualification layers of the business are meaningfully harder to enter than the commodity molecule layer, and most new entrants end up competing at the commodity tier rather than in the formulated-specialty tier where Rianlon increasingly operates.

Threat of substitutes is structurally low, and this is one of the quiet beauties of the business. There is no digital or software substitute for polymer stabilization. A plastic that has to last twenty-five years on a solar panel is going to need chemistry, not code. Long-term material-science trends—bioplastics, recycled content, circular polymers—do create some substitution risk at the edges, but even those alternative polymers generally need anti-aging additives; the formulations just change. In the long arc, the addressable market for anti-aging chemistry is more likely to grow than to shrink as the world deploys more, not less, polymer into durable applications like EVs, solar, wind, and water infrastructure.

Rivalry among existing competitors is the Force most visible in quarterly results. The Chinese antioxidant and light stabilizer industry is fragmented enough that periodic price wars are a feature, not a bug, of the landscape. Rianlon's response has been the one you'd want to see: move up the value chain, segment away from the pure-commodity battlefield, and use the global-customer base and formulated-product mix to protect margins even as peers discount.

The synthesis of the frameworks is reasonably consistent: Rianlon is not a company with a single overwhelming source of moat. It is a company that has assembled a layered set of advantages—switching costs at the customer-qualification level, scale economies in Chinese manufacturing, an emerging cornered-resource in global supply reliability, and a multi-year process advantage in formulation know-how—that collectively produce something durable. It is less impregnable than a network-effect technology monopoly. It is more durable than a typical Chinese industrial exporter.

For an investor, the question becomes: what does this combination teach us about how to think about specialty industrial businesses generally?

IX. The Playbook: Lessons for Founders & Investors

Pull back from Rianlon specifically for a moment. The more interesting question is what the arc of this company teaches us about a category of business that does not get enough oxygen in the tech-heavy investing narrative: the "anti-commodity" specialty industrial.

The first lesson, and it is one Acquired has hit on repeatedly in other contexts, is that "boring" industries are where business-model innovation compounds most quietly. A software company that doubles its margin is a headline. A specialty chemistry company that shifts fifteen percent of its revenue from commodity antioxidants to formulated U-packs over a decade is also doubling its margin, in a way, but nobody writes about it. The anti-commodity playbook—take a transacted ingredient, reframe it as a service, embed yourself in the customer's workflow, collect application data, charge for outcomes instead of tonnage—is a universal template that applies far beyond polymer stabilizers. You can run the same logic for industrial lubricants, adhesives, specialty coatings, enzymes, catalysts, and semiconductor wet chemicals. The companies that execute the reframe win. The companies that keep selling by the kilogram slowly lose.

The second lesson is the global-local balance. Zhang Jingwu did not just export product from Tianjin. He set up real commercial and technical operations in Ohio and Germany and staffed them with people who speak the customer's language, both literally and operationally. For a Chinese specialty industrial firm, this is the difference between being a low-cost vendor of last resort and being a strategic partner of first choice. For any firm in any country, the underlying principle is that you cannot sell specialty products to global customers from a single country and a single time zone. The cost of the localized presence, measured in dollars, is trivial compared to the cost of losing qualification trials because your customer-service response time to a Cleveland-based buyer is thirty-six hours.

The third lesson is about capital allocation and what I'll call "second curve discipline." When Rianlon had cash flow to deploy from the polymer-additive business, it had options. It could have diversified into Chinese real estate, which several of its peers did, to generally regrettable results. It could have bought a consumer brand. It could have chased an AI narrative by acquiring a software startup and slapping an "industrial AI" label on it. Instead, it bought Kangtai. A lubricant additives platform that is analogous to Rianlon's original business in structure, different in end-market exposure, and large enough in addressable market to support a decade of growth. The second curve, when you're building one, should be related to the first curve. This sounds tautological until you observe how many Chinese (and American, and European) industrial companies violate it.

The fourth lesson, implicit across everything above, is the value of boring patience. Rianlon took thirteen years from founding to serious product-line expansion, seventeen years from founding to the joint-stock transition, twenty-three years from founding to IPO. Zhang Jingwu is still running the company in his thirty-second year. That kind of duration match between the founder's horizon and the business's decision cycles is not something capital markets can easily generate. It is a feature of a specific kind of founder-led industrial that can compound advantages that shorter-horizon competitors cannot. When you are evaluating a specialty industrial business, the founder's biography matters.

Which, naturally, leads to the question most readers of a piece like this are asking: okay, but what is the investment case, and what could go wrong?

X. Conclusion & The Bull/Bear Case

Any honest look at Rianlon in 2026 has to sit with both sides of the ledger, because the company is at a transition point where the risks and the opportunities are equally real.

The bear case, laid out in its strongest form, has three pillars.

The first is Chinese industry oversupply. Polymer additives capacity in China expanded substantially in the late 2010s and early 2020s, and periodic price wars in commodity-tier products have been a feature of the industry for years. A prolonged downturn in downstream plastics demand, particularly in construction and consumer durables, combined with continued capacity additions, would compress margins across the industry, and Rianlon would not be immune—its formulated-product mix helps but does not fully insulate. Raw material price volatility in phenols, cresols, and certain specialty intermediates compounds this risk.

The second is the EV-transition wildcard, and this is subtler than the headlines suggest. Conventional intuition holds that electric vehicles reduce demand for lubricants because they do not have internal combustion engines. That is partially true—engine oil volumes decline—but it is incomplete. EVs still need transmission fluids, thermal-management fluids, electric-drive unit lubricants, and greases. And the lubricant-additive sophistication for EV-specific applications is actually higher, not lower, than for traditional engines. The net picture for Rianlon's lubricant segment probably remains growth-positive in the medium term, but there is genuine uncertainty about the trajectory, and anyone underwriting the Kangtai acquisition as "lubricants go up forever" is not being careful.

The third is execution risk on the "multi-platform specialty additives company" ambition. Running three segments—polymer, lubricant, life sciences—across multiple continents, with customer bases that range from plastic converters to pharmaceutical intermediate buyers, is genuinely harder than running a single-segment business. Integration fatigue on the Kangtai acquisition, potential cultural frictions, and the managerial bandwidth required to simultaneously scale the second curve while defending the first, are real. Rianlon's management track record is encouraging, but not yet infallible.

A broader risk worth flagging, briefly, is geopolitical. A Chinese specialty chemistry company that sells into multinational automotive, coatings, and industrial customers in the U.S. and Europe is, by definition, exposed to tariff risk, export-control risk, and procurement-nationalism risk. The company's distributed manufacturing footprint mitigates some of this. It does not eliminate it.

The bull case is the mirror image and, in my view, the more interesting side of the argument.

Start with the underlying market. The physical world is not shrinking. Plastics consumption, global wind and solar capacity, EV production, industrial machinery, and consumer durables are all projected to grow over the next decade, and all of them need anti-aging chemistry. The tonnage of polymer in the world is trending up, and as an increasing share of that polymer goes into applications with twenty-five-year service lives (solar panels, wind turbines, infrastructure pipes, EV structural components), the anti-aging intensity per kilogram of polymer is also trending up. This is a durable secular tailwind, and it is not contingent on any particular technology cycle.

Layer in Rianlon's strategic positioning. A company that has moved decisively from commodity ingredients to formulated solutions, that has built a globally distributed manufacturing and sales footprint, that has proven its supply chain reliability through the worst global disruption in decades, that has the balance sheet and the capital-allocation discipline to do adjacent acquisitions, and that has a founder-led management team with a long-duration perspective, is positioned in a way that a pure Chinese exporter, five years ago, simply was not.

The most evocative framing for the bull case is what I'll call the "LVMH of additives" concept. Not because Rianlon makes luxury products—it obviously does not—but because the strategic structure is analogous: a platform that accumulates specialty brands, specialty formulations, and specialty customer relationships across adjacent but distinct categories, with each category protected by genuine switching costs and each benefiting from the platform's scale. The polymer additives business. The lubricant additives business. The emerging life sciences business. Each of them, properly run, resembles a specialty category with pricing power, not a commodity category vulnerable to price compression.

If the bull thesis plays out, Rianlon in 2030 is not a Chinese antioxidant company. It is a multi-platform specialty additives company with meaningful presence across three end markets, revenue mix that has rebalanced toward higher-margin formulated products, and a global customer base for which "Rianlon inside" is a standard line on the specification sheet.

The KPIs that matter most for tracking whether that thesis is playing out, in my view, are three.

The first is segment revenue mix, specifically the share of total revenue coming from lubricant additives. The Kangtai thesis is either real or it is not, and the trajectory of the lubricant-additive contribution over the next several reporting periods is the most direct test. A meaningful re-weighting toward lubricants, at healthy margins, validates the second curve. Stagnation signals integration and execution issues.

The second is gross margin trajectory, with particular attention to the spread between commodity-tier and formulated-product margins. The U-pack strategy and the formulated-solutions playbook depend on the company continuing to shift revenue toward higher-margin customized products. If gross margin stays stubbornly tied to raw-material input price movements, the anti-commodity playbook is not actually working. If it drifts steadily higher over multiple cycles, it is.

The third is international revenue share, particularly in North America and Europe. This is the hardest metric for a Chinese specialty chemistry company to move, because it requires building qualified, high-service-content customer relationships in markets where the incumbents have a century of head start. If Rianlon's international share continues to climb, the global-local strategy is compounding. If it plateaus, the company is primarily a domestic Chinese story with an export side.

Watch those three numbers, and you are watching whether the thesis is proving out.

Pulling back from the specifics, the broader significance of Rianlon, for anyone interested in how businesses get built, is that it is one of the cleaner examples in Chinese specialty industry of a company that took the full journey: from commodity export to formulated solutions, from domestic manufacturer to global specialty platform, from single-segment operator to multi-platform capital allocator, without losing the founder's discipline and without breaking the business along the way.

The Acquired framing we started with—that everything around us is dying, and that Rianlon is, quietly, the SPF 50 for the physical world—is not just a turn of phrase. It is a business model statement. If you believe that polymer, in all its forms, is going to be the fabric of industrial civilization for another several decades, and if you believe that someone has to keep making the invisible chemistry that keeps that fabric from disintegrating, then the question is which company becomes the global platform for that role. The incumbents—BASF, Clariant, SONGWON—are formidable, credentialed, and deeply embedded. Rianlon is the most credible Asian challenger, and probably the most credible challenger globally outside the incumbents.

Whether the challenger ultimately becomes a peer, or plateaus as a respected regional specialist, is the story of the next ten years. The ingredients are in place. The execution is in progress. The proof is in the segment mix and the margin trajectory.

If the physical world continues to exist—and it is a reasonably confident bet that it will—there is, somewhere in the chain of companies that keep it from yellowing, cracking, and decomposing, a space for a company that is neither a German centenarian nor a Swiss specialist, but something new. A Chinese founder-led specialty platform that ran the anti-commodity playbook to its natural conclusion. Rianlon is the best candidate we have for what that company looks like.

It started, thirty-two years ago, with a chemist in Tianjin who figured out that the real product was not the powder. The real product was the protection. Everything since has been a three-decade-long exercise in staying true to that insight while scaling the business around it.

The dashboard in the Tesla is, right now, being held together by chemistry. So is the solar panel. So is the stadium seat. Whether Rianlon owns an increasing share of that invisible work over the next decade is a question that will be answered one qualified customer, one U-pack, one acquisition, and one carefully allocated capital commitment at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube