The Blue-Blood Titan: The Story of Cathay Financial Holding

There is a number that governs the sleep of Taiwan's insurance executives, and it is measured not in billions of New Taiwan dollars but in basis points. On any given morning in Taipei, the difference between a profitable year and a punishing one at 國泰金融控股股份有限公司 Cathay Financial Holding Co., Ltd. can come down to how many hundredths of a percent it costs to hedge a mountain of U.S. dollar bonds back into the currency its policyholders will actually be paid in. This is a company that controls over NT$13 trillion in assets — approaching USD 400 billion — and whose life-insurance arm alone touches the retirement savings of a staggering share of Taiwan's 23 million people. And yet its fate is lashed, day by day, to the gap between what the U.S. Federal Reserve pays and what the 中央銀行 Central Bank of the Republic of China (Taiwan) pays.

How did a family of humble vegetable and soy-sauce sellers from rural Miaoli build the financial fortress at the center of that story? This is the tale of Cathay: a house of "blue-blood" corporate royalty, a dynasty that split rather than fought, that survived the single worst financial scandal in the island's postwar history, and that now stands at the most consequential accounting cliff-edge the Taiwanese insurance industry has ever faced.

I. Introduction & Episode Roadmap

Picture two engines bolted to one airframe. The first is enormous, powerful, and temperamental: 國泰人壽 Cathay Life Insurance, an asset-heavy behemoth that swallows premiums and must find somewhere — anywhere — to invest them, mostly across the Pacific in American corporate bonds. The second is smaller, steadier, and quietly cash-generative: 國泰世華商業銀行 Cathay United Bank, a retail-and-digital lender that throws off predictable profit like a well-tuned turbine. Cathay's entire corporate identity is the tension between those two engines — the volatile giant and the dependable workhorse — and management's central task, for two decades, has been keeping them balanced.

Why should a global investor, sitting outside Taiwan, care about the internal accounting of a Taiwanese insurer? Because Cathay is a case study in a problem that afflicts the entire developed world's savings systems — how a nation's long-term savers get paid when domestic interest rates are too low to honor the promises made to them. Taiwan, like Japan before it, ran into that wall decades early, and Cathay is the largest laboratory for the workarounds: invest abroad, hedge the currency, and hope the regulator gives you time. Watching how this company manages that trilemma is watching, in miniature, the future stress test of every aging, low-yield economy. The stakes are not parochial. They are a preview.

That balance produced, in the first half of 2026, a record: cumulative net profit of NT$76.52 billion, up 67% year over year, with earnings per share of NT$4.95.1 But a single strong half tells you little about a company like this. The interesting parts are the fault lines. Cathay is the largest of fourteen major financial holding companies crowded onto one island, and it has spent forty years defining itself against a mirror-image rival run by its own cousins — 富邦金融控股股份有限公司 Fubon Financial Holding (2881.TW).

It is worth pausing on what "blue-blood" actually means in the Taiwanese context, because it is not a marketing phrase. Cathay is old money in a young market. The 蔡 Tsai family behind it has ranked for decades among the wealthiest clans in Taiwan, and the group's institutions carry a weight of establishment legitimacy that a challenger cannot simply buy.11 When ordinary Taiwanese households think about where to place a life-insurance policy that must survive them by fifty years, the Cathay name carries the reassurance of permanence — a brand asset built over three generations that shows up nowhere on the balance sheet but underwrites the whole distribution machine. That intangible, as much as any capital ratio, is what an investor is buying into.

Over the next several sections, the story moves through the pieces that made this empire and now test it: the rise of the 蔡 Tsai dynasty and the remarkable 1979 decision to partition it; the 1985 十信案 Tenth Credit Cooperative crisis, the dark family scandal that nearly torched the whole edifice; the golden age of housewife insurance agents and Taipei real estate; the multi-decade "Cousins' War" with Fubon; the capital-allocation record, from the Generali masterstroke to the Indonesian disaster at Bank Mayapada; the modern digital engine of the CUBE ecosystem; the structural currency mismatch that forces the hedging tax; and finally the regulatory reckoning of January 1, 2026, when Taiwan's insurers were dragged, all at once, into mark-to-market accounting under IFRS 17 and a stricter solvency regime. Each is a chapter in a single question: can a conservative, land-owning incumbent keep its crown, or will the agile cousins take the throne for good?

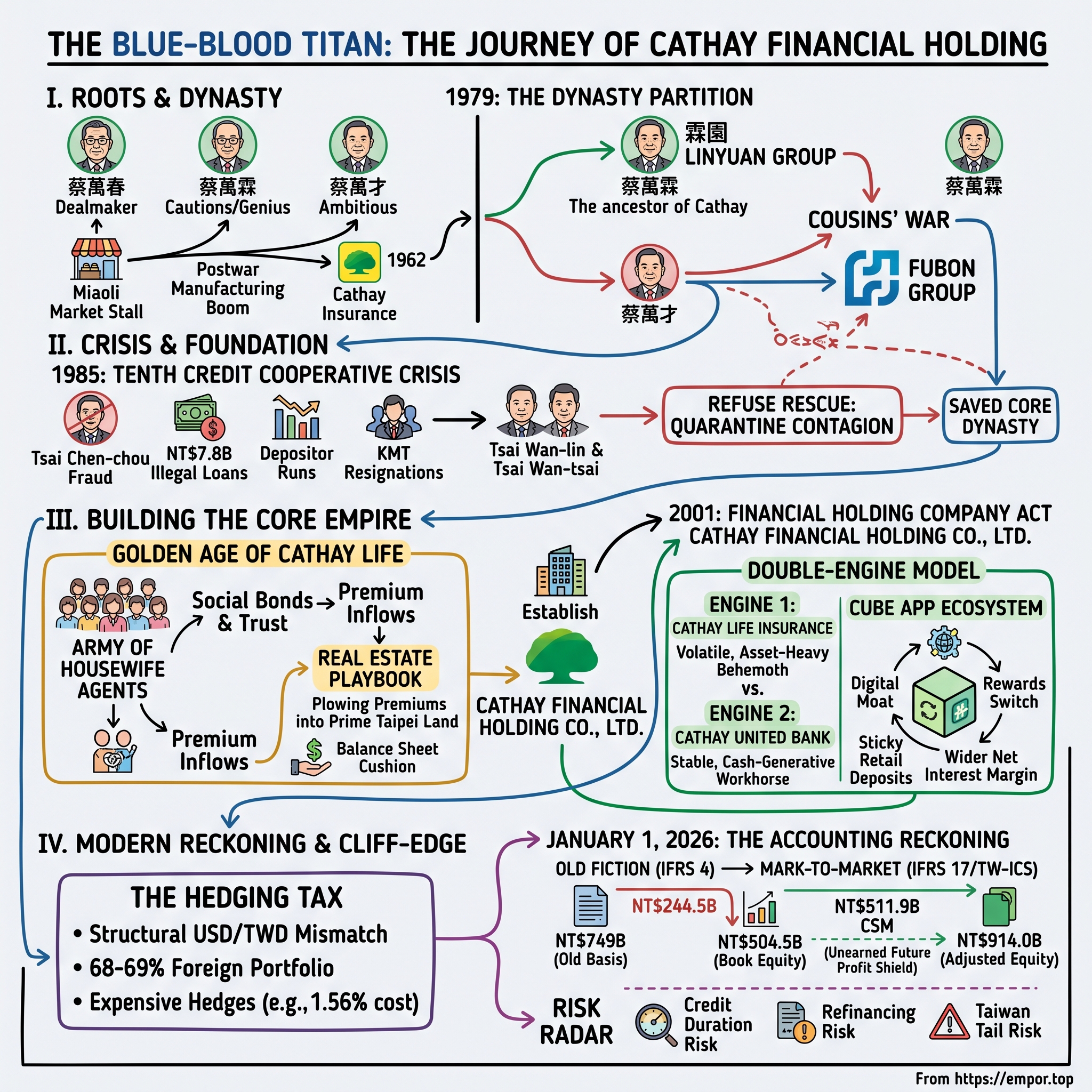

II. The Origins of the Tsai Dynasty & The 1979 Split

Begin not with a boardroom but with a market stall. In the years after the Second World War, in the rice-and-tea country of Miaoli in northwestern Taiwan, three brothers with almost nothing sold vegetables, soy sauce, and whatever else could be moved for a small margin. 蔡萬春 Tsai Wan-chun, the eldest, was the restless, charismatic dealmaker; 蔡萬霖 Tsai Wan-lin, the quiet, patient middle brother whose caution would later look like genius; and 蔡萬才 Tsai Wan-tsai, the youngest, sharp and ambitious. Their story is the founding myth every Taiwanese business student learns — poverty to plutocracy in a single generation — and like all founding myths it flattens the grind. The brothers moved from produce into a Taipei mutual-savings operation, then, riding the tailwinds of Taiwan's furious postwar industrialization and the population's newfound appetite for saving, into insurance. Cathay Insurance opened in 1962, at a moment when a fast-urbanizing island was generating exactly the kind of household savings a life insurer feeds on.

To understand why insurance, of all businesses, became the family's engine, you have to understand the Taiwan of the 1960s and 1970s. This was an economy compounding at rates the West would envy — a manufacturing miracle pulling millions of farmers into cities and factories, and, with them, into the money economy for the first time. Newly urban, newly waged households had something their parents never did: surplus income and a fear of losing it. Life insurance in Taiwan was sold less as a death benefit than as a disciplined savings vehicle, a way for a factory worker or a shopkeeper to squirrel away money against illness, old age, and the education of children. Cathay's founders read that appetite correctly and early. They were not selling actuarial protection so much as selling the promise of a secure future to a generation that had known war, dislocation, and poverty — a promise that resonated deeply and sold enormously.

For seventeen years the Tsai empire grew as one sprawling, interlinked group — insurance, plastics, construction, credit cooperatives, trust companies — held together by blood and by the eldest brother's ambition. And then, in 1979, the family did something that would look, in hindsight, like the single most important structural decision in its history. Rather than let succession disputes and diverging temperaments fester into a war for control, the brothers chose to carve the empire up.

The logic of a partition is worth dwelling on, because it runs against the instinct of most founding families, who cling to unity until unity destroys them. The Tsais did the opposite. 蔡萬霖 Tsai Wan-lin took the crown jewel — the life-insurance division — and built it into the 霖園 Linyuan Group, the direct ancestor of today's Cathay Financial Holding. 蔡萬才 Tsai Wan-tsai took the smaller, scrappier property-and-casualty business and turned it into the Fubon Group. And the eldest brother's branch, through his son, took Cathay Plastic and, fatefully, the Tenth Credit Cooperative.

That division did more than assign assets; it assigned personalities to institutions. Cathay, under the cautious Tsai Wan-lin, became the conservative, asset-heavy, land-owning incumbent — the tortoise that owned half of Taipei. Fubon, under the youngest and hungriest brother, became the agile, acquisitive challenger — the hare that would spend the next forty years trying to outrun its larger cousin. Two branches of one family, two opposite corporate DNAs, born in the same 1979 decision.

There is a deeper lesson in the partition than family harmony, and it is one long-term investors of family-controlled conglomerates should internalize. Most founding dynasties treat unity as a terminal value — the business must stay whole, whatever the cost — and that instinct routinely destroys value, because it forces incompatible temperaments and incompatible strategies to share a single balance sheet until the friction cracks it. The Tsais inverted the logic. By separating the businesses cleanly while the founders were still alive and in agreement, they let each branch pursue the strategy that fit its leader, and — crucially — they severed the financial contagion pathways between the branches. It looked at the time like a family carving up an inheritance. It was, in effect, a pre-emptive act of risk management, and its wisdom would be proven, brutally, just six years later — by the very branch that got the credit cooperative.

III. The 1985 Tenth Credit Cooperative Crisis: A Legacy Defined by Fire

Every dynasty has a near-death experience, and Cathay's arrived not from a market crash or a war but from within the family itself. The villain of the piece was 蔡辰洲 Tsai Chen-chou, son of the eldest brother, a man who had inherited ambition without his uncle Tsai Wan-lin's patience. As chairman of the 十信 Tenth Credit Cooperative — one of Taiwan's largest — Tsai Chen-chou sat atop a pool of ordinary depositors' savings. His industrial holdings, the Cathay Plastic group, were failing. And so he did the thing that has destroyed bankers since banking began: he used the depositors' money to prop up his own dying companies.

The scale was extraordinary for its era. Tsai Chen-chou funneled an estimated NT$7.8 billion of the cooperative's funds into his failing group through illegal loans and related-party lending — a web of self-dealing dressed up as ordinary credit. To grasp how large that was, remember that this was 1980s Taiwan, an economy a fraction of its present size; a run of this magnitude on a single credit cooperative was a systemic event, not a local embarrassment. The mechanism was the oldest fraud in finance: an insider using an institution that holds other people's money as a captive lender to his own failing ventures, booking loans that everyone involved knew would never be repaid.

To keep the regulators at bay, Tsai Chen-chou did what the well-connected have always done — he bought political cover. He assembled a bloc of legislators known as the 十三兄弟 "Thirteen Brothers" inside the Legislative Yuan, a clique that could lobby to bend financial rules, soften supervision, and buy time. In an era when Taiwan was still a one-party state and the lines between business, party, and government ran thick and unregulated, that kind of influence could hold examiners at bay for years. For a while, it worked. Money and influence bought time — right up until they didn't.

Time ran out in February 1985. As word spread that the cooperative was hollow, depositors did what depositors always do when trust evaporates: they ran. Crowds massed outside branches demanding their savings. The panic threatened to jump from one institution to the whole system, and the political fallout reached the top of the government — the crisis ultimately forced the resignations of the KMT government's ministers of finance and economic affairs, an almost unthinkable blow in the authoritarian-tinged politics of the time. The Tenth Credit Cooperative crisis remains the defining financial scandal of postwar Taiwan, the event against which every later banking wobble is measured.

Here is where the 1979 partition earned its keep, and where the story turns from tragedy to lesson. The two surviving uncles — Tsai Wan-lin at Cathay and Tsai Wan-tsai at Fubon — faced a choice. Family loyalty, and the fear of the Tsai name being dragged through the mud, pulled toward a rescue. Cold capital discipline pulled the other way. They chose discipline. They drew a hard line and refused to pour good money into their nephew's bankrupt branch.

Imagine the pressure of that decision. Your nephew is drowning; the family name is on every newspaper front page; depositors are screaming outside branches; and a rescue would buy short-term peace and preserve face. Everything in Chinese family culture — obligation, hierarchy, the shame of a public failure — pushed toward a bailout. Tsai Wan-lin and Tsai Wan-tsai said no anyway. They understood that pouring capital into a bankrupt entity to save face is how one sick company becomes three, and that the only way to protect the depositors and policyholders of the healthy businesses was to let the unhealthy one fall.

It was ruthless, and it was correct. Because the empire had been legally partitioned six years earlier, the failing credit cooperative was ring-fenced from the healthy core. Cathay Life's capital and Fubon's balance sheet were structurally insulated; the contagion could be quarantined to the branch that caused it. The scandal reshaped Taiwan's financial regulation for a generation, accelerating reforms of cooperative supervision and related-party lending rules — the crisis became the case study that a modernizing regulatory state built its rulebook around. In that sense the fire that nearly consumed the Tsai name also helped forge the supervisory apparatus that Cathay would later navigate, and the licensing regime that now protects it from competition.

For long-term investors, this is the most durable lesson the Cathay story offers, and it long predates any modern "resolution regime": in a financial conglomerate, strict liability boundaries between entities are not bureaucratic nuisance — they are the ultimate law of survival. A group that lets a sick subsidiary infect its healthy ones dies; a group that will let a subsidiary fail lives. The Tsais understood this in 1985, before it was fashionable, and it saved them. Tsai Chen-chou went to prison; the core dynasty went on to build the largest financial institution in the country. With the fire survived, Tsai Wan-lin turned to the patient work of building something that could not so easily burn.

IV. Building the Core: The Golden Age of Cathay Life & The Real Estate Playbook

If you want to understand how Cathay Life became a giant, don't start with actuaries or asset managers. Start with a middle-aged woman knocking on her neighbor's door. The single most important competitive weapon Cathay ever built was human, and overwhelmingly female: an army of local insurance agents — many of them housewives — who sold savings policies not through slick advertising but through the dense web of community, kinship, and obligation that binds Taiwanese social life. An agent selling to her cousin, her mahjong partner, and the family two doors down was selling on trust that no rival could buy. In an era before comparison-shopping and online quotes, that relationship-driven distribution channel gave Cathay a reach into ordinary households that competitors spent decades failing to match.

There is a subtle genius to this model that is easy to miss from a modern vantage point. The housewife-agent channel was not merely cheap labor; it was a distribution system perfectly matched to the product. Life insurance is a low-frequency, high-trust, high-inertia purchase — you buy it rarely, you must believe the seller, and once bought you almost never switch. A neighbor with standing in the community could close that sale where a stranger in a suit could not, and the very same social bonds that made the sale also made the policy sticky and the lapse rate low. The agent's embeddedness in the community was, in effect, a customer-retention mechanism disguised as a sales force. For decades this gave Cathay a structurally lower cost of acquiring and keeping policyholders than any challenger could achieve — the origin of the scale-and-distribution advantage that still anchors the bull case today.

Premiums poured in. And that created the second half of the golden-age playbook: what to do with the money. Here Tsai Wan-lin's instincts as a patient accumulator met one of the great one-way bets of the twentieth century — Taiwanese land. On a crowded, mountainous, rapidly industrializing island where flat, buildable urban ground was genuinely scarce, Cathay Life plowed its premium inflows into prime commercial real estate, above all in Taipei. It became, in effect, Taiwan's largest private corporate landlord.

The elegance of this strategy was that it required almost no leverage. Cathay was not a speculator borrowing to flip buildings; it was a life insurer with a river of long-dated premium cash buying trophy real estate outright and holding it for decades. As Taipei land values compounded through the boom years, that portfolio delivered enormous, un-leveraged capital appreciation that quietly fortified the balance sheet — a cushion of hard assets sitting beneath the insurance liabilities. For a company whose core business was making very long promises to policyholders, owning a large slice of the island those policyholders lived on was a remarkably durable form of collateral.

But here is where a neutral observer must plant a flag for later, because the real-estate strategy that looked like pure genius in an inflationary, land-scarce boom carries a hidden dependency: it only works while Taipei property compounds. A large, illiquid, low-yielding real-estate book is a wonderful thing when values rise and a dead-weight anchor when they stall — property throws off modest rental income relative to its carrying value, and it cannot be sold quickly to raise cash in a crisis. The same balance-sheet ballast that protected Cathay for decades became, under the modern accounting and solvency regimes discussed later, a large pool of capital that regulators scrutinize and that does not always earn its keep. The golden-age playbook, in other words, planted a seed that the 2026 rulebook would force the company to reckon with.

The final structural piece arrived with regulatory liberalization at the turn of the millennium. Taiwan's 金融控股公司法 Financial Holding Company Act of 2001 allowed banking, insurance, and securities to be consolidated under a single corporate umbrella for the first time — a deliberate policy push to build financial groups large enough to compete regionally. Cathay moved quickly. Cathay Financial Holding Co., Ltd. was formally incorporated on December 31, 2001, and set about assembling the "double-engine" model that defines it today, eventually bringing Cathay United Bank alongside Cathay Life. The strategic logic was to bolt a stable, cash-generative bank onto the volatile, lumpy cash flows of a life insurer — a diversification instinct that would matter enormously once the currency and accounting storms arrived. But before those storms, Cathay had a nearer rival to worry about, one that shared its surname and its ambitions.

V. The Fubon vs. Cathay Rivalry: The Cousins' War

There is no rivalry in Asian finance quite like it: two of the island's largest financial holding companies, run by first cousins, descended from brothers who once sold vegetables together, competing for the same customers, the same deposits, and the same national bragging rights. On one side stood 蔡宏圖 Tsai Hong-tu, Tsai Wan-lin's son, the steward of Cathay — cautious, disciplined, a capital allocator in his father's mold. On the other stood the Fubon brothers, 蔡明忠 Daniel Tsai and 蔡明興 Richard Tsai, sons of the youngest founder, who inherited their father's appetite for the deal. The second-generation succession turned the 1979 partition into a live competition, played out quarter after quarter on the Taipei exchange.

The personalities matter here, because they drive the numbers. Tsai Hong-tu, trained as a lawyer, ran Cathay like a fiduciary steward — his temperament visible in a preference for balance-sheet fortification over headline-grabbing deals. Daniel and Richard Tsai at Fubon carried their father's dealmaker gene, comfortable with leverage, hostile takeovers, and moves into businesses that had nothing to do with insurance. Same bloodline, opposite risk appetites — and the market, over decades, has rewarded them differently.

For much of the modern era, the scrappier hare has run faster. Despite Cathay's larger total asset base, Fubon repeatedly overtook it on the metrics that reward capital efficiency — market capitalization and return on equity — with Fubon's ROE running meaningfully ahead of Cathay's in recent periods. That gap is not an accident; it is the arithmetic of two different strategies. Cathay's engine is a life insurer whose vast, conservative, bond-heavy portfolio produces stable but unspectacular returns on a huge equity base. Fubon runs a more aggressive, equity-tilted investment book and a more diversified group, which in good markets compounds capital faster. The distinction an investor must hold is between size and quality of earnings: Cathay is bigger, but "bigger" in insurance means a larger, slower-turning asset base, and return on equity — not total assets — is what compounds a shareholder's wealth.

The anatomy of Fubon as a challenger is a study in aggression. It bought Taipei Bank in 2002, an early and formative acquisition. Two decades later, in 2022, it pulled off the acquisition of Jih Sun Financial Holding in what was widely described as Taiwan's first-ever hostile financial-holding-company merger — an audacious move in a market where consensus and face still govern much of corporate life. And crucially, Fubon diversified structurally outside of finance altogether, into telecommunications, through its control of 台灣大哥大 Taiwan Mobile. That gave Fubon a stream of non-cyclical cash flow — people pay their phone bills in recessions — that a pure financial group like Cathay simply does not have. When investors ask why Fubon has often commanded a richer valuation, part of the answer is that it is not only a financial company.

There is an activist's question lurking in the Fubon comparison, and a neutral analysis has to ask it: if the challenger's diversified, telecom-plus-finance structure keeps earning a higher return on equity, is Cathay's conservatism a virtue or a value trap? A skeptical investor would press management on whether the enormous, low-yielding real-estate and bond book is being managed for shareholder return or merely for stability — whether, in effect, Cathay is over-capitalized and under-earning by design. Management's answer, implicit in its behavior, is that stability is the product: a life insurer's promise is only as good as its ability to survive the worst decade, and a portfolio optimized for return-on-equity in the good years is the one that blows up in the bad ones. Both readings are defensible. Which one is correct depends entirely on how violent the next cycle turns out to be.

Cathay's counter has been the tortoise's game: don't chase, compound. Rather than match Fubon deal-for-deal, Cathay leaned on the assets its history handed it — a dominant share of Taiwan's wealth-management relationships and corporate-banking deposits, the largest life-insurance franchise on the island, and the balance-sheet ballast of that real-estate empire. Its bet is that slow, conservative capital accumulation wins across a full cycle, even if it lags in a bull market. For an investor, the Cousins' War frames the central choice in owning Cathay: you are choosing the disciplined incumbent over the agile challenger, and the case only works if conservatism is genuinely rewarded when markets turn. Nowhere is the quality of that discipline tested more sharply than in how Cathay has spent its money abroad — where it has produced both a masterstroke and a genuine disaster.

VI. Capital Allocation & International M&A: The Good, the Bad, and the Indonesian Ugly

Every large Taiwanese financial group eventually runs into the same wall: the island is too small. With a flat population of roughly 23 million served by fourteen major financial holding companies, the domestic market is saturated and fragmented — a knife fight for share in a room that never gets bigger. That structural trap is what pushes Taiwanese finance overseas in search of growth, and Cathay's expansion story is best understood as two very different answers to that pressure: one that destroyed capital and one that redeployed it brilliantly.

Start with the ugly. In January 2015, Cathay Life moved into Indonesia, agreeing to acquire a large stake in 印尼馬亞帕達銀行 PT Bank Mayapada Internasional for roughly USD 272 million, eventually building its holding to about 37.33% and positioning itself as the bank's largest shareholder.2 The strategic thesis was seductive: Indonesia was a huge, under-banked, fast-growing economy, and a minority stake in a local lender looked like a cheap ticket to that growth. The red flags, in hindsight, were not subtle. Bank Mayapada carried a non-performing loan ratio of 6.94% — more than double the Indonesian industry average of below 3% — a sign of a loan book far riskier than headline growth suggested. Worse, the bank became entangled in one of Indonesia's largest corruption scandals: a major debtor, Benny Tjokrosaputro, was named a suspect in the massive PT Asuransi Jiwasraya state-insurance fraud, which helped trigger a run on Mayapada itself.2

The reckoning came in August 2020. Cathay Life recognized a loss that effectively wrote its investment down to nothing — an NT$8.8 billion charge that completed a total investment loss of roughly NT$14 billion (about USD 470 million) across the life of the holding.23 The whole book value of the stake, gone. There is a bitter irony in the timing: even as the write-off crystallized, Cathay had been in discussions about increasing its stake toward a controlling 51%, precisely the kind of doubling-down that turns a bad investment into a catastrophic one.2 That it did not complete that move was, in the end, a mercy.

The lesson is one that emerging-market investors relearn in every generation: a minority, non-controlling stake in a bank you do not control, in a jurisdiction with weak corporate governance, is a bet on other people's integrity. A bank is a black box — its true asset quality is knowable only to insiders until the moment it isn't — and a 37% shareholder with no operational control cannot audit the loan book, cannot fire the lenders making bad loans, and cannot force a cleanup. When you are that shareholder, you are a passenger, not a driver, strapped into a vehicle whose brakes you cannot reach. The elevated non-performing loan ratio and the corruption entanglement were visible risk signals; the more damning question for management is why they were not treated as disqualifying before the check was written, and why the position was allowed to sit as the warning signs multiplied.

Now the masterstroke, and it starts from a similar place — an overseas ambition that didn't quite work — but ends far better. In 2014, Cathay bought the U.S. asset manager Conning Holdings for about USD 240 million, aiming to build a global asset-management capability. Conning was a respectable operator, but scaling a mid-sized American asset manager into a global franchise from Taipei proved hard. Rather than throw more money at a subscale asset, Cathay engineered an elegant exit-into-something-bigger. On April 3, 2024, it completed an asset-for-equity swap: it handed 100% of Conning to 忠利 Assicurazioni Generali, the Italian insurance giant, in exchange for a 16.75% stake in Generali Investments Holding — plus a ten-year asset-management partnership.4

Consider the chess move. Cathay traded a small, hard-to-scale U.S. operator for a material minority stake in a European institutional asset manager overseeing hundreds of billions of euros, and locked in a decade-long partnership to boot. It converted a strategic dead-end into a benchmarked position inside a genuine global platform, without writing a fresh check. The deal did something else, too, that speaks to institutional maturity: it acknowledged failure without pretending otherwise. Buying Conning and trying to scale it from Taipei had not worked; rather than sink good money after bad in a doomed attempt to build global scale organically, Cathay recognized the limits of its own franchise and swapped into a partner that already had the scale it lacked. Admitting a strategy has not worked, and restructuring around that admission cleverly rather than defensively, is exactly the behavior a fundamental investor wants to see from a capital allocator.

Set the Generali swap beside the Mayapada write-off and you get a fair, unflattering-but-not-damning read on Cathay's capital allocation: capable of real sophistication, but also capable of expensive naïveté in unfamiliar territory. The difference between the two, tellingly, was control and transparency — a minority stake in a well-governed European institution with a clean partnership structure is a fundamentally different animal from a minority stake in an opaque emerging-market bank. The pattern that emerges is that Cathay allocates capital best when it stays close to what it can actually see and influence, and worst when it reaches for growth in places where it must trust strangers. That is the very argument for the domestic double-engine model — and the steadier of those two engines was, by 2024, doing the heaviest lifting.

VII. The Modern Engine: Cathay United Bank & The CUBE Ecosystem

For all the drama of insurance and international deals, the quiet hero of the modern Cathay story wears a banker's suit. Cathay United Bank is the group's stabilizer — the dependable turbine that produces profit whether or not currency markets are cooperating. In 2024, CUB delivered a record after-tax profit of about NT$38.3 billion, up more than 30% year over year, on total loans that grew 17% to NT$2.6 trillion, with net interest margin widening to 1.55%.5 In a year when the insurance engine was fighting hedging costs and accounting transitions, the bank simply kept humming.

The most interesting thing CUB built, though, is not on the balance sheet — it is in millions of pockets. For years, like most banks, Cathay ran a fragmented mess of co-branded credit cards, each with its own narrow rewards and its own marketing budget. Then it consolidated the lot into a single, cleverly designed product: the CUBE Card, which grew to more than five million active cardholders.6 The mechanic is deceptively simple. Instead of locking a customer into fixed rewards categories, the CUBE App lets users dynamically switch which spending category earns the highest cash-back — dining this month, travel next month, online shopping the month after — with a tap.

Why does a switchable rewards card matter to a serious investor? Because of what it does underneath the rewards. The industry shorthand here is switching costs, one of Hamilton Helmer's classic "7 Powers": once a customer runs their daily spending through the CUBE App, optimizes their categories, and parks their salary and savings in the linked account, the friction of leaving rises with every month of use. But it is worth unpacking the economics in plain terms, because "the card is a funnel" is the kind of phrase that sounds like strategy and means nothing until you trace the cash.

A bank makes money on the spread between what it pays for deposits and what it earns on loans — the net interest margin. The single biggest lever on that margin is the cost of the deposits. A bank that funds itself with expensive wholesale borrowing or by bidding up time-deposit rates earns a thin spread; a bank that funds itself with millions of ordinary checking and savings accounts that sit there earning almost nothing earns a fat one. What the CUBE ecosystem does is manufacture the second kind of deposit at scale. Someone who runs their daily life through the app — cash-back, bill payments, salary deposit, savings — leaves idle balances in low-cost accounts, and those balances are the cheapest raw material a bank can have. The card, in other words, is not really a fee-income product at all. It is a customer-acquisition funnel that pulls in sticky, low-cost retail deposits and, through them, widens the net interest margin versus corporate-heavy competitors like the state-linked megabanks, who must pay up for chunkier wholesale funding. Seen this way, CUBE is less a loyalty program than a deposit-gathering machine dressed in consumer-friendly clothes — and CUB's expanding margin through 2024 is the evidence the machine is working.5

There is a caveat worth holding onto, and it is exactly the kind of thing an activist would press on an earnings call. Reward-switching customers can be mercenary; a rival with a richer offer can peel off the rate-chasers, and the "five million cardholders" headline says nothing about how many are genuinely anchored versus merely present. Rich cash-back also costs real money — a rewards war among Taiwanese banks could compress the very margins the deposits are meant to widen. The honest read is that switching costs here are moderate and behavioral, not the near-absolute lock-in of, say, an enterprise software system; they are strong enough to lower funding costs at the margin, not strong enough to make customers captive. The real test is deposit stickiness and funding cost through a full rate cycle, not card counts.

Still, on the evidence through 2024 and into 2026, the bank engine is doing exactly its intended job — throwing off stable, growing profit to offset the volatility next door, and helping power the group's record first-half 2026 result. The double-engine model was designed for precisely this: when the insurance engine coughs, the banking engine keeps the plane level. And that volatility, when you trace it to its root, comes down to a single structural mismatch built into every Taiwanese life insurer.

VIII. The Structural Mismatch: Hedging the USD/TWD Cliff

Here is the problem that keeps Cathay's executives awake, explained without the jargon. A life insurer collects premiums in one currency and promises to pay claims, decades later, in that same currency. For Cathay Life, that currency is the New Taiwan dollar. Simple enough — except for one brutal fact of geography and economics: there is nowhere in Taiwan to put all that money. The island's domestic government-bond market is small, and local yields are punishingly low. An insurer that took in trillions of NT dollars and tried to invest them all at home would be locking in returns far below what it promised its policyholders.

So Cathay does what every large Taiwanese insurer is forced to do: it sends the money abroad. Roughly two-thirds of Cathay Life's enormous investment portfolio — on the order of 68% to 69% of assets — sits overseas, overwhelmingly in U.S.-dollar-denominated corporate bonds that yield far more than anything available at home.7 This solves the yield problem and creates a new, arguably scarier one: a currency mismatch. The assets are in dollars; the liabilities are in NT dollars. If the NT dollar suddenly strengthens against the U.S. dollar, the value of those overseas assets — translated back into the currency the company reports and pays in — shrinks, and the capital base can erode with frightening speed.

To defend against that, Cathay buys insurance on its insurance: foreign-exchange hedges, in the form of FX swaps and non-deliverable forwards, that lock in a conversion rate and protect the balance sheet from a sudden NT-dollar surge. But hedges are not free, and this is where the basis points from the opening return. The cost of hedging is driven largely by the interest-rate differential between the United States and Taiwan — put simply, when you agree today to convert dollars back into NT dollars at a fixed future rate, the price of that agreement reflects the gap between the two countries' interest rates, and the wider the gap, the more you pay. When the Fed holds rates well above Taiwan's central bank — as it did through 2024 and into 2025 — hedging the dollar back to the NT dollar becomes expensive. In 2024, that hedging cost ran to roughly 1.56%, a punishing drag that eats directly into investment yield.5

To feel the weight of that number, do the arithmetic in your head. If Cathay earns, say, 4% to 4.5% on a U.S. corporate bond but must hand back 1.5% to hedge the currency, more than a third of the gross yield can evaporate before it reaches the policyholder or the shareholder. On a foreign portfolio measured in the trillions of NT dollars, one and a half percentage points is tens of billions of NT dollars a year — a tax the company must pay, every year, for the sin of having to invest abroad, set by the gap between two central banks it does not control. Management has options at the margin: it can hedge less and accept more raw currency risk, use cheaper "proxy" hedges against a basket of Asian currencies rather than the NT dollar directly, or — the current tactic — sell more U.S.-dollar-denominated policies so that some liabilities are naturally in dollars and need no hedge at all. Each option trades one risk for another, and none of them makes the mismatch disappear.

The swings can be violent enough to threaten reported earnings and solvency in any single period, which is why the regulator built a shock absorber. Taiwan's 金融監督管理委員會 Financial Supervisory Commission (FSC) allows insurers to run a Foreign Exchange Volatility Reserve — a smoothing mechanism that lets them set aside gains in calm periods and draw them down when the currency moves against them, damping the multibillion-NT-dollar quarterly swings that would otherwise whipsaw the income statement. In August 2024, the FSC eased the rules around this reserve to give insurers more room to absorb currency shocks. By mid-2026, Cathay Life's FX reserve had climbed above NT$130 billion, a record buffer.1 It is a genuinely useful tool — but it is a shock absorber, not a cure. The underlying mismatch remains, and it is precisely the kind of structural fragility that the coming accounting overhaul was designed to force into the open.

IX. The Regulatory Cliffhanger: IFRS 17 & TW-ICS 2.0

For years, Taiwanese insurers lived with a comforting fiction, and everyone knew it was a fiction. On January 1, 2026, the fiction ended. That was the transition date for the island's insurance sector to adopt IFRS 17 — which requires insurance liabilities to be measured at fair value — alongside TW-ICS, a stricter, more risk-sensitive capital-solvency regime modeled on international standards.8 Together they represent the most complex accounting and capital transformation in the history of Taiwanese finance, and Cathay Life sat squarely in the blast radius.

To see why, rewind to the 1990s and early 2000s, when Cathay Life — like its peers — sold enormous volumes of savings policies carrying guaranteed rates of 5% to 6%. At the time, with interest rates high, those guarantees looked affordable, even conservative. But then came the long global slide in interest rates, and rates fell and stayed low for a generation, leaving insurers on the hook for promises far richer than anything the bond market now offers. This is the "negative spread" problem that has haunted Taiwanese and Japanese life insurers for decades: they are contractually bound to pay policyholders more than they can safely earn on the assets backing those policies, and the gap has to come out of capital.

Here the accounting change bites. Under the old regime (IFRS 4), the true present-day cost of those legacy guarantees could be politely obscured — the liabilities were carried at historical assumptions that flattered the balance sheet. Under mark-to-market accounting, the fiction ends. Think of it like a mortgage you promised to pay at a fixed high rate: if you have to re-price that promise at today's low rates, its present value balloons, because a stream of rich future payments is worth far more when discounted at a low rate than at a high one. Those legacy liabilities must now be discounted using today's low interest rates, which inflates their measured value and blows a hole in reported equity. The hole was always there economically; IFRS 17 simply forced it into the light.

The anatomy of Cathay Life's transition balance sheet shows exactly how big the hole was — and how it was patched. On transition, Cathay Life's book equity fell sharply, from roughly NT$749 billion under the old IFRS 4 basis to about NT$504.5 billion under the new regime — a drop of nearly a quarter of a trillion NT dollars, driven precisely by re-valuing those legacy liabilities.1 But that is not the whole picture, and this is the part investors must grasp. IFRS 17 also forces companies to recognize a new item on the other side of the ledger: the Contractual Service Margin, or CSM. The CSM is best understood as a store of unearned future profit — the profit embedded in in-force policies that will be released into earnings gradually over the coming decades as the company delivers on those contracts. Cathay Life's after-tax CSM balance stood at roughly NT$511.9 billion, so that including the CSM, its "adjusted equity" was a far more robust NT$914.0 billion.1

So which number is real — the NT$504.5 billion or the NT$914.0 billion? The honest answer is both, and neither. The lower figure is today's accounting equity; the CSM is a genuine, quantified claim on future profits, but it is future profit, contingent on Cathay actually earning it over decades without adverse surprises. The CSM is a shield, not cash in the vault. Its accumulation is the single most important thing to watch in this business — Cathay adds new CSM each year from newly written protection policies, and management has guided to substantial annual additions in the years ahead as it shifts its product mix.

The distinction between the two equity numbers is not accounting trivia; it is the whole investment debate in miniature. A bear looks at NT$504.5 billion and sees a company whose real capital was quietly gutted by promises it made a generation ago. A bull looks at NT$914.0 billion and sees a franchise sitting on more than half a trillion NT dollars of contracted future profit that the old accounting never let it show. The neutral truth is that the CSM is real but deferred and conditional — it converts to cash only as policies run their course, over decades, and only if experience matches assumptions on mortality, lapses, and investment returns. An investor should treat rising CSM as the leading indicator of future earnings power and treat the transition-day equity drop as a reminder of how much of that power is promised rather than banked.

The transition also squeezed capital, and Cathay responded by raising a great deal of it. Across 2024 the group issued on the order of NT$80 billion of subordinated debt to shore up its solvency ratios — roughly NT$50 billion equivalent in April and May 2024 alone, with further issuance following — deliberately building a cushion ahead of the new rules.9 Even so, Cathay Life's regulatory capital ratio fell under pressure, with its RBC ratio dropping to around 328% by mid-2025, down from 359% at the end of 2024, largely on unrealized FX losses.10 It is worth noting the RBC ratio remained comfortably above the 200% regulatory minimum — this was a squeeze, not a solvency scare — but the direction of travel is what mattered to management, and it was downward.

Critically, the FSC granted the industry a 15-year transition grace period to phase in the full TW-ICS requirements — a long runway without which the simultaneous shock of mark-to-market liabilities and stricter capital rules could have triggered a system-wide capital crisis.8 The regulator faced a genuine dilemma: apply the new global solvency standard overnight and you might force the island's largest insurers to raise capital they could not raise, or dump assets into a falling market to meet ratios; phase it in too slowly and you leave the system under-capitalized against real risks. The 15-year glide path was the compromise, and it is the reason a wrenching transition became a manageable one. It is also, as the bear case will argue, a fifteen-year obligation hanging over shareholders — a decade and a half in which the regulator can keep asking for more capital, and in which Cathay must keep proving it can generate that capital internally rather than by tapping its owners.

X. The Investment-Story Spine: Why Win / Why Not

Strip away the history and the drama, and an investor is left with a simple question: from here, does Cathay win, and what would prove the case wrong? Both sides deserve an honest hearing.

Before the ledger, a word on a persistent myth. The consensus story on Cathay is that it is "the boring, safe one" — the conservative incumbent you own for stability while the exciting money is made at Fubon. That framing is half right and dangerously incomplete. The reality is that Cathay is not low-risk in any absolute sense; it is a highly leveraged bet on a specific set of macro variables — the U.S.–Taiwan rate differential, the NT dollar, long-term interest rates, and cross-strait peace — wrapped in a brand that feels safe. Its earnings can swing violently with currency and rate moves, as the very different results of recent years show. "Conservative" describes the intent of management and the composition of the asset book; it does not describe the volatility of the outcome. An investor who buys Cathay expecting a bond-like ride is misreading the company. The correct frame is a stable, dominant franchise sitting on top of a genuinely volatile financial engine.

The bull case rests on three pillars. The first is scale and distribution — what the 7 Powers framework calls scale economies. With a customer base numbering in the many millions across insurance, banking, and securities, Cathay enjoys cross-selling efficiency few rivals can match: every digital-banking user is a low-cost lead for a high-margin health, accident, or protection policy, and every insurance relationship is a channel for a deposit or a card. The evidence that this is real, not aspirational, sits in the operating numbers — a value of new business that grew strongly in 2024 as the group pushed higher-margin protection products through its distribution, and a bank whose loan book and margin both expanded off the same customer base.5 On a saturated island, owning the widest funnel is a durable structural advantage, and it is the one power that a challenger, however agile, cannot quickly replicate — you cannot manufacture eight million relationships in a quarter. The second pillar is the CSM accumulation engine described above: Cathay is deliberately shifting its mix away from low-margin single-premium savings products toward regular-paid, high-CSM protection policies, compounding a large store of deferred future profit year after year. If it sustains that shift, the earnings power builds quietly beneath the reported numbers. The third pillar is the digital moat of the CUBE ecosystem and the sticky, low-cost deposit base it feeds — the switching-cost mechanism that lowers the whole group's blended funding cost.

The bear case is equally concrete, and it targets the same balance sheet from the other side. First is the FX hedging drag: if the U.S.–Taiwan rate differential stays structurally wide, hedging costs will keep eating well over a percentage point of investment yield every year, a permanent tax that no amount of clever product mix fully escapes. And the alternative to hedging is worse in the wrong scenario — a sharp, sustained appreciation of the NT dollar, which Taiwan's export surpluses and any repatriation of capital could drive, would inflict mark-to-market pain on the vast unhedged or under-hedged portion of the foreign book. The company is squeezed between a certain cost (hedging) and an uncertain catastrophe (an unhedged currency surge), and it must pay something to stand anywhere on that spectrum.

Second is persistent dilution risk. To meet the full TW-ICS requirements by the end of the fifteen-year grace period, Cathay may need to keep raising capital — subordinated debt is not free, it carries coupons that drag on earnings, and if the company ultimately turns to common equity, it dilutes existing shareholders' per-share earnings. A company that must repeatedly tap the market to satisfy regulators is running to stand still, and the fifteen-year runway, comforting as it is, also means fifteen years in which this overhang never quite clears. Third is relative performance: in a sustained bull market, Fubon's more aggressive, equity-heavy book and its non-financial cash flows from telecom are likely to keep outrunning Cathay's conservative, bond-heavy portfolio, meaning Cathay can be a perfectly sound business and still be the underperforming cousin — the kind of company that is easy to admire and, for a return-hungry investor, easy to leave un-owned.

Run this through Porter's five forces and the picture sharpens. Rivalry is intense — fourteen holding companies on one island, led by a same-family rival that has repeatedly out-earned Cathay on returns. Bargaining power of customers is rising as digital comparison and open-banking tools erode the old relationship lock-in that housewife agents once provided; the young Taiwanese buying insurance today compares quotes on a phone rather than trusting a neighbor. Supplier power, in a financial context, shows up as the cost of capital and the terms regulators impose — and here Cathay is more taker than maker. The threat of substitutes and new entrants, by contrast, is muted by one of the highest regulatory barriers in the world — you cannot simply start a life insurer in Taiwan, and the licensing, capital, and solvency requirements form a moat that no fintech disruptor can vault. That barrier is the single strongest force working in Cathay's favor, and it is worth naming plainly: much of Cathay's durable advantage is a regulatory moat, the flip side of the regulatory burden that the 2026 transition represents. The same rulebook that squeezes its capital also fences out its competition.

Map the same business onto Hamilton Helmer's 7 Powers and three of the seven clearly apply — scale economies in distribution and cross-selling, switching costs in the CUBE deposit base, and a species of cornered resource in the brand-plus-license combination that sixty years and a founding-family legacy conferred. What Cathay conspicuously lacks is the power that Fubon has partly captured — counter-positioning, a fundamentally different and hard-to-copy business model — because Cathay's model is the incumbent model. Its edge is defensive and structural, not disruptive. That is a perfectly fine place to stand, but it caps the upside: incumbents protected by moats compound steadily; they rarely surprise to the upside the way a challenger reinventing the category can.

The net read is a company with a genuine, regulation-and-scale-protected moat around its franchise, but one whose economics are hostage to two things it does not control: the gap between two central banks, and the pace at which a 15-year capital regime demands to be fed. If an investor tracks nothing else, the three numbers that matter most are the annual net CSM added (is the future-profit engine compounding?), the FX-hedging cost (is the currency tax rising or easing?), and the RBC/solvency ratio net of any capital raises (is the balance sheet strengthening on its own, or only with fresh dilution?). Those three, watched over several years, will tell the story of whether the bull or the bear case is winning long before the reported net-income line does.

XI. Risky Business: Risk Radar & Management Assessment

Some risks a company chooses; others are simply the price of the address. For Cathay, the largest uncontrollable risk is written into the map. A serious cross-strait escalation between Taiwan and mainland China would be catastrophic in a way that dwarfs any hedging cost or accounting transition: it would trigger domestic asset fire-sales, capital flight, and an unhedged collapse of the NT dollar. This is the "Taiwan discount" that hangs over every asset on the island, and there is no FX reserve or CSM shield large enough to fully neutralize it. It is the tail risk an owner of Cathay is, knowingly or not, underwriting.

The nearer, more quotidian risks live inside that vast overseas bond portfolio. Because Cathay must hold hundreds of billions of dollars of foreign corporate credit to earn its yield, it carries refinancing and duration risk: if global refinancing costs stay high and corporate default rates rise, the credit quality of that portfolio could deteriorate, and losses there would flow straight to capital already stretched by the new solvency regime. The very strategy that solves the domestic yield problem imports credit and duration risk from the rest of the world. There is a second-order version of this risk worth naming — concentration. A portfolio that large, invested largely in U.S. investment-grade credit, is effectively a leveraged bet on the health of corporate America and the trajectory of U.S. rates. In a benign world that is a fine bet; in a world of stagflation, a credit cycle, or a disorderly move in long rates, it is a source of correlated losses precisely when the currency and equity books are also under strain. Cathay's risks do not arrive politely one at a time.

The credit-rating agencies provide a useful outside read here. Through the transition, Cathay Life held its Fitch Insurer Financial Strength rating in the 'A' range with a stable outlook, and the agency at one point removed a negative watch on Taiwanese life insurers as the sector's transition path clarified — an external, arm's-length signal that the balance sheet, while stretched, was being managed within tolerances rather than toward distress.7 Ratings are lagging and imperfect, but a stable 'A-' band from a skeptical third party is a meaningful counterweight to the more alarming transition-day equity optics.

Against that backdrop, how credible is management? On the evidence, Cathay's leadership deserves a genuinely mixed-to-favorable verdict rather than a cheerleading one. Chairman 蔡宏圖 Tsai Hong-tu has behaved, across cycles, as a disciplined capital allocator who prioritized balance-sheet stability over trophy acquisitions — a temperament visible in the decision to shore up capital ahead of the 2026 transition rather than be caught short, and one reinforced by the family's dominant shareholding, which aligns his interests tightly with long-term holders. On the execution side, the group's long-serving management, including president Chang-Ken Lee, oversaw a genuinely difficult multi-year IFRS 17 and digital-banking transition with more competence than many peers, and the double-engine model held up through shocks from COVID-era insurance payouts to currency whipsaws. On recent earnings calls, management has been notably concrete rather than evasive on the two subjects analysts press hardest — hedging cost and solvency — walking through the drivers of the RBC decline and the mechanics of the CSM build rather than retreating into reassurance.15 Concreteness under questioning is itself a credibility signal; management teams in trouble tend to get vaguer precisely where the numbers are worst, and Cathay's have not.

There is also a governance dimension a skeptical investor must weigh, and it cuts both ways. The Tsai family's dominant shareholding aligns management with long-term value — the people running Cathay are, overwhelmingly, spending their own family's money, which is the strongest antidote to the empire-building and short-termism that afflict widely held companies. But concentrated family control is a double-edged sword: it can entrench insiders, blunt independent board oversight, and make a company slow to change course when the family's preferences and shareholders' interests diverge. The Tenth Credit Cooperative scandal, whatever else it was, is a permanent reminder of what related-party dealing inside a family financial group can do. Cathay's modern governance is a world away from that era, and the ring-fencing lesson was learned in blood — but a neutral analyst keeps concentrated control filed under "risk to monitor," not "settled virtue."

But credibility is ultimately assessed on the misses, not only the hits. The Bank Mayapada episode is a real mark against the record: management was slow to identify the governance and credit risks in a bet it controlled poorly, and it cost shareholders the entire investment. The more reassuring counter-evidence is behavioral consistency in the years since — the pre-emptive capital raising ahead of 2026, the willingness to unwind the Conning experiment cleanly rather than defend a sunk cost, and a narrative across recent earnings calls that has stayed consistent on the hard subjects of hedging costs and solvency rather than shifting to obscure them. A fair investor holds both facts at once: disciplined and aligned at the core, but capable of expensive blind spots when it strays from the domestic franchise it understands. Watching whether management applies the hard lessons of Mayapada to future overseas ambitions, and whether it can navigate the 15-year capital runway without serial dilution, is the real test of the years ahead.

XII. Epilogue & Outro

Return, at the end, to the market stall in Miaoli. That three brothers who sold vegetables and soy sauce produced a dynasty that now sits at the center of Taiwan's financial system is a genuinely remarkable arc — but the more instructive part is what the family did with the empire once it had one. It partitioned rather than fought. It let a failing branch fail rather than infect the whole. It bought land when land was cheap, built distribution on trust, and bolted a steady bank onto a volatile insurer. The through-line across sixty years is not brilliance so much as a hard, unsentimental respect for boundaries — between entities, between currencies, between what you control and what you merely hope to.

It is worth remembering, too, the COVID chapter that this narrative has only glanced at, because it tested the model in a way no spreadsheet had modeled. When Taiwan's insurers sold cheap pandemic policies and then faced a wave of claims as infections surged, the industry absorbed billions in unexpected payouts — a live-fire drill in tail risk that the sector had not priced. Cathay came through it, capital intact, and the episode became one more entry in a long ledger of shocks survived: the cooperative run, the Asian financial crisis, the global financial crisis, the negative-spread era, the pandemic, and now the accounting cliff. A company's resilience is not a claim management makes; it is a record the years either write or refuse to write. Cathay's years have written it.

Those instincts carried Cathay through the worst cooperative crisis in the island's history, through a pandemic's insurance payouts, and into the most complex accounting regime finance has ever devised. The open question is whether they are enough for what comes next. Taiwan is entering an era of digital-first finance, where the relationship moats of the housewife-agent age erode and the winners are decided by app ecosystems, funding costs, and the disciplined compounding of unearned profit. Cathay enters that era as the larger, steadier, blue-blood incumbent — and its own cousins at Fubon enter it as the faster, hungrier challenger who has, for much of the modern era, earned the better return.

Whether the tortoise's conservatism finally gets its reward when the cycle turns, or whether the hare permanently secures the throne, is the story's unresolved final act. What is not in doubt is that the company built by vegetable sellers has become a fortress — and that, for a third of Taiwan's savers, the answer will be measured, as ever, in basis points.

References

-

Cathay Financial Holdings Posts Record NT$76.5 Billion First-Half Profit; Net Worth and Retained Earnings Hit All-Time Highs — BigGo Finance, 2026-07-15 ↩↩↩↩↩

-

Taiwan's Cathay Financial may up stake in Indonesia's Bank Mayapada to 51% — DealStreetAsia, 2020-07-15 ↩↩↩↩

-

Cathay Life to write off NT$14bn on Indonesia bank — Taipei Times, 2020-08-11 ↩

-

Generali completes the acquisition of Conning Holdings Limited and enters into a partnership with Cathay Life — Assicurazioni Generali, 2024-04-03 ↩

-

Cathay Financial Holding Co Ltd (TPE:2882) Q4 2024 Earnings Call Highlights: Record Profits — Yahoo Finance / GuruFocus, 2025-03-21 ↩↩↩↩↩

-

Cathay United Bank CUBE Card digital ecosystem and reward mechanics — Cathay United Bank, 2025-12-01 ↩

-

Fitch Ratings: Taiwanese Life Insurers Prepare for IFRS 17 and ICS Transition — Fitch Ratings, 2024-09-04 ↩↩

-

FSC outlines 15-year transition measures for Taiwan's insurance sector under ICS — Financial Supervisory Commission of Taiwan, 2023-11-28 ↩↩

-

Fitch Rates Cathay Life's Proposed USD Subordinated Dated Bond 'BBB+' — MarketScreener / Fitch Ratings, 2024 ↩

-

Cathay Financial Holding Q2 2025 Second Quarter Briefing — Cathay Financial Holding, 2025-08 ↩

-

Taiwan's Wealthiest Families: The Tsai Brothers of Fubon and Cathay — Forbes, 2025-05-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube