Japan Tobacco: The Global Sovereign Chimney

I. Introduction & Episode Roadmap

Picture the paradox. Somewhere in a Tokyo ministry building, a civil servant at the 財務省 Ministry of Finance (Zaimushō) tracks a single line item with unusual attention: the dividend from Japan Tobacco. The government is not a passive index holder. It is legally required to own at least one-third of the company, and JT's payout lands, in part, in the national accounts. When JT raises its dividend, the sovereign benefits. When JT stumbles, so does a slice of the state's finances. This is a company whose largest shareholder writes the tobacco laws it lives under.

Now hold that image against the second one: a fleet of engineers and brand managers in Geneva, Switzerland, running a global cigarette empire with the swagger of a Silicon Valley growth firm — buying US rivals in cash, launching heated-tobacco devices in dozens of countries, and openly defending operations in Russia and Iran on the grounds that leaving would destroy shareholder value. The bureaucrat and the buccaneer are the same company.

How does a former state monopoly, structurally chained to a declining domestic market, become a roll-up engine that has spent tens of billions of dollars acquiring foreign tobacco giants? That tension — between the cautious sovereign parent and the ravenous global operator — is the engine of this entire story.

In 2026, three battlegrounds define the investment case. The first is what we might call the RRP arms race: JT's roughly ¥450 billion counter-offensive to claw back the Heated Tobacco Product (HTP) market from Philip Morris International (PMI) — the American giant that humiliated JT on its own home turf with a device called IQOS.15 The second is the geopolitical trap: JT's decision to remain fully operational in Russia, where its subsidiary is the market leader, even as Western competitors took multibillion-dollar exits.[^17] The third is the portfolio clean-up: the 2025 divestment of JT's entire pharmaceutical division to 塩野義製薬株式会社 Shionogi & Co., Ltd., a move that stripped the company down to a pure-play nicotine and cash machine.[^11]

Over the following sections, the arc runs from Meiji-era monopolies and the Geneva "autonomous JTI" model, through the IQOS humiliation and the ¥450 billion fightback, into the Vector Group acquisition, the largest tobacco litigation settlement in Canadian history, and finally the sharpest question of all: from here, why does JT win — and what could break the case entirely? We will not take management's word for any of it. When the company says it will win, the job is to ask what evidence supports the claim and what would prove it wrong.

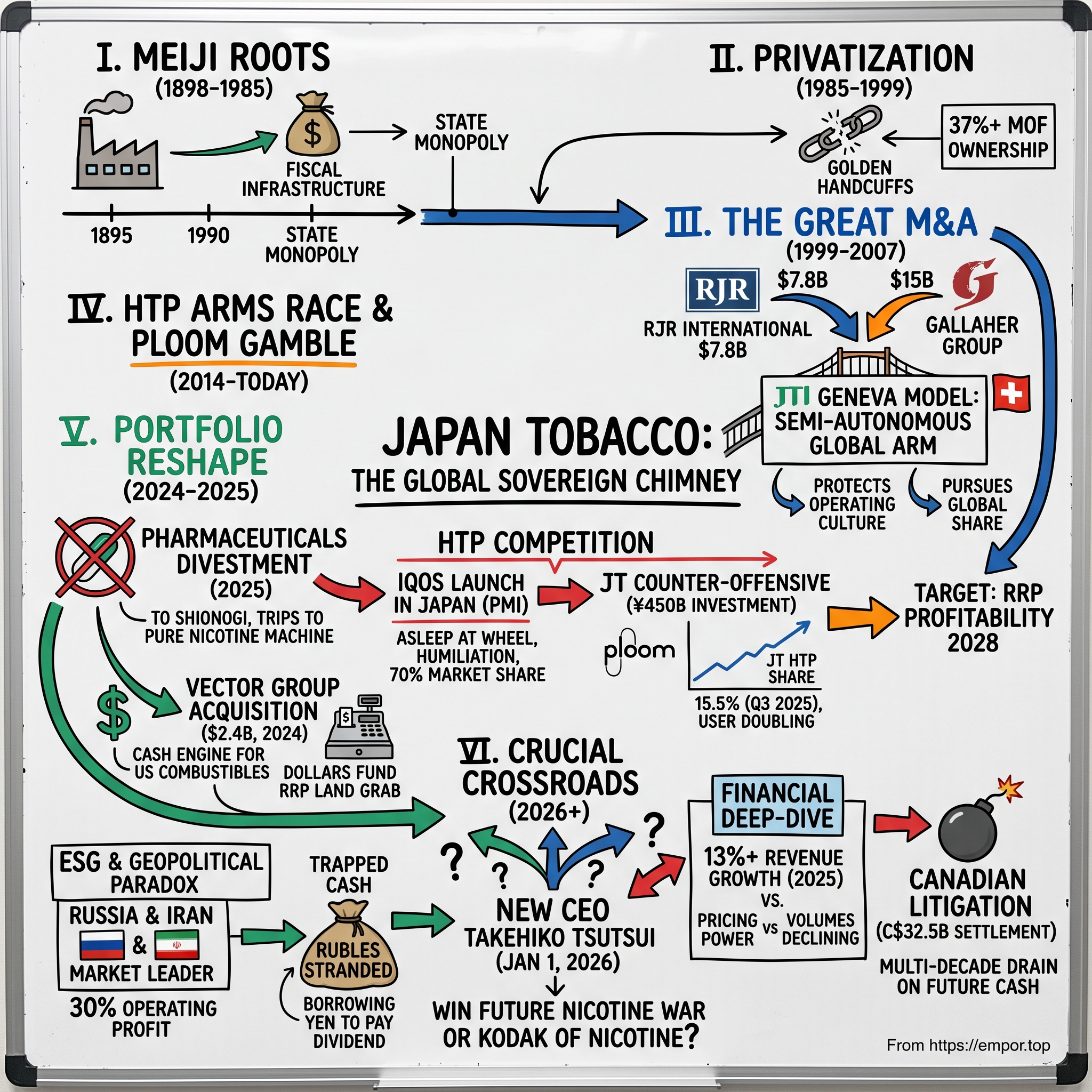

II. The Meiji Roots & State Monopoly (1898-1985)

To understand why the Japanese government still clutches a third of JT's shares in 2026, you have to go back to a war — and to a state that needed money to fight it.

At the turn of the twentieth century, Imperial Japan was a rising power with imperial ambitions and a chronically strained treasury. When it squared off against the Russian Empire in the 日露戦争 Russo-Japanese War (1904–1905), the Meiji government confronted the eternal problem of nations at war: how to pay for it without triggering a domestic revolt over taxes. The answer was a trick as old as governance itself — monopolize something people cannot stop buying. In 1904, the state established an absolute monopoly over tobacco (and, separately, salt), converting a private vice into a dependable, non-tax stream of revenue flowing straight into the war chest.12 Tobacco was not merely a product; it was fiscal infrastructure.

That founding logic never really left. For the next eighty years, the Japanese tobacco business was run not as a consumer enterprise but as an organ of the state. In 1949, in the reconstruction years after the Second World War, the monopoly was reorganized into the 日本専売公社 Japan Tobacco and Salt Public Corporation (Nihon Senbai Kōsha), a public corporation whose employees were, in effect, civil servants and whose mandate was as much fiscal as commercial.12

Imagine running a cigarette company where the goal is not to delight the customer but to reliably remit cash to the finance ministry. There was no foreign competition — imports were effectively locked out. There was no marketing arms race, no need to fight for shelf space. Brands like Seven Stars, Cabin, and Mild Seven (later rechristened Mevius) were woven into the texture of post-war Japanese life, as much a fixture of the salaryman's day as the commuter train and the after-work izakaya. The public corporation manufactured, priced, and distributed with the placid confidence of a utility.

And what a utility it was. At the zenith of the smoking era in the 1960s, male smoking rates in Japan exceeded 80% — four in five adult men lit up. The domestic market was a locked vault: no foreign brands, near-universal consumption, and a captive population of addicted, price-inelastic buyers. The cash flows were, by any standard, astronomical, and they belonged to the government.

But a monopoly built to fund a war has a hidden fragility. It teaches an organization nothing about competition. It breeds a culture of administration, not ambition. When the vault doors eventually opened — and they would — the bureau would discover that decades of guaranteed profits had left it dangerously unprepared to fight for a single customer. The reckoning began the moment Japan decided its state monopoly no longer fit a modern, trade-opening economy.

III. Privatization & The Golden Handcuffs of the State (1985-1999)

In the early 1980s, Prime Minister 中曽根康弘 Yasuhiro Nakasone set about doing to Japan's public corporations what Margaret Thatcher was doing to Britain's: privatizing them. The national railways, the telephone monopoly, and the tobacco-and-salt bureau were all on the block. In 1985, the public corporation was restructured into a joint-stock company — 日本たばこ産業株式会社 Japan Tobacco Inc. — explicitly to prepare the once-sheltered monopoly for the coming shock of foreign competition.12

But here the Japanese state did something revealing. It let go of the tobacco business — and refused to actually let go. The enabling legislation, the Japan Tobacco Inc. Act, hard-wired the government into the company's ownership. The Ministry of Finance was legally mandated to hold at least one-third of all issued JT shares.3 This was no accident of a slow privatization; it was designed permanence. Over four decades later, that stake still sits around 37–38% of the company — a controlling anchor that no market force can dislodge.3

Think about what that structure does to incentives. The government is not a dispassionate steward here. It is a beneficiary. A meaningful share of JT's dividend flows back to the state, which means the finance ministry has a direct, self-interested reason to want JT profitable, cash-generative, and generous with distributions. This is the origin of what has become JT's defining capital-allocation signature: a policy of returning a very large share of profits to shareholders, with management targeting a payout ratio around 75% of earnings.1 Most companies choose their dividend policy. JT, in a sense, inherited a shareholder who expects one.

These are the golden handcuffs. On one wrist, a guaranteed anchor shareholder and an implicit sense that the sovereign will not let the company fail. On the other, a permanent obligation to feed the dividend machine, which constrains how much capital JT can retain and reinvest on its own terms. For an income investor, the handcuffs look like security. For a growth strategist, they look like a leash.

And a leash was precisely the wrong thing to be wearing at the end of the twentieth century, because the ground under JT's home market was collapsing. By the 1990s the Japanese domestic cigarette business had entered terminal, structural decline. The population was aging fast. Anti-smoking sentiment was hardening, on the streets and in the ministries. And with the import barriers gone, PMI and British American Tobacco (BAT) were pouring into Japan with Marlboro and its rivals, peeling away share from a company that had never in its life had to defend a market.

The math was brutal and simple. A company confined to a shrinking, high-tax, socially retreating home market is not a business; it is a slow-motion liquidation with a dividend attached. JT's leadership grasped the existential arithmetic: stay purely domestic, and the sovereign chimney would eventually stop smoking. The only escape was to buy its way out — abroad, at scale, and fast. What came next was one of the boldest gambles in the history of Japanese business.

IV. The Great M&A Escape Hatch: RJR & Gallaher (1999-2007)

In 1999, a Japanese ex-monopoly with almost no international operating experience walked up to the poker table and shoved in $7.8 billion.

The chips bought the non-US operations of RJ Reynolds — the international arm of one of America's most storied tobacco houses, carrying legendary global brands like Winston, Camel, and LD.12 It was, at the time, the largest outbound acquisition ever attempted by a Japanese company, and the skeptics were merciless. The prevailing view on Wall Street and in the trade press was that this would be a slow-motion culture crash: cautious, consensus-driven Japanese former civil servants, weaned on 稟議 ringi bureaucratic decision-making, would smother the swaggering, entrepreneurial, results-obsessed sales culture of RJR International. The Tokyo parent would strangle the very asset it had paid a fortune to acquire.

JT's answer to that critique was the single most important organizational decision in its modern history — and it is a genuine case study in how to integrate across cultures. Rather than absorb RJR into Tokyo, JT quarantined it from Tokyo. It established JT International — JTI — as a semi-autonomous entity headquartered not in Japan but in Geneva, Switzerland. JTI was handed the global brand portfolio and, crucially, real operating independence, deliberately insulated from the parent's bureaucratic reflexes.12 The idea was almost counterintuitive: to protect the value of the acquisition, the acquirer agreed not to run it like an acquirer. Geneva would chase global market share; Tokyo would tend the domestic garden and the dividend.

The model worked well enough that JT ran the play again, bigger. In 2007, JT acquired the UK's Gallaher Group for roughly £7.5 billion (around $15 billion) — bringing Benson & Hedges, Silk Cut, and Sobranie into the fold, and cementing JTI's grip on Europe.12 Many analysts thought the price was rich, and by conventional valuation yardsticks it probably was. But strategically the outcome was hard to argue with: the Gallaher deal bought JT genuine global scale and a permanent seat at the table of the tobacco "Big Four," alongside PMI, BAT, and Imperial Brands.

What JT had actually built, beneath the deal headlines, was a repeatable capability — arguably its single most valuable one. Call it the two-headed giant: Tokyo governs Japan and the sovereign relationship; Geneva governs the world and the brands. The separation let JT do something most conglomerates fail at, which is to acquire foreign businesses without destroying the operating cultures that made them worth buying. That process power would become a recurring theme in every later chapter of the company.

But here is the uncomfortable footnote the bull case tends to skip. The Geneva model was a brilliant solution to a defensive problem: how to survive the decline of the Japanese cigarette. It was optimized for acquiring and running combustible cigarette businesses across many markets. It was not, it would turn out, optimized for inventing the future of nicotine. And the future was about to arrive — in Japan, of all places, delivered by the very American rival JT thought it had learned to compete with.

V. The Heat-not-Burn Counter-Revolution & The Ploom Gamble (2014-Today)

In 2014, Philip Morris International did something audacious: it chose Japan — JT's fortress, its home vault — as the global launch market for a device that would rewrite the industry. The device was IQOS, and it did not burn tobacco. It heated it.

The choice of Japan was shrewd, and it exposed a regulatory quirk JT should have exploited first. In Japan, liquid nicotine e-cigarettes — the vapes that swept the United States and Europe — were effectively banned under pharmaceutical law. That closed off one whole category of "smoke-free" product and left a gap for a different one: the Heated Tobacco Product, which heats real tobacco to produce an inhalable aerosol without combustion. Japan, in other words, was the one major market where an HTP had no vaping competition and a huge base of health-conscious but addicted smokers looking for an off-ramp. PMI walked straight through the open door.

JT, by most fair readings, was caught asleep at the wheel. The company appears to have assumed that Japanese smokers — loyal, traditional, brand-attached — would never abandon their combustible Sevens and Meviuses for a battery-powered gadget. That assumption was catastrophically wrong. IQOS triggered a consumer migration with almost no precedent in a mature consumer category. Smoke-free products — overwhelmingly HTPs — grew to represent a large and rising slice of the entire Japanese nicotine market, on the order of nearly half of it by the mid-2020s.17 An entire nation of smokers began switching hardware.

The strategic damage was severe. As the first mover with a superior product, PMI captured a commanding lead in the Japanese HTP category — a share widely estimated around 70%.17 JT's early answer, a hybrid vapor product line called Ploom TECH, was a commercial failure: the aerosol delivery was weak, the nicotine satisfaction low, and consumers — who do not switch addictions for a worse experience — voted with their wallets. For a company that had spent a century as the unchallenged king of Japanese tobacco, watching an American rival storm the castle with a better mousetrap was a genuine humiliation, and management has largely admitted the category lead was lost.

The counter-attack

What followed is the live drama of the JT investment case in 2026. The first move was organizational. In 2022, JT collapsed its historically separate domestic and international tobacco divisions into a single, unified tobacco business run out of Geneva — extending the autonomy model to the whole company and, in principle, speeding up decisions that Tokyo's structure had slowed.12 The message was blunt: never again would JT be too slow and too fragmented to respond to a category shift.

The second move was money. JT committed a multi-year war chest — roughly ¥450 billion — to a global rollout of its flagship next-generation device, Ploom X, explicitly framed as the counter to PMI's dominance.15 Then, in mid-2025, came the domestic catalyst: the launch of Ploom AURA, a new device accompanied by premium heated "sticks," aimed squarely at winning back Japanese consumers.1

The proof points are, so far, encouraging enough that they deserve to be taken seriously rather than dismissed. JT's heated-tobacco share in Japan climbed through 2024 and into 2025, reaching 15.5% of the heated-tobacco category in the third quarter of 2025 — a meaningful step up, with the number of Ploom users in Japan roughly doubling versus two years earlier.45 On the Q3 2025 call, management pointed to Ploom AURA and its EVO sticks as the engine of that gain, and RRP volumes grew around 40% year-on-year.4 Internationally, JT has been expanding Ploom X across dozens of markets, with a stated ambition to reach roughly 40 markets and to bring the global RRP business to profitability — management's guidance points toward the segment turning self-sustaining around 2028.5

Here is where the neutral posture matters. A move from near-zero to 15.5% is real momentum, and it is evidence that JT can build a competitive device and merchandise it. But investors should sit with the harder question the outline poses directly: is 15.5% a victory, or is it the cost of admission? PMI still leads the Japanese HTP category by a wide margin, and JT is spending hundreds of billions of yen to occupy second place in a category it once would have owned outright. The bull reads the share gains as an inflection. The bear reads the same numbers as an expensive, permanent runner-up buying share at negative margins until a 2028 break-even that has not yet been proven. Both are looking at the same KPI — and it is the single most important number to track in this entire story.

That RRP fight is also expensive enough that JT needs somewhere to get hard, predictable cash to pay for it. Which brings us to how the company reshaped its portfolio.

VI. The Portfolio Reshape: Vector Group & Shionogi Divestment (2024-2025)

Great capital allocators are often defined less by what they buy than by what they finally admit they should never have owned. In 2025, JT made both kinds of decision within months of each other — shedding a decades-old diversification and buying a cash engine to feed the nicotine war.

The Shionogi pivot

For much of its post-privatization life, JT hedged the terminal decline of tobacco by diversifying — most notably into pharmaceuticals, a business with attractive economics but almost nothing in common with cigarettes. The logic was defensive: if the core is dying, plant something else. But a pharma R&D operation inside a tobacco company is a strange animal — capital-hungry, culturally distinct, and a persistent distraction for management and investors alike.

In 2025, JT ended the experiment. It agreed to transfer its entire pharmaceutical research, development, and distribution business — including its US arm, Akros Pharma — to Shionogi & Co., Ltd., structured as a simplified absorption-type company split, with the transaction completed late in the year.[^11][^12] From the third quarter of 2025, the pharmaceutical business was reported as a discontinued operation.1

The strategic meaning is clean, and it is the kind of focus-inducing move that activists usually have to force on a company. JT chose to stop pretending it could be a diversified conglomerate and to become, instead, an undisguised pure-play on nicotine and cash generation. Whether that is wisdom or fatalism depends on your view of tobacco's terminal value — but as a statement of intent, it is unambiguous. Management is betting the whole company on nicotine, and it wants no side businesses muddying the capital-allocation story.

The Vector Group cash engine

If Shionogi was about subtraction, Vector was about addition — of exactly the kind of asset JT's strategy now demanded. In August 2024, JT agreed to acquire the US-based Vector Group Ltd. — owner of the Liggett cigarette business and brands like Eve and Pyramid — for $15.00 per share in cash, a deal valuing Vector at around $2.4 billion.67 The tender offer ran through early October, drew the large majority of shares, and closed with Vector becoming a wholly owned JT subsidiary on October 7, 2024.8

The rationale rewards a moment's thought. The United States is one of the most profitable tobacco markets on earth, and yet JT — for all its global reach — had historically had a microscopic presence there. Vector handed JT immediate access to a profitable, cash-generative US combustible network without the years of organic slog it would otherwise require. Deep-discount cigarettes are not glamorous, but they throw off exactly what JT needs.

And what JT needs is hard currency. This is the quiet strategic elegance of the two deals sitting together: US combustibles generate predictable dollar cash flows that can be directed toward the expensive, yen-and-euro-denominated global rollout of Ploom X — funding the RRP land grab without draining the domestic dividend pool that the finance ministry, and every income investor, is watching. Vector, in effect, is the flywheel: a mature, boring, dollar-generating combustible business bankrolling the risky, capital-hungry fight for the smoke-free future.

But hard currency is precisely the thing JT struggles to extract from its single most profitable and most controversial geography. To understand the real risk sitting under the dividend, you have to follow the cash to Moscow — and find out why so much of it cannot get home.

VII. The Geopolitical and ESG Paradox: Russia, Iran, and Trapped Cash

Every high dividend yield is the market's way of asking a question. In JT's case, the question is written in the geography of its profits.

When Russia invaded Ukraine in 2022, the Western corporate world staged one of the fastest mass exits in business history. Among the tobacco majors, BAT eventually agreed to sell its Russian operations, taking a substantial write-down, and PMI signaled a wind-down. JT did something different. It stayed.[^17] JTI remained fully operational in Russia, where it is the outright market leader and one of the largest fast-moving consumer goods companies in the country by sales value.12 JT's public defense, articulated by JTI's own corporate affairs leadership, leaned on continuity — a reluctance to abandon consumers and employees.[^17]

The unstated logic is colder and more honest, and management has gestured at it: exiting Russia would very likely mean handing the assets over for a pittance or watching them nationalized outright, converting a highly profitable business into a write-off. For a company whose largest shareholder is a government that depends on the dividend, torching a major profit center on principle is not a costless moral gesture — it is a direct hit to the sovereign's income and to every other shareholder's. That is the trap: the ethically cleanest move and the fiduciarily defensible move point in opposite directions.

The economic weight involved is not marginal. Russia, together with Iran — another sanctioned, high-risk geography where JT operates — is estimated to account for on the order of 30% of JT's total operating profits. Even allowing for uncertainty in that figure, it means roughly a third of the company's earning power sits behind some of the most politically fraught borders in the world. In its 2025 results, JT explicitly flagged hyperinflationary accounting for markets including Iran, Turkey, and Myanmar, and repeatedly cited Russia and Turkey as major contributors to pricing-led profit growth — a tacit admission of how load-bearing these markets have become.1

Then there is the problem of getting the money out. This is the part that should worry a dividend investor more than the headlines about ESG. Profits earned in Russia are lucrative on paper, but Western sanctions and Russian counter-sanctions — including strict capital controls — make repatriating those rubles to Tokyo genuinely difficult. The result is "trapped cash": earnings that show up in consolidated profit but cannot freely travel to headquarters to be paid out. To maintain its high payout target while a meaningful chunk of its cash generation is stranded, JT leans on its access to cheap domestic Japanese borrowing.16 In effect, the company can borrow in yen against cash it technically owns but cannot move.

This is the ESG-and-geopolitics paradox in one sentence: JT earns a superb return in places that make its cash hard to spend and its stock hard to own. Many Western institutional funds have screened JT out entirely on the basis of its Russia footprint, which is part of why the yield is so high in the first place — the buyer base is structurally narrowed. For the investor who is willing to hold it, the yield is compensation for a specific, nameable set of risks: nationalization, ruble devaluation, and a balance sheet quietly absorbing the strain of profits it cannot repatriate. Those risks are not hypothetical tail scenarios; they are live features of the business today. And they compound a second, entirely separate liability that JT booked into its accounts across 2024 and 2025 — one born not in Moscow but in a courtroom in Ontario.

VIII. Financial Deep-Dive, Segment-Level Unit Economics, and the Canadian Liability

Strip JT down to its financial skeleton and a very simple truth appears: this is a tobacco company with a rounding error attached.

The segment reality

For the 2025 financial year, JT reported record consolidated revenue of roughly ¥3,467.7 billion, up sharply — around 13% — from the prior year, helped by pricing, the Vector acquisition, and RRP growth.12 Behind that headline sits a business of startling concentration. The tobacco segment is not a division of JT; it is JT, generating the overwhelming majority of group revenue and effectively all of the meaningful profit.1 The company's adjusted operating profit at constant currency reached roughly ¥927.5 billion, up nearly 25%, driven by what management repeatedly described as pricing power — the ability to raise prices faster than volumes decline.2

The other businesses are, financially, almost decorative. The processed-food arm, TableMark — think frozen udon and packaged rice — is a steady, respectable operation that contributes a small fraction of group revenue and a negligible slice of profit.1 It is a legacy asset, not a growth engine, and its main function in the story is to remind you how little diversification is left after the Shionogi exit. JT is now, by design, a nicotine company with a food hobby.

What the numbers actually reveal, in plain English, is the anatomy of the classic tobacco machine: volumes in most markets are flat to falling, but price and mix rise faster, so revenue and profit grow even as fewer sticks are sold. That is pricing power in action, and it is the core reason a "declining" industry can keep minting cash. But pricing power is not infinite — it depends on addiction, on the absence of cheap substitutes, and on tax regimes that have so far raised prices without breaking the market. Investors should treat JT's revenue growth not as evidence of a healthy end market but as evidence of an extraordinarily durable ability to extract more money from a shrinking one. Those are very different things.

The Canadian class-action landmine

Now the liability that turned JT's 2024 accounts inside out. For decades, Canadian smokers and provincial governments pursued the tobacco majors — including JT's subsidiary, JTI-Macdonald — for the health consequences of smoking. The litigation ground on until a court-appointed mediator, in October 2024, proposed a comprehensive settlement across the industry.[^15] Creditors approved it, and on March 6, 2025, the Ontario Superior Court granted formal approval of a landmark plan totaling C$32.5 billion across the three companies — a sum the presiding judge called a milestone in Canadian restructuring history.910

The structure of that settlement is the whole point. Under the plan, the companies pay out the bulk of their existing cash and a majority of their future after-tax income until the enormous sum is satisfied — a process expected to stretch across roughly two decades, with over C$24 billion flowing to provinces, more than C$4 billion to Quebec class-action plaintiffs, and further amounts to other smokers and a disease-fighting foundation.910 JTI-Macdonald's share of the total runs to several billion Canadian dollars.11

For JT's financials, the accounting hit landed hard and early. To account for the liability, JT booked a very large litigation provision in its 2024 results, and the effect on reported (GAAP) operating profit was dramatic — it compressed reported operating profit far below the "adjusted" figure that strips such one-offs out.1 This is exactly the kind of gap between headline and adjusted earnings that a skeptical investor should interrogate rather than wave away: the adjusted number tells you about the ongoing business; the reported number reminds you that decades-old liabilities can still crystallize into billions of provisions overnight.

The saving grace — and it is a real one — is the payment schedule. Because the settlement is amortized over roughly twenty to thirty years rather than paid in a lump sum, it does not threaten JT with a sudden cash crisis.9 It is a slow, multi-decade drain rather than a heart attack. But it is a drain nonetheless: a long-dated claim on future cash flow that competes, year after year, with the dividend, the RRP investment, and any future M&A. Between trapped Russian cash on one side and a multi-decade Canadian liability on the other, JT's celebrated cash machine is running with two significant leaks. The question is whether the pricing power upstream is strong enough to keep the tank full — which is exactly what the strategic frameworks help us test.

IX. Playbook: Business & Investing Lessons

Step back from the news flow and ask the structural question: what, exactly, protects JT's profits — and where is the armor thin? Two frameworks make the answer legible.

Hamilton Helmer's 7 Powers

Scale Economies (High). JT buys leaf, manufactures at enormous automated volumes, and distributes across 130-plus markets. In a business where the product is cheap to make and the fixed costs of compliance, distribution, and brand maintenance are high, scale translates directly into cost advantage. The Big Four structure of the global industry is itself evidence: this is a game only giants can afford to play.

Switching Costs (rising in HTP). In traditional cigarettes, switching costs are really taste and habit — meaningful, but soft. In heated tobacco they become genuinely hard. An HTP consumer buys a proprietary device — an IQOS or a Ploom — and then must buy the matching sticks. Once someone has invested in the hardware and adapted to the ritual, moving to a rival ecosystem means buying a new device and re-learning the experience. That lock-in is precisely why the current land grab matters so much: whoever captures the consumer's device today may hold their consumable spend for years. It is also why JT's second-place device position is more dangerous than a second-place cigarette brand would be.

Process Power (High). This is JT's most distinctive and least replicable advantage — the Geneva autonomy model. The ability to acquire foreign tobacco businesses and run them without crushing their operating cultures is a genuine organizational capability built over 25 years and two landmark deals. Competitors cannot simply copy it; it is embedded in how JT is structured and governed.

Cornered Resource (High). Legal tobacco manufacturing licenses, entrenched distribution rights, and grandfathered market positions in tightly regulated countries function as near-absolute barriers. You cannot start a new global cigarette company today; the regulatory door is bolted shut. JT sits on the inside of that door.

Porter's Five Forces of the tobacco oligopoly

Threat of new entrants: near zero. Comprehensive advertising and marketing bans, plain-packaging regimes, and brutal regulatory approval hurdles make it effectively impossible for a new player to build brand awareness and scale. The very rules meant to shrink the industry also fossilize the incumbents' dominance — a regulatory moat that no amount of capital can breach.

Bargaining power of buyers: low. Nicotine's addictiveness and the historical price-inelasticity of demand mean JT can push through price increases year after year to offset falling volumes. This is the mechanical source of the pricing power visible in the financials.

Competitive rivalry: a tale of two industries. In combustibles, the Big Four behave like a peaceful oligopoly, harvesting profits and competing gently on price and mix. In RRPs, it is the opposite — a fierce, capital-intensive, zero-sum war for the device ecosystem, where JT and PMI are burning cash to win consumers who will be worth a fortune if retained. The same company therefore lives in two competitive climates at once: a calm cash-harvest and a knife-fight.

The synthesis for investors is this. JT's powers in the combustible business are formidable, durable, and largely intact — which is why the cash keeps coming and the dividend looks safe on a multi-year view. But every one of those powers is anchored in a declining category. The powers that matter for the future — switching costs and scale in HTPs — are exactly the ones JT does not yet clearly own, because PMI got there first. The bull case is that JT's process power and cash flow let it buy its way to parity over time. The bear case is that it is deploying strong old moats to defend a fortress while losing the battle for the new territory. That tension is the whole investment, and it is time to test it directly.

X. Analysis & Bear vs. Bull Case

Assessing management credibility

Leadership at JT turned a page as 2026 began. On January 1, 2026, 筒井岳彦 Takehiko Tsutsui took over as President and CEO, succeeding 寺畠正道 Masamichi Terabatake, who moved to the board.1314 The choice is itself a strategic signal. Tsutsui was an Executive Vice President at JT International in Geneva, with a background weighted toward business development and RRP strategy — a JTI man, a global-operations man, elevated at the precise moment the company's future hinges on winning the RRP war.13 A company that puts its heated-tobacco strategist in the top job is telling you where it believes the battle will be decided. The appointment was ratified at the annual general meeting on March 25, 2026, with 岡本秀朗 Shigeaki Okamoto moving up to chairman.1314

On credibility, the evidence is genuinely mixed, and honesty requires holding both sides. In JT's favor: the RRP KPIs have moved in the direction management promised, the Shionogi divestment followed through on a focus narrative rather than just talking about it, and the Vector deal fits the stated hard-currency logic cleanly. Management has also been willing, on recent calls, to acknowledge that it lost the early HTP category lead rather than spin it away.5 Against JT: the company was demonstrably slow and complacent when IQOS arrived — a strategic miss of the first order — and its 2028 RRP break-even target is a promise, not yet an achievement. The right posture is to grant management its recent execution while withholding judgment on the biggest claim until the numbers prove it.

The skeptical investor's stress test

A hard-nosed long/short investor would press on two pressure points, and both are real. First, the trapped-cash threat: if roughly a third of operating profit is earned behind Russian and Iranian capital controls, and JT is funding its 75% payout partly with Japanese debt to bridge the gap, how long can that continue before credit-rating agencies grow uncomfortable and the cost of that debt rises?16 The dividend's safety depends not just on earnings but on the convertibility of those earnings into distributable cash — a subtlety the headline yield conceals.

Second, the RRP-lag challenge already raised: spending ¥450 billion to reach a 15.5% domestic HTP share against PMI's entrenched lead may be less a comeback than a subsidy for permanent second place.415 An activist would want to see the unit economics of every incremental point of share, and proof that the path to 2028 profitability is real rather than aspirational.

The risk radar

The material risks are specific, not generic. Regulatory: excise-tax shocks and the ever-present threat of restrictions on HTP flavors or sticks, which could kneecap the very growth engine JT is banking on. Geopolitical: eventual nationalization or terminal devaluation of the Russian business, which would sever a load-bearing profit stream and force a reckoning with the dividend. Capital allocation: the multi-decade Canadian settlement acting as a standing claim on future cash, constraining opportunistic M&A. And execution: the ordinary but real risk that a global device rollout across 40 markets simply proves harder, slower, and less profitable than the plan assumes.

The bull case

The bull sees a fortress with a state guarantee. A high, stable dividend yield — in the mid-to-high single digits — underwritten by pricing power in combustibles and, implicitly, by a Ministry of Finance that owns a third of the company and needs the payout.3 Ploom X and AURA are showing genuine traction, with a credible line of sight to self-sustaining RRP profitability by 2028.15 The combustible business, now supercharged by Vector's US cash flows, remains an elite harvesting engine. In this reading, the ESG discount and geopolitical fear have simply made a superb cash machine cheap.

The bear case

The bear sees the Kodak of nicotine. In this reading, JT never breaks PMI's HTP network effects and switching-cost advantage, and is left holding a premium but structurally terminal combustible business while pouring capital into a category where it is a permanent runner-up. Layer on a geopolitical shock that severs the Russian profit pipeline, and the dividend — the entire reason to own the stock — comes under real pressure. In this version, the high yield was never a bargain; it was an accurate warning.

The honest verdict is that both cases are internally coherent and rest on the same facts read through different lenses. The deciding variable is knowable, and it is singular: whether JT's RRP economics inflect from cash-burn to cash-generation on something like the promised timeline. Watch that, and you are watching the whole thesis.

XI. Epilogue

Return, one last time, to the two images from the beginning — the finance-ministry official watching the dividend line, and the Geneva operator chasing global share. In 2026, both are watching the same man.

Takehiko Tsutsui inherited a company that has already performed one of the great escapes in corporate history — turning a Meiji-era tax bureau into a global tobacco power through the sheer audacity of the RJR and Gallaher gambles and the quiet genius of the Geneva model. His task is to perform a second escape, harder than the first: to convert that combustible empire into a genuinely smoke-free nicotine business before the domestic chimney cools and before geopolitics or regulation forces the issue. He must do it while wearing the golden handcuffs — feeding a 75% payout the sovereign expects, servicing a multi-decade Canadian liability, and managing a third of his profits trapped behind hostile borders.

The enduring lesson of Japan Tobacco is the one it learned in the 1990s and has re-learned in every chapter since: when your core business faces terminal decline, decentralization and aggressive M&A can buy you decades of survival — but they cannot, by themselves, win you the future. Winning the future requires being early, and being early is the one thing this cautious, sovereign-anchored, brilliantly adaptive company has repeatedly failed to be. Whether it can be early enough this time, in the RRP war it is currently fighting from second place, is the question that will decide whether the sovereign chimney keeps smoking — or finally goes cold.

References

-

JT Group 2025 Financial Results (Earnings Report) — Japan Tobacco International, 2026-02-12 ↩↩↩↩↩↩↩↩↩

-

Japan Tobacco FY2025 slides: record results driven by pricing power and RRP growth — Investing.com, 2026-02 ↩↩

-

JT Q3 2025: Revenue +18%, Profit +30%, RRP Volume +40%, Guidance Up — 2FIRSTS, 2025 ↩↩↩

-

Earnings call transcript: Japan Tobacco sees growth in Q3 2025 — Investing.com, 2025 ↩↩↩↩

-

JT Group to Acquire Vector Group Ltd. for $2.4 Billion — Business Wire, 2024-08-21 ↩

-

Japan Tobacco to Acquire Vector Group — Tobacco Reporter, 2024-08-21 ↩

-

Vector Group Ltd. Form SC TO-T/A (tender offer results) — U.S. Securities and Exchange Commission, 2024-10 ↩

-

Ontario court approves major $32.5B tobacco settlement — CBC News, 2025-03-06 ↩↩↩

-

Ontario court approves historic $32.5-billion tobacco settlement — The Globe and Mail, 2025-03-06 ↩↩

-

JTI-Macdonald CCAA Creditor Protection Proceedings Portal — JTI-Macdonald Corp. ↩

-

Japan Tobacco International — Tobacco Tactics, University of Bath ↩↩↩↩↩↩↩↩

-

JT Announces New Executive Appointments — Japan Tobacco Inc., 2025-11-25 ↩↩↩

-

JT Announces Board, Leadership Changes — Tobacco Reporter, 2025-11-26 ↩↩

-

Japan Tobacco Investing Heavy on RRPs — Tobacco Reporter, 2025-01-27 ↩↩↩

-

Geopolitical risk and trapped cash in Russia/Iran — S&P Global Ratings, 2025-09-12 ↩↩

-

Japan, the World's Most Dynamic HTP Market — Tobacco Asia ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube