Fubon Financial Holding: The Underdog Dynasty of Taiwanese Finance

I. Introduction & Episode Roadmap

Walk into the lobby of the Fubon Xinyi Financial Center in Taipei and you are standing inside a bet that took sixty-five years to pay off. The tower sits in the same district as Taipei 101, a few blocks from the trading floors that move a meaningful slice of Asian capital, and it houses a company that at its peak in 2026 was worth more than NT$1.6 trillion — north of fifty billion US dollars — making 富邦金融控股股份有限公司 Fubon Financial Holding Co., Ltd. (2881.TW, listed on the Taiwan Stock Exchange, TAI) one of the two most valuable financial institutions the island has ever produced.1

That "one of two" is the whole story. Because just up the road sits 國泰金融控股股份有限公司 Cathay Financial Holding Co., Ltd. (2882.TW), and the two companies are not merely competitors. They are cousins. They were, quite literally, one family business that split apart in 1979, and for the four decades since, the branch that inherited the glamorous life-insurance empire (Cathay) and the branch that got handed the unglamorous property-and-casualty scraps (Fubon) have been racing to see which inheritance was actually worth more. By mid-2026 the two trade within a whisker of each other by market value — Cathay around US$53 billion, Fubon around US$49 billion — a photo finish that would have seemed absurd in 1979, when Fubon's founding asset was a single tiny insurance office and Cathay held the crown jewels.2

So how did the underdog get here? How did a company that started life as Taiwan's first, smallest property-and-casualty insurer build a conglomerate that now owns a top-tier commercial bank, the second-largest life insurer on the island, a leading securities house, one of the "Big Three" mobile carriers, and the dominant e-commerce platform in Taiwan — and did it largely by buying assets nobody else had the nerve or the timing to buy?

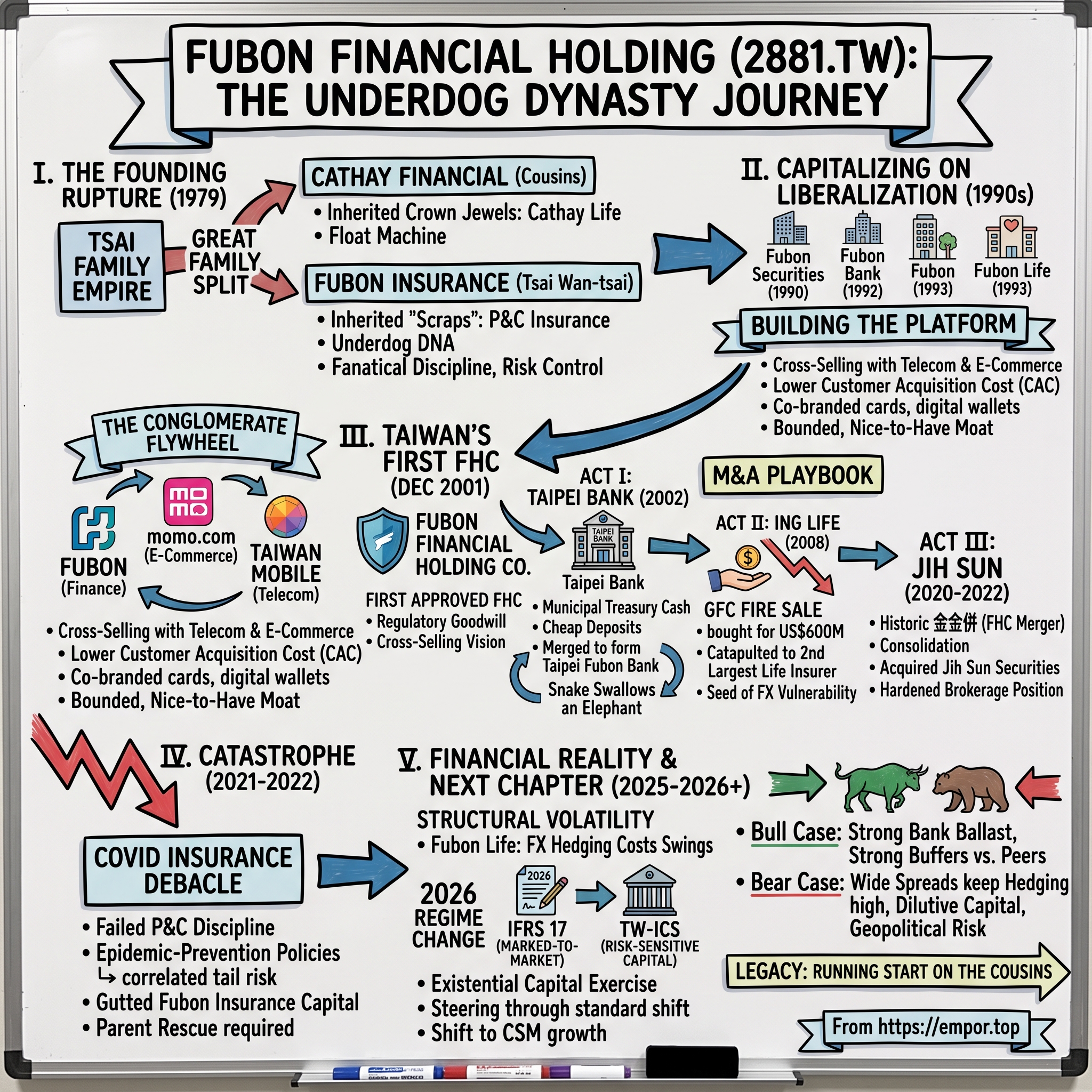

This is a story with a clear spine, and it is worth naming the vertebrae up front. First, the 1979 split of the Tsai family empire that gave Fubon its underdog DNA. Second, the sprint to become Taiwan's very first Financial Holding Company in December 2001. Third, a three-act M&A playbook that reads like a masterclass in buying when others are forced to sell: the politically explosive 2002 Taipei Bank acquisition, the counter-cyclical 2008 purchase of ING's Taiwan life business at the bottom of the Global Financial Crisis, and the landmark 2020–2022 takeover of Jih Sun that was the first time in Taiwanese history one financial holding company swallowed another. Fourth, the near-catastrophe of the 2022 COVID insurance debacle, when the family's own P&C roots nearly buried it. And fifth, the messy, unglamorous financial reality that defines the company today: a giant life insurer whose earnings swing violently on foreign-exchange hedging costs, now steering through the biggest accounting and solvency regime change in a generation as IFRS 17 and Taiwan's new insurance capital standard both land in 2026.

Along the way we will keep an independent eye on the ledger. Fubon's management tells a good story — record bank profits, disciplined M&A, a conglomerate flywheel — and much of it is true. But a company this complex, this leveraged to interest-rate spreads, and this exposed to the single most dangerous geopolitical fault line in the world deserves to have its claims tested rather than repeated. Let us start where the family did.

II. The Great Family Split: Cathay vs. Fubon

Picture Taiwan in the early 1960s: a poor, agrarian island under martial law, its financial system a state-run monopoly, its people accustomed to saving in gold and under mattresses because they trusted almost no institution. Into that vacuum stepped three brothers from a modest Miaoli farming family — Tsai Wan-chun, 蔡萬霖 Tsai Wan-lin, and 蔡萬才 Tsai Wan-tsai — who in 1962 seized on the government's first-ever licensing of private life insurers to co-found Cathay Life Insurance, the island's first private life insurer.3 It was an audacious move. Selling life insurance to a population that had just survived a war and hyperinflation meant selling something Taiwanese households had never bought before: a promise, backed only by paper, to be honored decades later.

They pulled it off, and spectacularly. Life insurance in a fast-industrializing, high-savings economy turned out to be one of the great business models of the twentieth century. Policyholders paid premiums for years before any claim came due, and that gap — the "float" — became an enormous, cheap, self-replenishing pool of capital the Tsais could invest in the land, buildings, and equities of a booming Taiwan. By the 1980s the family was among the richest in Asia, and Tsai Wan-lin would for years rank among the wealthiest men in the world.

But empires built by brothers rarely survive the second decade intact. In 1979 the Tsai clan formally divided its assets, a rupture driven by strategic disagreements and the ordinary gravitational pull of grown men wanting to run their own show.4 The division was profoundly asymmetric. Tsai Wan-lin kept the crown jewel — Cathay Life, the cash-gushing float machine that would eventually become Cathay Financial. His younger brother Tsai Wan-tsai was handed the consolation prize: the group's small, boring property-and-casualty insurance operation, a business that would later be renamed 富邦產險 Fubon Insurance.[^5]

Understand what that meant, because it is the psychological engine of everything that follows. Property-and-casualty insurance — car, fire, marine, liability — is a fundamentally different animal from life insurance. There is almost no float; policies are typically one year, premiums come in and claims go out on a short cycle, and a single bad year of typhoons or, as we will see, a pandemic, can vaporize a decade of profits. You cannot get rich slowly on accumulated float the way a life insurer can. You survive only through fanatical underwriting discipline, ruthless cost control, and a refusal to write business at prices that do not compensate for risk. Tsai Wan-tsai took the weaker hand and, out of necessity, built a culture around exactly those virtues — lean operations, obsessive risk control, and a demand that every unit of capital earn its keep.

He also drilled that mentality into his two sons, 蔡明忠 Daniel Tsai and 蔡明興 Richard Tsai, the men who run the empire today.5 The lesson the family absorbed from starting behind was that the incumbent's complacency is the challenger's opportunity — a worldview that would later justify some of the most aggressive deals in Taiwanese corporate history. When Tsai Wan-tsai died in 2014, Forbes still ranked the family among the richest in Asia, and the "underdog" had already begun to close the gap on the cousins who got the better inheritance.6

The irony, of course, is that the boring P&C business turned out to be the perfect launchpad — not because it made much money, but because it gave the family a licence, a brand, a distribution network, and a reason to be in the room when Taiwan's financial system finally cracked open. That crack came in the 1990s.

III. Capitalizing on Liberalization: From Beachhead to Taiwan's First FHC

For most of Fubon's early life, the deck was stacked by the state. Taiwan's banks were overwhelmingly government-owned, new licenses were rationed, and an entrepreneurial insurer could look at the sleepy, oligopolistic banking sector the way a hungry chef looks at a locked pantry. Then, in the early 1990s, as Taiwan democratized and its economy matured, the government did something that changed everything: it began issuing private licenses for banking, securities, and life insurance, dismantling the monopoly of the state-run institutions.

Fubon moved with a speed that would become its signature. Using the cash flow and the trusted brand of its P&C insurer as a beachhead, the family rapidly seeded an entire financial platform. 富邦證券 Fubon Securities came first, in 1990, riding the wave of a Taiwanese retail-investor culture that treats stock trading as something close to a national sport. 富邦銀行 Fubon Bank followed in 1992, and 富邦人壽 Fubon Life in 1993 — the family, notably, re-entering the very life-insurance business that had been given to the other branch of the clan fourteen years earlier.7

This was the strategic chess opening. Each piece was individually small; Fubon Bank in the 1990s was a minnow next to the state giants, and Fubon Life was a rounding error next to cousin Cathay's colossus. But the pieces were positioned. And the family understood something the incumbents did not fully price in: that the real prize would come when Taiwan allowed these separate businesses to be assembled under one roof and cross-sold to one another's customers.

That moment arrived in 2001. Taiwan passed the Financial Holding Company Act, explicitly designed to let banks, insurers, and securities firms sit under a single holding company and sell each other's products — bank tellers pitching insurance, insurance agents opening brokerage accounts, the whole "financial supermarket" model that had swept the US and Europe. Whoever moved first would get the branding, the regulatory goodwill, and a running start on integration.

Fubon won that race. In December 2001 it became the first officially approved financial holding company in Taiwan, incorporating its bank, insurer, securities arm, and life unit into a single listed entity.8 Being first was not a trophy; it was a genuine advantage. It signaled administrative competence to a regulator that would, over the next two decades, hold approval power over every acquisition Fubon wanted to make — and Fubon wanted to make a lot of them. The first test of that appetite came almost immediately, and it would drag a future president of Taiwan into a corruption scandal that outlived the deal by more than a decade.

IV. Act I of M&A: The Taipei Bank "Snake Swallowing an Elephant" Deal

Here is the problem Fubon faced in 2002. It had a shiny new holding-company structure and a grand cross-selling vision, but its bank was too small to matter. To build a bancassurance machine you need deposits — lots of cheap, sticky retail deposits — and Fubon Bank simply did not have them. What it needed was a large, deposit-rich commercial bank. And, improbably, one was about to come up for sale.

台北銀行 Taipei Bank was owned by the Taipei City Government, and it was a jewel. It held the city treasury's cash — a captive, near-zero-cost deposit base of enormous size. It had a prime branch footprint blanketing the wealthiest municipality on the island. And it held valuable public franchises, including a role in Taiwan's public-welfare lottery.9 For a challenger bank trying to lower its cost of funding overnight, Taipei Bank was close to a perfect target.

In 2002, Fubon won a public tender for it, bidding the highest price — NT$36 per share, a premium of roughly 37% — and merged the two institutions to create 台北富邦商業銀行 Taipei Fubon Commercial Bank.10 The name itself told the story: "Taipei" came first, because the acquired bank was the bigger, more established brand. Contemporaries called it "a snake swallowing an elephant" — the smaller Fubon Bank absorbing the larger, more profitable state institution.

And then came the firestorm. The mayor who signed off on selling this municipal crown jewel was 馬英九 Ma Ying-jeou, later President of Taiwan. Political opponents accused him of handing public assets to the Tsai family at a fire-sale price, alleging that municipal real estate had been valued at ancient historical book cost rather than market value. The scandal acquired a name that stuck for years: the "魚翅宴 fish-fin banquets," after revelations that Ma had attended private dinners hosted by Fubon's owners at an upscale shark-fin restaurant during the negotiation period.11 Critics pointed to the administrative speed of the approval — allegations that the merger cleared multiple layers of mayoral sign-off with unusual haste and secrecy — as evidence that the process had been greased. A civic group would still be filing corruption complaints against Ma over the deal as late as 2016, and Fubon would still be publicly refuting allegations of wrongdoing years after that.12 It is worth being precise here, as an independent observer: the accusations were political and legally contested, and Fubon has consistently denied any impropriety. What is not in dispute is that the optics were terrible and that the buyer got a very good price.

Because — and this is the uncomfortable truth for anyone keeping a neutral ledger — the deal was, in pure capital-allocation terms, a masterstroke. Overnight, Fubon acquired a mountain of cheap municipal deposits, slashing its cost of funding and giving it the low-cost liability base that every profitable bank is built on. It inherited an elite branch network in the capital and a ready-made channel to cross-sell Fubon's insurance and investment products to hundreds of thousands of affluent Taipei households. Today Taipei Fubon Bank is the single most reliable profit engine in the entire group, and its foundations were poured in 2002. The episode set a template Fubon would return to again and again: find an asset that is mispriced because its seller is distressed, constrained, or politically motivated to move quickly — and pounce. The next time it did so, the seller would be one of the largest financial institutions in Europe, and the catalyst would be the near-collapse of the global financial system.

V. Act II of M&A: The ING Life GFC Fire Sale

October 2008. Lehman Brothers had collapsed weeks earlier, credit markets were frozen, and across the West governments were nationalizing banks to stop the bleeding. In the Netherlands, the Dutch state was preparing a €10 billion capital injection into ING Group, and ING's management was doing what every over-extended financial giant was doing that autumn: hunting the balance sheet for anything it could sell to raise cash and shore up the parent. One of the assets on the block was ING's Taiwanese life-insurance business.

For most acquirers, the autumn of 2008 was a time to hide. For Fubon, it was Christmas. Richard Tsai led the group to strike an agreement to buy ING's Taiwan life operation for US$600 million, a deal announced in October 2008 and closed in February 2009.[^14] Consider the asymmetry of that price. Fubon was paying six hundred million dollars for a business carrying hundreds of billions of New Taiwan dollars in assets and an established agency salesforce of roughly seven-to-eight thousand agents.13 In normal times an insurer of that scale would have commanded a multiple of its embedded value; at the depths of the liquidity panic, with a forced seller desperate for cash, Fubon paid a fraction of it.

The strategic logic was even more powerful than the price. In a single stroke, the acquisition catapulted Fubon Life from a middling also-ran into the second-largest life insurer in Taiwan, trailing only — of course — cousin Cathay. The float machine that the family had been handed the wrong half of in 1979 was suddenly, forty years later, back in Fubon's hands at industrial scale. Integrating the legacy Fubon Life with the acquired ING book gave the group a life-insurance division large enough to become its dominant earnings contributor, at times generating the majority of consolidated group profit over the following decade.

But — and here the independent lens matters — this is the deal that also planted the seed of Fubon's biggest structural vulnerability. A life insurer of that size collects premiums in New Taiwan dollars and owes claims in New Taiwan dollars, yet Taiwan's domestic bond market is far too small and too low-yielding to invest NT$5 trillion of policyholder money at rates that cover the guarantees embedded in old policies. So the money has to go abroad, mostly into US-dollar bonds — and that, as we will see in Section IX, is the crack through which foreign-exchange volatility now floods the income statement every single quarter. The 2008 deal made Fubon a giant. It also made Fubon a giant currency-mismatched bond portfolio wearing an insurance company as a costume. Both things are true at once, and any honest telling has to hold them together.

For now, though, the ledger read triumph. Two acts of the M&A playbook were complete: a bank bought from a government under political fire, and a life insurer bought from a European giant under financial fire. The next phase would be less about crisis-buying and more about turning the sprawling group into a machine whose parts fed each other — a conglomerate flywheel connecting finance to phones and shopping carts.

VI. The Conglomerate Flywheel: Cross-Selling with Telecom and E-Commerce

Most financial conglomerates are just banks and insurers stapled together. Fubon is stranger and, in some ways, more interesting than that — because the Tsai family also controls a major telecom carrier and the dominant e-commerce platform in Taiwan, and it deliberately wires all of them together.

Start with the people, because Fubon's governance is genuinely unusual among Asian dynasties. Rather than a single autocrat or a bitter succession war, the two brothers who inherited the empire divided it along a clean seam. Daniel Tsai, the elder, generally presides over the wider Fubon Group and its non-financial media and telecom assets; Richard Tsai runs the financial holding company itself.14 The division of labor has held for decades without the public feuding that has hollowed out so many family conglomerates in the region — a genuine, if underappreciated, competitive asset, because coordinated family control lets Fubon make cross-company bets (a bank integrating with a telco's wallet, say) that a normal arms-length conglomerate could never align.

The two non-financial giants are serious businesses in their own right. 台灣大哥大 Taiwan Mobile (3045.TW) is one of the "Big Three" mobile carriers on the island, with millions of subscribers and, crucially, a billing relationship with a huge chunk of the Taiwanese population. 富邦媒體科技 momo.com (8454.TW) is the undisputed leader of Taiwanese business-to-consumer e-commerce — the local Amazon, essentially, with the logistics network, the daily consumer traffic, and the purchase data that implies.

Now watch the flywheel turn. The Fubon-momo co-branded credit card, issued in the millions, gives Taipei Fubon Bank something that pure-play banks pay dearly for: near-zero-cost customer acquisition, funneled straight from momo's shopping checkout into the bank's card portfolio, along with a rich stream of transactional data on what those customers actually buy. Taipei Fubon Bank integrates into Taiwan Mobile's payment gateways and digital wallets, capturing sticky retail deposits and payment flows from a captive telecom base. The insurance and wealth-management arms can then market to those same identified, data-rich customers.

Here is where the independent investor should apply a healthy discount, though. "Ecosystem synergy" is one of the most over-claimed concepts in all of finance, and Fubon's version is real but bounded. The co-branded card and wallet integrations genuinely lower acquisition costs at the margin, and in a small, saturated market like Taiwan that edge is worth having. But there is little public evidence that owning a telecom and an e-commerce platform generates the kind of transformative, compounding advantage that the word "flywheel" implies; Taiwan Mobile and momo compete hard in their own cut-throat markets and are valued as such, not as captive lead-generation machines for the bank. The synergy is a nice-to-have that sharpens Fubon's retail moat — not, on the current evidence, a moat unto itself. The more important consolidation move of the modern era was not about phones or parcels at all. It was Fubon doing to a rival what it had once done to Taipei Bank: swallowing something whole.

VII. Act III of M&A: The Historic Jih Sun Consolidation

By the late 2010s, Taiwan had a problem its regulators openly acknowledged: too many banks and financial holding companies, most of them sub-scale, all of them competing away each other's margins in an overbanked market. The government wanted consolidation but had been reluctant to force it. Fubon, ever the opportunist, decided to demonstrate how it could be done.

The target was 日盛金融控股 Jih Sun Financial Holding Co., Ltd., a mid-tier holding company whose real prize was 日盛證券 Jih Sun Securities, a brokerage with an unusually strong retail footprint and a well-regarded trading franchise. Fubon began accumulating a stake and, in December 2020, launched a tender offer — the opening move in what would become the first "金金併" (financial-holding-on-financial-holding) merger in Taiwan's history, a genuine first that other conglomerates had talked about for years but never executed.15

The deal was completed in stages. Fubon's tender offer succeeded, regulatory approval came through in 2022, and the two holding companies formally merged on November 11, 2022 — the estimated total consideration around NT$26.4 billion, pricing Jih Sun at roughly book value rather than the giveaway multiples of Fubon's crisis-era deals.16 The subsidiary-level mergers followed in April 2023, folding Jih Sun's bank and securities units into their Fubon counterparts.17

Contrast the character of this deal with the first two acts, because it reveals how Fubon's playbook matured. Taipei Bank and ING were opportunistic grabs of mispriced assets from distressed or motivated sellers, bought at fractions of fair value. Jih Sun was different: a fully-priced, strategically-chosen consolidation of a healthy business, executed patiently over two years and paid for at a fair multiple. Fubon was no longer just a bottom-fisher; it was using its scale and regulatory standing to lead industry structure. Merging Jih Sun Securities into Fubon Securities pushed Fubon's brokerage market share firmly into the top tier, hardening its position against rivals like 元大 Yuanta, and Fubon Securities went on to post record profits exceeding NT$10 billion for two consecutive years through 2025.18 Merging Jih Sun's bank added branches and SME relationships to Taipei Fubon's network.

An activist skeptic would still ask the fair question: does bolting together sub-scale brokerages and banks in an overbanked market create durable value, or just a bigger version of a low-return business? Taiwanese brokerage is cyclical and fee-competitive, and "top-tier market share" in a commoditized business is not the same as pricing power. The honest answer is that Jih Sun made Fubon bigger and modestly more diversified without obviously making it structurally more profitable — a reasonable, disciplined deal rather than a transformative one. And whatever synergies it unlocked would soon be overshadowed by a self-inflicted disaster brewing inside the very business the family had started with: property and casualty insurance.

VIII. Underwriting Catastrophe: The COVID-19 Epidemic Policy Crisis

Every so often an entire industry walks, eyes open, off the same cliff — and the wreckage teaches a lesson no textbook can. Taiwan's 防疫保單 epidemic-prevention insurance debacle of 2021–2022 is one of those events, and Fubon, the company whose founding DNA was supposedly fanatical P&C underwriting discipline, was right at the front of the herd.

Here is what happened. In 2021, Taiwan was a global success story in containing COVID-19. Case counts were minuscule, the "zero-COVID" strategy of aggressive quarantine was working, and to the Taiwanese public — and, fatally, to Taiwanese actuaries — the probability of any given person being quarantined or diagnosed looked vanishingly small. So the island's P&C insurers, Fubon Insurance prominent among them, sold millions of cheap epidemic-prevention policies. For a premium of only a few hundred New Taiwan dollars, a policyholder could collect tens of thousands if they were quarantined or diagnosed with COVID. When the disease is essentially absent, that is nearly free money — a high-volume, low-claim product that boosts premium income and looks like a triumph of distribution.

You can already see the trap. The premise held only as long as Taiwan's near-zero case count held. In mid-2022, facing the far more transmissible Omicron variant, Taiwan abandoned zero-COVID and let the virus circulate. Cases exploded from a handful a day into the tens and hundreds of thousands. And every one of those millions of policies became a live claim, all at once, all correlated to the same single event.

The result was a bloodbath that made a mockery of the "disciplined underwriter" story. Across the industry, epidemic policies had collected roughly NT$5.5 billion in total premiums against claims that soared past NT$270 billion — a loss ratio so grotesque it belongs in actuarial textbooks as a warning.19 Fubon Insurance's own capital was gutted: its reported capital and surplus collapsed by roughly 88%, from about NT$45.4 billion at the end of 2021 to just NT$5.2 billion a year later, dragging it toward the statutory Risk-Based Capital solvency floor.[^22] The parent had to mount a rescue. Fubon Insurance received a capital injection of about NT$15 billion in August 2022, followed by a second raise of around NT$16 billion in May 2023, to pull the subsidiary back from the brink.[^23]

The analytical lesson here is sharper and more damning than "pandemics are unpredictable." It is a lesson about correlation and tail risk in high-volume underwriting. A P&C insurer's entire model rests on the claims being independent — one house fire does not cause the next. Epidemic policies violated that principle at the deepest level: a single policy decision by the government could, and did, turn every policy into a claim simultaneously. Fubon, the company that supposedly learned counter-cyclical caution at Tsai Wan-tsai's knee, wrote a book of business whose losses were perfectly correlated to one binary event it did not control. The founding virtue failed exactly where it mattered most. For investors, the episode is a permanent reminder that the P&C arm, small as it is in the group, can generate sudden, capital-threatening losses that force the parent to divert billions from better uses. And it is not even the largest source of earnings volatility in the group. That distinction belongs to the life insurer, and to a problem that never goes away: the currency.

IX. The Double-Edged Sword: Fubon Life's High-Beta Foreign Exchange Realities

To understand the single most important thing about Fubon as an investment, you have to understand a structural bind that has nothing to do with management skill and everything to do with arithmetic. Fubon Life sits on over NT$5 trillion of assets — money it holds against decades of promises to policyholders, many of them old policies carrying guaranteed yields the insurer must earn or eat the difference.20 The trouble is that Taiwan's own bond market is small and its interest rates are structurally low, far too low to fund those guarantees. So Fubon, like every large Taiwanese life insurer, does the only thing it can: it sends the majority of that money overseas, chiefly into higher-yielding US-dollar bonds.

Now the mismatch bites. The assets earn dollars; the liabilities are owed in New Taiwan dollars. If the NT dollar strengthens against the greenback, the value of that vast foreign portfolio shrinks in home-currency terms — enough, in a bad move, to wipe out a year's earnings. To defend against that, Fubon hedges its currency exposure using swaps and foreign-exchange derivatives. Think of hedging as an insurance policy on the insurance company's own investments: it caps the currency risk, but it costs a premium, and that premium is brutally variable. When the gap between US and Taiwanese interest rates is wide — as it has been for much of the recent cycle — the cost of hedging can swallow one to two percentage points or more of Fubon Life's entire investment yield. In other words, a chunk of the extra return Fubon reaches abroad to capture is handed straight back to the counterparties who sell it protection. This is the "high beta" at the heart of the company: in good FX years the life insurer mints money, and in bad ones the same book of business produces mediocre results, with little that management can do about the underlying spread.

The numbers of 2025 make the point with painful clarity. Fubon Life had reported life-insurance net income of about NT$102.66 billion in 2024, a banner year. Then, in June 2025, following an FSC directive that let insurers adjust their liability-reserve basis, Fubon Life was required to make a one-time mandatory provision of NT$28.1 billion into its foreign-exchange volatility reserve — equal to roughly 30% of its pre-tax profit for the year — a charge that dragged the unit to a net loss in December and cut full-year life-insurance net income to roughly NT$62.5 billion.21 On a pro-forma basis, stripping out that one provision, Fubon Life's pre-tax profit for 2025 would have been on the order of NT$120 billion — which tells you the underlying business was strong and the reported collapse was, in large part, a regulatory and currency-reserve artifact.22 That is precisely the problem: a casual reader sees earnings nearly halve; the reality is a mandated bookkeeping move against FX risk. Distinguishing the two is the whole job of analyzing this company.

The 2026 Regulatory Regime Change: IFRS 17 & TW-ICS

All of this is now colliding with the biggest rule change in the history of the Taiwanese insurance industry, and it lands in 2026. Two things are happening at once. IFRS 17, the new global insurance-accounting standard, changes how legacy insurance liabilities are measured — moving from stale historical assumptions toward current, marked-to-market interest rates. Alongside it comes TW-ICS, Taiwan's localized version of the international Insurance Capital Standard, a far more risk-sensitive solvency regime that demands insurers hold capital calibrated to the real market risk in their portfolios.

For a company with Fubon Life's enormous, currency-mismatched, interest-rate-sensitive balance sheet, this is an existential-scale capital exercise, and Fubon has been visibly racing to build buffers ahead of the deadline. In September 2025, Fubon Life sold US$650 million of subordinated bonds — a 10.25-year note at a 5.45% coupon, issued through an offshore Singapore special-purpose vehicle and guaranteed by Fubon Life — explicitly to strengthen its financial structure and lift its capital-adequacy ratio ahead of the TW-ICS transition.23 Management has also signaled a deliberate shift in what it sells, steering away from the old high-guaranteed-yield savings policies toward protection-oriented and participating products that generate Contractual Service Margin — the store of future profit that IFRS 17 rewards, which we will unpack in Section XI.

The neutral read: the transition is genuinely dangerous for weaker insurers and manageable, but not free, for Fubon. Raising Tier-2 subordinated debt at a 5.45% coupon to shore up capital is a real cost that dilutes returns, and it is exactly the kind of "raise expensive capital to satisfy the regulator" dynamic that the bear case fixates on. Whether Fubon emerges from 2026 with a comfortable buffer or a strained one is the central open question in the stock — and it sets up the full bull-versus-bear debate. First, though, the lessons.

X. Playbook: Business & Investing Lessons

Step back from the sixty-five-year sweep and a handful of durable principles fall out of the Fubon story — some of them flattering to management, some of them cautionary, all of them useful to an investor trying to decide what this company actually is.

The first lesson is that M&A, done at the right moment, can be a core competency rather than a value-destroying vanity. Fubon's three defining deals share a pattern that is easy to describe and hard to execute: buy when the seller is constrained. Taipei Bank came out of a government privatization under political pressure in 2002; ING Taiwan came out of a European giant's crisis-driven fire sale in 2008; Jih Sun came out of a regulatory push for consolidation around 2020. Fubon's edge was not clairvoyance but readiness — a strong capital position, a fast-moving regulator-savvy management, and the institutional nerve to act when peers were frozen. The caution attached to this lesson is equally important: the best two of those three deals were only available because of dislocations that come along once a decade. A company cannot compound on crisis-buying alone, and much of Fubon's ordinary-times growth looks like the ordinary-times growth of any large Taiwanese financial group.

The second lesson is the genuine, if bounded, value of the cross-selling conglomerate. Fubon really does acquire banking and card customers more cheaply than a standalone bank could, by tapping momo's checkout and Taiwan Mobile's subscriber base. In a small, saturated market where customer-acquisition cost is the difference between profit and loss, that edge is worth something. But as noted, it is a sharpening stone, not a sword — helpful at the margin, not a category-defining moat.

The third lesson is the one the numbers scream: the solvency and earnings volatility of a cross-border life insurer is structural, not a passing phase. Collecting float and reaching abroad for yield is a wonderful business in the years when the currency and rate environment cooperates, and a grinding, capital-hungry one when it does not. Investors who buy Fubon for its "record profits" without understanding that a wide US–Taiwan rate spread can turn a banner year into a mediocre one — overnight, through no fault of management — are not really understanding what they own.

And the fourth lesson is the quiet one about governance. The symmetrical division of the empire between Daniel and Richard Tsai has, for decades, spared Fubon the inheritance wars that have wrecked other Asian dynasties. Family control concentrates decision-making and enables coordination that arms-length conglomerates cannot match; it is also, inevitably, a governance risk if the next generation's transition is less harmonious than the last. Which brings us to the question every investor ultimately has to answer: from here, does Fubon win, and what breaks the case?

XI. Analysis: Bull vs. Bear Case & Key KPIs

Let us war-game this properly, using the frameworks that force discipline on a story as sprawling as Fubon's.

Porter's Five Forces and the 7 Powers

Run Fubon through Porter's Five Forces and the picture is a mature, structurally competitive industry rather than a fortress. Rivalry is intense — Taiwan is chronically overbanked and over-insured, with more than a dozen financial holding companies knifing each other on price, which is precisely why the regulator wants consolidation. The threat of new entrants is low (licenses are scarce and capital requirements enormous), which is Fubon's friend. Buyer power is high and rising, as digital-savvy Taiwanese consumers shop rates for deposits, insurance, and brokerage with a few taps. Supplier power, in the odd sense that matters here, shows up as the cost of capital and the cost of FX hedging — and the counterparties who sell that hedging protection extract real economic rent from every Taiwanese life insurer. Substitutes are the slow, real threat: fintech payments, digital-only banks, and passive index products all chip at the edges of the traditional model.

Apply Hamilton Helmer's 7 Powers and Fubon holds a few real ones. It has genuine Scale Economies: spreading the fixed cost of running a NT$5 trillion investment operation and a nationwide branch and agency network over one of the largest asset bases on the island lowers unit costs in a way sub-scale rivals cannot match. It has Switching Costs, most concretely at Taipei Fubon Bank, whose role as the treasury bank for Taipei City and its deep, multi-product SME relationships make it painful for those clients to leave. And it arguably holds a Cornered Resource in that municipal treasury relationship and its associated public franchises — an asset a competitor simply cannot replicate by spending money. What Fubon does not obviously have is Branding power that commands premium pricing, or Network Economies in its core financial products. In Helmer's terms, Fubon is a scale-and-switching-cost business, not a pricing-power business — which is exactly why its returns live and die on cost of funding, cost of capital, and cost of hedging rather than on the prices it can charge.

The KPIs That Actually Matter

Ignore the dozens of line items and watch three things.

First, Contractual Service Margin (CSM) accumulation at Fubon Life. Under IFRS 17, CSM is the deferred, unearned profit embedded in the insurance book — the store of future earnings that gets released into income over the life of the policies. It is, more than any single quarter's net income, the truest forward indicator of life-insurance profitability under the new regime, and whether Fubon's shift toward protection and participating products is genuinely building CSM is the question that determines the next decade of the stock.

Second, net hedging costs as a percentage of foreign-investment assets. This is the swing factor that makes or breaks any given quarter for the life unit, the number that turned 2025's underlying strength into a reported loss month. When the US–Taiwan rate spread narrows and hedging cheapens, Fubon Life's yield expands; when it widens, the yield compresses. An investor who tracks this one ratio understands more about Fubon's near-term earnings than one who reads the entire press release.

Third, Taipei Fubon Bank's net interest margin and wealth-management fee growth. The bank is the ballast — the stable, compounding counterweight to the insurer's mood swings — and its NIM and fee trajectory tell you whether that ballast is holding.

The Bull Case

The optimistic case is coherent and rests on real evidence, not just management rhetoric. Fubon enters the 2026 IFRS 17 / TW-ICS transition from a position of relative strength, having pre-funded capital (the US$650 million subordinated issue among other moves) and carrying superior buffers to weaker peers who may be forced into distressed capital raises — a setup where, in true Fubon fashion, the strong could pick over the wreckage of the weak. The bank provides genuine, growing ballast: Taipei Fubon Bank delivered a record NT$36.33 billion of net profit in 2025, up 19% year-on-year, a reliable hedge against insurance volatility.24 The whole group posted 2025 net income of about NT$120.85 billion and industry-leading EPS of roughly NT$8.36, and Q1 2026 opened with NT$33.55 billion of net income and NT$2.40 of EPS — evidence that the underlying earnings power is intact even through the reserve turbulence.25 And the digital integration with momo and Taiwan Mobile continues to capture younger retail deposit and credit customers at low cost. If hedging costs normalize as US rates ease, the life unit's suppressed reported earnings could snap back sharply.

The Bear Case

The bear case is equally grounded, and it is mostly about things management does not control. The first is persistence: if the US–Taiwan interest-rate differential stays wide, elevated hedging costs will keep suppressing life-insurance returns indefinitely, and no amount of product-mix cleverness fully offsets a structural spread. The second is capital: TW-ICS may force Fubon to keep raising capital — dilutive equity or high-coupon subordinated debt like that 5.45% note — to satisfy an ever-more-demanding solvency regime, dampening return on equity even as headline profits look fine. The third is the one no framework can price: geopolitics. Fubon is a leveraged, capital-market-sensitive proxy for Taiwan itself, and a serious cross-strait escalation would trigger exactly the kind of systemic capital outflow and currency stress that its balance sheet is least equipped to absorb. This is not a risk that can be hedged away with swaps; it is the reason a Taiwanese financial holding company will always trade with a discount that a Singaporean or Japanese peer does not carry.

Weigh it honestly and Fubon is neither the invincible compounder its investor-relations deck implies nor the accident waiting to happen the 2022 COVID debacle might suggest. It is a well-run, scale-advantaged, family-controlled financial conglomerate with a genuinely strong bank, a structurally volatile insurer, and a set of tail risks — regulatory, currency, and geopolitical — that are large, real, and largely exogenous. The next chapter of the story will be written not by another audacious acquisition, but by how the third generation and the current leadership steer that balance sheet through the regime change of 2026 and whatever the cross-strait relationship does next.

XII. Epilogue & Outro

Sixty-five years is a long arc for a company that began as the runt of a family litter. From a single small property-and-casualty office — the piece of the empire nobody in 1979 wanted — Fubon built a group spanning commercial banking, the second-largest life insurer on the island, a top-tier securities house, a major mobile carrier, and the leading e-commerce platform in Taiwan, and it did so largely by being the buyer with cash and nerve when everyone else was a seller.

Tsai Wan-tsai took the weaker hand and, through discipline and opportunism, very nearly beat the brother who took the stronger one; by 2026 the two branches of the family stand shoulder to shoulder at the top of Taiwanese finance, the underdog's inheritance now worth almost exactly as much as the crown jewels. His sons preserved the unity that so many dynasties squander, and the empire enters its next phase intact.

What it does not enter is a period of calm. The company that starts this decade must prove it can carry a NT$5 trillion currency-mismatched insurer through the most demanding accounting and capital regime its industry has ever faced, keep its bank compounding, and do all of it in the shadow of a geopolitical risk no spreadsheet can fully model. The legacy of the P&C underdog was to teach a family that starting behind is survivable. Whether that lesson is enough for the challenges of 2026 and the third-generation transition beyond it is the open question at the heart of the Fubon story — and, for now, it remains genuinely open.

References

-

Fubon Financial (2881.TW) — Market capitalization — CompaniesMarketCap ↩

-

Tsai led family to dominate nation's finance business — Taipei Times, 2004-09-29 ↩

-

Taipei Fubon wins right to run nation's first sports lottery — Taipei Times, 2007-09-04 ↩

-

Fubon Financial refutes allegations of wrongdoing in 2002 Taipei Bank takeover — S&P Global Market Intelligence ↩

-

Group files corruption lawsuit against Ma over Fubon — Taipei Times, 2016-10-19 ↩

-

Fubon Financial refutes allegations of wrongdoing in 2002 Taipei Bank takeover — S&P Global Market Intelligence ↩

-

Fubon Rises in Taiwan on Plan to Buy ING Unit for $600 Million — Bloomberg, 2008-10-20 ↩

-

Fubon Financial offer for Jih Sun Financial succeeds — Taipei Times, 2021-03-24 ↩

-

FSC approves the merger of Fubon Financial and Jih Sun Financial — Financial Supervisory Commission, 2022-11-16 ↩

-

Bank, Securities and Futures have Successfully Completed the Merger — Fubon Financial, 2023-05-24 ↩

-

Press Release for the 2025 Annual Investor Conference — Fubon Financial ↩

-

Taiwan's Insurance Industry: A Story of Financial Resilience — The Actuary Magazine ↩

-

Taiwan's Life Insurers Face Crucial Currency Hedging Costs — Financial Times ↩

-

Fubon Financial Reports 2025 Profit of NT$120.85 Billion; Life Unit's One-Time Provision of NT$28.1 Billion — BigGo Finance ↩

-

Fubon Financial Holdings Reports December 2025 Earnings Results — Fubon Financial, 2026-01-13 ↩

-

Fubon Life Insurance sells US$650m of bonds — Taipei Times, 2025-09-05 ↩

-

Press Release for the 2025 Annual Investor Conference — Fubon Financial ↩

-

Fubon Financial Holdings Reported Net Income of NT$33.55 Billion for the First Quarter of 2026 — Fubon Financial ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube