Sunresin: The Alchemy of Modern Industry

I. Introduction: The Invisible Layer of Everything

Picture the Atacama Desert of Chile at dawn. Or the high-altitude salt flats of Qinghai Province, where the air is so thin that workers need oxygen tanks, and the brine beneath the crust sits at an altitude of 4,000 meters above sea level. These are the places where the modern world is being born—not the gleaming Tesla showrooms in Shanghai, not the ARM design studios in Cambridge, but these desolate, otherworldly landscapes where lithium hides in salty water.

For decades, the extraction of lithium from these brines was a story of patience and evaporation. You pumped the brine into massive ponds. You waited. You waited some more. You watched the sun do its work for 18 to 24 months. By the time you had your concentrate, the price cycle had moved on, and half the lithium had been lost to inefficient chemistry. This was not a system designed for the age of electric vehicles. This was a system designed for the 1990s, when lithium was a curiosity used in ceramics and psychiatric medication.

And then, almost without the world noticing, a quiet company in Xi'an, China—a city better known for its terracotta warriors than its chemistry—rewrote the rules.

The conventional narrative of the electric vehicle revolution goes something like this: CATL makes the cells, Tesla designs the cars, and the miners in Australia and South America dig up the raw materials. It's a story of batteries, software, and mining. But the real bottleneck, the hidden chokepoint, sits somewhere nobody thought to look: inside tiny plastic beads the size of poppy seeds, coated with proprietary chemistry, packed into steel columns, that can pluck lithium ions out of brine the way a magnet pulls iron filings from sand.

Those beads are called adsorbent resins. The company that makes the best ones in the world is Sunresin New Materials. And their ticker, 300487.SZ, is one of the most interesting "picks and shovels" plays in the entire energy transition.

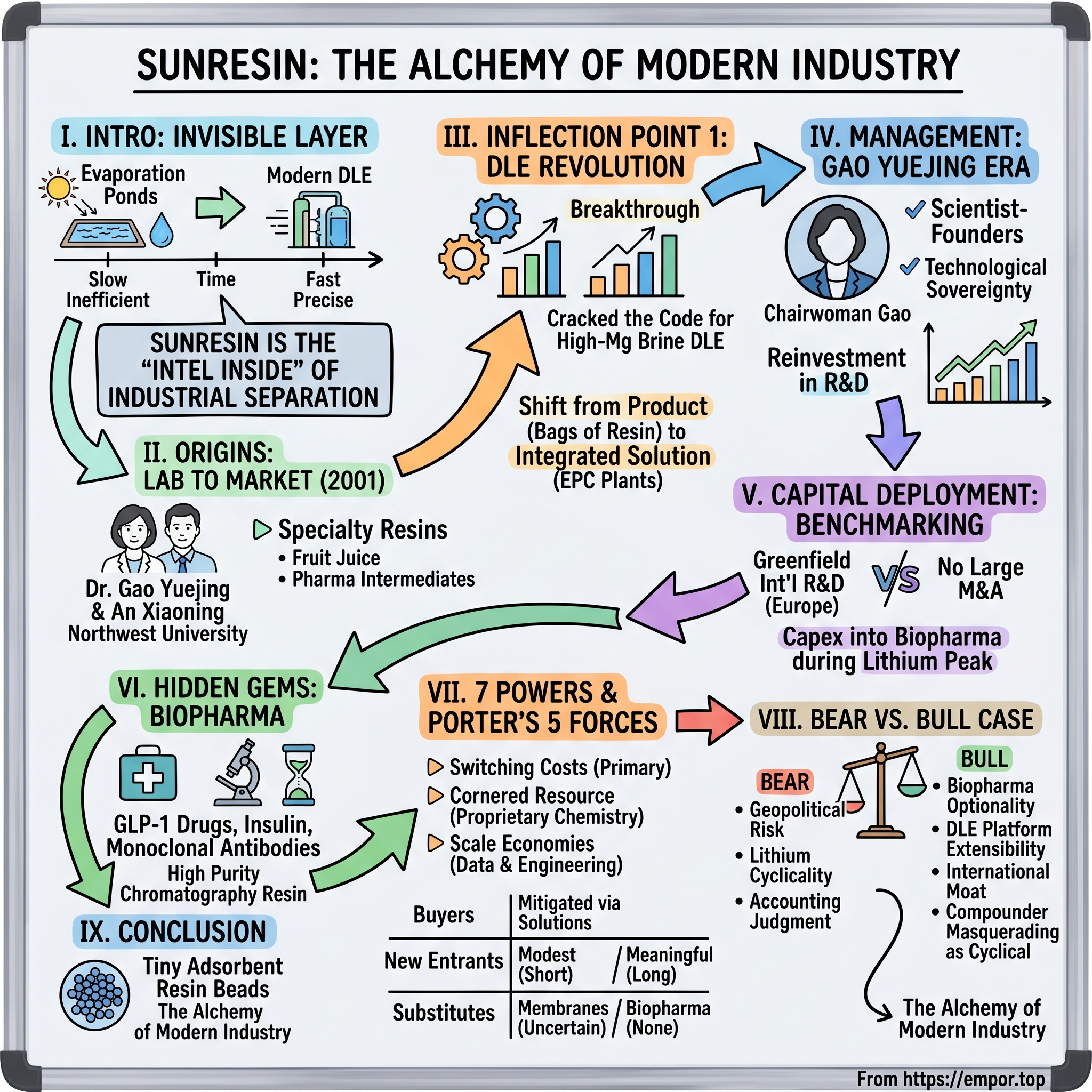

The thesis for this deep dive is simple but unconventional. Sunresin is not a chemical company. Sunresin is not a lithium company. Sunresin is the "Intel Inside" of industrial separation—the invisible layer that sits between raw materials and the finished products we care about. Whether you're extracting lithium from brine, purifying the active ingredient in a GLP-1 weight loss drug, or stripping heavy metals from industrial wastewater, the molecular workhorse doing the job is increasingly likely to be a Sunresin resin.

Over the next several hours, we'll trace this company's journey from an academic side project at Northwest University in Xi'an, to its ChiNext IPO, to its breakthrough moment in Direct Lithium Extraction (DLE), to its current expansion into biopharma—a move that could make the last twenty years look like the warm-up act. Along the way, we'll meet a chairwoman who trained as a chemist before most of her competitors had finished high school, we'll benchmark Sunresin against global giants like DuPont and Lanxess, and we'll try to answer a question that has puzzled sophisticated fundamental investors in Asia for years: is this a cyclical materials company priced like a growth stock, or a compounding platform priced like a cyclical?

Welcome to the alchemy of modern industry.

II. The Origins: From the Lab to the Market

In 2001, a woman named Gao Yuejing was at a crossroads familiar to every Chinese academic-entrepreneur of her generation. She held a doctorate in chemistry. She had spent years inside the university research system, publishing papers on ion exchange chemistry—a dry, unglamorous subfield known mostly for its role in making drinking water soft enough to wash your dishes. Her research partners and her husband, An Xiaoning, stood beside her. The question was whether to stay in the comfortable groove of academia, or to bet everything on the hypothesis that the next decade of Chinese industrial growth would need better molecules than the foreign chemical majors were willing to provide.

They bet on the molecules. Sunresin—technically Xi'an Sunresin Technology, later renamed and reorganized as Sunresin New Materials—was founded that year in a modest facility near the university. The ambition, viewed from today, sounds almost delusional. Bayer, Dow, Rohm and Haas, Mitsubishi Chemical, and a handful of other multinational giants had dominated global ion exchange resin production for half a century. Their production lines were measured in tens of thousands of tons per year. Sunresin's first commercial batch was measured in barrels.

But Gao and An had spotted something the multinationals had missed. The commodity ion exchange market—the one that served municipal water treatment and boiler feed for power plants—was a brutal, low-margin business. Chinese buyers were price-sensitive, substitution was easy, and the big foreign players had infinite capacity. Trying to compete there would be corporate suicide. The interesting opportunity, they reasoned, was one step up the value chain: in what the industry calls "adsorbent" and "special resin" applications.

What does that mean in plain English? Think of ion exchange resins as microscopic sponges that can be tuned to grab specific molecules out of a liquid. A commodity resin grabs calcium and magnesium—that's water softening. A special resin grabs just one specific amino acid out of a fermentation broth, or just one specific rare earth element out of a mining tailing, or just one specific molecule of lithium from a brine that contains forty other competing ions. The difference between commodity and specialty, in this business, is like the difference between a paper towel and a pharmaceutical-grade filter membrane. The specialty market was smaller, but the margins were several times higher, and—critically—the foreign giants weren't paying attention.

The early wins came from unglamorous places that Western investors have probably never considered. Fruit juice. If you've ever wondered why your orange juice doesn't taste unbearably bitter, the answer is that a resin column stripped out the naringin and limonin compounds before bottling. Sunresin built an early business serving Chinese juice producers. From there, they expanded into sugar refining, pharmaceutical intermediates, and heavy metal recovery from electroplating wastewater. Each application required a slightly different resin chemistry. Each customer relationship was sticky, because once a factory was designed around a specific resin's performance curve, switching meant requalifying the entire production process.

By the late 2000s, Sunresin had become a respected mid-sized player in a niche corner of the chemicals world. But it was still, in essence, a boutique. The founders knew they needed capital—both for R&D and for the kind of industrial-scale manufacturing that would let them leap from "respected domestic supplier" to "global player."

That capital arrived in December 2015, when Sunresin listed on the Shenzhen ChiNext board. The ChiNext was China's answer to the NASDAQ, the designated venue for innovation-focused smaller companies, and it was an appropriate home. The IPO was unglamorous by mainland standards—no fireworks, no CCTV specials, no celebrity endorsements. The proceeds were modest. But the listing did three things that would prove transformative. It gave Sunresin a publicly traded currency to attract and retain technical talent through equity compensation. It imposed the discipline of quarterly disclosure, which forced cleaner internal management systems. And it put the company on the radar of a small group of Chinese institutional investors who specialized in the "hidden champions" of the industrial base.

Within a few years, one of those hidden champions was about to discover a new element: lithium.

III. Inflection Point 1: The Lithium Revolution and DLE

To understand what Sunresin did in the mid-2010s, you have to understand how absurdly primitive the lithium industry was at the time. Imagine you told a chemical engineer in 2015 that the world's most important battery metal was being produced using a process pioneered in the 19th century for harvesting sea salt. They would laugh, assume you were joking, and then look at the data and stop laughing.

The process worked like this. In places like the Salar de Atacama in Chile, or the Salar de Uyuni in Bolivia, or the Qarhan Lake in Qinghai, vast underground reservoirs of brine sit beneath salt crusts. The brine contains lithium—usually at concentrations between 200 and 2,000 parts per million—alongside massive amounts of sodium, potassium, magnesium, calcium, and boron. To recover the lithium, producers pumped the brine into giant evaporation ponds, sometimes square kilometers in area, and let the desert sun do the work. Over 12 to 24 months, water evaporated, salts precipitated in sequence, and eventually a concentrated lithium solution remained that could be processed into battery-grade lithium carbonate.

The problems with this approach were legion. Recovery rates were often below 50%, meaning half your lithium was lost to co-precipitation or seepage. The lead time was measured in years, which made it impossible to respond quickly to price signals. It required enormous amounts of land, which was a problem in ecologically sensitive deserts and a dealbreaker in any brine deposit where the magnesium-to-lithium ratio was too high. And China's own salt lakes—the ones in Qinghai and Tibet—had notoriously high magnesium content, meaning the evaporation process essentially didn't work for them at commercially viable grades.

Direct Lithium Extraction, or DLE, was the theoretical answer to all of this. The idea was elegant. Instead of letting the sun do the work over years, you pumped the brine through a column packed with a selective adsorbent—a special resin, in other words—that grabbed lithium ions while letting everything else pass through. Then you rinsed the column with fresh water, releasing the lithium in concentrated form. Total cycle time: hours, not months. Recovery rate: potentially 80% or higher. Land footprint: tiny. And it could work on high-magnesium brines that were simply uneconomic for pond evaporation.

The catch was that in 2015, nobody had a DLE resin that actually worked at industrial scale. Researchers had proposed manganese oxide and aluminum-based selective adsorbents for decades, but making them durable enough to survive thousands of adsorption-desorption cycles in a real industrial column was a materials science problem of staggering difficulty. The resin had to be selective for lithium against magnesium and sodium at ratios sometimes exceeding 1,000 to 1. It had to not dissolve or degrade when contacted with concentrated brines. It had to work at the extreme pH levels that Chinese salt lakes threw at it. And it had to be producible at tons-per-month scale, not grams-per-week.

Sunresin's engineers cracked this problem in stages through the mid-2010s, in close collaboration with Chinese salt lake producers like Qinghai Lanke Lithium and a handful of state-owned resource companies. The specific chemistry remains partially undisclosed in its filings—Sunresin treats its adsorbent formulations as trade secrets—but the resulting product line, which the company markets under its own adsorbent brand, became the dominant DLE chemistry in Chinese salt lake deployments. By the late 2010s, Sunresin was not just supplying adsorbent. It was engineering, installing, and commissioning entire DLE plants.

This was the pivotal strategic shift, and it's worth dwelling on because it changed the company's identity. Before DLE, Sunresin sold bags of resin. The economics were attractive—specialty resins can carry gross margins of 40% or higher—but the revenue per customer was capped at the size of their resin replacement cycle. After DLE, Sunresin sold complete lithium extraction systems. Engineering, Procurement, and Construction—or EPC, in industry parlance—contracts ran into the hundreds of millions of renminbi each. A single Qinghai plant could anchor Sunresin's revenue for an entire year.

By the early 2020s, roughly a quarter of Sunresin's revenue came from system equipment and EPC work, with the adsorbent resin itself accounting for the bulk of the remainder. More importantly, each EPC deployment created a captive aftermarket: as the adsorbent wore out over its multi-year lifespan, only Sunresin could supply the replacement chemistry. The installed base became a compounding annuity.

Industry observers sometimes describe this transition as moving from being a component vendor to being a platform. That's not quite right. Sunresin became something more subtle—an integrated solution provider whose core intellectual property sat in the molecular design of the resin, but whose commercial moat sat in the engineering integration around it. When a Chinese salt lake developer called Sunresin, they weren't calling a chemical company. They were calling the only firm in the world that could turn a mineral-rich lake into a battery-grade lithium plant in under two years.

The lithium price boom of 2021 and 2022—when spot prices briefly exceeded $80,000 per ton of lithium carbonate—turned Sunresin's DLE pipeline from a promising line of business into a torrent of cash. The question that management faced was what to do with it.

IV. Management and Governance: The Gao Yuejing Era

Spend any time in Chinese industrial circles and you'll hear a particular kind of respect reserved for the scientist-founders. These are people who trained in technical disciplines during the 1980s and 1990s, who often started their careers inside state-affiliated research institutes, and who built their companies not because they wanted to be rich but because they believed a specific piece of chemistry or physics could change their country's industrial destiny. Ren Zhengfei at Huawei is the archetype. Gao Yuejing at Sunresin belongs unmistakably to the same tradition.

She is, by all available accounts, a reserved figure. She rarely gives interviews to the mainstream financial press. She does not cultivate a celebrity persona on Weibo or WeChat. Company filings describe her as the founder, chairwoman, and—along with her husband An Xiaoning and their coordinated family holdings—the controlling shareholder. Her ownership stake, held directly and through affiliated entities, has hovered in the 20 to 25% range for most of the post-IPO period, giving her clear voting control without the kind of pyramidal structure that invites governance concerns.

An Xiaoning, her husband, serves as CEO and chief operator. The division of responsibilities between them is the kind of arrangement that works beautifully when the founders are aligned and catastrophically when they're not. At Sunresin, it has worked. Gao sets the technical and strategic direction; An runs the factories, manages the customer relationships, and translates research breakthroughs into scaled production. Both are technically trained. Neither came up through marketing or finance. When they discuss the business in investor communications, they discuss it in the vocabulary of chemistry and process engineering, not the vocabulary of EBITDA bridges.

This matters for investors because it shapes capital allocation in a specific way. Management teams with technical backgrounds tend to reinvest aggressively in R&D during good times, and they tend to tolerate lower short-term margins if they believe a new application is opening up. Finance-trained managers, by contrast, tend to optimize the existing business and return capital when growth slows. Sunresin's pattern of reinvestment—plowing enormous shares of the 2021-2022 lithium windfall into biopharma-grade chromatography facilities, European R&D centers, and a new generation of adsorbents for uranium and rare earth extraction—is unmistakably the pattern of founders who see themselves as stewards of a technology platform rather than operators of a single product line.

The governance structure reflects this philosophy. In 2022 and again in 2023, the company rolled out multi-year employee stock ownership plans that tied vesting to specific R&D milestones and segment revenue targets. The structure was notable in two respects. First, the performance conditions were concrete rather than vague—vesting required hitting disclosed revenue figures in specific segments by specific years, not a fuzzy "sustained growth" criterion. Second, eligibility extended deeply into the technical staff, not just the senior executive ranks. This is an incentive design that says: we want the chemists who develop the next adsorbent to share in the upside, because those chemists are the ones who will determine whether we're a $10 billion company or a $100 billion company a decade from now.

Culturally, the word management uses repeatedly is "technological sovereignty"—a phrase that resonates in contemporary China far beyond Sunresin but has particular meaning here. In the adsorbent resin business, the traditional global leaders—Dow, Lanxess, DuPont, Mitsubishi Chemical, Purolite—dominated the upstream chemistry and licensed downstream applications to customers. Sunresin has insisted on owning the full stack. They design the polymer backbone, synthesize the functional groups, fabricate the beads, design the extraction columns, engineer the process flow diagrams, commission the plants, and service the installed base. At each stage, they refuse to license from outsiders. This is expensive in the short run and liberating in the long run.

The liberation became particularly valuable as geopolitical tensions between China and the West escalated through the mid-2020s. When a Chinese lithium developer or a Chinese biopharma firm worried about supply chain security, Sunresin could credibly offer a fully domestic stack. When a Southeast Asian or Latin American customer worried about being caught in a trade war, Sunresin could offer a non-Western supplier with global engineering experience. Technological sovereignty, it turned out, was not just a slogan. It was a market positioning strategy.

For fundamental investors, the human element here is what differentiates Sunresin from many of its mainland peers. You are not betting on a financial engineer. You are betting on a chemist who happens to run a public company, backed by a husband-partner who runs the factories, surrounded by technical staff whose equity vests when they deliver new molecules. That alignment doesn't guarantee outcomes, but it shapes them.

V. M&A and Capital Deployment: The Benchmarking

Here is a trivia question that should tell you something important about Sunresin's capital allocation philosophy. How many acquisitions larger than $100 million has the company made in the last decade? The answer, as of early 2026, is zero.

This is a surprising answer for a company that has generated enormous cash flows during the lithium boom, trades at an elevated price-to-earnings multiple, and operates in an industry where bolt-on acquisitions are a standard growth path. Most Chinese specialty chemicals companies of Sunresin's size have at least one major acquisition in their history—usually a poorly-integrated purchase of a stressed European or American competitor at a knockdown price. Sunresin has resisted this pattern, and the resistance is strategic.

The company's M&A playbook, such as it is, has focused on two things. First, small acquisitions of technical teams and niche technology—acqui-hires, essentially, where the target's product line is less important than the engineering capability that comes with it. Second, greenfield investments in international R&D presence, where Sunresin has set up facilities in Europe, particularly with R&D activity in Belgium and Italy oriented toward biopharma and advanced separation applications. These moves are more about planting flags and hiring talent than about buying revenue.

The contrast with global peers is instructive. Lanxess, the German specialty chemicals group that inherited Bayer's ion exchange business, has grown significantly through acquisition, including high-profile deals that consolidated the European resin market. DuPont's water solutions business similarly grew by rolling up smaller regional players. These strategies created scale quickly, but they also created integration headaches, cultural clashes between acquired teams, and the classic conglomerate problem of allocating R&D dollars across disparate product lines that no single manager truly understood.

Sunresin has chosen the slower path. When they want a new capability, they would rather spend five years hiring chemists and building pilot lines than buying a competitor. When they want international presence, they would rather open a small office in Antwerp or Milan than acquire a mid-sized European firm. The philosophical justification is that adsorbent chemistry is deeply integrated—the choice of polymer matrix, functional group, bead morphology, and production process all interact in ways that are hard to replicate if you're starting from someone else's legacy design. Acquiring a competitor means acquiring their chemistry legacy, and Sunresin management has consistently judged that legacy to be more of a liability than an asset.

Whether this is wisdom or hubris depends partly on what you believe about the future of the industry. If separation science is commoditizing, Sunresin should be consolidating aggressively to maintain scale advantages. If separation science is becoming more specialized and application-specific, Sunresin's bet on organic growth and proprietary development makes sense. The evidence in the biopharma segment, which we'll come to, suggests the specialization thesis is winning.

On the question of valuation and whether Sunresin has "overpaid" for its growth, the honest answer is that there's nothing to overpay for when you're not acquiring. Organic capital expenditure has been the dominant use of cash. Historical PE multiples in the 30 to 50 range reflected market expectations for continued high growth in DLE deployments and, increasingly, for the optionality value of the biopharma platform. These are not multiples that would let you make accretive acquisitions of peers trading at similar multiples. They are, however, multiples that allow management to reinvest retained earnings at attractive internal rates of return, assuming the underlying investments actually perform.

The capex efficiency question is where the real story gets interesting. During the peak of the lithium cycle, when cash was pouring in from DLE deployments and adsorbent sales to hungry salt lake developers, management made a choice that looks in retrospect like the most important strategic decision of the decade. They did not pay a large special dividend. They did not buy back stock aggressively. They did not chase the kind of headline-grabbing acquisition that would have generated investor applause. Instead, they built out capacity in biopharma chromatography resins.

Biopharma chromatography is a different business from industrial adsorption, technically and commercially. It requires higher purity tolerances, more rigorous quality systems, and customer qualification cycles that can last years. It also carries structurally higher margins and massively higher customer switching costs. By the time the lithium cycle turned—as all commodity cycles eventually do—Sunresin had put the capacity in place to ride the next wave without depending on the mood of the lithium market.

VI. Hidden Gems: Biopharma and Life Sciences

If you had asked a Chinese equity analyst in 2022 what Sunresin did, the answer would have been some variation of "lithium extraction." The DLE story was so dominant, so exciting, and so directly connected to the electric vehicle megatrend that it crowded out everything else in the investor narrative. The company's biopharma and life sciences segment, which was still a modest contributor to revenue, barely showed up in sell-side models.

That was a mistake, and it's a mistake that fundamental investors who have done the work on this company have been exploiting ever since.

Inside a pharmaceutical manufacturing plant, the single most expensive and most scrutinized piece of equipment is often the chromatography column. Chromatography is the process by which a drug's active pharmaceutical ingredient—its API—is separated from the soup of impurities, byproducts, and unreacted starting materials that come out of a fermentation tank or a chemical synthesis reactor. Without effective chromatography, you don't have a drug. You have a contaminated slurry that will never pass FDA inspection.

The workhorse of chromatography is resin. Not wildly different, at the level of basic chemistry, from the industrial resins Sunresin sells to lithium miners—but produced to radically higher purity and quality specifications, functionalized with different ligands for different biomolecules, and integrated into regulatory filings that make switching suppliers an eighteen-month affair.

Consider what's happening in pharma right now. GLP-1 drugs—the class that includes Ozempic, Wegovy, and Mounjaro—have become the fastest-growing category of prescription medication in modern history. These drugs are peptides, which means they're synthesized through processes that require multiple chromatographic purification steps. Every kilogram of GLP-1 API that leaves a manufacturing plant has passed through tons of chromatography resin. The global production demand for these drugs is measured in hundreds of tons of API per year and rising, which translates into an enormous and growing demand for purification-grade resin.

Insulin, monoclonal antibodies, vaccines, and the emerging category of peptide therapeutics all rely on similar purification workflows. The global biopharma resin market has historically been dominated by a small number of Western specialists—Cytiva, Tosoh, Bio-Rad, Purolite, Repligen—who built their businesses over decades by embedding their resins into FDA-approved manufacturing processes. Once a drug was approved with a specific resin in its filing, the switching costs became close to prohibitive. Changing resin required requalification, regulatory notification, and potentially new clinical bridging studies. Nobody switches unless forced to.

Sunresin's entry into this market has followed the logic that also drove its industrial adsorbent strategy: focus on the applications where Western incumbents are slow, expensive, or supply-constrained, and where Chinese biopharma demand is growing fastest. The domestic Chinese pharma industry has exploded over the past decade, driven by both the country's aging demographics and its rapidly expanding drug development ecosystem. Chinese contract manufacturers producing APIs for export markets have been eager to qualify non-Western suppliers, both for cost reasons and for supply chain resilience. And the sheer volume of peptide and protein drug production migrating to Chinese facilities has created a greenfield opportunity for a domestic chromatography resin supplier.

Sunresin has ridden this opportunity with segment growth rates that have been the most attractive in the company. While the specific year-over-year figures vary by reporting period, management commentary and filings have repeatedly highlighted life sciences as the fastest-growing segment, with margins meaningfully above the corporate average. The segment is still smaller than adsorbent materials in absolute terms, but the growth trajectory and margin profile make it arguably more valuable on a per-renminbi-of-revenue basis than the company's bread-and-butter business.

The razor-and-blade dynamic is what makes this so interesting. When a Chinese biopharma customer qualifies a Sunresin chromatography resin into an FDA filing—or the Chinese NMPA equivalent—Sunresin becomes embedded in the production process for the life of that drug. Given that modern biologics often have commercial lifecycles of fifteen to twenty years, a single successful qualification can produce recurring resin revenue for decades. The initial sale is small. The aftermarket is enormous. And because the customer has no reason to switch, the pricing power compounds over time.

The question for fundamental investors is not whether biopharma will become an important contributor to Sunresin's business. That's already happening. The question is how large it can ultimately become, and whether the company can successfully navigate the qualification cycles at major Western biopharma customers. The latter challenge is the real test. A Chinese chromatography resin supplier has never before been a tier-one provider to a major Western pharma company. Sunresin's push into European R&D presence and its quiet efforts to position itself as a credible alternative to the Western incumbents suggests management believes this is possible. The investment case, in part, is a bet that they're right.

VII. The 7 Powers and Porter's 5 Forces

Let's put Sunresin on the analytical dissection table and look at what makes the business genuinely defensible, as opposed to merely well-run. Hamilton Helmer's 7 Powers framework is a good place to start, because it forces a distinction between operational excellence (which can be copied) and structural advantages (which cannot).

Switching Costs. This is the primary power in Sunresin's business, and it shows up twice—once in DLE and once in biopharma—through structurally different mechanisms. In DLE deployments, switching costs come from plant integration. When Sunresin delivers an EPC project to a Chinese salt lake operator, the extraction towers, flow rates, regeneration cycles, and process control systems are all designed around a specific adsorbent chemistry. Replacing that adsorbent with a competitor's product would require redesigning significant portions of the plant, requalifying the output stream, and accepting months of downtime. For a lithium producer selling into a volatile spot market, that downtime risk alone is enough to keep them paying Sunresin's prices for the replacement resin. In biopharma, switching costs come from regulatory lock-in. Once a resin is filed with a drug approval, changing it is a multi-year regulatory event. The two mechanisms are different, but they produce the same economic outcome: customers who, once acquired, essentially cannot leave.

Cornered Resource. Sunresin's proprietary adsorbent formulations, refined through years of iteration on specific brine compositions and biomolecule targets, constitute a genuine cornered resource. These are not formulations that appear in public literature. They are not available through licensing. They were developed by Sunresin's chemists through an accumulation of thousands of experimental iterations, and the institutional knowledge of why certain formulations work on certain brines is held within the company's technical staff. Reverse engineering is difficult because the final bead is a composite of polymer chemistry, functional group placement, porosity structure, and surface modification—each of which can be measured, but whose interactions are not easily replicated. Competitors who have tried to copy Sunresin's DLE adsorbents have generally produced something that works in a laboratory but fails in the harsh chemistry of a real salt lake.

Scale Economies. Scale in this business is not about manufacturing cost—resin plants are actually fairly capital-light and can be replicated by anyone with the capital. Scale is about data and engineering experience. Sunresin has deployed DLE systems on more types of brine, with more varied impurity profiles, under more operating conditions, than any other adsorbent supplier on the planet. Every deployment generated process knowledge that makes the next deployment faster, cheaper, and more reliable. A new entrant would need to accumulate years of field experience before they could credibly compete on the engineering confidence that Sunresin offers to customers. This is a durable advantage, but it's also a time-based one—the gap will shrink as competitors gain their own experience, which is why management has kept moving into new applications where their experience moat can be refreshed.

Process Power. There's an argument that Sunresin also benefits from process power in the Helmer sense—a complex, coordinated organizational capability that cannot be easily isolated and copied. The integration between the chemistry team, the process engineering team, and the field commissioning team has been refined over two decades, and it shows up in deployment timelines that competitors have struggled to match. This is the kind of advantage that Toyota had with its production system—visible to everyone, imitable by almost no one.

Now let's look at Porter's Five Forces.

Bargaining Power of Buyers. On paper, this should be high. Lithium producers are concentrated, sophisticated, and well-capitalized. A Tianqi, a Ganfeng, or a Qinghai Lanke has every reason to play adsorbent suppliers against each other. In practice, Sunresin has mitigated this power by bundling the adsorbent with the full engineering solution. When you're not buying resin but rather buying a lithium extraction plant that happens to contain resin, the negotiation shifts from a commodity haggle to a capability assessment. The question becomes not "whose resin is cheapest" but "whose plant will actually deliver the throughput and recovery we modeled." That's a question where Sunresin's track record becomes the answer.

Threat of New Entrants. Modest in the short run, meaningful in the long run. New Chinese specialty chemical players do enter the adsorbent market periodically, typically backed by state investment and armed with licensed or reverse-engineered chemistry. Most have failed to achieve commercial-scale DLE performance. A few have succeeded in niche applications. The bigger threat is from adjacent Western incumbents—Lanxess, Purolite, DuPont—who have tried to enter DLE but have been slower to commercialize at Chinese salt lake conditions.

Threat of Substitutes. This is the most uncertain force. Membrane-based lithium extraction technologies have been developed in parallel with adsorbent DLE, and various players in North America and Europe have promoted them as superior alternatives. In practice, membranes have faced their own fouling and selectivity problems in high-magnesium brines. Resin-based DLE remains, as of 2026, the workhorse of commercial deployments. But the materials science race is ongoing, and a breakthrough in membranes or in some entirely new extraction chemistry could erode Sunresin's moat in lithium over a ten-year horizon. Biopharma, by contrast, has no credible substitute on the horizon. Chromatography resins have been the workhorse of biologic purification for forty years, and the physical principles that make them work are unlikely to be displaced.

Bargaining Power of Suppliers. Low. The raw materials for polymer resins are commodity chemicals, widely available from multiple suppliers.

Rivalry Among Competitors. Moderate. The global specialty resin market has a handful of serious players, but it is not a hyper-competitive commodity fight. Most players specialize in particular applications and geographies, and direct head-to-head competition is less common than in, say, basic chemicals.

The net assessment is that Sunresin sits in a structurally attractive competitive position, particularly in biopharma, with meaningful but erodible advantages in lithium. That profile is consistent with the elevated multiple the market has historically accorded the stock.

VIII. The Bear vs. Bull Case

The bear case on Sunresin begins with geopolitics and ends with cyclicality, with some accounting nuance along the way.

Geopolitical Risk. The most significant non-operational risk facing Sunresin is the possibility that Western jurisdictions restrict Chinese suppliers from participating in critical minerals and pharmaceutical supply chains. The Inflation Reduction Act in the United States, the Critical Raw Materials Act in the European Union, and various security reviews in Canada and Australia have all trended toward greater scrutiny of Chinese involvement in lithium, battery materials, and sensitive biopharma supply. If Sunresin's addressable market in North America and parts of Europe becomes effectively closed, the international growth story becomes materially harder. Management's response has been to lean into markets where this is less of a concern—South America, the Middle East, Central Asia, and domestic China—and to build European R&D presence partly as a hedge. But this is a headwind that no amount of good execution can fully neutralize.

Lithium Cyclicality. The lithium market is volatile. Spot prices moved from below $7,000 per ton in 2020 to above $80,000 per ton at the 2022 peak and then back down substantially in the ensuing years. Sunresin's new EPC projects tend to correlate with lithium capex spending, which itself correlates with the price cycle. When prices crash, salt lake operators defer projects, which hits Sunresin's forward pipeline. The company has historically been reasonably insulated by the installed base of adsorbent replacement revenue, but new project revenue is procyclical.

Customer Concentration in EPC. Any given year's EPC revenue can be dominated by a small number of large projects. This concentration creates lumpiness in reported results and introduces meaningful execution risk—a single troubled project can weigh heavily on segment margins and investor sentiment.

Valuation. The stock has frequently traded at price-to-earnings multiples in the 30 to 50 range, reflecting market expectations for continued high growth. At those multiples, there is little margin for disappointment. An EPS miss driven by a single delayed Qinghai project can trigger outsized stock price reactions.

Accounting Considerations. In project-based businesses that recognize revenue over time or at commissioning milestones, there is inherent management judgment about project progress and cost-to-complete estimates. No specific restatements have been disclosed at Sunresin that would raise immediate red flags, but investors should pay attention to any shifts in revenue recognition policy or unusual patterns in unbilled receivables.

Now the bull case.

Biopharma Optionality. The base case in the bull story is that life sciences grows from its current modest share of revenue to something much larger, with margins that meaningfully exceed the corporate average. If Sunresin becomes a credible tier-one chromatography resin supplier for Chinese biopharma production—which already appears to be happening—the business mix shifts toward higher-quality, recurring, less cyclical revenue. If, additionally, they manage to win qualification at one or two major Western biopharma customers, the addressable market expands dramatically.

DLE Platform Extensibility. The same underlying capability that extracts lithium from brine can, in principle, be applied to other separations of strategic importance. Uranium from seawater. Rare earth elements from mining tailings. Valuable metals from battery recycling streams. Each of these represents a potential major new application for Sunresin's adsorbent platform. Management has commented on several of these opportunities in various filings and investor communications, though commercialization timelines remain uncertain.

International Moat. Outside of North America, where geopolitical risk is most acute, Sunresin's competitive position is arguably stronger than any Western peer. They have demonstrated engineering at Chinese salt lakes that no Western firm can match, and they are increasingly the first-call supplier for South American and Central Asian lithium projects. As the global lithium supply chain decentralizes over the coming decade, Sunresin's international footprint becomes more valuable.

Compounder Masquerading as Cyclical. The real bull case, the one that serious long-term holders tend to articulate, is that the market has misclassified this company. The market sees a Chinese specialty chemicals company with lumpy EPC revenue and cycles with lithium prices. The more accurate description is a multi-application separation platform with high customer switching costs, deepening R&D moats, and a rapidly growing biopharma annuity. If the second description is correct, the stock should trade at compounder multiples—consistently high, justified by structural growth and return on invested capital—rather than getting re-rated down during lithium troughs.

For fundamental investors, the question is not whether this company has a moat. It clearly does. The question is whether the combination of moat breadth, reinvestment opportunities, and management quality justifies the multiple at which the stock trades at any given moment. On that question, the answer depends on assumptions about biopharma growth, international expansion, and the pace of lithium demand recovery.

The KPIs that actually matter for tracking this story going forward are narrower than the typical analyst dashboard suggests. First, life sciences segment revenue growth rate—because that's the canary in the coal mine for whether the compounder thesis is working. Second, the rate of DLE installed base expansion measured by total deployed adsorbent capacity, because that drives the long-term annuity of replacement resin revenue. Third, international revenue mix, because that reflects geopolitical derisking and market expansion. Everything else—quarterly margins, working capital swings, individual project timing—is noise around these three signals.

IX. Conclusion and Playbook Lessons

Walk through the story of Sunresin and a few patterns emerge that apply well beyond the specific facts of this one Chinese specialty chemicals company.

The first pattern is about where to compete. Gao Yuejing and An Xiaoning looked at the ion exchange resin market in the early 2000s and made a decision that seems obvious in retrospect but was radical at the time. They refused to compete in the commodity water treatment segment where they would have faced established global competitors on price, and they focused instead on specialty applications where their technical knowledge could generate disproportionate margins. Twenty-five years later, that decision looks less like a shrewd market positioning and more like the fundamental identity of the company. The commodity business would have been a grind. The specialty business became a platform.

This is the first playbook lesson. When you're a small company facing large incumbents, do not compete where the incumbents are strongest. Find the niches they consider beneath them, where your technical depth compounds faster than their scale advantages, and use those niches to build the cash flow that eventually funds your assault on larger markets.

The second pattern is about the evolution from product to solution. When Sunresin was selling bags of adsorbent to juice factories, they were a supplier. When they started selling complete lithium extraction plants with the adsorbent inside, they became a strategic partner. The economics of these two business models are fundamentally different. A supplier is replaceable; a strategic partner is embedded. The margins on solution selling are higher, the customer relationships are longer, and the moat is stickier.

The second playbook lesson is that whenever possible, you should be selling the outcome rather than the component. If you can wrap your product in the engineering expertise, the service, the integration, and the ongoing support that turns a commodity purchase into a capability purchase, you change the nature of the relationship entirely. This is why Sunresin's DLE EPC business is more interesting than its bulk adsorbent business, and it's why the biopharma chromatography business—where a resin sale is really a sale of future-proof purification capability—is more interesting still.

The third pattern is about reinvestment at the peak. The 2021 and 2022 lithium boom would have been an excellent time for Sunresin to maximize dividends, run up the stock with buybacks, or chase headline-grabbing acquisitions. Instead, management used that windfall to build out biopharma capacity, European R&D presence, and a pipeline of new adsorbent applications. The easy decision would have been to celebrate the lithium cycle. The harder and more valuable decision was to treat the windfall as seed capital for the next phase of the company.

Which brings us, finally, to the question with which we started. Is Sunresin the most important company in the EV supply chain that no one has heard of?

The honest answer is that within industrial circles, people have heard of them. Every serious lithium developer knows the name. Every Chinese biopharma quality engineer evaluating chromatography resins knows the name. The specialist funds that focus on Asian industrial hidden champions certainly know the name. But in the broader global investment community, where retail investors can quote the CEO of Tesla and know the supply agreements of CATL, Sunresin remains genuinely obscure. Their Shenzhen ChiNext listing, their limited English-language investor communications, and their refusal to cultivate a media presence have all contributed to a kind of strategic under-visibility.

There's a case that this under-visibility is itself an advantage. A company that becomes famous attracts competition, regulatory scrutiny, and political attention. A company that stays technical, stays in the background, and lets its customers be the public face of its work can build a moat that is hard to see and therefore hard to attack. Sunresin has executed this playbook with discipline for a quarter century.

Whether that discipline continues is the question that matters for the next decade. The biopharma bet will either pay off spectacularly or prove harder than expected. The international expansion will either open new markets or founder on geopolitical headwinds. The management succession—because Gao and An are not young anymore, and the transition to the next generation of leadership will eventually have to happen—will either preserve the technical culture or erode it.

For now, sitting in April 2026, what exists is a company that has quietly become the most important adsorbent resin specialist in the world's most important industrial economy, with a growing position in the world's fastest-growing biopharma markets, led by founders who act like stewards rather than operators. That combination does not guarantee future returns. But it is the kind of combination that fundamental investors tend to find worth paying attention to, long before it becomes conventional wisdom.

The alchemy of modern industry, it turns out, runs on tiny plastic beads made in Xi'an.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube