CTBC Financial Holding: The Empire of Taiwan's Elite Banking Dynasty

I. Introduction & Episode Roadmap

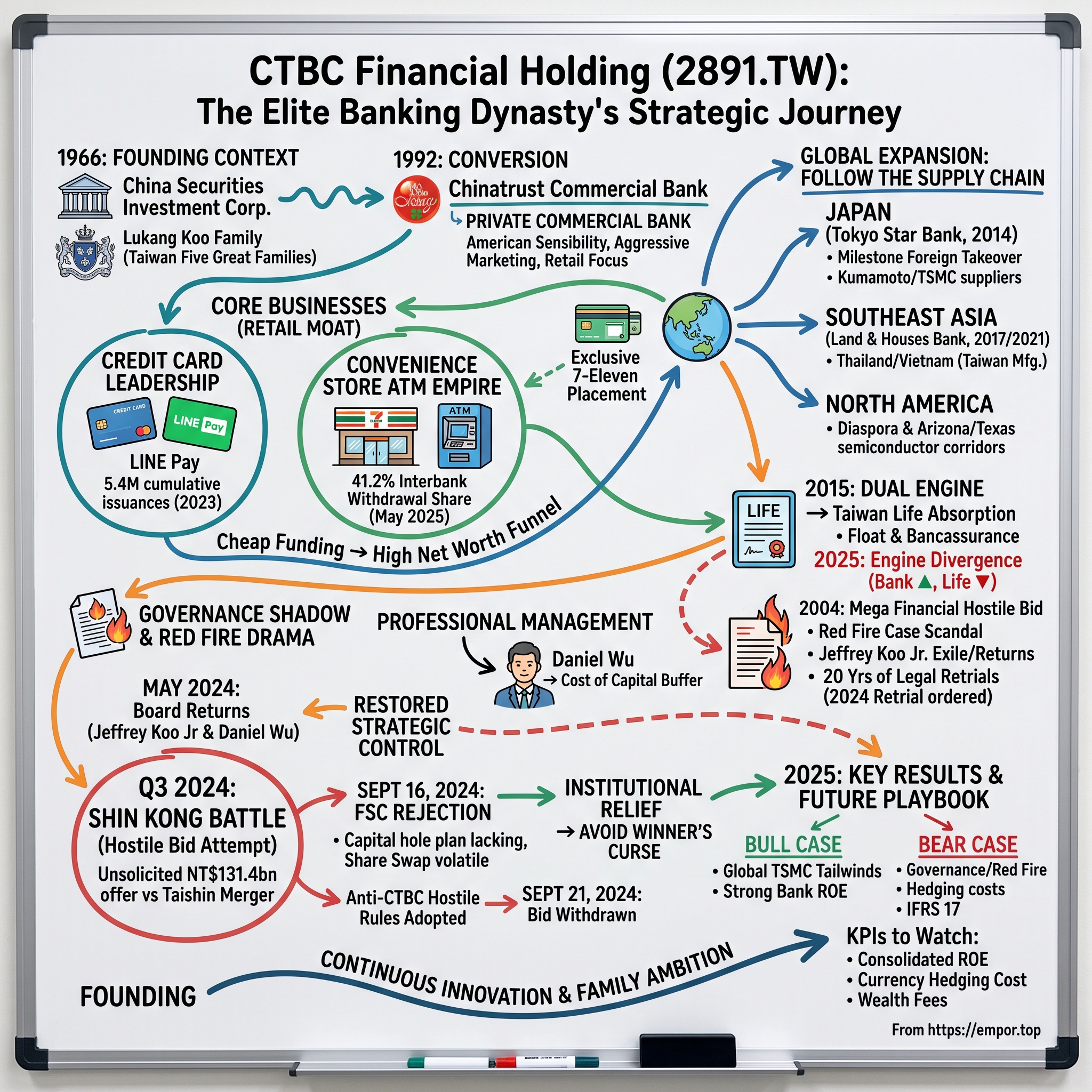

On the afternoon of August 23, 2024, the financial establishment of Taipei got the kind of jolt it had not felt in a generation. 中國信託金融控股公司 CTBC Financial Holding (2891.TW, listed on TAI) announced, without warning and without invitation, that it intended to buy 51% of a rival — 新光金融控股公司 Shin Kong Financial Holding — for NT$131.4 billion, roughly US$4.1 billion, in a mix of cash and its own shares.1 In a market where deals are traditionally arranged over long lunches and blessed by regulators before a word leaks, this was something close to heresy: an unsolicited, openly hostile tender offer, the largest ever attempted in Taiwan.

The timing was surgical. Only the day before, Shin Kong's board had approved a friendly, all-stock merger with 台新金融控股公司 Taishin Financial Holding. CTBC's bid — pitched at NT$14.55 per Shin Kong share, roughly a 28% premium to Taishin's offer — was designed to blow that agreement apart.1 Had it succeeded, it would have stitched together a financial group with something on the order of NT$13.6 trillion in assets, vaulting past the two reigning giants, 富邦金融控股公司 Fubon Financial Holding and 國泰金融控股公司 Cathay Financial Holding, to become the largest financial conglomerate in the country.2

To understand why this was such a thunderclap, you have to understand who had just walked back into the room. Three months earlier, in May 2024, the de facto patriarch of CTBC's founding family, 辜仲諒 Jeffrey Koo Jr., and the group's most respected professional manager, 吳一揆 Daniel Wu, had rejoined the board — Koo as a director, Wu as a director and group vice chairman.3 Their return was itself a story, because for two decades Koo's name had been shadowed by the 紅火案 Red Fire case, the defining white-collar scandal of modern Taiwanese finance. The Shin Kong bid read, to almost everyone watching, as their opening statement: the family was back, and it was hungry.

Then the twist. On September 16, 2024, the 金融監督管理委員會 Financial Supervisory Commission (FSC) — Taiwan's banking and insurance regulator — rejected the bid outright.5 It objected to the hostile structure, to the use of a volatile share swap, and, most pointedly, to the fact that CTBC had no concrete plan to plug the capital hole inside Shin Kong's troubled life-insurance arm.6 And here is the part worth sitting with: instead of falling on the news that its grand ambition had been blocked, CTBC's stock did fine. Institutional investors, it turned out, were quietly relieved. They had run the math and concluded that "winning" Shin Kong might have been the more expensive outcome.

That reaction is the whole puzzle of CTBC in miniature. This is a company that generated a record consolidated net profit of NT$80.6 billion in 2025, with a return on equity of roughly 16.9% — the highest among Taiwan's financial holding companies.7 It is a business so profitable and so disciplined that its own shareholders cheered when regulators stopped its chairman from making it bigger. How did a modest securities firm founded by an aristocratic family in 1966 become that machine? And can a machine that good resist the empire-building instincts of the family that controls it?

There is a further layer of context that makes the puzzle richer. Taiwan's financial sector is one of the most overcrowded in the developed world — more than a dozen financial holding companies fighting over a market of roughly 23 million people, a density that guarantees thin margins and perpetual pressure to consolidate. For two decades, successive governments have wanted fewer, stronger, more globally competitive banks, and for two decades the consolidation has crept forward at a glacial pace, snagged on family egos, regulatory caution, and the political sensitivity of putting state-linked institutions into private hands. Against that backdrop, CTBC's 2024 raid was not just a bid for one company; it was a test of whether the whole logjam could be broken by force rather than consensus — and the answer, delivered by the regulator, was no. Understanding why requires understanding how CTBC itself was built.

Here is the roadmap. First, the origin story — the 鹿港辜家 Lukang Koo family, one of Taiwan's "Five Great Families," and the founding of what became CTBC Bank. Second, the retail moat: credit cards, wealth management, and the almost absurdly effective decision to put an ATM inside nearly every 7-Eleven in Taiwan. Third, the global build-out that followed Taiwan's semiconductor champions to Japan and Southeast Asia. Fourth, the "second engine" — the 2015 absorption of 台灣人壽 Taiwan Life and the double-edged economics of pairing a bank with a life insurer. Fifth, the Red Fire drama and the strange governance arrangement it produced. Sixth, the anatomy of the 2024 takeover battle. And finally, the playbook, the bull-and-bear stress test, and the handful of numbers that actually matter.

II. The Lukang Koo Dynasty & Chinatrust's Founding Context

To find the roots of CTBC, drive south out of Taipei to Lukang, a small port town on Taiwan's west coast that was, in the late Qing dynasty, one of the island's great commercial harbors. It was there that the Koo family rose — first as merchants and salt traders, then, under Japanese colonial rule from 1895, as one of the small handful of Taiwanese clans the colonial administration allowed to prosper. By the twentieth century the "Koos of Lukang" had become what Taiwanese still call one of the island's 台灣五大家族, the Five Great Families: dynasties whose wealth and political reach straddled every regime change, from Qing to Japanese to Nationalist rule.

What made the Five Great Families distinctive was not merely money but survival — the rare capacity to remain elite across ruptures that wiped out lesser fortunes. The Koos had thrived under Japanese rule, which left some Taiwanese families politically radioactive when the Nationalist government arrived after 1945 and the island convulsed through the trauma of the late 1940s. Yet the Koos re-emerged, cultivating the incoming Kuomintang establishment as adeptly as they had the colonial one. That talent — the ability to stay close to whichever authority held the levers, without ever being wholly captured by it — is the family's deepest inheritance, and it explains a great deal about how a bank they controlled could later navigate regulators, scandals, and regime-defining political shifts without losing its footing.

The modern family produced two towering, complementary figures. The elder statesman was 辜振甫 Koo Chen-fu, who took the reins of Taiwan Cement in 1973 and built the Koos Group into an industrial pillar — but who is remembered above all for a single week in 1993, when, as chairman of the Straits Exchange Foundation, he sat across a table in Singapore from a mainland Chinese counterpart in the 辜汪會談 Koo-Wang Talks, the first formal cross-strait negotiations since 1949. Koo Chen-fu was the family's diplomat, the man who lent the Koo name a quasi-statesman's gravity.

The financier was his younger cousin, 辜濂松 Jeffrey Koo Sr., and he is the one whose fingerprints are on CTBC. A Wharton-trained banker with the manners of a diplomat and the instincts of an empire-builder, Koo Sr. spent decades doubling as Taiwan's roving "ambassador-at-large," using a private banker's Rolodex to conduct the economic diplomacy that a diplomatically isolated Taiwan could not conduct through embassies it did not have.10 When he died in New York in December 2012 at the age of 79, the obituaries described a man who had turned a family trust business into a financial dynasty and, along the way, made himself one of the most globally connected Taiwanese of his era.10

The institution itself began in 1966 as China Securities Investment Corporation, a securities and investment house — notable because, at the time, Taiwan simply did not permit privately owned commercial banks. The banking system was a state affair: a cluster of government-owned banks that lent conservatively against heavy collateral, served state-favored industries, and treated the ordinary consumer and the small business owner as afterthoughts. Renamed Chinatrust Investment Company in 1971, the firm spent a quarter-century as a trust and investment operation, learning the credit business in the cracks left by the state banks — precisely the retail and small-enterprise customers the incumbents ignored.

It is worth dwelling on what a "trust and investment company" actually was in that era, because it shaped the DNA of everything that followed. In an economy where the state banks hoarded the deposit franchise and lent it out along politically safe channels, a trust firm occupied the riskier, more entrepreneurial edge of finance — pooling savings, arranging installment credit, financing the small manufacturers and traders who powered Taiwan's export miracle but who could never satisfy a state bank's collateral demands. Chinatrust spent a quarter of a century in that school, learning to underwrite borrowers on the basis of cash flow and character rather than land deeds. When consumer credit and the credit card finally arrived, the firm already possessed the one thing incumbents lacked: an actual culture of pricing and managing unsecured retail risk at scale. That accumulated skill, more than any single product, was the true head start.

The hinge moment came in the early 1990s, when Taiwan finally liberalized its financial sector and allowed private commercial banking. In 1992, Chinatrust converted into Chinatrust Commercial Bank, and the head start showed immediately. While brand-new private banks were still writing their first loan policies, Chinatrust already had decades of consumer-credit experience and a culture oriented toward service rather than bureaucracy. It imported an American sensibility — aggressive marketing, dedicated customer service, professionalized risk management — into a market that had never seen it, and it grew fast.

Two principles set in those early decades still describe the company today. The first is an obsessive focus on the retail consumer and the underserved small-to-medium enterprise — the customers the state banks left on the table. The second is an internationalist reflex: from Koo Sr.'s ambassador years onward, the institution saw itself as the financial bridge for Taiwanese capital moving out into the world. Hold both of those threads. They lead directly to the two moats that make CTBC what it is — and the first of them was built, of all places, inside a convenience store.

III. The Retail Moat: Credit Cards, ATMs, and the 7-Eleven Empire

Walk into almost any 7-Eleven in Taiwan — and in a country of 23 million people there are more than 6,000 of them — and somewhere near the counter you will find an ATM. Look at the logo. It is, with near-total consistency, CTBC's. That mundane detail is one of the most quietly powerful competitive advantages in Asian banking, and to understand why, you first have to understand where CTBC makes its money.

The banking subsidiary, CTBC Bank, is the crown jewel of the group. It is the largest privately owned bank in Taiwan, with consolidated assets of about NT$6.47 trillion at the end of 2024 and a network of more than 370 outlets spread across 14 countries and territories.11 More to the point, it is the engine: in 2025 the bank generated NT$57.3 billion of the holding company's NT$80.6 billion consolidated net profit — a little over 70% — after contributing NT$49.4 billion of NT$72.0 billion the year before.78 Whatever else CTBC is, it is first and foremost a very good bank with two exceptional retail franchises bolted onto it.

The first franchise is plastic. CTBC was the first bank to issue a credit card in Taiwan, back in 1974, and it never surrendered the lead it took from being early.11 Taiwan's card market is astonishingly fragmented — 32 separate issuing institutions fighting over the same wallets — yet CTBC has stayed at or near the top for half a century, in a permanent knife-fight with Cathay United Bank and Fubon's card arm.15 Its sharpest modern weapon has been co-branding, and its instinct for partnership found its purest expression in the LINE Pay card, a tie-up with the messaging app that dominates Taiwanese daily life. By 2023 that single co-branded card had racked up about 5.4 million cumulative issuances, making it the most-issued credit card in the country.14

The knife-fight for card supremacy is worth lingering on, because it reveals how CTBC actually competes. In a market splintered across so many issuers, no single player can dominate on interchange economics alone; the winners are the ones who attach their card to something consumers already love and use daily. CTBC's answer has been to rent other companies' brand affection — the messaging app, airline programs, retail chains — rather than rely solely on its own. Cathay United Bank and Fubon's card arm play the same game, and the three of them trade the top spot back and forth as each lands or loses a marquee co-brand partner. This is a business where the moat is shallow at the level of any single card but deeper at the level of the ecosystem: the issuer with the widest, stickiest set of partnerships and the best cross-sell machinery wins the war of attrition even as it loses individual skirmishes. The risk, worth naming, is that co-branding cuts both ways — the partner owns the customer's affection, and if a giant like the LINE ecosystem ever decided to issue through its own bank rather than through CTBC, the co-brand advantage could evaporate as quickly as it was rented.

Why does a bank fight so hard for a business as commoditized as credit cards? Because the card is not the product; it is the funnel. Each cardholder is a merchant-fee stream and, more valuably, a warm lead — a customer whose spending data CTBC can mine to cross-sell mortgages, insurance, and, above all, high-margin wealth-management products. The card is the cheap top of a funnel whose bottom is a fee-earning private-banking relationship.

The second franchise — the 7-Eleven ATMs — is the more remarkable of the two, because it is a textbook example of what the strategist Hamilton Helmer calls a "cornered resource." CTBC secured an effectively exclusive arrangement to place its machines inside 7-Eleven Taiwan, operated by 統一超商 President Chain Store Corp. Of CTBC's roughly 5,777 machines in one recent tally, about 5,100 sat inside those convenience stores, and the footprint has since grown past 7,600 nationwide.13 The payoff shows up in the interbank data: as of May 2025, CTBC accounted for 41.2% of all interbank ATM withdrawal transactions in Taiwan — the single largest share by a wide margin.9

Here is the mechanism that makes this matter, explained plainly. A bank's profit is, at its core, the spread between what it pays for money (deposits) and what it earns lending that money out. The cheapest possible money is a checking or savings balance that sits there paying almost no interest. Customers keep those low-yield balances at whichever bank makes their daily life easiest — and in Taiwan, a CTBC ATM is on nearly every corner, open 24 hours, inside the store where people already buy coffee and pay their utility bills. That convenience is sticky in a way interest rates are not, and it hands CTBC an unusually cheap, unusually stable deposit base. When your funding is cheaper than your rivals', you can either lend more profitably or price more aggressively, and CTBC does both.

Layered on top is wealth management. In the early 2000s CTBC was among the first in Taiwan to put dedicated 理財專員 financial advisors in front of ordinary retail customers, professionalizing what had been an ad-hoc business. Today that operation is a substantial recurring-fee engine, insulated from the swings of interest rates because it is paid on assets and transactions rather than on spreads — though the group does not publicly break out a precise market share, and claims about its exact standing in high-net-worth banking should be treated as positioning rather than audited fact.

The distinction between fee income and spread income is worth making concrete, because it sits at the heart of why CTBC earns the returns it does. A bank that lives on spread income is at the mercy of the interest-rate cycle: when central banks cut, the gap between deposit costs and loan yields compresses, and profits sag through no fault of management. Fee income — the commissions on selling a mutual fund, an insurance policy, or a structured product, plus the recurring management fees on assets under advice — behaves differently. It scales with customer wealth and activity rather than with the rate environment, and it consumes very little of the bank's own capital. A dollar of fee income is therefore worth more than a dollar of spread income, because it is both steadier and cheaper to produce. The strategic prize of the card-and-ATM machine is that it manufactures the raw material — mass affluent customers and their transaction data — that a wealth business converts into exactly this higher-quality income.

There is a genuine threat to guard against, and management does not get to wave it away. Taiwan licensed a new breed of pure-digital, branchless banks in recent years — most visibly LINE Bank, backed by the same messaging platform whose card CTBC co-brands, alongside Rakuten and Next Bank. Their pitch is precisely to dissolve the convenience advantage that physical ubiquity confers: if your phone is your branch, who needs an ATM inside a 7-Eleven? So far these entrants have won accounts at the thin, price-sensitive edge of the retail market rather than the profitable core, and they have struggled to reach the scale and cross-sell depth of an incumbent. But the direction of travel is real, and the honest read is that CTBC's funding moat is durable today and slowly contestable tomorrow. The bank's own heavy investment in its digital app and its data capabilities is best understood not as offense but as defense — an attempt to make sure the convenience that keeps deposits cheap migrates from the street corner into the customer's pocket before a challenger gets there first.

Put the pieces together and the model is elegant: cheap deposits on one side, fee income on the other, a card business feeding customers into both, and a small-and-medium-enterprise lending franchise — inherited from the trust-company years — anchoring the corporate relationships. It is a genuinely hard combination to replicate. And once CTBC had perfected it at home, the obvious question was where to point it next — and the answer, increasingly, was wherever Taiwan's semiconductor industry was going.

IV. The Global Expansion Strategy: Following the Semiconductor Supply Chain

Every ambitious Taiwanese company eventually runs into the same wall: the home market is rich but finite, an island of 23 million people that even a dominant franchise can only squeeze so hard. CTBC's answer was to follow its customers abroad — and its customers, increasingly, were the sprawling supply chain of chip-makers, materials firms, and precision manufacturers orbiting Taiwan Semiconductor Manufacturing. Where they built factories, CTBC wanted a branch.

The first move was cosmetic but revealing. In June 2013, Chinatrust rebranded its English name to CTBC, spending real money to retire a brand it had used for decades.12 Management framed it as a play for a cleaner, more internationally legible identity, in the mold of an HSBC or an SMBC, and was careful to note that CTBC was "not an abbreviation" of the old name and that the Chinese name 中國信託 would stay untouched.12 Observers read a subtext the company did not emphasize: as it globalized, a Taiwanese bank had obvious reasons to want distance from the word "China" and from confusion with mainland state institutions. Whatever the motive, the rebrand signaled intent — this was a company preparing to be seen on foreign soil.

The most consequential foreign bet came in Japan. In 2014, CTBC acquired about 98% of 東京之星銀行 The Tokyo Star Bank for roughly ¥53 billion, around US$520 million, in a deal approved by Japan's regulator that April.1617 It was a genuine milestone: the first time a foreign lender had taken full control of a Japanese commercial bank, a market famous for being nearly impenetrable to outsiders.17 At the time the logic looked shaky. Japan was mired in ultra-low, even negative, interest rates; Tokyo Star was a mid-sized, unglamorous retail bank; critics called it an expensive way to buy into a stagnant market.

Buying a Japanese bank is one thing; making it earn its cost of capital is another, and the intervening decade was not a straight line. Japan's banking market is notoriously unforgiving to newcomers: relationship-driven, low-margin, and dominated by megabanks and regional lenders with century-old ties to their corporate clients. A Taiwanese owner could not simply parachute in and win domestic Japanese business on price. For years, Tokyo Star was exactly what the critics predicted — a modestly profitable retail bank in a zero-rate economy, its acquisition premium looking like a monument to CTBC's ambition rather than its acumen. The lesson embedded in that stretch is one every acquirer should heed: a strategically sound thesis can still take a decade to pay, and the interim years will test whether management bought for a real edge or for the thrill of the deal.

A decade later, the bet looks prescient — but for a reason no one could have fully underwritten in 2014. TSMC's decision to build a massive chip-fabrication complex in Kumamoto, on Japan's southern island of Kyushu, dragged dozens of Taiwanese suppliers into a corner of Japan that had never hosted them. Those companies — and the Taiwanese engineers relocating with them — needed banking that understood both Taiwan and Japan, and Tokyo Star positioned itself squarely to provide it, extending its presence toward Kumamoto to court exactly that cross-border flow of deposits, housing loans, trade finance, and foreign-exchange business.[^18] A sleepy retail bank acquired for defensive reasons had, through no genius of the original thesis, become a strategic node in the most important supply chain on earth. It is worth being honest about that sequence: the payoff was real, but it owed as much to TSMC's geopolitics as to CTBC's foresight.

The second axis of expansion ran south, into the countries absorbing manufacturing as it diversified away from mainland China — the logic Taipei branded the 新南向政策 New Southbound Policy. The vehicle was Thailand. In July 2017, CTBC bought a 35.6% stake in LH Financial Group Holdings, the parent of Land and Houses Bank, for about THB 16.6 billion.18 Four years later, in 2021, it lifted its holding to a controlling 46.61%, taking board control and folding LHFG in as a subsidiary.19 The strategic fit was to graft CTBC's wealth-management and trade-finance capabilities onto a Thai bank historically anchored in property lending, and to bank the Taiwanese manufacturers streaming into Thailand and Vietnam. Ratings agency Fitch has continued to affirm Land and Houses Bank's national ratings on the expectation of support from its Taiwanese parent — while noting that the linkage is tempered by CTBC's sub-50% ownership, a reminder that "control" and "full support" are not the same thing.20

The third leg reaches across the Pacific. CTBC has long maintained a North American banking presence rooted in the large Taiwanese-American communities of California and, increasingly, oriented toward the same high-tech corridor its home-market clients inhabit — the arteries connecting Taiwan's chip designers and foundry customers to Silicon Valley and, now, to the wave of advanced-manufacturing investment landing in Arizona and Texas as the semiconductor supply chain reshores toward the United States. The strategic logic is identical to the Japanese and Thai chapters: bank the diaspora and the corporate flow that domestic American lenders neither understand culturally nor prioritize commercially.

What ties all three legs together is a single, disciplined idea: CTBC does not try to out-compete local giants on their home turf. It attaches itself to a flow it already understands — Taiwanese corporate capital moving abroad — and monetizes the cross-border seam that domestic banks are poorly equipped to serve. It is a niche strategy, not a land-grab, and its ceiling is set by how far and how fast Taiwan's champions keep expanding.

There is a discipline test buried in this record that investors should apply skeptically. "Follow the client" is a seductive slogan, and it has a long history of leading banks into expensive foreign misadventures — buying assets at the top of a cycle, underestimating local competition, discovering that cross-border synergies are easier to draw on a slide than to bank. Tokyo Star was openly criticized as overpriced for a decade before geopolitics rescued the thesis; the LH Financial stake sits below the 50% threshold that would let CTBC fully consolidate its economics and support. The pattern that separates genuine strategy from empire-building is whether each foreign platform earns its keep on a standalone basis or merely flatters the group's growth narrative. So far CTBC's overseas franchise has looked more disciplined than most — small, targeted, tied to a real customer flow rather than to ambition for its own sake. That same appetite for scale, though, would soon push CTBC toward a very different kind of expansion at home: not a branch network, but a second business entirely.

V. The Dual-Engine Engine: Consolidating Taiwan Life (2015)

By the early 2010s, CTBC's leadership faced an uncomfortable structural truth about Taiwanese finance. After the Financial Holding Company Act of 2001 permitted banks, insurers, and securities firms to sit under one corporate roof, the market's center of gravity shifted decisively toward the groups that owned both a bank and a large life insurer. Cathay and Fubon had built exactly that pairing, and it gave them a scale of investable assets — the insurance "float" — that a pure-play bank simply could not match. CTBC was a superb bank without a second engine, and in Taiwan's competitive league table, that increasingly looked like a Ferrari with only one cylinder firing.

The fix was Taiwan Life. In 2015, CTBC acquired 100% of 台灣人壽 Taiwan Life in a share-swap deal valued at about NT$32.35 billion, roughly US$1.05 billion, completing the transaction that October and merging it with the group's own small insurance operation.2122 Overnight, CTBC had its dual engine: a fee-and-spread banking business paired with a balance-sheet-heavy life insurer that could gather premiums and deploy them across global markets.

The appeal of a life insurer, in the abstract, is the "float" — a concept worth explaining simply, because it is what makes insurance so attractive to empire-builders and so dangerous to the undisciplined. When a customer buys a long-dated life policy, they hand the insurer premiums today in exchange for a promise the insurer may not have to honor for decades. In the meantime, the insurer gets to invest that pile of other people's money. If it invests well and prices its policies correctly, the float is a nearly free source of investable capital — the mechanism that made fortunes for the great insurance-backed conglomerates. That is the dream CTBC bought into: a bank that gathers cheap deposits, bolted to an insurer that gathers cheap float, both feeding an investment machine.

The nightmare version is what Taiwan's insurers have been living through, and it flows from the same float turned against them. If you promise policyholders a fixed return and then interest rates fall, your investment income no longer covers your promises. If your policies are denominated in US dollars but your reporting currency is the New Taiwan dollar, every twist in the exchange rate reprices your entire balance sheet. The float, in other words, is only free if the assets behind it behave — and for Taiwanese life insurers stuffed with foreign bonds, they frequently do not.

The economics of that pairing are best understood by watching the two engines behave differently under the same conditions. In 2024, CTBC's consolidated profit jumped 28% to a then-record NT$72.0 billion, and a striking share of the surge came from insurance: Taiwan Life's contribution leapt about 73% to roughly NT$21.5 billion, riding a buoyant equity market that inflated its investment gains.8 In 2025, the pattern inverted. The bank powered ahead — up 16% to NT$57.3 billion — while Taiwan Life slipped about 3% to NT$20.8 billion even in a rising market, dragged by the costs of managing its currency exposure.7 Same company, same two years, two engines pulling in different directions. That is the dual-engine model in a single frame: the insurer amplifies good years and can sandbag them too.

The reason lies in a peculiarly Taiwanese problem. Taiwanese households buy enormous quantities of long-dated, often US-dollar-denominated insurance policies, which forces life insurers like Taiwan Life to invest heavily overseas — mostly in US bonds and equities — to match those liabilities and chase yields unavailable at home. That leaves them holding a mountain of foreign assets funded partly by New Taiwan dollar obligations, and every time the NT dollar strengthens against the greenback, the value of those foreign holdings falls in local terms. To blunt the swing, insurers pay to hedge their currency exposure, and those hedging costs can balloon precisely when exchange rates get volatile — quietly eating the investment gains the headlines celebrate.

The theoretical upside of owning both a bank and an insurer is "bancassurance" — the idea that a bank branch is the cheapest place on earth to sell an insurance policy, because the customer is already there, already trusts the institution with their money, and can be sold a savings-style life product across the same counter where they opened a deposit account. For CTBC, the wealth-management advisors who sell mutual funds can also steer clients toward Taiwan Life policies, and the insurer gains a distribution channel it would otherwise have to build from scratch or rent from agents. When it works, it lowers the insurer's customer-acquisition cost and deepens the bank's share of each household's financial life. The honest caveat is that bancassurance synergies are among the most over-claimed benefits in all of financial-conglomerate empire-building; they are real but rarely as large as the deal announcements promise, and they do nothing to solve the insurer's core problem, which is on the asset-and-hedging side, not the sales side.

Regulators have been rewriting the rules of this game in real time, which matters enormously for the sector's future. Through 2025, the FSC moved to give life insurers more flexibility in smoothing foreign-exchange gains and losses, while pushing them to channel the savings from cheaper hedging into a bigger foreign-exchange volatility reserve — a buffer the industry's regulators projected could swell from around NT$300 billion toward as much as NT$960 billion, with new amortized-cost accounting provisions phasing in from 2026.30 The subtext is an industry-wide transition to the IFRS 17 accounting standard and the Insurance Capital Standard, and it deserves a plain-English explanation because it is quietly reordering the whole sector. For years, insurers could book a policy in ways that let optimistic assumptions flatter today's earnings while the true cost of long-dated promises stayed politely offstage. IFRS 17 drags those promises onto the balance sheet at something closer to their honest economic value, and the accompanying capital standard demands that insurers hold a thick cushion of capital against them. The effect is to reveal, in hard numbers, which insurers made promises they cannot comfortably fund — and to require the weak ones to raise fresh capital to close the gap.

For Taiwan's financial holding companies, this transition threatens to turn life insurers from reliable cash cows into potential capital sponges — subsidiaries that need feeding rather than milking. A parent that owns a healthy insurer can absorb the change; a parent that acquires a sick one may find itself pouring shareholder capital into a black hole just to keep it compliant. That single dynamic — the difference between buying float and buying a future capital call — sat at the dead center of the Shin Kong battle, and it is why CTBC's shareholders were so uneasy about the target's ailing life arm. But first, we have to reckon with the long shadow the founding family cast over the whole enterprise.

VI. The Red Fire Drama & The Koo Family Shadow (2004–2024)

In 2004, CTBC — then still Chinatrust — set its sights on a prize that would have transformed it: 兆豐金融控股公司 Mega Financial Holding, a large, state-controlled financial group. What happened next became the most notorious corporate scandal in modern Taiwanese finance, and it would haunt the Koo family for the next twenty years.

The mechanics were baroque. To build a stake in Mega, CTBC Bank purchased around US$390 million of structured notes from Barclays whose value was tied to Mega's shares. Those notes were then sold, in a non-arm's-length transaction, to an offshore shell company registered in the British Virgin Islands and operating out of Hong Kong — a paper entity capitalized at a single US dollar, set up on the instruction of Jeffrey Koo Jr., and given the almost cinematically ominous name "Red Fire Development."424 When the trade paid off, roughly NT$1 billion in profit landed not with CTBC's shareholders but with Red Fire. Prosecutors alleged this was straightforward looting: the company had taken the risk and the insiders had pocketed the reward. Investigators further alleged that some NT$27.5 billion of funds had been used to buy a 9.9% stake in Mega without proper board approval, and a 2006 indictment put the illegal profit as high as NT$1.3 billion.24

The fallout was swift and personal. In July 2006, Jeffrey Koo Jr. resigned his chairmanship of the banking arm, and by that November he had left Taiwan altogether, spending time in Japan among other places — an exile that, to his critics, looked like flight from prosecution and, to his defenders, like a man stepping back from a business he had endangered.25 He returned to Taiwan in late 2008 to face the courts, and thus began one of the longest legal odysseys in Taiwanese corporate history.26

Trace the timeline and you get a sense of just how unresolved this all remained. In 2010, the Taipei District Court found the defendants guilty and sentenced Koo to nine years; on appeal in 2013, the High Court raised that to nine years and eight months. In 2014, the Supreme Court ordered a retrial. Then, in a dramatic reversal in April 2021, the High Court acquitted Koo of the major charges, and in December 2023 it again found him not guilty of breach of trust, money laundering, and stock manipulation.24 Vindication, it seemed — until September 2024, when the Supreme Court overturned that acquittal on the breach-of-trust count, faulted the lower court's reasoning, and sent the case back down yet again.4 Two decades on, the Red Fire case still had no final answer, and a permanent asterisk still hung over the man now steering the company.

Step back from the legal minutiae and the Red Fire case tells you something structural about family capitalism in Taiwan — and about the peculiar tension at the core of a listed company controlled by a dynasty. The alleged scheme, whatever a final court eventually decides, was a textbook example of the conflict that haunts every family-controlled public company: the risk that those who control the enterprise will treat its resources as an extension of the family's private balance sheet, capturing for themselves gains that belong to all shareholders. This is not a uniquely Taiwanese failing; it is the oldest problem in corporate governance. But it lands with particular force in a market where a handful of families sit atop sprawling financial groups, where independent directors have historically been deferential, and where minority shareholders have limited practical recourse. The enduring question CTBC poses is not whether the alleged conduct was proven — the courts have spent twenty years failing to settle that — but whether the governance guardrails that are supposed to prevent such conduct were ever strong enough.

This produces the central paradox of CTBC's governance. How did the institution not merely survive but thrive — building world-class franchises, executing complex cross-border acquisitions, maintaining pristine credit ratings — while its most powerful owner was, for years at a stretch, either abroad or on trial? The answer is a name: 吳一揆 Daniel Wu. A career professional manager, Wu ran CTBC as president and later vice chairman across roughly two decades until his retirement in 2021, and it was on his watch that the group institutionalized its risk management and pushed through the Tokyo Star and Taiwan Life deals.23 To international institutional investors and rating agencies, Wu was the credible, technocratic face that let them look past the family drama — the buffer between the Koo name's legal jeopardy and CTBC's cost of capital.

Which is what made May 2024 so significant. That month, Jeffrey Koo Jr. rejoined the board as a director, and Daniel Wu returned alongside him as director and group vice chairman — the professional manager brought back to legitimize the founder's return.3 Around the same time, 高麗雪 Rachael Kao, previously the group's chief of staff, was elevated to president of the holding company. The arrangement was unmistakable: the Koo family would once again hold the strategic controls, with a bench of respected managers executing the day-to-day and reassuring the outside world. It was, in effect, a restoration — and a carefully choreographed one. Elevating a seasoned insider like Rachael Kao to the presidency and pairing the returning founder with the most trusted professional manager in the group's history sent a deliberate signal to rating agencies and institutional holders: continuity of governance, not a lurch back to the freewheeling family control of the pre-scandal era. Whether that signal holds is a matter of behavior, not org charts. The genuine test of a "dual structure" is what happens when the family's strategic ambition collides with the managers' financial discipline — and investors would not have to wait long to see the first collision, because it arrived within the quarter. And a restored, ambitious family owner with a professional manager at his side does not come back to run things quietly. Within three months, CTBC launched the most aggressive takeover attempt in Taiwanese history.

VII. The 2024 M&A Battle: The Hostile Bid for Shin Kong Financial

To appreciate the drama, start with the target's troubles. Shin Kong Financial had spent years as a cautionary tale — weak profitability, a boardroom torn by feuding among its founding families, and, most damaging of all, a life-insurance subsidiary staring at a serious capital shortfall as the IFRS 17 and capital-standard deadlines loomed. It was a wounded animal, and in August 2024 the wounded animal agreed to be rescued. On August 22, Shin Kong's board approved a friendly, all-stock merger with Taishin Financial, itself controlled by a different branch of the Wu family — an orderly, regulator-friendly consolidation of the kind the FSC prefers.1

One day later, CTBC kicked over the table. Its unsolicited NT$131.4 billion tender offer for 51% of Shin Kong dangled NT$14.55 per share — NT$4.09 in cash plus a swap of 0.3132 CTBC shares — a package worth roughly 28% more than what Taishin was offering.1 For Shin Kong's beleaguered shareholders, it was a windfall. For Taishin, it was an ambush. And for the market, it was the clearest possible signal that the newly restored Jeffrey Koo Jr. and Daniel Wu intended to pursue outright domestic dominance: a combined CTBC–Shin Kong would have topped NT$13.6 trillion in assets, edging past Cathay's NT$13.3 trillion and leaving Fubon's NT$11.8 trillion behind.2

There was a cultural dimension to the shock that is easy for outside observers to miss. Hostile takeovers are the ordinary weather of American and British capital markets — unwelcome bids, proxy fights, and bidding wars are how public companies routinely change hands. In Taiwan, they are close to taboo. Deals are supposed to be negotiated, boards are supposed to bless them, and regulators are supposed to be consulted before the public ever hears a word. By launching an uninvited, premium bid designed to break a signed agreement, CTBC was not merely competing; it was importing a foreign combat style into a market whose unwritten rules forbade it. That it was two branches of the extended Wu family — Taishin's controlling family and CTBC's own Daniel Wu — on opposite sides only heightened the sense that something unusually raw was playing out. The bid forced a question the market had never really had to answer: was a hostile takeover of a Taiwanese financial institution even permissible?

Then the referee blew the whistle. On September 16, 2024, the FSC rejected CTBC's application, and its reasoning was a clinic in why regulators exist.5 First, the commission said, CTBC had shown a troubling lack of understanding of the actual financial condition of Shin Kong Life — the very unit whose capital hole was the whole problem — and had not committed to the capital injections that unit would need.6 Second, it objected on principle to a hostile takeover financed with a share swap: if CTBC's stock price gyrated during the long tender process, the value on offer would move with it, injecting instability into the market. The FSC pointedly noted it had never approved a share swap for acquiring a bank or life insurer.6 Third, CTBC had not adequately explained how it would fund the deal or what would happen if it won some but not all of the shares it sought. Underneath the technical objections ran a plainer message: Taiwan's regulator favored orderly, consensual consolidation and had little appetite for American-style corporate raids.

CTBC pushed back, resubmitted, and was rebuffed again. On September 21, 2024, it formally withdrew, clearing the path for Taishin — which promptly sweetened its own offer by roughly a quarter, to about NT$222.4 billion, to seal the deal.27 The saga's coda came the following summer: on July 24, 2025, the Taishin–Shin Kong merger took effect, creating TS Financial Holding (台新新光金控) with around NT$8.3 trillion in assets and the rank of Taiwan's fourth-largest financial group — the largest friendly financial-sector acquisition in the country's history.28 The regulator got the tidy outcome it wanted; Taishin got Shin Kong, capital hole and all.

And CTBC? Its investors exhaled — and the phrase for what they were relieved to avoid is the "winner's curse." In any contested auction, the bidder willing to pay the most is, by definition, often the one who has most overestimated the prize; winning becomes proof that you overpaid. In a hostile takeover of a financial firm, the curse is doubled, because the acquirer cannot fully inspect what it is buying. CTBC could not open Shin Kong Life's books before bidding; it was, in effect, offering a large premium for a balance sheet it could not fully see, on the eve of the very capital-standards transition most likely to expose hidden weakness in exactly that kind of asset. Standard analysis suggested the bid was dilutive, and swallowing Shin Kong Life's capital-starved balance sheet could have dented the very thing that makes CTBC exceptional — its industry-leading return on equity. The "loss" may well have been a save. The affair even reshaped the rulebook: chastened by the episode, the FSC drafted new hostile-takeover regulations in July 2025 and adopted them that November, raising the minimum initial stake a raider must seek from 10% to 25%, requiring that consideration be paid entirely in cash rather than volatile shares, and demanding a concrete plan for actually securing control.29 Taiwan had, in effect, written the "anti-CTBC rules" into law. The question left hanging was whether the appetite that produced the bid had truly been curbed, or merely postponed.

VIII. Playbook: Business & Investing Lessons

Strip away the drama and CTBC offers a set of unusually clean lessons about how durable advantages are actually built — and where they quietly leak.

The first is the convenience-store funding moat, and it is the sharpest illustration in Asian banking of two of Hamilton Helmer's "7 Powers" operating at once: a cornered resource and scale economies. The insight underneath it is that in banking, the asset side — lending, investing — is largely commoditized; everyone can buy the same bonds and chase the same borrowers. The real, defensible edge lives on the liability side, in the cost of the money you fund yourself with. By locking up the physical real estate of Taiwan's densest retail network, CTBC turned a mundane logistics decision into a structurally cheaper deposit base than its rivals can easily assemble. The lesson for investors is to look past a bank's loan book to its funding: cheap, sticky, low-cost deposits are the quiet foundation of a superior return on equity, and they are far harder to copy than a product feature.

The second lesson is the dual-engine trap. Pairing a capital-light, fee-generating retail bank with a capital-heavy, macro-sensitive life insurer is genuinely double-edged. In a bull market it delivers diversification and bancassurance cross-selling; in a volatile one, the insurer's foreign-exchange hedging costs and capital demands can overwhelm the bank's steady excellence — as 2025's divergence between the two engines showed in real time. The investor's takeaway is skepticism toward the word "synergy." A second engine adds horsepower, but it also adds a whole new category of things that can go wrong, and the capital it consumes is capital that cannot be returned to shareholders or deployed elsewhere.

There is a subtler lesson braided through the first two, about the double-edged nature of a regulatory moat. The same FSC that makes CTBC's franchise nearly unassailable — by refusing to license new entrants and by walling off the industry from disruption — is also the FSC that blocked CTBC's grandest ambition and then rewrote the rulebook specifically to constrain it. A heavily regulated industry hands incumbents extraordinary protection, but it also hands the regulator a veto over their strategy. Investors in any franchise built on a regulatory moat should internalize this trade: the wall that keeps competitors out is the same wall that keeps management penned in, and the value of the moat is inseparable from the disposition of the authority that maintains it. CTBC's shareholders benefit enormously from the barrier to entry; they also learned in 2024 that the barrier has a gate, and the regulator holds the key.

The third lesson is professionalization as a risk-mitigant. For a family-controlled conglomerate whose principal owner spent two decades entangled in the courts, the survival mechanism was the deliberate delegation of capital allocation and investor relations to credible outsiders. By putting a Daniel Wu between the Koo family's legal jeopardy and the rating agencies, CTBC protected its cost of capital from its owner's personal vulnerabilities. The lesson generalizes: in founder- or family-controlled companies, the quality and independence of the professional management bench is not a governance nicety — it is a core part of the investment case, and sometimes the load-bearing part. The flip side, worth holding onto, is that professionalization can be reversed. When the family walks back into the boardroom and immediately launches a hostile bid, the buffer starts to look thinner than it did.

IX. Analysis & Bear vs. Bull Case

Set CTBC inside Michael Porter's five competitive forces and the shape of the business snaps into focus. The threat of new entrants is close to nil: the FSC has not handed out a new financial-holding-company license in decades, and the regulatory moat around the industry is nearly insurmountable — a structural gift to every incumbent. The bargaining power of depositors is low, precisely because of the ATM-convenience dynamic that lets CTBC pay less for deposits than the value customers place on ubiquity. The bargaining power of borrowers and wealth clients is more mixed — accounts are easy to switch, but integrated wealth portfolios and daily-banking habits raise switching costs in practice. The threat of substitutes is modest; digital-only banks nibble at the retail edges, but traditional banking remains central to Taiwanese economic life. And rivalry is ferocious: fourteen financial holding companies grinding against each other for the wallets of 23 million people, in a market too saturated to grow much except by taking share or going abroad. It is an oligopoly with high walls and vicious interior competition — comfortable for the strong, brutal for the weak.

Hamilton Helmer's "7 Powers" framework sharpens the same picture by asking which specific, durable advantages CTBC actually possesses — and, just as usefully, which it does not. The clearest is the cornered resource: the effectively exclusive placement inside Taiwan's densest convenience-store network, a physical asset a competitor cannot simply replicate by spending money, because the shelf space is already taken. Close behind is scale economies in the deposit-gathering and card-processing machine, where CTBC's size lets it spread fixed costs — branch systems, risk models, compliance, technology — across a larger base than most rivals. There is a real element of switching costs, too, though a softer one: a customer whose salary, mortgage, credit card, and investment portfolio all sit at CTBC faces genuine friction in leaving, even if any single product is easy to move. What CTBC conspicuously lacks is network economies — a bank account does not get more valuable because your neighbors bank there — and it has no meaningful counter-positioning advantage against the digital challengers; if anything, the challengers are the ones counter-positioned against its branch-and-ATM cost base. Read together, the framework says CTBC's moat is real and rooted in physical distribution and scale, but it is a moat of the industrial era, not the platform era — durable today, and quietly exposed to a world where distribution migrates into the phone.

The bull case rests on three legs. First, the semiconductor-export tailwind: as Taiwan's chip supply chain decentralizes across Japan, Southeast Asia, and North America, CTBC is arguably the best-positioned bank to finance that migration and skim the cross-border trade, FX, and corporate-banking fees off it. Second, a pristine balance sheet: by walking away from Shin Kong, CTBC avoided a capital-destroying acquisition and preserved the roughly 16.9% return on equity that led all Taiwanese financial holding companies in 2025.7 Third, demographics: an aging, wealthy Taiwanese population feeds the recurring, high-margin wealth-management and inheritance-advisory fees that the bank's franchise is built to harvest.

The bear case is equally concrete. The first risk is governance and key-man exposure: the Supreme Court's 2024 order for yet another Red Fire retrial means the legal cloud over Jeffrey Koo Jr. is unresolved, and a fresh conviction — or simply the reputational drip of the proceedings — could unsettle investors and, at the margin, the group's cost of capital.4 The second is the hedging trap: a volatile NT-dollar/US-dollar exchange rate can spike Taiwan Life's currency-hedging costs and drag consolidated earnings, exactly as it did in 2025, and the ongoing IFRS 17 and capital-standard transition raises the amount of capital the insurer must hold to promise the same policies.30 The third is the M&A DNA itself. The family's return coincided with the boldest takeover attempt in the country's history; even with the FSC's new anti-raid rules in place, the instinct to build an empire through acquisition has not obviously been extinguished, and the next target might be one shareholders like less than they liked the idea of avoiding Shin Kong.

Hanging over all of it is a risk no analysis of a Taiwanese institution can honestly omit: the geopolitical exposure of the Taiwan Strait itself. CTBC is not a globally diversified bank that happens to be headquartered in Taipei; it is overwhelmingly a bet on Taiwan's economy, its currency, and its financial stability. Any serious escalation of cross-strait tension — a blockade, a conflict, or even a sustained scare that triggered capital flight and a run on the New Taiwan dollar — would hit CTBC through every channel at once: deposit outflows, funding stress, mark-to-market losses on Taiwan Life's portfolio, and a collapse in the cross-border trade finance that its overseas franchise is built to serve. This is not a forecast; it is a structural feature of the investment. The very Koo-family diplomacy that once positioned the group as a bridge across the strait is a reminder that the bridge could become a fault line. For a long-term investor, the geopolitical discount is not optional analysis to be bolted on at the end — it is a permanent term in the equation, and it is largely outside management's control.

An activist skeptic would press on precisely these seams. Why does a bank this good need a volatile insurer stapled to it, consuming capital that could be returned to shareholders? Is the holding-company structure obscuring the true, higher standalone value of CTBC Bank? And does the concentration of strategic control in a family with an unresolved legal history warrant a governance discount that the current valuation may not fully reflect? These are not knockout blows — CTBC's operating record answers many of them — but they are the questions a serious critic would keep asking, and they are the right lens through which to read every future capital-allocation decision.

On the question of management credibility, the record cuts both ways and deserves an honest reading. The bullish evidence is a long history of disciplined execution: through the years when the professional bench ran the company, CTBC set targets it generally met, maintained credit ratings that its peers envied, and delivered the sector's leading return on equity while resisting the temptation to chase growth into low-return corners. On its 2024 and 2025 results calls, management leaned on exactly the metrics that matter — the bank subsidiary's fee momentum, capital ratios, and return on equity — rather than obscuring performance behind one-off gains, and it was candid that Taiwan Life's softer 2025 was a currency-and-hedging story rather than an operational one.7 The bearish evidence is the Shin Kong episode itself: a management team that had preached discipline launched, within three months of the family's return, an aggressive share-swap raid that its own regulator judged under-planned on the single most important question — how the target's capital hole would be filled.6 Investors are left to weigh a two-decade habit of prudence against a fresh, vivid data point suggesting the restored ownership may prize scale over discipline. Both are real; which one dominates the next decade is precisely the open question.

It is worth pausing on a myth the headlines encourage. The popular story of 2024 is that CTBC "lost" the battle for Shin Kong — outmaneuvered by regulators, beaten to the prize by a smaller rival. The reality, on the numbers, is closer to the opposite: the company avoided overpaying for a capital-impaired asset at the worst possible moment in the accounting cycle, kept its balance sheet pristine, and watched its shares hold up while a competitor took on the hard work of fixing Shin Kong Life. In finance, the deal you walk away from is often worth more than the one you win, and the market's reaction suggests investors understood that even if the headlines did not.

Which points to the three KPIs that actually matter for tracking this company. The first is consolidated return on equity: it has run in the mid-teens (16.4% in 2024, 16.9% in 2025), and a sustained slide toward or below the low teens would be the clearest signal that capital is being deployed less efficiently — or that a dilutive deal has finally landed.87 The second is Taiwan Life's currency-hedging cost, best watched quarter to quarter, because it is the single line most likely to let macro volatility bleed into the group's otherwise steady earnings. The third is wealth-management fee income growth, the truest read on the health of the bank's core fee engine and the recurring, capital-light income that underwrites its premium returns. Track those three and you are tracking the real CTBC, underneath the headlines.

X. Epilogue & Outro

CTBC Financial Holding is, in the end, a study in a single tension held in balance for six decades: the discipline of a world-class banking machine versus the ambition of the aristocratic family that owns it. From its origins in the salt-trading harbor of Lukang, through the founding instinct to serve the customers the state banks ignored, to the convenience-store funding moat and the semiconductor-chasing branches in Kumamoto and Bangkok, the company has assembled an unusually durable domestic advantage and paired it with an opportunistic global reach. It has done so while carrying a founding family whose most powerful member has spent twenty years shadowed by the courts — a governance arrangement that should not work as well as it has.

The 2024 raid on Shin Kong crystallized the central question that will define the next chapter. The professional managers built something rare: a bank whose own shareholders would rather it stay disciplined than grow larger. The family, freshly restored to the boardroom, showed within three months that its instinct still runs toward empire. Whether the newly reunited leadership of Jeffrey Koo Jr. and Daniel Wu channels its ambition into the patient, high-return niches that have served the group so well — Tokyo Star's cross-border franchise, the wealth engine, the funding moat — or whether it reaches again for a transformational domestic conquest, is the story still being written. What makes CTBC such an instructive study is that it refuses the easy categories. It is neither the clean compounding machine that its return on equity might suggest, nor the governance disaster that a twenty-year scandal might imply. It is both at once — a genuinely excellent operating business wrapped inside a genuinely unresolved ownership question, and the tension between those two facts is not a bug to be fixed but the permanent condition of the investment. The funding moat is real and slowly contestable. The dual engine is a strength that is also a liability. The professional bench is a safeguard that can be overruled by the family it serves. And the regulatory wall that protects the franchise is the same wall that caged its ambition in 2024.

For long-term investors, the machine is the reason to watch. The people are the reason to watch closely — and the widening gap between what the operators have built and what the owners may yet do with it is the single most important thing to keep in view.

References

-

CTBC bids NT$131.4bn for Shin Kong Financial in surprise offer — Taipei Times, 2024-08-24 ↩↩↩↩

-

Shin Kong, Taishin merger to create nation's fourth-largest financial group — Taipei Times, 2024-08-21 ↩↩

-

Jeffrey Koo Jr, Daniel Wu return to CTBC board — Taipei Times, 2024-05-18 ↩↩

-

Supreme Court overturns Koo Jr acquittal in Red Fire case — Taipei Times, 2024-09-08 ↩↩↩

-

FSC rejects CTBC's Shin Kong takeover proposal — Focus Taiwan, 2024-09-16 ↩↩

-

FSC explains rejection of CTBC bid for Shin Kong Financial — Taipei Times, 2024-09-17 ↩↩↩↩

-

CTBC Financial Holding Q4 2025 earnings call: record profits — Investing.com, 2026-03-12 ↩↩↩↩↩↩

-

CTBC Financial Holding Q4 2024 earnings call: record profits — Investing.com, 2025-03 ↩↩↩

-

CTBC leads interbank ATM withdrawal share at 41.2% — Business Insider Taiwan, 2025 ↩

-

Jeffrey Koo Sr, Chinatrust founder and ambassador-at-large, dies at 79 — Taipei Times, 2012-12-15 ↩↩

-

Chinatrust changes English name to CTBC — Taipei Times, 2013-06-26 ↩↩

-

CTBC's ATMs exclusively installed in 7-Eleven stores — CardU ↩

-

The CTBC LINE Pay co-branded card, Taiwan's most-issued credit card — LY Corporation, 2024-07-04 ↩

-

Taiwan credit-card issuing institutions data — Financial Supervisory Commission, 2025 ↩

-

CTBC completes Tokyo Star Bank acquisition — Taipei Times, 2014-06-03 ↩

-

CTBC Bank's US$530m takeover of Tokyo Star Bank receives Japan's FSA approval — Retail Banker International, 2014-06-05 ↩↩

-

CTBC acquires 35.6% of Thailand's LH Financial Group — DealStreetAsia, 2017-07-27 ↩

-

CTBC Bank completes acquisition of additional 10.99% of LH Financial Group — MarketScreener, 2021 ↩

-

Fitch affirms Land and Houses Bank ratings on support from CTBC — Fitch Ratings, 2025-06-18 ↩

-

CTBC completes Taiwan Life acquisition via share swap — Taipei Times, 2015-10-16 ↩

-

Taiwan Life Insurance acquired by CTBC Financial Holding — InsuranceAsiaNews ↩

-

CTBC buys Tokyo Star Bank, Taiwan Life — The Japan Times, 2013-11-01 ↩

-

High Court acquits Koo Jr in Red Fire case — Taipei Times, 2021-04-30 ↩↩↩

-

Jeffrey Koo Jr resigns Chinatrust chairmanship — Taipei Times, 2006-07-22 ↩

-

Jeffrey Koo Jr returns to Taiwan — Taipei Times, 2008-11-25 ↩

-

CTBC drops Shin Kong bid as Taishin merger advances — Focus Taiwan, 2024-09-21 ↩

-

Taishin, Shin Kong complete merger to form TS Financial Holding — Taipei Times, 2025-07-25 ↩

-

A new framework for consolidation in Taiwan's financial sector — AmCham Taiwan TOPICS, 2026-04 ↩

-

FSC to boost insurers' FX volatility reserves — Taipei Times, 2025-12-25 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube