Sangfor Technologies: The Huawei Diaspora That Built China's VMware

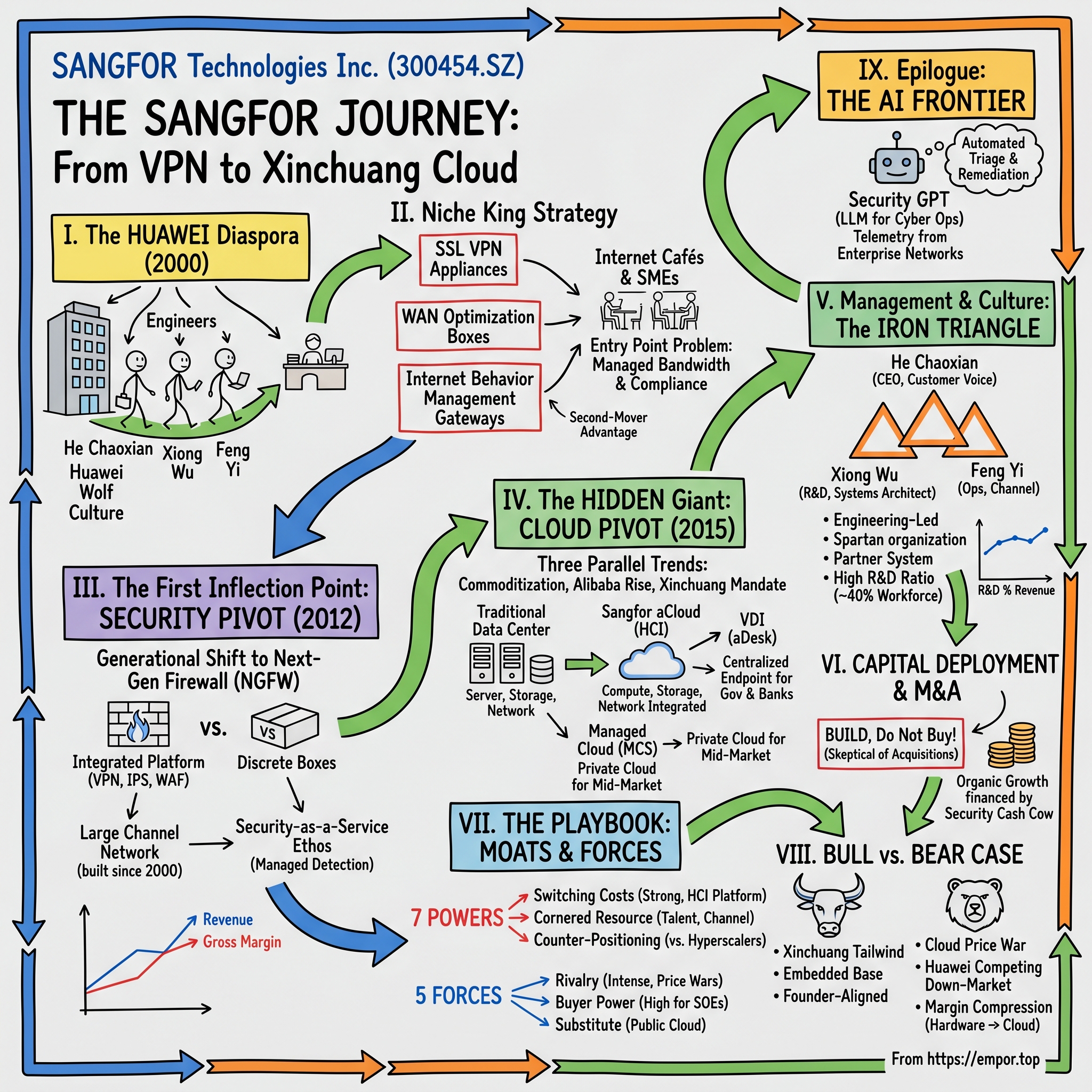

I. Introduction: The "Huawei Diaspora" (0:00 – 10:00)

Picture Shenzhen in the spring of 2000. The skyline is still half-finished, cranes outnumber finished towers, and along Shennan Boulevard the buses spit black diesel into the humid Guangdong air. Inside one nondescript office tower in the Nanshan district sits Huawei Technologies—already, by this point, the most feared company in Chinese telecommunications. Ren Zhengfei's "wolf culture" of relentless engineering and Spartan personal sacrifice had conquered the carrier-grade switching market in China and was beginning to claw at the heels of Cisco internationally. Working there meant 70-hour weeks, mattresses under desks, and the feeling that you were part of something close to a national mission.

And yet, in that very year, three young Huawei engineers walked out the door. They were not leaving in anger, and they were not leaving to build the next Huawei. He Chaoxian, Xiong Wu, and Feng Yi had spotted something quieter, less glamorous, and—as it would turn out—vastly more profitable than chasing telecom infrastructure. They had spotted the "entry point" problem.

China's small and medium-sized businesses were going online for the first time. Internet cafés were exploding across every Tier-2 and Tier-3 city. State-owned enterprises were just beginning to digitize their back-office workflows. But none of them had any idea how to manage the networks, secure the connections, or stretch the painfully expensive bandwidth that came in over the wires of the state-owned telcos. The big foreign players—Cisco, Check Point, F5—sold gear priced for Wall Street banks, not for a noodle restaurant in Chongqing wanting to install a point-of-sale system. Huawei itself was busy chasing carriers, not these smaller customers.

So the trio rented a small office, registered the entity as Shenzhen Sangfor Technology—the name a transliteration of "Sangfor," loosely meaning "harvest" and "fortune"—and got to work. They would spend the next eight years selling almost nothing the average tech investor had heard of: SSL VPN appliances, WAN optimization boxes, internet behavior management gateways. The kinds of products that show up as a 2U rack-mounted box humming somewhere in a wiring closet, not as a sticker on a laptop.

Here is the thesis of this episode. Sangfor Technologies, today listed on Shenzhen's ChiNext board under ticker 300454.SZ, is one of the most quietly important enterprise IT companies in China. It is the company that became the "Swiss Army Knife" of Chinese enterprise infrastructure—dominating network security in the SME and government segment, then pivoting in the mid-2010s into a hyper-converged cloud business that now competes with VMware, Nutanix, and even Alibaba Cloud inside its home market. It did this without ever achieving the brand recognition of its competitors, without burning capital on adventurous M&A, and without losing the original founders, all three of whom still run the place a quarter-century later.

The arc of this story runs from VPN boxes to hyper-converged infrastructure. From a company that sold caching appliances to internet cafés in 2003 to one that today sits on the privileged short-list of "trusted local vendors" the Chinese government wants installed when it rips out IBM mainframes, Dell servers, and VMware hypervisors as part of the Xinchuang—domestic substitution—mandate. Along the way, you get a clinic in second-mover strategy, in the power of a high-touch channel network, and in the underappreciated discipline of founders who would rather ship one more product than buy one more company.

This is also a story about a culture: the "Huawei diaspora," the wave of engineers who carried out into the broader Chinese tech ecosystem the rigor and hierarchy and customer-obsession of their alma mater, and built second-generation companies that, in many segments, the parent never bothered to dominate. Sangfor is arguably the cleanest example of that diaspora playing out at scale—a "Little Huawei" that grew up in the shadow, deliberately not picking the same fights, and arriving in 2026 with a market position the original Huawei would now find almost impossible to dislodge.

To understand how a small VPN startup became the backbone of digital sovereignty for an entire economy, we have to start where the founders did—in those Huawei cubicles, in a country that was about to plug in.

II. Founding & The Niche Strategy (10:00 – 25:00)

He Chaoxian was, by all accounts, the quiet one. A graduate of the University of Science and Technology of China, he had joined Huawei in the late 1990s and worked on data communications products. He was the kind of engineer who, colleagues later recalled, would write down every customer complaint by hand in a notebook and then refuse to leave the office until he had a working prototype to address it. Xiong Wu, the second of the trio, was the systems thinker—the one who could draw a network architecture on a whiteboard, step back, and immediately tell you which three components would fail under load. Feng Yi was the operations and sales mind, the one who understood that in China, technical superiority was nothing without a phalanx of channel partners willing to drive twelve hours into a county-level government office to install your gear.

That blend—deep engineering, systems intuition, and ground-game distribution—would become the Sangfor signature. But in 2000, none of it was obvious. What was obvious was that they did not want to compete with Huawei. The carrier infrastructure market was already a bloodbath. They wanted to find an adjacent space where Huawei's bureaucratic intensity would actually be a disadvantage. Enterprise networking, particularly for smaller firms, was that space.

Their first product, launched in 2000, was a content security and bandwidth management appliance. Imagine an internet café in 2002 with thirty PCs, all sharing a single 2-megabit DSL line. Without traffic shaping, three teenagers downloading films would saturate the pipe and crash the cybercafé's revenue model. Sangfor's appliance sat at the gateway, prioritized traffic, throttled file-sharing, and—crucially—logged everything for compliance with the Ministry of Public Security's increasingly vigilant rules around internet usage. It was a small, boring, beautiful product. And it sold.

By 2003, they had moved into SSL VPNs. This is one of those technologies that sounds dull but, in context, was an unlock. Chinese enterprises in the early 2000s were grappling with a basic problem: how do you let an employee in Shanghai securely access a database in the Shenzhen headquarters over a public internet that everyone, correctly, assumed was being snooped on? The international answer was an IPSec VPN, complex to deploy and configure. Sangfor's bet was on SSL VPN—simpler, browser-based, deployable by a customer with a single network admin and a cup of tea. By 2005, Sangfor had become the leading domestic SSL VPN vendor by units shipped, ahead of foreign incumbents like Juniper. Not because their crypto was better. Because their support team would actually drive to your office in Hefei when something broke.

The other early product line was WAN optimization—essentially, software that uses caching, deduplication, and protocol acceleration to make a slow connection feel fast. In a country where international bandwidth was rationed, where a Wuhan branch office might be on a half-megabit link to Beijing headquarters, this was magic. Sangfor's appliances could compress repetitive traffic by ratios that, to the customer, made the network feel three to five times faster without paying the telco a yuan more. They sold these into banking branches, government bureaus, and manufacturing facilities by the thousands.

This is the era of what insiders would later call "Niche King" Sangfor. The company never tried to take on Cisco's flagship core routers or Huawei's carrier switches. They picked five or six adjacent product categories—SSL VPN, WAN optimization, internet behavior management, application delivery controllers—and went deep in each. They were not the largest player in any single one outside their home segments. But they were the most reliable, the most affordable, and the easiest to support in the SME and lower-end enterprise market that the multinationals had effectively conceded.

Why did this work? Because the founders understood something foreign vendors did not. China in the 2000s was not a top-down market where Beijing's banks set the technology agenda for everyone else. It was a deeply fragmented, geographically dispersed market where the buyer was just as likely to be a local government IT director in Sichuan as a CIO in Pudong. Winning that market required a sales motion that a Cisco regional manager simply could not execute. It required hundreds of channel partners, a willingness to customize for each customer's quirks, and pricing that fit a procurement budget measured in tens of thousands of yuan, not millions.

By 2007, Sangfor had crossed RMB 200 million in revenue, almost entirely organic, almost entirely cash-generative. They had not raised meaningful outside capital. They had not gone international beyond a handful of opportunistic deals in Southeast Asia. They had simply found their niches and made them theirs. That patience—building a wide, dense, defensible base in unsexy categories—turned out to be the runway for everything that came next. Because the next move was about to take them out of the wiring closet and into the executive boardroom.

III. The First Inflection Point: The Security Pivot (25:00 – 45:00)

The conference room in Sangfor's Shenzhen headquarters in 2011 had a whiteboard, and on that whiteboard, sometime that year, He Chaoxian drew a simple two-by-two matrix. On one axis: hardware versus software. On the other: niche versus platform. The company was sitting comfortably in the "hardware-niche" quadrant. He pointed to the "hardware-platform" cell and said, in effect, that this was where they had to go next, or risk irrelevance.

The catalyst was a global one. Around 2009 to 2011, the entire enterprise security industry was undergoing a generational shift from "stateful firewalls"—the basic packet filters that had defined the previous decade—to what Palo Alto Networks had successfully marketed as the "Next-Generation Firewall," or NGFW. The NGFW promised to do far more than block ports. It would inspect application-layer traffic, detect intrusions, filter URLs, decrypt SSL, and integrate threat intelligence—all in a single appliance. The early winners in the United States were Palo Alto and Fortinet. In China, the early winners were domestic incumbents like Venustech and NSFOCUS, both of which had been founded in the late 1990s and had deep relationships with the central government.

Sangfor was, frankly, late. They did not ship their first true NGFW until 2012. By that point, Venustech had already been the official supplier for several Ministry of Public Security projects, and NSFOCUS had built a strong DDoS protection business on the back of major attacks on Chinese internet portals. If you were the CIO of an SOE in 2012 looking to buy a firewall, "Sangfor" was probably not the first name on your list.

So how did they win? This is where the second-mover playbook becomes visible. Sangfor did three things that, in retrospect, look obvious and at the time looked plodding.

First, they integrated. While the incumbents sold a firewall as a discrete box—and then a separate intrusion prevention system, and then a separate web application firewall, and then a separate VPN concentrator—Sangfor bundled all of those functions into a single appliance running a single management plane. For the customer, this collapsed the integration headache. One purchase order, one vendor support call, one console for the network engineer to learn. It was a softer version of the "platform" pitch that Palo Alto was making globally, adapted for a Chinese buyer who often did not have the staff to manage a multi-vendor security stack.

Second, they leaned into their channel. Sangfor's distributor network—built up patiently over the previous decade selling those VPN and WAN optimization boxes—was now the largest independent enterprise security channel in China. While Venustech and NSFOCUS focused on direct sales to top-tier government and financial accounts, Sangfor's partners were selling NGFWs into hospitals, universities, manufacturing plants, and city-level government bureaus by the thousand. By 2015, Sangfor had become the leading domestic NGFW vendor by shipment volume in the SME and mid-market segment, even as the headline-grabbing incumbents continued to dominate the largest accounts.

Third, and perhaps most importantly, they treated security as a service relationship long before the industry coined the term "Security-as-a-Service." Sangfor's appliances came with subscription-based threat intelligence updates. Their support engineers would proactively call customers when a new vulnerability was disclosed. They built early versions of what we would now call "managed detection and response" by simply having a team of analysts in Shenzhen who could remote into customer appliances and help triage incidents. None of this was unique to Sangfor; it was simply executed with an obsessive customer-success ethos that the more elite competitors did not bother with for mid-market accounts.

The financial result was transformative. Security gross margins in China were extraordinary—often 70% or higher on appliance hardware, with attached subscription revenue that compounded year after year. By 2015, Sangfor's network security business was generating the kind of cash flow that lets a company quietly fund its next major bet. And the next major bet was already being prototyped on a different floor of that Shenzhen office.

There is an old Sangfor anecdote, possibly apocryphal but instructive, about a customer in Wuhan who in 2013 told a Sangfor sales engineer that they were getting tired of buying a separate physical box every time they wanted a new function. Why couldn't all of this just be software, running on commodity servers, that they could spin up and tear down as needed? The sales engineer wrote it down—Sangfor culture, again, the notebook—and brought it back to Shenzhen. Within a year, an internal team had been chartered to figure out how Sangfor's hardware roadmap could be reborn as software. That team would eventually become the foundation of the cloud business.

The brilliance of the security pivot was not that Sangfor invented next-generation firewalls. They didn't. The brilliance was that they used the cash thrown off by a maturing security business to underwrite a bet on a category that, in 2014, almost no Chinese company had figured out yet. Hardware security was the cash cow. The cloud was the venture. And it was about to become a much bigger venture than anyone outside Sangfor's R&D building expected.

IV. The "Hidden" Giant: The Cloud Pivot (45:00 – 75:00)

By 2015, three things were happening in parallel that would reshape Sangfor's business for the next decade.

The first was a global commoditization of networking hardware. The white-box server revolution was migrating from the hyperscaler data centers of Google and Facebook into mainstream enterprise IT. Open-source hypervisors like KVM had reached production maturity. The economics of buying a custom-built proprietary appliance from a vendor like Cisco or—Sangfor itself—were being eroded by the option of running the same functions as software on a generic Intel server. Anyone running a hardware-only business model in 2015 could see the storm clouds.

The second was the meteoric rise of Alibaba Cloud, which had launched in 2009 and by 2015 was demonstrating that Chinese enterprises were prepared to put real workloads on a domestic public cloud. The implication for traditional enterprise IT vendors was stark: if companies started treating compute as a commodity rented from a hyperscaler, the entire on-premises infrastructure market would be slowly hollowed out from the top.

The third was a uniquely Chinese factor. Beginning around 2014 and accelerating after 2018, the Chinese government began articulating a policy initiative that would come to be known as Xinchuang, short for "xinxi jishu yingyong chuangxin"—roughly, "innovation in the application of information technology." The plain English translation: state-owned enterprises, government agencies, and critical infrastructure operators would, over the next decade, replace foreign IT systems with domestically produced alternatives. IBM mainframes out, Inspur and Sugon in. Oracle databases out, OceanBase and TiDB in. Microsoft Windows out, Kylin Linux in. And critically for Sangfor: VMware out, domestic hyper-converged infrastructure in.

Sangfor positioned itself, with quiet precision, at the intersection of all three trends. The product they bet the next decade on was hyper-converged infrastructure, or HCI. For the non-technical listener, here is the simplest analogy. In a traditional data center, you would have three separate pieces of equipment: a server for compute, a storage array for data, and a network switch for connectivity. Each came from a different vendor, ran different management software, and required a different specialist to operate. HCI collapses all three into a single software stack running on standard x86 servers. You buy a few identical "nodes," click them together, and instantly have a small data center that can run virtual machines, store data, and route traffic—all managed through one console.

This is the category that VMware effectively created with its vSAN and NSX products, and that Nutanix popularized as a pure-play HCI vendor in the United States. In China, by 2015, no domestic vendor had built a credible competitor. Sangfor entered the market with a product called aCloud—internally rebranded several times—that bundled their own hypervisor, software-defined storage, and software-defined networking on commodity hardware. They priced it aggressively below VMware. They sold it through the same channel partners who already trusted them on security. And they wrapped it in the kind of high-touch implementation services that Chinese enterprises, used to dealing with consultative IBM teams, expected.

The early traction was almost embarrassingly good. By 2018, Sangfor had become the leading domestic HCI vendor by market share in China, a position it has not relinquished. According to industry tracker IDC, in subsequent years Sangfor frequently ranked first or second in HCI software revenue in the mainland China market, ahead of both VMware and the local cloud divisions of Huawei and H3C. For a company that had been a pure security vendor five years earlier, this was a remarkable land grab.

Alongside HCI, Sangfor built a parallel virtual desktop infrastructure business—aDesk—which offered a domestic alternative to Citrix and VMware Horizon. VDI in China had a specific use case that played perfectly to Sangfor's strengths. Government agencies, banks, and schools wanted to centralize their endpoint computing for security and compliance reasons; they did not want sensitive data sitting on a thousand laptops in a thousand branch offices. Sangfor's VDI product let them deliver Windows desktops from a central data center, with all the security policies—encryption, audit logging, compartmentalization—built into the same stack the customer was already buying for HCI. By the early 2020s, Sangfor's VDI business was, by some measures, the largest in China.

And then there is the genuinely "hidden" piece of the cloud business: Managed Cloud, marketed under the brand "Managed Cloud Services" or MCS. This is essentially a private-cloud-as-a-service offering. Sangfor builds and operates regional data centers across China and offers customers, particularly mid-market enterprises and second-tier SOEs, a managed compute and storage service that is dedicated, isolated, and compliant with industry-specific data residency rules. It is not a public cloud in the Alibaba or Tencent sense. It is closer to what AWS calls "Outposts" or what European players like OVHcloud sell as "private hosted cloud." For a Chinese mid-market customer that wants the elasticity of cloud but does not trust putting sensitive data on a public hyperscaler, MCS has been an extraordinarily compelling offer. It is also, importantly, a recurring revenue business with much stickier economics than appliance sales.

The headline numbers behind the cloud pivot are worth pausing on. Sangfor's revenue mix has, over the past five years, shifted decisively. Network security, historically the dominant business, has settled into the role of mature, high-margin cash generator, accounting for somewhere around 55% of total revenue in recent years. Cloud computing—HCI plus VDI plus MCS—has grown to roughly 35% and continues to gain share within the mix, with its segment growth rates routinely outpacing security by a wide margin. The remainder, around 10%, comes from base infrastructure products like the original WAN optimization and internet behavior management lines, which Sangfor has kept alive as legacy cash producers.

What makes the cloud business so strategically interesting is the Xinchuang tailwind. Every time a provincial government or a state-owned bank decides to migrate off VMware, they are not just buying a hypervisor. They are buying a five-to-ten-year relationship that includes hardware refreshes, software upgrades, professional services, and deep operational integration. Sangfor, more than perhaps any other Chinese vendor, has positioned itself as the natural drop-in replacement for the foreign hypervisor stacks that dominated Chinese enterprises through the 2010s. The total addressable market is, by industry estimates, tens of billions of dollars over the coming decade, and Sangfor is one of the small handful of vendors with a credible product, channel, and reference list to capture meaningful share.

This is why Sangfor in 2026 is something quite different from the SSL VPN startup of 2003. It is, in revenue terms, still around half a security company. But in growth terms, it is increasingly a cloud infrastructure company. And the cloud business is where the next decade of value creation, according to most analysts following the name, will be made or unmade. The security cash cow funded the venture. Now the venture is on the verge of becoming the bigger business. And to understand how a company executes a transition this large without flying apart, we have to look at the people who, twenty-six years after founding it, are still in the building.

V. Management & Culture: The Iron Triangle (75:00 – 95:00)

There is a peculiar feature of Chinese tech companies in the mid-2020s that Western observers consistently underrate: the founders are leaving. Jack Ma stepped back from Alibaba years ago. Pony Ma at Tencent has steadily reduced his public profile. Liu Qiangdong at JD.com has cycled in and out of operational roles. Robin Li still chairs Baidu but the day-to-day is increasingly handled by a rotating cast of professionals. Even Ren Zhengfei at Huawei, while still revered, runs the company through a rotating CEO model that has institutionalized his absence as much as his presence.

Against that backdrop, the persistence of the Sangfor founding trio is genuinely unusual. He Chaoxian remains chairman and CEO. Xiong Wu and Feng Yi continue in senior roles overseeing R&D and operations. The three of them, together with their family holdings, control roughly 40% of the listed company—an unusually concentrated and stable ownership structure for a mainland-listed enterprise tech firm. They have not signaled retirement. They have not promoted a "professional CEO" to the top job. They run the company today the way they ran it in 2003: as an engineering-led, customer-obsessed, deliberately Spartan organization headquartered in Shenzhen.

He Chaoxian himself is not a public personality in the way Jack Ma or Lei Jun are. He gives few media interviews. He does not livestream on Douyin. He does not appear at Davos. The image that Sangfor employees and longtime customers describe is of a chairman who still walks the R&D floor, still personally reviews major product roadmaps, and still—per the original notebook discipline—keeps a running list of customer complaints that he expects engineering leaders to address by the next quarter. He is not, by any account, a charismatic leader in the Western mold. He is a builder, and the company has been built in his image.

Xiong Wu, who serves as a co-founder and senior executive on the technology side, is the architect figure. Internal lore credits him with the architectural decisions that allowed Sangfor's product portfolio to converge over time onto a unified software platform—the engineering choice that, more than any single product launch, made the cloud pivot possible. Where He Chaoxian is the customer voice, Xiong Wu is the systems voice.

Feng Yi has historically led the operations and channel side, the part of the business that, in many enterprise tech companies, is treated as a second-class citizen relative to engineering. At Sangfor, the channel organization is a first-class citizen. Distributor partners speak about Feng Yi the way Salesforce partners used to speak about Marc Benioff—as someone who genuinely understood that the channel was not a cost of distribution but a strategic moat. The dense network of regional resellers, system integrators, and managed service partners that Sangfor built over two decades is, in many ways, the company's most underappreciated asset.

The three of them together created what insiders call the "Iron Triangle." It is a leadership architecture in which technical, operational, and commercial decisions are made jointly, with a level of trust between the three principals that is almost impossible to replicate in a company brought together by professional management. In a market like China's, where strategic windows can open and close in months and where the ability to move decisively often beats the ability to move correctly, this triangle has been a meaningful competitive advantage.

Below the founders sits a partner system that Sangfor borrowed in spirit from Huawei but refined for a public-company context. Senior engineers, sales leaders, and product general managers can be promoted into a partner tier that comes with substantial equity exposure—through restricted stock units, employee stock purchase programs, and discretionary grants—as well as participation in strategic decision-making. The intent is clear: retain Huawei-caliber talent, with Huawei-caliber intensity, but without the rigid military-style hierarchy that has caused friction at the parent. Sangfor's annual employee turnover, while not publicly disclosed in detail, is widely understood within the industry to be low for a Chinese tech firm of comparable size.

The most striking organizational statistic, however, is the R&D ratio. Roughly 40% of Sangfor's total workforce is in research and development. By global enterprise software standards, this is extraordinarily high—Palo Alto Networks, for instance, runs closer to a third—and it is reflected in an R&D-to-revenue ratio that has consistently sat in the high twenties as a percentage of sales, well above the global enterprise software median. This is not a company that views R&D as a discretionary expense to be flexed against quarterly earnings. It is a company that views R&D as the product, with everything else as supporting infrastructure.

That intensity has costs. In several recent fiscal periods, Sangfor's operating margins have come under pressure as the company has continued to invest in cloud infrastructure expansion, AI-related research, and international expansion through its Asia-Pacific subsidiaries—even as security pricing has compressed under intensifying domestic competition. The founders have been clear, in the few public statements they have made on capital allocation, that they view this as the price of building a multi-decade franchise. Whether the public market will continue to grant them that latitude, especially during quarters when net income contracts year-over-year, is one of the live questions for shareholders.

The cultural through-line, from the 2000 Huawei resignation to the 2026 boardroom, is consistency. Sangfor has had no major management defections, no boardroom coups, no founder feuds, no whisper-campaign pressure to install a foreign-trained CEO. In a tech ecosystem that prizes drama, Sangfor's stability is so quiet that it is easy to miss. But it is precisely that stability—year after year of the same three people pointing the company in the same direction—that has made the long-arc pivots possible. Capital allocation decisions that would terrify a hired CEO with a three-year contract become possible when the people making them know they will personally be living with the consequences in 2030. That continuity sets the stage for the next part of the story: the way Sangfor has chosen, again and again, to deploy its capital.

VI. Capital Deployment & M&A Benchmarking (95:00 – 115:00)

Walk into the M&A division of a typical large American enterprise software company and you will find a team of bankers and corporate development professionals whose job, essentially, is to keep the deal pipeline full. Acquisitions are how companies like Cisco, Oracle, and Salesforce have built much of their product breadth over the last two decades. Cisco alone has acquired north of 200 companies in its history. Salesforce wrote a $27.7 billion check for Slack in 2021 and a $15.7 billion one for Tableau in 2019.

Walk into Sangfor's headquarters in Shenzhen and you will not find that team. Or rather, you will find it, but it will be small, quiet, and deeply skeptical of most opportunities that cross its desk. Sangfor has made very few acquisitions in its history, and the ones it has made have been small, technology-tuck-in deals that fold cleanly into the existing R&D organization. Strategic minority stakes in specialized AI startups, GPU infrastructure firms, or chip-related ventures appear from time to time in the company's filings, but the pattern is unmistakable: build, do not buy.

This is, by global standards, an unusual posture for a company of Sangfor's scale. Why has it persisted?

The first answer is cultural. The founders, having come out of Huawei, internalized Ren Zhengfei's deep skepticism of acquisition-driven growth. Huawei's history, particularly outside of China, has been one of organic product development, occasional joint ventures, and almost no headline M&A. The view inside Huawei, and clearly carried over into Sangfor, is that acquired teams almost never integrate cleanly, that acquired technology almost never matches the architecture of the platform you are trying to bolt it into, and that the customer relationships acquired in a deal almost always degrade once the new owner takes over. Better, in this view, to spend the same capital on hiring engineers and shipping product internally.

The second answer is structural. Sangfor's principal markets—Chinese enterprise security and cloud infrastructure—have not historically been characterized by the kind of fragmented competitive landscape where a roll-up strategy creates obvious value. The major competitors are themselves large, well-capitalized, and not for sale. The interesting smaller players are typically venture-backed startups whose valuations during the boom years were, frankly, divorced from the cash flow they were producing. Buying them at peak would have been a wealth-destroying exercise.

The third answer is balance sheet philosophy. Sangfor went public in April 2018 on the Shenzhen Stock Exchange's ChiNext board. The IPO raised proceeds in the range of RMB 800 million to RMB 1 billion—roughly $120 million to $150 million depending on the prevailing exchange rate. By the standards of major American enterprise software IPOs, this was a modest amount. But the founders did not deploy it on empire-building. The use of proceeds was overwhelmingly internal: cloud platform R&D, data center buildout for the Managed Cloud business, channel expansion, and working capital. There was no transformational acquisition financed by IPO cash. There was simply a continuation of the slow, organic, engineering-led capital deployment that had defined the company's first eighteen years.

In the years since the IPO, Sangfor's balance sheet has reflected the same conservatism. The company has carried minimal long-term debt, has avoided large stock buybacks, and has maintained a substantial cash and short-term investment balance. Dividends have been modest but consistent. There is no evidence, in any annual report from the past several years, of the kind of financial engineering—aggressive leveraged buybacks, special dividends, large-scale M&A funded by debt—that has characterized many global enterprise software peers.

This conservatism has costs. Critics argue that Sangfor has been too slow to scale its cloud business through inorganic expansion, that it has missed opportunities to acquire specialized AI security startups, and that its international presence remains subscale relative to what a few well-chosen acquisitions could have produced. There is some merit to these critiques. The cloud business in particular has had to be built, region by region, data center by data center, customer by customer, in a way that has constrained near-term operating leverage even as the long-term position improves.

Benchmarking the R&D-to-revenue ratio is instructive. Sangfor's R&D intensity sits in the high 20s as a percentage of sales—above Palo Alto Networks (typically in the high teens to low 20s), above Fortinet (typically in the high teens), and broadly comparable to or higher than Nutanix during its growth phase. Among Chinese peers, Sangfor's R&D intensity is also at the higher end, with only a handful of pure-play software companies running comparable numbers. This is not the financial profile of a company optimizing for next quarter's earnings. It is the profile of a company optimizing for a multi-decade product franchise.

There is also the matter of what Sangfor has notably not done. It has not split into multiple listed entities through a Chinese-style "spin-off plus IPO" of its cloud business, even though doing so might have unlocked short-term valuation. It has not pursued a secondary listing in Hong Kong or via an ADR in the United States, even though such listings have at times been fashionable. It has not engaged in the kind of related-party financing transactions—shareholder loans, asset injections, opaque off-balance-sheet vehicles—that have at times characterized other Chinese tech listings. The company's accounting, while operating within the constraints of Chinese GAAP, has been notably clean in its treatment of revenue recognition for hardware-plus-services contracts, capitalized R&D, and segment reporting.

A modest second-layer note worth flagging: in recent years, Sangfor has taken impairments on certain receivables and inventory tied to specific government and SOE customers as China's macro environment has slowed payment cycles in lower-tier government budgets. The magnitudes have not been large enough to constitute an accounting overhang, but they are a window into a real operational risk—the longer collection cycles in public sector business are a feature, not a bug, of selling into Chinese SOEs and government agencies, and they will continue to put pressure on cash conversion in ways that public market investors should track.

The capital deployment story, then, is one of disciplined organic growth funded by a security business that throws off cash, with restraint on M&A, restraint on financial engineering, and a consistent reinvestment in R&D and channel infrastructure. This is the financial mirror of the cultural and operational story we have already told. And it is the foundation on which Sangfor's competitive position—the moats and exposures we will examine next—has been built.

VII. The Playbook: 7 Powers & 5 Forces (115:00 – 135:00)

To make sense of why Sangfor has been able to build and hold its position despite well-resourced competitors, it is worth running the company through two of the cleanest strategic frameworks available: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. Together, they expose both the durable sources of advantage and the structural pressures that the business faces.

Begin with Switching Costs. This is, arguably, Sangfor's strongest single power. Consider what it means for a Chinese provincial government or a mid-sized commercial bank to have built its private cloud on Sangfor's HCI platform. The hypervisor, storage layer, and networking are integrated into a single stack. Application teams have written automation scripts against Sangfor's APIs. Operations teams have been trained on Sangfor's management console. Backup and disaster recovery systems are configured around Sangfor's storage primitives. Migrating away to VMware or another vendor is not a software upgrade—it is a multi-year, multi-million-yuan re-platforming exercise involving downtime, retraining, and operational risk. For a CIO whose career incentive is to keep things running, the inertia is profound. This is the same dynamic that historically protected VMware globally; Sangfor is now the beneficiary of it inside China.

Cornered Resource is the second power, and here Sangfor's position is genuinely distinctive. The "Huawei diaspora" talent pool that the founders tapped into in the 2000s has continued to be a recruiting advantage. Sangfor remains one of the most desirable employers for Huawei alumni, particularly engineers in their mid-thirties who have completed their initial career at Huawei and want a more equity-oriented, less hierarchical environment. Combined with Sangfor's deep relationships with leading Chinese engineering universities—the company recruits aggressively from Tsinghua, Beihang, Huazhong University of Science and Technology, and others—the result is a sustained pipeline of high-caliber technical talent that smaller competitors cannot easily replicate. The other cornered resource is the channel itself. The thousands of regional reseller and integrator relationships that Sangfor has built up over more than two decades cannot be acquired in a year or even five.

Counter-Positioning is more subtle but real. The big public cloud platforms in China—Alibaba Cloud, Tencent Cloud, Huawei Cloud—are structurally direct-sales operations that target large internet companies, hyperscale workloads, and digital-native businesses. They have not optimized their go-to-market for the mid-market industrial enterprise, the second-tier provincial government bureau, or the regional commercial bank. To re-orient toward those customers would require a fundamentally different sales motion, a fundamentally different partner ecosystem, and a fundamentally different product packaging. They are unlikely to do it because doing so would cannibalize their high-volume hyperscale business and dilute their brand. Sangfor sits comfortably in the segments those players are structurally disinclined to attack at depth.

Scale Economies are present but not overwhelming. R&D investment in security and cloud platforms scales reasonably well—the marginal cost of supporting one more customer on the same code base is small—but Sangfor is not the largest player in any single segment globally, and so cannot claim the kind of absolute scale advantage that defines, say, Microsoft's position in productivity software.

Network Economies are largely absent. Enterprise infrastructure is not a network business in the Metcalfe sense; one customer's adoption does not directly increase the value of the product to another customer.

Process Power and Branding are partial. Sangfor has, over twenty-six years, built genuine institutional capability in customer support, deployment services, and product integration that competitors find difficult to imitate at the same cost. The brand within the Chinese enterprise IT community is strong, but it does not have the consumer-facing recognition of a Huawei or an Alibaba.

Now turn to Porter's Five Forces.

Rivalry is intense. Sangfor competes with Huawei, Alibaba, H3C, Inspur, and a half-dozen specialized security vendors on different fronts. The Chinese cloud market in particular has been characterized by aggressive pricing—what some analysts have called the "Cloud Price War," with major hyperscalers cutting public cloud prices repeatedly over recent years to win market share. Sangfor is partly insulated from the worst of this because its cloud business is private and managed rather than public hyperscale, but pricing pressure inevitably bleeds across the boundary.

The Bargaining Power of Buyers is high in certain segments, particularly large SOEs and central government agencies, which run formal procurement processes designed to extract concessions on price and service levels. Sangfor's high-touch service model, with deep technical pre-sales engagement and long-term implementation services, partially offsets this by raising the perceived cost of switching vendors. In the SME and lower-mid-market segment, buyer power is much lower because customers lack the procurement leverage of large enterprises and place a premium on vendor reliability.

The Bargaining Power of Suppliers is moderate. Sangfor's hardware appliances depend on standard x86 server components from Intel, memory from major DRAM and NAND suppliers, and networking ASICs from a small set of vendors. Recent geopolitical pressures have made supply chain resilience a meaningful concern, and Sangfor has been progressively diversifying toward domestically produced chips and components where viable. The shift has cost margin in the short term but reduces strategic exposure.

The Threat of New Entrants is moderate to low in security and cloud infrastructure. The capital required to build a credible enterprise cloud platform from scratch is substantial, and the channel and customer relationships needed to sell it are not available to a startup. New entrants in adjacent areas—particularly AI-driven security analytics—are a real factor, and Sangfor has had to invest heavily in its own AI capabilities to keep pace.

The Threat of Substitutes is the most interesting force. The principal substitute for on-premises HCI is, of course, public cloud. Every workload that migrates from a customer data center to Alibaba Cloud or Tencent Cloud is a workload that Sangfor does not get to host on its HCI platform. The counter-trend, however, is the regulatory and sovereignty preference for private cloud or sovereign cloud deployments in many sensitive industries—government, financial services, healthcare, energy. The Xinchuang policy environment further tilts the balance toward private and managed cloud, where Sangfor competes effectively, rather than toward public hyperscale.

Putting the two frameworks together, the picture is of a company with strong switching cost moats and meaningful cornered resources, operating in an industry with intense rivalry but partially insulated by counter-positioning against the hyperscale clouds. The principal vulnerabilities are pricing pressure from intensifying competition and the long-running risk that Huawei, which has sat largely on the sidelines of the mid-market enterprise infrastructure space, decides at some point to compete more aggressively. Those vulnerabilities are real, and they sit at the heart of the bear case we will examine next.

VIII. Bear vs. Bull Case (135:00 – 145:00)

Every long-form investment narrative deserves to be tested against itself, and Sangfor is no exception. There are coherent bear and bull cases, and the reader's best service is to lay them out plainly.

Begin with the bear case. The first concern is the cloud price war. Public cloud pricing in China has been under sustained pressure as Alibaba, Tencent, and Huawei have repeatedly cut headline rates to drive workload migration. Even though Sangfor's principal cloud exposure is in private and managed cloud rather than public hyperscale, the price benchmarks set by the public cloud market inevitably anchor customer expectations across the entire stack. As enterprise buyers compare a managed cloud quotation from Sangfor with a public cloud quotation from a hyperscaler, the negotiation becomes harder, and gross margins on cloud services can compress over time.

The second concern is "Big Brother Huawei." For more than two decades, Huawei has largely allowed Sangfor to dominate the SME and mid-market enterprise infrastructure segment, focusing its own enterprise division on large accounts and carrier-related opportunities. There is no guarantee that this restraint continues indefinitely. Huawei Cloud has been growing aggressively, and the parent company's enterprise business has shown periodic interest in moving down-market. If Huawei ever decided to deploy its full balance sheet, brand strength, and channel reach against Sangfor's core segments, the competitive dynamics would change rapidly. Sangfor would not be eliminated—the switching costs are real—but new logo growth would slow materially.

The third concern is the long-term margin transition from hardware to cloud. Hardware appliance businesses, particularly in security, generate gross margins north of 70%. Managed cloud services generate gross margins meaningfully lower, often in the 30-to-50% range depending on the customer mix and the depth of services bundled in. As the revenue mix continues to shift toward cloud, blended gross margins are likely to drift lower, and the company will need to demonstrate that operating leverage from scale offsets the structural margin compression from mix shift. There will be quarters when this looks ugly on the income statement.

The fourth concern is geopolitical and regulatory. Sangfor's international ambitions, while modest, have been complicated by the broader U.S.-China technology decoupling. Selling into certain markets—particularly the United States and its closest allies—is effectively closed to Chinese cybersecurity vendors regardless of product merit. International expansion will be confined to Southeast Asia, the Middle East, and parts of Africa and Latin America, all of which are real but smaller addressable markets than a truly global vendor would enjoy.

The fifth concern is government and SOE collection cycles. As Chinese local government finances have come under strain, payment cycles for IT projects sold into provincial and municipal agencies have lengthened. This shows up as increases in days-sales-outstanding and elevated allowances for credit losses on receivables. None of this is fatal, but it pressures cash conversion and working capital in ways that are easy to miss if you only look at revenue growth.

Now the bull case. The first pillar is the Xinchuang tailwind. The Chinese government's commitment to domestic substitution of foreign IT infrastructure is not a quarter-by-quarter preference; it is a multi-year, multi-administration policy backed by procurement guidelines, budget allocations, and explicit references in successive five-year plans. Sangfor is one of a very small number of vendors that have credible products across hypervisor, software-defined storage, software-defined networking, and integrated security to compete for the workloads being decommissioned from VMware, Citrix, and the foreign security vendors. The total addressable market that opens up as Chinese enterprises and government agencies execute these migrations over the next decade is, by any reasonable estimate, very large, and Sangfor is one of the natural beneficiaries.

The second pillar is the embedded base. Tens of thousands of Chinese enterprises run mission-critical workloads on Sangfor security and cloud platforms. This embedded base is the foundation of an annuity-like revenue stream from maintenance, subscription, support, and incremental modules. As cloud and managed services subscriptions grow as a share of the total mix, the recurring revenue base becomes more visible and more valuable from a financial framework perspective. Markets that learn to recognize this transition—from box-shipping to subscription—often re-rate the underlying multiple meaningfully.

The third pillar is the founder-aligned governance structure. With three founders still operating the company, holding combined equity of around 40%, and showing no signs of the kind of capital allocation flights of fancy that have damaged other Chinese tech firms, Sangfor offers a rare combination in the Chinese enterprise tech universe: long-term thinking, clean accounting, organic growth discipline, and a management team whose interests are unambiguously aligned with long-term shareholders.

The fourth pillar is optionality in adjacent segments. Sangfor's underlying capabilities in security, virtualization, and managed services are a platform from which a number of adjacent businesses can be built—including the AI security business that we will discuss in the epilogue, expanded edge computing offerings, and deeper vertical-specific solutions in healthcare, manufacturing, and finance. Each of these is unproven, but each represents real call options on top of the core franchise.

The KPIs that matter for tracking Sangfor over the coming years are, in this analyst's view, narrow: first, the segment growth rate of the cloud computing business and its contribution to total revenue; second, the gross margin trajectory of the cloud segment as it scales, which will indicate whether the company is achieving the operating leverage required to justify the mix shift; and third, the operating cash flow conversion ratio, which will show whether the lengthening collection cycles in government and SOE accounts are being contained or are eroding the financial quality of the underlying growth.

The myth-versus-reality lens is also useful here. The consensus narrative on Sangfor has long been that it is a network security company. The reality is that it is increasingly a hybrid security-and-cloud infrastructure company, with the cloud half growing faster and likely to constitute the majority of incremental enterprise value created over the coming decade. A second consensus narrative is that Sangfor is a "Little Huawei" that lives or dies by Huawei's tolerance. The reality is more nuanced: while Huawei is unquestionably a competitive risk, Sangfor's customer base, channel structure, and product positioning make it considerably more independent than the nickname suggests. The third consensus narrative is that Sangfor is purely a domestic China play. The reality is that, while international revenue remains a small share of the total, Asia-Pacific markets outside mainland China have been growing meaningfully and provide a real, if modest, hedge against pure domestic exposure.

Both cases are coherent. Both are supported by the data available. Which one ultimately prevails depends on operational execution, on competitive dynamics that are difficult to predict, and on macro factors well outside any single management team's control. What the bear and bull cases share is the recognition that we are watching, in real time, a meaningful business transition—from a hardware-led security incumbent to a software-defined infrastructure platform—and that the quality of the management team executing it deserves serious credit. With that, the final chapter belongs to where the company is heading next.

IX. Epilogue: The AI Frontier (145:00 – 155:00)

In late 2023, Sangfor announced the launch of what it branded "Security GPT"—a large language model purpose-built for cybersecurity operations. The product was, in many ways, the natural evolution of the company's two-decade-long bet that customers wanted security to be done for them, not merely sold to them. Security GPT was designed to ingest log data, threat intelligence, and incident reports and to produce, in plain language, summaries of what was happening in a customer's environment, recommended remediation actions, and—critically—the ability to execute many of those actions automatically through Sangfor's existing security platform.

The strategic logic was straightforward. Cybersecurity, globally, suffers from an acute shortage of skilled analysts. In China, where the talent gap is even more pronounced relative to the size of the digital economy, mid-market customers simply cannot hire enough qualified people to monitor their security operations centers around the clock. An AI assistant that can triage alerts, escalate genuine threats, and quietly close low-priority tickets is not a luxury; it is, for many customers, the only way to operate a credible security posture at all.

Sangfor's approach to AI has been characteristically pragmatic. Rather than trying to compete head-on with the foundation model labs—Baidu's Ernie, Alibaba's Qwen, Moonshot, DeepSeek—the company has focused on fine-tuning open-source and partner-provided base models for specific security and IT operations use cases. The differentiation comes from the data: Sangfor has, by virtue of its installed base, access to vast amounts of telemetry from real Chinese enterprise networks, which allows it to train models that actually understand what normal and abnormal traffic patterns look like in those environments.

The same pattern is showing up in the cloud business. Sangfor has been progressively integrating AI-driven capabilities into its HCI platform—predictive failure analysis on hardware components, automated capacity planning based on workload patterns, intelligent placement of virtual machines to optimize resource utilization. None of these are revolutionary in the global landscape; what makes them notable is that Sangfor is bringing them to a Chinese mid-market customer base that has historically been served by simpler, more manual tools.

Stepping back from the AI specifics and considering the full arc of the company, the through-line is unmistakable. Sangfor is a company that started in 2000 by selling caching boxes to internet cafés in second-tier Chinese cities and that, by 2026, has become the dominant domestic vendor in private cloud infrastructure for Chinese enterprises and a pillar of the country's digital sovereignty strategy. The path was not glamorous. It involved no celebrity founders, no headline acquisitions, no capital markets pyrotechnics. It involved twenty-six years of three engineers in Shenzhen building one product, then another, then another, each one quietly displacing a foreign competitor in a market segment most observers had not even noticed.

There are companies whose stories are dominated by single decisive moments—a transformative acquisition, a viral product launch, a "bet the company" pivot. Sangfor is not one of them. Its story is dominated by the cumulative effect of thousands of small decisions made consistently in the same direction over more than two decades. It is a story about second-mover advantage, about the discipline of organic growth, about the strategic value of a deep channel network in a country where geography matters, and about the rare benefit of having the original founders still in the room, still walking the R&D floor, still keeping notebooks of customer complaints.

For long-term fundamental investors, the most interesting question about Sangfor in 2026 is not whether the company can grow—the Xinchuang tailwind, the embedded base, and the cloud transition all suggest it can and will. The interesting question is whether the cloud business can scale in a way that proves the unit economics, whether the security cash cow holds up long enough to fund the transition, and whether the founders' patient capital allocation philosophy continues to deliver returns competitive with more aggressive global peers. Those questions will be answered, slowly, over the next five to ten years, in earnings releases and segment disclosures that are unlikely to make front-page news but that will, in aggregate, determine whether Sangfor becomes the next fifty-billion-dollar Chinese enterprise software franchise or settles into the comfortable middle of its category.

The company that walked out of Huawei in 2000 to solve the entry-point problem for the Chinese internet has, in the intervening twenty-six years, quietly built something larger than any of the founders likely imagined when they signed the first office lease. The next chapter is being written now, in the data centers Sangfor is building across Chinese provinces, in the AI models being trained on enterprise telemetry, and in the boardrooms of customers deciding whose hypervisor to install when the VMware contract finally expires. The Iron Triangle is still in the building. The notebooks are still being filled. And in a country and an industry that prize dramatic narratives, the most underestimated company may, once again, be the one that simply keeps shipping.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube