Ajinomoto Co., Inc.: The Alchemy of Amino Acids and the AI Semiconductor Monopoly

I. Introduction & Episode Roadmap

Picture a modern data center in Texas, humming with the world's most expensive silicon. Racks of Nvidia Blackwell GPUs draw enough electricity to power a small town, each chip carrying a price tag north of $30,000. Now zoom in—past the fans, past the copper, past the wafer itself—to the thin organic substrate that carries the processor and connects it to the outside world. Laminated into that substrate is an ultra-thin insulating film, invisible to the naked eye, thinner than kitchen cling wrap. If that film cracks, warps, or traps an air bubble, the chip fails. And here is the punchline that has fascinated engineers and finally, in 2026, activist investors: that film is made almost exclusively by a 118-year-old Tokyo company best known for a white crystalline seasoning your grandmother sprinkled into soup.

The film is called Ajinomoto Build-up Film, or ABF, and its maker holds greater than 98% of the global market for the high-performance insulating layers used in advanced CPU and GPU packaging.1 The company controls well over 90% of the insulating material used across PC and data-center server chips.2 It is, by almost any definition, a monopoly sitting at a single point of failure for the entire AI hardware build-out. And it is owned by 味の素株式会社 Ajinomoto Co., Inc.—the inventor of monosodium glutamate, maker of frozen gyoza, and a household name across East Asia, Southeast Asia, and Latin America.

That is the core paradox this story pulls apart. How did a company founded to commercialize the taste of kelp broth end up as the quiet bottleneck of the global semiconductor supply chain? The answer is not a lucky accident dressed up as strategy. It is a story about amino acid chemistry, industrial-scale fermentation, a health panic that forced a pivot, and the strange serendipity by which the by-products of an MSG factory became one of the highest-margin materials in electronics.

The story also has a dramatic human hinge. In February 2025, Ajinomoto's board announced that CEO 藤江 太郎 Taro Fujie—the executive widely credited with the company's capital-efficiency turnaround—would step down after a health crisis, and be replaced by 中村 茂夫 Shigeo Nakamura.3 Nakamura is not a food executive. He is the research chemist who, as an "up-and-coming researcher" in the mid-1990s, led the team that invented ABF.1 For the first time in its history, Ajinomoto is run by a scientist from the electronic materials side of the house.

Then, in March 2026, London-based activist Palliser Capital arrived with a public campaign titled a "Value Enhancement Plan," arguing that Ajinomoto is "the most under-monetised AI infrastructure monopoly" on the planet and demanding a 30%-plus price hike on ABF and a spin-off of the electronics business.4 The stress test had begun.

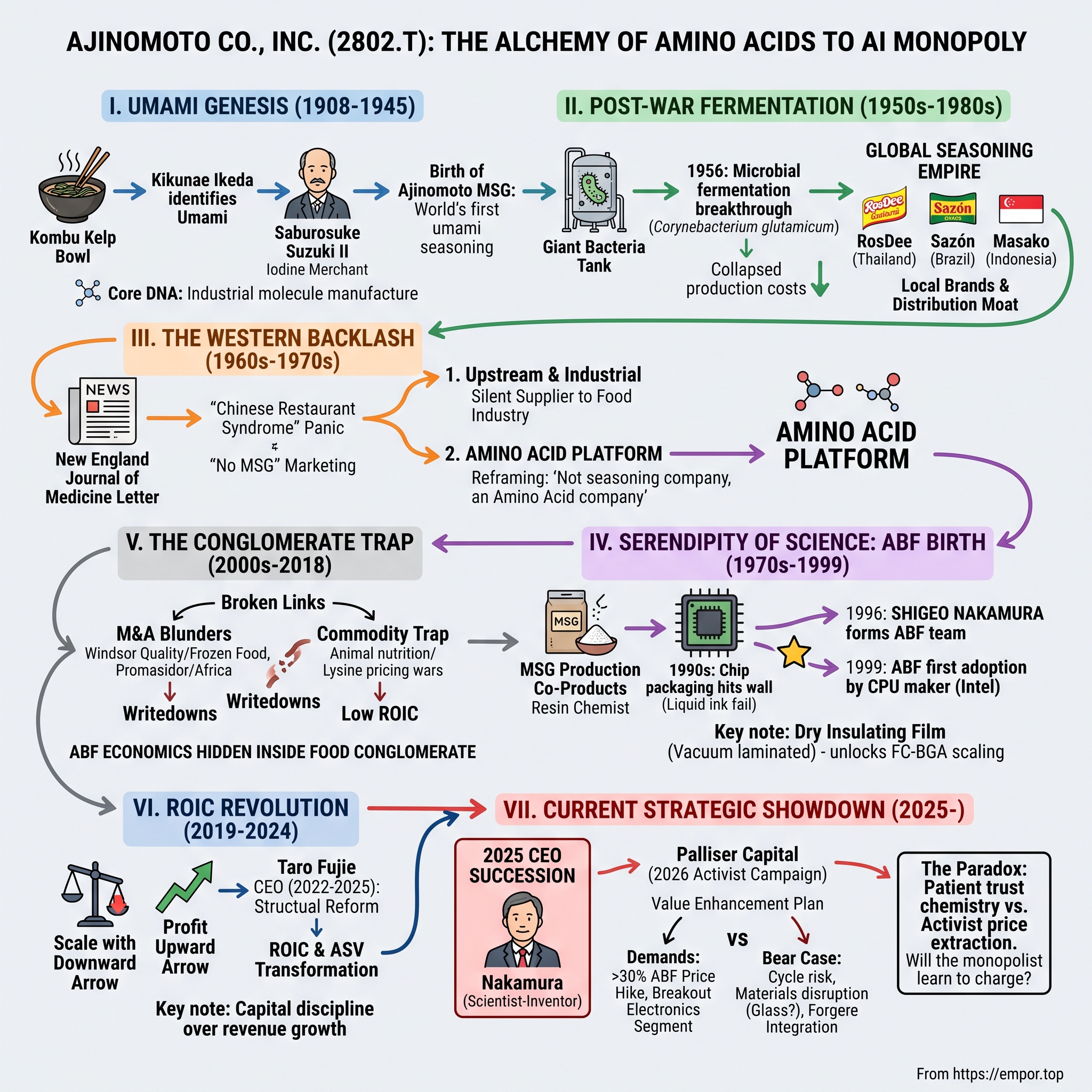

Here is the roadmap. We start with the scientific discovery of 旨味 umami and the birth of MSG; the shift from seaweed extraction to mass-scale microbial fermentation; the "Chinese Restaurant Syndrome" backlash that capped Western retail growth and pushed Ajinomoto deeper into industrial amino acids; the serendipitous epoxy chemistry that produced ABF; the conglomerate trap of value-destructive M&A; the return-on-invested-capital revolution; the 2025 succession and the biotech bet; the segment economics and the moat; and finally the activist showdown and the bull-versus-bear case. Let's begin where all of it began—with a professor tasting soup.

II. The Umami Genesis: Kikunae Ikeda & Saburosuke Suzuki (1908–1945)

In 1908, a chemistry professor at Tokyo Imperial University sat down to a bowl of dashi, the clear broth made from kombu kelp that anchors Japanese cooking. 池田 菊苗 Kikunae Ikeda had studied in Leipzig under the physical chemist Wilhelm Ostwald, and he brought a European laboratory's rigor to a very Japanese question: why did this broth taste good in a way that could not be explained by sweet, sour, salty, or bitter? He suspected a fifth basic taste. Working through the kelp broth, Ikeda isolated brown crystals of glutamic acid and concluded that the sodium salt of glutamate was responsible for the savory, mouth-filling quality he named 旨味 umami—literally "essence of deliciousness."5

This was not merely a culinary curiosity. Ikeda had identified, and in 1908 patented, a manufacturing process for a taste. The scientific community would take most of a century to formally accept umami as a fifth basic taste alongside the classic four, but Ikeda understood immediately that he had something commercial. A pure compound that made bland food delicious was, in the language of a later era, a platform.

Ikeda needed a businessman. He found one in 鈴木 三郎助 Saburosuke Suzuki II, an iodine merchant from a family trading company. In 1909 the two launched the sodium salt of glutamic acid under the brand name Ajinomoto—味の素, "essence of taste"—introducing the world's first umami seasoning to the market.5 The scientist supplied the chemistry; the merchant supplied the capital, the factory, and the nerve.

The early years were brutal, and this is the part the modern monopoly tends to obscure. The first production method relied on acid-hydrolysis of wheat gluten and defatted soybean—breaking down protein with hydrochloric acid to liberate glutamic acid. It was expensive, low-yield, and violently corrosive. Suzuki reportedly sold family assets to fund the Kawasaki factory, and the physical plant fought a constant war against acid that ate through equipment. Consumers, meanwhile, were suspicious of a white powder that came from a chemistry lab rather than a kitchen. Early marketing had to convince Japanese housewives that a laboratory crystal belonged in their soup—an audacious ask in an era with no concept of processed-food branding.

What Suzuki got right was distribution and identity. Ajinomoto tied itself to the modernization of the Japanese kitchen and, through it, to national industrial pride. By the interwar decades the brand had built early distribution networks into Taiwan, mainland China, and the United States, becoming a household staple across East Asia well before the Second World War. The little red-capped shaker became shorthand for modern cooking.

For investors, the founding era carries a lesson that echoes through everything that follows: Ajinomoto's DNA was never "food." It was the industrial-scale manufacture of a purified molecule, sold under a trusted brand. Glutamate was simply the first molecule. The corrosive wheat-hydrolysis process would soon prove to be a dead end on cost—and the search for a better way to make the same molecule would reshape the entire company. That search led straight to a bacterium.

III. Post-War Fermentation & The Global Seasoning Empire (1946–1980s)

Japan emerged from the war flattened, and Ajinomoto emerged with a chemistry problem it could no longer afford. Acid-hydrolysis of wheat was too costly and too capital-intensive to serve a mass market. The breakthrough, when it came in the mid-1950s, did not come from a chemistry department but from microbiology.

In 1956, Ajinomoto and Japanese researchers pioneered the production of glutamate through microbial fermentation, using a soil bacterium later classified as Corynebacterium glutamicum. The idea was elegant to the point of alchemy: feed cheap agricultural sugars—molasses, cassava starch, sugar-beet syrup—to a living culture of bacteria, and let the microbe's own metabolism excrete glutamic acid, which could then be crystallized and purified. Instead of tearing protein apart with acid, Ajinomoto now grew its product in giant aerated tanks.

The economic consequence was staggering. Production costs collapsed, and MSG transitioned from a premium chemical compound into a global mass-commodity ingredient. But the deeper prize was the capability. Large-scale aerobic fermentation is genuinely hard: it requires exquisite control of culture-media design, sterility, oxygen transfer, temperature, and the downstream art of crystallizing and purifying a single amino acid to high purity at industrial volume. Ajinomoto spent decades mastering a process that competitors could copy in principle but rarely match on cost and consistency. This fermentation expertise—not any single product—became the company's true core competency, and it is the same competency that would later underwrite pharmaceutical-grade amino acids and, indirectly, the raw materials for ABF.

Ajinomoto also made a distribution decision in this era that looks prescient in hindsight. Rather than exporting seasoning from Japan, it built local fermentation plants close to local feedstocks and local tastes—Brazil in 1956, Thailand around 1960, Indonesia in 1969—and, crucially, built local brands rather than pushing the Japanese label. In Thailand it became RosDee; in Brazil, Sazón; in Indonesia, Masako. These were not translations of a Tokyo product but locally formulated seasonings woven into national cuisines.

This is worth dwelling on, because it is the source of a moat that has nothing to do with semiconductors. A homemaker in Jakarta reaching for Masako, or one in Bangkok reaching for RosDee, is not buying "Japanese MSG"—she is buying a trusted local staple, distributed through dense networks of small shops that global giants like Nestlé or Unilever have struggled for decades to penetrate. It is a high-margin, defensive, cash-generative consumer franchise, and it quietly funds everything else the company does. When we later ask how a chemical company can afford to bankroll gene-therapy factories and semiconductor R&D, the answer is bouillon cubes in emerging markets.

The empire did not go uncontested. South Korea's 씨제이제일제당 CJ CheilJedang, and later Daesang, entered the global glutamate market with their own fermentation capacity, igniting decades of commodity price wars in bulk MSG and, later, in feed-grade amino acids like lysine. Commodity fermentation, it turned out, was a business anyone with capital and patience could enter. That competitive pressure would eventually push Ajinomoto to ask an uncomfortable question about which of its businesses actually earned their cost of capital. But first, the company had to survive a public-relations crisis in the West that had nothing to do with science and everything to do with fear.

IV. The Chinese Restaurant Syndrome & Western Backlash

In April 1968, a physician wrote a short letter to the New England Journal of Medicine describing numbness, palpitations, and weakness he experienced after eating at Chinese restaurants, and speculating about possible causes including MSG. The letter coined a phrase—"Chinese Restaurant Syndrome"—that would haunt Ajinomoto for half a century. There was no rigorous evidence, and the framing carried an unmistakable racial charge, tapping into Western unease about Chinese food specifically rather than the countless processed Western foods that also contained glutamate. But the panic spread through American and European consumer culture with a speed that clinical data never matched.

For Ajinomoto the damage was strategic rather than financial in any single quarter. The MSG scare effectively capped the growth ceiling for branded retail seasoning in the United States and Western Europe. "No MSG" became a marketing badge for restaurants and packaged-food brands. A company whose entire origin story was the purity and modernity of a laboratory crystal now found that same crystal recast, in its most lucrative Western markets, as something vaguely sinister. Decades of subsequent toxicology reviews by regulators broadly found MSG safe at normal consumption levels, but the reputational stain proved far stickier than the science.

Here the story reveals something about the company's temperament. Ajinomoto did not bet the future on winning a defensive public-relations war it had little power to control. Instead it executed a quiet dual strategy that would define the next fifty years.

First, it went upstream and industrial. If Western consumers didn't want to buy a red-capped shaker of MSG, they were nonetheless eating enormous quantities of glutamate inside packaged and restaurant food, often labeled as "yeast extract," "hydrolyzed vegetable protein," or "autolyzed yeast." Ajinomoto became a leading silent supplier of amino acids and savory ingredients to the global food industry—a business-to-business franchise invisible on the supermarket shelf but embedded in the supply chains of major food conglomerates. The brand panic in the front of the store did nothing to slow demand at the back of the factory.

Second, and more consequentially, the backlash accelerated a realization that Ajinomoto's real asset was amino acid science itself, not seasoning. Glutamate is one of some twenty amino acids, the building blocks of protein, and Ajinomoto's fermentation platform could in principle make many of them at high purity. The company pushed into clinical nutrition, ingredients for infant formula, pharmaceutical-grade amino acid infusion solutions for hospital patients, and animal nutrition—feed-grade lysine and threonine that improve livestock growth. Taste was becoming just one application of a much broader molecular platform.

That reframing—we are not a seasoning company, we are an amino acid company—is the intellectual bridge to the strangest chapter in the story. Because once you decide your business is the chemistry of amino acids and their derivatives, you start asking what else the molecules coming out of your fermentation tanks might be good for. In the 1970s, a group of Ajinomoto researchers asked exactly that question about the leftover raw materials of MSG production. The answer would take twenty years to arrive, and it would have nothing to do with food.

V. The Serendipity of Science: How MSG Waste Created a Semiconductor Monopoly (1970s–1999)

The origin of Ajinomoto's semiconductor monopoly reads like something a screenwriter would reject as too neat. In the 1970s, Ajinomoto's laboratories were handed a mandate that would sound familiar to any research-driven company: find commercial uses for the co-products and raw materials of umami seasoning production.1 Amino acid chemistry, it turned out, was chemically adjacent to a very different world—organic resins and coatings.

Researchers found that certain formulations combining epoxy resins with amino-acid-derived chemistry had unusual and valuable properties for electronics: excellent electrical insulation, strong heat tolerance, and—critically—exceptional adhesion to copper.1 For a while this was an interesting result in search of a market. Ajinomoto sold resin and coating agents into the electronics industry, but nothing that looked like a monopoly.

To understand why that changed, you need to understand a problem that was quietly strangling the semiconductor industry in the mid-1990s. Chips were getting faster, which meant the packaging around them—the substrate that fans the chip's thousands of connections out to a circuit board—had to carry more and more wiring in less and less space. Substrate makers built these connections in layers, and between each layer of copper wiring sat an insulating layer. Historically, that insulation was a liquid ink, applied by screen-printing and then cured.

Liquid ink was hitting a physical wall. As engineers drilled ever-smaller connection holes between layers—"micro-vias," some smaller than a human hair—liquid insulation could not fill and coat these sub-micron features cleanly. It trapped air bubbles and left uneven thickness, and in a chip package a trapped bubble is a latent bomb: it becomes a hot spot, a crack, a short circuit, a dead chip. The screen-printing approach was slow, attracted impurities, and generated environmentally harmful by-products.1 The industry needed a fundamentally different way to lay down insulation.

Enter the hero of the story. In 1996, a CPU maker approached the Ajinomoto group asking whether its amino-acid-based material chemistry could be turned into a film—a dry, solid insulating layer that could be laminated on like tape rather than printed on like ink.1 The effort was led by an up-and-coming researcher named 中村 茂夫 Shigeo Nakamura, who had a background in insulating materials for electronic circuit boards.1 Leaning on Ajinomoto's deep fine-chemistry expertise, the team produced a first working version of the film in roughly four months.1

The elegance of the solution is worth appreciating in plain terms. Instead of squeegeeing liquid into microscopic holes and hoping for the best, ABF is a thin thermosetting film that is vacuum-laminated over the surface. Under vacuum and heat, it flows just enough to fill every micro-via cleanly and conform to the copper without trapping air, then cures into a hard, stable insulating layer. It behaves like a shrink-wrap that melts precisely into every crevice and then sets like glass. This is what made ever-denser multi-layer wiring possible.

Named Ajinomoto Build-up Film, the material was first adopted by a major semiconductor manufacturer in 1999, with Intel as the launch customer, shipping in the Pentium III era.16 Nakamura reportedly assumed the film might stay in production for perhaps ten years; more than two decades later, ABF is still the standard.1

Why did ABF win so completely? It unlocked the high-density, multi-layer substrates—known as FC-BGA, or flip-chip ball grid array—that let processors scale in speed and pin count.7 Once the world's fastest chips were designed around ABF, the material became the de facto global standard for high-performance microprocessors, and Ajinomoto's share of that market climbed toward complete dominance.1 A seasoning company had accidentally cornered the packaging of the digital age. The tragedy, from a shareholder's perspective, is that for the next fifteen years almost nobody outside the substrate industry noticed—because ABF was buried inside a sprawling, discounted food conglomerate that was busy destroying value elsewhere.

VI. The Conglomerate Trap: M&A Blunders and Capital Inefficiency (2000s–2018)

For most of the 2000s and 2010s, if you asked a Tokyo equity analyst about Ajinomoto, you would hear a sigh. It was a "sleepy food company"—a sprawling, diversified Japanese conglomerate with dozens of businesses, a bloated balance sheet, and returns that flirted with the cost of capital. The extraordinary economics of ABF were real, but they were financially invisible, blended inside a consolidated structure alongside low-margin bulk commodities and struggling overseas divisions. The market applied a "conglomerate discount," and it was largely deserved.

The core problem was a management culture that prized top-line revenue growth over capital efficiency. Two acquisitions from this era became emblematic of the trap.

The first was frozen food. In September 2014, Ajinomoto agreed to acquire the US frozen-food maker Windsor Quality Holdings—the number-one manufacturer of Asian and ethnic frozen foods in America, with brands like Ling Ling and Tai Pei—for approximately $800 million.89 Windsor had fiscal-2013 sales of about $630 million, meaning Ajinomoto paid well over one times sales for a mature frozen-food business, an elevated multiple relative to the sector.9 The strategic logic was to make Ajinomoto the clear number-one in Asian frozen food in North America, riding its gyoza expertise.8 The execution was painful. Integration friction, surging US labor and logistics costs, and a bloated product range dogged the North American business for years. In its FY2022–FY2023 disclosures, the company recognized a goodwill impairment of roughly ¥13.4 billion (on the order of $100 million) tied to the North American frozen-food operations.[^10] A premium acquisition made to buy growth had instead delivered a writedown.

The second was Africa. In November 2016, Ajinomoto took a 33.33% stake in Promasidor Holdings, an Africa-focused packaged-food player, for approximately ¥55.8 billion (around $530 million), buying in from existing investors including Tana and PLEXUS.10 The rationale was to become a leading consumer-food player across African markets by piggybacking on Promasidor's distribution. The reality was brutal macro. Nigerian currency devaluation, foreign-exchange restrictions, and macroeconomic instability savaged the economics, and Ajinomoto was forced to recognize significant impairment losses on the investment's carrying value and trademark rights.10 The pattern rhymed with Windsor: pay a full price for growth in a business Ajinomoto did not deeply understand, then write it down when reality intruded.

Underneath the M&A misfires sat a structural drag: commodity animal nutrition. The feed-grade lysine business, in particular, was a textbook bad-commodity trap—global overcapacity, aggressive pricing from Chinese producers, and no pricing power. It was capital-heavy, cyclical, and frequently earned less than its cost of capital, dragging blended corporate operating margins into the mid-single digits and holding consolidated ROIC below the level that creates value.

The honest investor conclusion from this period is not that Ajinomoto's managers were foolish, but that they were optimizing for the wrong metric. Chasing revenue and scale, they accumulated a portfolio in which a genuine crown-jewel monopoly (ABF) and a defensive emerging-market seasoning cash cow were yoked to value-destroying commodities and poorly underwritten foreign acquisitions. The result was a company worth demonstrably less than the sum of its parts. Fixing that required not a new product but a new religion—and around 2019, Ajinomoto found one in the language of return on invested capital.

VII. The ROIC Revolution & ASV Transformation (2019–2024)

Every corporate turnaround needs a moment when management stops explaining away underperformance and starts measuring it honestly. For Ajinomoto, that moment crystallized under the successive leadership of Takaaki Nishii, CEO from 2015 to 2022, and Taro Fujie, who took over in 2022. Together they pushed a structural reform that amounted to a change of religion: from growth-worship to capital discipline.

The central instrument was return on invested capital. ROIC is a deceptively simple idea—it asks how much operating profit a business generates for every yen of capital tied up in it, and compares that to the cost of that capital, the WACC. If a business earns more than its cost of capital, it creates value; if it earns less, it destroys value no matter how fast its revenue grows. Ajinomoto began driving this framework down to the level of individual business units and, notably, disclosing segment-level ROIC against cost of capital—a level of transparency Japanese conglomerates have historically resisted.[^12] The discipline was blunt: a unit that could not clear its cost of capital faced restructuring or divestment.

The portfolio surgery followed the metric. The company began exiting or shrinking the low-margin, capital-heavy commodity businesses that had dragged returns—downsizing and partially divesting animal nutrition, consolidating bulk MSG capacity, and steering resources toward higher-margin consumer specialty seasonings and the electronic materials and healthcare franchises where returns were genuinely superior.[^12] This is the unglamorous work of a good capital allocator: not buying exciting things, but selling or fixing the things quietly eroding shareholder value.

Wrapped around the financial framework was a narrative one, which Ajinomoto branded ASV—Ajinomoto Group Creating Shared Value. On its face ASV is the familiar corporate language of purpose: redefining the mission from "selling food" to "improving health and wellness through amino acid science," including using amino acids to cut the sodium content of foods without sacrificing taste. A neutral observer should treat purpose-branding skeptically—it is cheap to announce and hard to verify. But ASV was not merely a slogan; it doubled as a portfolio filter, giving management a defensible story for why it was exiting commodities and leaning into health, nutrition, and advanced materials.

The results showed up where it counts. Over the reform years, group ROIC climbed from roughly the mid-single digits toward the low double digits, and consolidated business profit grew steadily; for the fiscal year ended March 2025 (FY2024), the company reported sales of about ¥1,530.5 billion, up 6.3%, and business profit of ¥159.3 billion, up 7.9%.6 Just as importantly, the market began to grasp what had been hiding in plain sight: that inside this "food company" sat a near-monopoly on a material the AI boom could not live without. Domestic and foreign institutional investors re-rated the shares, and the conglomerate discount began, at last, to narrow.

Two cautions belong in the ledger, though. First, a re-rating driven partly by a thematic AI narrative is only as durable as the underlying monetization—and, as we will see, Ajinomoto has been strikingly reluctant to actually raise ABF prices. Second, the ROIC gospel had not yet touched every corner of the portfolio; frozen foods, in particular, remained a laggard. The reform architect, Fujie, was widely credited with the discipline behind the re-rating. Which made what happened next both a personal tragedy and a strategic inflection.

VIII. The Ultimate Pivot: The 2025 CEO Succession & Forge Biologics

Before the leadership drama, there was one more large, contentious bet—this time in biology. In November 2023, Ajinomoto agreed to acquire Forge Biologics, a US gene-therapy contract development and manufacturing organization based in Columbus, Ohio, for $620 million in an all-cash deal.[^13] Forge, founded only in 2020, ran a 200,000-square-foot cGMP facility with over 300 employees and specialized in manufacturing adeno-associated virus (AAV) vectors and plasmid DNA—the delicate biological payloads at the heart of modern genetic medicines.[^13]

The strategic logic was a direct extension of the amino acid platform. Ajinomoto already sold high-purity ingredients and cell-culture media into biopharmaceutical manufacturing; Forge added the capability to manufacture the therapies themselves, positioning the group across the high-margin genetic-medicine value chain. Management framed it as a "buy-versus-build" leap into a business that would otherwise take a decade to construct organically.

A skeptical investor should sit with the price. $620 million for a three-year-old, essentially pre-profit CDMO in a gene-therapy sector that, by 2023–2024, was contending with a severe biotech funding winter and chronic overcapacity in viral-vector manufacturing, was a rich, optionality-driven premium. It fit an uncomfortable pattern with Windsor and Promasidor: Ajinomoto paying up for growth in a business adjacent to, but not identical with, its core competence. The bull framing is that this time the adjacency is real chemistry and real manufacturing rigor, not just a consumer brand in a hard geography. The bear framing is that the company's track record of paying premiums for growth outside seasoning is, so far, a track record of impairments. This one is unproven, and it deserves to be watched, not assumed.

Then came December 2024. Taro Fujie—the architect of the capital-efficiency turnaround, at the peak of his credibility with investors—suffered a health crisis. In early February 2025 the board announced that Fujie would step down as President and CEO and move to Chairman, and that Shigeo Nakamura would become Representative Executive Officer, President and CEO, effective February 3, 2025.3 The stated reason was candid: Fujie needed time to recover, and the board wanted to avoid a management vacuum.3

The symbolism was enormous. Nakamura is the first President and CEO in Ajinomoto's history with a scientific background, a researcher whose career at the company spanned more than three decades—and the very person who had led the invention of ABF.3 For a firm that had been run by food and general-management executives since 1909, elevating the electronic-materials chemist to the top job was a statement about what Ajinomoto now believed itself to be. When the succession is a food conglomerate handing the keys to the scientist who built its semiconductor monopoly, the message to the market is unmistakable: technology and materials are no longer a hidden segment; they are the future of the company.

There is a governance nuance worth flagging. Handing the CEO role to the inventor of the crown-jewel product is inspiring narratively but complicated commercially. Nakamura spent his career building trust with substrate customers, not extracting price from them—a tension that would become the central drama of the Palliser campaign. And in his first months, Nakamura publicly reaffirmed the group's 2030 sustainability targets, signaling continuity rather than rupture on strategy despite the abrupt handover.11 Continuity is reassuring; it is also, from an activist's chair, exactly the problem. To understand why, we have to look at the numbers underneath the story.

IX. The Core Engine: Segment Economics & Hamilton Helmer's 7 Powers

Strip away the narrative and Ajinomoto is, financially, three businesses stacked on top of a fermentation platform. In FY2024 (the year ended March 2025), the group reported roughly ¥1,530.5 billion in sales and ¥159.3 billion in business profit—a consolidated margin of about 10.4%.6 The composition beneath that number is where the whole investment case lives.

The largest engine is Seasonings and Foods, which generated sales of about ¥896.0 billion and business profit of roughly ¥113.9 billion in FY2024—a segment margin near 13%.67 This is the emerging-market bouillon-and-umami cash cow: stable, high-return, defensively moated by local brands and distribution, and utterly unglamorous. It is the ballast that funds everything else.

Frozen Foods is the problem child. On sales of about ¥289.3 billion it produced only around ¥8.0 billion of business profit—a margin under 3%.6 This is the segment that houses the North American gyoza and Windsor legacy, and its thin returns are exactly what an activist would target. A business earning low-single-digit margins is almost certainly not clearing its cost of capital.

The most important segment is the one with the blandest name: Healthcare and Others. On sales of about ¥328.3 billion it earned roughly ¥31.0 billion of business profit in FY2024.6 Crucially, this segment is where ABF lives—bundled together with the bio-pharma CDMO business (including Forge), specialty amino acids, and other electronic and healthcare materials. A blended segment margin near 9–10% actually understates ABF's economics, because the electronics monopoly is being averaged down by lower-margin and still-investing bio-pharma operations.7 That averaging is the crux of the activist thesis we will reach shortly: the market cannot see, and therefore cannot fairly value, a ~monopoly material because it is hidden inside a grab-bag segment.

Management's own guidance points to Healthcare and Others as the growth and margin driver going forward, with the group guiding to continued profit expansion into FY2025.12 But an investor should hold guidance lightly and instead ask the harder question: how durable is the moat under ABF? Here Hamilton Helmer's 7 Powers framework is genuinely clarifying.

Cornered Resource. ABF's specific epoxy-plus-amino-acid molecular formulation, and the process to manufacture it at the required purity and uniformity, are closely guarded trade secrets protected by decades of patents and, more durably, by accumulated institutional know-how.1 Rivals know roughly what ABF is; reproducing how to make it reliably at scale is another matter entirely.

Switching Costs. This is the deepest source of the moat. FC-BGA substrates require years of qualification. Once a substrate maker—Ibiden, Unimicron, 新光電気工業 Shinko Electric—and its end customers (Intel, Nvidia, AMD, TSMC) have designed and qualified a chip package around ABF, switching to an alternative film risks catastrophic, potentially billion-dollar physical failures across production chips.7 Nobody re-qualifies the insulation in a flagship GPU to save a rounding-error on material cost. This is why ABF's near-total share has proven so sticky.

Process Power. More than a century of large-scale fermentation and fine-chemistry mastery lets Ajinomoto produce high-purity, pharmaceutical-grade amino acids and specialty materials at a cost and consistency competitors struggle to match—a capability compounded over decades and not easily bought.

Scale Economies. Global production across Europe, the Americas, and Asia spreads fixed R&D and capital costs over large volumes in both the consumer and materials franchises.

The honest caveat: switching costs and cornered-resource advantages are strongest at the current technology node. They must be re-earned at every generation of packaging, and they do not protect against a discontinuous shift to a fundamentally different substrate—say, glass. A moat this deep is precisely what attracts a smart activist to ask why the company isn't charging for it. In March 2026, one did.

X. The Activist Stress Test: Palliser Capital's March 2026 Campaign

On March 31, 2026, the London-based activist hedge fund Palliser Capital went public with a detailed "Value Enhancement Plan" for Ajinomoto, framing the company as the most under-monetized AI-infrastructure monopoly in the world.4 Palliser had built its position over the prior six months and had become one of Ajinomoto's top-25 shareholders.12 The pitch was surgical, and it forced into the open a question long-term holders had only whispered.

The setup was a valuation grievance. Despite sitting on a material with more than 90% global share in PC and server chip insulation, Ajinomoto's shares had gained only around 3% over the prior six months—badly lagging the roughly 12% rise in the Topix, and humiliatingly behind chip-material peers like Ibiden and 레조낙 Resonac, which had rallied more than 60% on the AI theme.12 Palliser's implicit charge: Ajinomoto owned the best asset in the space and was capturing the least value from it.

The demands followed logically. First, pricing. Palliser argued that ABF represents less than 0.1% of the total manufacturing cost of an AI GPU, yet is a single point of failure—the definition of a product with near-zero customer price sensitivity. On that logic, the fund demanded a price hike of more than 30% on ABF, reasoning that because customers cannot practically switch, most of the increase would flow straight to Ajinomoto's bottom line.412

Second, structure. Palliser demanded that Ajinomoto break the electronic-materials business out of the "Healthcare and Others" grab-bag and report it as a standalone, pure-play AI-infrastructure segment, arguing the market would then value it on the 30-times-plus EBITDA multiples that comparable semiconductor-materials monopolies command, rather than burying it in a food-company multiple.412 Third, the fund pushed for aggressive restructuring of the underperforming Frozen Foods business toward a real return threshold.4

The intellectual force of the campaign is hard to deny. It is the cleanest possible statement of the bull case, made by an outsider with no incentive to flatter management: you own a monopoly, you are giving away its economics, and you are hiding it inside a structure that guarantees the market misprices it. Every point maps to a concrete, testable lever.

And yet the tension with CEO Nakamura's worldview is profound, which is what makes this a genuine stress test rather than a slam dunk. Nakamura spent thirty years building the substrate relationships that underpin the monopoly. In the Japanese semiconductor ecosystem, supply security, long-term joint R&D, and trust are prized over short-term price extraction, and a blunt 30% hike risks two dangerous responses. It could sour relationships with the very substrate makers who are Ajinomoto's customers—and it could hand competitors like 積水化学工業 Sekisui Chemical or Resonac the margin umbrella and the motivation to fund a credible alternative film, or accelerate the industry's shift toward glass substrates.13 A monopolist's worst move is to price so aggressively that it finances its own replacement.

Nakamura's apparent counter-strategy is subtler than Palliser's: rather than arbitrary hikes on legacy film, charge genuine premium pricing for the next-generation, ultra-thin films required for advanced chiplets and high-performance packaging—capturing value on new technology the customer actively wants, where Ajinomoto's edge is sharpest and the price is easiest to justify. Whether that is disciplined long-term stewardship or a convenient excuse for a scientist-CEO who is temperamentally uncomfortable squeezing his life's-work customers is, right now, the single most interesting open question about the company. The campaign is unresolved as of mid-2026, and it has done something valuable regardless of outcome: it has forced the monopoly into the daylight.

XI. Current Risk Radar & Strategic Playbook

Every monopoly narrative should be pressure-tested against the ways it could break, and Ajinomoto's has several genuine fault lines beneath the AI euphoria.

The first is cyclicality. AI demand may be secular, but ABF also rides the broader semiconductor market—PCs, standard servers, smartphones—which is violently cyclical. A conventional chip downturn would hit ABF volumes even as the AI narrative holds, and a stock that has partly re-rated on the AI theme could de-rate sharply on a cyclical air pocket. Monopoly on a cyclical product is still cyclical.

The second, and most existential, is materials disruption. The switching-cost moat protects the current architecture, not the concept of organic build-up film forever. Competitors including Sekisui Chemical have been developing rival dry insulation films, and more fundamentally, the industry's push toward glass-core substrates—championed by Intel and others—could, over time, alter or reduce the need for traditional organic films in the most advanced packages.13 Glass is years from displacing ABF at scale, and organic build-up film will coexist with it for a long time, but a prudent investor treats substrate architecture as a live technology risk rather than a settled one. This is the classic vulnerability of a cornered resource: it is worthless if the resource is designed out.

The third is input-cost and operational volatility. Ajinomoto's fermentation base depends on agricultural feedstocks—molasses, starch, sugar cane—whose prices swing with weather, harvests, and climate risk, alongside volatile energy costs. These pressures are more acute in the low-margin food and frozen segments, where there is little room to absorb a cost spike.

The fourth is execution risk in biopharma. The Forge Biologics bet places a substantial premium in a capital-intensive gene-therapy CDMO sector that is acutely sensitive to biotech funding cycles. Integration missteps or a prolonged funding winter could turn this into the next impairment in a company that has already booked several. Until Forge demonstrates real utilization and profitability, it is optionality, not earnings.

Against those risks, the playbook lessons that make Ajinomoto instructive are three. First, the power of serendipity harnessed by real research: exploring the chemical by-products of an MSG factory produced a dominant position in the digital revolution—a reminder that basic research inside an industrial company can yield asymmetric payoffs that no strategy deck would have predicted. Second, the ROIC cure for conglomerates: imposing capital-efficiency KPIs down to the business-unit level was the mechanism that forced accountability and began dissolving a decades-old discount. Third, and most subtle, monopoly humility: managing a ~100% share requires prioritizing long-term customer alignment over short-term price optimization, precisely to avoid inviting the disruption that ends monopolies. The Palliser campaign is, at bottom, a debate about whether Ajinomoto has been too humble. Which brings us to the scorecard.

XII. Epilogue & Bull vs. Bear Case

Step back and Ajinomoto is one of the most improbable businesses in global markets: a Japanese seasoning house that spent a century mastering the manufacture of purified molecules, stumbled into the insulating film that makes advanced chips possible, buried it inside a discounted conglomerate, found capital-allocation religion, and then handed the top job to the chemist who invented the monopoly—just as an activist arrived to demand it finally charge for that monopoly.

The bull case is clean. At the center sits an under-monetized, ~98%-share material with brutal switching costs, sitting at a single point of failure for the AI hardware build-out—an asset with obvious, un-pulled pricing levers.14 A technologist CEO who built the technology now runs the whole group, aligning strategy with the crown jewel. And a deeply defensive emerging-market seasoning franchise throws off the cash to fund advanced materials and bio-pharma R&D without stressing the balance sheet. Layer on a credible capital-allocation reform that has already narrowed the conglomerate discount and disclosed segment ROIC, and you have a rare combination: a monopoly with a self-funding consumer annuity attached.

The bear case is equally coherent. ABF volumes ride a cyclical semiconductor industry and face a real, if slow-moving, technology threat from glass substrates and rival films.13 The company has a demonstrated habit of overpaying for growth outside seasoning—Windsor, Promasidor, and now the unproven Forge premium—turning several such bets into impairments.9[^10]10[^13] Frozen Foods still earns returns that likely destroy value. And the very trait that makes Nakamura an inspiring CEO—three decades of customer trust-building—may make him structurally reluctant to extract the pricing an activist correctly identifies as available, meaning the monopoly could stay under-monetized precisely because the monopolist is too polite to press it.

Run it through Porter's Five Forces and the tension sharpens. Supplier power and buyer power in ABF both favor Ajinomoto today—buyers are locked in by qualification, suppliers of feedstock are commoditized. The threat of new entrants is low at the current node thanks to the cornered resource and process power. The two forces that matter are substitutes (glass, rival dry films) and, unusually, the behavior of the incumbent itself: a monopolist that under-prices avoids inviting substitutes but leaves enormous value uncollected, while one that over-prices harvests today at the risk of financing tomorrow's competitor. Helmer's 7 Powers explains why the moat is deep; Porter explains why the pricing decision is genuinely hard rather than obvious.

The three KPIs worth tracking distill the whole debate. First, the Healthcare and Others segment profit margin—the single best read on whether ABF's economics are improving and, if Palliser prevails, whether the electronics business gets broken out into visible, pure-play numbers. Second, ABF production capacity expansion—capex and utilization at the Gunma and Kawasaki facilities, the truest signal of how Ajinomoto reads secular AI demand with its own money rather than its slide decks. Third, Frozen Foods segment ROIC—the cleanest test of whether the capital-discipline gospel has finally reached the portfolio's weakest link.

The alchemy that turned kelp broth into a semiconductor monopoly is real, and rare, and largely settled history. The open question—the one that will define the next chapter—is whether a company built on the patient chemistry of trust can learn to price like the monopoly it has quietly become, without breaking the very relationships that made the monopoly possible.

XIII. Outro & Links

Ajinomoto's arc runs from a professor's bowl of soup in 1908 to the substrate beneath the world's most advanced AI processors—a 118-year chain of amino acid chemistry, fermentation mastery, serendipitous research, and hard-won capital discipline, now stress-tested by an activist and led, for the first time, by the scientist who built its most valuable asset. For readers who want to follow the story from the primary sources, the leads below are the places to watch as the pricing debate, the Forge integration, and the segment-disclosure question play out.

References

-

Ajinomoto Build-up Film (ABF) — Innovation Story — Ajinomoto Co., Inc. ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Palliser Takes Stake in Ajinomoto, Urges 30%+ ABF Price Increase — Yahoo Finance / Bloomberg, 2026-03-31 ↩

-

Ajinomoto Co., Inc. Announces Executive Personnel Changes of President and Executive Officers — Ajinomoto Co., Inc., 2025-02-03 ↩↩↩↩

-

Palliser Capital Publishes Value Enhancement Plan for Ajinomoto — Business Wire, 2026-03-31 ↩↩↩↩↩↩

-

Who Identified Umami and When? — The Ajinomoto Group Global Website ↩↩

-

Consolidated Financial Results for the Fiscal Year Ended March 31, 2025 — Ajinomoto Co., Inc., 2025-05-08 ↩↩↩↩↩↩

-

Understanding FC-BGA Packaging and the Critical Role of ABF — TSMC Technical Disclosures, 2024-06-15 ↩↩↩↩

-

Ajinomoto Group to Acquire Windsor Quality Holdings, LP, for Approximately USD 800 Million — Ajinomoto Co., Inc., 2014-09-10 ↩↩

-

Ajinomoto to buy Windsor Quality for $800M — Grocery Dive, 2014-09-10 ↩↩↩

-

Ajinomoto Co. to Acquire a 33.33% Stake in Promasidor Holdings Limited for Approximately JPY 55.8 Bn — Ajinomoto Co., Inc., 2016-11-08 ↩↩↩

-

Ajinomoto reaffirms 2030 sustainability goals despite CEO shift — FoodNavigator-Asia, 2025-10-06 ↩

-

Activist fund Palliser presses Ajinomoto to raise prices for chip material — The Japan Times, 2026-04-02 ↩↩↩↩↩

-

Sekisui Chemical Advanced Materials R&D & Competitor Film Progress — Sekisui Chemical IR Portal ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube